the bangchak petroleum plc

TRANSCRIPT

PRIVATE & CONFIDENTIAL ���� JANUARY 2008

The Bangchak Petroleum Plc.

1

STRICTLY PRIVATE & CONFIDENTIAL

The information contained herein is being furnished on a confidential basis for discussion purposes only and only for the

use of the recipient, and may be subject to completion or amendment through the delivery of additional documentation.

Except as otherwise provided herein, this document does not constitute an offer to sell or purchase any security or

engage in any transaction. The information contained herein has been obtained from sources that The Bangchak

Petroleum Public Company Limited (“BCP”) considers to be reliable; however, BCP makes no representation as to, and

accepts no responsibility or liability for, the accuracy or completeness of the information contained herein. Any

projections, valuations and statistical analyses contained herein have been provided to assist the recipient in the

evaluation of the matters described herein; such projections, valuations and analyses may be based on subjective

assessments and assumptions and may utilise one among alternative methodologies that produce differing results;

accordingly, such projections, valuations and statistical analyses are not to be viewed as facts and should not be relied

upon as an accurate representation of future events. The recipient should make an independent evaluation and

judgment with respect to the matters contained herein.

The Bangchak Petroleum Public Company LimitedThe Bangchak Petroleum Public Company Limited210 210 SukhumvitSukhumvit 64 Rd., 64 Rd., PhrakhanongPhrakhanong, Bangkok 10260, Bangkok 10260

Disclaimer

2

STRICTLY PRIVATE & CONFIDENTIAL

Contents

► Company Background

► Refinery Improvement

► Marketing Business

► Performance

► Appendices

3

Company Background

4

STRICTLY PRIVATE & CONFIDENTIAL

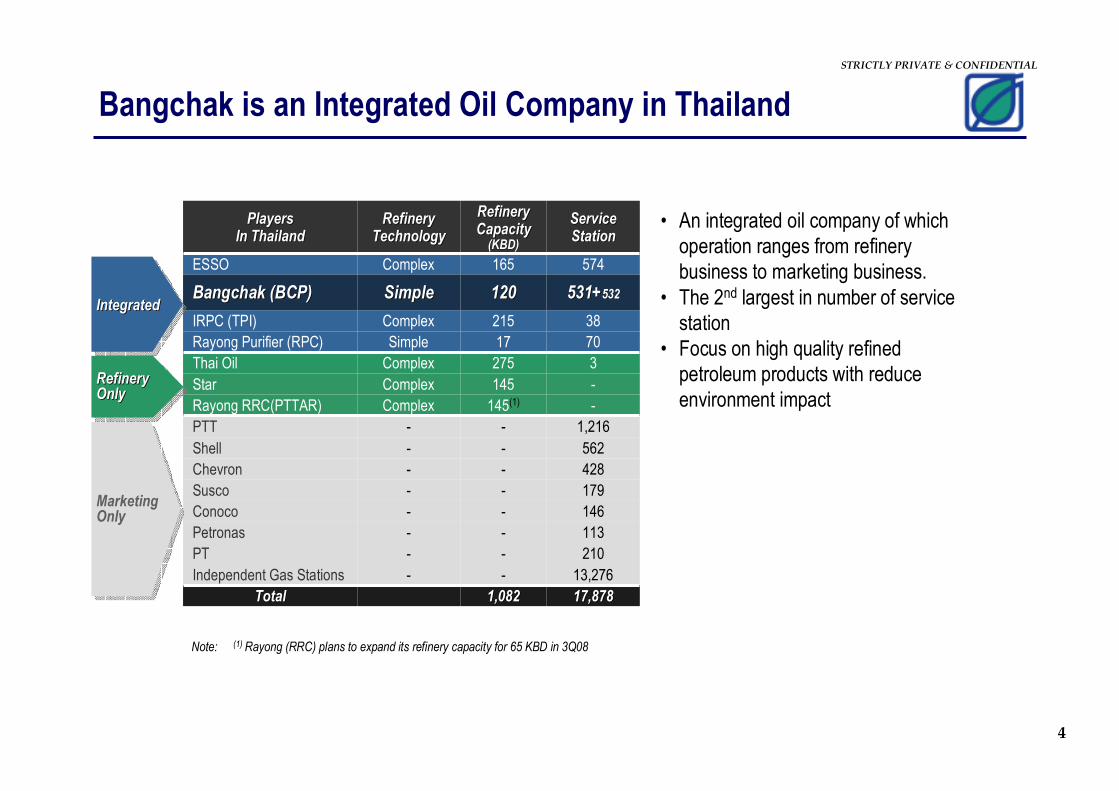

Bangchak is an Integrated Oil Company in Thailand

210--PT

38215ComplexIRPC (TPI)

3275ComplexThai Oil

-145ComplexStar

-145(1)ComplexRayong RRC(PTTAR)

574165ComplexESSO

531+531+532532120120SimpleSimpleBangchak (BCP)Bangchak (BCP)

7017SimpleRayong Purifier (RPC)

146--Conoco

13,276--Independent Gas Stations

113--Petronas

179--Susco

428--Chevron

562--Shell

1,216--PTT

17,87817,8781,0821,082TotalTotal

ServiceServiceStationStation

Refinery Refinery CapacityCapacity

(KBD)(KBD)

Refinery Refinery TechnologyTechnology

PlayersPlayersIn ThailandIn Thailand

• An integrated oil company of which operation ranges from refinery business to marketing business.

• The 2nd largest in number of service station

• Focus on high quality refined petroleum products with reduce environment impact

Note: (1) Rayong (RRC) plans to expand its refinery capacity for 65 KBD in 3Q08

IntegratedIntegratedIntegrated

RefineryOnly

RefineryRefineryOnlyOnly

MarketingOnly

MarketingOnly

5

STRICTLY PRIVATE & CONFIDENTIAL

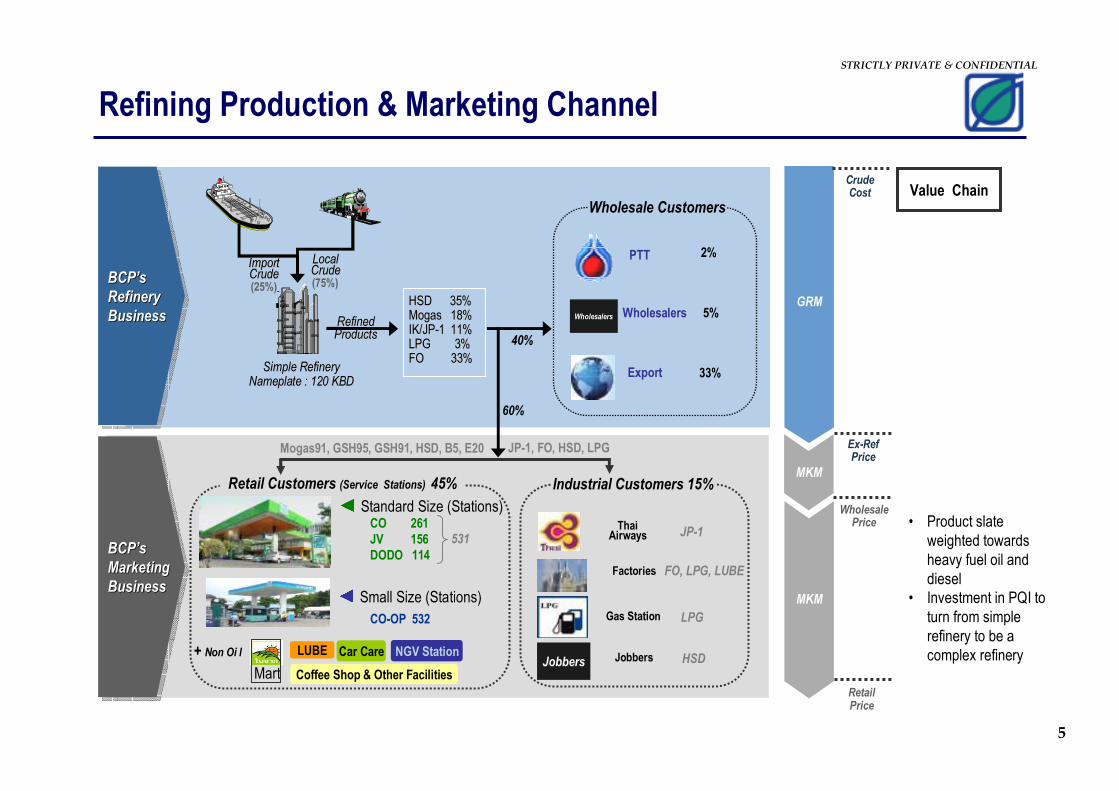

Refining Production & Marketing Channel

Jobbers

ThaiAirways

Factories

Jobbers

BCP’s

Refinery

Business

BCPBCP’’ss

RefineryRefinery

BusinessBusiness

ImportImportCrudeCrude(25%)

LocalLocalCrudeCrude(75%)

Simple RefinerySimple RefineryNameplate : 120 KBDNameplate : 120 KBD

Wholesalers

PTT

Wholesalers

Export

Wholesale Customers

Retail Customers (Service Stations) 45%

RefinedRefinedProductsProducts

BCP’s

Marketing

Business

BCPBCP’’ss

MarketingMarketing

BusinessBusiness

GRM

MKM

CrudeCost

Ex-RefPrice

WholesalePrice

RetailPrice

HSDHSD 35%35%MogasMogas 18%18%IK/JPIK/JP--1 1 11%11%LPGLPG 3%3%FOFO 33%33%

MKM

CO 261

JV 156

DODO 114

CO-OP 532

+ Non Oi l

Value Chain

40%

60%

2%

5%

33%�Standard Size (Stations)

NGV StationLUBE

�Small Size (Stations)

