african markets revealed — january 2012... · advanced economies growing at 1.9% in 2012, but we...

TRANSCRIPT

African Markets Revealed — January 2012

Fixed Income Research

Index

African markets Rolling with the punches 3

Angola Managing expansion 16

Botswana Commodity cycle to dominate sentiment 20

Côte d’Ivoire Strong post-crisis rebound 24

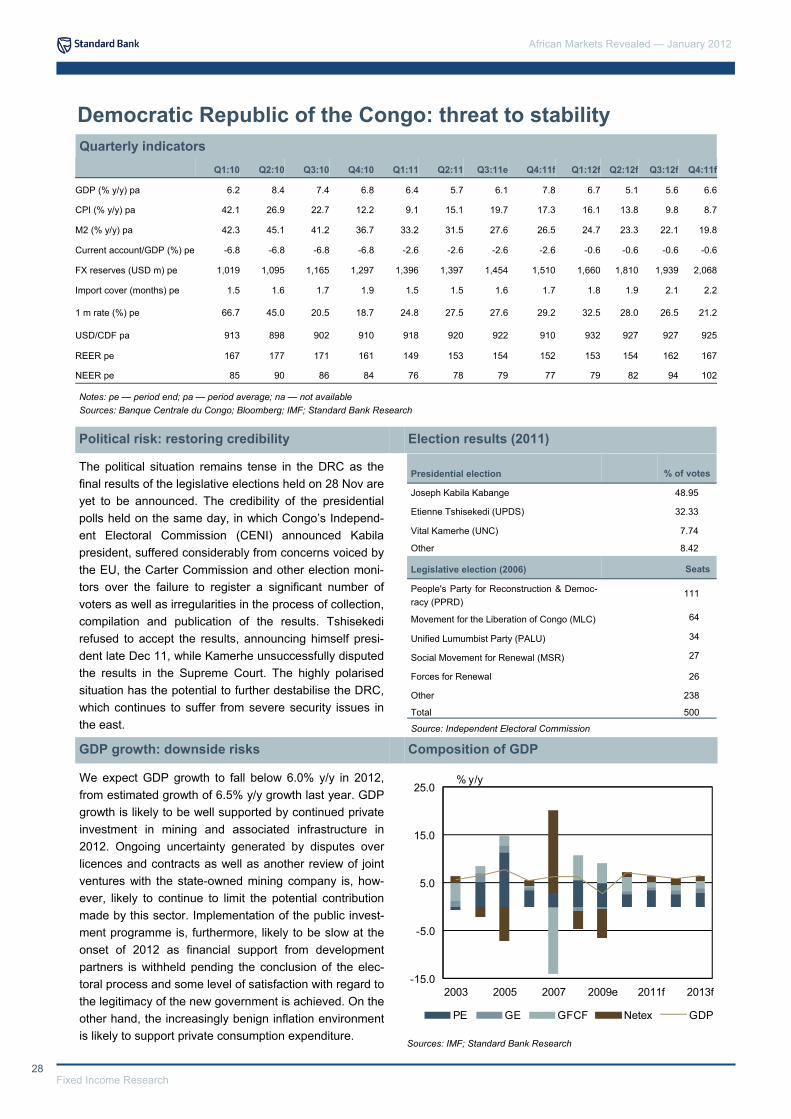

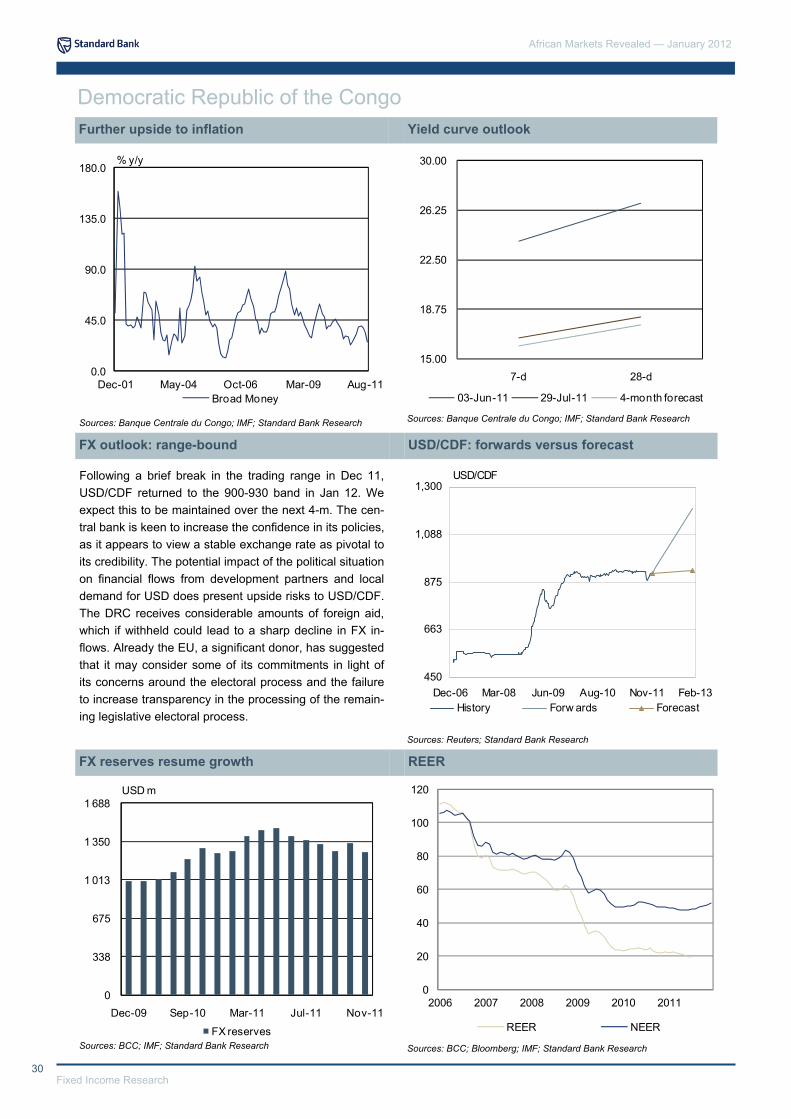

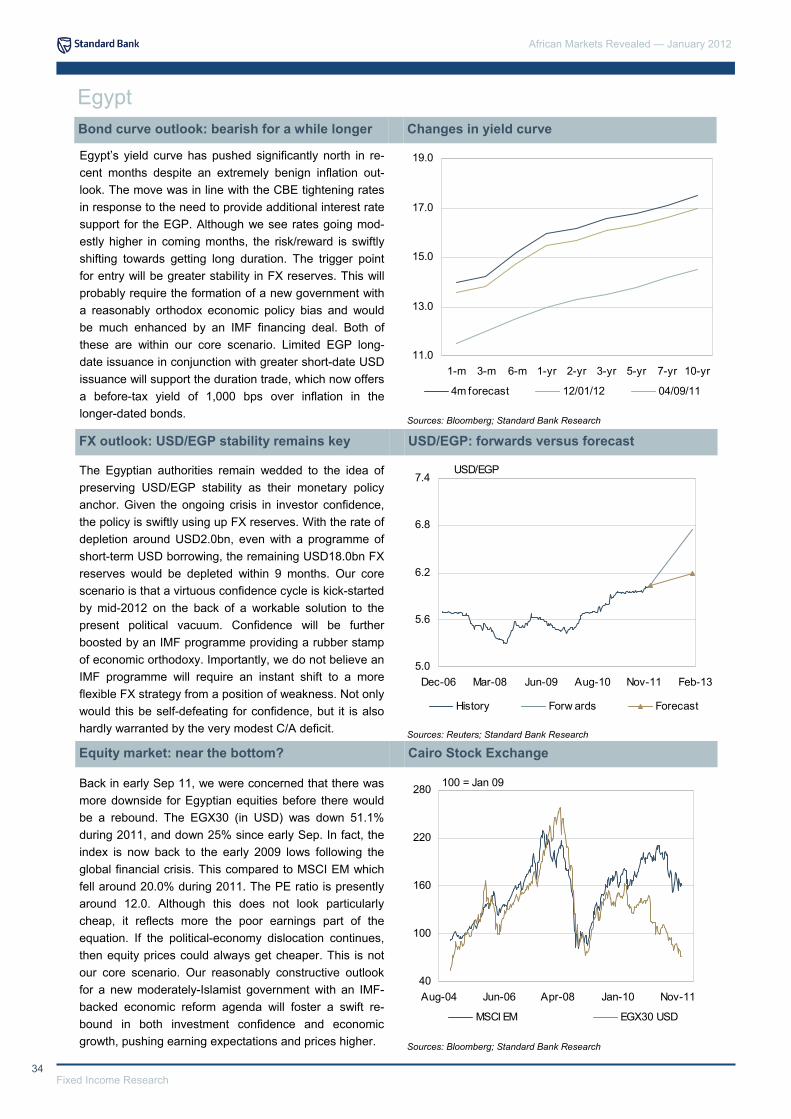

Democratic Republic of the Congo Threat to stability 28

Egypt New political dawn 32

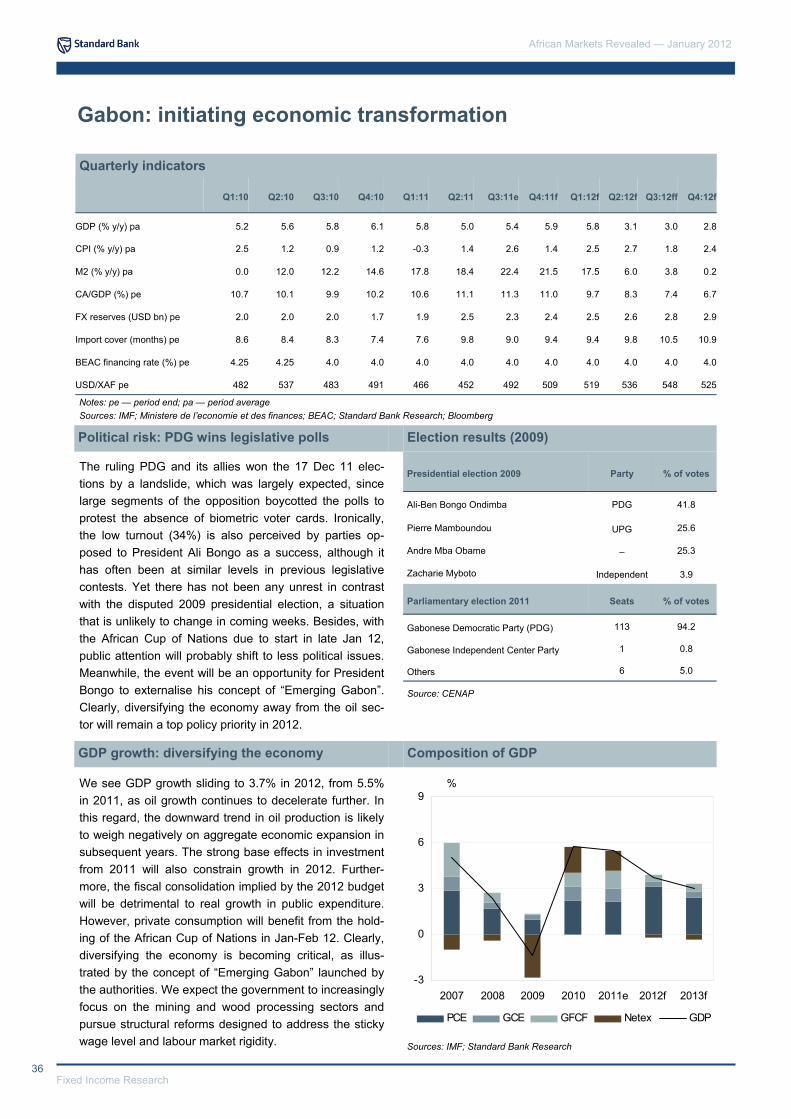

Gabon Initiating economic transformation 36

Ghana Seeking Goldilocks 40

Kenya Let the yield compression games begin 44

Malawi Subdued outlook for the economy 48

Mauritius Economic resilience pays off 52

Mozambique Moving to more accommodative policies 60

Namibia Commodity cycle to impact output growth 64

Nigeria Pushing through structural reforms 68

