veteran cpas who show no signs of slowing down...

TRANSCRIPT

ISSUE 11 VOLUME 8 NOVEMBER 2012

PLUS• Theevolutionofconsulting•Appointinganauditcommittee• JennyToofPernodRicardAsia

HK$70.00

Veteran CPAs whoshow no signs of slowing down

SECONDWIND

Connecting withyounger members

COLIN BEERE

Dear members,

A t the last Council meeting, we de-voted a section to meet the rep-resentative of the 25.35 Group because we wanted to understand

more about the needs and expectations of our younger members and to get their views on the work of the Institute. This age group is an impor-tant segment of the profession as more than 11,000 members are now under the age of 36. They make up 32 percent of our membership.

Through the 25.35 young members leadership panel, we aim to engage with younger members, hear their views and ideas, foster a close network among them and between them and the Institute, and support their social and career development.

Another important group of our membership consists of small- and medium-sized practitio-ners. We are organizing an SMP symposium at the end of this month to update them about the Institute’s support for SMPs, the practice review programme, tax issues and important account-ing and auditing standards that affect them. We will also discuss the latest Companies Ordinance reform and have invited the accountancy sec-tor’s LegCo representative to speak.

Turning to our students, we just held an an-nual award and graduation dinner, at which we conferred certificates to QP graduates as well as prizes and scholarships to top students. This celebratory event was for the December 2011 and June 2012 sessions of the programme, which 1,490 students successfully completed. The total number of QP graduates now stands at 10,790.

I extend a warm welcome and congratulations to these new graduates. They are one step closer to gaining their CPA designations and are well on

their way to becoming one of Hong Kong’s suc-cess ingredients.

Another landmark event is our Best Corporate Governance Disclosure Awards, which are now in their 13th year and have become prestigious recognition coveted by Hong Kong businesses in all sectors. The review and judging panels have spent months evaluating the quality of disclo-sure of contesting companies through their an-nual reports.

Winners will be announced on 23 November at the awards presentation ceremony, at which Sir C.K. Chow, chairman of the Hong Kong stock exchange, will be the guest of honour.

Later this month, you will receive information about the Institute’s annual general meeting and a review of our work and finances in the past year. I encourage you to read through it to learn more about what the Institute has done for you. We al-ways welcome your views and participation.

One way you can do your part is by either standing for the Council election or nominating a member who you think can represent you. At our AGM next month, some Council members are re-tiring in line with rules set out in the Professional Accountants Ordinance, and this is an opportu-nity for new ones to join.

Last but not least, with the year drawing to an end, it is time for us to gather, relax and revel. Our annual dinner, taking place on 3 December at the Hong Kong Convention and Exhibition Cen-tre, has adopted the theme “Guys and Dolls” (紅男綠女), borrowing the name of the classic Broad-way musical.

Let’s put on something red (for men) or green (for women) and celebrate with fellow members and friends.

Keith PogsonPresident

“ This age group is an important segment of the profession as more than 11,000 members are now under the age of 36.”

President’s message

November 2012 1

2 November 2012

56 Business travel Honnus Cheung marvels over Madrid

58 After hours Aloysius Tse on wine; Jemelyn Yadao on watches

60 Let’s get fiscal Nury Vittachi gets into bed with an accountant and a lawyer

LIFESTYLE

01 President’s message04 Institute news06 International news10 Greater China news

42 China finance Liu Yuting analyses a new financial model for development

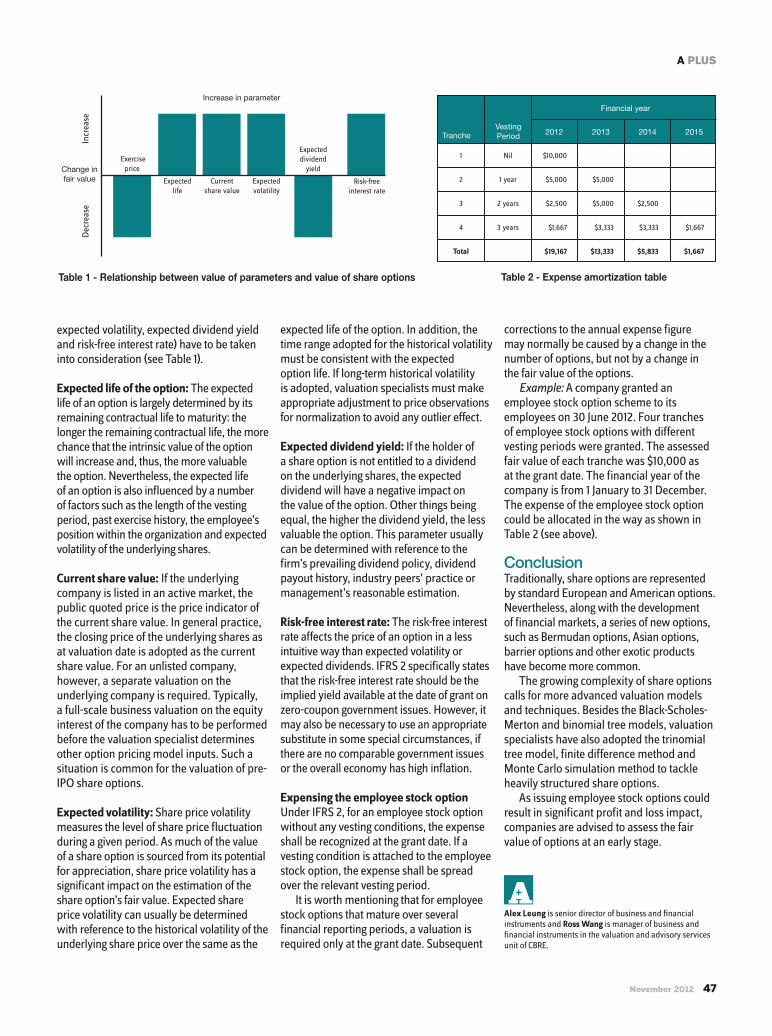

46 Share-based payment Alex Leung and Ross Wang look at options for IFRS 2 Share-

based Payment and how to use them for business purposes

48 TechWatch 120 The latest standards and technical developments

51 Tech Q&A Your questions about standards answered

54 Events A guide to forthcoming courses, workshops and member activities

55 People on the move The latest professional appointments from around the region

14 Giving good advice Alfred Romann asks how consulting firms are coping with the

pressure of China's competitive market

20 Working overtime Many CPAs are hard at work even after retirement. Jemelyn

Yadao meets some of the Institute's pioneering retired members

28 Panels of probity Audit committees are expected to be more active. George W.

Russell asks the experts about how the boards can be improved

34 Staying indie George W. Russell puts independent non-executive directors in

the spotlight and looks at the skills that they are expected to have

38 Success ingredient Jenny To, regional recruitment and talent development director at

Pernod Ricard Asia, tells George W. Russell about her versatility

14 REGULARS

FEATURES

SOURCE

ISSUE 11 VOLUME 8 NOVEMBER 2012

CONTENTS

President: Keith PogsonEmail: [email protected]

Vice Presidents: Susanna Chiu, Clement Chan

Chief Executive and Registrar: Raphael DingEmail: [email protected]

Deputy Director of Communications: Stella To

Editorial Advisers: Daniel Lin, Clement Chan, K.M. Wong

Editorial Manager: John So

Editorial Coordinator: Maggie Tam

OFFICE ADDRESS:37/F, Wu Chung House, 213 Queen’s Road East, Wanchai, Hong KongTel: +852-2287-7228 Fax: +852-2865-6603

MEMBER AND STUDENT SERVICES COUNTER:27/F, Wu Chung House, 213 Queen’s Road East, Wanchai, Hong Kong

WEBSITE: www.hkicpa.org.hkEMAIL: [email protected]

M&L

Editor: George W. Russell

Managing Editor: Gerry HoEmail: [email protected]

Copy Editors: Jemelyn Yadao, Alisha Haridasani

Production Manager: Jasmine Hu

Design Manager: Jennifer Chung

Contributor: Alfred Romann

Editorial Assistant: Lucid Wong

EDITORIAL OFFICE:2/F, Wang Kee Building, 252 Hennessy Road, Wanchai, Hong Kong

ADVERTISING ENQUIRIES:Advertising Director: Derek TsangEmail: [email protected]: +852-2656-2676

A PLUS is the official magazine of the Hong Kong Institute of Certified Public Accountants. The Institute retains copyright in all material published in the magazine. No part of this magazine may be reproduced without the permission of the Institute. The views expressed in the magazine are not necessarily shared by the Institute or the publisher. The Institute, the publisher and authors accept no responsibilities for loss resulting from any person acting, or refraining from acting, because of views expressed or advertisements appearing in the magazine.

