the road to recovery association of property bankers annual seminar graham emmett head of lending...

TRANSCRIPT

The Road to Recovery

Association of Property Bankers Annual Seminar

Graham EmmettHead of Lending

Tuesday 21st September 2010

Introduction

• Why NAMA

• NAMA Act 2009 & Powers

• Loan transfers

• The NAMA Process

• Business plans & Sales

Why NAMA?• In September 2008 Irish Government Deposit Guarantee put

in place with six irish banks to:– safeguard deposits– remedy serious disturbance caused by worldwide financial crisis– Reduce possibility of systemic bank failure.

• Examination of the Irish banks’ Balance Sheets showed: 40% of total loan book is CRE related (€160bn/€400bn). – Anglo Irish Bank nationalised January 2009– February 2009 Minister for Finance asked Dr. Peter Bacon to prepare

a report outlining options.– Recapitalisations via preference shares followed: €3.5bn in both BOI

(March ‘09) & AIB (May ‘09).– April 2009: Government decided to act on Dr. Bacon’s

recommendation & establish the National Asset Management Agency under the control of the National Treasury Management Agency.

Why NAMA? contd...• NAMA’s aim is to repair impaired Bank balance sheets and

improve liquidity. Achieved by:– taking most impaired loans off bank’s Balance Sheets: i.e Land &

Development loans– deal with the cumulative systemic debtor exposure inherent within

the system i.e all loans.

• NAMA Bonds issued to pay for loans, fresh bank capital. Injected also by Government if necessary.

• September 2009: NAMA Bill introduced in Dail.

• 21 December 2009: NAMA formally established

Why NAMA? contd...• 22 December 2009: NAMA Board appointed

• February 2010: EU approval of NAMA.

• March 2010: Transfer of initial 10 largest debtors (Tranche 1): €15bn of par loans.

NAMA• Five participating institutions (“PI”): AIB, Anglo, BOI, Irish

Nationwide & EBS.

• €81bn ‘eligible assets’ will transfer in 7 Tranches: – Transfers commenced March 2010.– Approx. 1,500 borrowers & 15,000 individual loans.– €27bn transferred (T1 & T2) to date, €12bn expected T3 end Sept ‘10.– Debtor loans from €5m to €2.5bn.– February 2011 EU deadline for the transfer of all tranches.

• NAMA buys par loans at November 2009 values: expected average discounts at inception were 30%. Now average 52% after due diligence.

• Banks revert to core business, assist economic recovery & safeguard Irish banking system.

NAMA contd...

NAMA contd...• NAMA addresses systemic borrower risk.

• Borrowers had loans with all PIs, no measure of total name exposure within the Regulator.

• Lending carried out in haste: inadequate security & documentation.

• NAMA’s key advantages:– Assess borrower’s aggregate exposure to all five banks & underlying

security/documentation.– Objective/No Legacy– Golden circle borrowers.– Act gives NAMA commercial and statutory powers.

NAMA contd...• NAMA is an asset management vehicle: capacity to take long

term view if makes commercial sense. Timeframe to manage and realise these assets is 7 – 10 years.

• Loan acquisition value (“LAV”) consists of:– 95% Government Guaranteed Securities & 5% Subordinated

Securities.– Surplus over LAV accrues to NAMA. – Loss: Banks to make Exchequer good: via non redemption of 5%

Subordinated securities and additional tax surcharge may be imposed.

Staff in NAMA

Independent Board of Directors: 7 members + CEOs NAMA + NTMA. 104 staff by Dec 2010.

NAMA Act 2009 & Powers

NAMA Act 2009• NAMA Act 2009: one of the most complex pieces of

legislation ever enacted by the Irish House of Parliament.

• NAMA is an asset management agency & not a bad bank.

• NAMA acquiring non performing loans and performing from five participating institutions.

• NAMA’s duties: managing and protecting acquired loans/properties and avoiding undue concentration/distortion in the market.

• NAMA is commercial – expected to make a profit of €1bn.

NAMA Powers• NAMA can:

– Provide equity capital and credit facilities as it sees fit;– Initiate enforcement, restructuring, reorganisation (e.g statutory

receiver);– Enter into a partnership or JV to perform its duties;– Acquire and dispose of properties;– Purchase non eligible bank assets if deemed necessary;– Make any planning permission for land;– Undertake development to realise full value of asset;– Do all things as the Board deems necessary to perform its duties.

