the bangchak petroleum plc · japan portfolio (19.5 mwac) biofuel business –increased capacity...

TRANSCRIPT

Opportunity Day - 3Q2016

November 15, 2016

The Bangchak Petroleum PLC

AGENDA

2

1 Performance Summary

2 Financial Performance Update

4 Investment Update

3 Oil Market Outlook

AGENDA

3

1 Performance Summary

2 Financial Performance Update

4 Investment Update

3 Oil Market Outlook

BCP Group Performance

4The Bangchak Petroleum Plc

Q3/16 Performance Snapshots

9M/16

EBITDA PerformanceUnit: THB Million

Refinery• Consistent high level of crude run • Softer market GRM

Marketing• Maintain 2nd market share• 11% retail sales volume growth (Jan-Sep 16/15) • Satisfied marketing margin

Green Power Plant• BCPG listing on schedule• COD 8.8 MWac of solar power business in Japan

Biofuel• COD of Biodiesel Plant 2 and Ethanol Plant (BBE)• Affected by the government reduced the portion

of B100 mixing with diesel from 7% to 3%

E&P• Galoc oil field recorded an Uptime of 99.3%• Cost reduction continue

4

Refinery51%

Marketing20%

Solar Power21%

Biofuel-2%

E&P6%

EBITDA

2,798THB Million

Q3/16

Refinery42%

Marketing31%

Solar Power22%

Biofuel2%

E&P3%

EBITDA

8,076THB Million

Q3/15 Q2/16 Q3/16

Accounting Operating

EBITDA Performance - BCP Group

5The Bangchak Petroleum Plc

Unit: THB Million

EBITDA Performance

28% YoY

-32% QoQ

Accounting EBITDA

-21% YoY

-10% QoQ

Operating EBITDA2,184

3,5674,085

3,143 2,798 2,833

Refinery Marketing Solar Power Biofuel E&P

Q3/16 EBITDA Performance Compare to Target by Business Unit

Target

1,503MB

607MB

612MB

-65MB

171MB

5

2,833

2,798

0 1,000 2,000 3,000 4,000 5,000

Operating

Accounting

Target3,700

Unit: THB Million

EBITDA Performance - BCP Group

0%

50%

100%

150%

200%

0.5 1.5 2.5 3.5 4.5 5.5

Solar Power1,765

Marketing2,531

Refinery3,389

Biofuel195 E&P

252

9M/16 Performance Compare to Target by Business Unit

Accounting EBITDA 8,076 Million Baht

Unit: THB Million

Target100%

6The Bangchak Petroleum Plc 6

BCP Group Portfolios

7The Bangchak Petroleum Plc

Green Power Plant Biofuel E&PRefinery Marketing

7

Refinery Performance: Smooth Operation

8The Bangchak Petroleum Plc

Q3/15 Q2/16 Q3/16

Domestic Import

16% 13% 12%1%

53% 53% 55%

10% 11% 11%

19% 20% 19%

2% 2% 3%

Q3/15 Q2/16 Q3/16

Crude SourcingUnit: KBD

Product YieldUnit: %

LPG

Gasoline

Jet

Diesel

Fuel OilUCO

117 112 115

59%

41%

65%

35%

52%

48%

100 96 101 101 98

48

97 102109 112 117 114

64

112 116

83% 80% 84% 84% 82%

40%

81%85%

91% 93% 97% 95%

53%

93% 96%

0%

20%

40%

60%

80%

100%

0102030405060708090

100110120130140

Q1/13 Q2/13 Q3/13 Q4/13 Q1/14 Q2/14 Q3/14 Q4/14 Q1/15 Q2/15 Q3/15 Q4/15 Q1/16 Q2/16 Q3/16

Crude Run UtilizationRefinery Crude RunUnit: KBD

TAMTAM

8

Refinery Performance

9The Bangchak Petroleum Plc

0

2

4

0

20

40

60

80

100

Q3/15 Q4 Q1/16 Q2 Q3

DB DTD/DB

Crude Price & Crack Spreads ($/BBL)

