the determinants of european banks' capital structure: is

TRANSCRIPT

The Determinants of European Banks’ CapitalStructure: Is There a Difference between Public

and Private Banks?∗

Vitor Oliveiraa,b and Clara Raposob,c

aBanco de PortugalbISEG – Lisbon School of Economics and Management,

Universidade de LisboacADVANCE/CSG

In this paper we examine whether the determinants ofEuropean banks’ capital structure depend on the type of theinstitution (private or public). Using an international sampleof 586 banks from 21 European countries for the period of2000 to 2016, we find that when compared with private banks,the determinants of public banks’ capital structure are moreclosely aligned with those that affect nonfinancial firms. Fur-thermore, this paper provides evidence that these differencescan result in certain consequences with regards to the accessto the market, which implies that public banks are more sub-ject to market discipline. This is a very topical question, par-ticularly when studied in the context of the introduction ofmore demanding capital requirements through Basel III and,in particular, in the context of the new resolution regime whichimposes additional capital requirements, where banks’ accessto equity and debt markets plays a pivotal role.

JEL Codes: G21; G32.

∗The authors acknowledge helpful comments and suggestions from AntonioAntunes, Diana Bonfim, Hugo Reis, Miguel Ferreira, Olivier De Jonghe, RaquelGaspar, Sudipto Karmakar, Teodora Paligorova, and the two anonymous referees.Clara Raposo gratefully acknowledges financial support from FCT - Fundacaopara a Ciencia e Tecnologia (Portugal), national funding through research grant(UID/SOC/04521/2013). Clara Raposo also acknowledges the support of FCTgrant PTDC/EGE-OGE/28603/2017. The views expressed in this article arethose of the authors and do not necessarily reflect the views of the Bancode Portugal or the Eurosystem. Author e-mails: [email protected] [email protected].

155

156 International Journal of Central Banking September 2021

1. Introduction

According to modern financial literature, the study of capital struc-ture began with Modigliani and Miller (1958), who stated that ina frictionless world with full information and complete markets, thevalue of firms is independent of their capital structure (Santos 2001),leaving room for further research regarding the impact of disregard-ing the “frictionless assumption,” i.e., by adding taxes, costs of finan-cial distress, imperfections in the product market, transactions costs,asymmetry of information, and agency costs.

The study of the above-mentioned frictions has originated sev-eral theories, such as the trade-off theory, the pecking order theory,and the market timing theory (Flannery and Rangan 2006).

The great majority of the published empirical evidence over thelast decades which is dedicated to the topic of capital structurewas developed for nonfinancial firms. For instance, Rajan and Zin-gales (1995) justify the exclusion of financial firms from their sam-ple, because their leverage would be strongly influenced by explicit(or implicit) investor insurance schemes, such as deposit insurance.Furthermore, regulation such as minimum capital requirements candirectly affect the capital structure of financial firms.

Nevertheless, more recent empirical research regarding bank cap-ital structure has contributed evidence which supports that theattributes that affect bank capital structure are not very differentfrom those that influence the capital structure of nonfinancial firms.Studies by Flannery (1994), Flannery and Rangan (2008), and Allen,Carletti, and Marquez (2011) have shown that market discipline(carried out by subordinated creditors, or even by depositors) hasplayed an important role in banks’ capital structure. By the sametoken, other empirical papers published on this matter, such as Bar-ber and Lyon (1997), Brewer Iii, Kaufman, and Wall (2008), Groppand Heider (2010), and De Jonghe and Oztekin (2015), have foundthat bank-specific indicators also explain, to a large extent, bankcapital structure, i.e., most banks seem to optimize their capitalstructure in much the same way as firms, except when their capitalratios are close to the regulatory minimum.

Nevertheless, most of the empirical studies developed so farregarding banks’ capital structure are focused on large, public banks(Gropp and Heider 2010) and also on the main determinants of

Vol. 17 No. 3 The Determinants of European Banks’ Capital 157

the speed of adjustment toward the banks’ target capital ratio (DeJonghe and Oztekin 2015), tending to omit an analysis of the rela-tionship between the type of banks and their behavior regardingcapital structure decisions. It is exactly this gap that we aim to fillwith this paper.

Accordingly, we attempt to empirically answer the followingquestion: Are the determinants of banks’ capital structure differentin public versus private banks? For the purpose of this paper, publicbanks are considered to be those that are quoted/listed in capitalmarkets, whereas private banks are those that are not quoted/listedin capital markets.

The answer to this question is relevant from an empirical aswell as a policy point of view. From an empirical point of view, itis important to challenge the conclusions drawn from the above-mentioned studies, which use samples that comprise only large andpublic banks—which are subject to a different intensity of mar-ket discipline and/or use a pooled data set of banks, extrapolatingthe results for the whole sample, which in turn could hide somenon-negligible differences regarding the determinants of the capitalstructure of public and private banks.

From a policy point of view, when examined in the context of therequirements for additional capital, which has led to banks increas-ingly having to resort to own funds through the issue of, amongothers, equity or debt instruments with certain specific characteris-tics (e.g., subordinated debt) where the access to the market playsa pivotal role, it is important to investigate how the determinants ofbanks’ capital structure have influenced banks’ access to the market(which is represented by the share of subordinated debt for totalassets).1

Using an international sample of 586 banks from 21 Euro-pean countries for the period of 2000 to 2016, our results for the

1Beyond the new capital requirements encompassing the new capital buffers—namely the conservation capital buffer, countercyclical capital buffer, and system-ically important institutions buffer (introduced with the Basel III framework)—the Directive on Banking Recovery and Resolution that entered into force in 2016implies banks’ compliance with the additional capital requirements so-called min-imum requirement for own funds and eligible liabilities (MREL) which shouldequal 2 × (pillar 1 requirements + pillar 2 requirements and the combined bufferrequirement) – 125 basis points.

158 International Journal of Central Banking September 2021

whole sample confirm, to some extent, those of Gropp and Heider(2010), where size is positively related with leverage, whereas profits,market-to-book value, and risk all have a negative impact on lever-age, which is broadly consistent with the pecking order and markettiming theories.

Furthermore, considering the argument that banks manage theircapital or leverage ratios based on achieving a target, we show thatthe speed of adjustment is material in banks, which enables theseinstitutions to converge toward their long-run target.

Interestingly, our results have identified important differencesbetween public and private banks. Whereas the determinants of thecapital structure of public banks present a set of similarities withnonfinancial firms (which is in line with the results presented byGropp and Heider 2010), for private banks we find that those deter-minants which are typical of the market timing and pecking ordertheories fail to evidence the same relevance as in the case of publicbanks.

Besides the higher asymmetry of information which characterizesprivate firms, including financial ones, this paper provides empiricalevidence that those banks whose capital structure has been drivenby the determinants envisaged in the literature (public banks) havebeen subjected to more market discipline (which is represented bythe share of funding through subordinated debt).

The consequences of the above-mentioned differences observedbetween public and private banks for both the empirical literatureand financial stability are twofold. From an empirical point of view,this is the first study which shows that “one size does not fit all,”i.e., that the determinants of banks’ capital structure vary betweenprivate and public banks. From a financial stability point of view,during an initial phase, the differences observed in this paper couldnegatively affect the access of private banks to capital and debt mar-kets and thus compound the difficulties in complying with the moredemanding capital requirements envisaged in Basel III, as well asin the new resolution regime—which implies the issuance of bail-in-able instruments. However, in the long term, it is expected thatthe implications of the new resolution regime (such as the issuanceof MREL, composed of bail-in-able instruments, such as subordi-nated debt) will contribute to broadening market discipline to alltypes of banks and to the alignment of the determinants of their

Vol. 17 No. 3 The Determinants of European Banks’ Capital 159

capital structure. Additionally, the supervisors and regulators maywell be able to reap the benefits of a wider market discipline—whichis detailed below in this paper.

The remainder of the paper is organized as follows: Section 2presents a literature review, which is focused on capital structuredeterminants (in general for nonfinancial firms, and specifically forbanks). Section 3 develops hypotheses about how the determinantsof capital structure in nonfinancial firms play a role in the caseof banks. Section 4 introduces the data set, including descriptivestatistics for bank-specific indicators and a cross-country analysis.The methodological approach is discussed in section 5. Section 6reports the results and robustness tests, and the main conclusionsare presented in section 7.

2. Literature Review

2.1 The Determinants of Capital Structure

Modern capital structure theory began with Modigliani and Miller(1958), advocating that the value of firms is independent of itscapital structure in a frictionless world with full information andcomplete markets (Santos 2001), leaving room to exploit certainfrictions.

To this end, Berger, Herring, and Szego (1995) summarize thatthe main frictions that cause capital decisions to depart fromModigliani and Miller (1958) are (i) taxes—as interest paymentsare tax deductible, whereas dividends are not, and that by sub-stituting debt for equity, firms are able to pass on larger returnsto investors by reducing payments to the government, and, there-fore, all else being equal, shareholders prefer to fund firms almostentirely with debt; (ii) financial distress—where more leverage canlead to an increase in the likelihood of incurring the costs of finan-cial distress; (iii) asymmetric information—which stems from thefact that managers generally have access to more information abouttheir own earnings prospects and financial condition than the mar-ket; (iv) transactions costs of new issues—which when combinedwith asymmetric information can also influence the relative costs ofinternal versus external finance, and the relative costs of debt versus

160 International Journal of Central Banking September 2021

equity, and; (v) agency costs between shareholders and creditors orbetween the former and managers (Jensen and Meckling 1976).