Republic of the Congo Output diversification is key 72

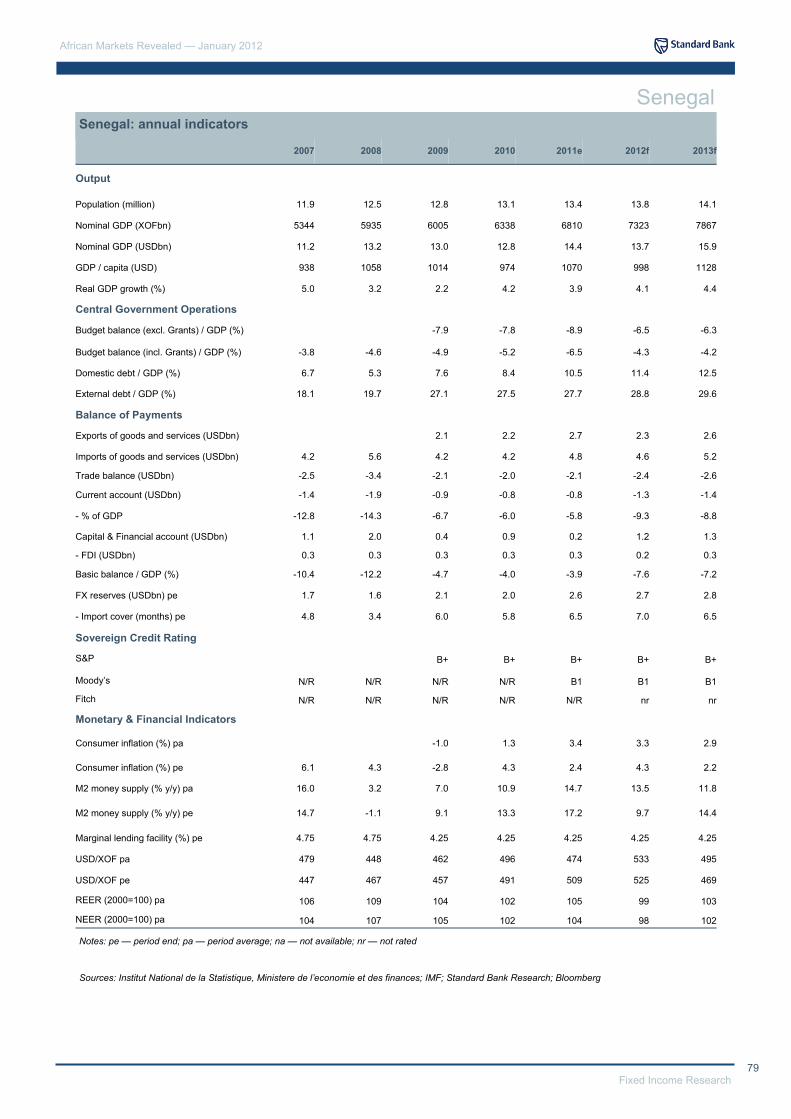

Senegal Decision time 76

South Africa Keeping its head above water 80

Tanzania Economic growth moderating 84

Uganda Policy focused on macroeconomic stabilisation 92

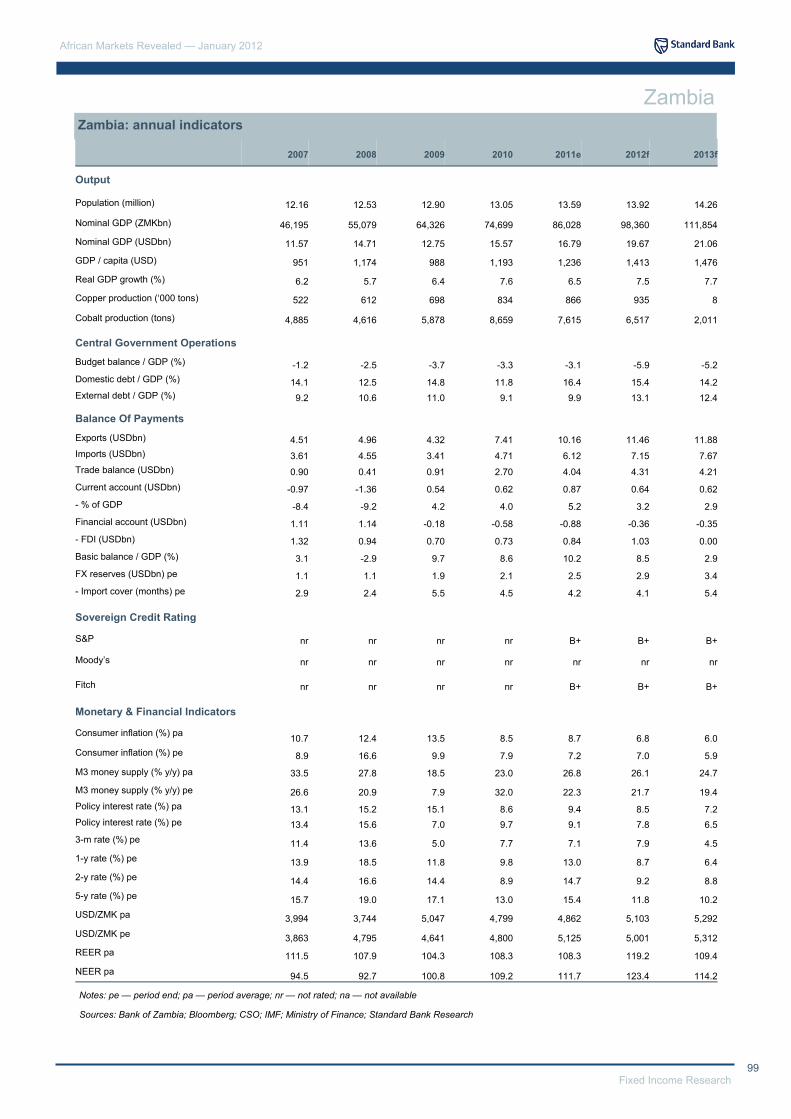

Zambia A new day, a new dawn 96

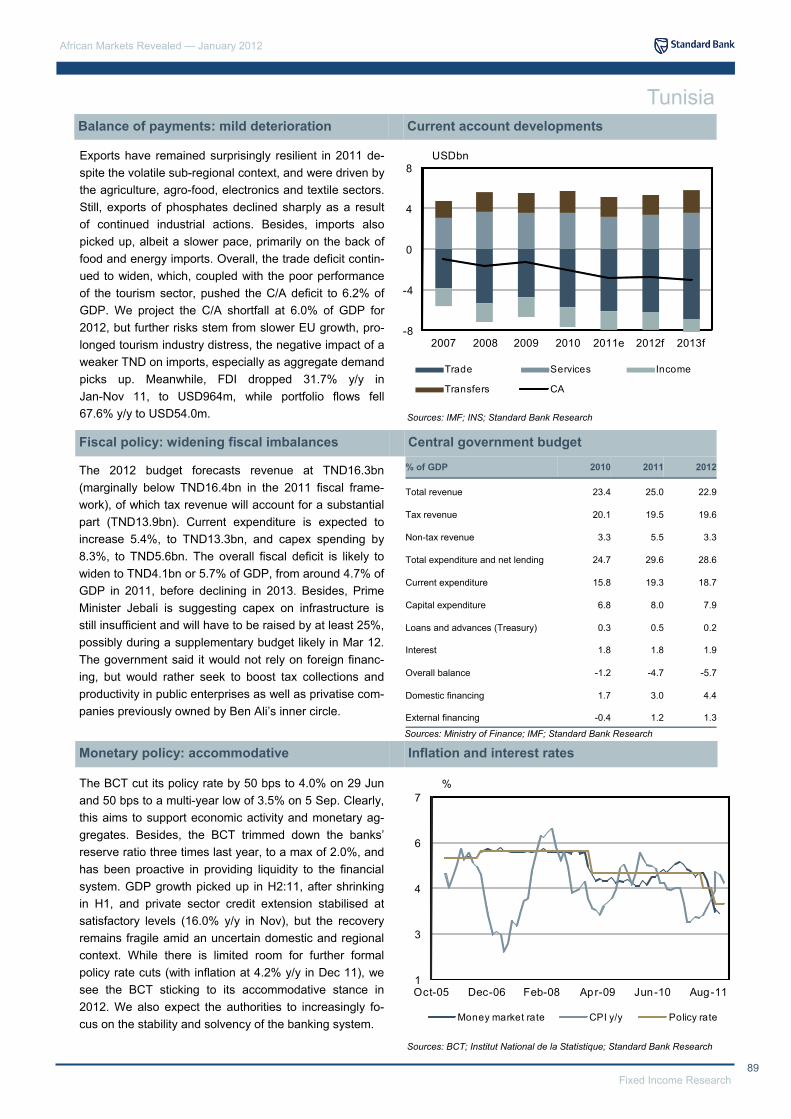

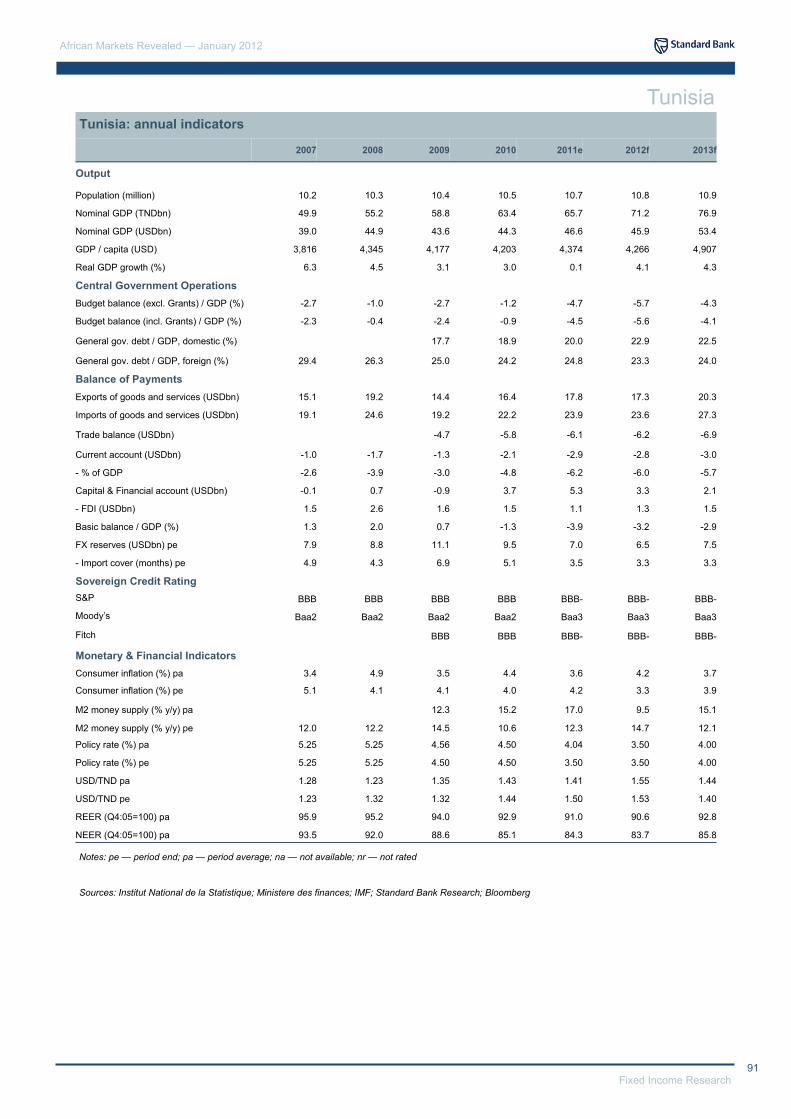

Tunisia Delivering a successful transition 88

Morocco A diversifier in a volatile region 56

African Markets Revealed — January 2012

2 Fixed Income Research

Yvette Babb* +27-11-378-7239 [email protected]

Stephen Bailey-Smith* +44-20-3145-6964 [email protected]

Adriaan du Toit* +27-11-378-7329 [email protected]

Jan Duvenage* +27-11-378-7229 [email protected]

Samir Gadio* +44-20-3145-6774 [email protected]

Thabi Leoka* +27-11-378-8151 [email protected]

Phumelele Mbiyo* +254 (020) 3638988 ext 89 [email protected]

Dmitry Shishkin* +44-20-3145-6963 [email protected]