-10

-5

0

5

10

15

20

Q3/15 Q4 Q1/16 Q2 Q3

GO/DB

UNL95/DB

FO/DB

7.906.27 5.62

-0.12

0.010.03

-3.72

2.510.32

Q3/15 Q2/16 Q3/16

Inventory Gain Loss

Hedging

Market GRM

Accounting GRM 4.07 8.79 5.97

GRM Performance

Q3/16: Market GRM softer than previous quarter

Refinery utilization increased lead to higher value product yield

FO/DB spread was improved while UNL95/DB were weak

Crude cost spread Dated Brent and Dubai (DTD/DB) widening QoQ

An inventory gain of THB 120 Million

764

2,531

1,503

2,103

1,6261,384

Q3/15 Q2/16 Q3/16

Accounting

Operating

Refinery EBITDAUnit: $/BBL

Unit: THB Million

9

0

200

400

600

800

1,000Retail Market

Industrial Market

Export

Wholesales

Distribution channel: Retail market is our main priority

10

Refined Petroleum Products: % Portion of total sales volume Q3/2016

Marketing Business

RetailMarket

IndustrialMarket

Wholesales

Export

46%

27%

14%

13%

Q3/15 = 45%, Q2/16 = 48% Q3/15 = 26%, Q2/16 = 28% Q3/15 = 9%, Q2/16 = 14% Q3/15 = 19%, Q2/16 = 12%

Unit: Million Litre

Total Sales Volume

670706

754777

851879

921

Distribution channel: Retail market is our main priority

11The Bangchak Petroleum Plc

803 921 879

469 529 503

Q3/15 Q2/16 Q3/16

Marketing Sales VolumeUnit: Million Litre

1,2721,450 1,382

Industrial Market+7% YoY-5% QoQ

Retail Market+9% YoY-5% QoQ

551

882

607574

858

609

Q3/15 Q2/16 Q3/16

Accounting

Operating

Marketing EBITDA

Unit: THB Million

11

0.97 1.09 1.04

0.24 0.50 0.38

Q3/15 Q2/16 Q3/16

Net Retail Margin Net Industrial Margin

0.70

0.870.80

Net Marketing MarginUnit: Baht/Litre

Retail & Industrial sales volume reduced by

seasonal factor

Retail Margin maintained its level

Industrial Margin dropped from seasonal factor

and excess supply in the market

Q3/16: Seasonal Effected

0

50

100

150

200

250

300

100

200

300

400

500

600

700

12

Marketing NetworkIncrease Thruput per S/S by Network Expansion

BCP - BGN S/S

Major M7 Oil excl. BCP

433

Unit: K.Litre/Station/ Month

Thruput per station

595

554

463

180

200

220

240

260

280

300

320

340

JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC

FY2012

FY2013

FY2014

FY2015

FY2016

+11% Average YoY Growth Unit: Million Litre/ Month

Retail Sales VolumeY2015 Jan-Sep 16 ∆

37.1% 37.0%

15.0% 15.0%

13.6% 12.9%

13.0% 12.9%

6.0% 5.7%

5.2% 5.0%

1.5% 1.8%

6.9% 7.9%

1.6% 1.6%

Market Share (Retail Channel)

BCP - Co-Op Type

BCP – Dealer Type

Standard TypeSmall Type

Minor M7 Oil

146

114

R&M PerformanceRefinery and Marketing business are the main source of overall earnings

13

8.345.88 6.96

9.055.80

3.31

2.683.47

3.53

3.90

2012 2013 2014 2015 9M2016

Net MKM

Market GRM

Unit: $/BBL

Normalize Integrated Margin

11.66 8.56 10.43 12.58 9.70

7,026 6,579 7,167

12,838

5,471

2,973 2,6083,562

4,134

3,731

2012 2013 2014 2015 9M2016

Unit: THB Million

R&M being fully integrated model, the profit can be optimized through business cycle

Refinery Business earning was volatile due to market conditions and Turnaround maintenance (TAM)