© Hong Kong Institute of Certified Public Accountants November 2012. Print run: 33,900 copiesSubscription: HK$760 for 12 issues per year.See www.hkicpa.org.hk/aplus for details.

Your chop Your Logo

IL

LUS

TRAT

ION

: HA

RR

Y H

AR

RIS

ON

About our name: A PLUS stands for excellence, a reference to our top-notch accountant members who are success ingredients in business and in society. It is also the quality that we strive for in this magazine — going an extra mile to reach beyond grade A.

4 November 2012

NEWSTHE INSTITUTE

Disciplinary findingLeung Chi-keung, CPA and Luk Ka-cheung, CPAComplaint: Noncompliance with the Funda-mental Principles of Statement 1.200 “Pro-fessional Ethics – Explanatory Foreword.” In July 2009, Leung and Luk were found by the Market Misconduct Tribunal to be culpable of insider dealing, which is contrary to section 270(1)(e)(i) of the Securities and Futures Ordi-nance (Cap 571). Leung and Luk held non-pub-lic and price sensitive information about the securities of China Overseas Land and Invest-ment Limited, a Hong Kong-listed company. The two accountants admitted the complaint.

Decision and reasons: Leung’s and Luk’s names shall be removed from the register for a period of one year. Each must also pay the Institute a penalty of HK$100,000 and pay costs towards the disciplinary proceedings amounting to HK$34,159 and HK$21,145 for Leung and Luk respectively. The Disciplinary Committee considered this case as a serious one, involving public interest and an element of breach of trust by both accountants.

Chan Kin-hang, Danvil, CPAComplaint: Noncompliance with the Funda-mental Principles of Statement 1.200 "Profes-sional Ethics – Explanatory Foreword" and paragraph 100.4(a) of the Code of Ethics for Professional Accountants; and guilty of pro-fessional misconduct. Chan was director of a company which submitted a tender to the Of-ficial Receiver for appointment as provisional liquidators. After the tender was accepted, the Official Receiver appointed Chan and a non-member as joint and several provisional liqui-dators for a number of companies. In October and December 2009, Chan and the non-mem-ber were removed as the joint and several liquidators/provisional liquidators for seven companies on the grounds that they did not carry out their duties appropriately and that Chan had included misleading information in the tender. Chan admitted the complaints.

The Disciplinary Committee found that Chan breached the above standards of ethics in submitting a declaration form used in the ten-der, which contained incorrect and misleading information. This misled the Official Receiver

Conference discusses CPAs role in Hong Kong’s future

The Institute responded to newspaper reports that questioned the effectiveness of its disciplinary system. On 28 September, several local newspapers reported that since the Financial Reporting Council was set up six years ago, it has completed 14 investigations, but only one disciplinary order has been made by the Institute.

The Institute clarified that by end of September it had received 16 cases re-ferred by the FRC, all of which had been introduced to its complaint assessment process. Of the 16 referred cases, eight had been concluded after completion of due process. Not all cases were sent for consideration by a Disciplinary Commit-tee because the Institute judged that they were more appropriately concluded by other sanctions available. The Institute added that the results of all con-cluded cases were communicated to the FRC, which has the option of pursuing its own prosecution if it was dissatisfied with case outcomes.

Of the eight cases in progress, six were referred to the Institute this year. One of the two pre-2012 cases still in progress was being dealt with by an inde-pendent Disciplinary Committee specifically set up for the case in accordance to the Professional Accountants Ordinance, and the other was being considered by Institute’s Council for referral to a Disciplinary Committee. The Institute advises the FRC of the progress of all referred cases on a quarterly basis.

Institute responds to media on disciplinary concerns

The Institute held a conference last month to discuss business sustainability and the future of the accounting profession. Keynote speakers included Chris-tine Loh, under-secretary for the environment, Paul Druckman, chief executive officer of the International Integrated Reporting Council, and Julia Leung, under-secretary for financial services and the treasury.

The one-day event was divided into two parts. During the morning session, Loh covered why sustainability is important for businesses and Druckman discussed how to communicate and report on it. In the afternoon, Leung talked about Hong Kong’s role as an international financial centre.

In his closing remarks, Clement Chan, vice president of the Institute, noted that the topics discussed were intertwined and impact the future of Hong Kong.

into accepting the tender. He was also found guilty of professional misconduct as a joint and several liquidator/provisional liquidator of three of the seven companies.

Decision and reasons: Chan’s name shall be removed from the register for a period of three years. He must also pay the Institute a penalty of HK$33,333.33 and costs of HK$288,511. The Disciplinary Committee took Chan’s personal circumstances and conduct during the proceedings into consideration when making its decision.

(Details of disciplinary findings are available on the Institute’s website: www.hkicpa.org.hk)

Disciplinary finding (continued)

6 November 2012

NEWSINTERNATIONAL

Bank of England policymakers are divided over the future of economy-boosting measures, in particular the quantitative easing programme. The bank’s monetary policy committee agreed to continue purchasing assets totalling £345 billion and keep interest rates at their current record low of 0.5 percent until next month.

However, according to min-utes of the committee’s meeting, the asset purchases will be com-pleted by next month and it is

uncertain if the bank will expand the measure: “There were some differences of view between members about the outlook and the likelihood that further easing in policy would be required.”

Inflation had fallen to 2.5 percent in August although it was still above the central bank’s 2 percent target and is expected to “remain broadly flat over the rest of the year,” according to the minutes. Furthermore, “slowing activity in the rest of the world had been a drag on United King-

dom exports and had hampered the rebalancing process.”

Figures from the Office for National Statistics show a fall in unemployment. The office stated that unemployment for June to August fell 0.2 percentage points to 7.9 percent year-on-year.

However, the bank’s commit-tee said any optimism would be premature. “It was particularly difficult to explain the recent strength of job creation,” it said, adding “it is unclear how long that strength would last.”

Food prices rising to 2008 crisis levels

The Food and Agriculture Organization’s monthly price index has indicated an increase in world food prices, bringing them closer to the levels reached as the global financial crisis unfolded in 2008.

After two months of stabil-ity, the Food Price Index, which measures monthly changes for a food basket of cereals, oilseeds, dairy, meat and sugar, rose by 1.4 percent in September, climbing to 216 points – just nine points short of the peak of 225 points reached in 2008 that some analysts blamed for igniting riots across the world.

The Cereals Price Index hit 263, which is 7 percent higher than the corresponding period last year and just 4 percent lower than 2008 levels when the index hit 274 points.

The price increases are attrib-uted to droughts in key cereal pro-ducing areas, such as the United States and Central Asia.

“Food prices and volatility have increased in recent years. This is expected to continue in the medium term,” said José Grazia-no da Silva, director general of the organization, a United Nations agency, calling for stronger global governance of food security.

Advances have already been made in improving food security, Graziano said, such as the estab-lishment of the High Level Task Force on Global Food Security and the Agricultural Market Information System.

Global economy unlikely to recover until 2018, says IMF chief economistNew report lowers expectations of growth next year

Bank of England uncertain about future measures

Olivier Blanchard AFP

The chief economist of the International Monetary Fund, Olivier Blanchard, says the global economy, dogged by the euro zone crisis, debt problems in Japan and the United States and a slowdown in China, will not recover from the financial crisis until at least 2018.

“It will surely take at least a decade from the beginning of the crisis for the world economy to get back to decent shape,” he was quoted as saying by Agence France-Presse.

Blanchard’s statement coin-cides with the release of an IMF report, World Economic Out-look: Coping with High Debt and Sluggish Growth, which revises forecasts presented by the fund in April this year to accommodate slower rates of growth around the world. Revised projections for 2013 see growth predictions

reduced from 2 percent to 1.5 per-cent for advanced economies and from 6 percent to 5.6 percent for emerging-market and developing economies.

According to the fund, these forecasts rely on two assumptions: that the euro zone will “adopt poli-cies that gradually ease financial conditions further in periphery economies” and that the U.S. will avoid “drastic automatic tax increases and spending cutbacks”

as well as raise the debt ceiling in a “timely manner.”

