mortgage lending and hoepa - american bankers association

TRANSCRIPT

What the New Rules on

Mortgage Lendingand HOEPA

Mean to Your Bank

1-800-BANKERS

www.aba.com

ABA MEMBERS ONLY

ABAW rkson Regulation Z

ABAWorks on Mortgage ReformIn July, 2008, the Federal Reserve amended Regulation Z, which implements the Truth in Lending Act and the HomeOwnership Equity Protection Act. The effective date is October 2009, except for the early disclosure provisions, which mustbe implemented by July 2009. In addition to new regulations that apply to all mortgage loans in areas such as appraisals,servicing, disclosure, and advertising, the new regulation also creates a new subset of loans considered to be “higher-pricedmortgage loans.” For many banks, this definition will include subprime loans as well as some loans previously considered to beprime loans.

This ABAWorks is designed to help you better understand and make decisions about whether and how to offer “higher-pricedmortgage loans” and to help you reorganize your compliance framework to take into account the new requirements that applyto all mortgages.

Who Should Read This ABAWorks?ABAWorks on Mortgage Reform is designed to help bank presidents, CEOs and chief compliance officers understand the scopeof the guidance and how to reorganize your compliance framework to ensure compliance with the new regulation. Any bankthat offers residential mortgages of all types — both prime and subprime — should read this ABAWorks. Besides seniormanagement, the guidance also focuses on the role of the Board of Directors, and we encourage you to use sections of thisABAWorks to advise your directors about ways they might be affected by the new regulations. ABAWorks is not a legal treatise,and you should always consult your bank’s counsel about any questions you have concerning the law.

How is This ABAWorks Organized?There are five sections to this ABAWorks. The first section presents a snapshot of the regulation and presents the case that allbanks should review these new regulations, even if they don’t currently make subprime loans. Because the new definition of“higher priced mortgage loans” picks up some prime loans, it’s critical to ascertain whether the mortgage loans you make arecovered under the regulation. The second section reviews the evolution of less-than-prime lending and why the FederalReserve Board determined it was necessary to implement new regulations regarding mortgage lending. The third section coversthe new category of “higher-priced mortgage loans.” This section includes a detailed definition of that loan category and adescription of all of the compliance issues associated with it. The fourth section covers the new regulations that will now beapplied to all mortgage lending, regardless of rate. The fifth section contains a framework and checklists to guide bank effortsto comply with the new rules.

The American Bankers Association brings together banks of all sizes and charters into one association. ABA works to enhance the competitiveness of the nation’s banking industry and strengthen America’s economy and communities. Its members — the majority of which are banks with less than $125 millionin assets — represent over 95 percent of the industry’s $13.6 trillion in assets and employ over two million men and women.

© 2009 American Bankers Association, Washington, D.C.

This publication was paid for in part with the dues of ABA member financial institutions and is intended solely for their use. Please call 1-800-BANKERS if you have any questions about this resource, ABA membership or would like to copy or license any part of this publication.

This publication is designed to provide accurate information on the subject addressed. It is provided with the understanding that neither the authors, contributors nor the publisher is engaged in rendering legal, accounting or other expert or professional services. If legal or other expert assistance is required,the services of a competent professional should be sought. This guide in no way intends or effectuates a restraint of trade or other illegal concerted action.

BANKER ADVISORS & REVIEWERS

C. AngelottiExecutive AssistantInsignia BankSarasota, FL

Tracy R. ArmstrongVice President - Lending ComplianceManagerGuaranty BankAustin, TX

Paul G. Balaschak, CMBVice President, Lending Compliance,CRA OfficerFirst Federal Bank of CaliforniaLos Angeles, CA

Howard T. Boyle IIPresident & CEOHome Savings BankKent, OH

Brian BrandtVice President - ComplianceGuaranty BankAustin, TX

Charles G. Brown IIIChairman & CEOInsignia BankSarasota, FL

Dennis CardelloPresident & CEOCollinsville Savings SocietyCanton, CT

William Grant Chairman & CEOFirst United Bank & TrustOakland, MD

Richard T. NadolskiSenior Vice PresidentNorth Shore BankBrookfield, WI

Larry S. KesselTrust Vice President and Loan OfficerFirst United Bank & TrustOakland, MD

Kenneth WitteVice President & DirectorFirst United Bank & TrustOakland, MD

ABA STAFF CONTRIBUTORS

Jim ChessenChief Economist

Susan EinfaltSenior Designer

Mako ParkerSenior Program Manager

Ellen CollierManager

Deanne MariñoWriter/Policy Analyst

Rod AlbaVP & Senior Regulatory Counsel

Richard RieseSVP, Center for Regulatory Compliance

Mark TenhundfeldSVP, Regulatory Policy

Ginny O’NeillSenior Counsel I

Rachaell DavisSenior Program Assistant

Ryan ZagoneSenior Research Assistant

Bob DavisExecutive Vice President

CONSULTANTS

Jeffrey P. NaimonPartnerBuckley Kolar, LLPWashington, DC

Thomas Pinkowish PresidentCommunity Lending Associates, LLCEssex, CT

Suzanne GarwoodAssociate Venable LLPWashington, DC

Special thanks to Krista Shonk, who began this project at ABA before moving to a new position at Freddie Mac.