Mogas91, GSH95, GSH91, HSD, B5, E20

Mart

Car Care

Coffee Shop & Other Facilities

Industrial Customers 15%

JP-1, FO, HSD, LPG

JP-1

FO, LPG, LUBE

HSD

Gas Station LPG

• Product slate weighted towards heavy fuel oil and diesel

• Investment in PQI to turn from simple refinery to be a complex refinery

531

6

STRICTLY PRIVATE & CONFIDENTIAL

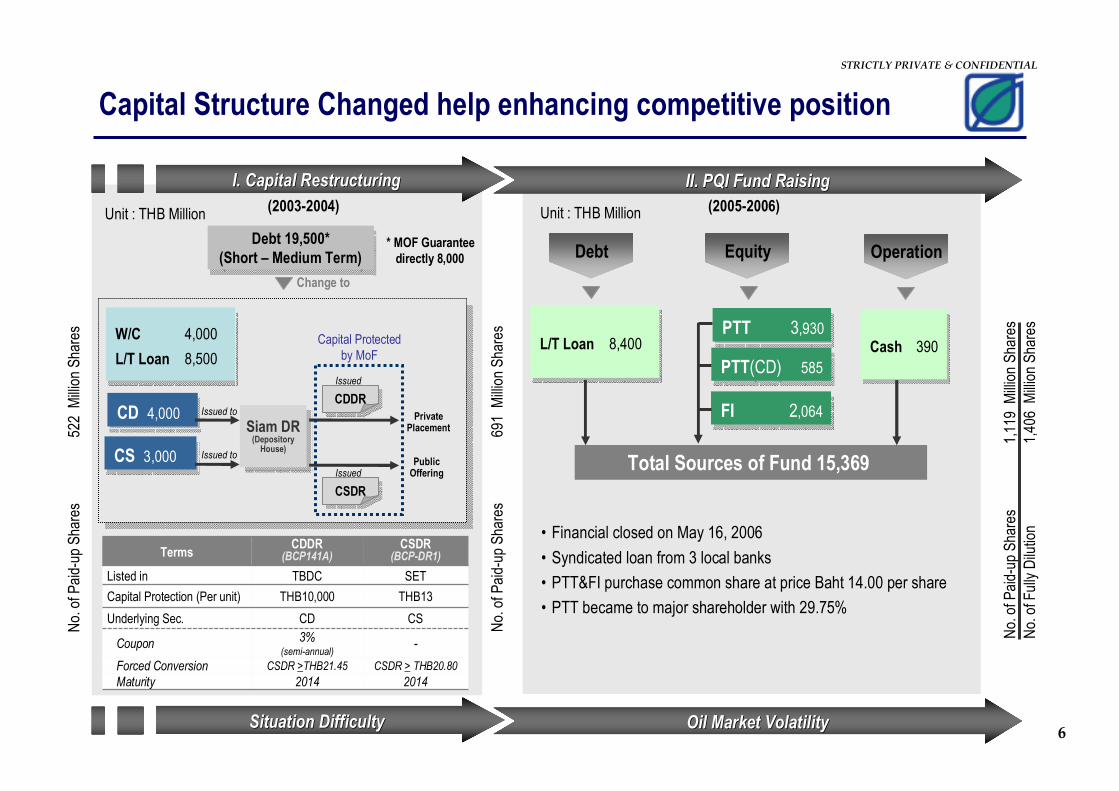

Capital Structure Changed help enhancing competitive position

I. Capital RestructuringI. Capital Restructuring II. PQI Fund RaisingII. PQI Fund Raising

Siam DR(Depository House)

Siam DR(Depository House)

W/C 4,000

L/T Loan 8,500

W/C 4,000

L/T Loan 8,500

CS 3,000CS 3,000

CD 4,000CD 4,000 PrivatePlacement

Issued to

Issued to

CSDRCSDR

PublicOffering

CDDRCDDR

Issued

Issued

Capital Protectedby MoF

Unit : THB Million

Debt 19,500*

(Short – Medium Term)

Debt 19,500*

(Short – Medium Term)

Change to

* MOF Guarantee

directly 8,000

No. of Paid-up Shares 522 Million Shares

No. of Paid-up Shares 691 Million Shares

No. of Paid-up Shares 1,119 Million Shares

No. of Fully Dilution

1,406 Million Shares

L/T Loan 8,400L/T Loan 8,400

FI 2,064FI 2,064

PTT 3,930PTT 3,930

Debt Equity Operation

Cash 390Cash 390

PTT(CD) 585PTT(CD) 585

Total Sources of Fund 15,369

Unit : THB Million

• Financial closed on May 16, 2006

• Syndicated loan from 3 local banks

• PTT&FI purchase common share at price Baht 14.00 per share

• PTT became to major shareholder with 29.75%

(2003-2004) (2005-2006)

Situation DifficultySituation Difficulty Oil Market VolatilityOil Market Volatility

SETTBDCListed in

2014

THB13

2014Maturity

CSDR > THB20.80CSDR >THB21.45Forced Conversion

-3%

(semi-annual)Coupon

CSCDUnderlying Sec.

THB10,000Capital Protection (Per unit)

CSDR(BCP-DR1)

CDDR(BCP141A)Terms

7

STRICTLY PRIVATE & CONFIDENTIAL

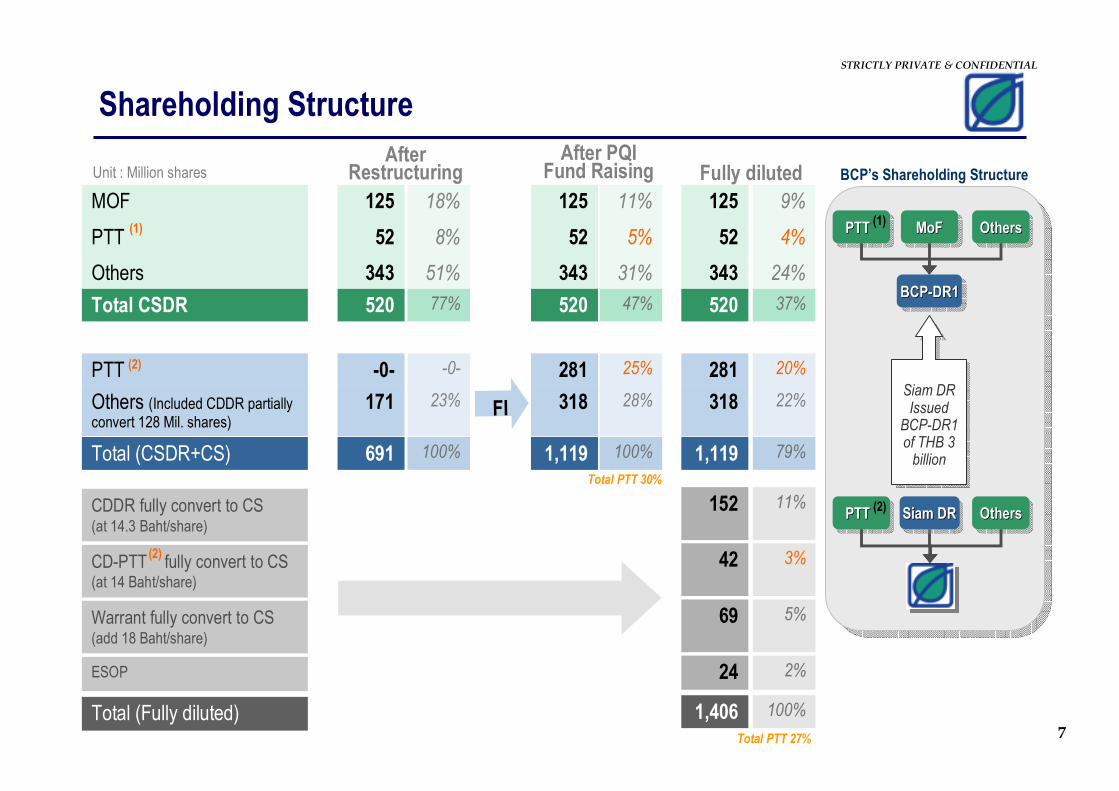

Shareholding Structure

MOF

PTT

Others

125

52

343

11%

5%

31%

FI

Total CSDR 520

PTT -0-

Total (CSDR+CS) 691

47%

25%

100%

Unit : Million shares

CDDR fully convert to CS(at 14.3 Baht/share)

Total (Fully diluted)

Warrant fully convert to CS(add 18 Baht/share)

CD-PTT fully convert to CS(at 14 Baht/share)

Fully diluted

125

52

343

520

281

1,119

ESOP

18%

8%

51%

77%

-0-

100%

After Restructuring

125

52

343

520

281

1,119

9%

4%

24%

37%

20%

79%

Others (Included CDDR partially convert 128 Mil. shares)

171 28% 31823% 318 22%

152 11%

42 3%

69 5%

24 2%

1,406 100%

BCP’s Shareholding Structure

PTT PTT PTT OthersOthersOthers

MoFMoFMoFPTT PTT PTT OthersOthersOthers

BCP-DR1BCPBCP--DR1DR1

Siam DRSiam DRSiam DR

Siam DR IssuedBCP-DR1of THB 3 billion

Siam DR IssuedBCP-DR1of THB 3 billion

(1)

(2)

(1)

(2)

(2)

Total PTT 30%

Total PTT 27%

After PQI Fund Raising

8

STRICTLY PRIVATE & CONFIDENTIAL

Key Strength & Opportunity

Bangchak Green Net

49%

(Subsidiary Company)

Fuel Pipeline Transportation

11%

(Related Company)

Key StrengthKey Strength

• Integrated oil company of which operation ranges from

refinery business to marketing business

• The 2nd largest in number of service stations through

out the country 1,063 stations

• Strong position in renewable energy and biofuels

• Plant configuration fit with gasohol base production

• PTT as a major shareholder

• Plant Locate in Bangkok which is the center of oil

damand

OpportunityOpportunity

• High oil prices drive demand in alternative fuel

• Government policy to support biofuels by widen price

gab between gasohol and gasoline normal grade

9

Refinery Improvement

• PQI• Cogeneration Unit• Natural Gas for Plant Feed

10

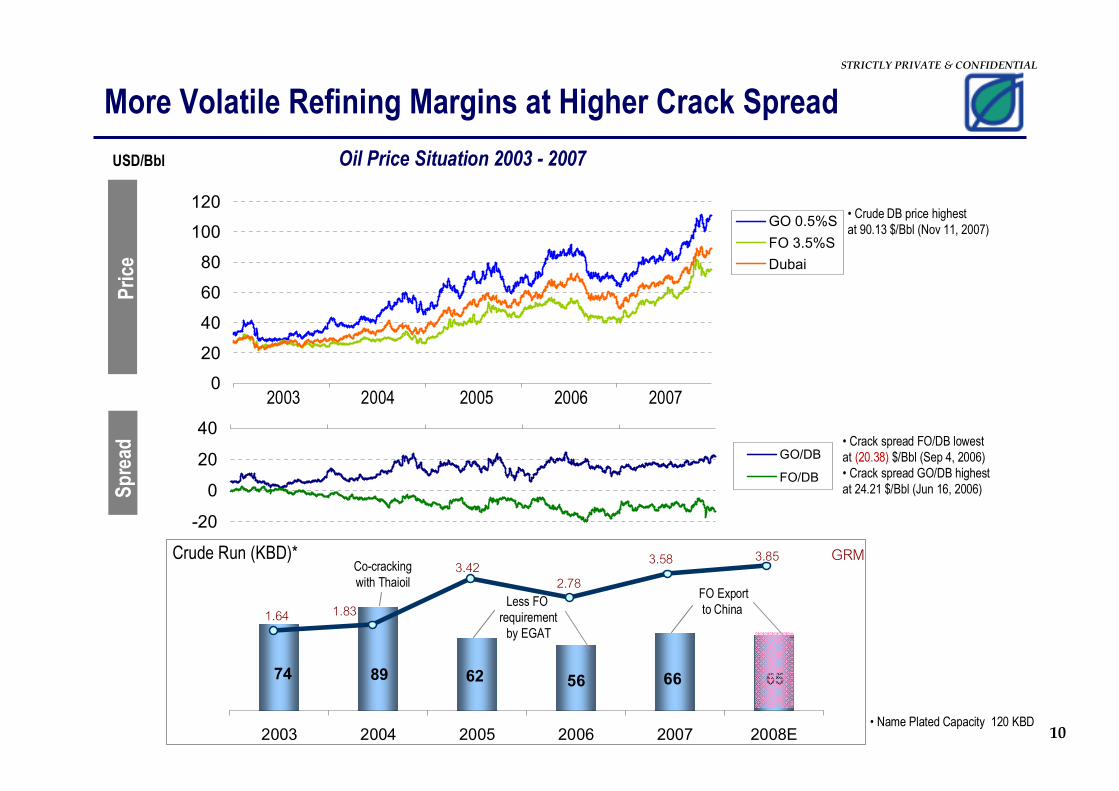

STRICTLY PRIVATE & CONFIDENTIAL

0

20

40

60

80

100

120

2003 2004 2005 2006 2007

GO 0.5%S

FO 3.5%S

Dubai

-40

-20

0

20

40

GO/DB

FO/DB

6566566274 89

-

20

40

60

80

100

120

2003 2004 2005 2006 2007 2008E

1.64 1.83

3.42

2.78

3.58 3.85 Base GRM

USD/Bbl

• Crack spread FO/DB lowest at (20.38) $/Bbl (Sep 4, 2006)• Crack spread GO/DB highest at 24.21 $/Bbl (Jun 16, 2006)

