2013 home ownership and equity protection act...

TRANSCRIPT

1

JANUARY 9, 2014

SMALL ENTITY COMPLIANCE GUIDE

2013 Home Ownership and Equity Protection Act (HOEPA) Rule

2

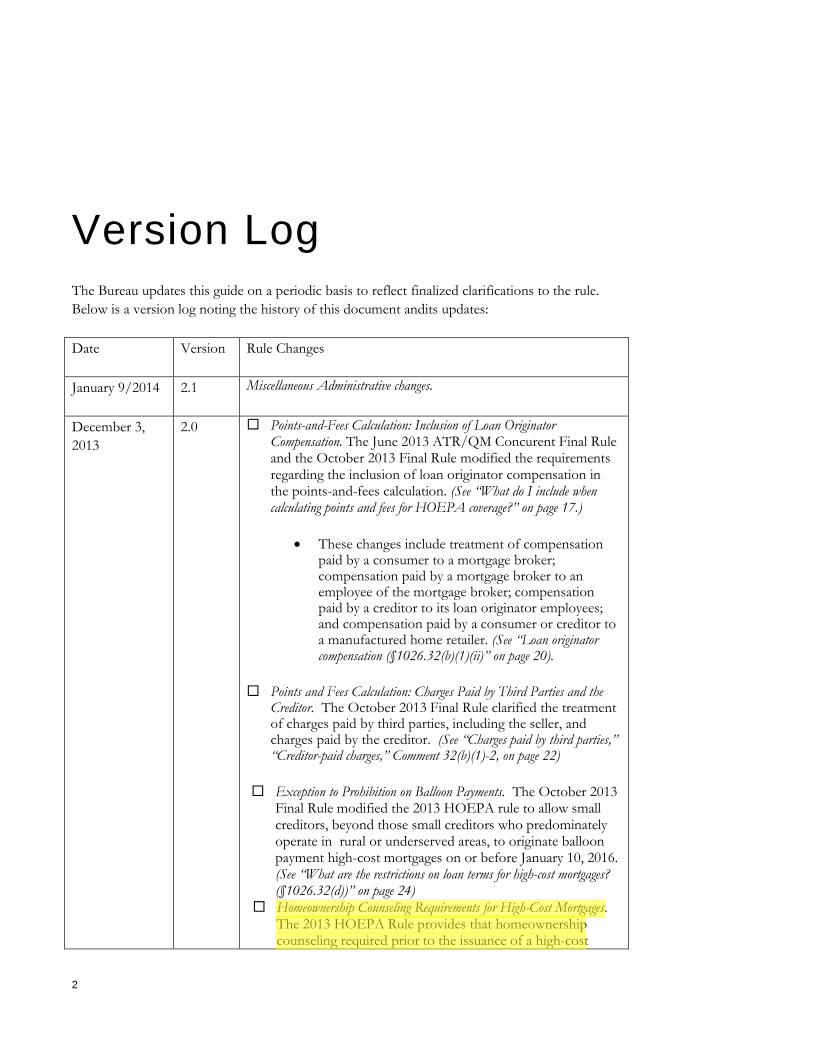

Version Log The Bureau updates this guide on a periodic basis to reflect finalized clarifications to the rule. Below is a version log noting the history of this document andits updates:

Date Version Rule Changes

January 9/2014 2.1 Miscellaneous Administrative changes.

December 3, 2013

2.0 Points-and-Fees Calculation: Inclusion of Loan Originator Compensation. The June 2013 ATR/QM Concurent Final Rule and the October 2013 Final Rule modified the requirements regarding the inclusion of loan originator compensation in the points-and-fees calculation. (See “What do I include when calculating points and fees for HOEPA coverage?” on page 17.)

• These changes include treatment of compensation paid by a consumer to a mortgage broker; compensation paid by a mortgage broker to an employee of the mortgage broker; compensation paid by a creditor to its loan originator employees; and compensation paid by a consumer or creditor to a manufactured home retailer. (See “Loan originator compensation (§1026.32(b)(1)(ii)” on page 20).

Points and Fees Calculation: Charges Paid by Third Parties and the Creditor. The October 2013 Final Rule clarified the treatment of charges paid by third parties, including the seller, and charges paid by the creditor. (See “Charges paid by third parties,” “Creditor-paid charges,” Comment 32(b)(1)-2, on page 22)

Exception to Prohibition on Balloon Payments. The October 2013 Final Rule modified the 2013 HOEPA rule to allow small creditors, beyond those small creditors who predominately operate in rural or underserved areas, to originate balloon payment high-cost mortgages on or before January 10, 2016. (See “What are the restrictions on loan terms for high-cost mortgages? (§1026.32(d))” on page 24)

Homeownership Counseling Requirements for High-Cost Mortgages. The 2013 HOEPA Rule provides that homeownership counseling required prior to the issuance of a high-cost

3

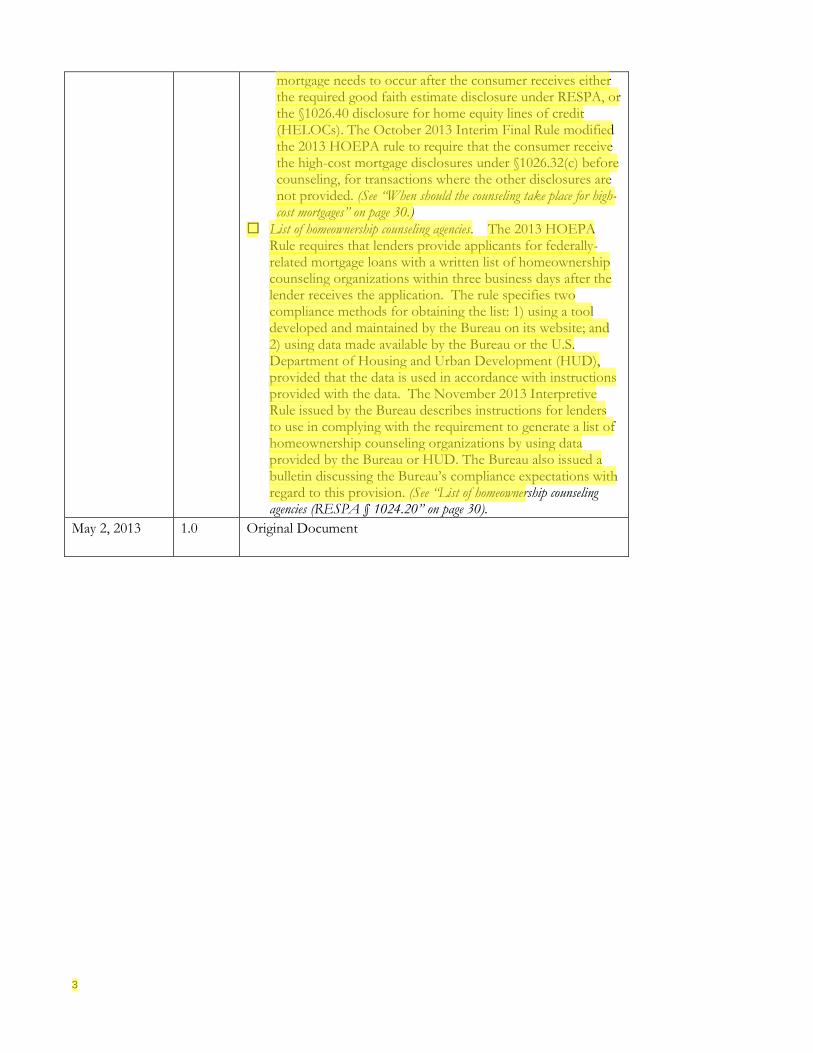

mortgage needs to occur after the consumer receives either the required good faith estimate disclosure under RESPA, or the §1026.40 disclosure for home equity lines of credit (HELOCs). The October 2013 Interim Final Rule modified the 2013 HOEPA rule to require that the consumer receive the high-cost mortgage disclosures under §1026.32(c) before counseling, for transactions where the other disclosures are not provided. (See “When should the counseling take place for high-cost mortgages” on page 30.)