3 Fixed Income Research

African Markets Revealed — January 2012

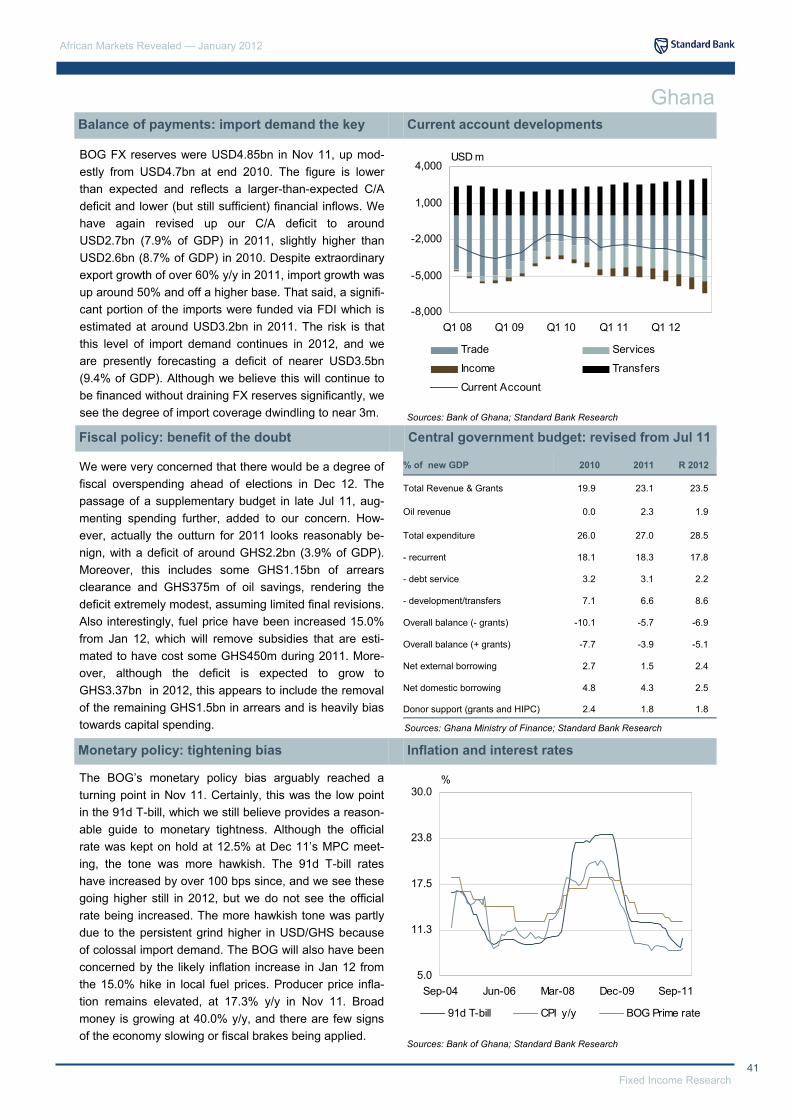

that recession is likely across EZ as a whole with the UK also getting sucked in. While the US may avoid negative growth, it will continue to struggle to keep economic ac-tivity growing, and the Fed is likely to further ease mone-tary policy in an attempt to do so. The last WEO saw advanced economies growing at 1.9% in 2012, but we suspect this will be nearer 1.2%.

China’s slowdown has further to go

With its clear export links to growth in the DM econo-mies, we have been fairly negative on China’s growth outlook since Q2:11. Not only is there a drag from the net export component of GDP, but China’s business/investment cycle also appears to be rolling over. While China is not fiscally constrained to the extent that most DM economies are, we are still looking for China to grow around 7.2% y/y in 2012 compared to the WEO estimate of 9.0%.

Global growth re-balancing

Growth in the EM economies is likely to be nearer 5.6% in 2012, compared to the 6.4% projected in the WEO. Importantly, while EM economic growth will clearly be dragged back by the problems facing the DM econo-mies, the increasing broadening of intra-EM trade and

Global growth: still slowing

Following the 2008 financial crisis, we were generally more constructive than the market on the likely strength of the economic rebound. As such, we generally found our global growth outlook on the bullish side of the mar-ket throughout 2009 and 2010. It was a position that proved appropriate. We switched our stance in Q2:11 and have since found ourselves on the bearish side of consensus. This still appears to be the case. In our Sep 11 AMR, we were looking for the IMF’s last WEO (Sep 11) to revise down its global economic growth outlook. This was indeed the case. The IMF is now looking for global growth of 4.0% in 2012, the same as in 2011, compared to their previous forecast of 4.4% y/y in 2011 and 4.5% y/y in 2012 in the Jun 11 WEO. Once again we suspect both will have to be revised down, with global growth probably nearer 3.0% in 2012.

Eurozone problems hold the key

Central to our more bearish global growth view has been our concern over the ability of EZ policy makers to de-liver a solution to the region’s structural troubles. We are still of the view that the credibility in EZ policy makers gets worse before it gets better. We are now of the view

African markets: rolling with the punches

• The significant downward re-pricing of global growth since May 2011 fostered a jittery risk environment, which added to the very testing circumstances already faced by many African markets. Although we are still cautious on global growth, we are more constructive on asset prices that have already discounted plenty of bad news and are benefiting from ample G4 liquidity. Such an outlook should prove more supportive for commodity prices and portfolio flows into Africa that have been extremely limited in recent years.

• Of the exogenous variables driving Africa’s markets, political risk derived from a series of elections will remain a key differentiator in 2012.

• In recent months we have also seen a marked improvement in the performance of Africa’s currencies as the markets again pressed home the message that real interest rates matter. The sharp increases in interest rates have added significant protection to a number of currencies and made them extremely attractive from a carry trade prospective. We are extremely constructive on UGX, KES and TZS seeing further appreciation. There is also attractive risk reward for being long NGN, AOA, MZN and probably EGP given the extra-ordinary rates of-fered by the NDFs. We are ambivalent on ZMK and ZAR and nervous on GHS.

• In the local bonds, we see huge yield compression in Uganda, Kenya, Zambia and possibly even in Egypt, if our core muddle-through political scenario materialises. We are relatively neutral on Nigeria, nervous on Ghana and we would be paying rates in South Africa at present.

• We are modestly constructive on African equity markets seeing some value in Nigeria, Kenya and arguably Egypt in coming months.

• In Africa’s Eurobonds, we are positive on Côte d’Ivoire 32s and Egypt’s 20s and 40s. We are neutral on Nigeria 21s and Rep Con 29s and negative on Gabon 17s, Senegal 21s, and Ghana 17s.

African Markets Revealed — January 2012

4 Fixed Income Research

financial flows means that the influence is increasingly muted. EM economies are likely to provide the bulk of the contribution to global growth for years to come. EM economies presently produce around a third of global output. The IMF assumes they would produce more than half by 2028. We suspect that they will contribute more than half of global output faster than that. We continue to believe that the 2008 global financial crisis marked a sig-nificant turning point in the organisation of the interna-tional economic system. An extended period of de-leveraging in the DM means slower growth and a sus-tained reversal of financial flows, which will foster a sharp outperformance by EM economies for years to come.

Search for yield

A key feature of EM economic outperformance will be the continued search for yield from DM investors and actually EM investors that had previously been long “safer” DM assets. In particular, the cyclical policy of degrading DM currencies via quantitative easing will foster greater de-mand for scarcer EM assets while the loose monetary policy stance persists. Interesting, while foreign direct investment into EM and frontier markets (FM) has been reasonably solid post 2008 crisis, FM, including Africa, have underperformed wider EM in terms of portfolio flows. We see this as a cyclical opportunity as part of a wider multi-year structural shift towards a search for al-pha returns from fast growing economies coming off low bases.

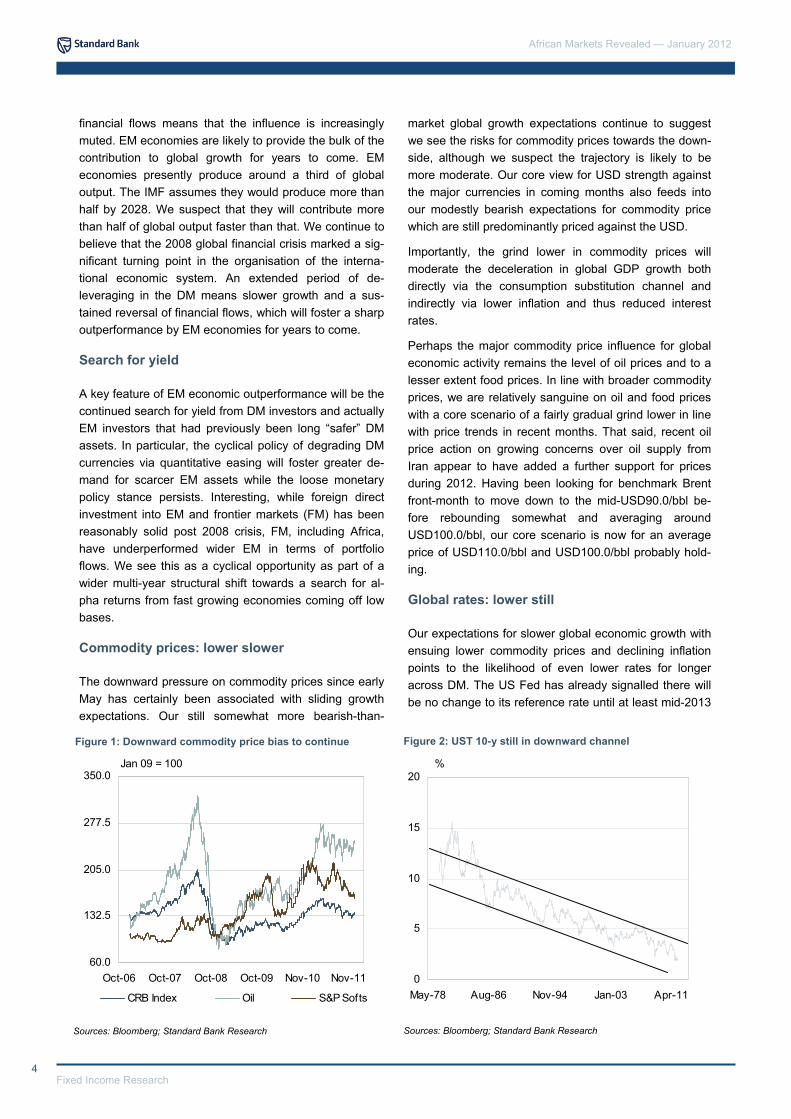

Commodity prices: lower slower

The downward pressure on commodity prices since early May has certainly been associated with sliding growth expectations. Our still somewhat more bearish-than-

market global growth expectations continue to suggest we see the risks for commodity prices towards the down-side, although we suspect the trajectory is likely to be more moderate. Our core view for USD strength against the major currencies in coming months also feeds into our modestly bearish expectations for commodity price which are still predominantly priced against the USD.

Importantly, the grind lower in commodity prices will moderate the deceleration in global GDP growth both directly via the consumption substitution channel and indirectly via lower inflation and thus reduced interest rates.

Perhaps the major commodity price influence for global economic activity remains the level of oil prices and to a lesser extent food prices. In line with broader commodity prices, we are relatively sanguine on oil and food prices with a core scenario of a fairly gradual grind lower in line with price trends in recent months. That said, recent oil price action on growing concerns over oil supply from Iran appear to have added a further support for prices during 2012. Having been looking for benchmark Brent front-month to move down to the mid-USD90.0/bbl be-fore rebounding somewhat and averaging around USD100.0/bbl, our core scenario is now for an average price of USD110.0/bbl and USD100.0/bbl probably hold-ing.

Global rates: lower still

Our expectations for slower global economic growth with ensuing lower commodity prices and declining inflation points to the likelihood of even lower rates for longer across DM. The US Fed has already signalled there will be no change to its reference rate until at least mid-2013

Sources: Bloomberg; Standard Bank Research

Figure 1: Downward commodity price bias to continue Figure 2: UST 10-y still in downward channel

0

5

10

15

20

May-78 Aug-86 Nov-94 Jan-03 Apr-11

%

Sources: Bloomberg; Standard Bank Research

Jan 09 = 100

60.0

132.5

205.0

277.5

350.0

Oct-06 Oct-07 Oct-08 Oct-09 Nov-10 Nov-11

CRB Index Oil S&P Softs

5 Fixed Income Research

African Markets Revealed — January 2012

and in Jan 12 it will start making their 2-year forecast for the reference rate explicit. What this probably means is that the period for which rates are expected to remain extremely low will be pushed out even further.

Meanwhile, the UK announced a programme of further quantitative easing as expected, which will run at least until Feb 12. At the same time the expected reversal of the ECB’s tightening bias has materialised. In fact, the ECB has arguably also started on its own attempt at additional liquidity creation via a programme of providing collateralised 3-y term loans for EZ banks.

