tesco profile 2007 (hr)

TRANSCRIPT

GENER AL RETAIL

Tesco is Britain’s leading food retailer and the third largest

in the world. Its first store was opened in 1929 in London

and by the early 1960s Tesco was a familiar feature of

most UK high streets. After joining the eighties trend for

large out-of-town supermarkets, in the 1990s the

company started pioneering many new innovations. It

developed new store concepts such as Tesco Metro, a city

centre store meeting the needs of local shoppers, and

Tesco Express, the first UK petrol station convenience

store. In 1995 the company introduced its Clubcard, the

UK’s first customer loyalty card, and two years later

formed a joint venture with the Royal Bank of Scotland to

offer a range of financial services. 2000 marked the start

of Tesco.com which was built on the back of existing

stores and, with low capital spend, was profitable from

the start – a key internal requirement. Tesco’s

international operation, which started in 1994, has

steadily expanded and now accounts for half of its total

retail space. Since 2000 there has also been an increasing

focus on building non-food sales both in store and online

with the result that, for example, Tesco is now the UK’s

largest CD retailer.

Pragmatic, customer focusedinnovation, driven bytangible insights anddelivered with class-leadingefficiency

TESCO

Book page layout 2007 (AW).qxd:Book page layout.qxd 29/3/08 22:58 Page 106

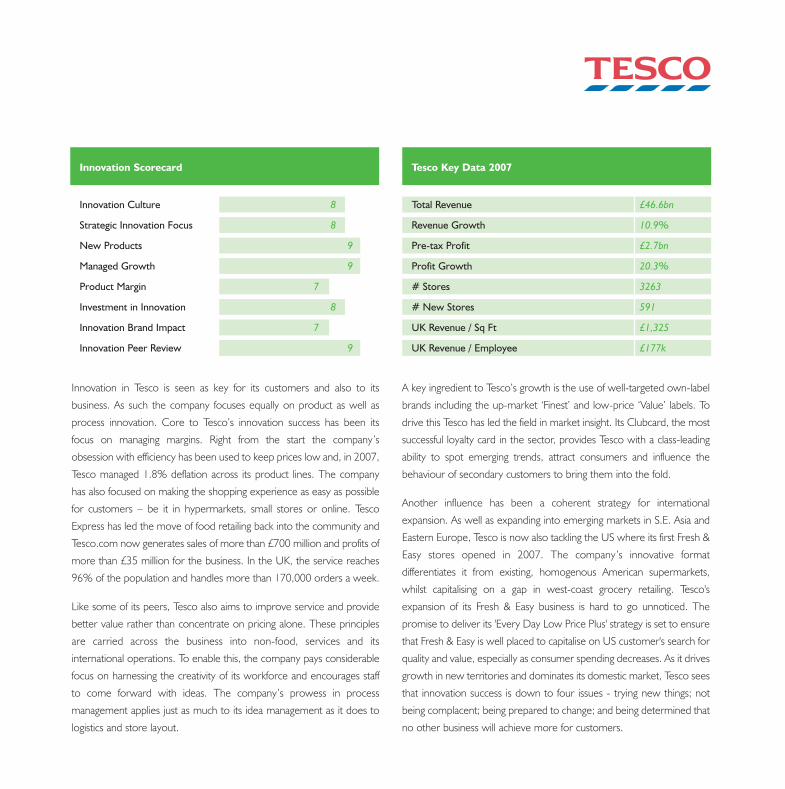

Innovation in Tesco is seen as key for its customers and also to its

business. As such the company focuses equally on product as well as

process innovation. Core to Tesco’s innovation success has been its

focus on managing margins. Right from the start the company’s

obsession with efficiency has been used to keep prices low and, in 2007,

Tesco managed 1.8% deflation across its product lines. The company

has also focused on making the shopping experience as easy as possible

for customers – be it in hypermarkets, small stores or online. Tesco

Express has led the move of food retailing back into the community and

Tesco.com now generates sales of more than £700 million and profits of

more than £35 million for the business. In the UK, the service reaches

96% of the population and handles more than 170,000 orders a week.

Like some of its peers, Tesco also aims to improve service and provide

better value rather than concentrate on pricing alone. These principles

are carried across the business into non-food, services and its

international operations. To enable this, the company pays considerable

focus on harnessing the creativity of its workforce and encourages staff

to come forward with ideas. The company’s prowess in process

management applies just as much to its idea management as it does to

logistics and store layout.

A key ingredient to Tesco’s growth is the use of well-targeted own-label

brands including the up-market ‘Finest’ and low-price ‘Value’ labels. To

drive this Tesco has led the field in market insight. Its Clubcard, the most

successful loyalty card in the sector, provides Tesco with a class-leading

ability to spot emerging trends, attract consumers and influence the

behaviour of secondary customers to bring them into the fold.

Another influence has been a coherent strategy for international

expansion. As well as expanding into emerging markets in S.E. Asia and

Eastern Europe, Tesco is now also tackling the US where its first Fresh &

Easy stores opened in 2007. The company’s innovative format

differentiates it from existing, homogenous American supermarkets,

whilst capitalising on a gap in west-coast grocery retailing. Tesco's

expansion of its Fresh & Easy business is hard to go unnoticed. The

promise to deliver its 'Every Day Low Price Plus' strategy is set to ensure

that Fresh & Easy is well placed to capitalise on US customer's search for

quality and value, especially as consumer spending decreases. As it drives

growth in new territories and dominates its domestic market, Tesco sees

that innovation success is down to four issues - trying new things; not

being complacent; being prepared to change; and being determined that

no other business will achieve more for customers.