List of homeownership counseling agencies. The 2013 HOEPA Rule requires that lenders provide applicants for federally-related mortgage loans with a written list of homeownership counseling organizations within three business days after the lender receives the application. The rule specifies two compliance methods for obtaining the list: 1) using a tool developed and maintained by the Bureau on its website; and 2) using data made available by the Bureau or the U.S. Department of Housing and Urban Development (HUD), provided that the data is used in accordance with instructions provided with the data. The November 2013 Interpretive Rule issued by the Bureau describes instructions for lenders to use in complying with the requirement to generate a list of homeownership counseling organizations by using data provided by the Bureau or HUD. The Bureau also issued a bulletin discussing the Bureau’s compliance expectations with regard to this provision. (See “List of homeownership counseling agencies (RESPA § 1024.20” on page 30).

May 2, 2013 1.0 Original Document

4

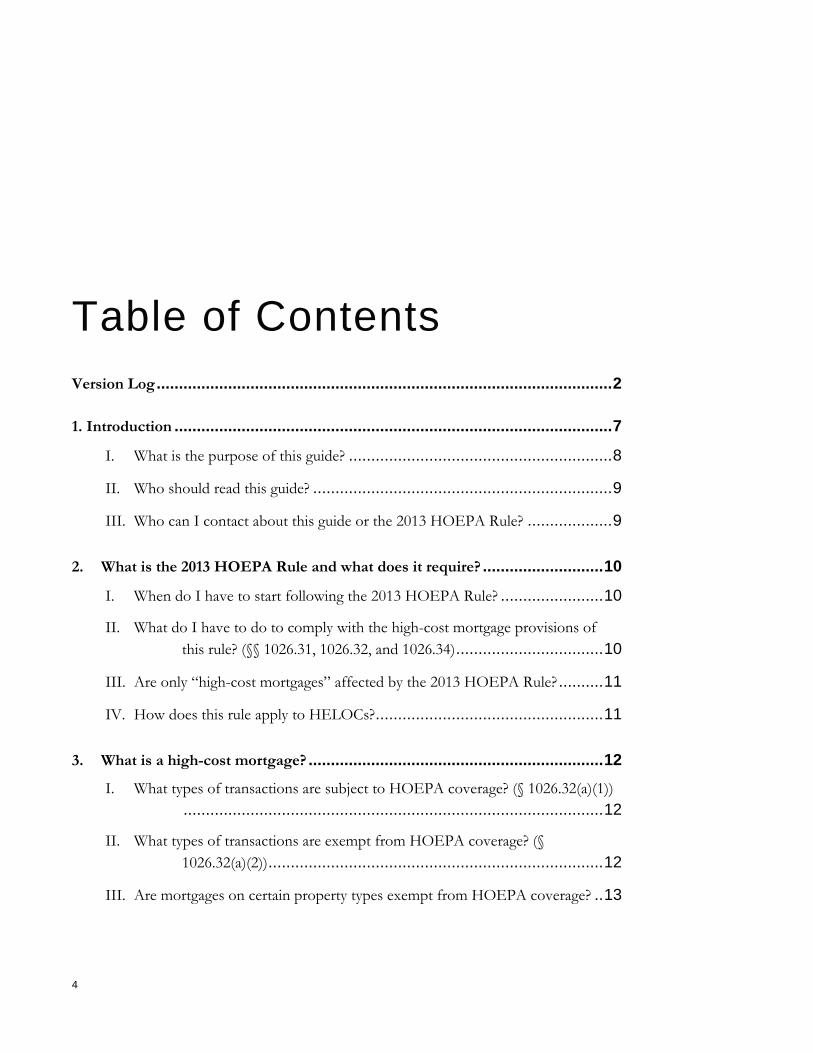

Table of Contents Version Log ...................................................................................................... 2

1. Introduction .................................................................................................. 7

I. What is the purpose of this guide? ........................................................... 8

II. Who should read this guide? ................................................................... 9

III. Who can I contact about this guide or the 2013 HOEPA Rule? ................... 9

2. What is the 2013 HOEPA Rule and what does it require? ........................... 10

I. When do I have to start following the 2013 HOEPA Rule? ....................... 10

II. What do I have to do to comply with the high-cost mortgage provisions of this rule? (§§ 1026.31, 1026.32, and 1026.34) ................................. 10

III. Are only “high-cost mortgages” affected by the 2013 HOEPA Rule? .......... 11

IV. How does this rule apply to HELOCs? ................................................... 11

3. What is a high-cost mortgage? .................................................................. 12

I. What types of transactions are subject to HOEPA coverage? (§ 1026.32(a)(1)) .............................................................................................. 12

II. What types of transactions are exempt from HOEPA coverage? (§ 1026.32(a)(2)) ........................................................................... 12

III. Are mortgages on certain property types exempt from HOEPA coverage? .. 13

5

IV. Coverage tests: How do I determine if a transaction is a high-cost mortgage? (§ 1026.32(a)(1)) ....................................................................... 14

V. How do I calculate the APR for HOEPA coverage? ................................. 15

VI. What is the points-and-fees coverage test?(§ 1026.32(a)(1)(ii)) .................... 16

VII. What do I include when calculating points and fees for HOEPA coverage? (§ 1026.32(b)(1) and (2)) ............................................................ 17

VIII. How does the 2013 HOEPA Rule regulate prepayment penalties? (§1026.32(a)(1)(iii) and 32(d)(6)) .................................................. 22

IX. What is considered a prepayment penalty? (§ 1026.32(b)(6)(i) (closed-end credit) and § 1026.32(b)(6)(ii) (HELOCs)) .................................... 23

4. What are the restrictions on and additional consumer protections for high-cost mortgages? (§§ 1026.32(d) and 1026.34) .............................................. 24

I. What special disclosures are required for high-cost mortgages? (§§ 1026.31 and 1026.32(c)) .............................................................................. 25

II. What are the restrictions on loan terms for high-cost mortgages? (§ 1026.32(d)) .............................................................................................. 25

III. What other acts or practices are prohibited or restricted for high-cost mortgages? .............................................................................. 26

IV. Which existing HOEPA and Regulation Z protections still apply to high-cost mortgages? (§§ 1026.32(d) and 1026.34(a)(1) to (3)) ....................... 27

V. What are the new ability-to-repay requirements for high-cost mortgages? (§ 1026.34(a)(4)) ........................................................................... 28

VI. What are the homeownership counseling requirements for high-cost mortgages? (§ 1026.34(a)(5)(i) to (vi)) ........................................... 29

VII. When should the counseling take place for high-cost mortgages? ............... 30

VIII. Who pays for homeownership counseling for high-cost mortgages? (§ 1026.34(a)(5)(v)) ....................................................................... 31

5. What are the additional homeownership counseling requirements? ............ 32

I. What homeownership counseling requirements apply to creditors regardless of whether or not they make high-cost mortgages? ............................ 32

6

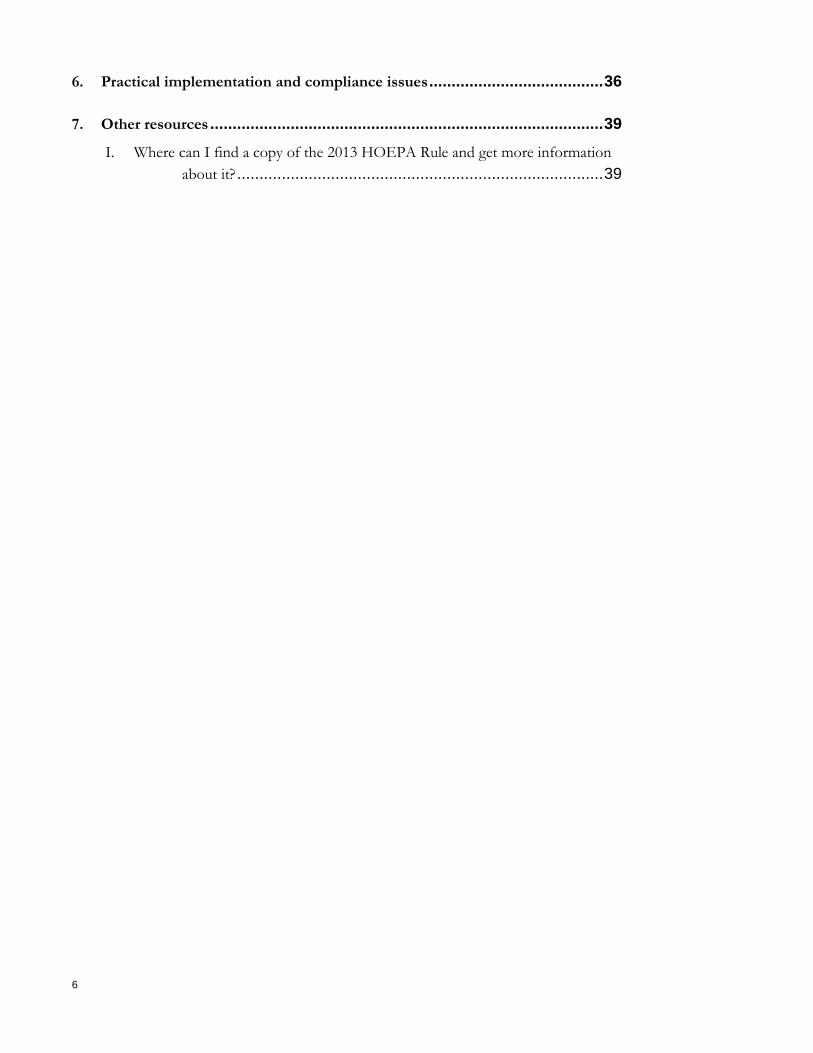

6. Practical implementation and compliance issues ....................................... 36

7. Other resources ........................................................................................ 39

I. Where can I find a copy of the 2013 HOEPA Rule and get more information about it? .................................................................................. 39

