1103-cswm global strategy note

TRANSCRIPT

8/7/2019 1103-CSWM Global Strategy Note

http://slidepdf.com/reader/full/1103-cswm-global-strategy-note 1/6

Drawing in our horns (temporarily)Japan

Ater the shocking news o the past ew days, the world looks on at Japan oering

expressions o sympathy and assistance. It’s too soon to assess the wider economic and

nancial impact o the earthquake, but that doesn’t stop markets already adjusting to

discount the news. In the absence o data we can only make the inevitable comparisons

with the 1995 Kobe earthquake, and inside we draw the ollowing conclusions. First,

the loss o industrial output is likely to be relatively small and temporary, second the

Yen is likely to temporarily appreciate, and nally the stock market may already have

discounted most o the bad news.

Middle East and North Arica (MENA)

Although the protagonist nations contribute little to global growth they do control

signicant amounts o the world’s oil supply. We believe that the market has already

priced in a substantial premium to Brent crude and that current dislocation can be

covered by OPEC spare capacity, but the situation warrants close attention, particularly

contagion in Saudi Arabia and Iran. A urther $25-40 increase in the benchmark price

may squeeze consumption by a magnitude that could derail the global recovery.

Political turmoil could also lead to a generic rise in global equity risk premiums,causing outfows rom risk assets. We see little evidence o this in both developed and

emerging markets.

Strategy conclusions

Bringing all o this together, the natural conclusion can only be that risk premia are

likely to remain elevated a while longer, and may even rise urther. While the economic

risks are abating or developed markets, mid cycle infation and interest rate risks are

becoming more prevalent. Continuing MENA tensions are likely to mean that the oil

price remains elevated, although it’s hard to see oil pressing too much higher without

urther political instability. While risk asset correlations haven’t risen markedly (a usual

precursor to market stress), and while we remain relatively sanguine about the impact

o these events on risk assets longer term, it’s probably not the right time to extend

overweights into equities, or indeed to position too heavily on a correction in the oil

price. We’re drawing in our horns and would recommend temporarily market neutral

positioning, whilst being vigilant to opportunity.

www.collinsstewartwealth.com

Global Strategy15th March 2011

Also inside:

“We would also expect

more tolerance and

support or Japanese

intervention in limiting

short-term appreciation”

“Political turmoil in the Middle

East & North Africa (MENA)

has added volatility to global

markets in early 2011”

For more information contact:

Robert Jukes

Global Strategist

T: +44 (0) 20 7523 4594

Edward Smith

Global Strategist

T: +44 (0) 20 7523 4537

8/7/2019 1103-CSWM Global Strategy Note

http://slidepdf.com/reader/full/1103-cswm-global-strategy-note 2/6

Kobe and Sendai: appreciating the dierence

It’s hard to resist the inevitable comparison o the Sendai earthquake and Tsunami with the 1995 Kobe disaster.

With so little reliable detail available on the ormer, any analysis at this stage really must rely on the latter. In

the months that ollowed the January 1995 earthquake, Japanese industrial production contracted nearly 2%,

with a similar contraction in GDP. O course it would be wrong to attribute all o that to the earthquake, the

developed world was in the midst o a mid cycle slowdown (Figure 1). German industrial output also contracted

5%, or example, but Japan accounts or just 3% o total German exports. Unlike Sendai, Kobe hit the industrial

base hard, but still industrial output recovered within just a ew months. Clearly the most recent tsunami has

been ar more devastating to the nation, but possibly less so to the industrial potential. Appendix 1 maps out the

areas aected.

The reconstruction costs o resulting rom the Kobe earthquake were around $150bn, and Japanese insurance

companies were quick to liquidate oreign assets to meet those liabilities. We have no reason to expect dierent

behaviour this time around, and that is likely to mean more appreciation pressure on the Yen (Figure 2). Againstthe dollar, Yen could break past 80, but longer-term we see urther Yen weakness. Indeed a ew salient dierences

with 1995 mean we should expect less Yen strength: recent BOJ liquidity support worth ¥21tn, increased BOJ

asset purchases, and likely more tolerance and support or Japanese intervention in limiting short-term Yen

appreciation given its current strength.