A sizable amount of research has been carried out since then,which can be summarized into three main theories (Flannery andRangan 2006): the trade-off theory, the pecking order theory, andthe market timing theory. According to the trade-off theory, firmsselect target debt-equity ratios to trade off the costs and benefitsof leverage, contradicting the unrealistic assumption that firms arealways at their equilibrium leverage (Oztekin and Flannery 2012).The benefits of leverage include the tax deductibility of the debtservice (the well-known “interest tax shield”) and the agency ben-efits of debt associated with conflicts of interest between managersand stockholders. The costs of debt can be identified as costs ofbankruptcy or financial distress, agency costs due to misalignmentof interests between stockholders and creditors, and trading costs(according to Oztekin 2015, if a country’s characteristics make theissuance of debt and equity expensive, firms tend to exhibit sloweradjustment speeds). The pecking order theory, which was first sug-gested by Myers and Majluf (1984), is based on the assumptionthat information asymmetries between insiders and outsiders canlead managers to perceive that the uninformed market would gen-erally underprice their firm’s equity—and for this reason, managershave a preference for investments to be financed first with internalfunds, second with secured debt, and lastly with equity—which isonly used as a last resort. This order of preference between internalversus external funds, and between debt versus equity, is a justifi-cation for firms to maintain a certain financial slack, particularlythose firms that operate in industries which are particularly opaqueand are subject to asymmetry of information between insiders andoutsiders. The market timing theory argues that a firm’s leveragereflects its cumulative ability to sell overpriced equity shares, i.e.,share prices fluctuate around their “true” value, and managers tendto issue shares when the firm’s market-to-book value is high. There-fore, by exploiting asymmetric information, firms increase the wealthof their current shareholders.

Recent research on capital structure has been developed aroundthese three competing, but not necessarily mutually exclusive, the-ories. Many empirical studies have tried to identify the correctmeasures for characterizing the attributes present in these theories.

Vol. 17 No. 3 The Determinants of European Banks’ Capital 161

Amongst the main studies of interest in this context, we highlightTitman and Wessels (1988), Rajan and Zingales (1995), Flanneryand Rangan (2006), Lemmon, Roberts, and Zender (2008), andFrank and Goyal (2009). The measures used in these papers comprise(i) collateral, which is defined as being the sum of liquid assets andfixed assets; (ii) firm size, which is represented by total assets; (iii)market-to-book ratio, which is defined as being the ratio between themarket value of assets and the book value of total assets; (iv) firmrisk, which is usually computed as the standard deviation of a firm’smarket stock returns; and (v) profits. Collateral and firm asset riskcan be included in the trade-off theory, whereas profits and market-to-book value are more easily aligned with the pecking order the-ory and market timing, respectively. To this end, Harris and Raviv(1991) showed that leverage increases with fixed assets (collateral),as well as with nondebt tax shields, growth opportunities, and firmsize, and that it decreases with volatility, advertising expenditures,bankruptcy probability, and the uniqueness of the products.

With regards to the relationship between the above-mentionedvariables and firms’ capital structure, Rajan and Zingales (1995)concluded that (i) the relationship between the ratio of fixed assetsto total assets and leverage is positive—the rationale underlying thisfactor being that tangible assets are easy to collateralize and theythus reduce the agency costs of debt; (ii) leverage is negatively cor-related with market-to-book value for two reasons: first, in theory,firms with high market-to-book ratios have higher costs of finan-cial distress and, second, this negative correlation stems from firms’tendency to issue stock when their stock price is high in relationto earnings or book value (which thus supports the assumptionsunderlying the market timing theory); (iii) size is positively corre-lated with leverage, as, in theory, larger firms are better diversifiedand have a lower probability of being in financial distress; and (iv)profitability is negatively correlated with leverage (which supportsthe pecking order theory). To a large extent, these results are con-sistent with those obtained by Frank and Goyal (2009), who used adifferent sample of firms as well as a different time span.

Flannery and Rangan (2006), Lemmon, Roberts, and Zender(2008), Oztekin and Flannery (2012), and Oztekin (2015) all focusedon testing firms’ willingness to move toward their target leverageratio, and found that firms converge toward their long-run targets

162 International Journal of Central Banking September 2021

at a rate of more than 30 percent per year, which depends, to alarger extent, on the institutional environment. An example is thosecountries which ease the issuance of debt and/or equity contributeto accelerate the speed of adjustment toward the optimal leverageratio (Oztekin and Flannery 2012 and Oztekin 2015).

2.2 The Special Case of Banks

In many ways, banks are different from nonfinancial firms, whichare able to induce differences in their capital structure decisions.Cocris and Ungureanu (2007) surmise that the main differences arethat a high proportion of bank failures lead to negative externalities;agency problems are enhanced by the inefficient monitoring of banksby depositors and other stakeholders; information flow is complex,due to the opaque environment in which banks operate; banks areheavily regulated; sometimes the regulator itself is a bank stake-holder; the diversification of activities within a bank conglomerateintensifies agency problems between corporate insiders and smallshareholders; in general, banks have a more concentrated equityownership than nonfinancial firms, which makes it more difficultfor small equity holders to exert influence over the management ofbanks; there is less competition regarding financial products andtakeover activity; and banks have a safety net available, which affectsthe stakeholders’ incentives to monitor banks. In addition, Harding,Liang, and Ross (2013) highlight the high levels of leverage whichcharacterizes banks’ capital structure, which was arguably respon-sible for the failure of the majority of investment banks during therecent global financial crisis.

To some extent, the identification of these special features ofthe banking sector are shared by Berger, Herring, and Szego (1995)and Santos (2001), who both mention that the main frictions in thebanking sector which can justify the departure from Modigliani andMiller (1958) are the following: the existence of a safety net—whichis defined as all government actions which are devised to improvethe safety and soundness of the banking system and thus shieldbanks’ creditors (mainly depositors) from the full consequences ofbank risk-taking; and the capital requirements stated by the regu-lators to protect themselves against the costs of financial distress,

Vol. 17 No. 3 The Determinants of European Banks’ Capital 163

agency problems, the reduction in market discipline (caused by thesafety net), and the systemic risk posed by the banking sector.

These characteristics explain why the majority of the empiricalresearch on firm capital structure was carried out with nonfinancialfirms (see, for example, Rajan and Zingales 1995).

Nevertheless, the empirical research regarding banks’ capitalstructure has evidenced that those attributes that affect bank capitalstructure are not so far removed from the attributes which influencenonfinancial firms’ capital structure. Thus, Modigliani and Miller’stheory holds, within limits, for banks as well (Miles, Yang, andMarcheggiano 2013). Research carried out by Flannery (1994), Flan-nery and Sorescu (1996), Morgan and Stiroh (2001), Flannery andRangan (2008), and Allen, Carletti, and Marquez (2011) has shownthat market discipline demonstrated by subordinated creditors, andeven by depositors (as in Martinez Peria and Schmukler 2001), hasplayed an important role in explaining banks’ capital structure.

Regarding the existence of similarity, or not, between the deter-minants of banks’ capital structure and nonfinancial firms andwhether the traditional capital determinants also hold for finan-cial institutions, an empirical work carried out by Barber and Lyon(1997) and Brewer Iii, Kaufman, and Wall (2008) established thatbank-specific indicators also contribute to explain banks’ capitalstructure. Barber and Lyon (1997) concluded that the relationshipsbetween size, market-to-book value, and security returns are posi-tive and similar for both financial and nonfinancial firms. BrewerIii, Kaufman, and Wall (2008) found that leverage is positively andsignificantly correlated with banks’ risk; however, the remainingvariables, such as return on assets and size, are not significantlyrelated to leverage. Nevertheless, bank-specific variables collectivelyexplain banks’ leverage, taking into account the result from the Waldtest. With regards to speed of adjustment, the value attained was12 percent.

The more recent studies on banks’ capital structure were devel-oped by Gropp and Heider (2010)—who expound on the influence ofbank-specific indicators on banks’ capital structure, comparing thesewith those evidenced by nonfinancial firms—and also De Jongheand Oztekin (2015), whose focus was to investigate the adjustmentprocess for targeting capital. Using a sample of large public banksfrom the United States and Europe (from 1991 to 2004), the first

164 International Journal of Central Banking September 2021

study evidences that regulation is not the main feature that causesthe divergence of banks’ capital structure from that which wasargued by Modigliani and Miller (1958). For these authors, mostbanks seem to optimize their capital structure in much the sameway as firms do, except when their capital ratios approach the levelsof the regulatory minimum. Additionally, as demonstrated by Lem-mon, Roberts, and Zander (2008), banks move toward their targetleverage ratios at a speed of adjustment of 45 percent. This evidencecontradicts the “regulatory view” of banks, whereby they shouldconverge toward a common target, namely the minimum require-ment set under Basel I, which gives support to the results obtainedby Berger et al. (2008), who argue that banks actively manage theircapital ratios.

The second study, that of De Jonghe and Oztekin (2015), usinga sample of banks from 64 countries during the 1994–2010 period,based on the studies developed for nonfinancial firms by Oztekin andFlannery (2012) and Oztekin (2015), found that in the case of banks,the speed of adjustment is heterogeneous, depending on the insti-tutional environment—which is consistent with the results obtainedwith nonfinancial firms. That is to say that the speed of adjustmenttoward the target capital ratio increases in those countries that havemore stringent capital requirements, better supervisory monitoring,and more-developed capital markets—which in turn decreases thecosts of debt and/or equity issuance. In addition, and consistentwith those studies developed so far, this study found that smaller,more profitable, and cost-efficient banks have higher capital ratios.

3. Research Question and Hypothesis Development

This paper aims to empirically answer the following question: Arethe determinants of banks’ capital structure different in public ver-sus private banks? Public banks are those that are quoted/listedin capital markets, whereas private banks are those that are notquoted/listed in capital markets.

On the one hand, we expect that the determinants of publicbanks’ capital structure and their respective decisions regarding theoptimal capital are different from those of private banks, due to thefact that the former has easier access to capital and debt markets, as

Vol. 17 No. 3 The Determinants of European Banks’ Capital 165

a result of having less of the information asymmetry which charac-terizes public firms, whether they be financial or nonfinancial firms.On the other hand, considering that the banking sector is one of themost regulated in the world (Santos 2001), supplemented by the factthat all banks (public or private) are obliged to disclose informationthrough pillar 3 of the regulatory framework, the determinants ofpublic banks’ capital structure, as identified by Gropp and Heider(2010), may well be not so different from those of private banks.

Accordingly, we test the hypothesis that the determinants of pub-lic banks’ capital structure are different from the determinants ofprivate banks against the hypothesis that the determinants of banks’capital structure are the same for both types of banks.