7

1. Introduction The Home Ownership and Equity Protection Act (HOEPA) was enacted in 1994 as an amendment to the Truth in Lending Act (TILA) to address abusive practices in refinances and closed-end home equity loans with high interest rates or high fees. Since HOEPA’s enactment, refinances or home equity mortgage loans meeting any of HOEPA’s high-cost coverage tests have been subject to special disclosure requirements and restrictions on loan terms, and consumers with high-cost mortgages have had enhanced remedies for violations of the law.

Historically, these transactions have been referred to as “HOEPA loans” or “Section 32 loans.” This guide refers to such transactions as “high-cost mortgages,” which is consistent with the terminology used in the Dodd-Frank Wall Street Reform and Consumer Protection Act (the Dodd-Frank Act) and the 2013 HOEPA Rule.

In 2010, the Dodd-Frank Act amended TILA by expanding the scope of HOEPA coverage to include purchase-money mortgages and open-end credit plans (i.e., home equity lines of credit, or HELOCs) and amended HOEPA’s coverage tests. Throughout this guide, transactions that may potentially be high-cost mortgages and thus must be tested against HOEPA’s coverage tests are referred to as transactions that are “subject to HOEPA coverage.” The Dodd-Frank Act also added new protections for high-cost mortgages, including a requirement that consumers receive homeownership counseling before obtaining a high-cost mortgage.

In January 2013, the Consumer Financial Protection Bureau issued a rule (referred to throughout this guide as the “2013 HOEPA Rule”) that amends TILA’s Regulation Z to implement the Dodd-Frank Act’s changes to HOEPA.

The 2013 HOEPA Rule also implements two additional Dodd-Frank counseling requirements that may apply to creditors regardless of whether or not they make high-cost mortgages. Specifically, these provisions require or encourage consumers to obtain homeownership counseling for other types of loans. Users of this guide should keep in mind that these homeownership counseling-related requirements are not amendments to HOEPA, but are separate amendments to the Real Estate Settlement Procedures Act ’s (RESPA’s) Regulation X and the Truth in Lending Act ’s (TILA’s) Regulation Z that apply to different types of transactions. These requirements are covered separately in Part 5 of this guide.

8

The Bureau’s June 2013 ATR/QM Concurrent Final Rule, October 2013 Final Rule, October 2013 Interim Final Rule, and November 2013 Interpretive Rule amended and clarified certain provisions of the January 2013 HOEPA rule. All requirements in the 2013 HOEPA Rule will apply to transactions for which you receive an application on or after January 10, 2014.

I. What is the purpose of this guide?

The purpose of this guide is to provide an easy-to-use summary of the Bureau’s 2013 HOEPA Rule. This guide also highlights issues that businesses, in particular small businesses and those that work with them, might find helpful to consider when implementing the rule.

The Bureau anticipates that some creditors will have to make changes to their processes, underwriting guidelines, software, contracts, or other aspects of their business operations in order to comply with this rule. Changes related to this rule may take careful planning, time, or resources to implement. This guide will help you identify and plan for any necessary changes.

The guide summarizes the 2013 HOEPA Rule, but it is not a substitute for the rule. Only the rule and its Official Interpretations can provide definitive information regarding its requirements. The discussions below provide citations to the sections of the rule on the subject being discussed. Keep in mind that the Official Interpretations, which provide detailed explanations of many of the rule’s requirements, are found after the text of the rule and its appendices. The interpretations are arranged by rule section and paragraph for ease of use. The complete rule, as published on January 10, 2013 and the Official Interpretations are available at http://www.consumerfinance.gov/regulations/high-cost-mortgage-and-homeownership-counseling-amendments-to-regulation-z-and-homeownership-counseling-amendments-to-regulation-x/. Additionally, as noted, the CFPB issued several rules to amend and clarify provisions in the January 2013 HOEPA Final Rule: the June 2013 ATR/QM Concurrent Final Rule, the October 2013 Final Rule, the October 2013 Interim Final Rule, and the November 2013 Interpretive Rule.

The focus of this guide is the 2013 HOEPA Rule. This guide does not discuss other federal or state laws that relate to the origination of high-cost mortgages or to homeownership counseling, or other rulemakings implementing Title XIV of the Dodd-Frank Act that take effect at the same time as the 2013 HOEPA Rule.

At the end of this guide, there is more information about where to find the rule and a list of additional resources.

9

II. Who should read this guide? If your organization originates loans secured by a consumer’s primary residence, you may find Part 3 of this guide helpful. It will help you determine whether the transactions you originate are covered by the high-cost mortgage provisions of the 2013 HOEPA Rule, and if so, what your compliance obligations are.

If your organization originates federally-related mortgage loans or makes negative-amortization loans to first-time borrowers, you may find Part 5 of this guide helpful. Part 5 will help you determine when you need to provide mortgage applicants with a list of homeownership counselors, and whether you need to confirm that a first-time borrower has received pre-loan counseling.

III. Who can I contact about this guide or the 2013 HOEPA Rule?

If, after reviewing this guide and the regulation(s) and commentary it addresses, you have a question regarding regulatory interpretation, please email [email protected] with your specific question, including reference to the applicable regulation section(s). If you do not have access to the internet, you may leave this information in a voicemail at 202-435-7700.

Email comments about the guide to [email protected]. Your feedback is crucial to making sure the guide is as helpful as possible. The Bureau appreciates hearing your suggestions for improvements and your thoughts on the guide’s usefulness and readability.

The Bureau is particularly interested in feedback relating to:

How useful you found this guide for understanding the rule

How useful you found this guide for implementing the rule at your business

Suggestions you have for improving the guide, such as additional implementation tips

10

2. What is the 2013 HOEPA Rule and what does it require?

I. When do I have to start following the 2013 HOEPA Rule?

The rule applies to loans for which you receive an application on or after January 10, 2014.

II. What do I have to do to comply with the high-cost mortgage provisions of this rule? (§§ 1026.31, 1026.32, and 1026.34)

When you originate a high-cost mortgage, you must give additional disclosures, avoid certain loan terms, and ensure the consumer receives additional protections, including homeownership counseling.

11

III. Are only “high-cost mortgages” affected by the 2013 HOEPA Rule?

Some parts of the 2013 HOEPA Rule are related to homeownership counseling. These provisions are outlined in Part 5 of this guide. Whether these provisions apply does not depend on whether a loan is a high-cost mortgage. Under these requirements:

Creditors must provide a list of homeownership counseling organizations to most mortgage loan applicants within three days of application. This requirement applies to most types of closed-end and open-end credit transactions, including high-cost mortgages. (See” List of homeownership counseling organizations (RESPA § 1024.20)” on page 33.)

Prior to making a loan that permits negative amortization to a first-time borrower, a creditor must confirm that the consumer received homeownership counseling. This requirement applies to most types of closed-end loans secured by a dwelling, but will not apply to high-cost mortgages (which cannot have negative amortization). (See “Negative-amortization counseling (TILA § 1026.36(k))” on page 32.)

IV. How does this rule apply to HELOCs?

The 2013 HOEPA Rule extends HOEPA coverage to HELOCs. HELOCs will thus need to be analyzed under HOEPA’s coverage tests, and any HELOCs that are high-cost mortgages will be subject to most of the same requirements and restrictions as closed-end, high-cost mortgages.