The anticipated bull flattening in DM sovereign rates curves (with the exception of those under extreme credit stress) is also materialising and we see this continuing in coming months. Importantly, we see the bid for 10-y UST continuing to push down yields (albeit modestly) in coming months, which will continue to provide solid sup-port for EM sovereign USD Eurobonds.

Although average EM 10-y yields are higher than they were in early Sep 11, prior to a sharp sell-off at the end of that month, they have now taken back most of the losses. We are thus relatively sanguine on the future direction seeing sideways price action similar to that seen over the last two years. The key driver of short-term moves is likely to remain currency developments, which in turn remain subject to significant swings in global risk appetite.

Global currency: further EUR/USD downside

Our core view for EUR/USD downside has materialised well since May 2011 and we see few reasons to reverse our core view, while the fiscal and debt issues facing the EZ countries remain in place. We have shifted our multi-

month EUR/USD target to 1.15.

That said, with all G4 continuing to deliberately under-mine their currency values, the ugly currency competi-tion looks set to role on for some time. As such, we con-tinue to look for EM currencies to outperform DM on an outright basis and certainly on a interest rate adjusted (forward) basis.

That said, there has been limited evidence of EM FX outperformance since our Sep 11 AMR. Not including interest rates, our simple average EM FX basket has lost around 9.4% against the EUR, while it has only gained a modest 1.5% against the EUR. This is hardly a solid argument for EM outperformance over DM. The much-mused problem remains the correlation between negative global risk-appetite and USD strength.

Sources: Bloomberg; Standard Bank Research

Figure 3: Simple average EM 10-y bond yield Figure 4: EUR/USD in solid down channel post May 11

Sources: Bloomberg; Standard Bank Research

Sources: Bloomberg; Standard Bank Research

Figure 5: EM FX performance is mixed

6.00

7.75

9.50

11.25

13.00

Jun-99 May-02 Apr-05 Mar-08 Feb-11

EM 10-y bond yield

1.15

1.25

1.35

1.45

1.55

Apr-10 Sep-10 Feb-11 Jul-11 Dec-11

EUR/USD

Jan 00 = 100

80.00

107.50

135.00

162.50

190.00

Jun-99 Jul-02 Aug-05 Sep-08 Oct-11

USD/EMFX EUR/EMFX

African Markets Revealed — January 2012

6 Fixed Income Research

crisis, because of the thin positioning by international investors. This means that the main source of beta is extremely diluted at present, which is probably a good thing in a muddle-through risk-on, risk-off jittery type of environment.

Global equities: further downside

Our negative expectations for global equities back in early Sep 11 was broadly born out. MSCI DM was flat between early Sep and end Dec 11, taking the decline for 2011 to a moderate 7.6%. Interestingly, S&P500 was up 7.1% over the last 4-m of 2011, taking the index flat for 2011. MSCI EM was down 10.3% in the last 4-m of 2011 taking the decline to 20.4% for the full year. MSCI FM was again the star underperformer losing 22.1% during 2011, although it was only 6.7% down in the final 4-m period.

Interestingly, price action in the first couple of weeks of 2012 has been more encouraging for equity markets gen-erally. MSCI DM is up 1.6%, MSCI EM is up 4.0%, al-though MSCI FM is down 1.2%. We have been arguing for the outperformance of FM equities for some time and still believe they offer significant upside relative to EM and especially DM. However, by nature they are less highly correlated than other equity markets and thus rely more on local idiosyncratic factors. These have not been particularly supportive during 2011 in a number of the larger countries in the index, especially in the Middle-East and peripheral Europe.

We are generally looking for another year of muddle through for global equities with a volatile but ultimately directionless year. We would expect EM to outperform DM after its underperformance in 2011, but still not to offer much in the way of price upside, despite the best

Global risk appetite: reasonable

Ironically, the failure of EM FX to outperform DM since early Sep 11 is not just a product of global risk appetite, but actually reflected a decided anti-EM risk bias during the period. Actually after the Sep 11’s spike, risk appe-tite, as measured by the VIX which is a traded volatility index based on the S&P500 and arguably the best ba-rometer of global risk sentiment, improved significantly. In fact, there was an associated shift lower in EM FX volatility suggesting that there was not so much uncer-tainty but a clear lack of demand for EM FX.

Ironically, the high level of risk aversion throughout 2011, but particularly in Sep 11, actually makes us moderately more constructive on sentiment going forward, as we feel that there is a considerable amount of bad news built into assets prices. Indeed, for another marked downturn in assets prices, we would need a major negative event to overturn fairly thin long positioning. These are by nature difficult to predict and thus impossible to position for. Thus our core risk scenario is for a muddle-through in the EZ crisis with the authorities continuing to provide enough liquidity to prevent massive dislocation in the banking sector and to smooth the inevitable de-leveraging of the banking sector across the EZ. Such a course of action will, however, arguably make the length of the corrective G4 de-leveraging period longer.

The combination of moderate muddle-through risk senti-ment and extremely low G4 rates should provide a rea-sonably constructive environment for EM and FM assets. Such a muddle through prognosis is also likely to make investors more discerning regarding the peculiarities of particular cyclical or structural stories, which are able to offer some genuine alpha. Importantly, FM assets have clearly been underperforming post the 2008 financial

Sources: Bloomberg; Standard Bank Research

Figure 6: risk appetite recovering

0.00

22.50

45.00

67.50

90.00

Sep-05 Apr-07 Oct-08 May-10 Nov-11

EM FX Volatility VIX

Figure 7: DM equity outperformance in 2011

Jan 09 = 100

60.0

107.5

155.0

202.5

250.0

Oct-06 Jan-08 May-09 Aug-10 Dec-11

MSCI EM MSCI DM MSCI FM

Sources: Bloomberg; Standard Bank Research

7 Fixed Income Research

African Markets Revealed — January 2012

efforts of the G4 policy makers to keep liquidity ample and growth rolling forward.

Africa’s election schedule remains heavy

Africa’s investment climate was heavily influenced by the continent’s shifting political sands in 2011. There was the usually risk going into elections generated by policy uncertainty. Yet from early 2011, political risk was addi-tional augmented by the clamouring for democratic change across the Arab world. The risk of a popular uprising to overthrow less democratic leaders added to the risk around elections. Political risk perceptions across the continent were also increased by the slide into civil war in Côte d’Ivoire due to the incumbent’s un-willingness to relinquish power.

There is no shortage of election risks across Africa in 2012, with elections (or referendums) taking place in possibly 20 out of the 54 countries across the continent. The most closely followed by the international investor community will be the outcome of the ongoing electoral process in Egypt, presidential election in Senegal on 26 Feb 12, parliamentary and presidential elections in

Kenya (although they may be delayed until 2013) and parliamentary and presidential elections in Ghana in Dec 12.

African growth: slower

Since May 2011 we have been revising down our growth estimates for Africa predominantly in line with an expected slowdown in global growth activity. Our projec-tion for weighted sub-Saharan African growth was 5.0% in 2011 (which is still below the IMF’s expectation of 5.2% revised down from 5.6%) and a similar trajectory in 2012, which is well below the IMF’s expectation of 5.8%.

One of the key issues of disparity between the IMF and our view is with regards to South Africa, which remains the largest economy on the continent. The IMF has South Africa growing at 3.6% in 2012 (up from 3.4% in 2011), but we expect both of these numbers to be lower than expected, pulling down the SSA aggregate. An-other potential complicating factor will be the likely sharp upward revision to GDP that Nigeria is likely to get from the result of new survey data. This will increase the weights of the faster growing sectors of the economy in a similar way to the process in Ghana in late 2010.

Interestingly, excluding SA and Nigeria, the IMF sees SSA growth of 6.8% y/y in 2012 from 5.4% y/y in 2011. Once again we are more cautious, projecting a figure of 6.0% for 2012 as more likely, as we see SA as the key drain rather than Nigeria.

It is also worth noting, that we are broadly in accord with the IMF in seeing not one economy actually slipping into recession in SSA during 2012.

The transmission mechanism between global growth and African growth remains complex. The channel of trade in goods and services (especially tourism) will be most marked in South and North Africa, where the link-ages are most developed.

Good and service linkages actually remain rather weak in most of the countries in the middle of Africa, where we maintain the main linkage to global growth will be commodity prices. The transmission from commodity prices will also be complex across countries. The key division remains between oil importers and oil exporters, with the importers looking like they will benefit less than we had previously thought in line with our modest up-ward revision in international oil prices for 2012.

Remittances will be another potential dampener as growth slows across DM. However, we continue to see growing evidence of the market pro-cyclicality tied to expectations of currency movements. As such, we sus-pect higher rates, more stable currencies and improving

Figure 8: Africa’s election schedule 2012

Country Election type DateEgypt Parliamentary (Stage 3) 03-Jan-12Egypt Legislative (1st round) 03-Jan-12Senegal Presidential 26-Feb-12Gambia, The Legislative 24-Mar-12Egypt Presidential Mar-12Madagascar Presidential (Tentative) Mar-12Madagascar

y(Tentative) Mar-12

Mali Presidential (1st round) 29-Apr-12Mali Presidential (2nd round) 13-May-12Burkina Faso Parliamentary May-12Mali

y (round) 01-Jul-12

Maliy (

round) 22-Jul-12Cameroon Legislative Jul-12Kenya Presidential (1st round) 14-Aug-12Kenya Parliamentary 14-Aug-12Sierra Leone Legislative Aug-12Angola Parliamentary Sep-12Sierra Leone Presidential 17-Nov-12Ghana Presidential Dec 12Ghana Legislative Dec-12Senegal Parliamentary 2012Lesotho Parliamentary 2012Togo Parliamentary 2012Zimbabwe

y(Tentative) 2012

Equatorial Guinea Parliamentary 2012Congo (Brazzaville) Legislative 2012Algeria Legislative 2012Guinea Legislative 2012Sudan Referendum 2012Zimbabwe Referendum (Tentative) 2012Zambia Referendum 2012

Source: Standard Bank Research

African Markets Revealed — January 2012

8 Fixed Income Research

relative investment opportunities will certainly neutralise some of the negative impact from slowing DM growth.

The key linkage between Africa’s growth and the global environment is via investment confidence. It is quite pos-sible that we see a slowing of investment decisions as confidence in the global financial system continues to be questioned and assumptions around commodity prices have to be re-cut. That said, as already discussed we are reasonably sanguine on global risk sentiment in 2012, having had a period of extreme risk aversion during 2011.

There are, of course, a number of endogenous cyclical drivers of African growth that should be taken into consid-eration. We have argued for some time that the expan-sionary fiscal and monetary policies post the 2008 crisis were inappropriate for many of Africa’s economies which would subsequently overheat fostering depreciation/inflation spirals. The resulting sharp increases in interest rates across a number of countries will almost certainly undermine credit extension to both the private and public sides of the economy, slowing growth.