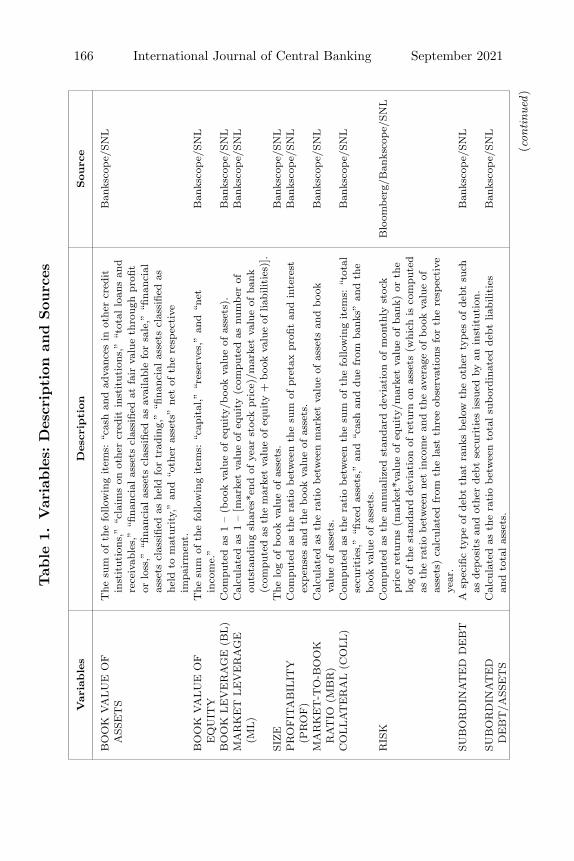

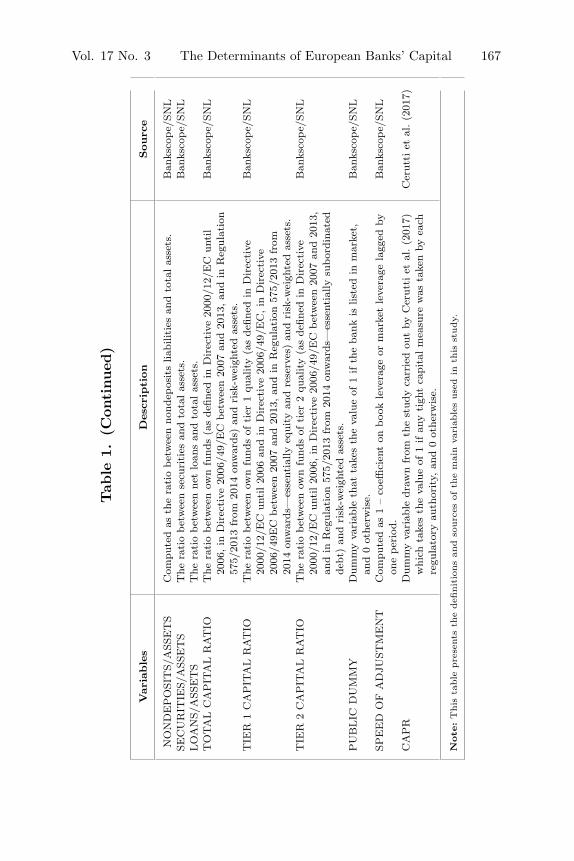

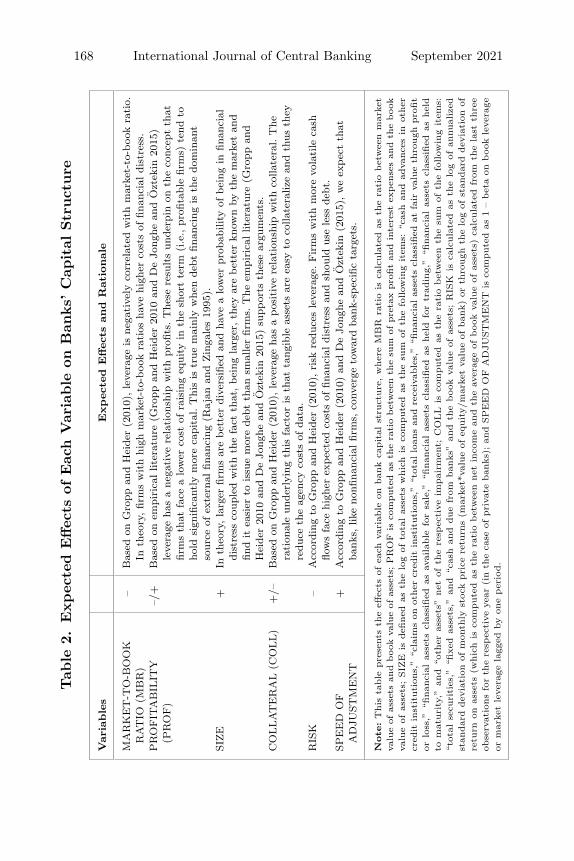

A detailed overview of the explanatory variables and their sourcesis provided in table 1. Table 2 presents the expected signs of theeffects of bank-specific indicators on banks’ capital structure, as wellas a summary of the arguments that support such expectations.

4. Data

The data for this paper include banks which have their headquar-ters in 21 European countries, as well as subsidiaries of foreign banks(mainly from the United States), which add up to 586 banks, for theperiod of 2000–16. The data give rise to a panel of 6,065 bank-yearobservations. As mentioned in table 1, all data were collected fromthe Bankscope and SNL databases.

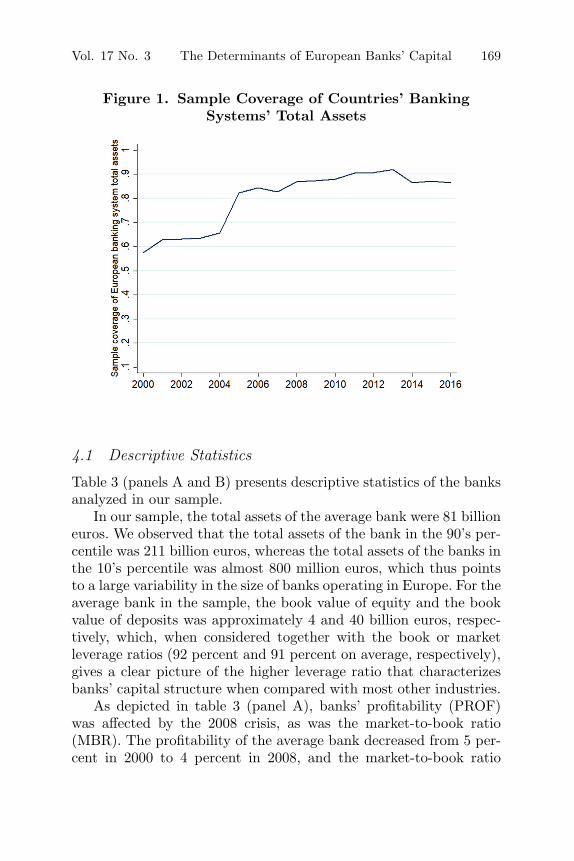

As shown in figure 1, the sample covers a high percentage ofthe European banking system’s assets, which represents a shareof 90 percent in 2012, decreasing slightly to 85 percent from 2012onward—which is due to the change of the database from Bankscopeto SNL.

We obtain an unbalanced panel data set, on account of a data gapand entry/exit in the sample. It is worth noting that the occurrenceof certain mergers and acquisitions, together with the emergence ofnew banks, caused changes in the constitution of the sample dur-ing the period under analysis (table 3). It should be mentioned thatthese mergers and acquisitions events are included in banks’ fixedeffects.

166 International Journal of Central Banking September 2021Tab

le1.

Var

iable

s:D

escr

iption

and

Sou

rces

Var

iable

sD

escr

ipti

on

Sourc

e

BO

OK

VA

LU

EO

FA

SSE

TS

The

sum

ofth

efo

llow

ing

item

s:“c

ash

and

adva

nces

inot

her

cred

itin

stitut

ions

,”“c

laim

son

othe

rcr

edit

inst

itut

ions

,”“t

otal

loan

san

dre

ceiv

able

s,”

“fina

ncia

las

sets

clas

sifie

dat

fair

valu

eth

roug

hpr

ofit

orlo

ss,”

“fina

ncia

las

sets

clas

sifie

das

avai

labl

efo

rsa

le,”

“fina

ncia

las

sets

clas

sifie

das

held

for

trad

ing,

”“fi

nanc

ialas

sets

clas

sifie

das

held

tom

atur

ity,

”an

d“o

ther

asse

ts”

net

ofth

ere

spec

tive

impa

irm

ent.

Ban

ksco

pe/

SNL

BO

OK

VA

LU

EO

FE

QU

ITY

The

sum

ofth

efo

llow

ing

item

s:“c

apital

,”“r

eser

ves,

”an

d“n

etin

com

e.”

Ban

ksco

pe/

SNL

BO

OK

LE

VE

RA

GE

(BL)

Com

pute

das

1–

(boo

kva

lue

ofeq

uity

/boo

kva

lue

ofas

sets

).B

anks

cope/

SNL

MA

RK

ET

LE

VE

RA

GE

(ML)

Cal

cula

ted

as1

–[m

arke

tva

lue

ofeq

uity

(com

pute

das

num

ber

ofou

tsta

ndin

gsh

ares

*end

ofye

arst

ock

pric

e)/m

arke

tva

lue

ofba

nk(c

ompu

ted

asth

em

arke

tva

lue

ofeq

uity

+boo

kva

lue

oflia

bilit

ies)

].

Ban

ksco

pe/

SNL

SIZE

The

log

ofboo

kva

lue

ofas

sets

.B

anks

cope/

SNL

PR

OFIT

AB

ILIT

Y(P

RO

F)

Com

pute

das

the

ratio

bet

wee

nth

esu

mof

pret

axpr

ofit

and

inte

rest

expen

ses

and

the

boo

kva

lue

ofas

sets

.B

anks

cope/

SNL

MA

RK

ET

-TO

-BO

OK

RAT

IO(M

BR

)C

alcu

late

das

the

ratio

bet

wee

nm

arke

tva

lue

ofas

sets

and

boo

kva

lue

ofas

sets

.B

anks

cope/

SNL

CO

LLAT

ER

AL

(CO

LL)

Com

pute

das

the

ratio

bet

wee

nth

esu

mof

the

follo

win

gitem

s:“t

otal

secu

rities

,”“fi

xed

asse

ts,”

and

“cas

han

ddu

efr

omba

nks”

and

the

boo

kva

lue

ofas

sets

.