• Crude DB price highest at 90.13 $/Bbl (Nov 11, 2007)

2003 2004 2005 2006 2007

Crude Run (KBD)*

FO Exportto China

More Volatile Refining Margins at Higher Crack Spread

• Name Plated Capacity 120 KBD

Price

Spread

Oil Price Situation 2003 - 2007

Co-crackingwith Thaioil

Less FO requirementby EGAT

11

STRICTLY PRIVATE & CONFIDENTIAL

USD/bbl

10

8

6

4

2

0

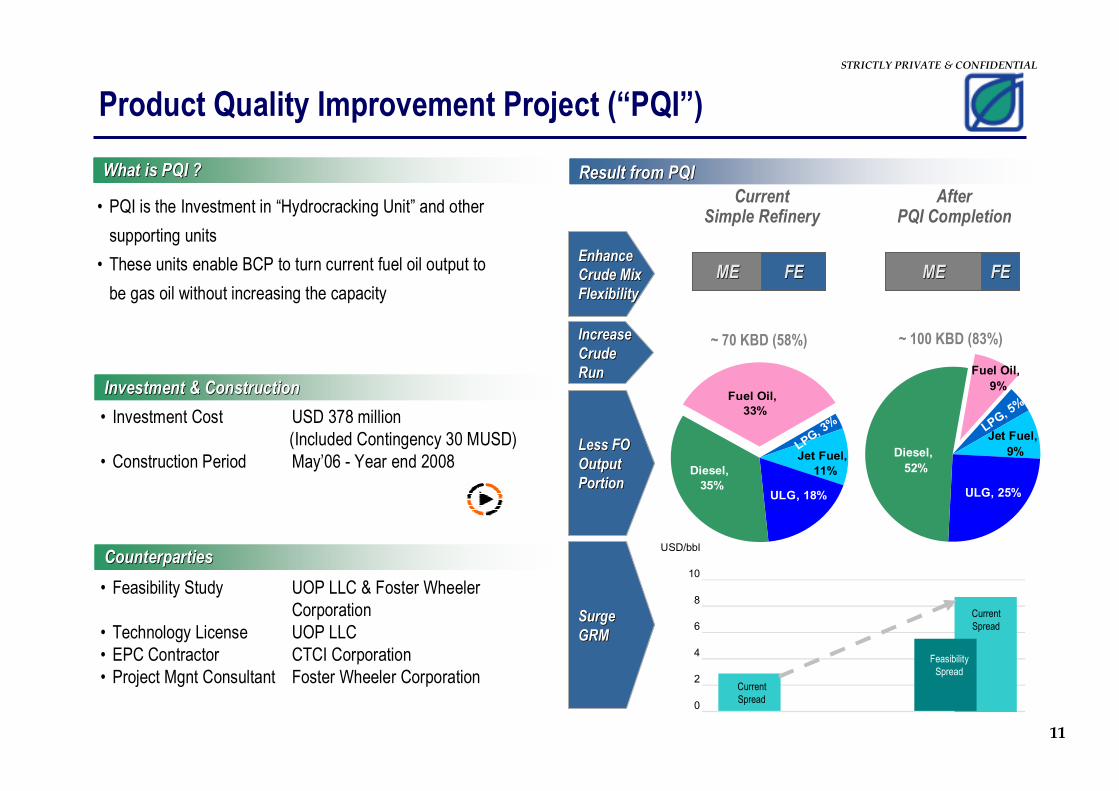

Product Quality Improvement Project (“PQI”)

What is PQI ?What is PQI ? Result from PQIResult from PQI

CounterpartiesCounterparties

• PQI is the Investment in “Hydrocracking Unit” and other

supporting units

• These units enable BCP to turn current fuel oil output to

be gas oil without increasing the capacity

• Feasibility Study UOP LLC & Foster Wheeler Corporation

• Technology License UOP LLC• EPC Contractor CTCI Corporation• Project Mgnt Consultant Foster Wheeler Corporation

• Investment Cost USD 378 million (Included Contingency 30 MUSD)

• Construction Period May’06 - Year end 2008

Investment & ConstructionInvestment & Construction

MEME FEFEMEME FEFE

CurrentSimple Refinery

AfterPQI Completion

EnhanceEnhance

Crude MixCrude Mix

FlexibilityFlexibility

Less FOLess FO

OutputOutput

PortionPortion

SurgeSurge

GRMGRM

CurrentSpread

CurrentSpread

FeasibilitySpread

LPG, 3%

Diesel,

35%ULG, 18%

Jet Fuel,

11%

Fuel Oil,

33%

LPG, 5%

Diesel,

52%

ULG, 25%

Jet Fuel,

9%

Fuel Oil,

9%

IncreaseIncrease

Crude Crude

RunRun

~ 70 KBD (58%) ~ 100 KBD (83%)

12

STRICTLY PRIVATE & CONFIDENTIAL

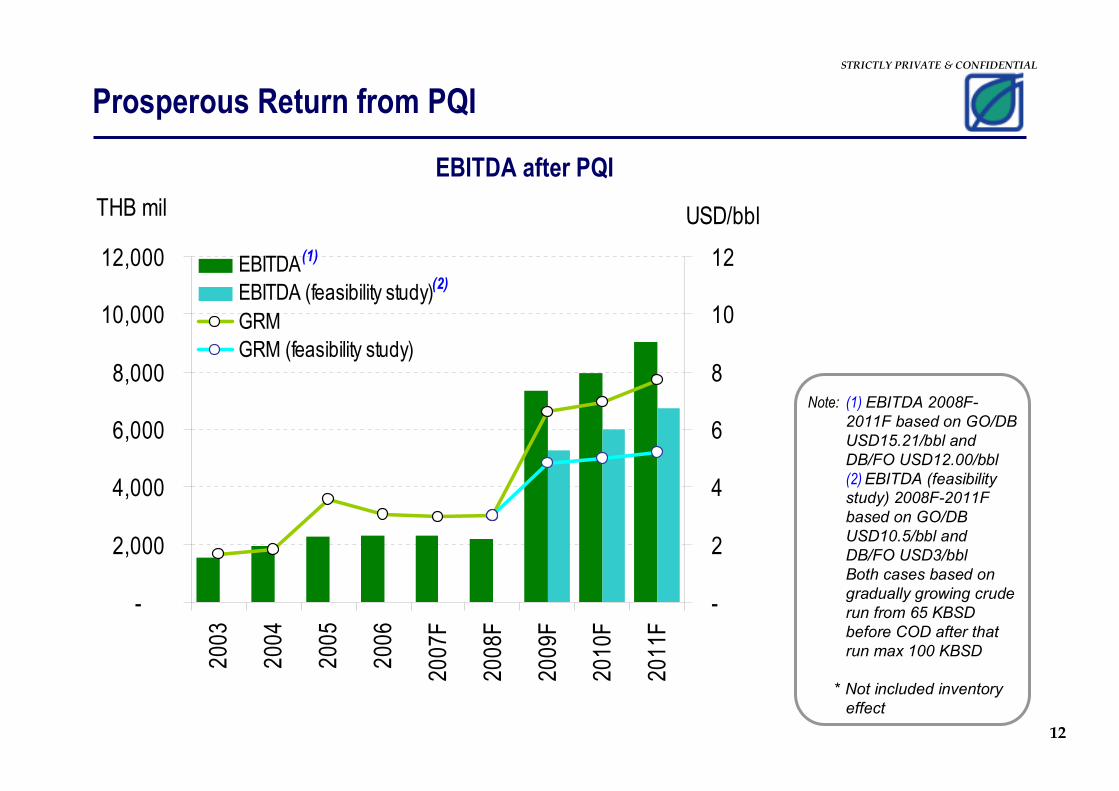

-

2,000

4,000

6,000

8,000

10,000

12,000

2003

2004

2005

2006

2007F

2008F

2009F

2010F

2011F

THB mil

-

2

4

6

8

10

12

USD/bbl

EBITDA

EBITDA (feasibility study)

GRM

GRM (feasibility study)

EBITDA after PQI

Prosperous Return from PQI

Note: (1) EBITDA 2008F-

2011F based on GO/DB

USD15.21/bbl and

DB/FO USD12.00/bbl

(2)EBITDA (feasibility

study) 2008F-2011F

based on GO/DB

USD10.5/bbl and

DB/FO USD3/bbl

Both cases based on

gradually growing crude

run from 65 KBSD

before COD after that

run max 100 KBSD

* Not included inventory

effect

(1)

(2)

13

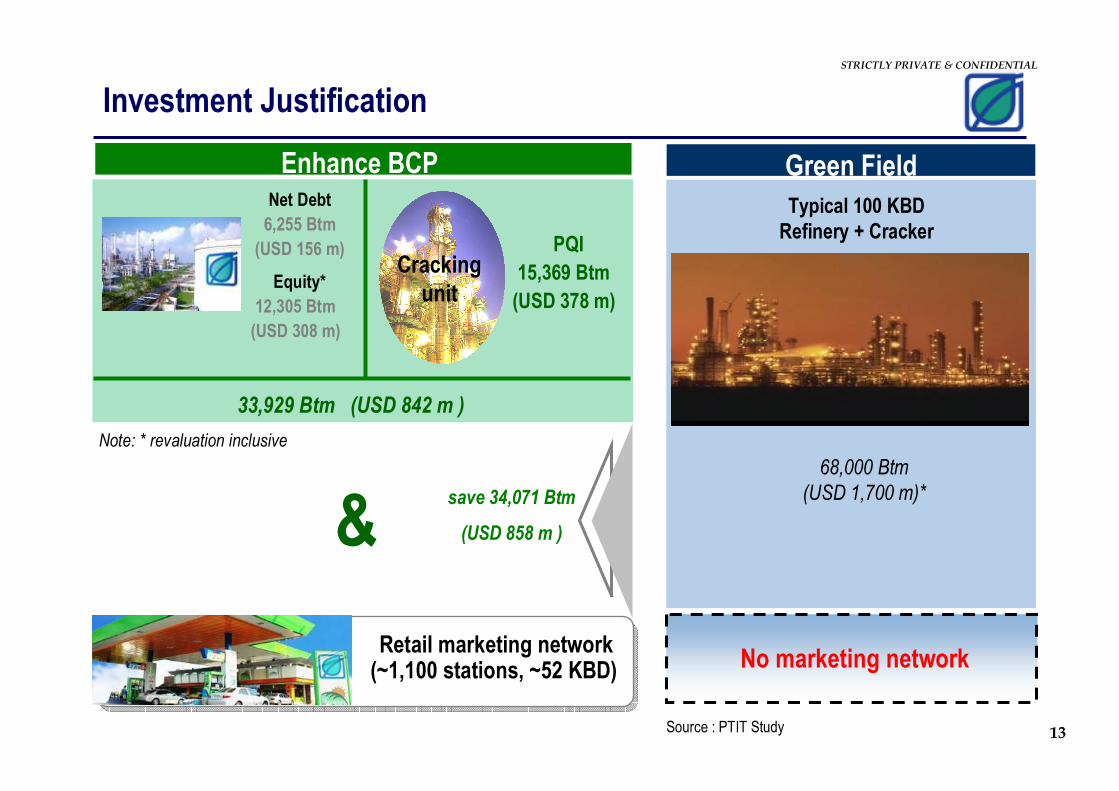

STRICTLY PRIVATE & CONFIDENTIAL

PQI

15,369 Btm

(USD 378 m) Equity*

12,305 Btm

(USD 308 m)