The 2013 HOEPA Rule provides additional guidance to help creditors apply HOEPA’s coverage tests to HELOCs. For example, in order to complete HOEPA’s annual percentage rate (APR) coverage test for HELOCs, the rule tells creditors how to identify a comparable closed-end transaction It also sets forth special points-and-fees requirements for HELOCs. (See “What is a high-cost mortgage?” on page 12.)

The 2013 HOEPA Rule also provides details to help creditors apply certain HOEPA requirements and restrictions to HELOCs. For example, the rule tells creditors how to calculate a consumer’s ability to repay a high-cost HELOC, as well as how to apply the prohibition against balloon payments to high-cost HELOCs with a draw period and a repayment period. (See “What are the restrictions on and additional consumer protections for high-cost mortgages?” on page 24.)

12

3. What is a high-cost mortgage?

I. What types of transactions are subject to HOEPA coverage? (§ 1026.32(a)(1))

In general, the following types of consumer credit transactions that are secured by a consumer’s principal dwelling are subject to HOEPA coverage under the rule. These types of transactions must be tested against the HOEPA coverage tests. If they meet any of the coverage tests, they must comply with the restrictions on loan terms and other protections relating to high-cost mortgages. These types of transactions are:

Purchase-money mortgages

Refinances

Closed-end home equity loans

Open-end credit plans (i.e., HELOCs)

II. What types of transactions are exempt from HOEPA coverage? (§ 1026.32(a)(2))

The 2013 HOEPA Rule exempts the following types of transactions from HOEPA coverage. You do not need to test these types of transactions against the HOEPA coverage tests. These types of transactions do not need to comply with the restrictions on loan terms and other protections relating to high-cost mortgages. However, these transactions may still be subject to some of the counseling rules discussed in Part 5.

13

Reverse mortgages

Construction loans

Loans originated and directly financed by a Housing Finance Agency (HFA), as defined in 24 CFR 266.5

Loans originated under the U.S. Department of Agriculture’s (USDA’s) Rural Development Section 502 Direct Loan Program

Note, however, that these exemptions can have qualifications:

The exemption for construction loans applies only to loans that finance the initial construction of a new dwelling. It does not extend to loans that finance home improvements or home remodels.

The exemption is straightforward for construction-only loans, but a bit more complicated for construction-to-permanent loans.

o When you make a construction-to-permanent loan as two separate transactions, the construction loan transaction is exempt, but the permanent financing transaction is not. (Comment 32(b)-1)

o For a construction-to-permanent loan originated as a single transaction, coverage must be determined in accordance with appendix D to Regulation Z. (Comment 32(b)-1 and Appendix D)

o The exclusions for HFA and USDA loans apply only to loans that these organizations directly finance, not loans they guarantee or insure.

III. Are mortgages on certain property types exempt from HOEPA coverage?

As discussed above, HOEPA applies to most types of consumer credit transactions secured by a consumer’s principal dwelling. As a result, mortgages secured by vacation or second homes are not covered.

Mortgages secured by manufactured housing (whether titled as real property or personal property) and other types of personal property (e.g., an RV or a houseboat) are subject to HOEPA coverage if the dwelling is the consumer’s primary residence.

14

IV. Coverage tests: How do I determine if a transaction is a high-cost mortgage? (§ 1026.32(a)(1))

If you determine that a transaction is not exempt from HOEPA coverage, then you must apply the HOEPA coverage tests to determine if the transaction is a high-cost mortgage.

There are three separate HOEPA coverage tests, based on:

1. The transaction’s annual percentage rate (APR)

2. The amount of points and fees paid in connection with the transaction

3. The prepayment penalties you may charge under the loan or credit agreement

i. APR coverage test (§ 1026.32(a)(1)(i) and comments 32(a)(1)(i)-1 to -3 and 32(a)(1)(i)(B)-1)

First, determine if a transaction is a high-cost mortgage based on its APR. A transaction is a high-cost mortgage if its APR (measured as of the date the interest rate for the transaction is set) exceeds the Average Prime Offer Rate (APOR) for a comparable transaction on that date by more than:

6.5 percentage points for first-lien transactions, generally

8.5 percentage points for first-lien transactions that are for less than $50,000 and secured by personal property (e.g., RVs, houseboats, and manufactured homes titled as personal property)

8.5 percentage points for junior-lien transactions

ii. Applying the APR coverage test (§ 1026.32(a)(1)(i) and comments 32(a)(1)(i)-1 to -3 and 32(a)(1)(i)(B)-1) First, determine which of the thresholds listed above applies to your transaction.

Next, calculate the APR for your transaction according to the special rules provided in the 2013 HOEPA Rule. (See “How do I calculate the APR for HOEPA coverage?” on page 15.) (§ 1026.32(a)(3))

15

Finally, compare your transaction’s APR to the APOR for a comparable transaction on the same date (i.e., the last date you set – or lock – the interest rate before consummation or account opening). The APOR is published at http://www.ffiec.gov/ratespread. (Comment 32(a)(1)(i)-1)

If the APR for your transaction is more than 6.5 or 8.5 percentage points (as applicable) higher than the APOR, then your transaction is a high-cost mortgage.

For example, if the APOR is 5 percent, a first-lien transaction for $50,000 or more is a high-cost mortgage if it has an APR (calculated according to the special rules for HOEPA coverage) above 11.5 percent.

Creditors originating a HELOC should compare the HELOC’s APR (calculated according to the special rules for HOEPA coverage) to the APOR for the most closely-comparable closed-end transaction. (§ 1026.32(a)(1)(i) and comment 32(a)(1)(i)-2)

To identify the most closely-comparable closed-end transaction, first determine if the HELOC is fixed- or variable-rate. If the HELOC has a variable rate and an optional, fixed-rate feature, the HELOC is a variable-rate transaction for purposes of the APR coverage test.

For a variable-rate HELOC, the most closely-comparable closed-end transaction will be a variable-rate transaction with an initial, fixed-rate period that lasts approximately as long as the introductory period, if any, on the HELOC. (If the HELOC has no initial, fixed-rate period, assume an initial, fixed-rate period of one year.)

For a fixed-rate HELOC, the most closely-comparable closed-end transaction will be a fixed-rate transaction with the same loan term (in years) as the term of the HELOC to maturity. (If the HELOC has no definite plan length, assume a 30-year term until maturity.)

V. How do I calculate the APR for HOEPA coverage? (§ 1026.32(a)(3) and comments 32(a)(3)-1 to -5)

You calculate the APR that you use to determine if a transaction is a high-cost mortgage differently from the APR that you disclose on your TILA disclosures.

For fixed-rate transactions, calculate the APR by using the interest rate in effect on the date you set the interest rate for the transaction.

16

For transactions where the interest rate varies with an index, use the greater of the introductory interest rate (if any) or the fully-indexed rate (i.e., the interest rate that results from adding the maximum margin permitted at any time during the term of the transaction to the value of the index rate in effect on the date you set the interest rate for the transaction).

If the interest rate for the transaction may or will vary other than in accordance with an index, such as in a step-rate loan, use the maximum rate that the applicant may pay during the term of the transaction.

VI. What is the points-and-fees coverage test?(§ 1026.32(a)(1)(ii))

Next, determine if a transaction is a high-cost mortgage based on the transaction’s total points and fees, as defined in § 1026.32(b)(1) and (2). A transaction is a high-cost mortgage if its points and fees exceed the following thresholds:

5 percent of the total loan amount for a loan amount greater than or equal to $20,000

8 percent of the total loan amount or $1,000 (whichever is less) for a loan amount less than $20,000

The $20,000 and $1,000 amounts will be adjusted annually for inflation. The updated figures will be published each year in the commentary to Regulation Z.

Implementation Tip: The threshold for the points-and-fees coverage test varies based on loan size and is higher for smaller transactions.

17

VII. What do I include when calculating points and fees for HOEPA coverage? (§ 1026.32(b)(1) and (2))

i. Closed-end credit transactions (§ 1026.32(b)(1)) To calculate points and fees for HOEPA coverage of closed-end credit transactions, use the same general approach that you use for calculating points and fees for qualified mortgages under the Bureau’s Ability to Repay/Qualified Mortgage Standards under the Truth in Lending Act (Regulation Z). A copy of the ATR/QM Rule is available at http://www.consumerfinance.gov/regulations/ability-to-repay-and-qualified-mortgage-standards-under-the-truth-in-lending-act-regulation-z/. Other Bureau rules amending and clarifying the ATR/QM Rule on points and fees are the June 2013 ATR/QM Concurrent Final Rule, the October 2013 Final Rule, and the October 2013 Interim Final Rule available at http://www.consumerfinance.gov/mortgage-rules-at-a-glance/.