Ban

ksco

pe/

SNL

RIS

KC

ompu

ted

asth

ean

nual

ized

stan

dard

devi

atio

nof

mon

thly

stoc

kpr

ice

retu

rns

(mar

ket*

valu

eof

equi

ty/m

arke

tva

lue

ofba

nk)

orth

elo

gof

the

stan

dard

devi

atio

nof

retu

rnon

asse

ts(w

hich

isco

mpu

ted

asth

era

tio

bet

wee

nne

tin

com

ean

dth

eav

erag

eof

boo

kva

lue

ofas

sets

)ca

lcul

ated

from

the

last

thre

eob

serv

atio

nsfo

rth

ere

spec

tive

year

.

Blo

omber

g/B

anks

cope/

SNL

SUB

OR

DIN

AT

ED

DE

BT

Asp

ecifi

cty

pe

ofde

btth

atra

nks

bel

owth

eot

her

types

ofde

btsu

chas

depos

its

and

othe

rde

btse

curi

ties

issu

edby

anin

stitut

ion.

Ban

ksco

pe/

SNL

SUB

OR

DIN

AT

ED

DE

BT

/ASS

ET

SC

alcu

late

das

the

ratio

bet

wee

nto

talsu

bor

dina

ted

debt

liabi

litie

san

dto

talas

sets

.B

anks

cope/

SNL

(con

tinu

ed)

Vol. 17 No. 3 The Determinants of European Banks’ Capital 167

Tab

le1.

(Con

tinued

)

Var

iable

sD

escr

ipti

on

Sourc

e

NO

ND

EP

OSI

TS/

ASS

ET

SC

ompu

ted

asth

era

tio

bet

wee

nno

ndep

osits

liabi

litie

san

dto

talas

sets

.B

anks

cope/

SNL

SEC

UR

ITIE

S/A

SSE

TS

The

ratio

bet

wee

nse

curi

ties

and

tota

las

sets

.B

anks

cope/

SNL

LO

AN

S/A

SSE

TS

The

ratio

bet

wee

nne

tlo

ans

and

tota

las

sets

.T

OTA

LC

AP

ITA

LR

AT

IOT

hera

tio

bet

wee

now

nfu

nds

(as

defin

edin

Dir

ective

2000

/12/

EC

until

2006

,in

Dir

ective

2006

/49/

EC

bet

wee

n20

07an

d20

13,an

din

Reg

ulat

ion

575/

2013

from

2014

onw

ards

)an

dri

sk-w

eigh

ted

asse

ts.

Ban

ksco

pe/

SNL

TIE

R1

CA

PIT

AL

RAT

IOT

hera

tio

bet

wee

now

nfu

nds

oftier

1qu

ality

(as

defin

edin

Dir

ective

2000

/12/

EC

until20

06an

din

Dir

ective

2006

/49/

EC

,in

Dir

ective

2006

/49E

Cbet

wee

n20

07an

d20

13,an

din

Reg

ulat

ion

575/

2013

from

2014

onw

ards

—es

sent

ially

equi

tyan

dre

serv

es)

and

risk

-wei

ghte

das

sets

.

Ban

ksco

pe/

SNL

TIE

R2

CA

PIT

AL

RAT

IOT

hera

tio

bet

wee

now

nfu

nds

oftier

2qu

ality

(as

defin

edin

Dir

ective

2000

/12/

EC

until20

06,in

Dir

ective

2006

/49/

EC

bet

wee

n20

07an

d20

13,

and

inR

egul

atio

n57

5/20

13fr

om20

14on

war

ds—

esse

ntia

llysu

bor

dina

ted

debt

)an

dri

sk-w

eigh

ted

asse

ts.

Ban

ksco

pe/

SNL

PU

BLIC

DU

MM

YD

umm

yva

riab

leth

atta

kes

the

valu

eof

1if

the

bank

islis

ted

inm

arke

t,an

d0

othe

rwis

e.B

anks

cope/

SNL

SPE

ED

OF

AD

JUST

ME

NT

Com

pute

das

1–

coeffi

cien

ton

boo

kle

vera

geor

mar

ket

leve

rage

lagg

edby

one

per

iod.

Ban

ksco

pe/

SNL

CA

PR

Dum

my

vari

able

draw

nfr

omth

est

udy

carr

ied

out

byC

erut

tiet

al.(2

017)

whi

chta

kes

the

valu

eof

1if

any

tigh

tca

pita

lm

easu

rew

asta

ken

byea

chre

gula

tory

auth

ority,

and

0ot

herw

ise.

Cer

utti

etal

.(2

017)

Note

:T

his

table

pre

sent

sth

edefi

nit

ions

and

sourc

esof

the

mai

nva

riab

les

use

din

this

study.

168 International Journal of Central Banking September 2021Tab

le2.

Expec

ted

Effec

tsof

Eac

hV

aria

ble

onB

anks’

Cap

ital

Str

uct

ure

Var

iable

sExpec

ted

Effec

tsan

dR

atio

nal

e

MA

RK

ET

-TO

-BO

OK

RAT

IO(M

BR

)–

Bas

edon

Gro

ppan

dH

eide

r(2

010)

,le

vera

geis

nega

tive

lyco

rrel

ated

with

mar

ket-

to-b

ook

ratio.

Inth

eory

,fir

ms

with

high

mar

ket-

to-b

ook

ratios

have

high

erco

sts

offin

anci

aldi

stre

ss.

PR

OFIT

AB

ILIT

Y(P

RO

F)

–/+

Bas

edon

empi

rica

llit

erat

ure

(Gro

ppan

dH

eide

r20

10an

dD

eJo

nghe

and

Ozt

ekin

2015

)le

vera

geha

sa

nega

tive

rela

tion

ship

with

profi

ts.T

hese

resu

lts

unde

rpin

onth

eco

ncep

tth

atfir

ms

that

face

alo

wer

cost

ofra

isin

geq

uity

inth

esh

ort

term

(i.e

.,pr

ofita

ble

firm

s)te

ndto

hold

sign

ifica

ntly

mor

eca

pita

l.T

his

istr

uem

ainl

yw

hen

debt

finan

cing

isth

edo

min

ant

sour

ceof

exte

rnal

finan

cing

(Raj

anan

dZin

gale

s19

95).

SIZE

+In

theo

ry,la

rger

firm

sar

ebet

ter

dive

rsifi

edan

dha

vea

low

erpr

obab

ility

ofbei

ngin

finan

cial

dist

ress

coup

led

with

the

fact

that

,bei

ngla

rger

,th

eyar

ebet

ter

know

nby

the

mar

ket

and

find

itea

sier

tois

sue

mor

ede

btth

ansm

alle

rfir

ms.

The

empi

rica

llit

erat

ure

(Gro

ppan

dH

eide

r20

10an

dD

eJo

nghe

and

Ozt

ekin

2015

)su

ppor

tsth

ese

argu

men

ts.

CO

LLAT

ER

AL

(CO

LL)

+/–

Bas

edon

Gro

ppan

dH

eide

r(2

010)

,le

vera

geha

sa

pos

itiv

ere

lation

ship

with

colla

tera

l.T

hera

tion

ale

unde

rlyi

ngth

isfa

ctor

isth

atta

ngib

leas

sets

are

easy

toco

llate

raliz

ean

dth

usth

eyre

duce

the

agen

cyco

sts

ofda

ta.

RIS

K–

Acc

ordi

ngto

Gro

ppan

dH

eide

r(2

010)

,ri

skre

duce

sle

vera

ge.Fir

ms

with

mor

evo

latile

cash

flow

sfa

cehi

gher

expec

ted

cost

sof

finan

cial

dist

ress

and

shou

ldus

ele

ssde

bt.

SPE

ED

OF

AD

JUST

ME

NT

+A

ccor

ding

toG

ropp

and

Hei

der

(201

0)an

dD

eJo

nghe

and

Ozt

ekin

(201

5),w

eex

pec

tth

atba

nks,

like

nonfi

nanc

ialfir

ms,

conv

erge

tow

ard

bank

-spec

ific

targ

ets.

Note

:T

his

table

pre

sent

sth

eeff

ects

ofea

chva

riab

leon

ban

kca

pit

alst

ruct

ure

,w

her

eM

BR

rati

ois

calc

ula

ted

asth

era

tio

bet

wee

nm

arke

tva

lue

ofas

sets

and

boo

kva

lue

ofas

sets

;PR

OF

isco

mpute

das

the

rati

obet

wee

nth

esu

mof

pre

tax

pro

fit

and

inte

rest

expen

ses

and

the

boo

kva

lue

ofas

sets

;SIZ

Eis

defi

ned

asth

elo

gof

tota

las

sets

whic

his

com

pute

das

the

sum

ofth

efo

llow

ing

item

s:“c

ash

and

adva

nce

sin

other

cred

itin

stit

uti

ons,

”“c

laim

son

other

cred

itin

stit

uti

ons,

”“t

otal

loan

san

dre

ceiv

able

s,”

“finan

cial

asse

tscl

assi

fied

atfa

irva

lue

thro

ugh

pro

fit

orlo

ss,”

“finan

cial

asse

tscl

assi

fied

asav

aila

ble

for

sale

,”“fi

nan

cial

asse

tscl

assi

fied

ashel

dfo

rtr

adin

g,”

“finan

cial

asse

tscl

assi

fied

ashel

dto

mat

uri

ty,”

and

“oth

eras

sets

”net

ofth

ere

spec

tive

impai

rmen

t;C

OLL

isco

mpute

das

the

rati

obet

wee

nth

esu

mof

the

follow

ing

item

s:“t

otal

secu

riti

es,”

“fixe

das

sets

,”an

d“c

ash

and

due

from

ban

ks”

and

the

boo

kva

lue

ofas

sets

;R

ISK

isca

lcula

ted

asth

elo

gof

annu

aliz

edst

andar

ddev

iati

onof

mon

thly

stoc

kpri

cere

turn

s(m

arke

t*va

lue

ofeq

uity/

mar

ket

valu

eof

ban

k)or

thro

ugh

the

log

ofst

andar

ddev

iati

onof

retu

rnon

asse

ts(w

hic

his

com

pute

das

the

rati

obet

wee

nnet

inco

me

and

the

aver

age

ofboo

kva

lue

ofas

sets

)ca

lcula

ted

from

the

last

thre

eob

serv

atio

ns

for

the

resp

ecti

veye

ar(i

nth

eca

seof

pri

vate

ban

ks);

and

SPEED

OF

AD

JUST

MEN

Tis

com

pute

das

1–

bet

aon

boo

kle

vera

geor

mar

ket

leve

rage

lagg

edby

one

per

iod.