In addition, Italy and Spain need “not only a continuous process of internal adjustments but also a guarantee of financing on condition that these

countries really implement their plans,” Blanchard told AFP.

Weak growth in Asia is in large part due to reduced activity in China and India, the report states. In China tighter credit conditions to avert a real estate bubble and weaker external demand explain the slowdown, while in India low business confidence, weak structural reforms and flagging external demand have deceler-ated the economy.

November 2012 7

European Union policymakers have agreed to create a supervi-sory board run by the European Central Bank to watch over the banking sector across the euro zone.

The legal framework for the board is likely to be completed by 1 January 2013. The board is expected to become operational over the course of 2013, after which it will oversee 6,000 banks.

Under direction from the board, the EU’s rescue fund – the European Stability Mechanism – can directly funnel financial as-sistance to failing banks without adding to government debt.

“The quicker the mechanism is in place, the sooner recapital-ization can take place,” French President François Hollande said at a press conference after the decision on the initiative was reached on 19 October by euro zone leaders meeting in Brussels.

However, German Chancel-lor Angela Merkel cautioned that it would take time for the new supervisory board to run effectively. “It’s not just a matter of months,” she said.

It is also apparently unde-cided whether Spanish banks can request recapitalization funds from this new mechanism, since Spain was already committed to a rescue package agreed to at a summit in June. A final decision on whether Spain’s banks will be included in the mechanism is expected to be made before the end of 2012.

EU chiefs OK new banking supervisor

Google worries investors with third-quarter report

Google released a disappointing third quarter earnings report that led to a nosedive in the company’s stock price, reflecting the chal-lenges ahead for the Internet giant in an increasingly mobile world.

The report, which was accidentally released before Google approved it, revealed that revenue increased by 45 percent to US$14.10 billion. However, Google’s revenue per click on ads fell by 15 percent, the fourth consecutive quarter that figure has declined.

The fall is attributable to the increased use of smart phones and other mobile gadgets where ads cost less because they don’t translate into purchases as much as ads on desktops.

Larry Page, Google’s chief executive, assured investors and analysts on a conference call that Google can tackle the mobile ads issue. “Monetization on mobile queries right now is a significant fraction of desktop,” he said.

Page added that Google was exploring ways of making more

money from mobile ads and that the firm was “uniquely positioned to get through that transition and to profit from it.”

Additionally, operating costs of Motorola Mobility, the cell-phone maker that Google recently acquired, are increasing.

The report pushed stock prices down by 9 percent, before NASDAQ halted trading in the company.

The report also comes at a time when Google is undergoing pri-vacy and antitrust investigations.

Citigroup CEO resigns abruptlyamid reports of board tensionsBank taps head of European operations as replacement

AFP

The chief executive of Citigroup, Vikram Pandit, resigned abruptly last month amid reports of tensions with Michael O’Neill, the bank’s chairman, and other members of its board.

The bank’s board of directors immediately named Michael Corbat, its head of operations in Europe, the Middle East and Africa, as its new CEO.

Pandit told Reuters that the decision to resign was entirely his own, adding that he had been “thinking about [it] for a while.” According to the news service, sources within and outside Citi stated that Pandit’s decision to step down followed months of tension with O’Neill over a range of issues. Moreover, O’Neill told investors after Pandit’s resigna-tion that he had been planning to replace Pandit with Corbat for

“quite some time.” The bank’s president and

chief operating officer, John Havens, also resigned on the same day. The departures came just a day after Citi announced a third-quarter operating profit of US$3.27 billion, exceeding Wall Street expectations.

In April this year, Pandit clashed with the board over his US$15 million pay package that 55 percent of shareholders had re-jected during an advisory vote. In

March, the Federal Reserve Board, the United State’s central bank, rejected a Citi proposal to return capital to shareholders because Citi was not deemed in a fit enough position – a result that further strained relations between the bank’s management and its

investors. Throughout his tenure, Pandit was adamantly opposed to breaking up Citi despite critics saying the group had become too unwieldy to manage.

Pandit was appointed to the top job in 2007 when the bank was on the brink of collapse and had to turn to the federal govern-ment for a US$45 billion bailout. At the time, Citi was in such a dire position that Pandit had to take a US$1 token annual salary until the bank returned to profitability.

Vikram PanditAFP

8 November 2012

Audit work that accounting firms in the United States outsource to centres in India is not routinely inspected by American regulators, according to Indian accounting officials and employees of large audit firms.

Almost 5 percent of U.S. audit work is now carried out in India, an American ac-counting professor told Reuters. That figure is up from 1 to 2 percent five years ago.

Douglas Carmichael, former chief auditor of the Public Company Account-ing Oversight Board , told Reuters that “the risks are that the work will be offshored that is beyond the training, skills and experience of the people that it is offshored to.”

The lower wages in India – where a junior accountant can earn less than a fifth of the salary of a United States counterpart – have prompted the U.S. arms of the Big Four to open centres across India. In total, Deloitte, Ernst & Young, KPMG and PricewaterhouseCoopers now employ 22,000 workers there. Three of the firms replied to Reuters’ requests for comment, stating that work done in India is routine and reviewed to meet the same standards as work done in the U.S.

An executive from PwC, which has transferred 4 percent of its audit work to “alternate delivery centers” outside the U. S., said the work done offshore is “limited to standardized tasks, none of which involves auditor judgment.”

Although work done in India is sent back to the U.S. where the PCAOB can re-view it, there is no formal agreement that allows the board to inspect audit firms in India. In addition, the Institute of Chartered Accountants of India has no way of regulating centres carrying out U.S. work.

World Bank says 600 million new jobs needed by 2020A study by the World Bank states that the global economy needs to produce at least 600 million new jobs by 2020 to absorb a surging workforce and keep current employment levels constant, particularly in Asia and sub-Saharan Africa. The report, 2013 World Development Report, stated that the private sector is the main engine of job creation and urged governments to implement policies that encourage businesses to hire more workers.

India, Australia to increase trade under new pactIndia and Australia have agreed to double bilat-eral trade to US$40 billion by 2015 under a new agreement signed last month. While New Delhi is reforming its aviation, energy and retail indus-tries, Australia has changed its position on ban-ning the sale of uranium to India – changes that will allow greater economic cooperation. Current two-way trade has increased by 13 percent an-nually in the past five years and stands at US$21 billion.

Japan cabinet to draw up fresh stimulus plansYoshihiko Noda, the Japanese prime minister, has ordered his cabinet to draw up a stimulus pack-age by the end of this month in a bid to boost Ja-pan’s subdued economy. Hurt by falling demand for exports and low domestic consumption, Japan’s economy grew by just 0.3 percent in the second quarter of this year. No details of the size of the package have been revealed.

Models sue agencies for fraudulent accountingFashion models are suing several agencies in the United States claiming that they have lost up to US$20 million due to fraudulent accounting methods. The class-action lawsuit accuses the modelling agencies of hiding funds and not pro-viding accurate financial statements. Companies being sued include Wilhelmina Models, Ford Models, Trump Model Management and Elite Models Management, advertising agencies Saat-chi & Saatchi and Leo Burnett, and the cosmetics giants Revlon and Maybelline.

New combined CPA designation to be rolled out in Canada from 1 JanuaryThe Canadian Institute of Chartered Accountants and CMA Canada have announced they will jointly oversee a new Chartered Professional Accountant Canada designation.

The two accounting organizations said they will launch a new combined oversight body for the new designation on 1 January 2013, as part of a larger plan to merge CAs and CMAs across Canada and create a new CPA designation that would streamline regulation.

The new body will create a certification programme for new CPAs and hold the first examinations in 2015.

Accounting is regulated on a provincial level in Canada and accounting organizations in each province must agree to merge and create the new CPA designation before it can actually be adopted. When the new CPA is launched, the CICA and CMA Canada will also continue their separate operations until all member provinces have merged.

CAs and CMAs have agreed to merger talks in seven of Canada’s 10 provinces. Provincial bodies of Canada’s third main accounting body – the Certified General Accountants Association – have opted out of the merger plan.

Concerns mount over U.S. audit work done in IndiaEx-PCAOB official criticizes oversight

NEWSINTERNATIONAL

10 November 2012

NEWSGREATER CHINA

ING Groep, one of Europe’s largest financial companies, has confirmed that it will sell all of its insurance and pension assets in Hong Kong, Macau and Thailand to the high-profile businessman Richard Li for US$2.14 billion.