NAMA CAN CARRY OUT ITS FUNCTIONS WITHIN AND OUTSIDE THE STATE.

• NAMA can apply to the Court for a vesting order & an acquisition order.

• NAMA can appoint a statutory receiver: very wide ranging powers. A Borrower CANNOT remove a Statutory Receiver (Irish Law).

Loan transfers

• Much public debate that NAMA is a bailout mechanism for:a) the Developersb) the Banks

• Widely assumed that NAMA would overpay for loans and continue to fund Developers’ excessive building plans and lifestyles. – Initial average loan discount rates expected to be 35 – 40%.– Actual discount rates of 50% & 56% for T1 & T2.– NAMA paying fair value.– Price of loan is highly correlated with current market value of property.

• NAMA will manage top 100 borrower relationships directly (c.€50bn) & remaining 1,400 (€31bn) will be managed by Participating Institutions, but NAMA will act as Credit Committee.

• PIs continue to act as loans servicer through their NAMA unit in Ireland and London.

Relationship Management Structure

The Valuation Process• Each property valued individually after an intensive property &

legal due diligence process to derive loan value as at Nov 2009.– Potential uplift added to get Long term Economic Value (LEV) if

deemed appropriate by NAMA. Maximum 25% uplift.– LEV is the value that NAMA can reasonably expect to realise on its

acquired assets over a 7 – 10 year horizon.– Further factors considered to arrive at loan value:

» Underlying security and imperfections» Additional collateral offered by debtor» Whether loan is income producing» Value of derivative arrangements (currency/interest

hedging)

• Section 93 Act: if information comes to light post transfer that NAMA valuation incorrect, then rebate process begins.

• Debtor still liable for Par value of loans.

Breakdown of Par Value (€81bn)

Banks Par Loans €bn’s % of Par Value per Bank

AIB 23 28

Anglo 36 45

BOI 12 15

EBS 1 1

Irish Nationwide 9 11

Total 81 100

Summary of Tranches 1 & 2

€bn AIB BOI Anglo INBS EBS Total €bn

Acquired Loans 6.01 3.75 15.99 1.26 0.18 27.19

NAMA € paid to institutions

3.31 2.39 6.72 0.44 0.11 12.97

Discount on Tranches 1 & 2 45% 36% 58% 64% 38% 52%

Breakdown of NAMA Portfolio• Tranche 1 comprised 10 largest Borrowers: €15.3bn Par debt, acquired by

NAMA for €7.7bn: 50% discount.

• Tranche 2 totalled €11.9bn of Par debt, acquired for €5.3bn; 56% discount.

• Total discount for T1 & T2 = 52%

• €27bn Par debt acquired for €12.9bn: €12.9bn liquidity for Irish Banks.

• EU agreed that if NAMA bought loans based on CMV then NAMA would underpay and PIs would lose out on any future market recovery.

=> Act applies some element of “LEV” uplift to ascertain fair and reasonable price.

Breakdown of NAMA Portfolio contd...

RESULT: €12.98bn paid for T1 & T2 which had a total LEV of €14.2bn and CMV €12.86bn: 9% discount on LEV and 1% uplift on CMV. NAMA has 100% Asset Cover.

• End of Sept €12bn is expected in Tranche 3. At this point 50% of total loan value will have transferred. Feb. 2011 EU deadline for all Tranches.