Vol. 17 No. 3 The Determinants of European Banks’ Capital 169

Figure 1. Sample Coverage of Countries’ BankingSystems’ Total Assets

4.1 Descriptive Statistics

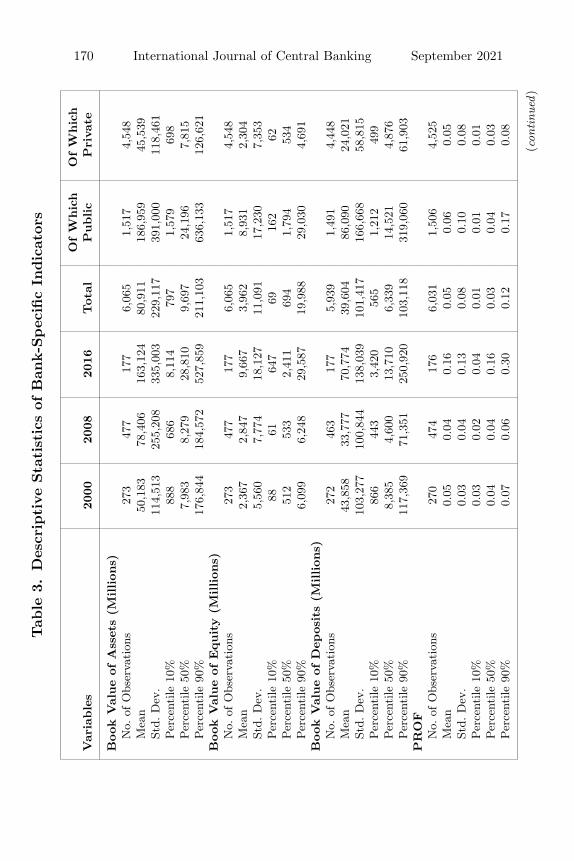

Table 3 (panels A and B) presents descriptive statistics of the banksanalyzed in our sample.

In our sample, the total assets of the average bank were 81 billioneuros. We observed that the total assets of the bank in the 90’s per-centile was 211 billion euros, whereas the total assets of the banks inthe 10’s percentile was almost 800 million euros, which thus pointsto a large variability in the size of banks operating in Europe. For theaverage bank in the sample, the book value of equity and the bookvalue of deposits was approximately 4 and 40 billion euros, respec-tively, which, when considered together with the book or marketleverage ratios (92 percent and 91 percent on average, respectively),gives a clear picture of the higher leverage ratio that characterizesbanks’ capital structure when compared with most other industries.

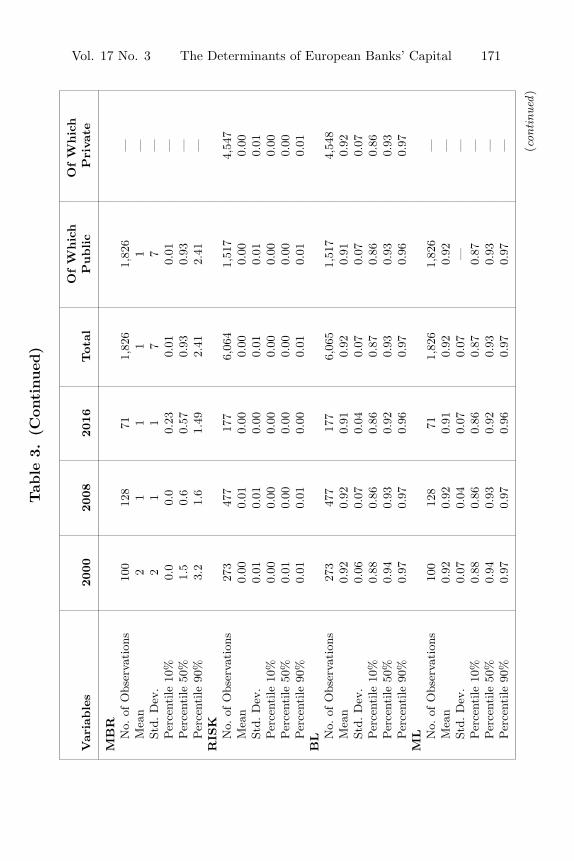

As depicted in table 3 (panel A), banks’ profitability (PROF)was affected by the 2008 crisis, as was the market-to-book ratio(MBR). The profitability of the average bank decreased from 5 per-cent in 2000 to 4 percent in 2008, and the market-to-book ratio

170 International Journal of Central Banking September 2021Tab

le3.

Des

crip

tive

Sta

tist

ics

ofB

ank-S

pec

ific

Indic

ator

s

OfW

hic

hO

fW

hic

hV

aria

ble

s20

0020

0820

16Tot

alP

ublic

Pri

vate

Book

Val

ue

ofA

sset

s(M

illion

s)N

o.of

Obs

erva

tion

s27

347

717

76,

065

1,51

74,

548

Mea

n50

,183

78,4

0616

3,12

480

,911

186,

959

45,5

39St

d.D

ev.

114,

513

255,

208

335,

003

229,

117

391,

000

118,

461

Per

cent

ile10

%88

868

68,

114

797

1,57

969

8Per

cent

ile50

%7,

983

8,27

928

,810

9,69

724

,196

7,81

5Per

cent

ile90

%17

6,84

418

4,57

252

7,85

921

1,10

363

6,13

312

6,62

1B

ook

Val

ue

ofEquity

(Million

s)N

o.of

Obs

erva

tion

s27

347

717

76,

065

1,51

74,

548

Mea

n2,

367

2,84

79,

667

3,96

28,

931

2,30

4St

d.D

ev.

5,56

07,

774

18,1

2711

,091

17,2

307,

353

Per

cent

ile10

%88

6164

769

162

62Per

cent

ile50

%51

253

32,

411

694

1,79

453

4Per

cent

ile90

%6,

099

6,24

829

,587

19,9

8829

,030

4,69

1B

ook

Val

ue

ofD

epos

its

(Million

s)N

o.of

Obs

erva

tion

s27

246

317

75,

939

1,49

14,

448

Mea

n43

,858

33,7

7770

,774

39,6

0486

,090

24,0

21St

d.D

ev.

103,

277

100,

844

138,

039

101,

417

166,

668

58,8

15Per

cent

ile10

%86

644

33,

420

565

1,21

249

9Per

cent

ile50

%8,

385

4,60

013

,710

6,33

914

,521

4,87

6Per

cent

ile90

%11

7,36

971

,351

250,

920

103,

118

319,

060

61,9

03P

RO

FN

o.of

Obs

erva

tion

s27

047

417

66,

031

1,50

64,

525

Mea

n0.

050.

040.

160.

050.

060.

05St

d.D

ev.

0.03

0.04

0.13

0.08

0.10

0.08

Per

cent

ile10

%0.

030.

020.

040.

010.

010.

01Per

cent

ile50

%0.

040.

040.

160.

030.

040.

03Per

cent

ile90

%0.

070.

060.

300.

120.

170.

08

(con

tinu

ed)

Vol. 17 No. 3 The Determinants of European Banks’ Capital 171

Tab

le3.

(Con

tinued

)

OfW

hic

hO

fW

hic

hV

aria

ble

s20

0020

0820

16Tot

alP

ublic

Pri

vate

MB

RN

o.of

Obs

erva

tion

s10

012

871

1,82

61,

826

—M

ean

21

11

1—

Std.

Dev

.2

11

77

—Per

cent

ile10

%0.

00.

00.

230.

010.

01—

Per

cent

ile50

%1.

50.

60.

570.

930.

93—

Per

cent

ile90

%3.

21.

61.

492.

412.

41—

RIS

KN

o.of

Obs

erva

tion

s27

347

717

76,

064

1,51

74,

547

Mea

n0.

000.

010.

000.

000.

000.

00St

d.D

ev.

0.01

0.01

0.00

0.01

0.01

0.01

Per

cent

ile10

%0.

000.

000.

000.

000.

000.

00Per

cent

ile50

%0.

010.

000.

000.

000.

000.

00Per

cent

ile90

%0.

010.

010.

000.

010.

010.

01B

L No.

ofO

bser

vati

ons

273

477

177

6,06

51,

517

4,54

8M

ean

0.92

0.92

0.91

0.92

0.91

0.92

Std.

Dev

.0.

060.

070.

040.

070.

070.

07Per

cent

ile10

%0.

880.

860.

860.

870.

860.

86Per

cent

ile50

%0.

940.

930.

920.

930.

930.

93Per

cent

ile90

%0.

970.

970.

960.

970.

960.

97M

L No.

ofO

bser

vati

ons

100

128

711,

826

1,82

6—

Mea

n0.

920.

920.

910.

920.

92—

Std.

Dev

.0.

070.

040.

070.

07—

—Per

cent

ile10

%0.

880.

860.

860.

870.

87—

Per

cent

ile50

%0.

940.

930.

920.

930.

93—

Per

cent

ile90

%0.

970.

970.

960.

970.

97— (c

ontinu

ed)

172 International Journal of Central Banking September 2021

Tab

le3.

(Con

tinued

)

OfW

hic

hO

fW

hic

hV

aria

ble

s20

0020

0820

16Tot

alP

ublic

Pri

vate

CO

LL

No.

ofO

bser

vati

ons

264

458

175

5,87

61,

473

4,40

3M

ean

0.22

0.28

0.26

0.28

0.26

0.28

Std.

Dev

0.13

1.12

0.14

0.95

0.14

1.09

Per

cent

ile10

%0.

090.

080.

130.

080.

110.

07Per

cent

ile50

%0.

210.

200.

230.

210.

230.

20Per

cent

ile90

%0.

450.

440.

470.

450.

460.

45

Note

s:T

hista

ble

pres

ents

desc

ript

ive

stat

istics

ofba

nks’

spec

ific

indi

cato

rsdu

ring

the

per

iod

2000

–16.

The

tabl

epr

esen

tsth

enu

mber

ofob

serv

atio

ns(N

),th

em

ean,

stan

dard

devi

atio

n(S

td.