What the New Rules on MortgageLending and HOEPA Mean to Your Bank

SECTION ONE

Executive Summary 1

SECTION TWO

The Evolution of Less-Than-Prime Mortgage Lending 5

SECTION THREE

Higher-Priced Mortgage Loans (§ 226.32-226.35) 11

SECTION FOUR

Requirements Applicable to Mortgage Loans Regardless of Rate 29

SECTION FIVE

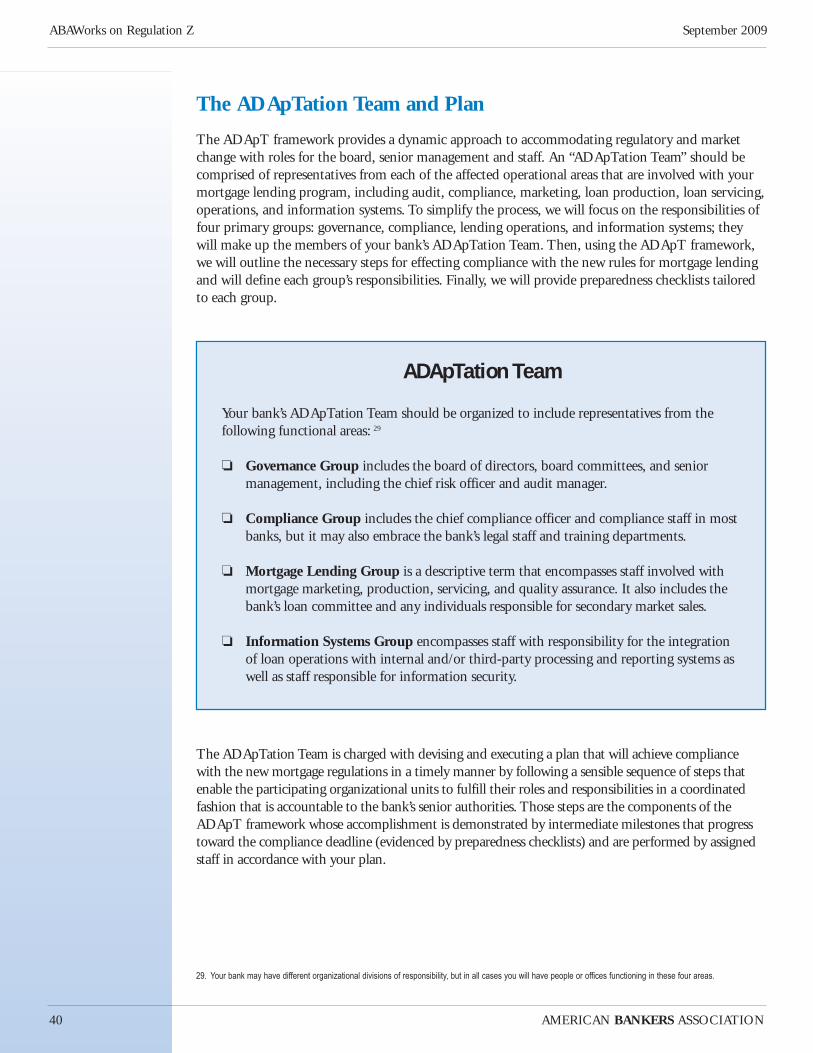

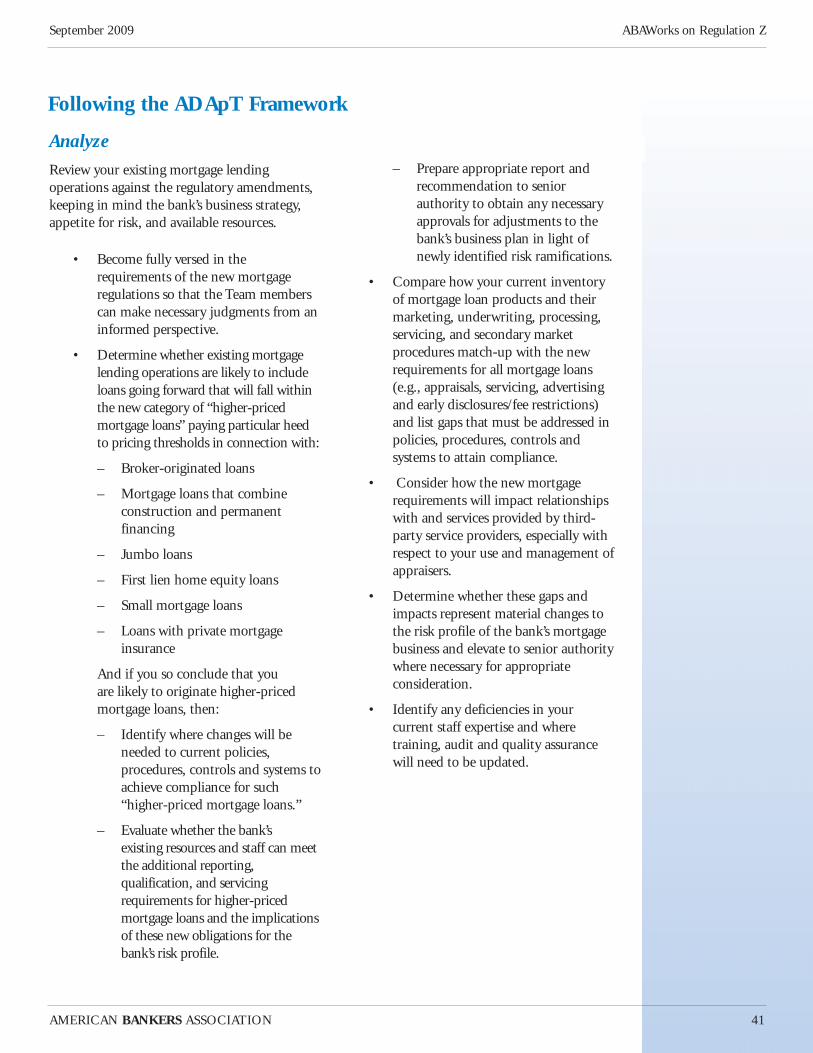

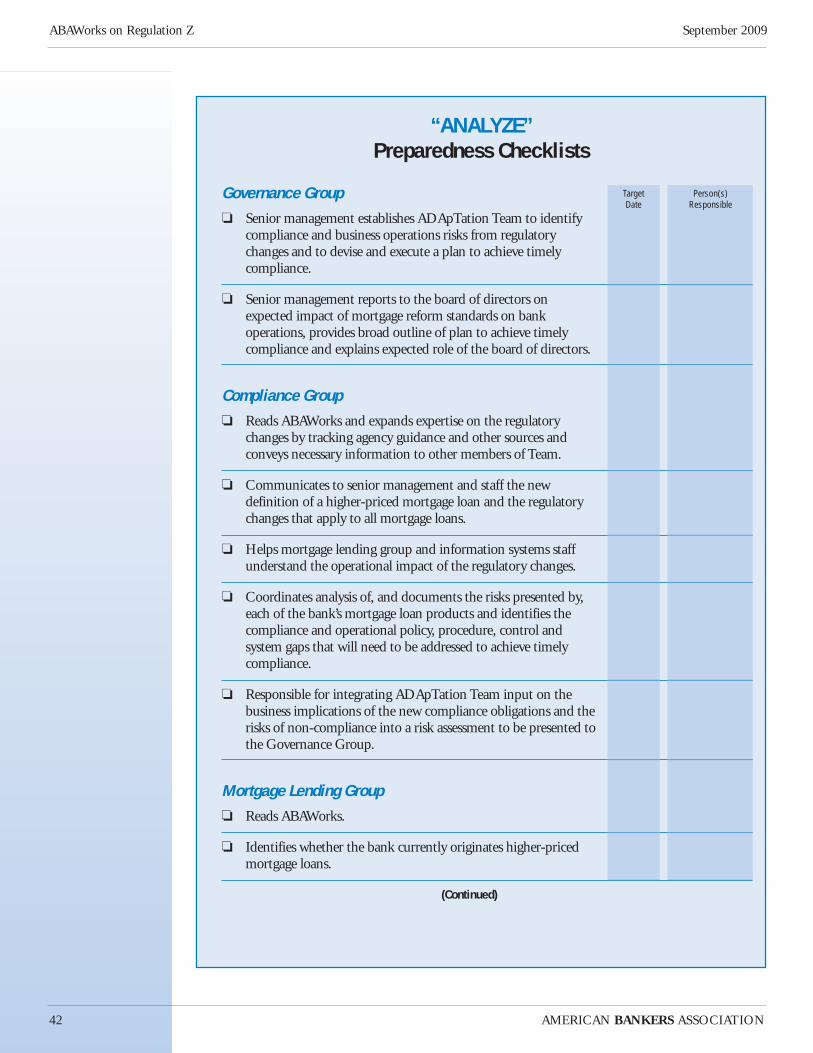

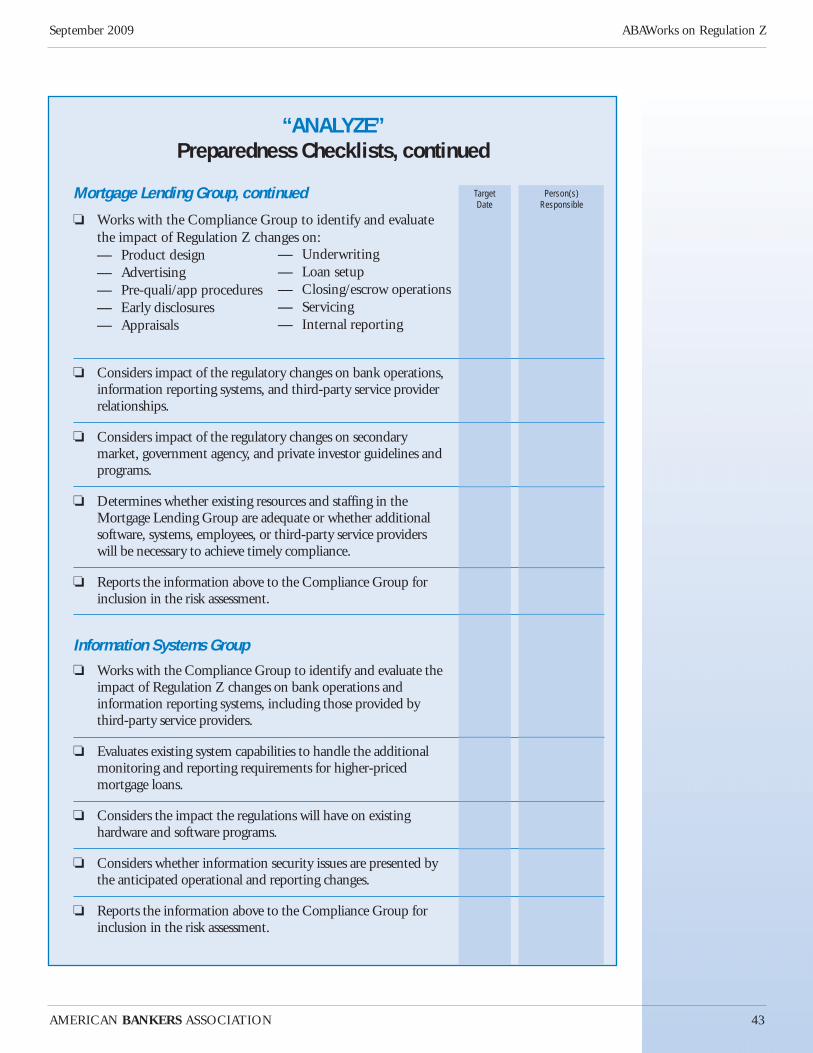

ADApT to Mortgage Reform: A Framework for Achieving Compliance 39

APPENDICES

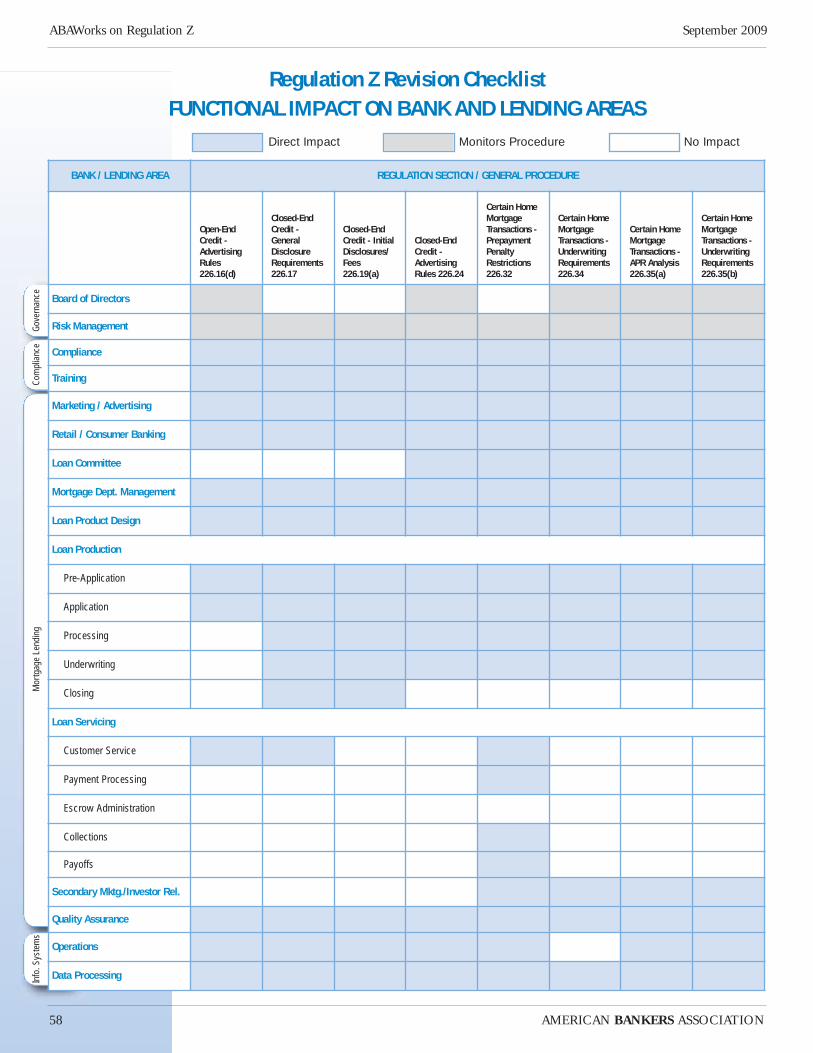

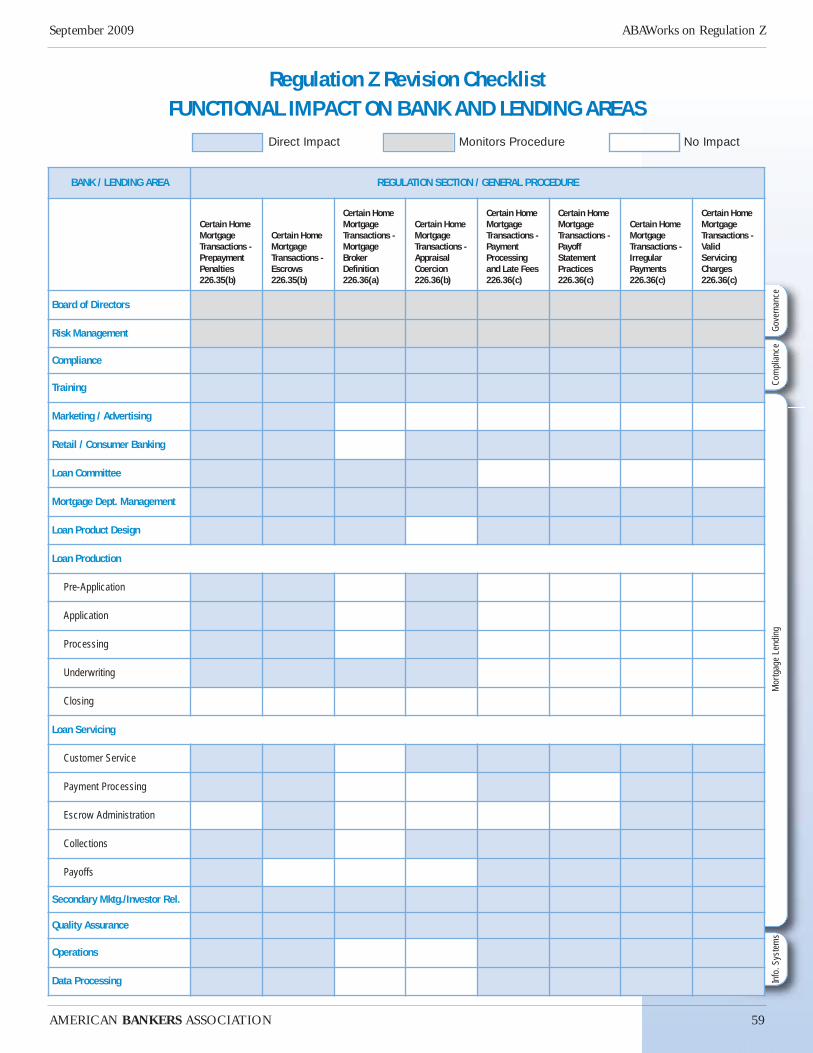

Appendix A: Methodology for Determining Average Prime Offer Rates 53Appendix B: Functional Impact on Bank and Lending Areas 57

In the past few years, many mortgage loanswere extended that were poorly underwrittenor whose terms were inadequately disclosed ... The resulting costs have been felt not only byborrowers but also by entire communities ... The decline in the national housing market,which has been a major cause of the broaderslowdown in economic activity, was in turngreatly exacerbated by the collapse of subprime lending.