Net Debt

6,255 Btm

(USD 156 m)

68,000 Btm

(USD 1,700 m)*

&

33,929 Btm (USD 842 m )

Enhance BCP

Retail marketing network (~1,100 stations, ~52 KBD)

Typical 100 KBD

Refinery + Cracker

No marketing network

Note: * revaluation inclusive

Investment Justification

Green Field

save 34,071 Btm

(USD 858 m )

Cracking

unit

Source : PTIT Study

14

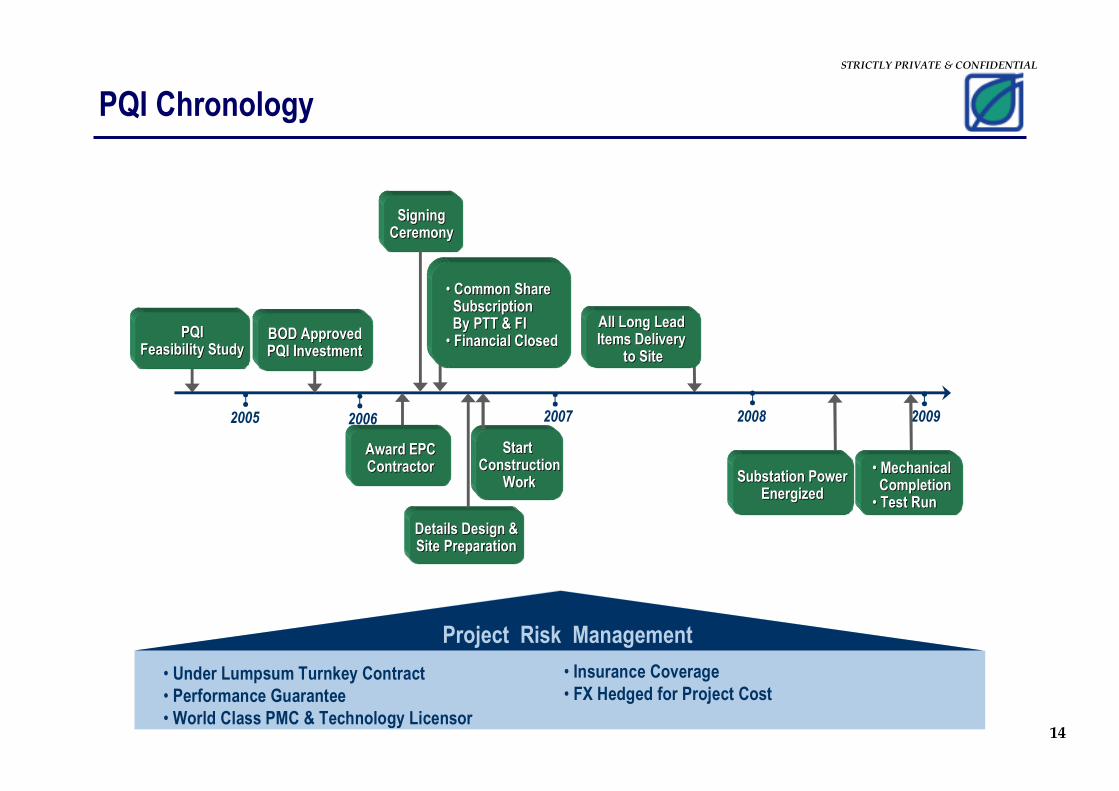

STRICTLY PRIVATE & CONFIDENTIAL

2006

PQIPQIFeasibility StudyFeasibility Study

Substation PowerSubstation PowerEnergizedEnergized

2007 2008

All Long Lead All Long Lead Items Delivery Items Delivery

to Siteto Site

2009

Award EPCAward EPCContractorContractor

2005

BOD ApprovedBOD ApprovedPQI InvestmentPQI Investment

Signing Signing Ceremony Ceremony

•• Common Share Common Share SubscriptionSubscriptionBy PTT & FIBy PTT & FI•• Financial Closed Financial Closed

Details Design &Details Design &Site PreparationSite Preparation

Start Start ConstructionConstruction

WorkWork•• MechanicalMechanicalCompletionCompletion•• Test RunTest Run

PQI Chronology

• Under Lumpsum Turnkey Contract

• Performance Guarantee•World Class PMC & Technology Licensor

Project Risk Management

• Insurance Coverage• FX Hedged for Project Cost

15

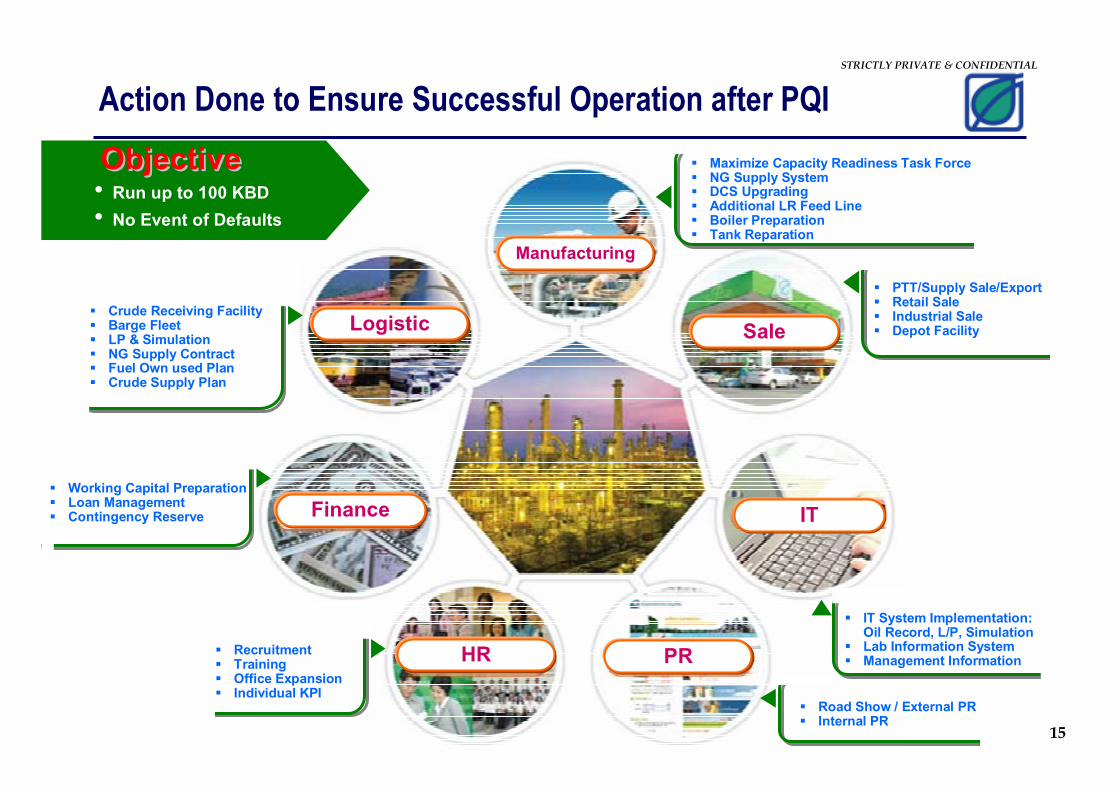

STRICTLY PRIVATE & CONFIDENTIAL

ObjectiveObjective• Run up to 100 KBD

• No Event of Defaults

Logistic

Manufacturing

Sale

PR

Finance

HR

IT

Action Done to Ensure Successful Operation after PQI

� Maximize Capacity Readiness Task Force� NG Supply System� DCS Upgrading� Additional LR Feed Line� Boiler Preparation � Tank Reparation

� PTT/Supply Sale/Export � Retail Sale� Industrial Sale� Depot Facility

� IT System Implementation:Oil Record, L/P, Simulation

� Lab Information System� Management Information

� Road Show / External PR� Internal PR

� Crude Receiving Facility� Barge Fleet� LP & Simulation� NG Supply Contract� Fuel Own used Plan� Crude Supply Plan

� Working Capital Preparation� Loan Management� Contingency Reserve

� Recruitment� Training� Office Expansion� Individual KPI

16

STRICTLY PRIVATE & CONFIDENTIAL

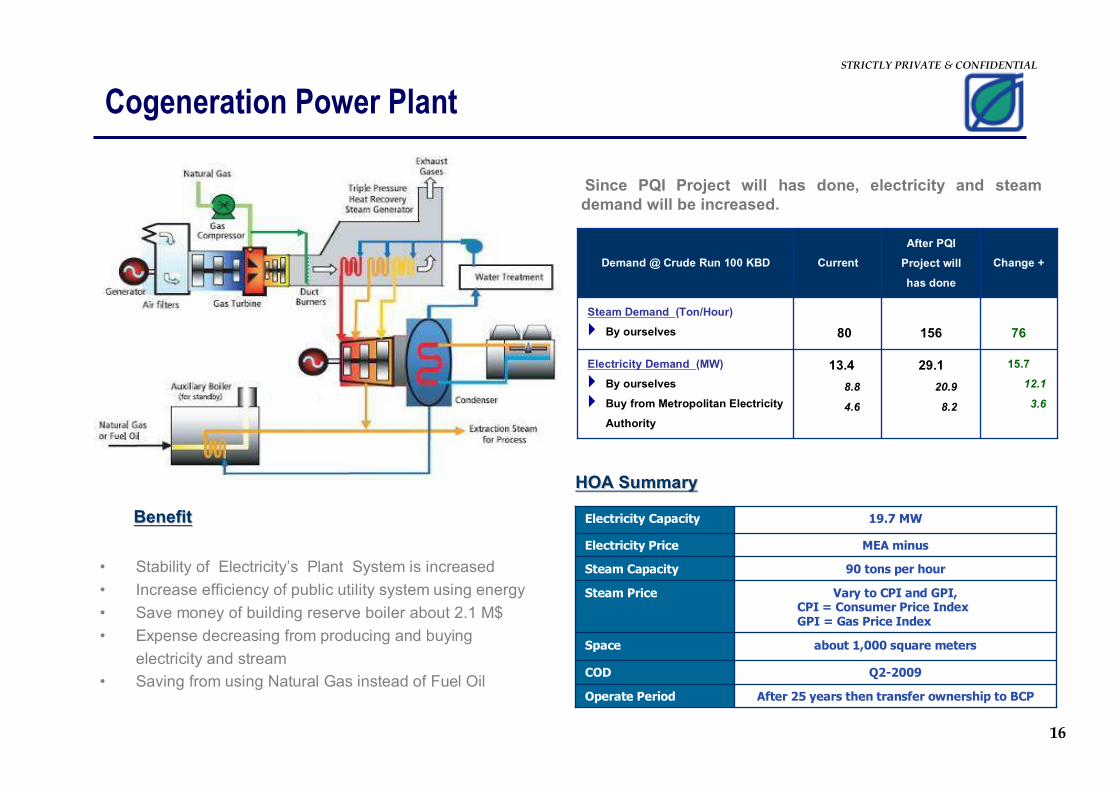

Cogeneration Power Plant

• Stability of Electricity’s Plant System is increased

• Increase efficiency of public utility system using energy

• Save money of building reserve boiler about 2.1 M$

• Expense decreasing from producing and buying

electricity and stream

• Saving from using Natural Gas instead of Fuel Oil

BenefitBenefit

Since PQI Project will has done, electricity and steam

demand will be increased.