Marketing Business Captures a Demand Surge During Low Oil Price Environment

Net MKM

Market GRM

BCP Group Portfolios

14

Green Power Plant Biofuel E&PRefinery Marketing

3.7

7

7.7

1

3.4

4

8.0

7

Q2/16 Q3/16

Target2 Actual3

55.6

5

65.3

5

60.6

5

63

.88

65

.03

61

.01

Q3/15 Q2/16 Q3/16

Target Actual

Green Power Plant – New commercial operated plant in Japan

15

Thailand Portfolio (118 MWac)

Electricity Sales by Country (Unit: Million kWh)

Revenue from Electricity Sales (Unit: THB Million)

Steady steam of cash flow

Thailand: Lower Electricity Sales due to the

rainy season

Japan: Higher Electricity Sales during summer

time & additional COD of 8.8 MW PPA

692

525612

Q3/15 Q2/16 Q3/16

Accounting

Green Power EBITDAUnit: THB Million

731 716 680

43 105

Q3/15 Q2/16 Q3/16

TH JP

Japan Portfolio (19.5 MWac)

Biofuel Business – Increased capacity from new biodiesel plant

16

366 387452

568

741

478

Q3/15 Q2/16 Q3/16

Daily Production Sales Volume

Capacity expanded from 2nd Biodiesel plant’s COD

Lower demand of Biodiesel (government’s policy of decreasing

the portion of B100 mixing with diesel from 7% in to 3%)

Biodiesel plants recorded a 56% utilization rate, current

capacity increased to 810 K. Litre / day

Short term CPO & B100 price fluctuation hence to an

inventory loss

Biodiesel Plant: Daily Production and Sales Volume

Unit: K. Litre per day

62

113

-65

83101 89

Q3/15 Q2/16 Q3/16

Accounting

Operating

Biofuel EBITDAUnit: THB Million

B7 to B5 in July B5 to B3 in Aug

28

30

32

34

36

38

40

42

CPO Price B100 Price

(Baht / Kg.) (Baht / Litre)

Average Monthly CPO and B100 product price

Source: Department of Energy Business, Ministry of Energy

E&P Business – Self Revision, Survival Plan Cutting Down Costs

17

6.115.12 5.08

3.412.86 2.84

Q3/15 Q2/16 Q3/16

Gross Production Net to NIDO

Production (Unit: KBD)

Q3/15 Q2/16 Q3/16

Volumes lifted and Sold*

(bbls)201,003 393,375 196,474

Cargo 1 Cargo 2 Cargoes 1 Cargo

All prices are on FOB

realized basis

($/BBL)

Cargo 47

49.84

Cargo 51

40.53

Cargo 53

45.46

Cargo 52

48.15

49.9943.23 43.19

49.84 44.34 45.46

Q3/15 Q2/16 Q3/16

Dubai Nido

Comparing Nido Selling Price to Dubai benchmark priceUnit: $/BBL

Note: The cargo#52 sold in June was subject to the DES (Delivery Ex Ship) condition, Nido realized the revenue in July 2016

Implement cost cutting plan

Galoc oil filed uptime was 99.3%

Cost saving plan still implemented

Use derivatives to hedge against crude oil price volatility

156

59

171

Q3/15 Q2/16 Q3/16

AccountingE&P EBITDAUnit: THB Million

AGENDA

18

1 Performance Summary

2 Financial Performance Update

4 Investment Update

3 Oil Market Outlook

19

Quarterly Remark – From Financial Aspects

Q3/16 Remarks

BCP

o Long-term loan from financial institution repayment of the company and BCPG Plc. of THB 4,309 million.

o Dividend payment for Shareholders of the Company at 0.80 per share, totaling THB 1,101.54 million.

o The capital increase of Bangchak Bioethanol (Chachoengsao) Co., Ltd. of THB 425 million.

o The capital increase of Bangchak Retail Co., Ltd. of THB 800 million.

o The capital increase of Bongkot Marine service of THB 300,000.

o Paid up share capital of BCP Trading Pte. Ltd. of USD 1 million.

BCPG

o The newly issued ordinary shares of 590 million shares is listed in the Stock Exchange of Thailand,

the company’s shareholding portion in BCPG Plc. was reduced to 70.35%

o BCPG Plc. received cash from selling of equity of Baht 5,711 million.