Federal Reserve Board Chairman Ben BernankeJuly 8, 2008

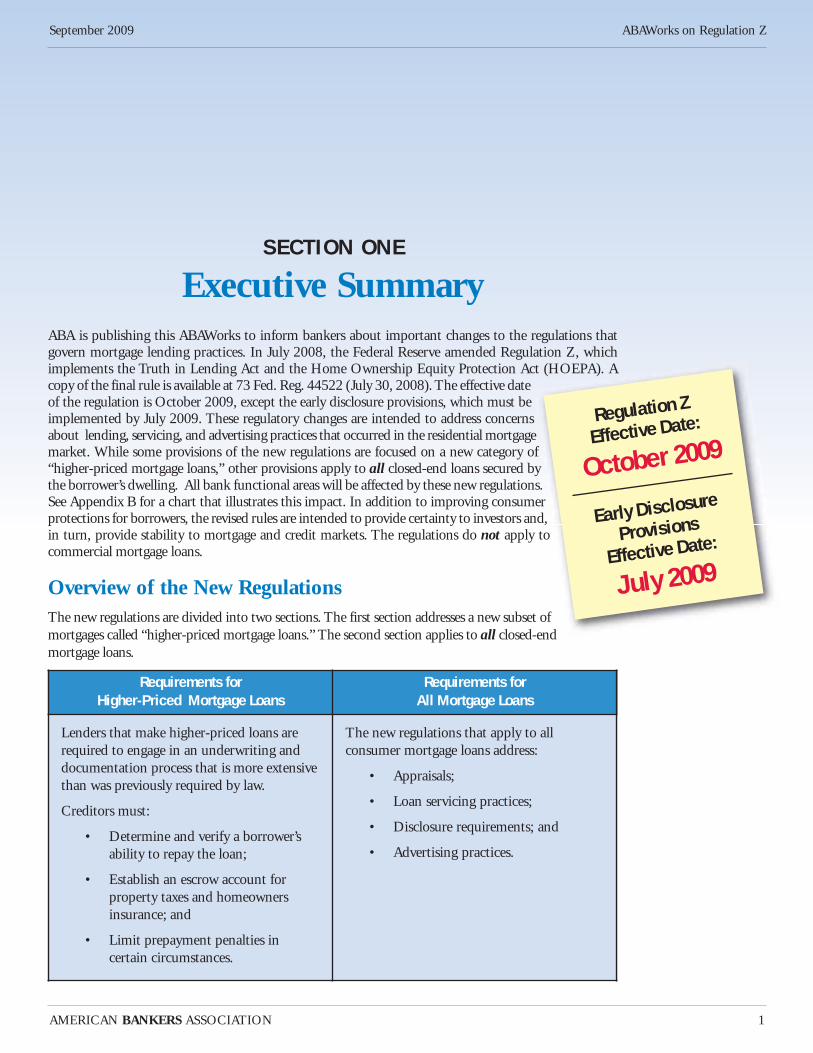

Requirements for Higher-Priced Mortgage Loans

Requirements for All Mortgage Loans

Lenders that make higher-priced loans arerequired to engage in an underwriting anddocumentation process that is more extensivethan was previously required by law.

Creditors must:

• Determine and verify a borrower’sability to repay the loan;

• Establish an escrow account forproperty taxes and homeownersinsurance; and

• Limit prepayment penalties incertain circumstances.

The new regulations that apply to allconsumer mortgage loans address:

• Appraisals;

• Loan servicing practices;

• Disclosure requirements; and

• Advertising practices.

AMERICAN BANKERS ASSOCIATION

September 2009 ABAWorks on Regulation Z

1

SECTION ONE

Executive SummaryABA is publishing this ABAWorks to inform bankers about important changes to the regulations thatgovern mortgage lending practices. In July 2008, the Federal Reserve amended Regulation Z, whichimplements the Truth in Lending Act and the Home Ownership Equity Protection Act (HOEPA). Acopy of the final rule is available at 73 Fed. Reg. 44522 (July 30, 2008). The effective dateof the regulation is October 2009, except the early disclosure provisions, which must beimplemented by July 2009. These regulatory changes are intended to address concernsabout lending, servicing, and advertising practices that occurred in the residential mortgagemarket. While some provisions of the new regulations are focused on a new category of“higher-priced mortgage loans,” other provisions apply to all closed-end loans secured bythe borrower’s dwelling. All bank functional areas will be affected by these new regulations.See Appendix B for a chart that illustrates this impact. In addition to improving consumerprotections for borrowers, the revised rules are intended to provide certainty to investors and,in turn, provide stability to mortgage and credit markets. The regulations do not apply tocommercial mortgage loans.

Overview of the New RegulationsThe new regulations are divided into two sections. The first section addresses a new subset ofmortgages called “higher-priced mortgage loans.” The second section applies to all closed-end mortgage loans.

Regulation Z

Effective Date:

October 2009

Early Disclosure

Provisions

Effective Date:

July 2009

AMERICAN BANKERS ASSOCIATION

ABAWorks on Regulation Z September 2009

2

Why Read This ABAWorks?

• You may make higher-priced loans even though you are not a subprime lender.

• The regulation may require changes to your loan policy.

• Non-compliance could be costly — violating the new requirements can subject lenders toadministrative action and litigation, including special damages and class action lawsuits.

• Utilize checklists provided to help comply with the regulation.

• Get examples of how to comply with new underwriting requirements.

• Gather tips for implementing an escrow system.

• Learn about new advertising and disclosure requirements.

• Make sure you don’t violate restrictions on prepayment penalties.

The Higher-Priced Loan Regulations Will Impact All Banks

In general, the new requirements for higher-priced loans were crafted to apply to all subprime loans,though the scope of the rule may be sufficiently broad to reach to some segments of the primemarket as well. That means that the new regulations may impact lenders that make only prime,conforming loans as well as subprime lenders. Thus, it will require all lenders to ascertain whetherany loan they make is covered by these requirements. Based on current market rates, there is someevidence that some prime products will be classified as higher-priced loans.

The penalties for non-compliance could be severe — including the possibility of both expensivebank-specific penalties and class action litigation. As a result, it is important that all lenders assesstheir current loan policies and practices to ensure they can identify all higher-priced loans that theyoriginate and to ensure that any such loans conform to the new regulatory requirements. Someinstitutions may elect not to make higher-priced loans in order to avoid potential legal andreputation risks associated with these kinds of loans. Institutions that elect not to make higher-pricedloans should consider implementing a monitoring system in order to flag any loans thatunintentionally cross the threshold for higher-priced loans and should ensure that such an electiondoes not inadvertently create or exacerbate fair lending or Community Reinvestment Act issues.

This ABAWorks summarizes the new regulations and provides practical information that will helpbanks to comply with the new requirements.

AMERICAN BANKERS ASSOCIATION

September 2009 ABAWorks on Regulation Z

3

Snapshot of the New Mortgage Lending Regulations

Effective Date: October 1, 2009

Requirements for Higher-Priced Loans Requirements for All Mortgage Loans

• Repayment: Creditors must determineand verify a borrower’s ability to repaythe loan.

• Escrow: An escrow account for propertytaxes and homeowners insurance isrequired for at least the first 12 monthsof the loan.

• Prepayment Penalties: Prepaymentpenalties are limited in certaincircumstances.

• Structuring: A creditor may notstructure a higher-priced loan as an open-end loan to evade the regulation.

• Appraisals: Creditors and mortgagebrokers cannot coerce or improperlyinfluence appraisers to misrepresent thevalue of a home. In addition, a creditorcannot extend credit if it knows or hasreason to know that a broker has coercedan appraiser.

• Servicing:Loan servicers:– Must credit a payment to a borrower

on the date it is received.– Must provide a payoff-statement

within a reasonable time afterreceiving a request for suchinformation — typically five days.

– Are prohibited from “pyramiding”late fees.

• Advertising: Advertisements for closed-end and open-end mortgage credit mustinclude additional information aboutbuy-downs, variable and promotionalrate transactions, and balloon payments.Alternative disclosures are permitted fortelevision and radio advertisements.

• Early Disclosures/Early Fee Restriction:Creditors must provide a good faithestimate of loan costs within three daysafter a borrower applies for a closed-endmortgage loan that is secured by aborrower’s dwelling. Consumers cannotbe charged any fee until after they receivethe early disclosures, except a reasonablefee for obtaining a credit report. (Theseprovisions were amended by the Housingand Economic Recovery Act of 2008 andmust be implemented by July 2009. Seepage 35 for more information.)

In recent years, mortgage markets have seen aremarkable wave of financial innovation. … Butsome of these innovations also have negativeaspects … The Board is responding to theseproblems with proposed rules that were carefullycrafted with an eye toward deterring improperlending and advertising practices withoutunduly restricting mortgage credit availability.

Federal Reserve Board Chairman Ben BernankeDecember 18, 2007

The year 2008 will go down as one of the mostvolatile periods in history for financial markets.Economic growth has stopped and economiesaround the world are in recession. While manyfactors contributed to this collapse of confidence,the precipitating event was the bursting of thehouse price bubble that had been ballooning inmany areas of the U.S. and, indeed, around theglobe. No one could predict just how widespreadthe collapse of home prices would be felt — orthat it would reverberate throughout so much ofthe financial world.

Though amendments to Regulation Z weren’tcreated to address the economic collapse, theFederal reserve was looking to use its authorityunder the Truth in Lending Act and the HomeOwnership and Equity Protection Act to addresssome concerns that led to the house price bubbleand the accompanying overextension of credit thatensued. The Federal Reserve pointed to threeprimary areas of concern:

• Escalating mortgage delinquency and default rates for subprime and Alt-A (nearprime/nonconforming) mortgages;

• The loosening of underwriting standardsover the course of the real estate boom,especially among nondepository financialinstitutions; and

• Increased market imperfections, particularlymortgage product complexity, that made itharder for borrowers to protect themselves.

The United States mortgage industry, particularlysince the 1980s, has dramatically increased itsvolume and variety of products, greatly enhancingthe ability of individuals to become homeowners.

Upon the release of the final regulation, on July14, 2008, Chairman Ben Bernanke praised themortgage market’s “financial innovation” for theincreased capital allowed by a large secondarymarket and the widening access to credit thatcapital enabled. However, he also noted that theseinnovations have brought “negative aspects,” aswell. Particularly, he commented that, “[a]s themortgage market has become more segmentedand as risk has become more dispersed, marketdiscipline has in some cases broken down and theincentives to follow prudent lending procedureshave, at times, eroded.”

Of course, the events since last July when theregulation was released has demonstrated justhow dramatic the consequences can be. TheFederal Reserve did note that nondepositoryfinancial institutions were competingaggressively for market share, seeking clientswho may not have qualified for a mortgagepreviously. Many of these homebuyers werebarely able to make the initial mortgagepayment, as some lenders allowed inflatedincome estimates to pass through theunderwriting process. Such buyers were at ahigh risk of default when adjustable interestrates reset higher.

Another element to this mix, from theperspective of the Federal Reserve, were“market imperfections” that could “make itharder for consumers to protect themselvesfrom abusive or unaffordable loans, even withthe best disclosures.” The Federal Reserve haspointed to subprime products as particularlycomplex and difficult to compare betweenlenders, especially ones originated through amortgage broker. This complexity has made it

SECTION TWO

The Evolution of Less-Than-PrimeMortgage Lending

5AMERICAN BANKERS ASSOCIATION

September 2009 ABAWorks on Regulation Z

“Developments in thehousing sector havebecome interlinkedwith the evolution of financial markets and the economy as a whole.”