Tesco Key Data 2007

Total Revenue £46.6bn

Revenue Growth 10.9%

Pre-tax Profit £2.7bn

Profit Growth 20.3%

# Stores 3263

# New Stores 591

UK Revenue / Sq Ft £1,325

UK Revenue / Employee £177k

Innovation Scorecard

Innovation Culture 8

Strategic Innovation Focus 8

New Products 9

Managed Growth 9

Product Margin 7

Investment in Innovation 8

Innovation Brand Impact 7

Innovation Peer Review 9

Book page layout 2007 (AW).qxd:Book page layout.qxd 29/3/08 22:58 Page 107

SECTOR OVERVIEW

The supermarket and the one-stop-shop transformed the dynamics

of the food and general retail sectors. Pioneered by the likes of

Sainsbury’s, Safeway, Carrefour and Wal-Mart, the advantages are

clear; securing large volume discounts allows supermarkets to under-

cut traditional stores and greater space means they can offer as good

if not better selection of produce. In recent years, there has been a

focus on multi-format capability and blurring of formats as retailers

‘mix and match’ to increase effectiveness and offer customers a

reason to shop at their stores. Linked to issues such as out-of-town

planning constraints this has led to consolidation including the

opening of smaller stores within communities, the incorporation of

pharmacies, post offices and travel agencies, joint retail ventures with

the likes of BP, Shell and Exxon and the growth of on-line shopping.

In addition, the rise of own-label products and an increasing

migration to non-food have fundamentally changed the product mix.

By 2010, the value of the European private label market is forecast

to reach €430.8 billion, up from €298.1 billion in 2005.

With price deflation and commoditisation a threat in most markets,

genuine innovation remains the key for many retailers. In more

mature markets there is a growing appreciation that a 'one size fits

all' approach is no longer valid. Some retailers are adapting by

focusing on other differentiation than just price using new channels

to develop tailored products and services to suit more sophisticated

customer requirements. Growing consumer spending and a hunger

for modern retail in emerging markets such as China, India and Russia

also provide significant opportunities for growth. Large international

and regional grocers are acquiring market share across the world at

a remarkable rate with the top 100 retailers already capturing 45%

of the world's modern grocery distribution. Companies like Wal-

Mart, Ahold, Carrefour and Tesco now face the challenge of

managing increasingly complex supply chains, building critical volume

in different countries and maintaining comparable levels of product

quality and customer experience.

Book page layout 2007 (AW).qxd:Book page layout.qxd 29/3/08 22:58 Page 108

In this highly competitive arena, innovation is rife. From introducing new

technology and broadening the product portfolio to positioning the

brand and deepening customer relationships, there are several key

drivers gaining widespread attention. Today’s two main technological

sources of innovation are the on-line provisions market and an

improved supply chain-focused technology such as smart tags. Both are

addressing improved efficiency of goods supply and provision, but are

also areas of consumer-focused innovation around convenience and

traceability. In terms of broadening the product mix, the migration of

food to general product supply has been followed by service

development using the retailer brand as the focal point. Starting with a

limited range of joint venture financial products, this has spread to loans,

insurance, holidays, car retail and, most recently, energy supply, virtual

mobile phone operations and real estate. All are usually delivered in

partnership with leading existing suppliers, but are positioned around

the increasing levels of trust that consumers have with their favorite

retail brand.

Many retailers are using the migration of their loyalty cards into their

joint venture services and relationships such as Nectar in the UK to gain

new information about their wider customer base that feeds into

detailed segmentation analysis and opportunities for cross selling.

Retailers can now find out what their customers spend their money on

outside the store and can use this to develop new branded service

propositions and improve the levels of cross-selling between groups.

Together these are all providing the leading retailers with the

opportunity to take consumer-centric innovation to a whole new level.

Lastly, as efficiency is such a driver of margins in this sector, internal

process innovation is a correspondingly key area of focus. Customers

largely see the visible impacts from innovation in terms of new products,

services, store layouts and website usability. But as new technologies hit

the supply chain it is the companies that can best manage the flow of

materials that will win the day. As such an efficient IT infrastructure is

vital and this has been a major area of spend in recent years for the

main players.

INNOVATION DRIVERS

Wal-Mart

The world’s largest retailer has been through a number of challenges

over recent years but is now making a major success of its innovation

focus on the sustainability agenda: Wal-Mart has an ambitious strategy to

reinvent itself as a champion of the environment. The company plans to

eliminate 30% of the energy used in stores, reduce solid waste from its

U.S. stores by 25% within three years, and invest up to $500 million in

sustainability projects. Wal-Mart is creating competition in its supply base

around being green that is already having significant impact on

innovation in packaging and waste management.

WuMart

At the other end of the scale at the moment, China’s WuMart is seen

by some as the future of retail. The company has only been around

since 1994, and although only having $320m of sales and 500 stores at

the moment, this is one of the fastest growing retailers in China with

grand expansion plans and a different take on customer service. The

company tailors stores to suit local tastes and fresh food is a major

feature, aware, for example, shoppers can pick live fish to have for

dinner. With 700% growth predicted for retailing in China alone over

the next decade, WuMart is intent of having a major role in this.

ONES WE ARE WATCHING

GENERAL RETAIL

Book page layout 2007 (AW).qxd:Book page layout.qxd 29/3/08 22:58 Page 109