BCP Energy International Pte.

o Increase of registered share capital from USD 91.31 million to USD 111.41 million for appraisal wells program in the Mid-Galoc area of Galoc oil field in Philippines

Established Oam Suk social Enterprise Co.,Ltd.

o BCP holds 40% in joint venture with Buddhist Economic Foundation, initial registered capital of THB 10 Million

20

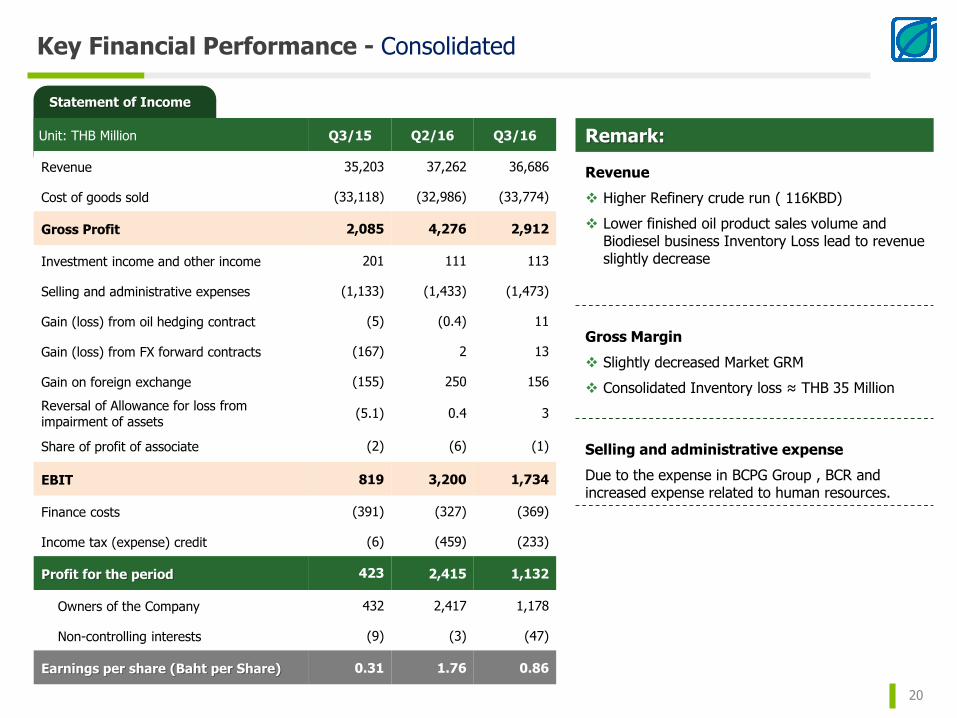

Key Financial Performance - Consolidated

Statement of Income

Unit: THB Million Q3/15 Q2/16 Q3/16

Revenue 35,203 37,262 36,686

Cost of goods sold (33,118) (32,986) (33,774)

Gross Profit 2,085 4,276 2,912

Investment income and other income 201 111 113

Selling and administrative expenses (1,133) (1,433) (1,473)

Gain (loss) from oil hedging contract (5) (0.4) 11

Gain (loss) from FX forward contracts (167) 2 13

Gain on foreign exchange (155) 250 156

Reversal of Allowance for loss from impairment of assets

(5.1) 0.4 3

Share of profit of associate (2) (6) (1)

EBIT 819 3,200 1,734

Finance costs (391) (327) (369)

Income tax (expense) credit (6) (459) (233)

Profit for the period 423 2,415 1,132

Owners of the Company 432 2,417 1,178

Non-controlling interests (9) (3) (47)

Earnings per share (Baht per Share) 0.31 1.76 0.86

Remark:

Revenue

Higher Refinery crude run ( 116KBD)

Lower finished oil product sales volume and Biodiesel business Inventory Loss lead to revenue slightly decrease

Gross Margin

Slightly decreased Market GRM

Consolidated Inventory loss ≈ THB 35 Million

Selling and administrative expense

Due to the expense in BCPG Group , BCR and increased expense related to human resources.