Federal Reserve BoardChairman Ben Bernanke,December 4, 2008

AMERICAN BANKERS ASSOCIATION

ABAWorks on Regulation Z September 2009

6

[C]ertain practiceshave led too manypeople into homeownership thatthey cannot sustain.When this happens,especially when this happens in large or concentratednumbers, consumerssuffer, and their neighbors and communities suffer, as well …

Former Federal ReserveBoard Governor Randall S. Kroszner

Chart 1 Chart 2

Percent of Annual

Mortgage Originations

Yearly Mortgage OriginationsDollars in Trillions

Source: Inside Mortgage Finance, September 5, 2008 Source: Inside Mortgage Finance, September 5, 2008

difficult for borrowers to shop around. Whenthey did shop, consumers were offereddisclosures that were focused on too fewelements of the product — monthly paymentor initial (teaser) interest rate — rather than thewhole loan package, causing borrowers to“unwittingly accept loans that they [would]have difficulty repaying” [73 FR 1676].

Such complexity has also led to the FederalReserve’s view that disclosures alone cannottake care of these structural imperfections. Agrowing consensus emerged that borrowerslacked enough basic financial knowledge tounderstand the mortgage products, even withadequate disclosures, and thus had a need for“protection” rather than simply information.This section reviews the changes in themortgage markets that led to the rapidexpansion of less-than-prime lending, theloosening of underwriting criteria, and theregulatory philosophy underpinning thechanges in the regulations.

CHANGING MORTGAGE MARKETS

The prime and subprime mortgage marketshave undergone dramatic change this decadespurred by the low interest rate environment of2001-2005 and a desire for buyers to ride theappreciating values in the housing market.During this period, housing starts grew rapidly,

rising from a seasonally adjusted annual rate of1.6 million units following the 2001 recessionto a peak of 2.2 million units in February 2005.Refinancing also accelerated; homeowners wereanxious to extract equity via “cash-out”refinancing as home values appreciated.Less-qualified borrowers wishing to ride thiswave found non-traditional, “affordability”mortgage products to be a good option(see Charts 1 and 2). These loans wereattractive, because most borrowers believed thatthe rise in home values would enable them torefinance their loans well before the lower initialfixed rate period expired and the new — muchhigher — adjustable rate period began. Othernon-traditional and non-conforming loans,such as Alt-A mortgage loans, also expandedduring this time. The percentage and dollarvolume of sub-prime and Alt-A loanoriginations together actually exceeded primeloan originations in 2005 and 2006, beforesignificantly receding in 2007 and almostceasing entirely in 2008 to date.

As real estate markets cooled, however, bettingon rapidly rising home values proved to beimprudent; many borrowers were unable, orunwilling, either to make the higher paymentor to refinance, leading to defaults. Of course,neither the lender nor borrower benefits from aforeclosure. Homeowners face the loss ofaccumulated home equity, higher rates for

AMERICAN BANKERS ASSOCIATION

September 2009 ABAWorks on Regulation Z

7

Underwriting standards loosened in largeparts of the mortgagemarket in recent years as lenders —particularly nondepository institutions, many ofwhich have sinceceased to exist —competed moreaggressively for market share.

Federal Register, Vol. 73,No. 6/ Wednesday, January 9, 2008 Pg 1674

Chart 3

Subprime Loans:

Structure and Underwriting of 2006 Vintage

Source: FDIC

other credit transactions, and reducedaccess to credit. Such foreclosures haveadded to the supply of homes for sale,overwhelming what little demand thatexists. As a consequence, sales of new andexisting homes have reached the lowestlevels since the housing recession of the early 1990s. And when foreclosures are clustered, they can injure entirecommunities by reducing property values in surrounding areas.

THE LOOSENING OF

UNDERWRITING STANDARDS

As home values drop, the consequences of poor underwriting are being felt:delinquencies, defaults and foreclosures haverisen rapidly and precipitated a collapse ofconfidence across financial markets. This wasparticularly pronounced in the subprimesector, where the frequent combination ofseveral riskier loan attributes — high loan-to-value ratio, payment shock on adjustable-ratemortgages, no verification of borrowerincome, and no escrow for taxes and insurance— increased the risk of default for subprimeloans originated in 2005 through early 2007.

The vast majority of subprime loans closedin 2006, at the very height of their

popularity, were adjustable rate loanstypically with a fixed teaser rate (below thecomparable risk-adjusted rate) and a two- orthree-year first reset (so-called 2/28s and3/27s). A majority, 56 percent, of suchloans were refinances, and almost half, 46percent, were either low- or no-doc loans(see Charts 3, 4 and 5).

Before the dramatic fall in home prices,borrowers were able to refinance out of these2/28s and 3/27s. With home values falling,this became impossible, and “paymentshock” became a well-worn term. Withstated income often inflated by borrowers,the burden of these payment increases wouldbe much heavier. Even though the reductionin interest rates by the Federal Reservehelped to close the gap between the initialand reset rates, defaults have continued. Infact, about one-third of all the adjustablerate subprime loans were in default beforethe first reset, indicating that borrowers were unable to meet their obligations almost from the start. Moreover,prepayment penalty clauses, which weretypical of most subprime loans, made itharder for borrowers to refinance.

Loose underwriting was not limited to thesubprime market. Interest-only mortgages(most of them with adjustable rates)

Purchase vs. Refinance

AMERICAN BANKERS ASSOCIATION

ABAWorks on Regulation Z September 2009

8

A decline in underwriting standards does notjust increase the riskthat borrowers will be provided loans they cannot repay. It also increases the risk that originatorswill engage in abusive tactics.

Chart 4 Chart 5

Alt-A Loans:

Structure and Underwriting of 2006 Vintage

Underwriting Performance Ratios

Source: FDIC Source: FDIC

accounted for 43 percent of all Alt-A loans closedduring 2006. Thirty-five percent of such loanscarried negative amortization and 83 percentwere low- or no-doc. While the resets of the 2/28s and 3/27s have most likely peaked, most of the Alt-A mortgages have not. These will startto increase this year to levels similar to thesubprime market.

It is too soon to tell how these Alt-A loans will perform, as the reset period is typicallyfive years. However, many Alt-A loans hadnegative amortization features and havealready reached the maximum adjustment,triggering an early reset. The failures ofIndyMac and the problems suffered byWashington Mutual and Wachovia show how devastating the fallout from these non-traditional loans can be.

The market for subprime and Alt-A mortgageloans has practically disappeared, while themarket for conventional/conforming loanscontinues to rebound (see Charts 6 and 7).Nonetheless, delinquencies and foreclosureinitiations in subprime ARMs are expected to rise further as more of these mortgages seetheir rates and payments reset at significantlyhigher levels. Home price declines, which have exceeded 30 percent from last year in the largest 20 metropolitan markets, havedestroyed homeowners’ equity (which in

many cases was small to begin with) and willcontinue to create problems for repayment of these mortgages.

REGULATION REQUIRED TO PREVENT ABUSIVEAND UNAFFORDABLE LOANS

Underpinning the rulemaking is thephilosophy that “market imperfections” orother “structural factors” make regulationsnecessary to prevent a recurrence of theproblems. Thus, the natural adjustment ofunderwriting standards and repricing of riskthat is occurring — and which isacknowledged by the Federal Reserve to beproceeding rapidly — is not enough toovercome all the problems that could lead toabusive and unaffordable loans. The factorsnoted by the Federal Reserve include: (1)limited transparency and limits of disclosure;(2) limited ability of borrowers to effectivelyshop around and compare offers; (3) thetendency on the part of borrowers to focusonly on a few loan attributes to the exclusionof others; (4) limits of disclosures to protectborrowers from unfair loan terms or lendingpractices; and (5) misaligned incentives andobstacles to monitoring inherent in the“originate-to-distribute” model. The followingbriefly reviews the philosophy underlying each factor:

100%

80%

60%

40%

20%

0%

AMERICAN BANKERS ASSOCIATION

September 2009 ABAWorks on Regulation Z

9

While the cost of continuing to shop is likely obvious, the benefit may not beclear or may appearquite small.

A borrower’s focus on the initial monthlypayment during a complex subprimemortgage transactioncan greatly increasehis or her risk.

Chart 6 Chart 7

Quarterly Mortgage OriginationsPercent of Annual Mortgage Originations

Changes in Residential Real Estate

Underwriting StandardsPercent of Responses

Source: Inside Mortgage Finance, September 5, 2008 Source: OCC

Limited Transparency and Limits of DisclosureThe Federal Reserve argues that thecombination of complex products and lack ofcomparable pricing information makes it“harder for consumers to protect themselvesfrom abusive or unaffordable loans, even withthe best disclosures.” Such an outcome is“often compounded by misleading orinaccurate advertising,” which often focuses on“easy approval and low payments.” The FederalReserve cites as examples of complexity the useof adjustable rate loan products, whichaccounted for nearly three-quarters of allsubprime originations and which were oftenaccompanied by prepayment penalties.

The Federal Reserve also noted that the role ofmortgage brokers — which accounted for asmuch as 60 percent of all originations — isoften misunderstood. Many borrowers, theFederal Reserve posits, believe withoutquestion that the broker is working in theirbest interest to find the best interest rate andmost suitable loan terms available. Inparticular, the Federal Reserve stated that“consumers are often unaware that a creditorpays a broker more to originate a loan with a rate higher than the rate the borrower qualifies for based on the creditor’sunderwriting criteria.”

Limited Ability of Borrowers to Shop Around and Compare OffersThe Federal Reserve expresses the concern thatsubprime borrowers may not shop beyond thefirst approval and, thus, may be willing toaccept unfavorable terms. This is more likely inthis market as borrowers have often been turneddown by several lenders before being approved.Thus, once approved, there is little advantage tocontinuing to shop. Plus, the Federal Reservenotes that “the costs of further shopping may besignificant, including completing anotherapplication form and paying yet anotherapplication fee.” Finally, the Federal Reservecommented that: “An unscrupulous originatormay also seek to discourage a borrower fromshopping by intentionally understating the costof an offered loan.”

Limited Focus of Borrowers on Only a Few Characteristics of the LoanWith complex loans, borrowers may choose tofocus on a few attributes of the product orservice that seem most important, or whichhave the most obvious and immediateconsequence, e.g., loan amount, downpayment, initial monthly payment, initialinterest rate, and up-front fees. As aconsequence, other features — future increasesin payment amounts or interest rates,prepayment penalties, negative amortization,income verification, and escrows for future tax

AMERICAN BANKERS ASSOCIATION

ABAWorks on Regulation Z September 2009

10

Obtaining widespread customer under-standing of the many potentially significantfeatures of a typicalsubprime product is a major challenge.

Weak underwritingstandards, the FederalReserve noted,increases the risk that “originators willengage in an abusive strategy of‘flipping’ borrowers in a succession ofrefinancing” that ultimately “strip borrowers’ equity and provide them nobenefit. Moreover, the Federal Reservenoted that an atmosphere of relaxedstandards may attractless scrupulous originators and morevulnerable borrowersinto the market whichwould lead borrowersto pay more for loans than their riskprofiles warrant.

and insurance obligations — may be ignored.Thus, the Federal Reserve concludes:“consumers may unwittingly accept loans thatthey will have difficulty repaying.”