The acquisition by Pacific Cen-tury Group, which is controlled by Li, is valued at 1.9 times the estimated book value of €865 million, according to a statement from Amsterdam-based ING.

“This acquisition is abso-lutely in line with Pacific Century Group’s strategy as a long-term holder and developer of assets and investments in three areas: financial services; technology, media and telecommunications; and property projects,” Li told the South China Morning Post.

Li’s father, business tycoon Li Ka-shing, promised to financially support his son’s new invest-ments when he detailed his suc-cession plans in May.

“With the money from his dad, it’s sensible for Li to make more of these acquisitions going for-

ward,” Benjamin Tam, an analyst at IG Investment Hong Kong, told Bloomberg before the announce-ment. “He has personal passion for the financial industry and had exposure in the insurance sector.”

The ING acquisition follows Li’s US$68 billion purchase of PineBridge Investments from American International Group in 2010.

The deal with Pacific Cen-tury Group was ING’s second significant sale in a month, after it agreed to sell its Malaysian business to AIA Group for US$1.7 billion.

ING has been selling its insur-ance and investment manage-ment operations in an attempt to repay the bailouts it received from the European Union.

The Hong Kong Monetary Author-ity intervened to weaken the Hong Kong dollar seven times in two weeks after the currency’s value was pushed up by increased inves-tor confidence around the world.

In its latest action, the author-ity sold HK$2.3 billion into the currency market on 1 November as the local currency repeatedly touched the upper limit of a 29- year-old peg to the U.S. dollar.

On 30 October, the HKMA added HK$2.1 billion to the Hong Kong banking system. On the day before, the authority sold HK$2.71 billion.

On 23 October the HKMA sold US$395 million worth of Hong Kong dollars in New York trade. Earlier on the same day, the au-thority, Hong Kong’s de facto cen-tral bank, said it had sold HK$6.63 billion in the foreign-exchange market in two interventions.

This followed a HK$4.67 bil-lion intervention on 19 October, the first time HKMA intervened since December 2009.

The authority said in a state-ment that it expects net inflows into the Hong Kong dollar to per-sist as investors seek investment opportunities in Hong Kong and

the Mainland.“Since the U.S. Federal Re-

serve’s launch of the third round of quantitative easing, demand for Hong Kong dollars has increased and similar rises are also noted in other currencies within the region,” the statement added.

The Hong Kong dollar is pegged at HK$7.80 to one U.S. dol-lar but is allowed to trade between HK$7.75 and HK$7.85. Under the currency board system adopted in 1983, the authority must inter-vene when the Hong Kong dollar hits either the upper or lower limit to keep the band intact.

PricewaterhouseCoopers is imposing a no-pay leave policy and a career-break programme for its Hong Kong staff in a bid to cut costs.

According to a PwC Hong Kong statement, all of the firm’s staff will be granted 12 days of additional leave, eight of which will be unpaid.

Departments in the Big Four firm will have different timelines for staff taking extra leave.

The firm will also launch a voluntary career break programme, which will allow its staff to take an extended break for either professional or personal reasons.

With this programme, staff can take a break, of between two weeks and six months, and will be paid 20 percent of their salaries during that time.

“We believe the approach taken is the most ideal in these challenging circumstances,” PwC said in a statement.

“The measured and bal-anced approach allows our people to spend more time with family and friends, while avoid-ing the unnecessary need for headcount reductions as PwC has no plans to implement any redundancy programmes,” the firm’s statement added.

In 2009, PwC instituted an unpaid leave programme in several of its offices, including the United Kingdom, Australia and Romania.

PwC staff face unpaid leave incost-cutting bid

ING sells its Asian insurance units to Richard Li in US$2 billion dealBusinessman says acquisition fits long-term development

HKMA steps in to weaken Hong Kong currency

Richard Li

AFP

November 2012 11

BDO, the fifth biggest accounting firm in Hong Kong by revenue, plans to merge with other firms in order to diversify its services.

The firm’s past mergers focused primarily on expanding its audit ability, said BDO’s chairman, Albert Au, but future acquisitions will focus on widening its services.

“Looking ahead, we would like to merge with firms with consultancy or other specialized skill sets so as to diversify... and provide more comprehensive services to the customers. The ultimate goal is for us to challenge... the Big Four firms,” the South China Morning Post quoted Au as saying.

According to the paper, Au also said that acquiring more specialists would help attract bigger customers and expand BDO’s client base.

The firm’s change in strategy has been expected by analysts, the SCMP reported, due to the substantial decline of initial public offerings and the low demand for auditing services in 2012.

In the first eight months of this year, the total value of new listings reached just under HK$43 billion, down 77 percent from last year.Hong Kong was the world’s largest IPO market in the last three years.

China’s GDP grew 7.4 percent in the July-September quarter from a year earlier, accord-ing to the National Bureau of Statistics, indicating that the economy had slowed for a seventh consecutive quarter. Annual growth in the second quarter was 7.6 percent.

The figures also marked the slowest growth since the first quarter of 2009, when the economy grew 6.5 percent.

A day before the release of the data, Premier Wen Jiabao gave what observers said was his most optimistic assessment of the economy since the start of the year.

“The economy in the third quarter was quite good. We can now say with confidence

that the growth of the Chinese economy is basically stabiliz-ing... As policies are imple-mented and hit their mark, the Chinese economy will stabilize further,” read Wen’s comments published on a government website.

He added that the govern-ment’s target of 7.5 percent an-nual growth – reduced this year from the previous 8 percent target – was well within reach.

Measures that the Chinese government has implemented include getting the central bank to cut interest rates in

June and July. Last month the government also approved infrastructure projects worth about US$157 billion. However, Beijing has not yet said where the money to fund these proj-ects is coming from.

Despite the weaker GDP data, other information released showed some signs of stabilization. In the year to Sep-tember, fixed asset investment grew 20.5 percent, industrial output grew 9.2 percent and retail sales grew 14.2 percent. Also more than 10 million jobs were created this year.

BDO in merger plans to take onbigger rivals

World trade body upholds ban on steel tariffsThe World Trade Organization last month upheld a ruling that Chinese tariffs on imports of steel from the United States were illegal.

China had imposed anti-dumping and anti-subsidy tariffs on grain-oriented electrical steel imported from the U.S. in response to the “Buy America” provisions of the 2009 U.S. stimulus package, which Beijing said was in effect giving subsidies to U.S. steel manufacturers.

In June, the WTO ruled against the tariffs, saying that China had failed to prove Buy

America’s damaging impact on the Chinese steel industry.

“Today we are again plainly stating that we will continue to take every step necessary to ensure that China plays by the rules and does not unfairly restrict exports of U.S. products,” BBC News quoted U.S. trade representative Ron Kirk as saying.

“The Obama administration will not allow China to break international trade rules,” added Kirk.

China’s Ministry of Commerce had no immediate

comment on the WTO ruling, Reuters reported.

The case is the latest in a series of trade conflicts between the two countries. Last month, the Obama administration filed a complaint accusing China of restricting exports of rare earth metals. In September, China filed a WTO complaint challenging U.S. anti-dumping measures on certain Chinese products exported to the U.S.

The WTO ruling came during the U.S. presidential debates, in which the issue of China came up several times.

Third-quarter GDP growth data reflect slowdown’s persistencePremier says latest figures suggest economy is stabilizing

7.4%Q3

7.6%Q2 growth growth

12 November 2012

NEWSGREATER CHINA

Former KPMG boss appointed SFC chairman The government has appointed Carlson Tong, former chairman of KPMG China and a for-mer vice president of the Institute, as the chairman of the Securities and Futures Com-mission. Tong’s term started on 20 October and ends on 19 October 2015. “The SFC plays a vital role in upholding Hong Kong’s position as a leading international financial centre, and I feel honoured to have been appointed as its chairman,” Tong said. He succeeds Eddy Fong, who retired last month.

Businesses keen for younger workers: report The Grant Thornton International Business Report revealed that at least a quarter of the workforce is under 30 years old in 60 percent of businesses in Hong Kong, up from 52 per-cent six months ago. The report found that 82 percent of responding employers highly value the adaptability of young recruits and 76 per-cent value their better grasp of technology.

Award winning accountant becomes CPC delegate Zhou Mingjue has become the only represen-tative selected from the Mainland’s 250,000 CPAs to attend the 18th National Congress of the Communist Party of China on 8 Novem-ber. Zhou works as the party chief in the Changsha, Hunan province branch of the ac-counting firm ShineWing. During his career in auditing, he has participated in national projects and has won numerous awards for his work.