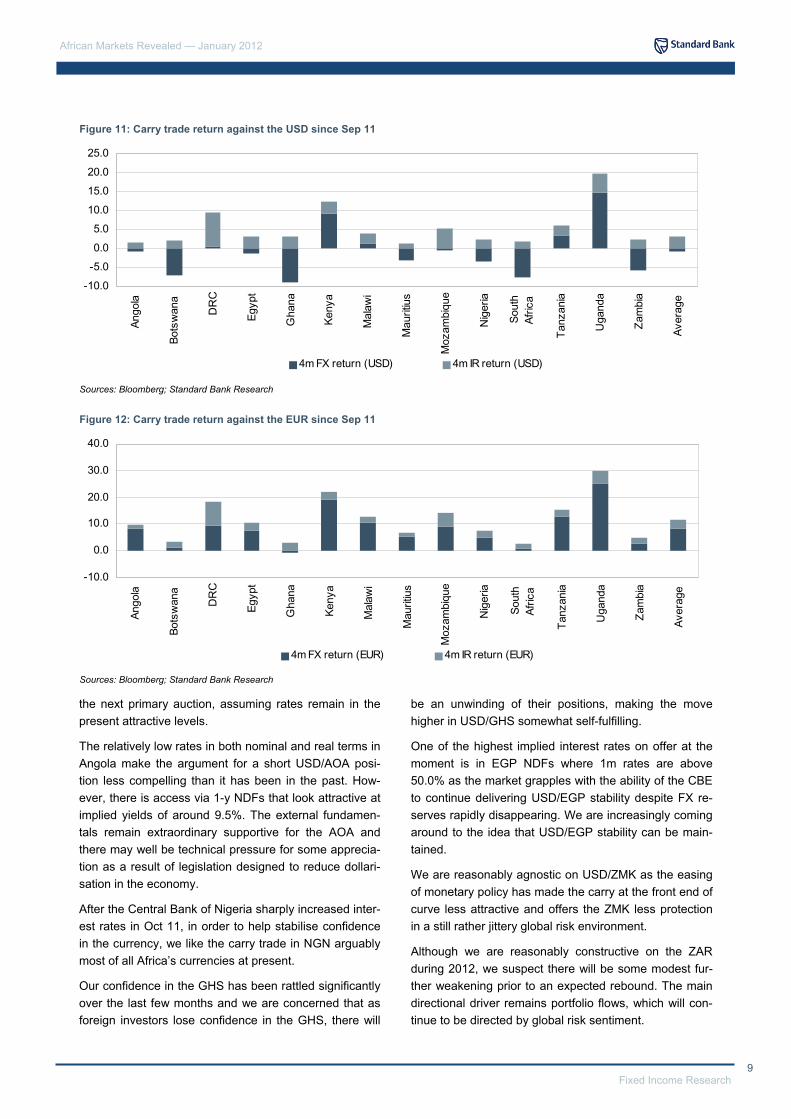

African FX: time for outperformance

Our AF10 index (which includes 10 of the most easily traded African currencies) has performed much better over the months since Sep 11. The AF10 depreciated 7.3% against the USD and 5.5% against the EUR during 2011. However, since early Oct 11 the situation has changed. The AF10 has appreciated 2.0% against the USD and around 11.4% against the EUR.

Importantly, we believe a great deal of the recent outper-formance reflects the product of the reversal of previous

weakness, in line with drastic changes in monetary pol-icy. Once the sharply higher interest rates are taken into account, the situation looks even more favourable with the AF10 returning around 5.0% against the USD over the last 4-m which was a significant outperformance rela-tive to EM benchmark bond indices (down around 5.0% over the period).

Interestingly, there has been a huge discrepancy be-tween the performances of the various African currencies suggesting they have the potential to offer genuine idio-syncratic low beta risk at present.

The outlook for Africa’s currencies still looks extremely mixed, but with some offering exceptional carry trade opportunities.

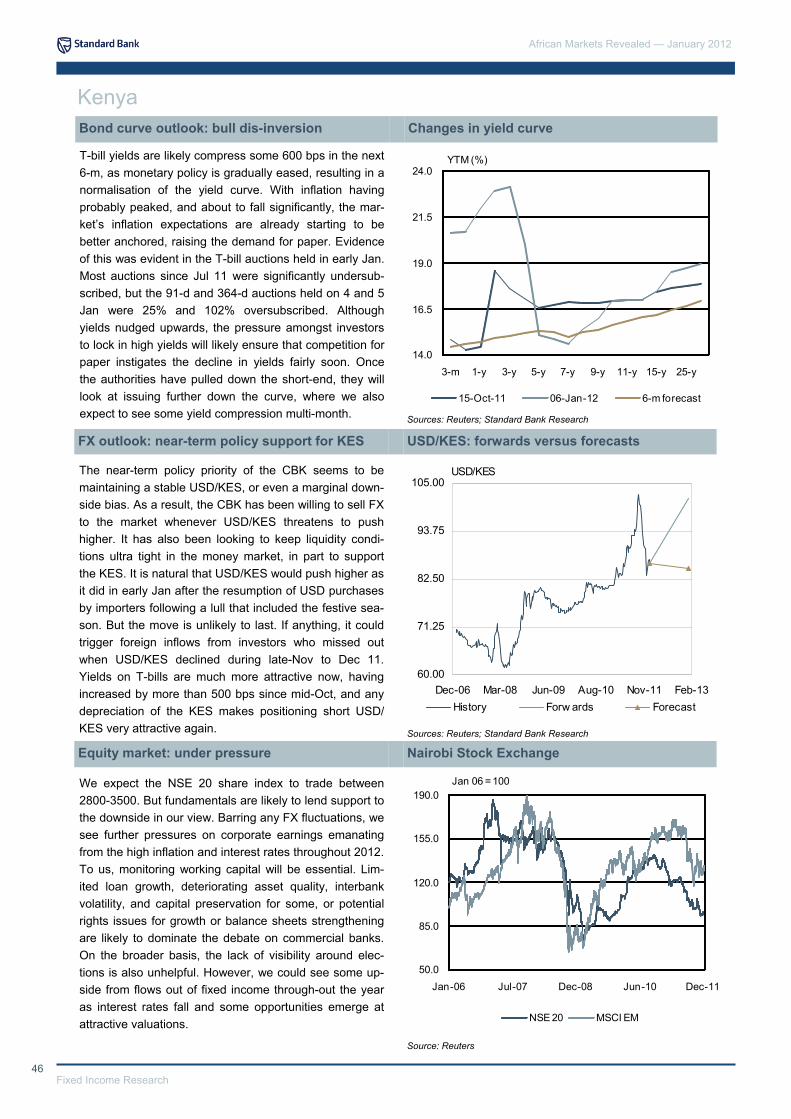

Our favourite carry trade back in Sep 11 was UGX, which has performed extremely well and we see this continuing over the next few months at least. We certainly see it as unlikely that the USD/UGX upside will be greater than the 20.0% plus interest rates on offer. In fact, we are targeting a move down to 2150.

We feel similarly about the potential for the carry trade in KES, where T-bill rates are also 20.0% plus and we sus-pect the authorities will go out of their way to ensure KES stability or strength in coming months at least.

We suspect that USD/TZS would prove a similarly posi-tive investment, but it is extremely difficult for foreign investors to gain access to the carry.

We feel that the appreciation of MZN against the USD has run its course and that the MZN has now joined the group of heavily managed currencies which attempt to remain stable against the USD. Access remains difficult, but we would look to buy the local bonds when offered at

Figure 9: Sub-Sahara Africa GDP by demand

-5.0

0.0

5.0

10.0

15.0

2005 2006 2007 2008 2009 2010 2011f 2012f

%

Investment Imports

Exports Private consumption

Gov consumption Real GDP

Sources: IMF; WEO; Standard Bank Research

Figure 10: AF10(1) index has lost against EUR and USD

Jan 09 = 100

85.0

93.8

102.5

111.3

120.0

Nov-08 Aug-09 May-10 Mar-11 Dec-11

AF10 USD AF10 EUR

Sources: Bloomberg; Standard Bank Research

1. Note AF10 is Botswana, Egypt, Ghana, Kenya, Mauritius, Nigeria, South Africa, Tanzania, Uganda and Zambia.

9 Fixed Income Research

African Markets Revealed — January 2012

the next primary auction, assuming rates remain in the present attractive levels.

The relatively low rates in both nominal and real terms in Angola make the argument for a short USD/AOA posi-tion less compelling than it has been in the past. How-ever, there is access via 1-y NDFs that look attractive at implied yields of around 9.5%. The external fundamen-tals remain extraordinary supportive for the AOA and there may well be technical pressure for some apprecia-tion as a result of legislation designed to reduce dollari-sation in the economy.

After the Central Bank of Nigeria sharply increased inter-est rates in Oct 11, in order to help stabilise confidence in the currency, we like the carry trade in NGN arguably most of all Africa’s currencies at present.

Our confidence in the GHS has been rattled significantly over the last few months and we are concerned that as foreign investors lose confidence in the GHS, there will

be an unwinding of their positions, making the move higher in USD/GHS somewhat self-fulfilling.

One of the highest implied interest rates on offer at the moment is in EGP NDFs where 1m rates are above 50.0% as the market grapples with the ability of the CBE to continue delivering USD/EGP stability despite FX re-serves rapidly disappearing. We are increasingly coming around to the idea that USD/EGP stability can be main-tained.

We are reasonably agnostic on USD/ZMK as the easing of monetary policy has made the carry at the front end of curve less attractive and offers the ZMK less protection in a still rather jittery global risk environment.

Although we are reasonably constructive on the ZAR during 2012, we suspect there will be some modest fur-ther weakening prior to an expected rebound. The main directional driver remains portfolio flows, which will con-tinue to be directed by global risk sentiment.

Figure 11: Carry trade return against the USD since Sep 11

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

Ango

la

Bots

wan

a

DR

C

Egyp

t

Gha

na

Keny

a

Mal

awi

Mau

ritiu

s

Moz

ambi

que

Nig

eria

Sout

hAf

rica

Tanz

ania

Uga

nda

Zam

bia

Aver

age

4m FX return (USD) 4m IR return (USD)

Sources: Bloomberg; Standard Bank Research

Figure 12: Carry trade return against the EUR since Sep 11

-10.0

0.0

10.0

20.0

30.0

40.0

Ango

la

Bots

wan

a

DR

C

Egyp

t

Gha

na

Keny

a

Mal

awi

Mau

ritiu

s

Moz

ambi

que

Nig

eria

Sout

hAf

rica

Tanz

ania

Uga

nda

Zam

bia

Aver

age

4m FX return (EUR) 4m IR return (EUR)

Sources: Bloomberg; Standard Bank Research

African Markets Revealed — January 2012

10 Fixed Income Research

Sources: Bloomberg; Standard Bank Research

Sources: Bloomberg; Standard Bank Research

Figure 13: SB FX Money Market Index vs. EM Global bond indices

0.8

0.9

1

1.1

1.2

1.3

1.4

1.5

1.6

1.7

1.8

Nov-06 Jun-07 Jan-08 Jul-08 Feb-09 Aug-09 Mar-10 Sep-10 Apr-11 Nov-11

SB FX Index Markit iBoxx Global Bond EM JPMorgan GBI-EM Global

Figure 14: AF10 yield curve: simple yield average

8%

9%

10%

11%

12%

13%

14%

15%

16%

0 2 4 6 8 10 12 14 16 18 20

Modified duration

Sep-11 Jan-12

11 Fixed Income Research

African Markets Revealed — January 2012

Africa’s simple average local yield curve, as measured by our AF10 currencies, has bear flattened over the last four months. We suspect the curve will deliver significant yield compression during 2012, with some moderate compression occurring in the next few months as the start of the easing cycle in a number of countries gets underway.

As with our conviction currency trades, Uganda and Kenya once again come top of the list, with the potential for some 1000bps of compression at the short-end of the bond curve as they normalise in line with inflation falling dramatically.

The heavily inverted nature of the Nigerian curve means we are looking for some bear flattening before we look at taking on duration again. Although this may be within weeks, once the market has dealt with the partial re-moval of fuel subsidies and the CBN’s response to the change.

We are a little ambivalent on duration in Zambia, al-though the heavy tax and illiquidity make our conviction rather marginal.

We are still watching and waiting to get involved in dura-tion in Egypt’s local curve despite the 5-y bond yields reaching 16.7% on 17 Jan 12. While we are becoming more constructive as we see the possibility of an end to present political uncertainty, we need to see a little more confidence return to the currency first.

In line with our concern over the GHS, we have become a lot less constructive on duration in Ghana and expect to see yields pick up along what is already a fairly steep curve.

We are not presently constructive on duration in South

Africa and would be paying rates as we suspect there is more risk to inflation expectations increasing in coming months as we get a spike in inflation fuelled by ZAR weakness and regional food prices.

African equities: enough already

Our negative outlook for equities across Africa in Sep 11 proved reasonably appropriate with MSCI Africa index down 1.8%. That said, so far 2012 has opened up on a more constructive tone for a number of markets. The JSE is at all time highs at the time of writing.

We suspect that there is a degree of catch up that takes place in coming months between EM equities and the performance of the S&P500, which actually performed well, increasing 17.9% since its lows in early Oct 11.

The mildly bullish equity tone should assist Africa’s mar-kets but will need significant improvement in some of the endogenous drivers to really rebound aggressively.

We are still in wait-and-see mode in Egypt, but are tempted to start mildly accumulating on a modestly more constructive political view, as we feel a huge amount of negative political economy news is already in the prices.

We are also becoming mildly constructive on Nigeria mainly because the valuation have started to look very cheap with the main index on a PE value of around 7.0. We are reasonably happy on the stability of the NGN which has been a major constraint to foreign participa-tion in past years. High interest rates will, however, con-tinue to mitigate equity market growth and we are not convinced this is coming down any time soon.

If one is looking for underperforming equity markets, Kenya has to qualify, falling around 30.0% during 2011.