You may also consult the Bureau’s Ability-to-Repay/Qualified Mortgage Rule Small Entity Compliance Guide.

ii. Open-end credit plans (HELOCs) (§ 1026.32(b)(2)) To calculate points and fees for HOEPA coverage of HELOCs, use the same general approach that you use for calculating points and fees for closed-end credit transactions, but include the additional items noted below, if applicable:

Participation fees payable at or before account opening

Fees you charge consumers to draw on their HELOCs (you should assume that the consumer will draw on the credit line at least once)

When deciding whether you have to include a particular fee in your points-and-fees calculation, follow these rules:

iii. Points & Fees Calculation To calculate points and fees, add together the amounts paid in connection with the transaction or the open-end credit plan (as applicable) for the categories of charges listed below:

18

Unless specified otherwise, include amounts that are known at or before consummation (for closed-end transactions) or account opening (for open-end credit plans), even if the consumer pays them after consummation or account opening by rolling them into the loan amount or drawing on the credit line.

In addition, unless specified otherwise, closing costs that you pay and recoup from the consumer over time through the interest rate are not counted in points and fees.

a. Finance charge (§ 1026.32(b)(1)(i)) In general, include all items included in the finance charge (see § 1026.4(a) and (b)). However, you may exclude the following types and amounts of charges, even if they normally would be included in the finance charge:

Interest or the time-price differential

Mortgage insurance premiums (MIPs)

o Federal or state government-sponsored MIPs: For example, exclude up-front and annual FHA premiums, VA funding fees, and USDA guarantee fees.

o Private mortgage insurance (PMI) premiums: Exclude monthly or annual PMI premiums. You may also exclude up-front PMI premiums if the premium is refundable on a prorated basis and a refund is automatically issued upon loan satisfaction. However, even if the premium is excludable, you must include any portion that exceeds the up-front MIP for FHA loans. Those amounts are published in HUD Mortgagee Letters, which you can access on HUD’s website at: http://portal.hud.gov/hudportal/HUD?src=/program_offices/administration/hudclips/letters/mortgagee.

Bona fide third-party charges not retained by the creditor, loan originator, or an affiliate of either (§ 1026.32(b)(1)(i)(D))

o In general, you may exclude these types of charges even if they would be included in the finance charge. For example, you may exclude a bona fide charge imposed by a third-party settlement agent (for example, an attorney) so long as neither the creditor nor the loan originator (or their affiliates) retains a portion of the charge.

o However, you must still include any third-party charges that are specifically required to be included under other provisions of the points-and-fees calculation (for example, certain PMI premiums, certain real estate-related charges, and premiums for certain credit insurance and debt cancellation or suspension coverage).

19

o Note that up-front fees you charge consumers to recover the costs of loan-level price adjustments imposed by secondary market purchasers of loans, including the GSEs, are not considered bona fide third-party charges and must be included in points and fees.

Bona fide discount points (§ 1026.32(b)(1)(i)(E), (F), and 32(b)(3))

o Exclude up to 2 bona fide discount points if the interest rate before the discount does not exceed the APOR for a comparable transaction by more than 1 percentage point; or

o Exclude up to 1 bona fide discount point if the interest rate before the discount does not exceed the APOR for a comparable transaction by more than 2 percentage points.

o For transactions that are secured by personal property, exclude up to 1 or 2 bona fide discount points as set forth above, except compare the interest rate before the discount to the average rate for a loan insured under Title I of the National Housing Act (12 U.S.C. 1702 et seq.), not to the APOR.

Note that a discount point is “bona fide” if it reduces the consumer’s interest rate by an amount that reflects established industry practices, such as secondary mortgage market norms. An example is the pricing in the to-be-announced market for mortgage-backed securities.

iv. Loan originator compensation (§ 1026.32(b)(1)(ii) and comments 32(b)(1)(ii)-1 to -5)

Include compensation paid directly or indirectly by a consumer or creditor to a loan originator other than compensation paid by a mortgage broker, creditor or retailer of manufactured homes to an employee. Include compensation that is attributable to the transaction, to the extent that such compensation is known as of the date the interest rate for the transaction is set. In general, include the following:

Compensation paid directly by a consumer to a mortgage broker: Include the amount the consumer pays directly to the mortgage broker. If this payment is already included in points and fees because it is included in the finance charge under § 1026.32(b)(1)(i), it does not have to be included again as loan originator compensation under § 1026.32(b)(1)(ii).

Implementation Tip: In the context of determining what loan origination compensation must be included in points and fees, a “mortgage broker”refers to both brokerage firms and individual brokers. Compensation paid by a mortgage broker to an employee is not included in points and fees.

20

Compensation paid by a creditor to a mortgage broker: Include the amount the creditor pays to the broker for the transaction. Include this amount even if the creditor included origination or other charges paid by the consumer to the creditor as points and fees under § 1026.32(b)(1)(i) as a finance charge or if the creditor does not receive an up-front payment from the consumer to cover the broker’s fee but rather recoups the fee from the consumer through the interest rate over time.

Compensation paid by a consumer or creditor to a manufactured homeretailer: Include the amount paid by a consumer or creditor to a manufactured home retailer that qualifies as a loan originator under § 1026.36(a)(1) for loan origination activities. Compensation paid by the manufactured home retailer to its employees does not have to be included. (§ 1026.32(b)(1)(ii)(D) and comment 32 (b)(1)(ii)-5).

Compensation included in the sales price of a manufactured home. Include loan originator compensation that the creditor has knowledge is included in the sales price of a manufactured home. The creditor is not required to investigate the sales price of a manufactured home to determine if the sales price includes loan originator compensation. (Comment 32 (b)(1)(ii)-5).

a. Real estate-related fees (§ 1026.32(b)(1)(iii)) The following categories of charges are excluded from points and fees only if:

1. The charge is reasonable;

2. The creditor receives no direct or indirect compensation in connection with the charge; and

3. The charge is not paid to an affiliate of the creditor.

If one or more of those three conditions is not satisfied, you must include these charges in points and fees even if they would be excluded from the finance charge:

Fees for title examination, abstract of title, title insurance, property survey, and similar purposes

Fees for preparing loan-related documents, such as deeds, mortgages, and reconveyance or settlement documents

Notary and credit-report fees

Property appraisal fees or inspection fees to assess the value or condition of the property if the service is performed prior to consummation, including fees related to pest-infestation or flood-hazard determinations

21

Amounts paid into escrow or trustee accounts that are not otherwise included in the finance charge (except amounts held for future payment of taxes)

b. Premiums for credit insurance; credit property insurance; other life, accident, health or loss-of-income insurance where the creditor is beneficiary; or debt cancellation or suspension coverage payments (§ 1026.32(b)(1)(iv))

Include premiums for these types of insurance that are payable at or before consummation even if such premiums are rolled into the loan amount, if permitted by law.

You do not need to include these charges if they are paid after consummation (for example, monthly premiums).

Note that credit property insurance means insurance that protects the creditor’s interest in the property. It does not include homeowner’s insurance that protects the consumer.

You do not need to include premiums for life, accident, health, or loss-of-income insurance if the consumer (or another person designated by the consumer) is the sole beneficiary of the insurance.

c. Maximum prepayment penalty (§ 1026.32(b)(1)(v))

Include the maximum prepayment penalty that a consumer could be charged for prepaying the loan. To determine if you are permitted to charge a prepayment penalty. (See “How does the 2013 HOEPA Rule regulate prepayment penalties?” on page 22.)

d. Prepayment penalty paid in a refinance (§ 1026.32(b)(1)(vi))

If you are refinancing a loan that you or your affiliate currently holds or is currently servicing, then include any penalties you charge consumers for prepaying their previous loans.

22

v. Charges paid by third parties (Comment 32(b)(1)-2) Include charges paid by third parties that fall within the definition of points and fees in § 1026.32(b)(1)(i) through (vi) (discussed above), including charges included in the finance charge. Charges paid by third parties that are excluded from points and fees in § 1026.32(b)(1)(i)(A) though (F) do not have to be included in points and fees. Seller’s points are excluded from the finance charge (see § 1026.4(c)(5)) and therefore can be excluded from points and fees, but charges paid by the seller should be included if they are for items listed as points and fees in § 1026.32(b)(1)(ii) through (vi).

vi. Creditor-paid charges. (Comment 32(b)(1)-2) Charges paid by the creditor, other than loan originator compensation paid by the creditor that is required to be included in points and fees under § 1026.32(b)(1)(ii), can be excluded from points and fees.