Hong Kong enforces property tax for non-localsHong Kong’s Chief Executive Leung Chun-ying implemented the city’s first property tax for non-local buyers in order to address fears of a property bubble riding on the backs of low interest rates and monetary easing policies in the United States. Under this new policy, overseas buyers will have to pay a 15 percent tax upon purchase of prop-erty. Additionally, resale tax on property was raised by 5 percent.

Albert Au, chairman of BDO, has supported Ernst & Young’s citing of Chinese laws on state secrets as the reason for withholding audit-related records from the Securities and Futures Commission.

According to Au, his firm – a competitor of E&Y – and many other accounting firms had more than 70 percent of their Hong Kong staff doing auditing work in China. If the firm breached China secrecy laws, staff would be at risk, he added, the South China Morning Post reported.

“How about if such a breach of secrecy law caused all my staff to be banned from going to the Mainland, or what if they were detained as a result?” Au told the SCMP. “I can fully understand why E&Y refused to help the commission.”

While Au acknowledged the importance of accounting firms complying with the SFC’s rules in Hong Kong, he said that firms also need to follow Mainland laws and regulations. “China has clearly defined accounting papers to be a type of state secret,” he added.

The High Court is set to make a ruling in March next year on whether E&Y has to comply with SFC’s request for records related to the audit of the Chinese company Standard Water.

Au said that the court ruling would act as a guideline for all accounting firms in handling requests from the commission.

In August, E&Y declined a request from the SFC to hand over audit papers and accounting documents relating to the listing application of Standard Water. The firm resigned as the company’s auditor in March 2010 after finding inconsisten-cies in company documents. Standard Water subsequently withdrew its listing application.

BDO backs Ernst & Young in state secrets explanation

U.S. regulators reach auditing deal with Beijing PCAOB gains access to Mainland auditsThe Public Company Accounting Oversight Board in the United States an-nounced that it has reached an agreement allowing it to inspect audits in China.

Accounting regulators in the U.S. have long sought access to the audits of U.S.-listed corporations from China in order to address a growing number of business scandals. China previously resisted, citing sovereignty concerns.

The PCAOB and Chinese authorities “have signed an agreement to proceed with observational visits,” Colleen Brennan, spokeswoman for the board, said. “We expect them to take place within the next couple of months.”

James Doty, PCAOB chairman, had repeatedly said that a plan for such inspections had to be in place by the end of this year, reported Reuters.

Before an agreement was reached, the PCAOB and U.S. Securities and Exchange Commission had been working for months with China to try to reach a deal that would allow their inspectors into the Mainland. The two U.S. regula-tors met with their Chinese counterparts in Beijing in July and also in January in Washington to negotiate an agreement.

Consulting

14 November 2012

GIVINGAlfred Romann looks at the state of the consulting business and how pure consulting firms and accounting firms are competing in the Greater China market

THE BUSINESS OF

Illustrations by Harry Harrison

November 2012 15

J ust as schadenfreude had to be borrowed from German to ex-plain the concept of expressing delight at someone else’s mis-ery, there is no pre-cise English expres-

sion for turning challenges and difficulties into opportunity. But that’s what the consult-ing industry has been focusing on for years.

“In the past 10 to 15 years we have seen more problems,” says Joe Ngai, managing director of the Hong Kong office of McKinsey & Company, one of the world’s largest man-agement consulting firms. “Every corpora-tion we go to, we see problems. And problems are good for us because you need someone to solve those problems.”

Ngai’s optimistic candour – expressed at a recent business forum – is all the more re-markable because the consulting business is usually reluctant to talk about itself. While barely a day goes by without a consulting firm issuing an industry survey or business out-look, the firms are surprisingly averse to dis-cussing their own sector’s prospects.

Spokespeople for two of the world’s larg-est consulting firms, Accenture and Bain & Company, said that their staff couldn’t dis-cuss the industry itself, while Boston Con-sulting Group, another global giant, did not respond to a request for comment.

This reticence may be understandable. After all, the jury is still out on whether the consulting industry’s problem solving outweighs its problem creation. McKinsey famously advised U.S. telecoms giant AT&T in 1980 that there was little future in mobile phones, forecasting a market in 2000 that was less than 1/120th of its actual size.

Nevertheless, the consulting industry has continued to grow: Plunkett Research fore-casts worldwide consulting revenues in 2012 of US$391 billion, up almost 7 percent over 2011’s total of US$366 billion.

The consulting industry suffered a set-back as the global financial crisis took hold – 2009 saw a 9 percent decline in revenues over the previous year, according to Kennedy Information, an industry data provider.

But growth resumed the following year – McKinsey saw revenues rise 6 per-cent to US$7 billion in 2010 – as companies sought the services of consultants to over-see restructuring, mergers and acquisitions, turnarounds, corporate regime change and performance improvement. Concerns over complying with ever-tighter regulatory re-quirements also boosted the business.

The market potential did not go unno-ticed by the Big Four accounting firms who have re-entered the market in a big way since the aftermath of the collapse of Enron, when regulator and media pressure forced many to spin off their consulting arms. For instance,

Deloitte’s consulting revenue grew 15 per-cent in 2010, more than twice the pace of the previous year. China sets the paceThe Asia Pacific, with its tight-knit family companies and established connections, has been a harder slog for the consultants but slowly doors are opening.

New York-based Alvarez & Marsal has invested heavily in Asia in recent years, espe-cially in the China market. “Demand in Chi-na is on the rise,” says Olly Stratton, manag-ing director and co-head of the firm’s Asian practice. “I think it will continue to evolve and there will be more opportunities.”

McKinsey, too, sees potential in China. The company is among the leaders in consult-ing for Chinese clients, who seek advice on managing strategy, operations, information technology and human resources. More re-cently, Chinese clients have used consulting firms to advise on restructuring, expansion and foreign investment, brand building, cor-porate governance and long-term growth.

When management consultants entered the Chinese market in the early 1990s, most operated from Hong Kong regional head-quarters, but that has changed. “For most professional services today, there are no more Hong Kong offices – everyone is calling themselves the Greater China office,” says Ngai. “Most consultants today are spending

GOODADVICE

16 November 2012

Consulting

November 2012 17

The Big Four accounting firms might be in a better position than the pure consulting firms to grow their risk and advisory businesses in China because Chinese companies like having more services under one roof.at least 50 percent of their time or more on Mainland projects,” he adds. “Fifteen years ago, Mandarin was not a requirement. Today it is.”

Despite the apparent rush to the China market, some experts are wary about the reality of the Mainland. Fiona Czerniawska, founder of London-based Source for Consult-ing, which researches the consulting indus-try, cites a shortage of experienced Chinese consultants and fees that are often sub-stantially lower than in other, more mature markets as two significant obstacles. “At the moment, they see easier, if not bigger, oppor-tunities in Brazil and India,” she says.

Competing for clientsAccording to Czerniawska, the Big Four ac-counting firms might be in a better position than the pure consulting firms to grow their risk and advisory businesses in China be-cause Chinese companies like having more services under one roof. Accounting firms agree, citing a combination of their consult-ing capabilities and traditional strengths such as finance and accounting expertise.

Babak Nikzad, partner in charge at KPMG’s China and Hong Kong consulting practice says Big Four firms possess a “breadth of experi-ence we can bring to the client.” For example, he says, pure consulting firms usually lack experience in tax matters – an area in which accounting firms excel.

Norman Sze, managing partner of De-loitte Consulting China, cites a Mainland fi-nancial institution that commissioned IBM Global Services to design and implement the first phase of a financial management sys-tem. He says Deloitte was able to leverage its broader services to win the contract to imple-

ment the second phase of the contract.Sze, based in Shanghai, adds that De-

loitte can use its financial acumen to help the Mainland banking and insurance sectors im-plement international compliance standards such as Basel II or localized versions of global standards.

Already the figures are showing that the Big Four are expanding in the China consult-ing market. PwC employs about 1,000 staff in its China consulting practice and plans to grow it this year by about 20 percent. A joint venture between its U.S., China and Austra-lia operations will see an influx of consul-tants parachuted into China for three-year engagements. Hong Kong partner Andy Wat-kins, who runs the new joint venture, says the prospects in China are particularly good. “We have experienced rapid growth in the past few years. However, we believe it is still relatively early days in China,” he says.