Figure 15: Africa aggregate comparative equity performance

Jan 09 = 100

20

80

140

200

260

Jan-02 Jun-04 Dec-06 May-09 Nov-11

MSCI EM MSCI Africa MSCI FM MSCI DM

Sources: Bloomberg; Standard Bank Research

Figure 16: Africa’s individual stock market performances

Jan 09 = 100

-10.0

60.0

130.0

200.0

270.0

Oct-07 Nov-08 Nov-09 Dec-10 Dec-11Egypt Nigeria KenyaMauritius SA MSCI Africa

Sources: Bloomberg; Standard Bank Research

African Markets Revealed — January 2012

12 Fixed Income Research

We are tempted to suggest that there will be a rebound on a multi-month basis as a great deal of the bad news is in the price. The elections, which the market had thought would be in Aug 12 now look likely in Mar 13 and will push political risk down the road a little. Perhaps most importantly the stability and probably additional strength of the KES will make foreign investors happy to own the local equities. P/E ratio have increased in recent months to around 11.0, as earnings have been worse than anticipated. Our expectation that inflation and thus interest rates will come off aggressively during 2012 also add to our growing conviction on Kenyan equities.

African Eurobonds: differentiated

According to our African sovereign Eurobond indices, the underperformance of our Africa indices with and without South Africa relative to the EMBI Global index continued in the 4-m since early Sep 11 and the last AMR. In terms of total return, EMBI Global was up 1.0% taking the return for 2011 to 8.5%. Our Africa (SBAFSO Bloomberg) which in-cludes SA returned 1.7% since Sep 11 but was up 5.6% during 2011. Our (SBAFSOZ) which excludes SA performed similarly falling 1.5% since Sep 11 and returning 5.3% during 2011.

We remain broadly constructive on the sovereign Eurobond asset class during 2012. In particular, we see the risks to a sharp rebound in US treasury yields as modest, with the risks probably skewed towards lower UST yields for longer. Such an outlook will continue to give the asset class protec-tion going forward.

In terms of the African index we are actually reasonably con-structive. In particular, we are looking for a marked rebound in the performance of Egypt 40s and 20s, which have been the star underperformers in recent months. Importantly, we are becoming more constructive on a muddle-through politi-cal outcome, which provides enough stability for investment decisions to start being made again.

Our other favourite overweight position remains Côte d’Ivoire 32s and our strategy of accumulation on sell-offs to the low 50s appears appropriate at present. Indeed, we suspect that after the investor meeting with the Ivorian government on 23 Jan 12, at which we expect more clarity on the process of the government becoming current on the CIV 32s, the price will shift into a new range between 55 and 60 until the Jun 12 coupon payment is actually made. Our longer-term expecta-tion is for Côte d’Ivoire to trade near to Ghana which pres-ently would be a price of around 75.0.

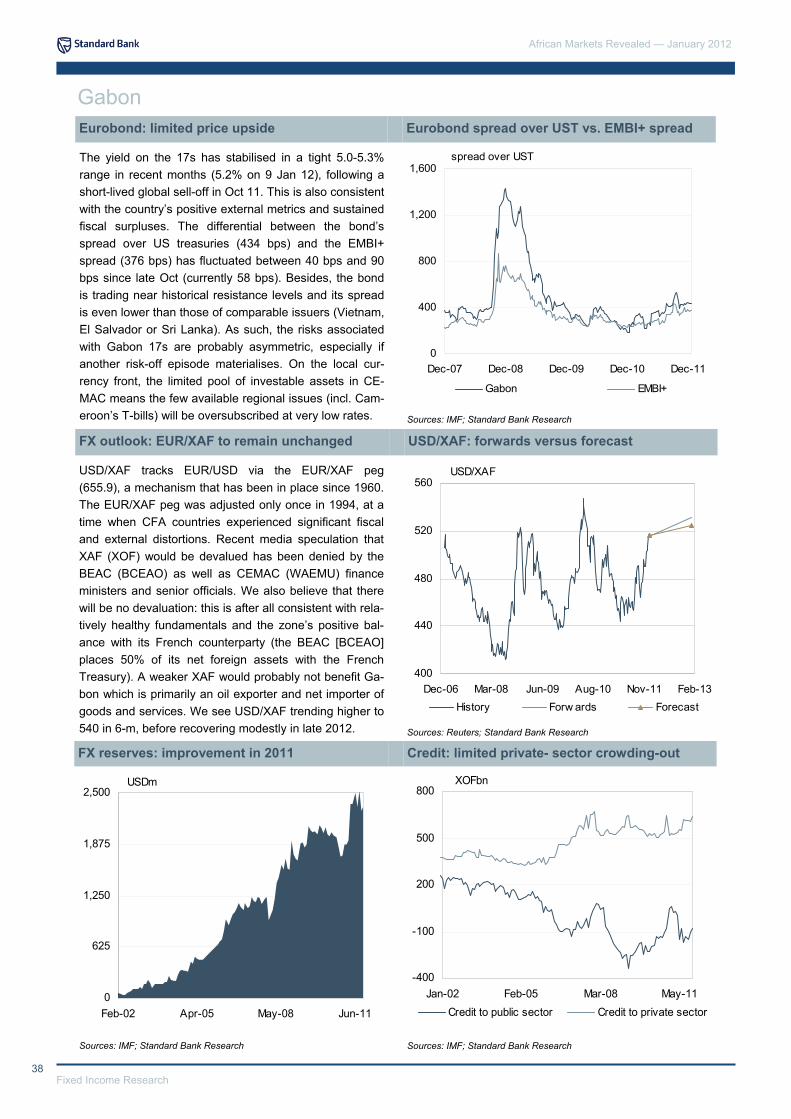

We would be underweight Gabon 17s, which continue to trade a little rich despite us being reasonably happy with credit matrix on the back of some apparent diversification effort.

We are also nervous of being long Senegal 21s going into Feb 12 elections, which will probably be noisy with a fairly uncertain outcome.

We are also nervous of holding Ghana 17s going into elections in Dec 12, which will continue to place funding pressure on the government at a time when the currency is demonstrating signs that the economy is overheating.

We are relatively neutral to negative on Nigeria 21s as they are trading reasonably tight and require a coherent structural adjustment strategy to start being delivered in order to tighten the bond spreads much further. Although we are less bearish on oil prices for 2012, Nigeria clearly still remains extremely vulnerable to them moving sharply lower.

We remain constructive on Rep Con 29s given the ex-tremely strong fundamentals. Yet the bonds have rallied hard already and we would probably look to dips to build larger positions.

13 Fixed Income Research

African Markets Revealed — January 2012

Figure 17: African Sovereign and Corporate bonds (spread over US Treasuries)

Congo '29

IvyCoast '32

Nigeria '21

Senegal '21

Seychelles '26

BTUN '27Gabon ' 17

Ghana '17

Grtbnl '16

Esafrb '16

Afrln '16

Afrexi '16

Afrexi '14

Namibia '21

0

300

600

900

1200

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14Modified duration

Bps

Egypt S. Africa African Corporares

Sources: Bloomberg; Standard Bank Research

Figure 18: African and broader EM bonds (spread over US Treasuries versus credit rating)

S. Africa '20

Namibia '21

Egypt '20

Gabon '17

Ghana '17

Nigeria '21

Senegal '21

Tunisia '27

Seychelles '26

Afrln '16

Afrexi '16

Esafrb '16

Grtbnl '16

0

300

600

900

1200

AA- A+ A A- BBB+ BBB BBB- BB+ BB BB- B+ B B-

S&P credit rating

Bps

Sources: Bloomberg; Standard Bank Research

African Markets Revealed — January 2012

14 Fixed Income Research

Figure 19: 5-year performance of African sovereign USD bonds vs. JPM EMBI Global index

0.70

0.80

0.90

1.00

1.10

1.20

1.30

1.40

1.50

1.60

Jan-07 Jul-07 Feb-08 Aug-08 Mar-09 Oct-09 Apr-10 Nov-10 May-11 Dec-11

Bps

SB Africa Sovereign SB Africa Sovereign (ex ZA) EMBI Global

Sources: Bloomberg; Standard Bank Research

Figure 20: 1-year performance of African sovereign USD bonds vs. JPM EMBI Global index

0.94

0.96

0.98

1.00

1.02

1.04

1.06

1.08

1.10

1.12

1.14

1.16

Jan-11 Feb-11 Mar-11 Apr-11 May-11 Jun-11 Jul-11 Aug-11 Sep-11 Oct-11 Nov-11 Dec-11 Jan-12

Bps

SB Africa Sovereign SB Africa Sovereign (ex ZA) EMBI Global

Sources: Bloomberg; Standard Bank Research

15 Fixed Income Research

African Markets Revealed — January 2012

Figure 21: 5-year history of spread between African sovereign USD bonds and US Treasuries

0

200

400

600

800

1000

1200

1400

Jan-07 Aug-07 Feb-08 Sep-08 Mar-09 Oct-09 Apr-10 Nov-10 Jun-11 Dec-11

Bps

SB Africa Sovereign SB Africa Sovereign (ex ZA) EMBI Global

Sources: Bloomberg; Standard Bank Research

Figure 22: 1-year history of spread between African sovereign USD bonds and US Treasuries

200

335

470

605

740

Jan-11 Feb-11 Mar-11 Apr-11 May-11 Jun-11 Jul-11 Aug-11 Sep-11 Oct-11 Nov-11 Dec-11 Jan-12

Bps

SB Africa Sovereign SB Africa Sovereign (ex ZA) EMBI Global

Sources: Bloomberg; Standard Bank Research

African Markets Revealed — January 2012

16 Fixed Income Research

Angola: managing expansion

Notes: pe — period end; pa — period average; na — not available Sources: Banco Nacional de Angola; Bloomberg; Angola Ministry of Finance; Standard Bank Research

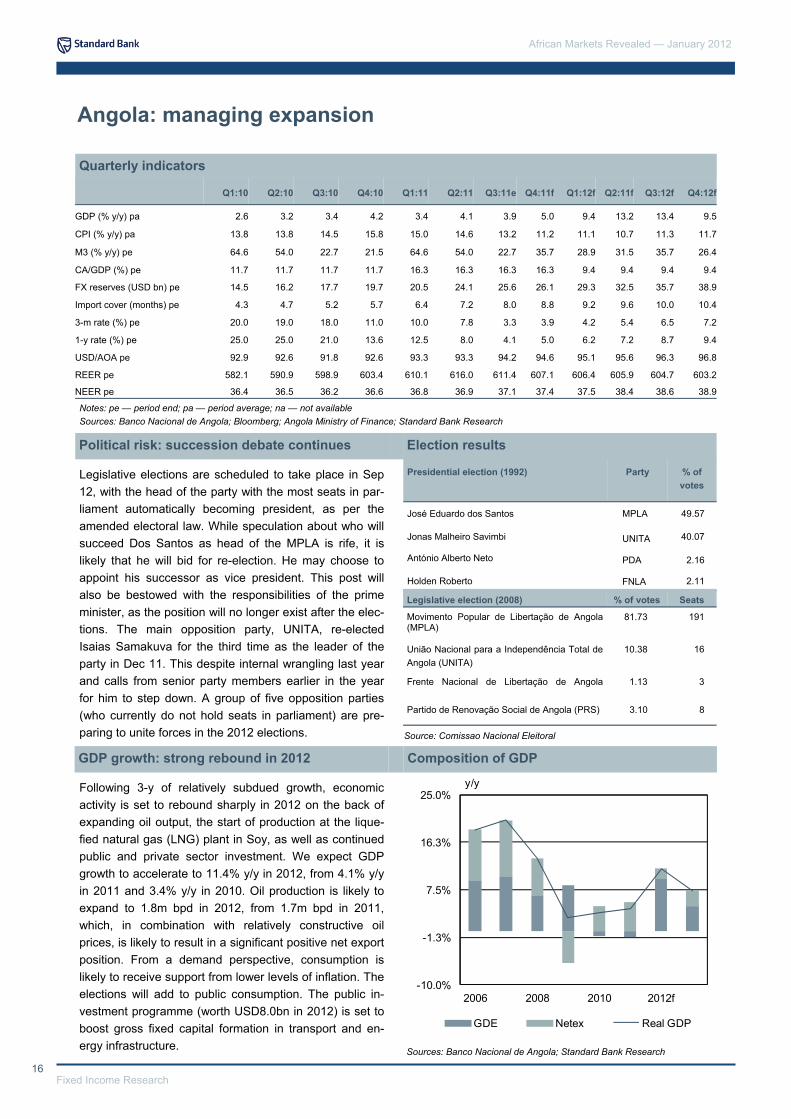

Legislative elections are scheduled to take place in Sep 12, with the head of the party with the most seats in par-liament automatically becoming president, as per the amended electoral law. While speculation about who will succeed Dos Santos as head of the MPLA is rife, it is likely that he will bid for re-election. He may choose to appoint his successor as vice president. This post will also be bestowed with the responsibilities of the prime minister, as the position will no longer exist after the elec-tions. The main opposition party, UNITA, re-elected Isaias Samakuva for the third time as the leader of the party in Dec 11. This despite internal wrangling last year and calls from senior party members earlier in the year for him to step down. A group of five opposition parties (who currently do not hold seats in parliament) are pre-paring to unite forces in the 2012 elections.