Disclosures May Not Sufficiently ProtectBorrowers from Unfair Loan TermsWhile acknowledging that disclosuresdescribing the multiplicity of features of acomplex loan “could help some consumers inthe subprime market,” the Federal Reserve notesthat “disclosures may not be sufficient to protectthem against unfair loan terms or lendingpractices.” Moreover, the Federal Reserve statesthat “even if all of a loan’s features are disclosedclearly to consumers, they may continue tofocus on a few features that appear mostsignificant. Alternatively, disclosing all featuresmay ‘overload’ consumers and make it moredifficult for them to discern which features aremost important.”

Furthermore, the Federal Reserve notesdisclosures cannot be effective unless there is acertain minimum level of understanding of themarkets and products by the borrower andcomments that: “Disclosures themselves likelycannot provide this minimum understanding fortransactions that are complex and thatconsumers engage in infrequently.” Due to thelack of knowledge, borrowers may rely more ontheir originators to explain the disclosures whenthe transaction is complex and “some originatorsmay have incentives to misrepresent thedisclosures so as to obscure the transaction’s risksto the borrower.” Such a misrepresentation ismore likely if the originator is face-to-face withthe customer.

Misaligned Incentives and Obstacles to MonitoringIn justifying the changes in regulations, theFederal Reserve also sets forth the concern thatincentives — particularly of originators thatintend only to sell the loan quickly — are notaligned with the interests of borrowers. TheFederal Reserve cites the recent dramatic rise inserious delinquencies on subprime mortgages asclear evidence that originators did not give“adequate attention to repayment ability” andhad little incentive to do so as the risk upon saletypically is passed to the purchaser and theoriginator bears little loss if the mortgagesdefaulted. The Federal Reserve also noted thatwarranties by sellers and other repurchase loanagreements have “little meaningful benefit if

originators have limited assets.” Finally, riskrises in cases where originator fees are related toloan volume, which encourages aggressive push-marketing strategies.

The Federal Reserve also believes that themonitoring of sellers by purchasers of loans isinadequate to impose sufficient discipline onthe originator to prevent abusive practices.Moreover, “investors may not exercise adequatedue diligence on mortgages in the pools inwhich they are invested, and may instead relyheavily on credit-ratings firms to determine thequality of the investment.”

The fragmentation of the originator market canfurther exacerbate the problem, according to theFederal Reserve. Thus, a securitized pool ofmortgages may have been the product of tens oflenders and thousands of brokers. The FederalReserve notes that: “Investors have limitedability to directly monitor these originators’activities. Similarly, a lender may receive ahandful of loans from each of hundreds orthousands of small brokers every year. A lenderhas limited ability or incentive to monitor everysmall brokerage’s operations and performance.”

A ROLE FOR NEW HOEPA RULES

Given the market imperfection, the FederalReserve concluded that borrowers in thesubprime market “face serious constraints on their ability to protect themselves from abusiveor unaffordable loans, even with the best disclosures; originators themselves may at timeslack sufficient market incentives to ensure loansthey sell are affordable; and regulators face limits on their ability to oversee a fragmentedsubprime origination market.” The conclusion isthat regulations are needed to ensure thatborrowers receive the mortgage loans they canafford to repay.

The ABA supports the Federal Reserve’s effortsto curb abusive mortgage lending practices andto provide increased transparency for borrowers.While ABA believes that its members are alreadyadhering to the loan origination, underwritingand servicing standards that protect mortgagecustomers and the bank, it is appropriate for theFederal Reserve to provide additional consumerprotections, and to apply that uniform standardto all financial firms that make mortgage loans,including non-federally regulated lenders.

SECTION THREE

Higher-Priced Mortgage Loans(§ 226.32-226.35)

AMERICAN BANKERS ASSOCIATION

September 2009 ABAWorks on Regulation Z

11

The new amendments to Regulation Z providespecial consumer protections to a subset ofconsumer residential mortgages called “higher-priced mortgage loans.” While the rules forhigher-priced mortgages are intended to applyprimarily to loans that have historically beencategorized as subprime, the definition of“higher-priced mortgage loan” is based on theloan’s Annual Percentage Rate (APR) instead ofborrower credit or loan product characteristics.As a result, this new category is likely to includemany prime loans in certain markets, dependingon market conditions. The new rules requirethat lenders that make higher-priced loans mustengage in an underwriting and documentationprocess that is more extensive than was previouslyrequired by law. The new regulations requirecreditors to:

• Determine and document a borrower’sability to repay the loan;

• Limit prepayment penalties in certaincircumstances; and

• Establish an escrow account for propertytaxes and homeowners’ insurance.

Most insured depository institutions have time-tested lending standards that substantiallycomply with many of the new requirements forhigher-priced loans. Nevertheless, banks of allsizes and levels of complexity — includingprime-only lenders — should review their loanpolicies and underwriting standards todetermine whether any changes are necessary in

order to fully comply with the consumer protectionrequirements for higher-pricedloans. As explained in greaterdetail below, some prime loansmay be classified as higher-pricedloans even though the newrequirements are intended to applyto only subprime loans.

Rationale Behind the New Rule

The Federal Reserve goal in issuingthe new rule was to protect vulnerableborrowers from lending practices they consider unfair.

Subprime Lending Not Prohibited

Subprime lending can include borrowers whohave little or no credit history or have weakenedcredit histories as a result of late payments,charge-offs, judgments, and bankruptcies. It can also include borrowers with fewer assetsnecessary to make a downpayment or withundocumented income or higher debt-to-income ratios. However, the Federal Reservebelieves that when underwritten correctly,subprime mortgage credit can be beneficial tosome borrowers. For this reason, the changes toRegulation Z do not ban all subprime lending.

Some prime loans may be classified ashigher-priced loanseven though the newrequirements aredesigned to regulatesubprime loans.

Regulation Z

Effective Date:

October 2009

Early Disclosure

Provisions

Effective Date:

July 2009

Focus on Price, Not Products

The regulation identifies subprime loans on thebasis of loan price (discussed fully later in thissection) rather than borrower characteristics orspecific loan products or terms. The FederalReserve reasoned that focusing solely on loanswith particular features may not capture all of theloans in the subprime market. In addition, theFederal Reserve believes that identifyingsubprime loans on the basis of price is morelikely to remain relevant over time as creditorsintroduce new products into the marketplace andas lending practices change.

Rule Will Likely Apply to Some Prime Loans

While the new regulations for higher-pricedloans are intended to apply to subprime loans,the Federal Reserve noted that there is “inherentuncertainty” in crafting rules that cover thesubprime market but that generally exclude theprime market. In the end, the Federal Reserveopted to err on the side of being over-inclusiverather than under-inclusive. Depending onmarket conditions, the rules are likely to applyto the Alt-A market and to some primeproducts. For example, if the new rules were ineffect at the time of the publication of thisABAWorks, a substantial portion of the “JumboA” market would be considered higher-pricedmortgage loans. Therefore, it is important thatall banks examine all of their lending policiesand procedures to ensure that they comply withthe new regulations. Later in this section there isan in-depth discussion of the extent to which thenew regulations could extend to prime loans.

Parties Covered by the Higher-Priced Loan Regulation

Banks and savings associations have generallymaintained conservative and prudent mortgageunderwriting standards. They are heavilyregulated and examined regularly by thebanking regulatory agencies for compliancewith laws and regulations. Most of theseinstitutions and their employees are linked

closely to the communities in which they lendand, therefore, have very strong incentives tomake responsible, sustainable loans. This hasnot consistently been the case with mortgagebrokers and non-federally regulated lenders.

Non-bank lenders and brokers have not beensubject to the same lending requirements andregulatory oversight as federally-insureddepository institutions. To address this problem,the higher-priced loan regulations apply to“creditors,” which includes insured depositoryinstitutions as well as non-federally regulatedbanks and other lenders.1 Applying theregulation to all creditors is one step towardestablishing national standards that protectborrowers from practices the Federal Reserveconsiders abusive. However, the regulation onits own will not impose on non-bank lendersexactly the same standards.

In most cases, non-federally regulated lendersdo not undergo bank-like examination andsupervision and have marketed products that, insome cases, resulted in borrowers financinghomes that they could not afford over the long-term. Despite the progress made by theamendments to Regulation Z, policy-makersand regulators still have much work to do inorder to provide comparable supervision andenforcement for insured depository institutionsand non-bank financial firms. Under thecurrent regulatory and enforcement structure,non-bank lenders are unlikely to be examinedfor underwriting decisions and tend to be lesscomprehensively examined for compliance.Until there is a comparable enforcementprogram for all lenders, compliance obligationswill be uneven.

Similarly, policy-makers are still contemplatinghow to best regulate and oversee the actions ofmortgage brokers. Mortgage brokers have beena major conduit for home loans in recent years.Despite their significant role in the mortgagemarket, brokers are not “creditors” underRegulation Z and, therefore, are not directlysubject to most of the new requirements forhigher-priced loans. Brokers are, however,subject to the provisions prohibiting influencing

AMERICAN BANKERS ASSOCIATION

ABAWorks on Regulation Z September 2009

12

The higher-priced loan regulations apply to “creditors,”which includesinsured depositoryinstitutions as well as non-banks and other lenders.

Brokers are not“creditors” underRegulation Z and,therefore, are notsubject to the newrequirements forhigher-priced loans.

1. 12 C.F.R. §226.35(b).

appraisals. As a result, banks are responsiblefor ensuring that broker-originated higher-priced loans comply with the regulation’sunderwriting, escrow, and prepaymentprovisions. Banks will need to monitor broker-generated loans closer than ever before toensure that these loans comply with regulatoryrequirements as well as with the bank’s ownpolicies regarding higher-priced loans.

What is a Higher-Priced Loan?

Whether a loan is classified as higher-priceddepends on two factors: the type of the loanand the price of the loan. Below is a detaileddiscussion of this two-part test for determiningwhether a loan is subject to the three newconsumer protection requirements that areapplicable to higher-priced mortgages.

Loan Type

The protections for higher-priced loans apply tofirst-lien and subordinate-lien closed-endmortgages that are secured by the borrower’sprincipal dwelling. In contrast to HOEPAloans, this includes home purchase loans as wellas refinancings that meet the pricing trigger(explained below) as long as the borrower’sprimary residence serves as the collateral forthose loans.2

The regulation does not apply to home equity lines of credit, reverse mortgages,3

construction-only loans, bridge loans, andloans having primarily a real estateinvestment purpose. Loans for the purchaseor the improvement of a second home willnot be considered higher-priced unless theloan for the second home was secured bythe borrower’s principal dwelling.4

In excluding some second homes and loanswith a real estate investment purpose from thedefinition of higher-priced loans, the FederalReserve reasoned that (1) real estate investorsare expected to be more sophisticated than

ordinary borrowers about the real estatefinancing process, and (2) applying the newregulations to real estate investments would beinconsistent with TILA’s focus on consumer-purpose transactions.

✲ COMPLIANCE ALERT

Construction-Only Loans

As noted above, construction-only loans that are solelyfor the purpose of financing the initial construction of adwelling are excluded from the requirements for higher-priced loans. However, the permanent financing that isput into place after construction is completed could be ahigher-priced loan depending on the price of the loanand the type of the loan.

In excluding construction-only loans, theFederal Reserve reasoned that these loans donot present the same risk of customer abuse asother loans that the rule covers. In addition,construction loans typically have a higherinterest rate than permanent financingreflecting higher relative risk of loss.

Discussions with ABA members have raisedquestions about how to treat constructionfinancing arrangements that do not separate theconstruction loan from the permanentfinancing for the home. Under these kinds ofarrangements, the interest rate during theconstruction period is higher than the interestrate for the remainder of the loan. Theborrower is given one TILA disclosure andthere is only one loan closing. Since thesearrangements are treated as one loan, the higherrate of interest that is charged during theconstruction period will increase the likelihoodthat these kinds of loans will exceed thethreshold for higher-priced loans. ABA willwork with the Federal Reserve to determinehow these financing arrangements should betreated for purposes of complying with therequirements for higher-priced loans.