Dev

.),

and

som

eper

cent

iles

ofth

efo

llow

ing

vari

able

s:B

OO

KVA

LU

Eof

ASS

ET

S,w

hich

isth

esu

mof

the

follo

win

gitem

s:“c

ash

and

adva

nces

inot

her

cred

itin

stitut

ions

,”“c

laim

son

othe

rcr

edit

inst

i-tu

tion

s,”

“tot

allo

ans

and

rece

ivab

les,

”“fi

nanc

ialas

sets

clas

sifie

dat

fair

valu

eth

roug

hpr

ofit

orlo

ss,”

“fina

ncia

las

sets

clas

sifie

das

avai

labl

efo

rsa

le,”

“fina

ncia

las

sets

clas

sifie

das

held

for

trad

ing,

”“fi

nanc

ialas

sets

clas

sifie

das

held

tom

atur

ity,

”an

d“o

ther

asse

ts”

net

ofth

ere

spec

tive

impa

irm

ent;

BO

OK

VA

LU

Eof

EQ

UIT

Y,w

hich

isth

esu

mof

the

follo

win

gitem

s:“c

apital

,”“r

eser

ves,

”an

d“n

etin

com

e”;B

OO

KVA

LU

Eof

DE

PO

SIT

S,w

hich

isto

talde

pos

its

from

clie

nts;

PR

OF,w

hen

com

pute

das

the

ratio

bet

wee

nth

esu

mof

pret

axpr

ofit

and

inte

rest

expen

ses

and

the

boo

kva

lue

ofas

sets

;M

BR

ratio,

whi

chis

calc

ulat

edas

the

ratio

bet

wee

nm

arke

tva

lue

ofas

sets

and

boo

kva

lue

ofas

sets

;R

ISK

,w

hich

isco

mpu

ted

asth

elo

gst

anda

rdde

viat

ion

ofre

turn

onas

sets

(whi

chis

com

pute

das

the

ratio

bet

wee

nne

tin

com

ean

dth

eav

erag

eof

boo

kva

lue

ofas

sets

)ca

lcul

ated

from

the

last

thre

eob

serv

atio

nsfo

rth

ere

spec

tive

year

;BL,w

hich

isco

mpu

ted

as1

–(b

ook

valu

eof

equi

ty/b

ook

valu

eof

asse

ts);

ML,w

hich

isca

lcul

ated

as1

–[m

arke

tva

lue

ofeq

uity

(com

pute

das

num

ber

ofou

tsta

ndin

gsh

ares

*end

ofye

arst

ock

pric

e)/m

arke

tva

lue

ofba

nk(c

ompu

ted

asth

em

arke

tva

lue

ofeq

uity

+boo

kva

lue

oflia

bilit

ies)

];an

dC

OLL,w

hich

isco

mpu

ted

asth

era

tio

bet

wee

nth

esu

mof

the

follo

win

gitem

s:“t

otal

secu

rities

,”“fi

xed

asse

ts,”

and

“cas

han

ddu

efr

omba

nks”

and

the

boo

kva

lue

ofas

sets

.P

ublic

bank

sar

eth

eon

esth

atha

veth

eir

equi

tyqu

oted

/lis

ted

inth

eca

pita

lm

arke

tw

here

aspr

ivat

eba

nks

are

bank

sth

atdo

not

have

thei

req

uity

quot

ed/l

iste

din

the

capi

talm

arke

t.

Vol. 17 No. 3 The Determinants of European Banks’ Capital 173

dropped from 2 to 1 during the same period. While banks’ prof-itability has recovered to a level of around 16 percent up until 2016,market-to-book ratio has never recovered to its pre-crisis level.

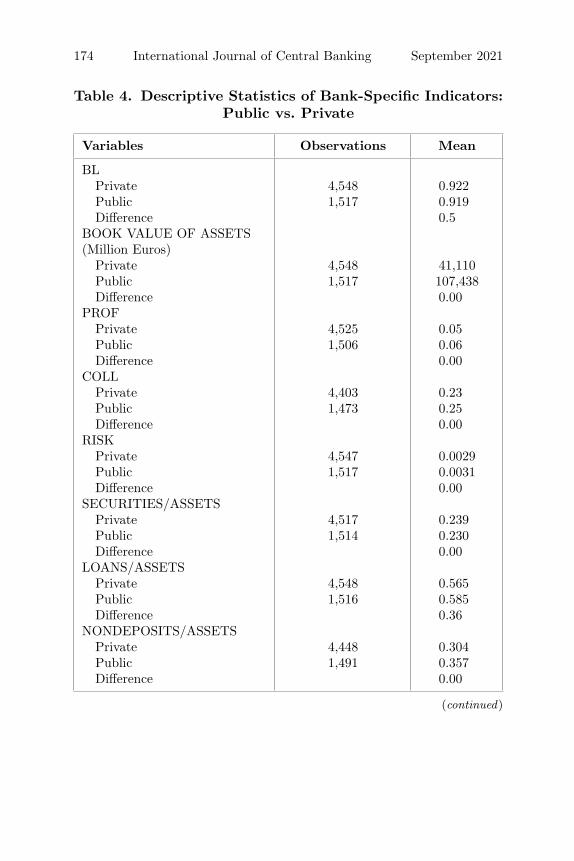

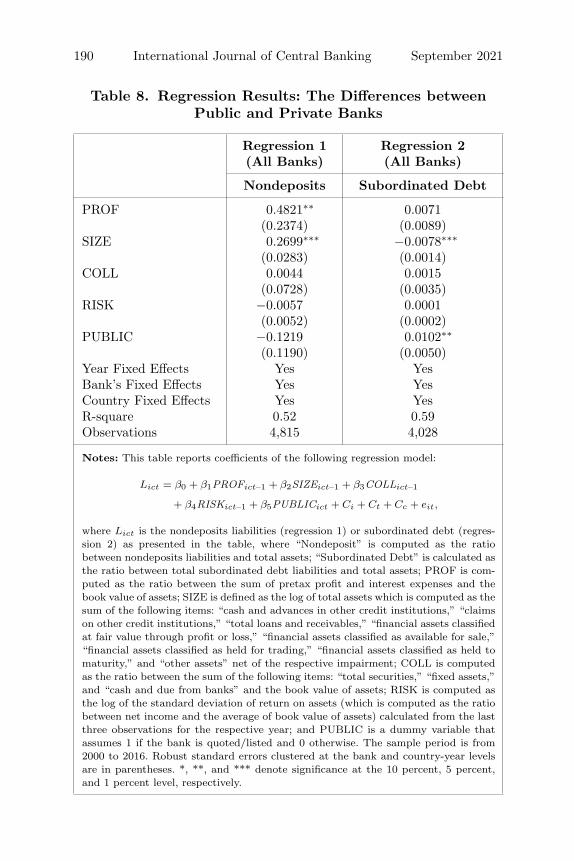

Table 3 also shows that there are significantly more private banksthan public banks, which appears to indicate that the EuropeanBanking System is mainly composed of small and medium-sizedprivate banks, with the sample of public banks being more het-erogeneous than that of private banks—as the standard deviationin several bank-specific indicators is higher in the case of publicbanks. Furthermore, public banks are larger, on average (with aver-age assets of 187 billion euros, when compared with 46 billion eurosfor private banks), although they are more profitable (1 percent-age point above the average profitability of private banks) but lessleveraged (1 percentage point below the average leverage shown byprivate banks) than private banks. These differences are statisti-cally significant when the Wilcoxon signed-rank test is carried out,as shown in table 4. In addition, public banks seem to rely more onnondeposits debt and subordinated debt than private banks. Accord-ing to Flannery (1994), Flannery and Sorescu (1996), Morgan andStiroh (2001), Flannery and Rangan (2008), and Allen, Carletti,and Marquez (2011), this kind of debt is more subject to marketdiscipline than deposits.2

4.2 Cross-Country Comparison Throughout thePeriod 2009–16

This subsection explores the main differences between countries, inparticular the distribution of public and private banks and theircapital composition.

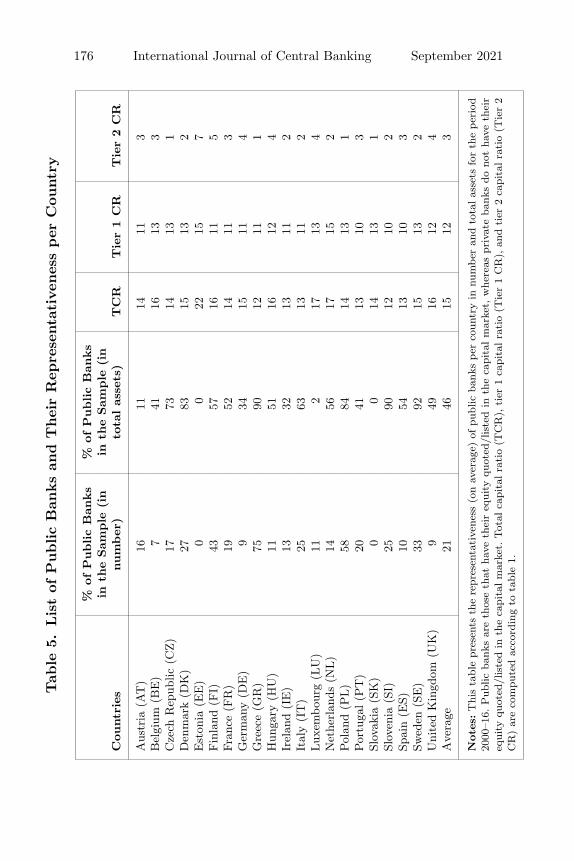

In table 5 we can observe that the percentage of public banksacross European countries for the period of 2000 to 2016, in bothnumber and percentage of total assets of each country’s banking sys-tems, varies significantly, ranging from 0 percent to 75 percent, and0 percent to 92 percent, respectively. It should be added that themajority of banks are private at the European level.

2Some of the differences between the data presented in table 3 and thoseshown in table 4 are due to the fact that the variables presented in table 4 werewindsorized, whereas those presented in table 3 were not.