VIII. How does the 2013 HOEPA Rule regulate prepayment penalties? (§1026.32(a)(1)(iii) and 32(d)(6))

As required by the Dodd-Frank Act, the 2013 HOEPA Rule adds a prepayment penalty coverage test and also prohibits prepayment penalties for high-cost mortgages. Therefore, the prepayment penalty coverage test below establishes the maximum prepayment penalty amount you may charge and the maximum time frame during which you may charge that prepayment penalty on a transaction that falls within the categories of loans that HOEPA covers. (See “What types of transactions are subject to HOEPA coverage?” on page 12.)

i. Prepayment penalty coverage test (§ 1026.32(a)(1)(iii))

A transaction is a high-cost mortgage if you charge a prepayment penalty:

More than 36 months after consummation or account opening, or

In an amount more than 2 percent of the amount prepaid.

23

IX. What is considered a prepayment penalty? (§ 1026.32(b)(6)(i) (closed-end credit) and § 1026.32(b)(6)(ii) (HELOCs))

For a closed-end credit transaction, a prepayment penalty generally means a charge imposed for paying all or part of the loan’s principal before the date on which the principal is due. For purposes of the 2013 HOEPA Rule, the term “prepayment penalty” means the same thing for a closed-end credit transaction as in the Bureau’s Ability-to-Repay/Qualified Mortgage Rule. (§ 1026.43)

For a HELOC, a prepayment penalty generally means a charge imposed if the consumer terminates the HELOC prior to the end of its term.

The rule does not consider it a prepayment penalty if you pay bona fide third-party charges on a consumer’s behalf on the condition that the consumer does not fully prepay a closed-end credit transaction (or terminate a HELOC) sooner than 36 months after origination.

As discussed above, you should include prepayment penalties in your points-and-fees calculation. Specifically, points and fees include the maximum prepayment penalty amount you may charge on the transaction. If you are refinancing a transaction you currently hold, then points and fees also include any penalties you are charging the consumer for prepaying his previous transaction. (See “What is the points-and-fees coverage test?” on page 16 and “What do I include when calculating points and fees for HOEPA coverage?” on page 17.)

24

4. What are the restrictions on and additional consumer protections for high-cost mortgages? (§§ 1026.32(d) and 1026.34)

If you do not make any transactions that are high-cost mortgages, then you will have no compliance obligations under the remaining HOEPA rules discussed in this section. However, please see the counseling requirements discussed in Part 5, which are not limited to high-cost mortgages.

If you do make high-cost mortgages, you must comply with the rules described in this section and will find it helpful to closely examine §§ 1026.31, 1026.32, and 1026.34. These rules provide several consumer protections for high-cost mortgages, including:

Specific disclosure requirements

Restrictions on transaction terms

Restrictions on fees and practices

Ability-to-repay requirements

A pre-loan counseling requirement

The Truth in Lending Act generally provides consumers with enhanced remedies for violations of these provisions.

25

I. What special disclosures are required for high-cost mortgages? (§§ 1026.31 and 1026.32(c))

The 2013 HOEPA Rule continues to require you to provide a disclosure to consumers at least three business days prior to consummation or account opening of a high-cost mortgage. The disclosure must be in writing and in a form the consumer may keep, and must:

Inform the consumer that the loan will not be effective until consummation or account opening occurs

Explain the consequences of default

Disclose loan terms such as APR, amount borrowed, and monthly payment

In the case of variable-rate loans, explain the maximum monthly payment that may be required under the terms of the loan or credit plan

II. What are the restrictions on loan terms for high-cost mortgages? (§ 1026.32(d))

The rule restricts or bans certain risky loan features for high-cost mortgages, including balloon payments, prepayment penalties, and due-on-demand features. It also leaves several existing HOEPA protections unchanged.

i. Balloon payments Balloon payments are generally banned for high-cost mortgages and allowed in four circumstances: (§ 1026.32(d)(1))

1. The payment schedule is adjusted to accommodate the consumer’s seasonal or irregular income. (§ 1026.32(d)(1)(A))

2. The loan is a short-term bridge loan (12 months or less) to finance a new home purchase for a consumer selling an existing home. (§ 1026.32(d)(1)(B))

Implementation Tip: There is required wording you must include in this disclosure, which you will find in § 1026.32(c)(1). In addition, appendix H to Regulation Z also contains some sample disclosures. Sample H-16 illustrates the disclosures required under § 1026.32(c).

26

3. The creditor meets criteria for a small creditor predominantly serving a rural or underserved area, and the loan meets specific criteria set forth in the Bureau’s Ability-to-Repay/Qualified Mortgage Rule. (§§ 1026.32(d)(1)(C) and 1026.43(f))

4. Only for loans made on or before January 10, 2016, the creditor meets the criteria for a small creditor -- regardless of whether it operates predominately in rural or underserved areas -- and the loan meets the specific criteria for qualified mortgages set forth in the Bureau’s Ability-to-Repay/Qualified Mortgage Rule. (§§ 1026.32(d)(1)(ii)(C) and 1026.43(e)(6).)

For additional guidance on determining when a transaction may be considered to have a balloon payment, see comments 32(d)(1)(i)-1 to -3.

ii. Prepayment penalties (§ 1026.32(d)(6)) Prepayment penalties are banned for high-cost mortgages. (See “How does the 2013 HOEPA rule regulate prepayment penalties?” on page 22.)

iii. Due-on-Demand Features (§ 1026.32(d)(8)) Due-on-demand features that allow for acceleration in high-cost mortgages are allowed only in cases where:

The consumer commits fraud or makes a material misrepresentation in connection with the loan or credit agreement.

The consumer defaults on payment.

The consumer’s action or inaction adversely affects your security interest for the loan.

III. What other acts or practices are prohibited or restricted for high-cost mortgages?

The 2013 HOEPA Rule places these additional restrictions and prohibitions on high-cost mortgages:

Creditors and mortgage brokers are prohibited from recommending default on an existing loan to be refinanced by a high-cost mortgage. (§ 1026.34(a)(6) and comments 34(a)(6)-1 and -2)

Creditors, servicers, and assignees cannot charge a fee to modify, defer, renew, extend, or amend a high-cost mortgage. (§ 1026.34(a)(7))

27

Late fees are restricted to 4 percent of the past due payment, and pyramiding of late fees is prohibited. There are rules for imposing late fees when a consumer resumes making payments after missing one or more payments. (§ 1026.34(a)(8) and comments 34(a)(8)(i)-1, 34(a)(8)(iii)-1, and 34(a)(8)(iv)-1)

Fees for generation of payoff statements are generally banned, with limited exceptions. (§ 1026.34(a)(9))

Points and fees cannot be financed (i.e., rolled into the loan amount). However, you can finance closing charges excluded from the definition of points and fees, such as bona fide third-party charges. (See “What do I include when calculating points and fees for HOEPA coverage?” on page 17.) (§ 1026.34(a)(10) and comments 34(a)(10)-1 and -2)

You cannot purposely structure a transaction to evade HOEPA coverage (for example, splitting a loan into two loans to divide the loan fees to avoid the points-and-fees threshold). (§ 1026.34(b) and comments 34(b)-1 and -2)

IV. Which existing HOEPA and Regulation Z protections still apply to high-cost mortgages? (§§ 1026.32(d) and 1026.34(a)(1) to (3))

HOEPA and Regulation Z prohibit the following loan terms for high-cost mortgages, which the final rule leaves unchanged:

Negative amortization (§ 1026.32(d)(2))

A payment schedule that consolidates more than two periodic payments and pays them in advance from loan proceeds (§ 1026.32(d)(3))

An increase in the interest rate after default (§ 1026.32(d)(4))

In the case of acceleration as a result of default in payment, a refund of interest calculated in a manner less favorable to the consumer than the actuarial method (§ 1026.32(d)(5))

The 2013 HOEPA Rule also leaves these HOEPA and Regulation Z prohibitions unchanged:

28

Paying a contractor under a home-improvement contract from the proceeds of a high-cost mortgage (with certain exceptions) (§ 1026.34(a)(1))

Selling a high-cost mortgage in the secondary market without providing a high-cost mortgage notice to the assignee (§ 1026.34(a)(2))

Refinancing any high-cost mortgage into another high-cost mortgage within one year after having extended credit, unless the refinancing is in the consumer’s interest (§ 1026.34(a)(3))

V. What are the new ability-to-repay requirements for high-cost mortgages? (§ 1026.34(a)(4))

The rule requires you to determine a consumer’s ability to repay a high-cost mortgage prior to consummation or account opening. There are different rules for closed-end high-cost mortgages (i.e., loans taken out to purchase a home or refinance an existing mortgage) and open-end high-cost mortgages (HELOCs).

i. Closed-end credit transactions (§§ 1026.34(a)(4) and 1026.43)

Historically, regulations implementing HOEPA have prohibited creditors from extending high-cost mortgages without regard to the consumer’s repayment ability. The Dodd-Frank Act established new ability-to-repay requirements for most closed-end mortgage loans, including high-cost mortgages.