AMERICAN BANKERS ASSOCIATION

September 2009 ABAWorks on Regulation Z

13

2. Id. at §226.35(a).3. Id. at §226.35(a)(2). 4. 73 FR 44538 (July 30, 2008).

The protections forhigher-priced loansapply to first-lien and subordinate-lienclosed-end mortgagesthat are secured by the borrower’sprincipal dwelling and exceed thehigher-priced loanthresholds.

The Federal Reserve isreviewing reversemortgage products inan initiative that isseparate from thisrulemaking in order todetermine whetheradditional consumerprotection measuresare necessary forthese kinds of loans.

✲ COMPLIANCE ALERT

Bridge Loans

Bridge loans are also excluded from the requirementsapplicable to higher-priced loans. The Federal Reservebelieves that this exemption is “in borrowers’ interestand support homeownership.”5

The Federal Reserve warns creditors againstattempting to circumvent the higher-pricedloan requirements by financing a series of short-term mortgage loans. For example, a 12-monthloan with a substantial balloon payment wouldnot qualify for the exemption where it wasclearly intended to lead a borrower to refinancerepeatedly into a chain of 12-month loans.

Loan Price

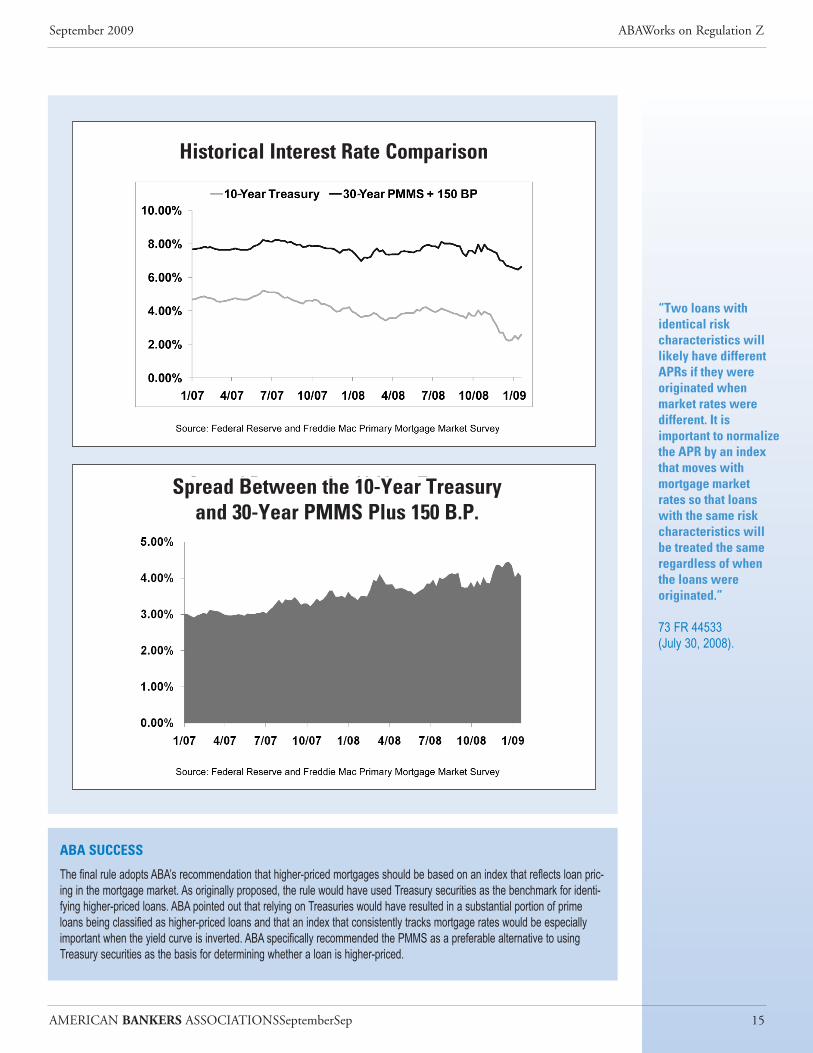

The APR of a loan is the second factor indetermining whether a loan triggers therequirements for higher-priced mortgages. Theregulation defines a higher-priced loan as aconsumer residential mortgage loan with anAPR of 150 basis points or more over the“average prime offer rate” for first liens and 350basis points or more over the average primeoffer rate for subordinate liens.6 This sectionexplains how the Federal Reserve will determinethe average prime offer rate and discusses theFederal Reserve’s rationale in adopting the APRpricing test for higher-priced loans.

Average Prime Offer Rate

The “average prime offer rate” is defined as anAPR “that is derived from average interest rates,points, and other pricing terms offered … by arepresentative sample of creditors for mortgagetransactions that have low-risk pricingcharacteristics.”7

The Federal Reserve will calculate the averageprime offer rate of different kinds of loans usingthe weekly Freddie Mac Primary MortgageMarket Survey (PMMS). Each week, FreddieMac surveys lenders about the rates and pointsfor their 30-year fixed-rate, 15-year fixed-rate,5/1 hybrid amortizing adjustable-rate, and 1-year amortizing adjustable rate mortgageproducts.8 The Federal Reserve will use thepricing terms from the PMMS, such as interestrate and points, in order to calculate an APR foreach of the four types of transactions that thePMMS reports.9 This APR will be the averageprime offer rate for the four products includedin the PMMS.

The Federal Reserve will publish these rates intwo tables, one each for variable-rate and non-variable-rate loans. The tables will set forthaverage prime offer rates for each of the 14products (six variable rate and eight non-variable-rate loans), and the methodologyprovides assignment rules for all other initial,fixed-rate periods or terms to maturity, asapplicable.10 In short, the site will carry a fullexplanation of how to identify a comparabletransaction (and therefore the average primeoffer rate), in the event an institution develops aloan product for which the Federal Reserve hasnot derived an average prime offer rate.

AMERICAN BANKERS ASSOCIATION

ABAWorks on Regulation Z September 2009

14

5. One example of a temporary or a bridge loan is a loan to purchase a new dwelling where the consumer plans to sell a current dwelling within 12 months. The Federal Reserve noted that this is not the only potentialexample of a temporary or a bridge loan. 73 FR 44539 (July 30, 2008).

6. 12 C.F.R. §226.35(a).7. 12 C.F.R. §226.35(a)(2).8. The survey is based on first-lien prime conventional conforming mortgages

with a loan-to-value ratio of 80 percent. The adjustable-rate mortgage(ARM) products are indexed to constant-maturity U.S. Treasury rates andlenders are asked for both the initial coupon rate and points as well as the margin on the ARM products. Currently, 125 lenders are surveyed eachweek and the mix of lender types — thrifts, commercial banks and mort-gage lending companies — is roughly proportional to the level of mortgage business that each type commands nationwide. The survey is collectedfrom Monday through Wednesday and the results are posted on Thursdays.http://www.freddiemac.com/dlink/html/PMMS/display/PMMSOutputYr.jsp.

9. For multiple reasons, the Federal Reserve elected to use the PMMS as thebasis for calculating the average prime offer rate. First, the PMMS is the onlypublicly available data source that has rates for more than one kind of fixed-rate mortgage and more than one kind of variable-rate mortgage. Therefore, itprovides a firmer basis for estimating the rates for other fixed and variablerate products that are not included in this or other publicly available data.Second, the survey includes information that will allow for the calculation ofan APR rather than an average offered contract rate. This will make the rule’scoverage more accurate and consistent. 73 FR 44535 (July 30, 2008).

10. The preamble states that the indices’ methodology will remain on the Website along with the tables.

The Federal Reservewarns creditorsagainst attempting to circumvent thehigher-priced loanrequirements byfinancing a series of short-term mortgage loans.

Average Prime Offer Rate

The Federal Reserve will calculate theaverage prime offer rate of differentkinds of loans using the weekly FreddieMac Primary Mortgage Market Survey(PMMS). The full methodology isincluded as Appendix A.

ABA SUCCESS

The final rule adopts ABA’s recommendation that higher-priced mortgages should be based on an index that reflects loan pric-ing in the mortgage market. As originally proposed, the rule would have used Treasury securities as the benchmark for identi-fying higher-priced loans. ABA pointed out that relying on Treasuries would have resulted in a substantial portion of primeloans being classified as higher-priced loans and that an index that consistently tracks mortgage rates would be especiallyimportant when the yield curve is inverted. ABA specifically recommended the PMMS as a preferable alternative to usingTreasury securities as the basis for determining whether a loan is higher-priced.

AMERICAN BANKERS ASSOCIATIONSSeptemberSep

September 2009 ABAWorks on Regulation Z

15

“Two loans withidentical riskcharacteristics willlikely have differentAPRs if they wereoriginated whenmarket rates weredifferent. It isimportant to normalizethe APR by an indexthat moves withmortgage market rates so that loanswith the same riskcharacteristics will be treated the sameregardless of when the loans wereoriginated.”

73 FR 44533 (July 30, 2008).

Historical Interest Rate Comparison

Spread Between the 10-Year Treasuryand 30-Year PMMS Plus 150 B.P.

APR: Spread Over the Average Prime Offer Rate

A first-lien, closed-end mortgage loan with an APRof 150 basis points or more over the average primeoffer rate (350 basis points or more for subordinateliens) will be classified as a higher-priced loan. Afterconsulting loan data for subprime and Alt-Asecuritized pools for the period 2004 to 2007, theFederal Reserve believes that these benchmarks willcapture all of the subprime market and part of theAlt-A market.

When to Determine Whether a Loan isHigher-Priced

In order to determine whether a loan is higher-priced, a lender must compare the APR of theloan to the average prime offer rate as of thedate that the interest rate is locked beforeclosing (also known as the lock date). In theevent that a creditor sets the interest rateinitially and then resets it at a different levelbefore consummation, the creditor should usethe last date that the interest rate is set.11

Under the new rules, creditors must use themost recently available average prime offer rateas of the rate-lock date. Since PMMS figures areupdated weekly, the Federal Reserve will alsoupdate average prime offer rates weekly. This

will, in turn, require that lenders revise theirtrigger calculations on a weekly basis. TheFederal Reserve states that updates to the tablesmade each Friday will be effective the followingMonday.12

The Federal Reserve is not changing the currentmeaning of when the rate is “set” for purposesof defining the comparable APR. Thus, if aloan’s rate is subject to change for any reason,then it has not been “set” for the final timebefore closing. The final rules preserve theexisting “assignment rules” currently applicableunder HMDA, where (1) a loan with a termnot represented among the Treasury securityterms listed in the table matches to the Treasurysecurity with the term closest to the loan’s term,and (2) when a loan has a term exactly halfwaybetween two Treasury security terms it matchesto the Treasury security with the shorter of thetwo terms.

✲ COMPLIANCE ALERT

Higher-Priced Loan Determined by APR

The actual APR of a mortgage loan — that is, the APRat closing — will determine whether a loan is higher-priced. Lenders must compare this APR to the averageprime offer rate as of the date that the rate is locked.

AMERICAN BANKERS ASSOCIATION

ABAWorks on Regulation Z September 2009

16

Lenders shouldmonitor loans that are between theapproval and theclosing process toensure that last-minute adjustments(i.e., customer opts to pay morepoints, broker feesincrease, etc.) do notinadvertently causethe loan to becomehigher-priced.