15.7

12.1

3.6

76

Change +

29.1

20.9

8.2

13.4

8.8

4.6

Electricity Demand (MW)

� By ourselves

� Buy from Metropolitan Electricity

Authority

15680

Steam Demand (Ton/Hour)

� By ourselves

After PQI

Project will

has done

CurrentDemand @ Crude Run 100 KBD

about 1,000 square metersSpace

Q2-2009 COD

90 tons per hourSteam Capacity

After 25 years then transfer ownership to BCPOperate Period

Vary to CPI and GPI,CPI = Consumer Price IndexGPI = Gas Price Index

Steam Price

MEA minusElectricity Price

19.7 MWElectricity Capacity

HOA SummaryHOA Summary

17

Marketing Business

18

STRICTLY PRIVATE & CONFIDENTIAL

19.4%

Full Range of Products Under Marketing Business

Co-op

Standard

LPG

Diesel B5

Mogas 91

Gasohol 95

Gasohol 91

Diesel B2

JP1

Fuel Oil

NGV StationLUBE

Non Oil

Retail M

arketing

Industrial M

arketing

10.2

KBD %

10.1%5.3

7.6%4.0

9.1%4.8

28.8%15.1

0.8%0.4

14.1%7.4

10.1%5.3

100.0%52.5Total

Industrial

19

STRICTLY PRIVATE & CONFIDENTIAL

The Leader in Renewable Energy

• Sales volume ~52 KBD (250 ML/Month , 4th Market

Share)

• Pioneer in co-operative type service station and self

service station

• Leader in renewable energy (1st market share in diesel

B5 & 2nd in Gasohol)

• Cooperate with PTT to sell NGV in service stations

• Operating In - Station Non - Oil Business such as

Inthanin Café, Green Serve, Green Auto Service etc. • Service station Re-branding to capture new target group which

is younger generation

• Seeking partnerships for additional business in service stations

• Strengthen Gasohol and Biodiesel sales volume though

marketing network

• Researching and Developing renewable energy products

Marketing Strategy

Marketing Business Overview

20

STRICTLY PRIVATE & CONFIDENTIAL

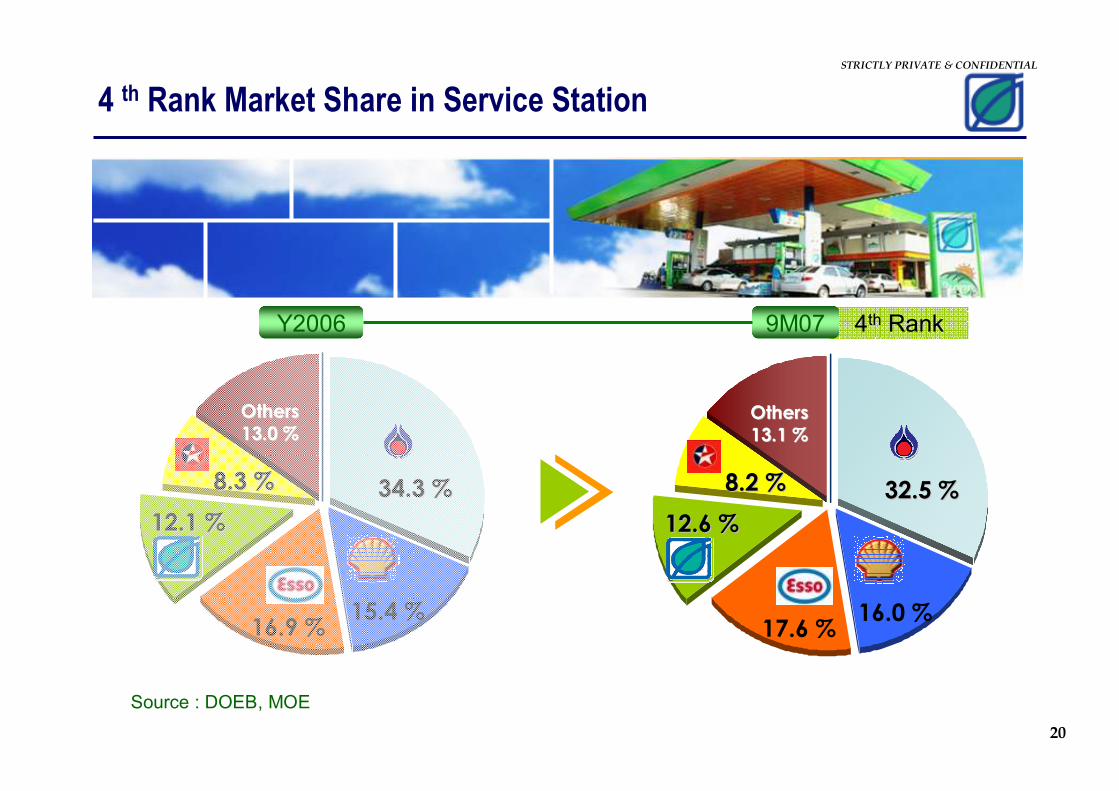

32.5 %32.5 %

16.0 %17.6 %

12.6 %12.6 %

8.2 %8.2 %

OthersOthers

13.1 %13.1 %

34.3 %34.3 %

15.4 %16.9 %

12.1 %12.1 %

8.3 %8.3 %

OthersOthers

13.0 %13.0 %

4th RankY2006 9M07

Source : DOEB, MOE

4 th Rank Market Share in Service Station

21

STRICTLY PRIVATE & CONFIDENTIAL

BCP

78.6%

PTT

21.4%

0

5

10

15

20

25

30

35

40

45

50

55

0

100

200

300

400

500

600

700

800

FY2006 Dec. 07

0

50

100

150

200

250

300

350

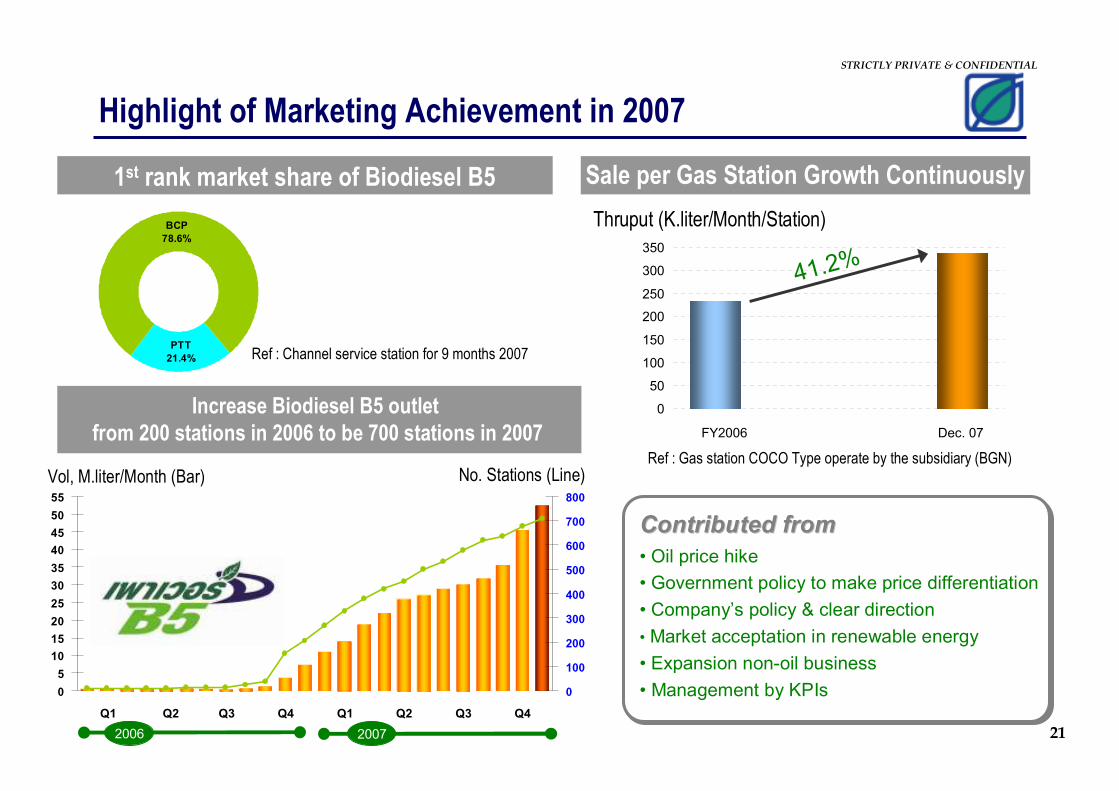

Highlight of Marketing Achievement in 2007

Thruput (K.liter/Month/Station)

Contributed fromContributed from

• Oil price hike

• Government policy to make price differentiation

• Company’s policy & clear direction

• Market acceptation in renewable energy

• Expansion non-oil business

• Management by KPIs

Sale per Gas Station Growth Continuously1st rank market share of Biodiesel B5

41.2%

Ref : Channel service station for 9 months 2007

Increase Biodiesel B5 outlet

from 200 stations in 2006 to be 700 stations in 2007

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2006 2007

Vol, M.liter/Month (Bar) No. Stations (Line)Ref : Gas station COCO Type operate by the subsidiary (BGN)