Following 3-y of relatively subdued growth, economic activity is set to rebound sharply in 2012 on the back of expanding oil output, the start of production at the lique-fied natural gas (LNG) plant in Soy, as well as continued public and private sector investment. We expect GDP growth to accelerate to 11.4% y/y in 2012, from 4.1% y/y in 2011 and 3.4% y/y in 2010. Oil production is likely to expand to 1.8m bpd in 2012, from 1.7m bpd in 2011, which, in combination with relatively constructive oil prices, is likely to result in a significant positive net export position. From a demand perspective, consumption is likely to receive support from lower levels of inflation. The elections will add to public consumption. The public in-vestment programme (worth USD8.0bn in 2012) is set to boost gross fixed capital formation in transport and en-ergy infrastructure.

Quarterly indicators

Political risk: succession debate continues Election results

GDP growth: strong rebound in 2012 Composition of GDP

Sources: Banco Nacional de Angola; Standard Bank Research

Presidential election (1992) Party % of votes

José Eduardo dos Santos MPLA 49.57

Jonas Malheiro Savimbi UNITA 40.07

António Alberto Neto PDA 2.16

Holden Roberto FNLA 2.11

Legislative election (2008) % of votes Seats

Movimento Popular de Libertação de Angola (MPLA)

81.73 191

União Nacional para a Independência Total de Angola (UNITA)

10.38 16

Frente Nacional de Libertação de Angola 1.13 3

Partido de Renovação Social de Angola (PRS) 3.10 8

Source: Comissao Nacional Eleitoral

Q1:10 Q2:10 Q3:10 Q4:10 Q1:11 Q2:11 Q3:11e Q4:11f Q1:12f Q2:11f Q3:12f Q4:12f

GDP (% y/y) pa 2.6 3.2 3.4 4.2 3.4 4.1 3.9 5.0 9.4 13.2 13.4 9.5

CPI (% y/y) pa 13.8 13.8 14.5 15.8 15.0 14.6 13.2 11.2 11.1 10.7 11.3 11.7

M3 (% y/y) pe 64.6 54.0 22.7 21.5 64.6 54.0 22.7 35.7 28.9 31.5 35.7 26.4

CA/GDP (%) pe 11.7 11.7 11.7 11.7 16.3 16.3 16.3 16.3 9.4 9.4 9.4 9.4

FX reserves (USD bn) pe 14.5 16.2 17.7 19.7 20.5 24.1 25.6 26.1 29.3 32.5 35.7 38.9

Import cover (months) pe 4.3 4.7 5.2 5.7 6.4 7.2 8.0 8.8 9.2 9.6 10.0 10.4

3-m rate (%) pe 20.0 19.0 18.0 11.0 10.0 7.8 3.3 3.9 4.2 5.4 6.5 7.2

1-y rate (%) pe 25.0 25.0 21.0 13.6 12.5 8.0 4.1 5.0 6.2 7.2 8.7 9.4

USD/AOA pe 92.9 92.6 91.8 92.6 93.3 93.3 94.2 94.6 95.1 95.6 96.3 96.8

REER pe 582.1 590.9 598.9 603.4 610.1 616.0 611.4 607.1 606.4 605.9 604.7 603.2

NEER pe 36.4 36.5 36.2 36.6 36.8 36.9 37.1 37.4 37.5 38.4 38.6 38.9

-10.0%

-1.3%

7.5%

16.3%

25.0%

2006 2008 2010 2012f

y/y

GDE Netex Real GDP

17 Fixed Income Research

African Markets Revealed — January 2012

As Africa’s second-largest oil producer, Angola continues to enjoy a large trade surplus, which, combined with sub-stantial financial inflows and fiscal prudence, is likely to contribute to further FX reserve accumulation in 2012. Oil production was constrained by various technical issues in 2011. Our assumptions for oil production in 2012 remain fairly conservative, at 1.8m bpd (in line with budget as-sumptions); however, there is considerable upside risk to these projections as new projects come online and fields undergoing maintenance come back on line. Contrary to 2011, we expect foreign direct and portfolio investments received by Angola to exceed outflows, allowing the C/A surplus to be complemented by a positive balance on the financial account. As such, we expect considerable re-serve accumulation as a result, reaching USD38.9bn by Dec 12, from USD25.5bn in Nov 11.

Fiscal prudence is set to continue in 2012, with the budget expected to reach a sizeable surplus of 9.5% of GDP. The government, which has already repaid USD5.7bn in arrears, aims to conclude the arrears clear-ance process by Jun 12, with a final USD1.5bn to settle the rescheduled arrears in full. Comprehensive reform of the tax system starts this year. Fiscal management has benefited from the establishment of a debt management unit within the Ministry of Finance, which, through the formulation of a MT debt management strategy, will more effectively ensure sustainable levels of public debt. Under this strategy, the government aims to reduce its debt to 23% of GDP within 5-y, from around 33% of GDP in Dec 11. The government is also considering some fiscal sav-ing rules (and potentially a stabilization fund) to assist in smoothing expenditure. Sources: Angola Ministry of Finance; Standard Bank Research

The central bank aims to reduce inflation further, to 10% y/y by Dec 12, from 11.3% y/y in Nov 11 (which marked 14-m of disinflation). Under the new monetary policy framework, the BNA announces its interest rate decision on a monthly basis. The exchange rate will, however, remain the main anchor for monetary policy. We expect the central bank to continue to maintain a relatively stable USD/AOA exchange rate in order to limit the impact of the cost of imported goods on inflation. The BNA’s ability to stabilise the exchange rate is likely to be bolstered by the favourable BOP developments we antici-pate in 2012. We believe that demand side pressures may limit further downside for inflation in 2012, not least as a result of a rise in public spending in the run-up to the elections. We expect inflation to reach 10.7% y/y by the end of Q1:12, before increasing as we move closer to the elections.

Balance of payments: FX reserves to swell BOP developments

Sources: Banco Nacional de Angola; Standard Bank Research

Monetary policy: disinflation to slow Inflation and interest rates

Sources: Banco Nacional de Angola; Standard Bank Research

Angola

Fiscal policy: avoiding boom-bust cycles Central government budget

% of GDP 2010 2011e

Total revenue (+ grants) 43.5 48.3

- oil 33.0 38.3

Total expenditure 36.7 39.0

- current 27.0 28.2

- interest 1.2 1.8

- transfers 6.7 5.5

- development 9.7 10.8

Overall balance (- arrears) 6.8 9.3

2012f

47.6

36.6

38.3

27.4

1.4

5.0

11.0

9.3

-50

-25

0

25

50

75

2005 2007 2009 2011f 2013f

USD bn

Trade balance Services (Net)Income account TransfersCurrent account

10

14

18

8

16

24

32

Jan-07 Jan-08 Jan-09 Dec-09 Dec-10 Nov-11

%

Rediscount CPI y/y (RHS)Central Bank Rate

African Markets Revealed — January 2012

18 Fixed Income Research

We expect yields on domestic securities to continue to edge higher towards the end of H1:12. Increased flows to the local banking system from the oil and gas sector un-der the new FX regulations as well as increased public spending in the run-up to the elections are likely to add to AOA liquidity. In line with the central bank’s intentions to reduce inflation to 10.0% y/y in 2012, it will undoubtedly seek to limit the impact this increased liquidity may have on demand side inflation pressures. Consequently, the BNA is likely to increase its issuance of central bank pa-per to mop up the excess liquidity in the money market. While this is likely to be concentrated in T-bills, the Ango-lan authorities have indicated that bonds will be a key element of their medium-term debt strategy.

The USD/AOA is the main monetary policy anchor, with the central bank likely to remain the main source of FX. Thus, the BNA is expected to continue to heavily manage the exchange rate in 2012, despite claims that is it is looking to gradually allow more flexibility in the market. The BNA’s preference is likely to remain in favour of USD/AOA stability to avoid inflationary pressure from imported goods that would follow from the AOA deprecia-tion. The new FX regulations for the gas and oil sectors bring downside risks for USD/AOA. The BNA is unlikely to welcome sharp currency strengthening as this would be detrimental to growth in the non-oil sectors of the economy, which remains a key priority. The law will therefore be phased in over 2-y so as to allow the BNA to enhance the effectiveness of its monetary policy frame-work and instruments.

Bond curve outlook: increased issuance Changes in yield curve

Sources: BNA; Standard Bank Research

FX outlook: USD/AOA downside risks USD/AOA: forwards versus forecast

Sources: Bloomberg; Standard Bank Research

Money supply growth: managing expansion Oil earnings and FX reserves

Sources: Bloomberg; Standard Bank Research Sources: Banco Nacional de Angola; Standard Bank Research

Angola

3.00

5.25

7.50

9.75

91-d 182-d 364-d

YTM (%)

29-Dec 07-Jul 4-m forecast

0.0

35.0

70.0

105.0

140.0

Jan-05 Jan-07 Jan-09 Jan-11M3 y/y

0.0

1.4

2.8

4.2

5.6

7.0

0.0

5.5

11.0

16.5

22.0

27.5

Dec-08 Mar-10 Jun-11

Thou

sand

s

Oil earnings per month (USD bn) LHSGross FX reserves (USD bn) RHS

70

79

88

96

105

Dec-06 Mar-08 Jun-09 Aug-10 Nov-11 Feb-13

USD/AOA

History Forw ards Forecast

19 Fixed Income Research

African Markets Revealed — January 2012

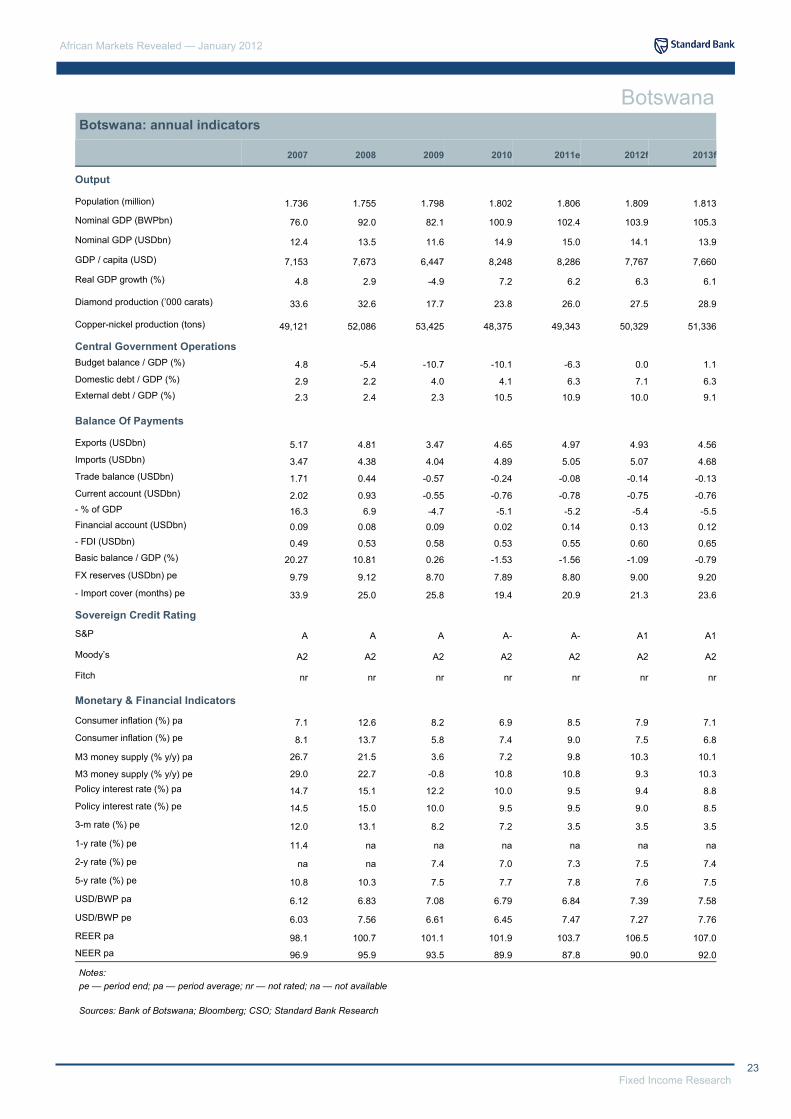

Angola: annual indicators

Notes: pe — period end; pa — period average; na — not available; nr — not rated

Sources: Banco Nacional de Angola; Angola Ministry of Finance; Standard Bank Research; Bloomberg