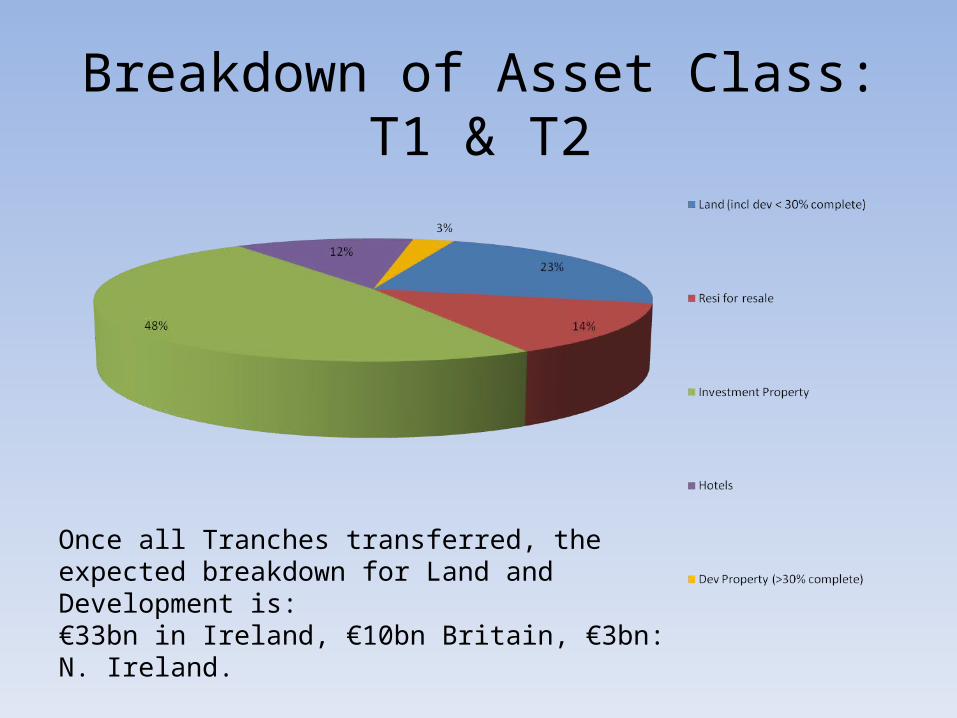

Breakdown of Asset Class: T1 & T2

Once all Tranches transferred, the expected breakdown for Land and Development is:€33bn in Ireland, €10bn Britain, €3bn: N. Ireland.

Geographical Breakdown of T1 & T2

• Expected breakdown of total loans: c.67% of assets will be based in Ireland, 27% in UK (6% in N. Ireland).

The NAMA Process

• NAMA’s remit: manage acquired loans effectively in best interests of the State with overall objective to obtain best financial return subject to acceptable financial risk.

• Financial return must take account of loan acquisition value, NAMA’s running costs + NAMA’s cost of capital.

• Process (typically 3 months):– All debtors must submit a Business Plan within 6 weeks of loan

acquisition: detailed REALISTIC repayment plan (3 – 5 years).– Independent Business Plan Reviewer analyses this plan.– NAMA decides on a course of action and negotiates terms with debtor.

• NAMA will work with debtors if it makes commercial sense but expects FULL CO-OPERATION & FULL DISCLOSURE.

• NAMA will foreclose on Debtors who:– have Business Plans that NAMA deem unviable or are un co-operative or

can’t service their debts.

Types of Borrowers• 2 types of borrowers: COMPLIANT AND NON COMPLIANT.

• Compliant Borrower: provides full disclosure and works to agreed Business Plan => may subsequently be rewarded: e.g Personal Guarantee /Liabilities reduction and Debt restructuring.

• Non Compliant Borrower: fails to meet NAMA strategy=> ENFORCEMENT LIKELY.

• NAMA is not about hoarding assets & waiting for the market to recover. It is about setting debt reduction targets, selling assets to achieve this & for borrowers to prove they have Managerial capacity to deliver on this.

• NAMA has the property expertise to manage properties directly.

Business plans & Sales

• In total, NAMA expects to pay €40.5bn for €81bn par value of loans.

• Just over a week ago, NAMA CEO announced that NAMA in ‘advanced discussions’ with debtors on disposals worth €500m.

• The NAMA Board has set targets for significant debt reduction over a three year period which will have a bearing on future property sales:Year % NAMA Bonds Repaid (€40.5bn)

2013 25

2015 40

2017 80

2018 90

2019 100

• Strategy:– NAMA will reduce its exposure to undeveloped land/partially

completed developments as soon as feasible via public auction.– NAMA will provide new loans where the loans add € for € value & it

makes commercial sense to complete a development.– NAMA will actively seek JV Partners where they own assets directly.– NAMA will take control of assets where debtor is not demonstrating a

value add.– If compliant borrowers, NAMA may agree 3-5 year debt repayment

plan.– NAMA will dispose of assets depending on market conditions and not

engage in speculative hoarding of assets or fire sales.

• NAMA will, where viable, work with debtors to maximise debt repayment.

• All gains accrue to the tax payer: NPV best case €3.9bn, worst case (€0.8bn) and central scenario of €1bn.

• Over the next few years the NAMA plan will have stabilised the Irish economy and:

Ireland will be on the road to recovery

With credit readily available

BUT with more stringent capability testing by banks in place for debtors.

NAMA is an honest solution, recognise losses in the banks, recapitalise and get market moving.

NAMA wants to be innovative, Irish REIT.

Real money Investors – we will be commercial.

Questions?