22

Performance

23

STRICTLY PRIVATE & CONFIDENTIAL

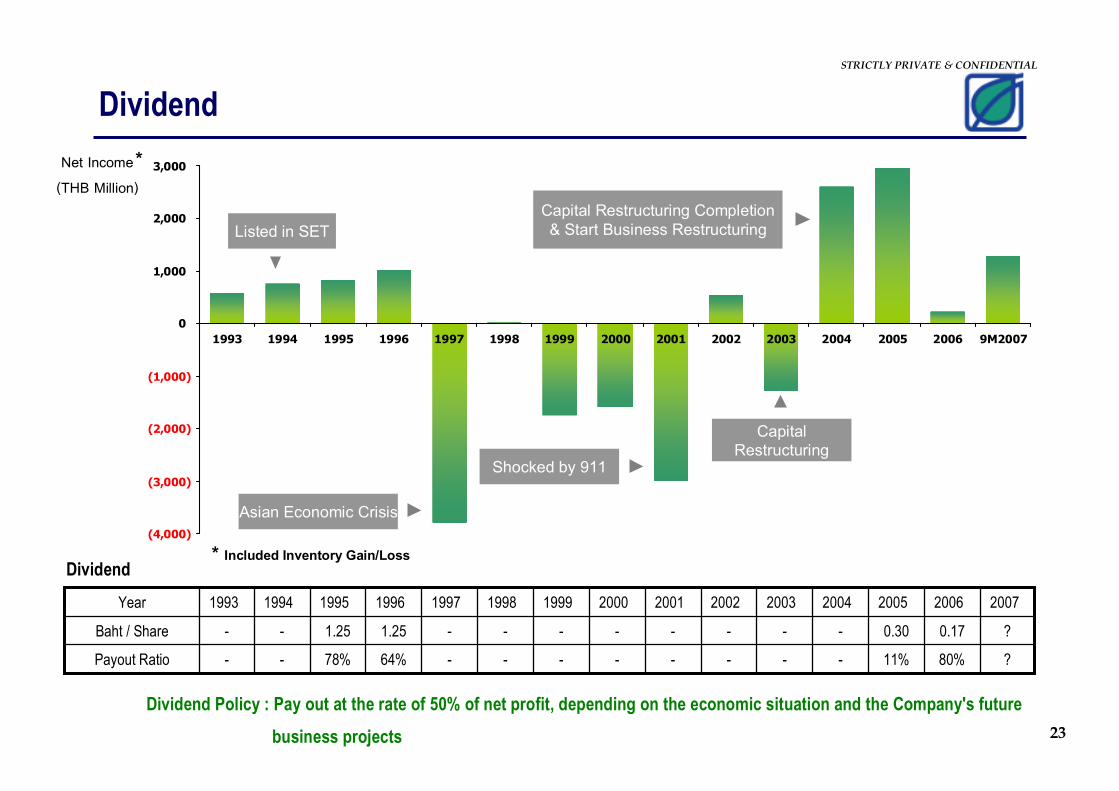

Net Income

(THB Million)

Dividend

(4,000)

(3,000)

(2,000)

(1,000)

0

1,000

2,000

3,000

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 9M2007

Listed in SET

Asian Economic Crisis

Shocked by 911

CapitalRestructuring

Capital Restructuring Completion& Start Business Restructuring

*

* Included Inventory Gain/LossDividend

-

-

1998

-

-

1997

64%

1.25

1996

-

-

2000

-

-

1999

-

-

2002

-

-

2001

-

-

2004

-

-

2003

11%

0.30

2005

78%

1.25

1995

?

?

2007

80% --Payout Ratio

0.17--Baht / Share

200619941993Year

Dividend Policy : Pay out at the rate of 50% of net profit, depending on the economic situation and the Company's future

business projects

24

STRICTLY PRIVATE & CONFIDENTIAL

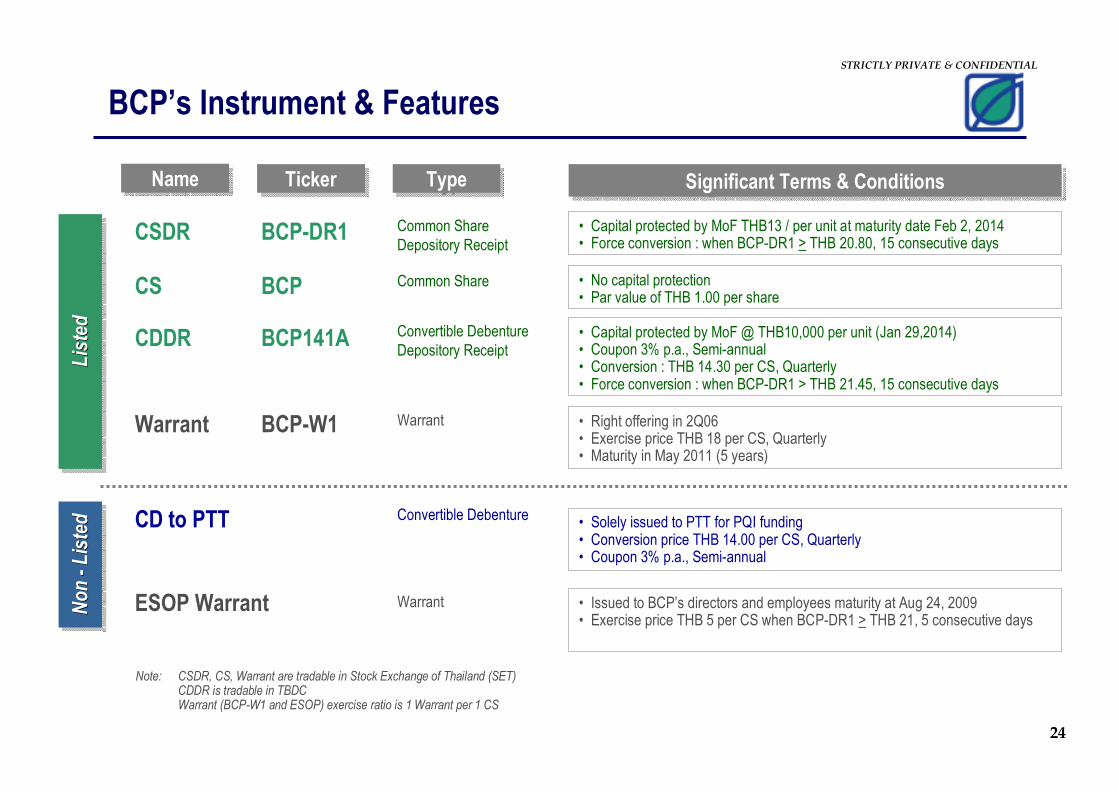

CSDR

CD to PTT

CS

Warrant

CDDR

ESOP Warrant

Lis

ted

Lis

ted

Lis

ted

Non -

Lis

ted

Non

Non --

Lis

ted

Lis

ted

• Capital protected by MoF THB13 / per unit at maturity date Feb 2, 2014• Force conversion : when BCP-DR1 > THB 20.80, 15 consecutive days

• No capital protection• Par value of THB 1.00 per share

• Right offering in 2Q06• Exercise price THB 18 per CS, Quarterly• Maturity in May 2011 (5 years)

• Capital protected by MoF @ THB10,000 per unit (Jan 29,2014)• Coupon 3% p.a., Semi-annual• Conversion : THB 14.30 per CS, Quarterly• Force conversion : when BCP-DR1 > THB 21.45, 15 consecutive days

• Solely issued to PTT for PQI funding• Conversion price THB 14.00 per CS, Quarterly• Coupon 3% p.a., Semi-annual

BCP-DR1

BCP

BCP-W1

BCP141A

TickerTickerNameName

• Issued to BCP’s directors and employees maturity at Aug 24, 2009• Exercise price THB 5 per CS when BCP-DR1 > THB 21, 5 consecutive days

Note: CSDR, CS, Warrant are tradable in Stock Exchange of Thailand (SET)CDDR is tradable in TBDCWarrant (BCP-W1 and ESOP) exercise ratio is 1 Warrant per 1 CS

Significant Terms & ConditionsSignificant Terms & ConditionsTypeType

Common Share Depository Receipt

Convertible Debenture

Common Share

Warrant

Convertible Debenture Depository Receipt

Warrant

BCP’s Instrument & Features

25

STRICTLY PRIVATE & CONFIDENTIAL

-

2

4

6

8

10

12

14

16

18

20

Dec Mar Jun Sep Dec Mar Jun Sep Dec Mar Jun Sep Dec Mar Jun Sep Dec

-

2

4

6

8

10

12

14

16

18

20

2004

Baht / Share

Stock Trading Price

Book Value as of Sep 30, 2007 at Baht 17.54 per share

Capital Protected

by MOF

only on BCP-DR1

2005 2006 2007

BCP-DR1 BCP Book Value

26

Appendices

27

STRICTLY PRIVATE & CONFIDENTIAL

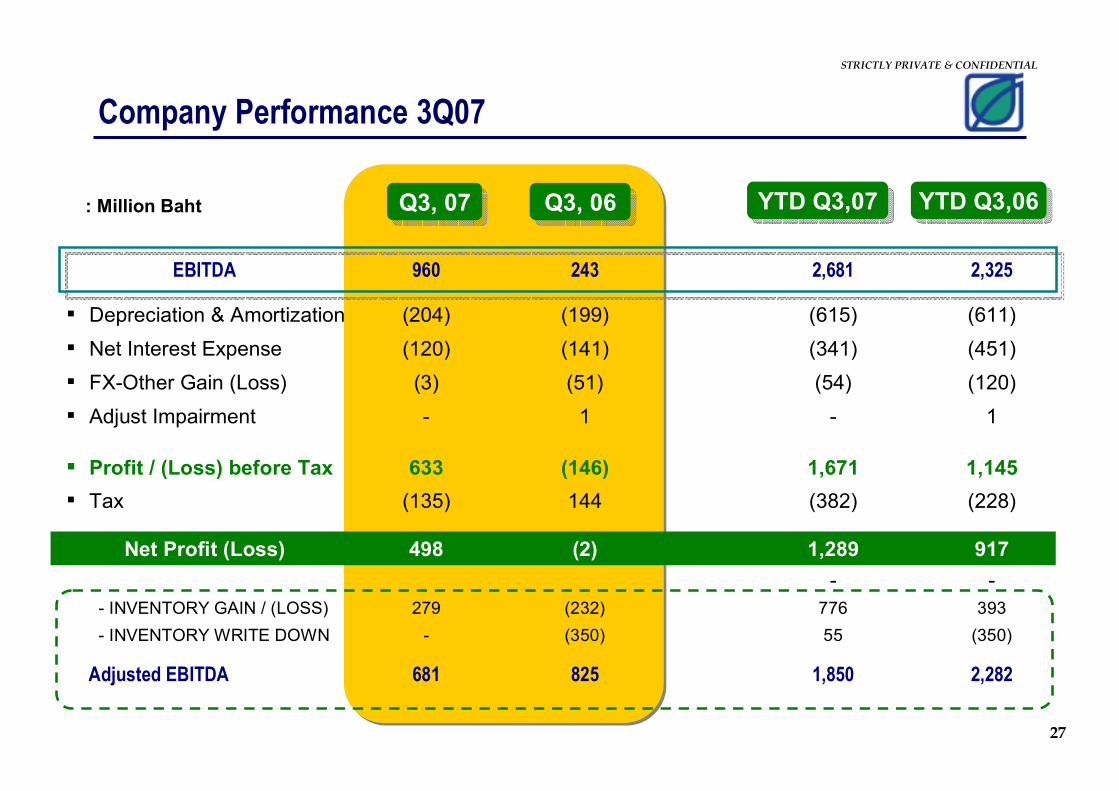

Company Performance 3Q07

Q3, 07Q3, 07 Q3, 06Q3, 06 YTD Q3,07YTD Q3,07 YTD Q3,06YTD Q3,06: Million Baht

EBITDA 960 243 2,681 2,325

� Depreciation & Amortization (204) (199) (615) (611)