ABA SUCCESS

The ABA cautioned against creating separate definitions of higher-priced loans under Regulation Z and higher-cost loansunder Regulation C, which implements the Home Mortgage Disclosure Act (HMDA). Having separate definitions for nearlyidentical concepts pertaining to subprime mortgage loans would add complexity and regulatory burden without protectingborrowers or improving the stability of the mortgage market.

Consistent with the ABA’s recommendations, the Federal Reserve has proposed to conform the triggers for higher-cost loansunder Regulation C to the new triggers for higher-priced loans under Regulation Z. Under this approach, HMDA reportingwould be required for loans that have a spread of 150 basis points or more above the average prime offer rate forfirst liens and 350 basis points or more above the average prime offer rate for subordinate liens. Currently, Regulation Crequires lenders to report the spread between the APR on a loan and the yield on Treasury securities of comparable maturity ifthe spread meets or exceeds 300 basis points above Treasuries for a first-lien or 500 basis points for a subordinate-lien.

Aligning the definitions of “higher-priced” and “higher-cost” would reduce compliance complexities and would standardize themeanings of similar terms that are intended to identify subprime loans.

11. 73 FR 44537 and 44613 (July 30, 2008).12. For consistency’s sake, lenders may not apply new benchmarks before the Monday following publication, even if their systems are capable of applying the new

benchmarks earlier.

Lenders should monitor loans that are betweenthe approval and the closing process to ensurethat last-minute adjustments (e.g., customeropts to pay more points, broker fees increase,etc.) do not inadvertently cause the loan tobecome higher-priced. Banks that decide not tomake higher-priced loans due to the legal andreputation risks associated with these kinds ofloans should be especially vigilant about theeffect that last-minute changes have on theactual APR of a loan.

Practical Application: Some Prime Loans Higher-Priced

It is possible that some popular prime loanproducts will exceed the pricing threshold forhigher-priced loans.

Financial institutions commonly price a riskpremium into loan products based on manyfactors, including the amount of the loan, theamount of the borrower’s down payment, theterm of the loan, and whether the loan will beheld in portfolio. Risk-based pricing practicescommonly associated with popular creditproducts may cause some loans to becategorized as higher-priced even if they areprime loans that are made to prime borrowers.

ABA members should review all of theirmortgage lending policies and procedures inorder to: (1) ensure that they are in compliancewith the new regulation, and (2) to minimizepossible legal risk. Lenders should pay particularattention to the impact that the regulation willhave on the following prime mortgage products.

Jumbo Loans: The vast majority of jumboloans are made to low-risk borrowers withprime credit. However, these loans may exceedthe triggers for higher-priced loans. This isbecause jumbo loans typically carry higherinterest rates than conforming loans that areeligible to be purchased by Fannie Mae andFreddie Mac. The higher rate compensates theinvestment community for a lack of GSEguarantee. After pricing for this risk, however,jumbo mortgages have an increased likelihoodof being classified as higher-priced loans.

Historically, jumbo loans had interest rates thatwere 25 to 50 basis points higher than the ratefor conforming loans. However, recenttightening in the credit markets has resulted injumbo loan rates that are 100 to 125 basispoints higher than the rates charged onconforming loans.

✲ COMPLIANCE ALERT

Requirements in High-Cost Areas

Lenders in high-cost areas, such as Washington, D.C.,California, New York, and Florida where jumbomortgages are common should pay particular attentionto the new requirements for higher-priced mortgages. If the spread between conforming and jumbo loansremains wide when the rule takes effect in October2009, the regulation will cover a significant share oftransactions that would be prime jumbo loans. TheFederal Reserve declined to create a separatebenchmark for jumbo loans that would prevent theseprime loans from being classified as “higher priced.” The Federal Reserve reasoned that the pricing onjumbo loans may not always trigger the higher-pricedloan requirements in the future.

First Lien Home Equity Loans: Home equityloans that are first liens have an increasedlikelihood of being higher-priced loans underthe new requirements.13 First lien home equityloans have funding, origination costs, and loanterms that differ from other first mortgages(such as a home purchase loan), even thoughthey are in the same loan position and aresecured by the same collateral. Often, banksprice home equity loans on the assumption thatthey are second liens, so the pricing on a firstlien will not improve based on lien position.Home equity loans are fixed for a specific term,typically ranging from 60 to 360 months. Abank’s cost of funds for these loans can vary byover 200 basis points. Due to these pricingfactors, first lien home equity loans couldtrigger the requirements for higher-priced loanswhen market conditions are similar to thosethat we are experiencing at this time. In somecases, this leaves little room for an institution toprice for risk and make a profit withoutcrossing the proposed higher-priced threshold.

AMERICAN BANKERS ASSOCIATION

September 2009 ABAWorks on Regulation Z

17

13. A home equity loan can be in first lien position when the initial mortgage onthe property is paid in full.

Lenders in areaswhere jumbomortgages arecommon, such asWashington, D.C.,California, New York,and Florida, shouldpay particularattention to the newrequirements forhigher-pricedmortgages.

Zero Upfront Closing Costs: Loan productswith no upfront closing costs (such as loanapplication fees, title insurance costs, appraisalfees, or credit report fees) are a popular way for borrowers to reduce the initial costs associatedwith purchasing or refinancing a home. Lendersthat provide zero closing cost loans usuallycharge a higher rate of interest in order torecoup their origination costs on this product.These products can be very helpful to youngfamilies with good credit that are trying topurchase their first home. However, lendersshould be aware that loans with zero closingcosts (including no closing cost home equityloans) have an increased likelihood of exceedingthe pricing triggers for higher-priced loans.

Small Mortgage Loans: Small mortgage loansare another example of common prime loanproducts that may be categorized as higher-priced loans.

The cost of a home varies dramaticallydepending on where the property is located inthe United States. For example, ABA memberslocated in the nation’s mid-section and in partsof the southern U.S. report that they commonlyoriginate mortgage loans ranging between$50,000 and $75,000. In addition, many banks provide loans for the purchase of manufactured(mobile) homes. The cost of mobile homes canrange from several thousand dollars to over$15,000 or $20,000.

Small mortgage loans are commonly held inportfolio and often have pricing structures thatare different than other mortgage products. Forexample, lenders incur comparable costs fororiginating and servicing mortgage loans,regardless of the size of the loan, but institutionssometimes charge a higher rate of interest on asmaller loan in order to recover overhead costsand to ensure that the loan is profitable. Inaddition, pricing for small loans can be affectedby characteristics that are unique to thecollateral that secures the loan or by specificloan terms that may not be available for largermortgage loans. For instance, mobile homespose a higher risk to creditors as compared to

site-built homes due to the collateral’s tendencyto depreciate. As a result, these loans commonlycarry a higher interest rate than homes that arefixed to real property and may be more likely tobe classified as higher-priced mortgage loans.

Construction Loans: Banks should alsomonitor whether their lending policies andprocedures would cause the APR on aconstruction loan to trigger the requirements forhigher-priced loans. While construction-onlyloans are excluded from the requirements forhigher-priced loans, some banks finance theconstruction of a home without separating theconstruction financing and the permanentfinancing. As mentioned previously in thisABAWorks, there is concern that since thesearrangements are treated as one loan, the higherrate of interest during the construction period willincrease the likelihood that these kinds of loanswill exceed the threshold for higher-priced loans.

Loans with Private Mortgage Insurance: Inaddition, recent adjustments to the rates formortgage guarantee insurance will impact theprice of a home loan. Like the GSEs, privatemortgage insurance companies have adjustedtheir pricing structure in recent months in orderto protect against additional losses stemmingfrom the downturn in the housing market. Onaverage, mortgage insurance premiums haveadded 50 basis points to the cost of a loan. This amount can increase or decreasedepending on the borrower’s credit score andthe property’s loan-to-value ratio and theseamounts may change as mortgage insurersreassess their risk, including with respect todeclining collateral values.

Because premiums for private mortgageinsurance must be incorporated into APR andfinance charge disclosures, increasing premiumsfor private mortgage insurance will increase thelikelihood that prime mortgage loans would fall inadvertently into the higher-priced category.Mortgage insurance premiums will not bereflected in average prime offer rate because thePMMS surveys lenders on rates and fees forloans with an 80 percent loan-to-value ratio.

AMERICAN BANKERS ASSOCIATION

ABAWorks on Regulation Z September 2009

18

Banks should discussthe new mortgagelending rules withtheir software vendorsas soon as possible.Banks should inquirewhat preparations thevendor is undertakingin order to help thebank flag higher-priced loans.

AMERICAN BANKERS ASSOCIATION

September 2009 ABAWorks on Regulation Z

19

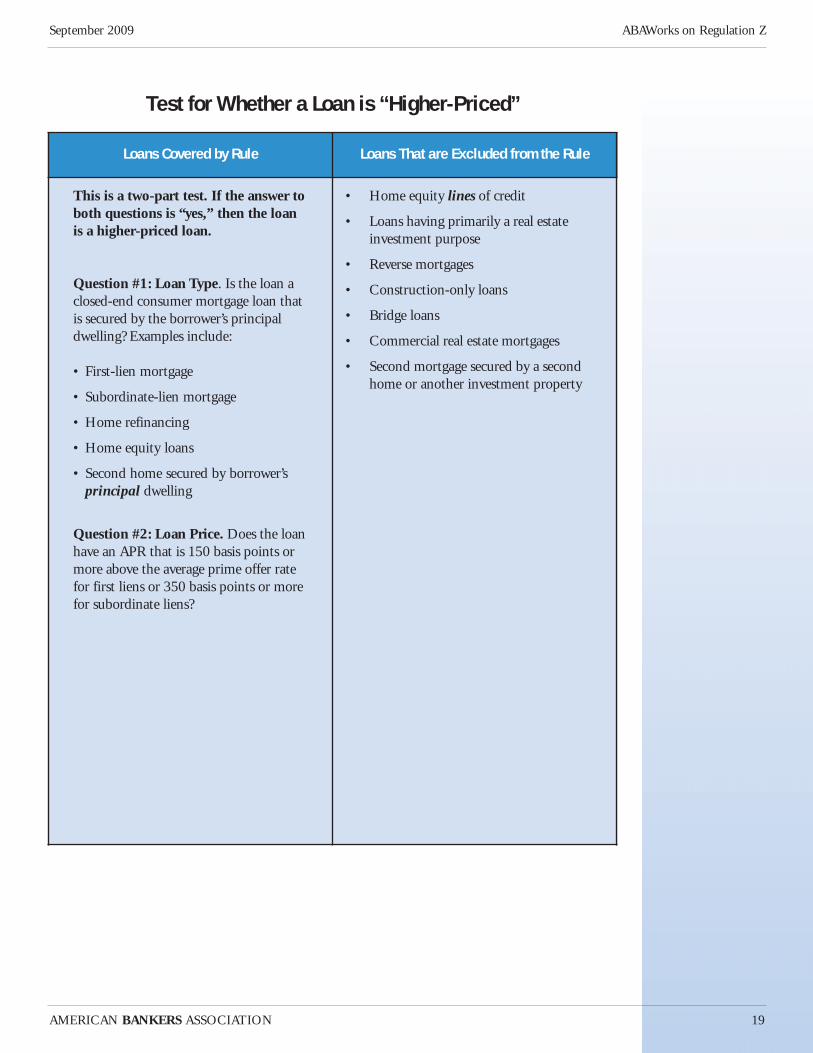

Test for Whether a Loan is “Higher-Priced”

Loans Covered by Rule Loans That are Excluded from the Rule

This is a two-part test. If the answer toboth questions is “yes,” then the loanis a higher-priced loan.