21

BCP Group Performance - Consolidated

Q3/2016 BCP BGN BBF BCPG BCR BBE BCPE BCPI BCPT NIDO Total

% of Share holding 100% 70% 70.35% 100% 85% 100% 100% 100% 81.41%

Revenue 34,506 7,430 1,553 785 0.3 - - 644

Net Profit 949 27 (108) 365 (25) (8) (0.1) - (0.2) (70) 1,128

UBE - Share of profit of investments in associates (2)

Eliminations 6

Net Profit for the period 1,132

Profit (loss) attributable to:

Owner of the company 1,178

Non-controlling interests (46)

Unit: THB Million

22

BCP Group Performance - Consolidated

9M/2016 BCP BGN BBF BCPG BCR BBE BCPE BCPI BCPT NIDO Total

% of Share holding 100% 70% 70.35% 100% 85% 100% 100% 100% 81.41%

Revenue 98,281 21,555 5,641 2,327 0.3 - - 1,176

Net Profit 2,716 90 110 1,214 (55) (8.0) (0.3) 2 (0.2) (423) 3,646

UBE - Share of profit of investments in associates 5

NIDO - Adjust loss from impairment of assets (399)

Eliminations 269

Net Profit for the period 3,521

Profit (loss) attributable to:

Owner of the company 3,642

Non-controlling interests (121)

Unit: THB Million

23

Key Financial Performance - Consolidated

EBITDA Structure of the Company and its subsidiaries

Q3/15 Q2/16 Q3/16 YoY QoQ

Total Revenue 35,203 37,262 36,686 4% -2%

Total EBITDA 2,184 4,085 2,798 28% -32%

EBITDA Refinery 764 2,531 1,503 97% -41%

EBITDA Marketing 1/ 551 882 607 10% -31%

EBITDA Solar Power 2/ 692 525 612 -12% 17%

EBITDA Biofuel 3/ 62 113 (65) -204% -157%

EBITDA Exploration and Production 4/ 156 59 171 10% 191%

EBITDA Others 5/ (41) (25) (31) 25% -23%

Profit attributable to

owners of the Company432 2,417 1,178 173% -51%

Earnings per share (Baht) 0.31 1.76 0.86 177% -51%

1/ EBITDA from Marketing Business, Bangchak Greenet Co.,Ltd, and Bangchak Retail Co.,Ltd2/ EBITDA from Solar Power Plant Business, BCPG Co.,Ltd. and its subsidiaries3/ EBITDA from Bangchak Biofuel Co., Ltd. and share of profit/ (loss) from Ubon Bio Ethanol Co, Ltd4/ EBITDA from Nido Petroleum Limited 5/ EBITDA from BCP Energy International Pte, Ltd. and others

24

Key Financial Position - Consolidated

Assets:

Cash & Equivalents increased by 11,222 MB mainly from cash from operation of 8,203 MB

Inventory decreased by 1,329 MB mainly from lower volume of finished products from 3.25 to 2.11 MBBL

PP&E increased by 4,445 MB from refinery machinery and equipment, acquisition of solar power plant and biodiesel plant.

Other Non Current assets increased mainly from goodwill & license of BCPG Japan and fair value measurements for investment in Lithium Americas Corp.

Liabilities & Equity:

Current Liabilities increased mainly from

Account Payable increased by 1,592 MB from the value of crude oil purchase in Sep 2016 higher than in Dec 2015, and from the finished oil products import of Bath 400 million.

Long-term debt increased by 5,298 MB

BCP loans decreased from repayment and prepayment

Subsidiary’s long-term loans increased from BBF, BBE and BCPG

Equities mainly increased from Net Profit 3,642 MB and decreased by 2,478 from dividend payment

Unit: THB Million

40,044 44,489

8,09910,387

13,94512,616

11,9839,717

7,87219,094

Cash and Equivalents

Current Assets

Inventory

PP&E

Non Current Assets

81,942

96,303

Assets

31 Dec 15 30 Sep 16

35,983 43,066

2,8383,385

33,658

38,956

9,462

10,89681,942

96,303

Liabilities & Equity

31 Dec 15 30 Sep 16

Current Liabilities

Long Term Debt

Total Equity

Non Current Liabilities

(Including current portion of L/T debt)