� Net Interest Expense (120) (141) (341) (451)

� FX-Other Gain (Loss) (3) (51) (54) (120)

� Adjust Impairment - 1 - 1

� � � � Profit / (Loss) before Tax 633 (146) 1,671 1,145

� Tax (135) 144 (382) (228)

Net Profit (Loss) 498 (2) 1,289 917

- -

- INVENTORY GAIN / (LOSS) 279 (232) 776 393

- INVENTORY WRITE DOWN - (350) 55 (350)

Adjusted EBITDA 681 825 1,850 2,282

28

STRICTLY PRIVATE & CONFIDENTIAL

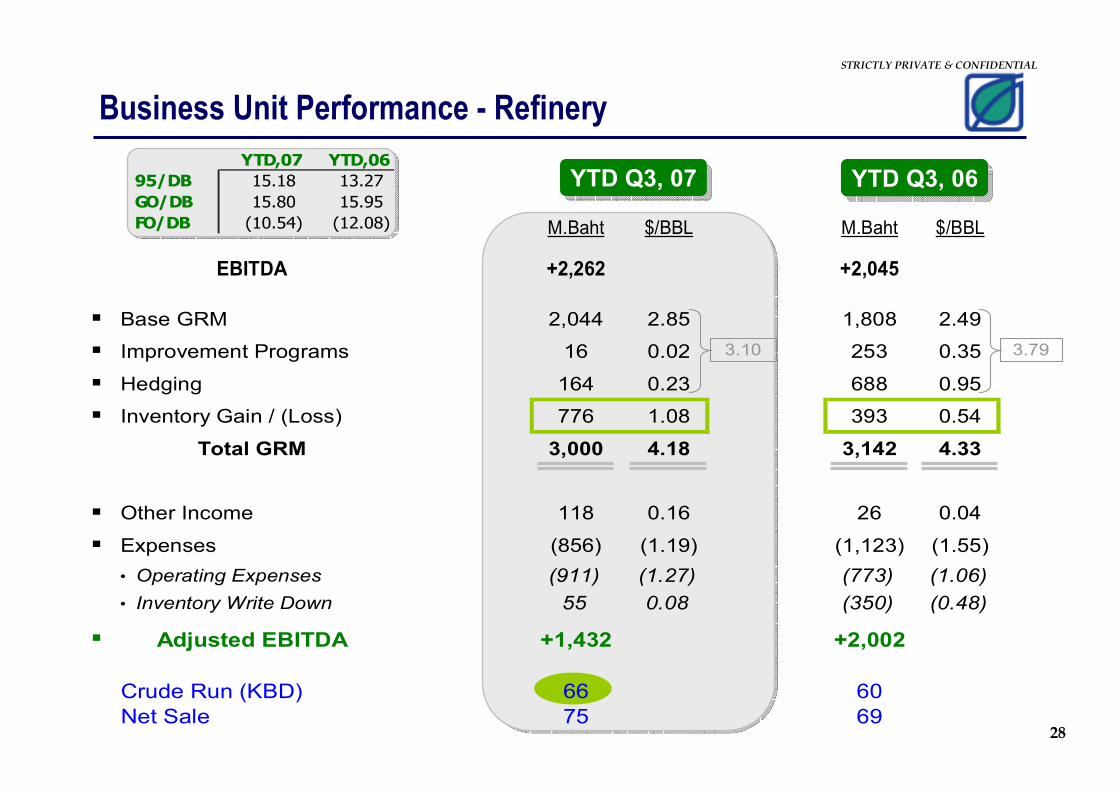

YTD,07 YTD,06

95/DB 15.18 13.27

GO/DB 15.80 15.95

FO/DB (10.54) (12.08)

YTD Q3, 07YTD Q3, 07 YTD Q3, 06YTD Q3, 06

Business Unit Performance - Refinery

M.Baht $/BBL M.Baht $/BBL

EBITDA +2,262 +2,045

� Base GRM 2,044 2.85 1,808 2.49

� Improvement Programs 16 0.02 253 0.35

� Hedging 164 0.23 688 0.95

� Inventory Gain / (Loss) 776 1.08 393 0.54

Total GRM 3,000 4.18 3,142 4.33

� Other Income 118 0.16 26 0.04

� Expenses (856) (1.19) (1,123) (1.55)

• Operating Expenses (911) (1.27) (773) (1.06)

• Inventory Write Down 55 0.08 (350) (0.48)

� Adjusted EBITDA +1,432 +2,002

Crude Run (KBD) 66 60

Net Sale 75 69

3.10 3.79

29

STRICTLY PRIVATE & CONFIDENTIAL

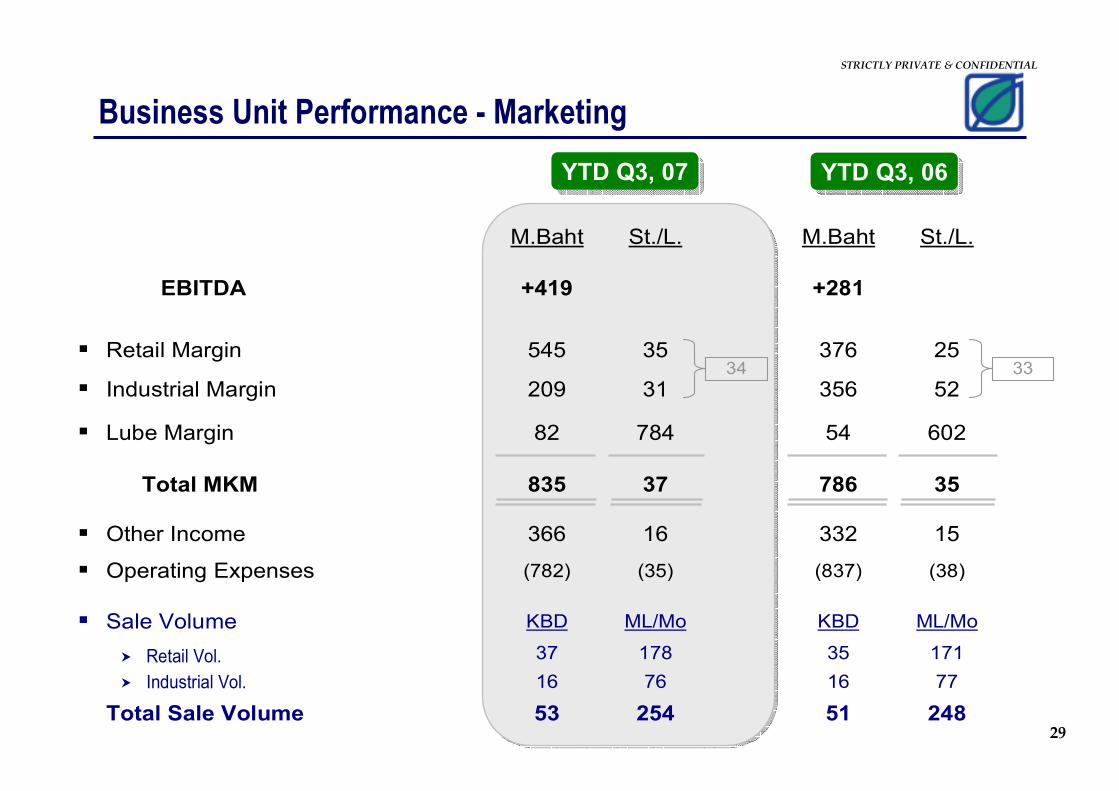

YTD Q3, 07YTD Q3, 07 YTD Q3, 06YTD Q3, 06

Business Unit Performance - Marketing

M.Baht St./L. M.Baht St./L.

EBITDA +419 +281

� Retail Margin 545 35 376 25

� Industrial Margin 209 31 356 52

� Lube Margin 82 784 54 602

Total MKM 835 37 786 35

� Other Income 366 16 332 15

� Operating Expenses (782) (35) (837) (38)