Using Kobe as a barometer, o the short-term stock market consequences, the Japanese market may also be close

to having discounted last week’s events. In 1995 the Topix ell 8% in the preceding 5 days, to then rally 5% over

the 5 days ater that. It did, however, take nearly a year to recover beyond the pre-earthquake levels, but then the

equity market was clearly over-valued, and producing a relatively low return on equity (gure 4). Indeed the Topix

in 1995 was already in the midst o a correction (Figure 3). Ahead o last week’s events; the equity market was

approaching overbought levels, it’s now already oversold.

Fig 1: Japanese industrial production versus major economies

Fig 3: Topix was over bought ahead o Sendai quake…

Fig 2: Further (temporary) Yen strength likely over the short-term

Fig 4: …but with more attractive valuations and stronger RoE

-20

-15

-10

-5

0

5

10

15

20

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

US

UK

BD

JP

Japanese producion loss circa 2%

-8

-6

-4

-2

0

2

4

6

8

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

circa 20%correction already

8% correction in first 5 days

Overbought/Oversold

+/- 2sd

Current level

90

100

110

120

130

140

150

160

170

180

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

Kobe, resulted in asset repatrication and Yen strength, it seemslikely to use that Sendai will result in much the same kind of reaction - further (temporarary) Yen strength

Japanese Yen, trade weighted

Source: Datastream, Collins Stewart Wealth Management Global Strategy

Global Strategy

15 March 2011

“It’s hard to resistthe inevitable

comparison o the

Sendai earthquake and

Tsunami with the 1995

Kobe disaster”

“Using Kobe as a

barometer, o the

short-term stock

market consequences,

the Japanese market

may also be close to

having discounted last

week’s events”

0

10

20

30

40

50

60

70

80

90

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

-4

-2

0

2

4

6

8

10

12

Overvalued & low RoE

Closer to fair value & high RoE

PE

ROE (inv, rhs)

8/7/2019 1103-CSWM Global Strategy Note

http://slidepdf.com/reader/full/1103-cswm-global-strategy-note 3/6

Middle East & North Arica

Political turmoil in the Middle East & North Arica (MENA) has added volatility to global markets in early 2011.

Although the nations involved account or a very small proportion o global output (see Appendix 2) and make

negligible contributions to global growth (indeed, it is prolonged underinvestment and high unemployment that

has in part precipitated the disquiet), the unrest poses two key risks to investors in the short to medium term.

The primary risk is an intensication o the oil price shock as the supply chain becomes more dislocated. We do

not believe that current oil prices are o a magnitude that could dramatically squeeze global consumption and

derail the recovery. Today’s annual rate o change o Brent crude is just 43% and it usually takes a considerably

aster rise in the price o oil to throw the world into recession (Figure 5). That said, i oil switly rises another

$25-40 we would want to reassess that view. We believe that investors have already built in a very substantial

risk premium into the price o oil. By modelling oil with the trade-weighted dollar (a liquidity proxy) and global

oil consumption alone, any upside deviation rom this ‘air value’ is arguably the market’s assumption about

the uture insuciency o supply. Today’s premium is $25-30 over this model (Figure 6). Moreover, the mostalarming unrest has occurred in countries that produce less than 4% o the world’s oil supply. Beore the supply

disruptions, OPEC spare capacity was 2.5-3m bpd: this would cover supply i Egypt’s, Yemen’s, Libya’s and Tunisia’s

pumps were to be shut o completely.

Secondly, heightened geopolitical tensions could trigger a generic rise in risk premiums, making risk assets less

desirable than they were previously. There is little sign o this in developed markets. The S&P 500 is up on the year

and our market derived ERP has barely moved either (Figure 7). We proxy EM ERP with the earnings yield + long-

run growth orecasts - bond yield, and this measure has resumed only a mild upswing this year (Figure 8). Lastly,

correlations between risk assets have barely trended up, a common precursor to major market events, and a key

input into our CSWM market Stress Indicator which has not had a stressed reading since Q3 2010.

Fig 5: UK money supply depressed

Fig 7: US input versus output prices. Cost push?