25

Cash Flow - Consolidated

Beginning Cash7,872 MB

Change in Cash11,255 MB

Ending Cash19,094 MB

FX adjustment(33 MB) 7,821

1,022

839

4,309

14,584

7,888

3,499

2,523

254

Cash From Operation(CFO)

Funding

Others

26,997

Sources of Cash Used of CashDebt Service

15,742

Asset PurchaseAcquisition

Cash Received from maturity of short-term investment

9M/2016 Sources and Uses of CashUnit: THB Million

Dividend Paid

Prepayment

Change in Working Cap

0.54 0.59 0.55 0.52 0.45

Q3/15 Q4/15 Q1/16 Q2/16 Q3/16

Net IBD/E Ratio (Times)

11,98131%

6,94018%

4,04910%

15,98641%

Baht LoanBaht Bond

USD Loan

38,956 THB Million

(as of Sep 30, 2016)

Long-Term Debt Portion

JPY Loan

Asset Purchase / Acquisition

PP&E refinery machinery and

equipment(BCP) 3,243 MB, BCR 24 MB

Biodiesel plant(BBF,BBE) 1,413 MB

Acquisition of solar power business

1,537 MB

leasehold right 371 MB

Intangible assets and Others 358 MB

Other

Mainly from Cash for selling Equity 5,770 MB (BCPG)

AGENDA

26

1 Performance Summary

2 Financial Performance Update

4 Investment Update

3 Oil Market Outlook

Oil Balance seen tighten in 2017

27

• In the fourth quarter of 2016, winter supply/demand fundamentals together with new OPEC policy should push price into a $50-$55 /BBL bythe end of this year.

• Supply creation will become the market’s focus in 2017 and this will require higher oil prices.

57.60 56.60 57.00

6.80 6.90 7.00

32.10

95.10 96.30 97.50

0

10

20

30

40

50

60

70

80

90

100

2015 2016 2017

MB

D

Global Oil Balance 2015 - 2017

Non-OPEC Supply OPEC(NGLs) OPEC Production Total Demand

Call on OPEC

33.50 MBD

Call on OPEC 32.80 MBD

Tighten supply if OPEC policy reducing production to 32.5-33.0 MBD

Actual OPEC ProductionJan-Oct’16: 33.075 MBD

Crude Oil Prices Outlook

28

Q4: OPEC decision is an important bullish development for oil prices

2017: Surplus stock will continue to decline lead to higher oil prices

0

20

40

60

80

Jan-15 Apr-15 Jul-15 Oct-15 Jan-16 Apr-16 Jul-16 Oct-16 Jan-17 Apr-17 Jul-17 Oct-17

$/BBL

Iran nuclear deal reached

Greece Debt Default U.S.

Presidential election

Stronger winter demand / La Niña?

Rig count drop

Upstream investment cut

China’s stock rout

No OPEC production ceiling agreement

Iran’s sanction lifted

Possible of OPEC and Non-OPEC

coordination

FED rate hike

Dubai AVG: Q1/16 = 30.42 Q2/16 = 43.19 Q3/16 = 43.16 Q4/16 (F) = 47.5FY2015 = 50.8 $/BBL FY2016 (F) = 41.06 $/BBL FY2017 (F) = 53.00 $/BBL

Hurricane Season

Q4-16

• New OPEC’s policy to cut oil production.

• Higher oil demand during winter.

• Refineries return from maintenance.

• Fed rate hike Expectation in Dec.

• Chinese economic slowdown.

2017

• Stronger world Economic.

• China buying for SPR filling.

• Weak Chinese economy.

• Some U.S. shale production return.

• Higher non-OPEC supplies.

OPEC talks

Fed Rate Hike Expectation

Significant global inventories decrease

Shale oil production recovery

Effects from Trump win on oil industry

• Opposed Iran sanctions oil supply issue.

• Support U.S. upstream and open federal land and water for fossil exploration.

• Support to coal industry return.

• Emerge from international trade leads to U.S. oil demand growth.

Higher Refinery Product Margins in Q4-16 on Middle Distillate cracks Supports

29

Singapore Product Cracks Spread Outlook

Market Highlights in Q4-16:

• Seasonally softer gasoline demand in Q4 but the Colonial pipeline shutdown, refinery maintenance in Asia (Oct) and ME (Nov) support gasoline cracks.