These new requirements were implemented in the Bureau’s Ability-to-Repay/Qualified Mortgage Rule. A copy of that rule is available at http://www.consumerfinance.gov/regulations/ability-to-repay-and-qualified-mortgage-standards-under-the-truth-in-lending-act-regulation-z/.

In light of these new requirements, creditors that originate closed-end high-cost mortgages are required to satisfy the same ability-to-repay requirements as other closed-end mortgages under § 1026.43. You may also find it helpful to consult the Bureau’s Ability-to-Repay and Qualified Mortgage Rule Small Entity Compliance Guide.

Note that the Bureau’s Ability-to-Repay/Qualified Mortgage Rule allows for a loan that meets the criteria for a qualified mortgage but that is a high-cost mortgage because of its APR to be considered a qualified mortgage. Thus, it is possible for a loan with a rate that exceeds the HOEPA rate threshold to be a qualified mortgage if the loan otherwise meets the qualified mortgage criteria.

29

A qualified mortgage that is also a high-cost mortgage would be eligible for a presumption of compliance with the Ability-to-Repay/Qualified Mortgage Rule. Closed-end high-cost mortgages that do not meet the criteria for a qualified mortgage will receive no presumption of compliance with the ability-to-repay requirements.

ii. Open-end high-cost mortgages (HELOCs) (§ 1026.34(a)(4) and comments 34(a)(4)-1 to -7 and 34(a)(4)(ii)(B)-1)

The new Dodd-Frank Act ability-to-repay requirements do not apply to HELOCs. Thus, for open-end high-cost mortgages, repayment ability will still be determined using HOEPA’s ability-to-repay rules (which have been revised in the 2013 HOEPA Rule to apply to HELOC transactions). (§ 1026.34(a)(4)(i) to (iv)) These criteria are similar to those found in the pre-Dodd-Frank Act Section 34 of Regulation Z.

In general, you must consider the consumer’s:

Current and reasonably expected income or assets (verified with W-2s, tax returns, payroll receipts, financial institution records, or other third-party documents that provide reasonably reliable evidence) (§ 1026.34(a)(4)(ii)(A))

Current obligations, including any mortgage-related obligations such as property taxes, required insurance premiums, community association fees, ground rent, and leasehold payments (§ 1026.34(a)(4)(i) and (ii)(B) and comments 34(a)(4)-1 to -7 and 34(a)(4)(ii)(B)-1)

These repayment-ability provisions still provide for a presumption of compliance if specified criteria are met. (§ 1026.34(a)(4)(iii) and (iv) and comments 34(a)(4)(iii)-1 and -2)

For more information, see § 1026.34(a)(4)(i) to (iv) and related commentary.

VI. What are the homeownership counseling requirements for high-cost mortgages? (§ 1026.34(a)(5)(i) to (vi))

Prior to making a high-cost mortgage, you must receive written certification that the consumer has received homeownership counseling on the advisability of the mortgage from a HUD-approved counselor or a state housing finance authority, if permitted by HUD.

30

The homeownership counselor cannot be affiliated with or employed by your organization. You cannot steer the consumer to a particular counseling agency. (§ 1026.34(a)(5)(iii), (iv), and comments 34(a)(5)(vi)-1 and -2)

VII. When should the counseling take place for high-cost mortgages?

The consumer will need to have received either the RESPA good-faith estimate or the disclosures required under § 1026.40 for HELOCs before the homeownership counseling session on the advisability of the mortgage. For transactions where neither the RESPA good-faith estimate or the § 1026.40 disclosure for HELOCs is provided, counseling must occur after the consumer receives the disclosures required for high-cost mortgages under §1026.32(c).

Note that the homeownership counselor must verify that the consumer received all of the high-cost mortgage disclosures or the disclosures required under RESPA, including the settlement disclosures, before the counselor can issue the certification of counseling.

Because the consumer typically gets some of these documents at or just before closing, it may be best for counseling to occur in two stages:

1. In the first stage, the consumer receives counseling on the mortgage after receipt of the initial good-faith estimate or § 1026.40 disclosure, or the high-cost mortgage disclosures under § 1026.32(c), if necessary.

2. In the second stage, the consumer has a second contact with the counselor, so the counselor can verify receipt of all the additional required disclosures prior to issuing certification.

The high-cost mortgage disclosures under § 1026.32(c) are required to be provided at least three business days before closing. For closed-end, non-RESPA transactions where only the high-cost mortgage disclosures under §1026.32(c) are provided, the creditor may wish to provide the disclosures sooner to provide sufficient time for the counseling and the written certification that the consumer has received the counseling. (Comment 34(a)(5)(ii)-2).

Note that the rule does not require in-person counseling. Counseling may be provided via telephone, so long as it is provided by a HUD-approved counselor. A self-study program may not be used to satisfy the counseling requirement.

The counselor can send you the written certification via mail, email, or facsimile, so long as the certification is in a retainable form. (§ 1026.34(a)(5)(i) and comment 34(a)(5)(i)-4)

31

VIII. Who pays for homeownership counseling for high-cost mortgages? (§ 1026.34(a)(5)(v))

You can pay the counseling fee for the consumer, but you cannot condition payment on the consumer getting the high-cost loan. Consumers can pay the fee themselves, or they can finance the fee as part of the mortgage transaction if the fee is a bona-fide third-party charge. (Comment 34(a)(5)(v)-1)

32

5. What are the additional homeownership counseling requirements?

I. What homeownership counseling requirements apply to creditors regardless of whether or not they make high-cost mortgages?

In addition to the pre-loan counseling requirement for high-cost mortgages, the 2013 HOEPA Rule implements two other Dodd-Frank Act homeownership counseling provisions:

1. An amendment to Regulation Z (TILA) that requires pre-loan counseling for negative-amortization loans made to first-time borrowers

2. An amendment to Regulation X (RESPA) that requires you to give federally-related loan applicants a list of housing counselors

i. Negative-amortization counseling (TILA § 1026.36(k))

You must obtain sufficient documentation showing that a first-time borrower has received homeownership counseling prior to making most types of closed-end, dwelling-secured loans that permit negative amortization. You cannot steer the consumer to a particular counselor or counseling agency. A few things to note concerning this rule:

It is specific to first-time borrowers and does not apply to consumers who have taken out mortgages before.

33

It does not apply to high-cost mortgages since negative amortization is prohibited for high-cost mortgages.

Like the HOEPA counseling requirement, the counselor must be federally-certified or approved. You must receive documentation that the consumer has obtained pre-loan counseling before making the loan.

ii. List of homeownership counseling organizations (RESPA § 1024.20)

The final rule contains a new requirement that you must give applicants for federally-related mortgages (whether or not a high-cost mortgage) a written list of homeownership counseling organizations within three business days of receiving the application. Applicants for reverse mortgages and loans f or time-shares are excluded.

In order to comply, you have two options for obtaining the list required to be provided to loan applicants:

Use a tool developed and maintained by the Bureau on its website, www.consumerfinance.gov/find-a-housing-counselor (which uses U.S. Department of Housing and Urban Development (HUD) data on HUD-approved counseling agencies) (§ 1024.20(a)(1)(i)) or

Use data made available by the Bureau or HUD, provided that the data is used in accordance with instructions provided with the data. (§ 1024.20(a)(1)(ii)))

See the Bureau’s November 2013 Interpretive Rule (“Homeownership Counseling Organizations Lists Interpretive Rule”), describing data instructions for lenders to use in complying with the § 1024.20(a)(1)(ii) requirement to generate a list of counseling organizaions by using data provided by the Bureau or HUD. The following summarizes those instructions:

The list of housing counseling agencies provided to each consumer must comply with the following general requirements:

You must provide a list of ten HUD-approved housing counseling agencies.. The tool maintained by the Bureau will generate a list of ten HUD-approved housing counseling agencies.