There are several reasons for the Big Four’s optimism. One is that companies are increasingly looking for consultants who can address industry-specific issues that the Big Four specialize in, rather than general business ones. The complexity of emerging challenges like risk management and regu-latory compliance, both in China and glob-ally, are also areas in which the accounting giants have experience. Finally, there are an increasing number of Chinese companies in need of services outside China, which re-quires global networks.

Like PwC, KPMG’s consulting arm has also been growing rapidly and, with 800 members of professional staff in the Main-land, has a much larger presence in China than pure consulting firms. By comparison, Boston Consulting Group, which has been in

China for 30 years, has about 200 profession-al staff. Bain has about 150 consultants in its Greater China team. McKinsey, one of the largest, has about 350 consultants and 45 global partners in its China and Hong Kong practice.

Regulatory challengesFor a decade, the accounting firms have been playing catch-up in the consulting market. After the collapse of Enron, the Big Four saw their consulting arms in the U.S. restricted by the Sarbanes-Oxley Act. The new rules limit-ed the consulting services that auditors could provide to companies they audit, in order to avoid the conflicts of interest that led to En-ron’s auditor, Arthur Andersen, overlooking accounting misdemeanours.

The subsequent sell-off of two of the Big Four’s consulting arms changed the indus-try. IBM absorbed PwC Consulting in 2002 and turned it into an industry giant, while KPMG’s unit became Bearing Point, now smaller and focused mainly on Europe. Ernst & Young sold its consulting unit in 2000 to what is now Capgemini, while Deloitte Con-sulting was never spun off. (Arthur Ander-sen’s consulting unit was spun off as Accen-ture prior to the accounting firm’s demise.)

As the spotlight of Enron dimmed, the Big Four started re-launching or re-building their consulting arms. By 2007, all the Big Four firms were once again among the top 10 con-sultants in the world in terms of revenue.

While U.S. regulators don’t appear likely to re-visit the issues, the Big Four’s moves back into the consulting business have not gone unnoticed by regulators in Europe. Last year, the European Commission proposed that auditing firms be banned from pro-

November 2012 19

viding consulting services to companies they audit, or even be banned altogether from consulting.

Big Four firms say a decade of experience has enabled them to put controls into place to avoid conflicts of interest. Sze at Deloitte says avoidance of conflicts of interests is funda-mental to his firm’s culture.

“We keep lists of audit clients who can-not be pursued as relationship clients and vice versa,” he says. Further checks begin the moment the firm considers a project or new client. The firm also takes into account the rules covering listed companies in China, Hong Kong, the U.S. and any other relevant jurisdiction. OvercrowdingConsultants say they are feeling the pres-sure of a crowded market. The large number of consulting firms has led to brutal price competition, especially in China. “My biggest challenge at the moment is the pricing in the market,” says Nikzad at KPMG.

In China particularly, not only are the firms vicious when pricing, but there are double the bidders. Where once four or five firms would bid for a particular mandate in China, the number is now seven or eight, says Nikzad.

Consultants say it also means that firms have to think a little harder about their of-ferings, such as providing better service for lower prices or providing niche services that others don’t have.

“Specialist business advisory firms are increasingly moving... towards event-driv-en consulting,” adds Mavis Tan, a member of the Hong Kong Institute of CPAs who is senior managing director at FTI Consulting.

By “event-driven” services Tan means areas such as forensic and litigation con-sulting, regulatory and fraud-risk mitiga-tion, corporate restructuring and strategic communications. “As these firms get more traction in Hong Kong and the region, the markets gets more familiar with them and dependent on their services,” she says.

Fortunately for the crowd of competitors, demand in China is growing for new servic-es, particularly as a result of the international expansion of Chinese companies.

“Much of professional services today is across borders,” says Ngai of McKinsey. “Even in China today, most of the work we are seeing has some element of going abroad, of thinking about the competition that is coming from all over the world.”

“ We keep lists of audit clients who cannot be pursued as relationship clients and vice versa.”

20 November 2012

Veteran members

f all the ornaments, pho-tographs and paintings, one piece stands out in Sanford Yung’s beauti-

fully kept living room. On a dark wood book-stand by the wall sits the

autobiography My Life in China and America by Yung Wing.

“He was the first Chinese to graduate from an American University,” says San-ford Yung, a retired accountant, a member of the Hong Kong Institute of CPAs, founder of Sanford Yung & Co. and a former chair-man of Coopers & Lybrand (now Pricewater-houseCoopers), referring to the man on the cover. “He was my step-grandfather.”

In 1854, Yung Wing graduated from Yale University. After returning to Qing Dynasty China, he headed what was known as the Chinese Educational Mission under which a total of 120 Chinese students aged eight to 11 received education in the U.S.

Sanford Yung shares his step-grandfa-ther’s commitment to education. After retir-ing, he established the Sanford Yung Schol-ars Programme for Excellence in Accounting Studies in 2001, which began in Hong Kong and later expanded to Shanghai and Beijing.

Like Yung, many retired CPAs have had vibrant careers and have witnessed – indeed were involved in – the shaping of the ac-counting profession.

But even in retirement, with the can-do attitude they developed as accountants, many are finding themselves achieving new ambitions.

History makerTwo years after Sanford Yung founded his eponymous accounting firm in 1962, Coopers & Lybrand United Kingdom – then part of the Big Eight – approached Yung, seeking a pres-ence in Hong Kong. “They were big, I was small, and they asked if we would represent them in Hong Kong. I said yes,” Yung remembers.

Coopers & Lybrand originally wanted to work with Yung’s firm for a trial period of five years, but good impressions caused that plan to fall by the wayside. “After only one year, in 1965 they were so satisfied with my practice and professional standards, and perhaps also me personally, they hastened the so-called engagement and said, ‘Let us get into bed. Let’s go into partnership.’

“When I started my firm I had a staff of three. When I first represented Coopers I had a staff of 20. Thirty years later when I retired

Many of the Institute’s senior members have retired as accountants but are showing no signs of slowing down. Jemelyn Yadao looks back on their eventful careers and asks them what they’ve been up to Photography by Samantha Sin

WORKING OVERTIME

November 2012 21

“I said, ‘I’m the only partner and you allow my staff below me, an Englishman, to look at the minute books and not me? I don’t want the job.’ So I thanked him and left.”

Sanford Yung

22 November 2012

from practice I had a staff of 750. So the ex-pansion was quite rapid and quite gratify-ing,” recalls Yung, who became chairman of Coopers & Lybrand Hong Kong in 1965.

Of course, the rapid growth of the firm meant Yung had to deal with many challenges.

He recalls one in particular involving the 1959 purchase of Mercantile Bank by the Hongkong and Shanghai Banking Corpo-ration. In 1965, Mercantile moved its head office from the U.K. to Hong Kong and was jointly audited by Peat Marwick Mitchell (now known as KPMG) and Coopers & Ly-brand. An invitation to meet with a man named Freddie Knightly from Mercantile Bank in Hong Kong led to Yung sitting in an uncomfortable meeting.

Knightly reminded Yung that Mercan-tile was now a subsidiary of Hongkong and Shanghai Banking Corporation, alluding to the parent bank’s policy of allowing only ex-patriates into the secrets of its financial re-cords. “I said, ‘I’m the only partner and you allow my staff below me, an Englishman, to look at the minute books and not me? I don’t want the job.’ So I thanked him and left.”

Half an hour after Yung got back to his office, he received a call from Knightly. “Knightly said: ‘You win. You can certainly look at our private books.’

“I accepted it on those terms and became the first Chinese in the then 75-year histo-ry of Mercantile Bank to sign their secrecy book – a book directors and auditors must sign vouching that you would not divulge anything you see,” says Yung. “I stood up for the Chinese in my profession of which I am extremely proud. I made it a point to raise the standard of my profession.”

Although the Sanford Yung Scholars Pro-gramme is now fully sponsored by PwC, his interest in the charity’s work remains strong. “The main purpose of the scholarship is to recognize and encourage good students [in accounting],” Yung explains. “We send stu-dents from Hong Kong to do internships in PwC London. And those from Shanghai and Beijing we second to New York for intern-ship. This is very meaningful.”

Yung is also chief donor to the Sir Ed-ward Youde Memorial Fund, which was established in 1987 in memory of the gover-nor of Hong Kong between 1982 and 1986, who died suddenly on a visit to Beijing. “Two days after his death I sent HK$1 mil-lion to start the memorial fund and now ev-ery year I contribute money,” he says.