174 International Journal of Central Banking September 2021

Table 4. Descriptive Statistics of Bank-Specific Indicators:Public vs. Private

Variables Observations Mean

BLPrivate 4,548 0.922Public 1,517 0.919Difference 0.5

BOOK VALUE OF ASSETS(Million Euros)

Private 4,548 41,110Public 1,517 107,438Difference 0.00

PROFPrivate 4,525 0.05Public 1,506 0.06Difference 0.00

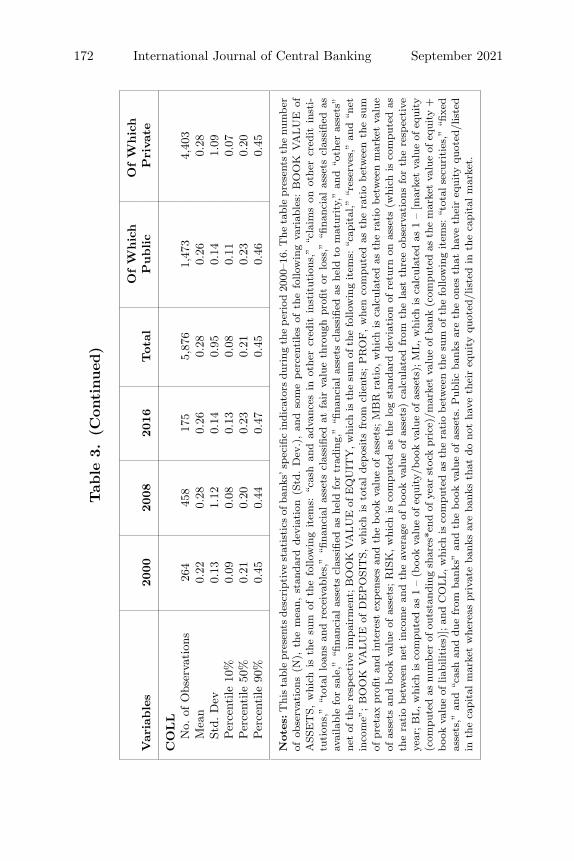

COLLPrivate 4,403 0.23Public 1,473 0.25Difference 0.00

RISKPrivate 4,547 0.0029Public 1,517 0.0031Difference 0.00

SECURITIES/ASSETSPrivate 4,517 0.239Public 1,514 0.230Difference 0.00

LOANS/ASSETSPrivate 4,548 0.565Public 1,516 0.585Difference 0.36

NONDEPOSITS/ASSETSPrivate 4,448 0.304Public 1,491 0.357Difference 0.00

(continued)

Vol. 17 No. 3 The Determinants of European Banks’ Capital 175

Table 4. (Continued)

Variables Observations Mean

SUBORDINATED DEBT/ASSETSPrivate 3,547 0.017Public 1,337 0.018Difference 0.02

Notes: This table presents the main differences between public and private banksregarding the following variables: BL, which is computed as 1 – (book value ofequity/book value of assets); BOOK VALUE of ASSETS, which is the sum of the fol-lowing items: “cash and advances in other credit institutions,” “claims on other creditinstitutions,” “total loans and receivables,” “financial assets classified at fair valuethrough profit or loss,” “financial assets classified as available for sale,” “financialassets classified as held for trading,” “financial assets classified as held to maturity,”and “other assets” net of the respective impairment; PROF, which is computed asthe ratio between the sum of pretax profit and interest expenses and the book valueof assets; COLL, which is computed as the ratio between the sum of the follow-ing items: “total securities,” “fixed assets,” and “cash and due from banks” andthe book value of assets; RISK, which is computed as the log standard deviation ofreturn on assets (which is computed as the ratio between net income and the averageof book value of assets) calculated from the last three observations for the respectiveyear; SECURITIES/ASSETS, which is the ratio between securities and total assets;LOANS/ASSETS, which is the ratio between set loans and total assets; NONDE-POSITS/ASSETS, which is computed as the ratio between nondeposits liabilitiesand total assets; and SUBORDINATED DEBT/ASSETS, which is calculated as theratio between total subordinated debt liabilities and total assets. Each variable waswindsorized at 0.05 on both the left and right tail. We test for the differences betweenthe two types of banks using a nonparametric test of significance knows as Wilcoxonrank-sum test. Public banks are the ones that have their equity quoted/listed inthe capital market, whereas private banks are banks that do not have their equityquoted/listed in the capital market.

Table 5 also shows that a high percentage of public banks (bothin terms of number and with regards to the share of the totalassets of countries’ banking systems) are located in northern andcentral European countries. With a few exceptions, these countriesrepresent those which have the most capitalized banks and alsothose which have shown more access to tier 2 capital instruments—mostly composed of subordinated debt. This feature is in alignmentwith the recent analysis published by the European Central Bank(Gaiduchevici and Zochowski 2017), which stresses that Germanyand France have the largest bank debt markets. In another research

176 International Journal of Central Banking September 2021Tab

le5.

Lis

tof

Public

Ban

ks

and

Thei

rR

epre

senta

tive

nes

sper

Cou

ntr

y

%of

Public

Ban

ks

%of

Public

Ban

ks

inth

eSam

ple

(in

inth

eSam

ple

(in

Cou

ntr

ies

num

ber

)to

talas

sets

)T

CR

Tie

r1

CR

Tie

r2

CR

Aus

tria

(AT

)16

1114

113

Bel

gium

(BE

)7

4116

133

Cze

chR

epub

lic(C

Z)

1773

1413

1D

enm

ark

(DK

)27

8315

132

Est

onia

(EE

)0

022

157

Fin

land

(FI)

4357

1611

5Fr

ance

(FR

)19

5214

113

Ger

man

y(D

E)

934

1511

4G

reec

e(G

R)

7590

1211

1H

unga

ry(H

U)

1151

1612

4Ir

elan

d(I

E)

1332

1311

2It

aly

(IT

)25

6313

112

Lux

embo

urg

(LU

)11

217

134

Net

herl

ands

(NL)

1456

1715

2Pol

and

(PL)

5884

1413

1Por

tuga

l(P

T)

2041

1310

3Sl

ovak

ia(S

K)

00

1413

1Sl

oven

ia(S

I)25

9012

102

Spai

n(E

S)10

5413

103

Swed

en(S

E)

3392

1513

2U

nite

dK

ingd

om(U

K)

949

1612

4A

vera

ge21

4615

123

Note

s:T

his

tabl

epr

esen

tsth

ere

pres

enta

tive

ness

(on

aver

age)

ofpu

blic

bank

sper

coun

try

innu

mber

and

tota

las

sets

for

the

per

iod

2000

–16.

Pub

licba

nks

are

thos

eth

atha

veth

eir

equi

tyqu

oted

/lis

ted

inth

eca

pita

lm

arke

t,w

here

aspr

ivat

eba

nks

dono

tha

veth

eir

equi

tyqu

oted

/lis

ted

inth

eca

pita

lm

arke

t.Tot

alca

pita

lra

tio

(TC

R),

tier

1ca

pita

lra

tio

(Tie

r1

CR

),an

dtier

2ca

pita

lra

tio

(Tie

r2

CR

)ar

eco

mpu

ted

acco

rdin

gto

tabl

e1.

Vol. 17 No. 3 The Determinants of European Banks’ Capital 177

note published by BBVA Research (Garcia and Rocamora 2018),the banks of Greece, Portugal, Ireland, and Spain all display thegreatest shortfalls of MREL—which proves that countries with asmall number of public banks are more likely to be able to overcomedifficulties in complying with MREL requirements.

Attention should be paid to Greece—which recorded a high per-centage of public banks and yet a lower number of tier 2 capitalinstruments—which is an exceptional case, originating from the dra-matic reduction of the number of total banks after the onset of thebanking and sovereign crisis in that country, which led to a con-solidation of Greece’s banking system. However, as they are public,these public banks overcame many difficulties by issuing bail-in-ableinstruments, as a result of concerns regarding the sustainability ofboth Greek banks and the Greek economy as a whole. Estonia is atthe other end of the spectrum, as it has no record of listed banks,although its banking system has the highest percentage of tier 2capital instruments in the sample. This feature could be explainedby the fact that this country is inundated by subsidiaries of foreignbanks, whose listed holding companies have much easier access tocapital markets to fund their activities, and they thus gain from thebenefit of belonging to reputable and well-known banking groups.

5. Methodology

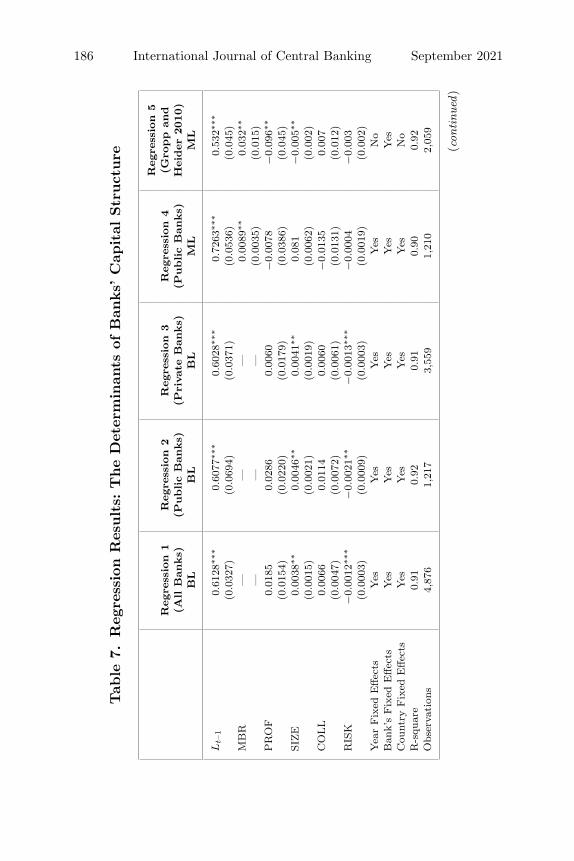

To address the research question presented in section 3, we carry outthe following empirical analysis for year, country, and bank’s fixedeffects:

Lict = β0 + β1PROFict−1 + β2SIZEict−1 + β3COLLict−1

+ β4RISKict−1 + Ci + Ct + Cc + eit,

where Lict is book leverage (BL), and the remaining variables arethose described in table 1. i, c, and t represent bank, country, andtime, respectively, and Ci, Ct, and Cc represent bank, time, andcountry fixed effects. Banks’ specific variables are lagged by one year(as used by Gropp and Heider 2010), in order to mitigate possible