• Improving gasoil cracks due to seasonally stronger demand.

• Higher demand and tight supply remain support fuel oil cracks.

• Asian CDU capacity additions will rebound in 2017 but some delay is likely.

• Continuation of relative light end support compared to middle distillates on still strong demand.

• Bunker demand slowdown following oil prices rise although fuel oil supply decrease on export tax hike and refinery upgrade in Russia.

Factors to watch 2017:

15.4

19.8 19.4 18.7 18.8

14.411.6

14.0

18.3

14.714.1

16.3

13.710.8

13.7

9.7 10.5 10.913.0 13.6

11.012.5

-1.9-3.5

-8.1-6.6 -5.2

-8.7

-4.3 -4.0-5.0 -5.6 -6.0

-15

-10

-5

0

5

10

15

20

25

Q1-15 Q2-15 Q3-15 Q4-15 Q1-16 Q2-16 Q3-16 Q4-16 2015 2016 2017

ULG95 - Dubai

Gas oil 0.05%S - Dubai

Fuel Oil - Dubai

$/BBL

AGENDA

30

1 Performance Summary

2 Financial Performance Update

4 Investment Update

3 Oil Market Outlook

New Co-Gen Power Plant

3E Project – Project Progress

31

Y2016 Y2017 Y2018 Y2019 Y2020

Completion

Project Timeline

New Co-Gen Power Plant (≈12 MW)

Under Construction

Continuous Catalyst Regeneration Unit (CCR)

(Extend Maintenance Cycle)

FEED&ITB Preparation for Enlarge Capacity

Debottlenecking

(For light end products)

Basic Design Preparation

Completion EPC Award

Completion EPC AwardNPU and ISOU

Boiler Stack/ Structure HRSGOverall Site

Progress: 86%

Oam Suk Social Enterprise Company Limited

32

Oam Suk Social Enterprise

Company Limited

Buddhist Economic

Foundation

40%holds

60%holds

Resources Business

33

E&P

Increase of registered share capital from USD 91.31 million to USD 111.41 million for appraisal wells program in the Mid-Galoc area (GMA) of Galoc oil field in Philippines

Nido’s budgeted participating interest share of well costs is estimated to be A$24.0 million (US$18.5 million)

2P – 4.1MMstb2C – 7.4MMstb

Galoc Reserves & Resources1/

1/Reserves estimates as at 31 December 2015 and Contingent Resources estimates as at 1 August 2016

If successfully developed:

Production & Cost Saving

expected to start production in 2019

would save Galoc total cost by 30%

Optimal timing

• Enough time window for GMA to be developed before decommissioning of Galoc Field and related infrastructure

• Lower global oil price reduced drilling & developing cost by almost 50%

Bangchak Service Station - Greenovative Experience

34

“New paradigm shift to be Customer Centric”

o Introduced new service stations design

o Expanded new potential service stations

New Service Station Design

35

Greenovative Experience

Developed Non oil one roof concept

New Chapter of Bangchak Retail Non-Oil Business

36

37

Disclaimer : The information contained herein is being furnished on a confidential basis for discussion purposes only and only for the use of the

recipient, and may be subject to completion or amendment through the delivery of additional documentation. Except as otherwise provided

herein, this document does not constitute an offer to sell or purchase any security or engage in any transaction. The information contained herein

has been obtained from sources that The Bangchak Petroleum Public Company Limited (“BCP”) considers to be reliable; however, BCP makes no

representation as to, and accepts no responsibility or liability for, the accuracy or completeness of the information contained herein. Any

projections, valuations and statistical analyses contained herein have been provided to assist the recipient in the evaluation of the matters

described herein; such projections, valuations and analyses may be based on subjective assessments and assumptions and may utilize one among

alternative methodologies that produce differing results; accordingly, such projections, valuations and statistical analyses are not to be viewed as

facts and should not be relied upon as an accurate representation of future events. The recipient should make an independent evaluation and

judgment with respect to the matters contained herein.

Thank You

Q&A