The fund, which bestows fellowships,

scholarships and education awards to out-standing students in Hong Kong, has contrib-uted about HK$21 million to nearly 600,000 students over 25 years, says Yung. “The par-ents of those young awardees are so grateful they come with their son or daughter with tears in their eyes to collect the prize.”

Getting China on track Nellie Fong remembers her education in ac-counting being somewhat different to the

programmes students experience today.As part of her training, the now retired Insti-tute member and former chairman of PwC’s China operations, did two things: adding all the numbers in a telephone directory and going to the supermarket to calculate total costs at the till using mental arithmetic.

“At that time in England, 12 pence equalled one shilling and 20 shillings equalled one pound… I would stand by the screen and add in my head and at the end I

Veteran members

November 2012 23

A PLUS

should know exactly how much it would say on the receipt. I was as good as that.”

While doing long additions became second nature to Fong, a trip to newly opened China wasn’t as easy. Fong, who joined Arthur An-dersen in 1973, volunteered to go to the Main-land in the 1980s to set up an office for the firm and was faced with a list of difficulties.

“The laws and rules were not in order and you couldn’t hire your own people because the Chinese government controlled employ-

ment agencies. Everything was very dif-ficult,” Fong remembers. “The hardest part was we were losing money because there were no jobs and no work. Every year I had to explain to management why we were not making money and appear before the board to explain that it wasn’t an expense, it was an investment.”

Eventually, the firm built up a roster of clients made up of foreign multinational companies investing in China.

Fong’s decision to pursue her career in the Mainland changed her life in more ways than one. After being a member of the Hong Kong Legislative Council from 1988 to 1991, Fong was appointed by the Chinese govern-ment as a Hong Kong adviser for the prepara-tory committee on the territory’s transfer of sovereignty to China. It was during this time that Fong devised a project that she holds dear to her heart to this very day. “Provinces in China were planning on giving us a gift to mark the occasion so I felt that Hong Kong should give back to China,” she recalls. “I came up with a hospital built on a train.”

Fong founded the charity project Lifeline Express – a train-mounted eye hospital that travels to remote areas of China to provide free operations to blind cataract patients. It launched on 1 July 1997, the day Hong Kong returned to Chinese sovereignty.

With around five million cataract pa-tients in China and an increase of 500,000 patients each year, Fong is working to ex-pand the reach of her trains. “We are now training local doctors to do cataract opera-tions and setting up cataract centres in local hospitals. We call it a Lifeline Express train that never leaves,” she says.

Fong, who in 2008 received a Global Initiative Award from former U.S. Presi-dent Bill Clinton for her charity work, now has four trains, 15 training facilities and 17 cataract centres. Rather than using her time in retirement to wind down, she is fully en-gaged with the charity’s work, addressing issues such as the lack of senior eye doctors in China. “I went all over the world, ap-pealed to international experts to come to China and help... That’s why I’m very busy. I’m retired from my accounting career yet found something very worthwhile.”

Man of the match Taking orders for tea, coffee and sandwich-es was just one of T. Brian Stevenson’s duties while working for an audit group, fresh out of university in Scotland. “It was a master-servant relationship, that’s how it was,” re-

“We are now training local doctors to do cataract operations and setting up cataract centres in local hospitals.”

Nellie Fong

Veteran members

24 November 2012

calls Stevenson, a past Institute president, a veteran tax accountant and the chairman of the Hong Kong Jockey Club. “Maybe we had a longer learning path,” he ponders. “Nowa-days you might be thrown straight into the deep end.”

When Stevenson first moved to Hong Kong in 1970, he brought with him his love for a game he played often as a schoolboy – rugby. After holding nearly every office in the Hong Kong Rugby Union, he is now presi-dent. “Rugby has really developed in Hong Kong and I’ve been involved in the Hong Kong Sevens. It’s been fortunate being in-volved in things that have turned out quite successfully.”

Rugby is of course not the only sport he has a passion for. The Scotsman was elected

chairman of the Jockey Club in 2010 and takes great pride in the club’s charity work. “The club’s charity trust is just an amaz-ing organization. Our donations last year reached a record high of HK$1.73 billion in one year. To be involved in it, I regard it as a serious privilege,” he said.

Stevenson, who also serves on the boards of HSBC and the Mass Transit Railway Cor-poration, looks back fondly at an eventful four decades in Hong Kong.

He helped set up the accounting firm Tur-quands Barton Mayhew in the city in 1974.

“There were two of us and we had 2,000 empty square feet in the Pedder Building. I was actually involved with engaging staff to start a business, buying second-hand furni-ture to put into the office and ended up with

one of Hong Kong’s largest accounting firms. It was a marvellous experience,” he says.

The firm grew with mergers including, those with Whinney Murray Ernst & Ernst that formed Turquands Ernst & Whinney in 1979, until the merger of Ernst & Whinney and Arthur Young created Ernst & Young.

Just a week before that merger was an-nounced, Stevenson was appointed senior partner of Ernst & Whinney for Asia. “I was dealing with people older than me, more se-nior than me from across the world in pull-ing the firm together.”

While managing the rapid growth of the firm was a challenge, Stevenson says man-aging the insolvency of the Carrian Group while he was at Ernst & Whinney in 1983 was one of the hardest tasks in his career.

Carrian’s reach was so broad that it had been a client of many accounting firms, which eliminated them from the role of liquidator. “Most major firms were out and we came in. It was a major case for the firm globally.”

Despite the firm’s lack of insolvency ex-perience they won the engagement.

“I’m a very competitive person, which comes from sports, and I apply that to busi-

“The club’s charity trust is just an amazing organization. Our donations last year reached a record high of HK$1.73 billion in one year. To be involved in it, I regard it as a serious privilege.”

T. Brian Stevenson

November 2012 25

ness as well,” says Stevenson. “I do want to try and win.”

Right time, right placeWhen Marina Wong first joined Coopers & Lybrand in 1968, she was one of the few female auditors in the company. Her then boss Sanford Yung encouraged her to move departments and expand her skills even fur-ther. “He asked me whether I was interested in joining another department: corporate services and accounting. So I was able to do a bit of tax, secretarial, accounting and also liquidation work there,” recalls Wong, an Institute member and an independent non-executive director of Kerry Properties and Hong Kong Ferry Holdings.

Wong’s career at PwC spanned more than 30 years before she retired as partner in

2004. During her time at the firm, she volun-teered to help spearhead the development of the firm’s business in China, just as the Main-land was opening to the outside world.

“To be able to witness the development of the firm, especially in China, and also the development of China, I consider myself re-ally lucky,” she says. “My timing was just perfect.”

She helped set up the firm’s first office in Guangzhou in 1979, followed by offices in Shanghai, Beijing and Shenzhen in the 1980s. And she was there to grapple with the effects of the Tiananmen Square crackdown in 1989. “I had to convince my partners, es-pecially those overseas, that China was still a great market for the firm. It cast a lot of doubt,” she remembers.

Retiring at the age of 55, she found that

slowing down was not for her. “I guess I’m still energetic. I think it’s important to keep yourself to date with what’s going on in the society, in the world and also the business sector,” she said.

Like many of her retired peers, Wong is applying her expertise and experience to help companies as a director. As well as her engagements at Kerry Properties and Hong Kong Ferry, she was a director and consul-tant of Tricor Services, a business consul-tancy, from 2004 to 2006. In 2010, she took up another independent non-executive di-rector position at China World Trade Center Company, based in Beijing.

“If there is anything I can help with and contribute, I certainly would like to.”

Bottling successAs chairman and self-professed “chief talker” of Wan Corporate Services, a brand-building and distribution business of con-sumer products in the Asia Pacific, Vincent Wan considers himself semi-retired. “I don’t do any real work but I still keep busy. If there are strategic things for me to take on, then I’ll do it,” he says.

“To be able to witness the development of the firm, especially in China, and also the development of China, I consider myself really lucky. My timing was just perfect.”

Marina Wong

November 2012 27

Wan is talkative, a trait he developed from years of working in a broad range of industries. Wan was trained both as an ac-countant and an industrial engineer and went from founding his own consultancy firm in 1979 to serving as the Asia Pacific di-rector of manufacturing for American jeans- maker Levi Strauss & Co.

Then Wan decided to go into the world of marketing. “I felt I should use the skills I learned from accounting and from industri-al engineering to go on to communicate with people,” he recalls.