178 International Journal of Central Banking September 2021

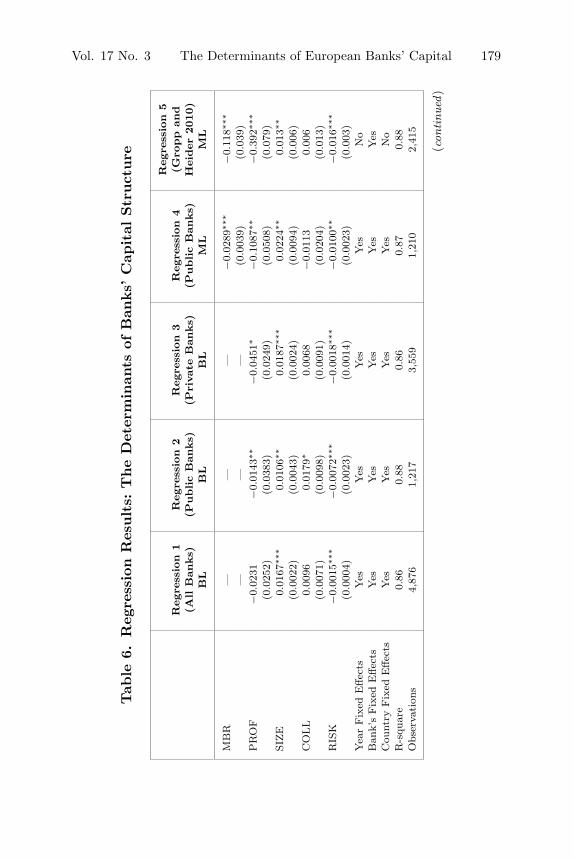

endogeneity problems.3 We ran the model above for all the banks inthe sample, and subsequently distinguished between public and pri-vate banks in the subsamples. As a first step, we apply exactly thesame model to private and public banks, adopting the same depen-dent and explanatory variables for both types of banks (table 6,regressions 2 and 3). Apart from the variables considered above, wenext add the MBR in the case of public banks, and also the marketleverage, rather than use book leverage, as expressed below:

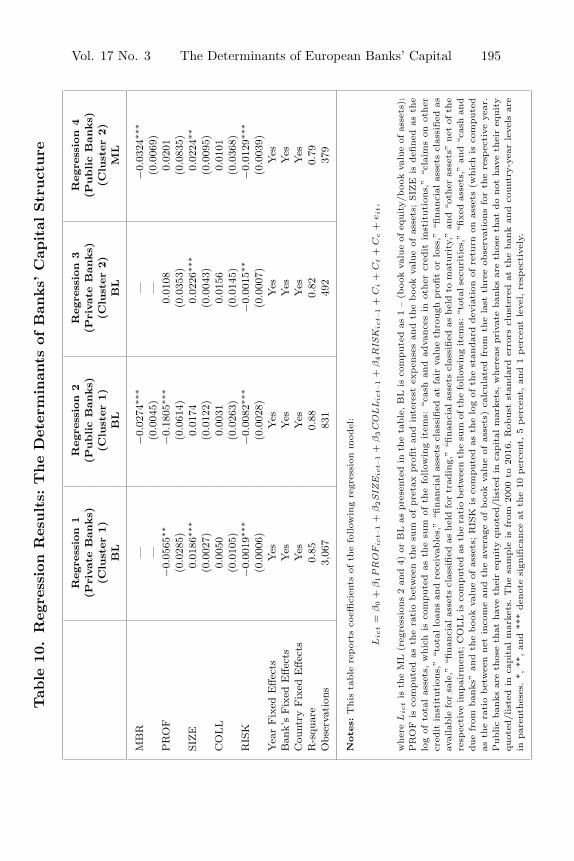

Lict = β0 + β1MBRict−1 + β2PROFict−1 + β3SIZEict−1

+ β4COLLict−1 + β5RISKict−1 + Ci + Ct + Cc + eit.

At a first glance, this second step could undermine the compari-son between public and private banks, as we can observe regressionswith one different dependent variable and one additional explana-tory variable. In order to properly assess the determinants of publicbanks’ capital structure, we opt to consider market values insteadof book values in terms of leverage ratio, as the former are themost frequently used to make decisions in all types of public firms(including banks). Additionally, it is essential to control for market-to-book ratio (MBR) in order to assess the capital structure of listedfirms/banks, as well as to evaluate the behavior of the other deter-minants. Furthermore, by not considering MBR, which is a specialfeature of public firms or banks, we choose to neglect the empiricalwork which has been carried out to date. In particular, the resultsobtained by Gropp and Heider (2010), whose sample was only com-posed of public and large banks, showed that the regressions witha higher R2 (and thus with the greatest explanatory power) werethose which use market leverage as a dependent variable and MBRas one of the explanatory variables. In this paper, the particularitiesof public banks gain even more importance and need to be takeninto consideration, as the sample is more heterogeneous than thatconsidered by Gropp and Heider (2010), which only includes large,public banks.

As in Gropp and Heider (2010), we consider the regulation andsupervision frameworks in year and country’s fixed effects. It should

3We do not include dividends as used by Gropp and Heider (2010) due toavailability issues.

Vol. 17 No. 3 The Determinants of European Banks’ Capital 179

Tab

le6.

Reg

ress

ion

Res

ults:

The

Det

erm

inan

tsof

Ban

ks’

Cap

ital

Str

uct

ure

Reg

ress

ion

5R

egre

ssio

n1

Reg

ress

ion

2R

egre

ssio

n3

Reg

ress

ion

4(G

ropp

and

(All

Ban

ks)

(Public

Ban

ks)

(Pri

vate

Ban

ks)

(Public

Ban

ks)

Hei

der

2010)

BL

BL

BL

ML

ML

MB

R—

——

−0.

0289

∗∗∗

−0.

118∗

∗∗

——

—(0

.003

9)(0

.039

)P

RO

F−

0.02

31−

0.01

43∗∗

−0.

0451

∗−

0.10

87∗∗

−0.

392∗

∗∗

(0.0

252)

(0.0

383)

(0.0

249)

(0.0

508)

(0.0

79)

SIZE

0.01

67∗∗

∗0.

0106

∗∗0.

0187

∗∗∗

0.02

24∗∗

0.01

3∗∗

(0.0

022)

(0.0

043)

(0.0

024)

(0.0

094)

(0.0

06)

CO

LL

0.00

960.

0179

∗0.

0068

−0.

0113

0.00

6(0

.007

1)(0

.009

8)(0

.009

1)(0

.020

4)(0

.013

)R

ISK

−0.

0015

∗∗∗

−0.

0072

∗∗∗

−0.

0018

∗∗∗

−0.

0100

∗∗−

0.01

6∗∗∗

(0.0

004)

(0.0

023)

(0.0

014)

(0.0

023)

(0.0

03)

Yea

rFix

edE

ffec

tsYes

Yes

Yes

Yes

No

Ban

k’s

Fix

edE

ffec

tsYes

Yes

Yes

Yes

Yes

Cou

ntry

Fix

edE

ffec

tsYes

Yes

Yes

Yes

No

R-s

quar

e0.

860.

880.

860.

870.

88O

bser

vation

s4,

876

1,21

73,

559

1,21

02,

415

(con

tinu

ed)

180 International Journal of Central Banking September 2021

Tab

le6.

(Con

tinued

)

Note

s:T

his

tabl

ere

por

tsco

effici

ents

ofth

efo

llow

ing

regr

essi

onm

odel

s:

Lic

t=

β0

+β1PRO

Fic

t–1

+β2SI

ZE

ict–

1+

β3C

OLL

ict–

1+

β4R

ISK

ict–

1+

Ci+

Ct+

Cc

+e i

t

Lic

t=

β0

+β1M

BR

ict–

1+

β2PRO

Fic

t–1

+β3SI

ZE

ict–

1+

β4C

OLL

ict–

1+

β5R

ISK

ict–

1+

Ci+

Ct+

Cc

+e i

t,

whe

reL

ict

isth

eM

L(r

egre

ssio

ns4

and

5)or

BL

aspr

esen

ted

inth

eta

ble,

BL

isco

mpu

ted

as1

–(b

ook

valu

eof

equi

ty/b

ook

valu

eof

asse

ts);

ML

isca

lcul

ated

as1

–[m

arke

tva

lue

ofeq

uity

(com

pute

das

num

ber

ofou

tsta

ndin

gsh

ares

*end

ofye

arst

ock

pric

e)/m

arke

tva

lue

ofba

nk(c

ompu

ted

asth

em

arke

tva

lue

ofeq

uity

+boo

kva

lue

oflia

bilit

ies)

];M

BR

isca

lcul

ated

asth

era

tio

bet

wee

nm

arke

tva

lue

ofas

sets

and

boo

kva

lue

ofas

sets

;P

RO

Fis

com

pute

das

the

ratio

bet

wee

nth

esu

mof

pret

axpr

ofit

and

inte

rest

expen

ses

and

the

boo

kva

lue

ofas

sets

;SI

ZE

isde

fined

asth

elo

gof

tota

las

sets

whi

chis

com

pute

das

the

sum

ofth

efo

llow

ing

item

s:“c

ash

and

adva

nces

inot

her

cred

itin

stitut

ions

,”“c

laim

son

othe

rcr

edit

inst

itut

ions

,”“t

otal

loan

san

dre

ceiv

able

s,”

“fina

ncia

las

sets

clas

sifie

dat

fair

valu

eth

roug

hpr

ofit

orlo

ss,”

“fina

ncia

las

sets

clas

sifie

das

avai

labl

efo

rsa

le,”

“fina

ncia

las

sets

clas

sifie

das

held

for

trad

ing,

”“fi

nanc

ialas

sets

clas

sifie

das

held

tom

atur

ity,

”an

d“o

ther

asse

ts”

net

ofth

ere

spec

tive

impa

irm

ent;

CO

LL

isco

mpu

ted

asth

era

tio

bet

wee

nth

esu

mof

the

follo

win

gitem

s:“t

otal

secu

rities

,”“fi

xed

asse

ts,”

and

“cas

han

ddu

efr

omba

nks”

and

the

boo

kva

lue

ofas

sets

;an

dR

ISK

isco

mpu

ted

asth

ean

nual