Fig 6: Wage growth and labour productivity Vs ination

Fig 8: Producer prices not ully passing through to CPI

1970 1973 1976 1979 1982 1985 1988 1991 1994 1997 2000 2003 2006 2009

-100%

-50%

0%

50%

100%

150%

200%

250% Recession periods

Crude oil price $, yoy %ch (rhs)

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011

Equity Risk premium

Average ERP

+/- 1 standard deviation

0

25

50

75

100

125

150

1994 1996 1998 2000 2002 2004 2006 2008 2010

Brent Oil

Simple model

R2

= 81%

0

2

4

6

810

12

14

16

18

20

22

24

26

19 98 1999 2000 2001 20 02 2003 2 004 2005 2 006 200 7 2 008 200 9 2010 20 11

Emerging market ERP proxy

Source: Datastream, Collins Stewart Wealth Management Global Strategy

Global Strategy

15 March 2011

“Today’s annual rate of

change of Brent crude is

just 43% and it usually

takes a considerably

faster rise in the price of

oil to throw the world

into recession”

8/7/2019 1103-CSWM Global Strategy Note

http://slidepdf.com/reader/full/1103-cswm-global-strategy-note 4/6

Sendai and com

parisons with Kobe

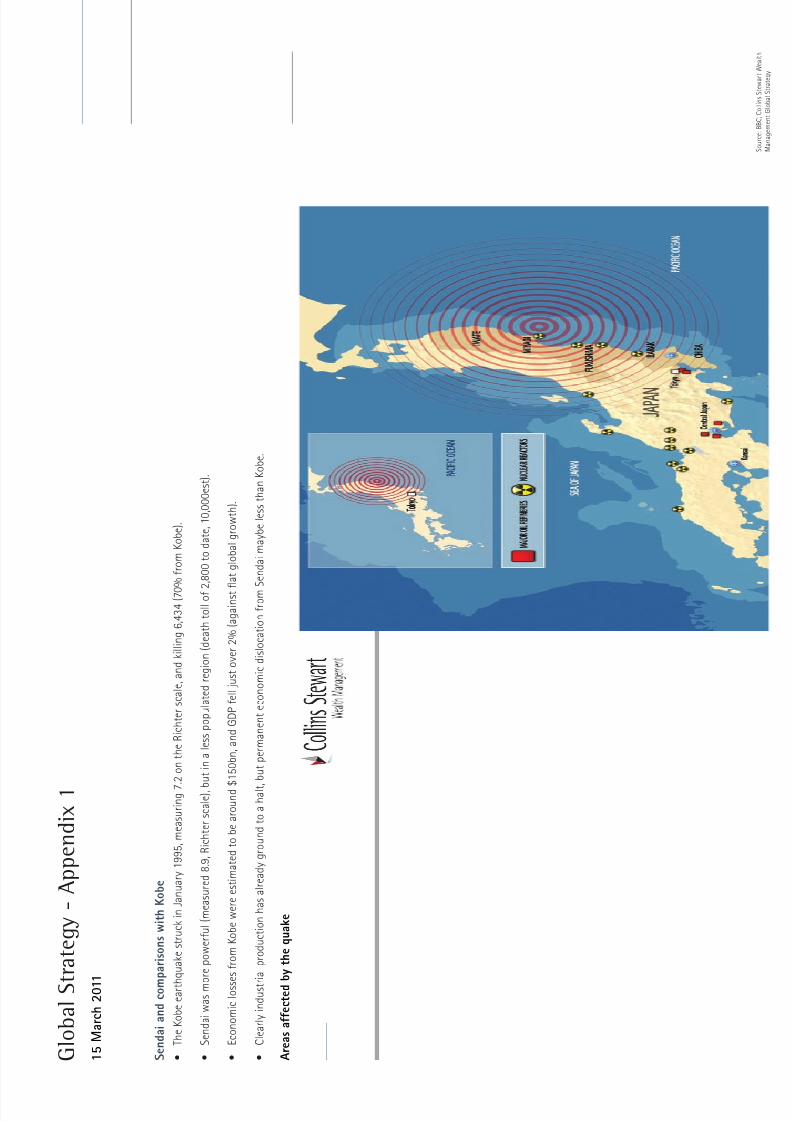

•TheKobeearth

quakestruckinJanuary1995,measuring7.2ontheRichterscale,andkilling6,434(70%fromKobe).

•Sendaiwasmo

repowerful(measured8.9,Richterscale),b

utinalesspopulatedregion(deathtollof2,800todate,10,000est).

•EconomiclossesfromKobewereestimatedtobearound$

150bn,andGDPfelljustover2%(againstatglobalgrowth).

•Clearlyindustrialproductionhasalreadygroundtoahalt,butpermanenteconomicdislocationfromSendaimaybelessthanKobe.