“At the end of the day, as head of manu-facturing of a jeans company, I am not the person who sits behind the sewing ma-chine... Levi’s is a very people-oriented orga-nization that was kind enough to give me the opportunity.”

Shortly after his career at Levi’s, he es-tablished Wan Corporate Services and has since been engaged in the marketing and distribution of consumer products including Perrier.

The versatile Wan recalls feeling unim-pressed when a friend offered him his first sip of the bottled fizzy water.

“Back in 1978, Perrier wasn’t known in Hong Kong. I tasted it and said, ‘What’s so special?’ My friend said, ‘Time [magazine] called it the marketing miracle of the de-cade.’ In New York in those years there was a power drink – the martini. This was the new definition of a power drink.”

Wan successfully launched Perrier throughout the Asia Pacific and was equal-ly successful in handling a blow to the product’s reputation in 1990, when small amounts of benzene – a carcinogenic solvent – were found in several bottles in the U.S.

“The press were very surprised that I was the first to answer the phone, but because of this crisis I made it a rule that nobody else apart from me should answer incoming calls,” he recalls. “I said: ‘If it’s a journalist calling, let me handle it.’ ” The subsequent

worldwide recall by Perrier made the French company seem responsible and Wan’s open-ness made the brand name far more recog-nizable in Hong Kong. “At that time I can-not tell you I enjoyed it, but now thinking back, it was a very good experience,” Wan recalls.

Today, the products Wan’s company dis-tributes are mostly natural. “When I passed the age of 50, I became less materialistic so the way I look at life has changed. I don’t believe in pharmaceutical products, I like herbal, natural things and I believe in doing exercise even at my age.”

Wan plays table tennis and squash twice a week. “I don’t play all the four corners. I play the back two corners and make sure I don’t overstretch myself,” he says with a laugh.

“The press were very surprised that I was the first to answer the phone, but because of this crisis I made it a rule that nobody else apart from me should answer incoming calls.”

Vincent Wan

Corporate governance

28 November 2012

November 2012 29

PANELS OF

PROBITY

When Enron collapsed in 2002, the United States Senate com-mittee that led the post-mortem accused

the company’s audit committee of sitting idly by and carelessly overlooking risky ac-counting practices, conflicts of interest and hidden debt.

Ten years later, audit committees remain in the spotlight.

In the European Union, moves are afoot to tighten audit committee accountability, including making all audit-related services subject to the prior approval of the audit committee, while regulators in the U.S. say

they will examine final EU legislation for possible adaptation.

In the U.S., audit committee documents are reported to have spurred a probe into bribery allegations concerning Sands China, the casino operator. Meanwhile, a regulator in Canada recently barred the chairman and chief executive of a controversial Toronto-listed Chinese shoemaker, Zungui Haixi, from securities trading for not properly maintaining an audit committee.

An audit committee forms a vital lynch-pin of effective corporate governance. Po-sitioned between senior management and the external auditor, a good audit commit-tee monitors the management’s judgment

on financial reporting matters and suggests improvements that can be made to internal controls.

In the past seen as more of a passive over-seer, audit committees are increasingly be-ing asked to step up to a more active role.

“They should have a good understanding of the business,” says Nancy Tse, director of finance and information technology servic-es of the Hospital Authority and formerly a member of the Hong Kong Institute of CPAs’ audit committee guide review task force. “They should study the reports they receive and spend time preparing for meetings.”

While many experts agree that audit committees need to demonstrate more in-

Audit committees are being required to take on a more active role in monitoring companies, as

George W. Russell reportsIllustrations by Vivian Ho

volvement in the companies they serve, there is still some uncertainty surrounding precisely how they should do it and the skills needed by committee members to achieve it.

Fresh eyesIndependence, most agree, is one of the cornerstones of an audit committee’s effec-tiveness, particularly as they are charged with overseeing areas where judgments and estimates are significant. “A commit-tee composed only of independent directors is a leading practice and in many countries is a requirement,” says Paul Ngai, a risk and control solutions partner with Pricewater-houseCoopers in Beijing.

An audit committee is supposed to give a fresh point of view, and their views should be precisely that: independent. “The board should have a strong understanding of the relevant definitions of independence and how a lack of independence occurs and is in-terpreted in practice,” says Tim Copnell, an associate partner at KPMG and director of the firm’s audit committee institute in London.

In Hong Kong, the stock exchange List-ing Rules were amended in 2004 to mandate that all audit committee members have to be non-executive directors and that at least one of them must have appropriate financial ex-perience.

From 1 April this year, the Listing Rules were further amended. The recommended best practice that an audit committee’s terms of reference should include arrangements for employees to raise concerns, in confi-dence, about financial reporting impropri-eties was upgraded to a code provision – meaning issuers must comply or explain why they are not.

A new recommended best practice rec-ommending the audit committee establish a whistleblowing policy for other matters was also introduced in the amendments.

“We consider the audit committee the most appropriate committee to be respon-sible for an issuer’s whistleblowing policy,” an HKEx spokesman says. “We believe that an issuer should be able to define a whistle-blowing policy that is appropriate to its own circumstances, so we do not propose to de-fine in detail the contents of its policy.”

The new changes include a recommend-ed best practice that the audit committee should meet with the external auditor at least twice a year so that the performance and progress of the audit is discussed. This is also a recommendation in the audit commit-tee guidelines published by the Hong Kong

Institute of CPAs.Audit committee relations with exter-

nal auditors are an international concern. “There has been increasing focus on the im-portance of a strong relationship between the audit committee and the external audi-tor, and the need for candid, ongoing com-munication,” says Catherine Bromilow, a PwC partner in New York who leads the firm’s U.S. corporate governance practice.

However, parts of the HKEx rules, espe-cially those to do with the skills that audit committee members should possess, are open to interpretation. “While the Listing

Rules provide for specific requirements on what constitutes ‘independence,’ the defini-tion of ‘appropriate financial experience’ is seen as too general,” says Randy Hung, ex-ecutive director and chief financial officer of China Fiber Optic Network System Group and an Institute member. “For example I have seen non-accountants or junior accoun-tants named as independent non-executive directors.”

Peter Tisman, the Institute’s director of specialist practices, says the Institute sup-ports the stock exchange’s efforts to incre-mentally strengthen the requirements for audit committees under the Listing Rules and Corporate Governance Code. “It is now a mandatory requirement under the Listing Rules that listed companies form an audit committee, with a majority of independent non-executive directors,” he says. “The com-position is specified and the minimum scope of the terms of reference is set out.”

However, he adds that more could be done to strengthen audit committees, such as stipulating a minimum number of audit committee meetings to be held annually and introducing clearer requirements for evalu-ations of individual directors’ performance.

“Given the fundamental importance of the accounting and finance-related over-sight role of an audit committee, the effec-tiveness of the committee could be improved

by specifying that there should be a quali-fied accountant as an independent non-executive director among its membership,” says Tisman.

Becoming more activeAs well as independent oversight, experts say audit committees need to demonstrate leadership and actively ascertain informa-tion. At present, some observers view audit committees as mere box-tickers. “Audit com-mittees often play a very passive role in a company,” notes Julian Russell, managing director of Pacific Risk, a Hong Kong-based consultancy. “They are sometimes merely shown the accounts and asked for comments on them.”

After the collapse of Enron and World-Com, the Sarbanes-Oxley Act in the U.S. forced audit committees into a more active role. New requirements forced audit com-mittees to be more probing, for example de-manding reports from external auditors on the principles used and the effects of alterna-tive choices.

“Once a simple board committee with few specific duties, the audit committee is now a key element of corporate governance,” says Tom Gorman, a securities lawyer with the Dorsey & Whitney firm in Washington with wide Sarbanes-Oxley experience. “The post Sarbanes-Oxley audit committee is more than the supervisor of the issuer’s financial functions,” he adds. “The committee has been transformed into an in-house monitor, which at times appears to be virtually a sepa-rate entity from the company.”

In Hong Kong, the direct effects of Sar-banes-Oxley were more muted. While it cre-ated few new obligations, it has ultimately led to more thorough documentation of in-ternal controls such as information technol-ogy systems that support financial report-ing, and governance controls such as ethics and standards, anti-fraud and whistleblow-er guidelines. “Its main impact was on moni-toring the effectiveness of internal financial controls at companies with U.S. connec-tions,” says Tisman at the Institute.