Question #1: Loan Type. Is the loan aclosed-end consumer mortgage loan thatis secured by the borrower’s principaldwelling? Examples include:

• First-lien mortgage

• Subordinate-lien mortgage

• Home refinancing

• Home equity loans

• Second home secured by borrower’sprincipal dwelling

Question #2: Loan Price. Does the loanhave an APR that is 150 basis points ormore above the average prime offer ratefor first liens or 350 basis points or morefor subordinate liens?

• Home equity lines of credit

• Loans having primarily a real estateinvestment purpose

• Reverse mortgages

• Construction-only loans

• Bridge loans

• Commercial real estate mortgages

• Second mortgage secured by a secondhome or another investment property

Special ComplianceRequirements for Higher-Priced Loans

Higher-priced loans must meet three newcompliance requirements. Lenders must:

1. Determine a borrower’s ability to repaythe higher-priced loan based on verifiedincome and non-collateral assets;

2. Limit prepayment penalties in certaincircumstances;14 and

3. Establish an escrow account for taxesand insurance.

This section of the ABAWorks explains thesecompliance requirements as well as the litigationand reputation risks that could be associatedwith higher-priced loans. It also provides acompliance checklist as well as a list of factorsthat institutions may want to consider whendeciding whether to include higher-priced loansin their loan product mix.

Evaluate and Verify the Borrower’sAbility to Repay the Loan

Evaluating a borrower’s repayment ability is akey principle of safe and sound lending.However, all too often, loosely-regulated non-bank lenders and brokers appear to haveengaged in practices that resulted in borrowerstaking out loans that they did not understandand/or could not afford. In some cases,borrowers misrepresented their ability to repayunaffordable loans or whether they intended tooccupy the property as their principal residence.To address these problems, the new regulationspecifically requires creditors to evaluate andverify a borrower’s ability to repay a higher-priced mortgage loan.16

Repayment Ability

In determining a borrower’s ability to repay aloan, creditors are responsible for consideringfactors such as the borrower’s current andreasonably expected income, current andreasonably expected obligations, employment,and assets other than the collateral. In addition,creditors must verify the borrower’s repaymentability using third-party documents that“provide reasonably reliable evidence of theborrower’s income or assets.”17

Verification of income, assets, andemployment: The regulation provides broadflexibility and gives examples of the types ofincome, assets, and employment on which acreditor may rely when extending credit. Thecommentary to the regulation clarifies that acreditor may use information about current orexpected salary, wages, bonus pay, tips,commissions, interest or dividends, retirementbenefits, public assistance, alimony, childsupport, and assets held in a bank account whenevaluating a borrower’s ability to repay a loan.18

Lenders may use a variety of third-party sourcesto verify this information, including W-2s, taxforms, payroll receipts, check-cashing receipts,and remittance receipts. The documentationprovision is intended to be flexible. The onetype of verification that may not be used is astatement only from the borrower regarding theborrower’s assets and income.

AMERICAN BANKERS ASSOCIATION

ABAWorks on Regulation Z September 2009

20

14. 12 C.F.R. §226.35(b).15. 73 FR 44532 (July 30, 2008).16. 12 C.F.R. 226.35(b)(1); 226.34(a)(4).17. 73 FR 44546 (July 30, 2008).18. Comment 6 to 12 C.F.R. 226.34(a)(4).

“The Board believes that the practices in §226.35 would prohibit — lending without regardto ability to pay from verified income and non-collateral assets, failure to establish an escrowfor taxes and insurance, and prepayment penalties outside of prescribed limits — are soclearly injurious on balance to consumers within the subprime market that they should becategorically barred in that market.”15

Previous regulatoryprovisions imposing“ability to repay”standards underHOEPA werestructured asprohibitions againstengaging in a“pattern andpractice” of makingunaffordable loans.

Under the new TILArequirements, aborrower does notneed to demonstratethat a violation ofthis standard is partof a “pattern orpractice.” A lenderwould violate thestandard based on a single instance of making anunaffordable loan.

AMERICAN BANKERS ASSOCIATION

September 2009 ABAWorks on Regulation Z

21

✲ COMPLIANCE ALERT

Employment Verification

Some lenders currently obtain a borrower’s writtenpermission to verify employment and income directlywith the borrower’s employer. These kinds of employerverifications are often verbal. At this stage, it is unclearwhether this practice would meet the income verificationrequirement for higher-priced loans. Verbal verification ofemployment is a well-established underwriting procedureand ABA will raise this potentially significant underwritingchange with the Federal Reserve. In the meantime,lenders that use this practice should prepare to makeadjustments to their income verification procedures.Because a “higher priced mortgage loan” borrower will beable to assert a violation of this underwriting requirementas a counterclaim for all finance charges from closinguntil the foreclosure action, most banks will seek to havewritten verifications in the loan file to ensure that they canprove the verification took place.

Ability to repay as of consummation:Lenders are responsible for assessing aborrower’s repayment ability based on facts andcircumstances that the lender is aware of on thedate of consummation. A lender will not bepresumed to have violated the ability to repayrequirement in the event that a borrowerdefaults because of significant expenses orincome loss after the loan is closed.19

Obligations: A creditor must consider theborrower’s current non-mortgage debt obligationsas well as non-principal and interest mortgage-related obligations (i.e., taxes and insurance).Lenders may use a credit report to verify currentobligations. However, a creditor is responsible forconsidering obligations that it knows about, evenif those obligations are not reflected on a creditreport. For example, a creditor that knows of a“piggy-back” second, (i.e., a loan that isundertaken at the same time as the primarymortgage transaction) must include it.

✲ COMPLIANCE ALERT

Unknown Subordinate Liens

Banks should request that both borrowers andsettlement agents certify to them that there is not a“piggy-back” second lien being obtained other than asfully disclosed to the bank.

Presumption of Compliance

A creditor is presumed to have complied withthe ability to repay requirement if it completesthe following underwriting procedures:

• Verify the borrower’s repayment ability(discussed above);

• Determine the borrower’s ability torepay using the largest payment sched-uled in the first seven years followingconsummation (taking into accountcurrent obligations); and

• Assessing the borrower’s repaymentability using either a debt-to-incomeratio (DTI) or the borrower’s residualincome after paying debt obligations.20

While the vast majority of insured depositoryinstitutions already comply with theseunderwriting requirements, lenders should notethat the Federal Reserve has stated that “thecreditor’s presumption of compliance forsatisfying these requirements is not conclusive.”In order to better document that it meets thepresumption, banks should consider whether to require the loan underwriter to certify at the time of loan approval that each of thosesteps has been completed, thus creating acontemporaneous business record of the actionsfor inclusion in the loan file. A borrower mayrebut the presumption of compliance withevidence that the creditor disregardedrepayment ability despite following these threesteps. As an example, the Federal Reserve statedthat “evidence of a very high debt-to-incomeratio and a very limited residual income couldbe sufficient to rebut the presumption,depending on all of the facts andcircumstances.”21

Lenders are required to comply with the firstunderwriting practice — verifying a borrower’sability to repay a higher-priced loan. However,the second and third practices — underwritingto the fully-indexed rate and evaluating acustomer’s DTI or residual income — areoptional. A lender that does not use the second

A lender that does notuse the second andthird underwritingcriteria —underwriting to thefully-indexed rate and evaluating aborrower’s DTI orresidual income —will not be deemed tohave violated theability to repayrequirement per se.

Rather, the lender willnot be presumed tohave met the ability torepay requirement. Inthis circumstance,whether a lender hasevaluated theborrower’s ability torepay the loan willdepend on the totalityof the facts andcircumstances.

Nevertheless, there isrisk that lenders whodo not qualify for thepresumption ofcompliance may find itdifficult to provecompliance otherwise.

19. 12 C.F.R. §226.34(a)(4) and Comment 5 to §226.34(a)(4).20. 12 C.F.R. §226.34(a)(4)(iii).21. Comment 1 to §226.34(a)(4)(iii).

and third underwriting criteria will not bedeemed to have violated the ability to repayrequirement per se. Rather, the lender will notbe presumed to have met the ability to repayrequirement. In this circumstance, whether alender has evaluated the borrower’s ability torepay the loan will depend on the totality of thefacts and circumstances. Nevertheless, there isrisk that lenders who do not qualify for thepresumption of compliance may find it difficultto prove compliance otherwise.

Repayment ability based on a fully indexedrate and fully amortizing payment: In orderto obtain a presumption of compliance with therule’s ability to repay requirement, a lendermust evaluate the borrower’s ability to repay avariable rate loan using the largest scheduledpayment of principal and interest in the firstseven years of the loan. A lender may elect touse a lower payment in its underwriting, butthe lender would not be presumed to complywith the repayment requirement.

Ratio of debt obligations: To have thepresumption of compliance, creditors mustfactor into the evaluation of the borrower’sability to repay the loan either (1) thecustomer’s DTI ratio or (2) the income that the borrower will have after paying debtobligations. While the rule requires creditors touse only one of these metrics in order to obtainthe presumption, banks may opt to use bothmeasures to predict repayment ability.

The final rule does not contain quantitativethresholds for either DTI or residual income. In declining to set acceptable benchmarks, theFederal Reserve noted that establishing specificdebt-to-income ratios or residual income levelscould limit the availability of credit withoutsubstantially benefitting borrowers. Someindustry participants agree that the FederalReserve should not be overly prescriptive ordiscourage new ideas and innovative thinking.Others, however, believe that the Federal Reserveshould establish specific parameters in order tominimize the legal risk for responsible lendersthat make higher-priced loans. Ironically, theFederal Reserve observed that “it is not clearwhat thresholds would be appropriate.”22

✲ COMPLIANCE ALERT

Affordability Standards

Banks seeking to limit their exposure might considersetting their DTI and residual income standards to be consistent with federal government affordabilitystandards embedded in the Federal HousingAdministration and Department of Veterans Affairs loanprograms and the FDIC’s loss mitigation program. Whilethe Federal Reserve has not created an express safeharbor for these standards, most experts expect thatfew courts would find an “ability to repay” violation for aloan that meets FHA, VA or FDIC standards foraffordability. It is less clear whether setting a bank’sstandards to be consistent with Fannie Mae or FreddieMac standards would give similar protection.

AMERICAN BANKERS ASSOCIATION

ABAWorks on Regulation Z September 2009

22

22. 73 FR 44550 (July 30, 2008).

AMERICAN BANKERS ASSOCIATION

September 2009 ABAWorks on Regulation Z

23

Limit Prepayment Penalties OnlyTo Specific Circumstances

In addition to ensuring that at-risk borrowersare able to repay their mortgage, the newregulations governing higher-priced loans areintended to limit certain prepayment penalties.

Prepayment penalties that are clearly disclosedcan benefit both borrowers and lenders.Consumers can benefit from receiving a lowerinterest rate or lower closing costs, while lenderscan benefit from increased predictability forloan duration.

The Federal Reserve believes that some productsin the mortgage market contained prepaymentpenalties that were not fair to borrowers. Forexample, some products effectively prohibitedcustomers from refinancing hybrid ARM loansthat had low teaser rates for an initial period(typically two or three years) but had asignificantly higher rate after the initial period.

The restrictions limited this ability of theborrower to refinance in anticipation of thereset. To address this practice, the amendmentsto Regulation Z impose the followingrestrictions on prepayment penalties:

• Prepayment penalties are prohibited onloans where payments can change dur-ing the first four years of a higher-priced loan.