Areas affected by the quake

Global St

rategy - Appendix 1

15 March 2011

Source: BBC, Collins Stewart Wealth

Management Global Strategy

8/7/2019 1103-CSWM Global Strategy Note

http://slidepdf.com/reader/full/1103-cswm-global-strategy-note 5/6

Middle East & N

orth African turmoil I

•ClearlytheseregionsareaverysmallproportionofglobalGDP.

•Neitherdotheycontributetoglobaleconomicgrowth-yearsofunderinvestmentandhighunemployment.

•Themostalarm

ingunresthasoccurredincountriesthatp

roducelessthan4%oftheworld’soilsupp

ly.

•Beforethesup

plydisruptions,OPECsparecapacitywas2.5-3mbpd,coveringsupplyifEgypt,Yemen,LibyaandTunisia’spumpswereshutoffcompletely(highlyunlikely).

MENA unrest – countries affected

Global St

rategy - Appendix 2

15 March 2011

Source: BP, IMF, Collins Stewart Wealth Management Global Strategy

8/7/2019 1103-CSWM Global Strategy Note

http://slidepdf.com/reader/full/1103-cswm-global-strategy-note 6/6

Contact Collins Stewart Wealth Management

Collins Stewart ofces:

France, Guernsey, Ireland, Isle o Man, Jersey, Singapore, Switzerland, UK, USA

London

8th Floor

88 Wood Street

London

EC2V 7QR

T: +44 (0) 20 7523 4600

F: +44 (0) 20 7523 4599

Jersey

38 The Esplanade

St Helier

Jersey

JE4 0XQ

T: +44 (0) 1534 708090

F: +44 (0) 1534 708050

Guernsey

PO Box 45

Collins Stewart House

The Grange

St Peter Port

Guernsey GY1 4AX

T: +44 (0) 1481 712889

F: +44 (0) 1481 713460

Isle o Man

Anglo International House,

Bank Hill

Douglas

Isle o Man

IM1 4LN

T: +44 (0) 1624 690100

F: +44 (0) 1624 690101

Geneva

7, Avenue Pictet-de-

Rochemont,

1207 Geneva,

Switzerland

T: +41 (0) 22 707 0080

F: +41 (0) 22 707 0088

This document is or inormation purposes only and is not to be construed as a solicitation or an oer to purchase or sell investments or related nancial instruments. This document has no regard or the specic investment

objectives, nancial situation or needs o any specic entity. Investment involves risk. The investments discussed in this document may not be suitable or all investors. Investors should make their own investment decisions based

upon their own nancial objectives and nancial resources and, i in any doubt, should seek advice rom an investment advisor. Past perormance is not a guide to uture perormance. The value o investments and any income

rom them can go down as well as up and you may not get back the amount originally invested. Levels and bases or taxation may change. For the UK: this document is issued by Collins Stewart Europe Limited (“CSEL”) which is

authorised and regulated by the Financial Services Authority. Registered Oce: 9th Floor, 88 Wood Street, London, EC2V 7QR. For Guernsey, Isle o Man and Jersey: this document is issued by Collins Stewart (CI) Limited (“CSCI”)

which is licensed and regulated by the Guernsey Financial Services Commission, the Isle o Man Financial Supervision Commission and the Jersey Financial Services Commission and is a member o the London Stock Exchange, the

Channel Islands Stock Exchange and ICMA. CSCI is registered in Guernsey and is a wholly owned subsidiary o Collins Stewart plc. CSEL, CSCI and/or connected persons may, rom time to time, have positions in, make a market

in and/or eect transactions in any investment or related investment mentioned herein and may provide nancial services to the issuers o such investments. The inormation contained herein is based on materials and sources

that we believe to be reliable, however, CSEL and CSCI make no representation or warranty, either express or implied, in relation to the accuracy, completeness or reliability o the inormation contained herein. All opinions and

estimates included in this document are subject to change without notice and CSEL and CSCI are under no obligation to update the inormation contained herein. None o CSEL, CSCI, their aliates or employees shall have any

liability whatsoever or any indirect or consequential loss or damage arising rom any use o this document. CSEL and CSCI do not make any warranties, express or implied, that the products, securities or services advertised are

available in your jurisdiction. Accordingly, i it is prohibited to advertise or make the products, securities or services a vailable in your jurisdiction, or to you (by reason o nationality, residence or otherwise) such products, securities

or services are not directed at you.

Portfolio Management Stockbroking Investment Funds