Implementation Tip: The Regulation X homeownership counseling provisions (as opposed to the pre-loan counseling requirements for high-cost mortgages and negative-amortization loans) require you only to provide consumers with a list of counseling resources. It is up to these consumers to decide if they want to get counseling—the rule does not require them to do so.

34

It must list the ten counseling agencies that are closest to the centroid of the zip code of the borrower’s current address, in descending order of proximity to the centroid. Lenders, should they choose may offer borrowers the option of generating the list from a zip code different from their home address, or from amore precise geographic marker such as a street address but they are not required to do so. The Bureau’s tool will permit generating the list of HUD-approved housing counseling agencies through entry of a zip code.

It must contain the following data fields on each counseling agency to the extent they are available through HUD’s application programming interface ( HUD API) containing data on HUD-approved housing counseling agencies–

o Agency name

o Phone number

o Street address

o Street address continued

o City

o State

o Zip code

o Website URL

o Email address

o Counseling services provided

o Languages spoken

The list must include the following text: “The counseling agencies on this list are approved by the U.S. Department of Housing and Urban Development (HUD), and they can offer independent advice about whether a particular set of mortgage loan terms is a good fit based on your objectives and circumstances, often at little or no cost to you. This list shows you several approved agencies in your area. You can find other approved counseling agencies at the Consumer Financial Protection Bureau’s (CFPB) website: .consumerfinance.gov/mortgagehelp or by calling 1-855-411-CFPB (2372). You can also access a list of nationwide HUD-approved counseling intermediaries at http://portal.hud.gov/hudportal/HUD?src=/ohc_nint. .

Please Note: On November 8, 2013 the Bureau issued a CFPB Bulletin 2013-13 which included the following statements:

35

“The 2013 HOEPA Final Rule requires lenders to provide applicants for federally-related mortgages with a written list of HUD-approved housing counseling agencies. A lender may fulfill the requirement in one of two ways: the lender may obtain the lists through the Bureau’s website, www.consumerfinance.gov/find-a-housing-counselor; or, in the alternative, the lender may generate lists by independently using the same HUD data that the Bureau uses on HUD-approved counseling agencies, in accordance with Bureau’s list instructions. The Bureau published an interpretative rule on November 8, 2013, which provides the list instructions and clarifies how lenders may generate their own lists.

The Bureau’s website is available for lenders who opt to use the first alternative means of providing the lists to consumers on the January 10, 2014 effective date. However, lenders who prefer to adopt the second alternative have informed the Bureau that they must undertake significant development of compliance systems to ensure that lists are generated in compliance with the RESPA Homeownership Counseling Amendments and the November interpretive rule. The Bureau understands that the systems development may take approximately six months. Thus, these lenders appear unable to provide the lists under the second alternative approach in time for the rule’s January 10, 2014 effective date.

Accordingly, while lenders are incorporating § 1024.20(a)(1)(ii) list instructions into their systems, they may direct borrowers to the Bureau’s housing counseling agency website to obtain a list of housing counselors, using the format and text suggested below, www.consumerfinance.gov/find-a-housing-counselor. These steps, if taken by lenders in good faith while they are building their systems or are working with vendors to build systems, would achieve the goals of the regulation and would not raise supervisory or nforcement concerns. Following is the suggested text to be used for this interim procedure:

‘Housing counseling agencies approved by the U.S. Department of Housing and Urban Development (HUD) can offer independent advice about whether a particular set of mortgage loan terms is a good fit based on your objectives and circumstances, often at little or no cost.

If you are interested in contacting a HUD-approved housing counseling agency in your area, you can visit the Consumer Financial Protection Bureau’s (CFPB) website, www.consumerfinance.gov/find-a-housing-counselor, and enter your zip code.

You can also access HUD’s housing counseling agency website via www.consumerfinance.gov/mortgagehelp.

For additional assistance with locating a housing counseling agency, call the CFPB at 1-855-411-CFPB (2372).”

36

6. Practical implementation and compliance issues

You should consult with legal counsel or your compliance officer to understand your obligations under the rule and to devise the policies and procedures you will need to have in place to comply with the rule’s requirements.

How you comply with the 2013 HOEPA Rule may depend on your business model. When mapping out your compliance plan, you should consider practical implementation issues in addition to understanding your obligations under the rule.

Your implementation and compliance plan may include:

1. Identifying affected products, departments, and staff

Your organization may offer some, or all, of the loan products discussed in the 2013 HOEPA Rule. To begin planning for compliance with the rule, you may find it useful to identify all affected products, departments, and staff.

2. Identifying the business-process, operational, and technology changes that will be necessary for compliance

Fully understanding the changes required may involve a review of your existing business processes, as well as the hardware and software that you, your agents, or other business partners use. Gap analyses may be a helpful output of such a review and can help to inform a robust implementation plan. For example, even if your organization does not originate high-cost loans, you will need to update your systems and processes which execute the HOEPA coverage tests to ensure compliance with the criteria as defined in this rule.

3. Identifying impacts on key service providers or business partners

37

Third-party updates may be necessary to update transaction coverage and calculations; to obtain required information or verifications; to incorporate new disclosures; and to make sure your underwriting software, compliance, quality-control, and recordkeeping protocols comply with this rule.

Software providers, or other vendors and business partners, may offer compliance solutions that can assist with any necessary changes. These key partners will depend on your business model. For example, banks and credit unions may find it helpful to talk to their correspondent banks, secondary market partners, and technology vendors. In some cases, you may need to negotiate revised or new contracts with these parties, or seek a different set of services.

If you seek the assistance of vendors or business partners, make sure you understand the extent of the assistance they provide. For example, if vendors provide software that calculates loan cost to determine which loans are subject to the rule, do they guarantee the accuracy of their conclusions?

The CFPB expects supervised banks and nonbanks to have an effective process for managing the risks of service provider relationships. For more information on this, view CFPB Bulletin 2012-03 - Service Providers.

4. Identifying training needs

Consider the training that will be necessary for your loan-officer, secondary marketing, processor, compliance, and quality-control staff, as well as anyone else who approves, processes, or monitors credit loans. Training may also be required for other individuals you, your agents, or your business partners employ.

5. Considering other Title XIV rules

The 2013 HOEPA Rule is just one component of the Bureau’s Dodd-Frank Act Title XIV rulemakings.

Other Title XIV rules include:

Ability-to-Repay and Qualified Mortgage Rule

ECOA Valuations Rule

TILA Higher-Priced Mortgage Loans Appraisal Rule

Loan Originator Rule

RESPA and TILA Mortgage Servicing Rules

TILA Higher-Priced Mortgage Loans Escrow Rule

38

Each of these rules affects aspects of the mortgage industry and its regulation. Many of these rules intersect with one or more of the others. Therefore, the compliance considerations for these rules may overlap in your organization. You will find copies of these rules online at http://www.consumerfinance.gov/regulations/.

39

7. Other resources

I. Where can I find a copy of the 2013 HOEPA Rule and get more information about it?

You will find the 2013 HOEPA Rule on the Bureau’s website at http://www.consumerfinance.gov/regulations/high-cost-mortgage-and-homeownership-counseling-amendments-to-regulation-z-and-homeownership-counseling-amendments-to-regulation-x/.

In addition to a complete copy of the January 2013 final rule, that web page also contains:

The preamble, which explains why the Bureau issued the rule; the legal authority and reasoning behind the rule; responses to comments; and analysis of the benefits, costs, and impacts of the rule

Official Interpretations of the rule

Links to final rule amendments, including the June 2013 ATR/QM Concurrent Final Rule, the October 2013 Final Rule, the October 2013 Interim Final Rule and the November 2013 Interpretive Rule.

Other implementation support materials including videos and proposed rule amendments

Useful resources related to regulatory implementation are also available at http://www.consumerfinance.gov/regulatory-implementation/.

For email updates about Bureau regulations and when additional Dodd-Frank Act Title XIV implementation resources become available, please submit your email address within the “Email updates about mortgage rule implementation” box here.