� Sale Volume KBD ML/Mo KBD ML/Mo

� Retail Vol. 37 178 35 171

� Industrial Vol. 16 76 16 77

Total Sale Volume 53 254 51 248

34 33

30

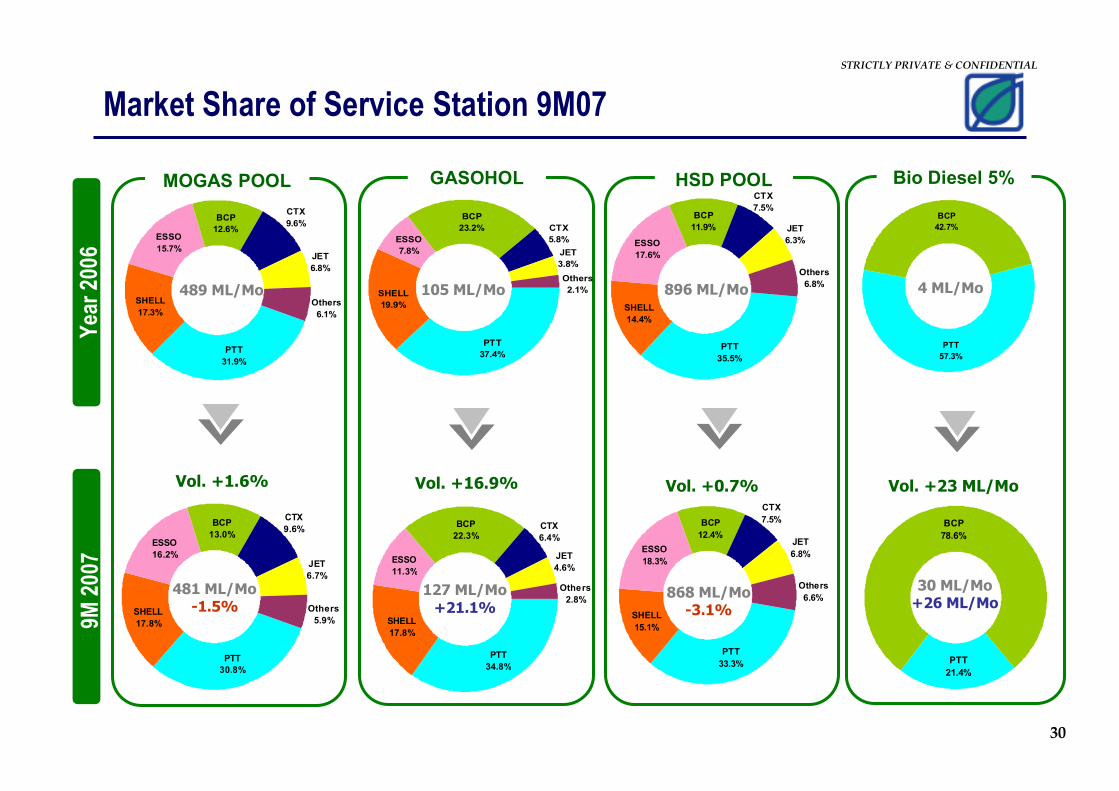

STRICTLY PRIVATE & CONFIDENTIAL

PTT

34.8%

SHELL

17.8%

ESSO

11.3%

BCP

22.3%CTX

6.4%

JET

4.6%

Others

2.8%

GASOHOLMOGAS POOL HSD POOL Bio Diesel 5%

Year 2006

9M 2007

481 ML/Mo-1.5%

127 ML/Mo

+21.1%868 ML/Mo-3.1%

30 ML/Mo+26 ML/Mo

PTT

31.9%

SHELL

17.3%

ESSO

15.7%

BCP

12.6%

Others

6.1%

JET

6.8%

CTX

9.6%

PTT

37.4%

SHELL

19.9%

ESSO

7.8%

BCP

23.2% CTX

5.8%

JET

3.8%

Others

2.1%

PTT

35.5%

SHELL

14.4%

ESSO

17.6%

BCP

11.9%

CTX

7.5%

JET

6.3%

Others

6.8%

PTT

57.3%

BCP

42.7%

489 ML/Mo 105 ML/Mo 896 ML/Mo 4 ML/Mo

Vol. +16.9%Vol. +1.6% Vol. +0.7% Vol. +23 ML/Mo

Market Share of Service Station 9M07

PTT

30.8%

SHELL

17.8%

ESSO

16.2%

BCP

13.0%

Others

5.9%

JET

6.7%

CTX

9.6%

PTT

33.3%

SHELL

15.1%

ESSO

18.3%

BCP

12.4%

CTX

7.5%

JET

6.8%

Others

6.6%

PTT

21.4%

BCP

78.6%

31

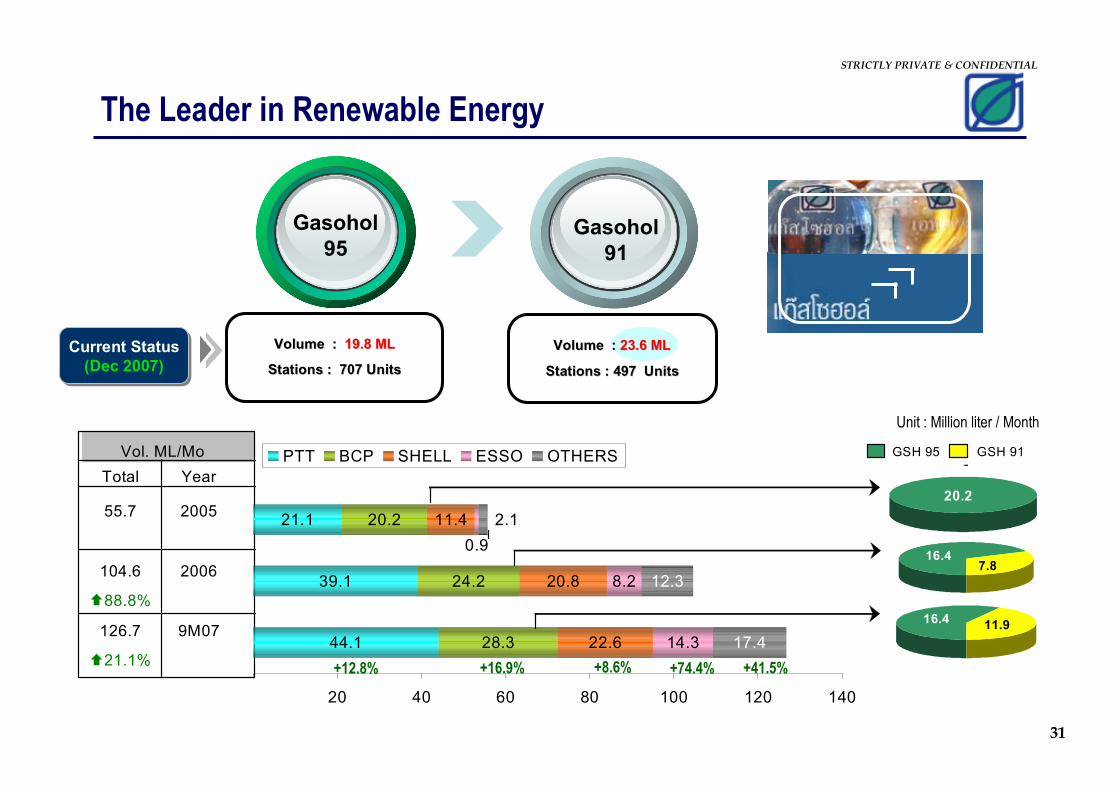

STRICTLY PRIVATE & CONFIDENTIAL

Vol. ML/Mo GSH 95 GSH 91

Total Year PTT BCP SHELL ESSO OTHERS

55.7 2005

104.6 2006

�88.8%

126.7 9M07

�21.1%44.1

39.1

21.1

28.3

24.2

20.2

22.6

20.8

11.4

14.3

8.2

17.4

12.3

0.9

2.1

- 20 40 60 80 100 120 140

PTT BCP SHELL ESSO OTHERS-

20.2

16.4 7.8

11.9 16.4

Gasohol

95Gasohol

91

Current Status

(Dec 2007)

Current Status

(Dec 2007)

Volume : Volume : 19.819.8 MLML

Stations : 707 UnitsStations : 707 Units

Volume : Volume : 23.6 ML23.6 ML

Stations : 497 UnitsStations : 497 Units

+12.8% +16.9% +8.6% +74.4% +41.5%

The Leader in Renewable Energy

Unit : Million liter / Month

32

STRICTLY PRIVATE & CONFIDENTIAL

-

5.00

10.00

15.00

20.00

25.00

30.00

35.00

Ja

n-0

6

Fe

b-0

6

Ma

r-0

6

Ap

r-0

6

Ma

y-0

6

Ju

n-0

6

Ju

l-0

6

Au

g-0

6

Se

p-0

6

Oct-

06

No

v-0

6

De

c-0

6

Ja

n-0

7

Fe

b-0

7

Ma

r-0

7

Ap

r-0

7

Ma

y-0

7

Ju

n-0

7

Ju

l-0

7

Au

g-0

7

Se

p-0

7

Oct-

07

No

v-0

7

De

c-0

7

-

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

Vol U91 Vol GSH91 Price GSH91 Price U91

The Leader in Renewable Energy

Baht / Liter

(Line)Million liter / Month

(Bar)

“Since the government had the policy to increase price gap, we got success in promotion of gasohol91“

33

STRICTLY PRIVATE & CONFIDENTIAL

Rewards

2nd Consecutive Time

“Board of the Year for Exemplary

Practices”

2006/2007

December 11, 2007

2nd Consecutive Time

“Board of the Year for Exemplary

Practices”

2006/2007

December 11, 2007

34

STRICTLY PRIVATE & CONFIDENTIAL

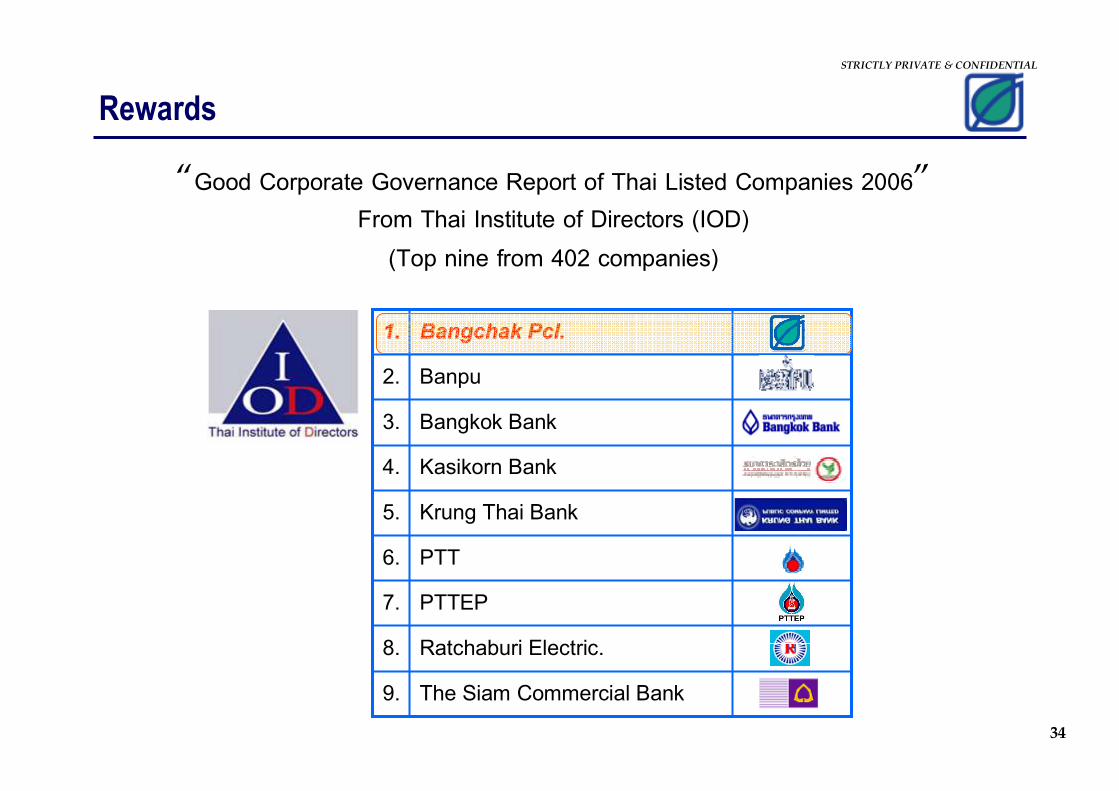

Rewards

“Good Corporate Governance Report of Thai Listed Companies 2006”

From Thai Institute of Directors (IOD)

(Top nine from 402 companies)

“Good Corporate Governance Report of Thai Listed Companies 2006”

From Thai Institute of Directors (IOD)

(Top nine from 402 companies)

The Siam Commercial Bank9.

Ratchaburi Electric.8.

PTTEP7.

PTT6.

Krung Thai Bank5.

Kasikorn Bank4.

Bangkok Bank3.

Banpu2.

Bangchak Bangchak PclPcl..1.1.

35

STRICTLY PRIVATE & CONFIDENTIAL

Rewards

2nd Year

“Best Corporate Governance Report”

in SET AWARDS 2006

July 26, 2006

2nd Year

“Best Corporate Governance Report”

in SET AWARDS 2006

July 26, 2006

“Best Corporate Social Responsibility”

in SET AWARDS 2006

July 26, 2006

“Best Corporate Social Responsibility”

in SET AWARDS 2006

July 26, 2006

SET AWARDS 2007 IS SKIPED TO Y2008

Contact • [email protected] or

[email protected] Tel. 02-335-4583

Website • www.bangchak.co.th click Investor Relation

Thank YouThank You