Angola

2007 2008 2009 2010 2011e 2012f

Output

Population (million) 17.6 18.0 18.5 19.1 19.6 20.2

Nominal GDP (AOAbn) 4,637 6,316 5,989 7,580 8,913 10,927

Nominal GDP (USDbn) 60.4 84.2 75.6 82.5 95.1 113.9

GDP / capita (USD) 3,440 4,673 4,087 4,328 4,846 5,634

Real GDP growth (%) 20.3 13.4 2.4 3.4 4.1 11.4

Oil production capacity ('000 bpd) 1,410 1,700 1,795 1,831 1,690 1,840

Central Government Operations

Budget balance / GDP (%) 12.4 8.9 -9.8 8.9 9.3 9.3

Domestic debt / GDP (%) 16.0 15.0 16.3 16.0 15.4 12.4

External debt / GDP (%) 9.9 16.5 20.0 19.0 17.5 14.7

Balance Of Payments

Exports of goods & services (USDbn) 33.3 38.0 40.0 41.9 53.6 68.6

Imports of goods & services (USDbn) 16.3 26.3 43.1 41.8 35.6 44.8

Trade balance (USDbn) 17.1 11.7 -3.1 0.1 18.0 23.8

Current account (USDbn) 9.7 7.2 -7.6 9.6 15.5 10.7

- % of GDP 16.1 8.5 -10.0 11.7 16.3 9.4

Capital & Financial account (USDbn) -6.3 -0.7 -1.6 -3.5 -9.2 2.1

- FDI (USDbn) -0.9 1.7 2.2 9.9 4.2 5.4

Basic balance / GDP (%) 14.6 10.5 -7.1 23.7 20.7 14.1

FX reserves (USDbn) pe 11.2 17.9 13.7 19.7 26.1 38.9

- Import cover (months) pe 8.3 8.2 3.8 5.7 8.8 10.4

Sovereign Credit Rating

S&P NR NR NR B+ BB- BB-

Moody’s NR NR NR B1 Ba3 Ba3

Fitch NR NR NR B+ BB- BB-

Monetary & Financial Indicators

Consumer inflation (%) pa 12.3 12.5 13.7 14.4 13.5 11.2

Consumer inflation (%) pe 11.8 13.2 14.0 15.3 11.0 11.6

M3 money supply (% y/y) pa 42.9 74.4 45.4 16.5 21.6 34.1

M3 money supply (% y/y) pe 45 93.1 21.5 21.5 35.7 26.4

BNA discount rate (%) pa 18 24.5 29.2 21.7 20.8 20.0

BNA discount rate (%) pe 19.6 30.0 25.0 20.0 20.0 20.0

3-m rate (%) pe 14.1 14.6 15.0 11.0 3.9 7.2

1-y rate (%) pe 14.0 14.5 20.4 13.6 5.0 9.4

USD/AOA pa 76.8 75.0 79.2 91.9 93.7 96.0

USD/AOA pe 75.0 75.2 89.2 92.6 94.6 96.8

REER pa 503 563 603 630 594 603 NEER pa 27.7 28.5 29.4 31.6 36.4 38.9

2013f

20.8

13,076

133.3

6,402

8.9

2,105

6.7

11.3

14.4

73.4

47.0

26.5

17.5

13.1

1.0

6.7

18.2

57.4

14.7

BB-

Ba3

BB-

10.8

9.7

24.2

17.4

17.6

16.5

5.9

8.2

98.1

99.4

596 38.7

African Markets Revealed — January 2012

20 Fixed Income Research

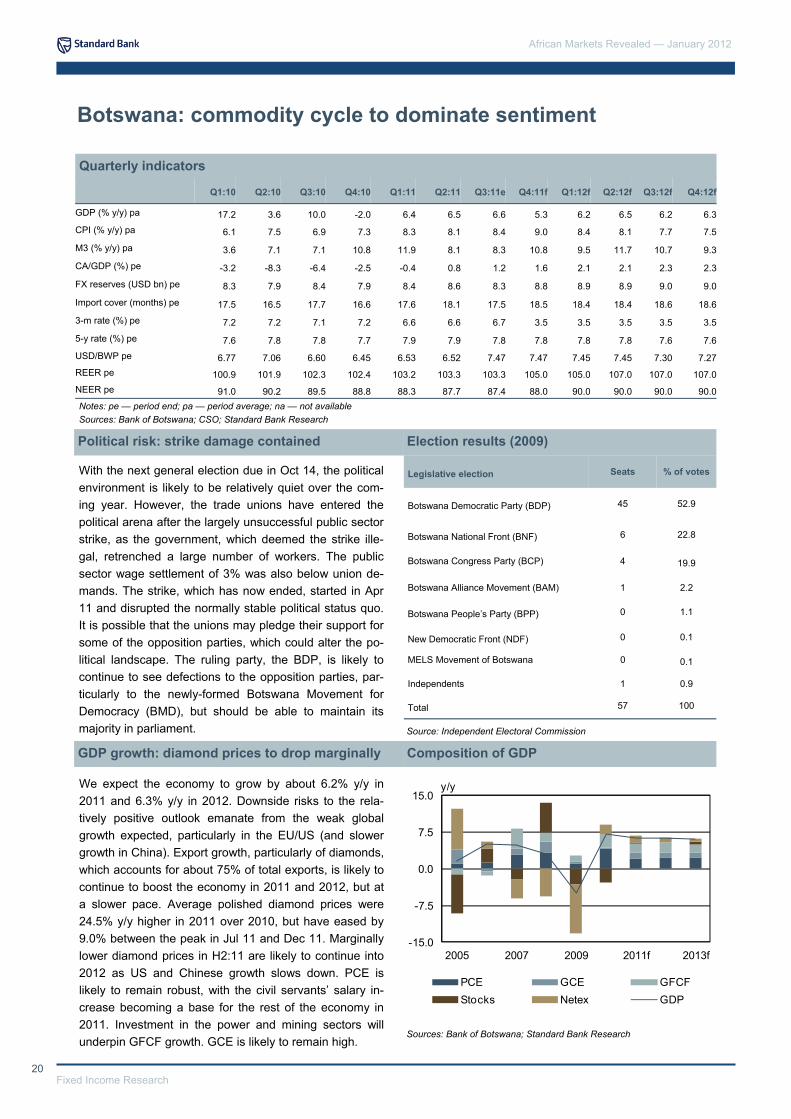

Botswana: commodity cycle to dominate sentiment

With the next general election due in Oct 14, the political environment is likely to be relatively quiet over the com-ing year. However, the trade unions have entered the political arena after the largely unsuccessful public sector strike, as the government, which deemed the strike ille-gal, retrenched a large number of workers. The public sector wage settlement of 3% was also below union de-mands. The strike, which has now ended, started in Apr 11 and disrupted the normally stable political status quo. It is possible that the unions may pledge their support for some of the opposition parties, which could alter the po-litical landscape. The ruling party, the BDP, is likely to continue to see defections to the opposition parties, par-ticularly to the newly-formed Botswana Movement for Democracy (BMD), but should be able to maintain its majority in parliament.

We expect the economy to grow by about 6.2% y/y in 2011 and 6.3% y/y in 2012. Downside risks to the rela-tively positive outlook emanate from the weak global growth expected, particularly in the EU/US (and slower growth in China). Export growth, particularly of diamonds, which accounts for about 75% of total exports, is likely to continue to boost the economy in 2011 and 2012, but at a slower pace. Average polished diamond prices were 24.5% y/y higher in 2011 over 2010, but have eased by 9.0% between the peak in Jul 11 and Dec 11. Marginally lower diamond prices in H2:11 are likely to continue into 2012 as US and Chinese growth slows down. PCE is likely to remain robust, with the civil servants’ salary in-crease becoming a base for the rest of the economy in 2011. Investment in the power and mining sectors will underpin GFCF growth. GCE is likely to remain high.

Quarterly indicators

Political risk: strike damage contained Election results (2009)

GDP growth: diamond prices to drop marginally Composition of GDP

Q1:10 Q2:10 Q3:10 Q4:10 Q1:11 Q2:11 Q3:11e Q4:11f Q1:12f Q2:12f Q3:12f Q4:12f

GDP (% y/y) pa 17.2 3.6 10.0 -2.0 6.4 6.5 6.6 5.3 6.2 6.5 6.2 6.3 CPI (% y/y) pa 6.1 7.5 6.9 7.3 8.3 8.1 8.4 9.0 8.4 8.1 7.7 7.5

M3 (% y/y) pa 3.6 7.1 7.1 10.8 11.9 8.1 8.3 10.8 9.5 11.7 10.7 9.3

CA/GDP (%) pe -3.2 -8.3 -6.4 -2.5 -0.4 0.8 1.2 1.6 2.1 2.1 2.3 2.3

FX reserves (USD bn) pe 8.3 7.9 8.4 7.9 8.4 8.6 8.3 8.8 8.9 8.9 9.0 9.0

Import cover (months) pe 17.5 16.5 17.7 16.6 17.6 18.1 17.5 18.5 18.4 18.4 18.6 18.6

3-m rate (%) pe 7.2 7.2 7.1 7.2 6.6 6.6 6.7 3.5 3.5 3.5 3.5 3.5

5-y rate (%) pe 7.6 7.8 7.8 7.7 7.9 7.9 7.8 7.8 7.8 7.8 7.6 7.6 USD/BWP pe 6.77 7.06 6.60 6.45 6.53 6.52 7.47 7.47 7.45 7.45 7.30 7.27 REER pe 100.9 101.9 102.3 102.4 103.2 103.3 103.3 105.0 105.0 107.0 107.0 107.0 NEER pe 91.0 90.2 89.5 88.8 88.3 87.7 87.4 88.0 90.0 90.0 90.0 90.0 Notes: pe — period end; pa — period average; na — not available Sources: Bank of Botswana; CSO; Standard Bank Research

Sources: Bank of Botswana; Standard Bank Research

Legislative election Seats % of votes

Botswana Democratic Party (BDP) 45 52.9

Botswana National Front (BNF) 6 22.8

Botswana Congress Party (BCP) 4 19.9

Botswana Alliance Movement (BAM) 1 2.2

Botswana People’s Party (BPP) 0 1.1

New Democratic Front (NDF) 0 0.1

MELS Movement of Botswana 0 0.1

Independents 1 0.9

Total 57 100

Source: Independent Electoral Commission

-15.0

-7.5

0.0

7.5

15.0

2005 2007 2009 2011f 2013f

y/y

PCE GCE GFCFStocks Netex GDP

21 Fixed Income Research

African Markets Revealed — January 2012

We expect the trade account to register small deficits in 2011 to 2013. Relatively high polished diamond prices are likely to support export earnings over the coming year. The capital and financial account is likely to be boosted by foreign direct investment, particularly in the mining (the De Beers relocation, and coal and copper mines) and finance sectors. However, imports will proba-bly outpace exports as capital imports for infrastructure development, new mining ventures and power sector investments, drive total imports higher. Fuel imports, the second-largest import item, are likely to rise on the back of the weaker BWP. Higher SACU receipts are expected to boost the transfer account. The C/A is likely to register a deficit of 5.1% of GDP in 2012. We expect FX reserves of about USD9.0bn in Dec 12, covering ca. 18 months of imports.

We expect the fiscal deficit to be lower than projected in the FY2011/12 budget. South Africa’s Budget Review 2011 projected that total SACU payments would rise by 21.6% y/y in FY2011/12, to ZAR21.76bn (USD3.1bn). In FY2012/13, total SACU payments are projected to rise by 49.0%, to ZAR32.43bn (USD4.4bn). The higher total SACU revenue will boost union members’ revenues, in-cluding Botswana’s revenues. SACU revenue contributed 26.4% to Bostwana’s total revenue in FY2009/10. Higher mining taxes will also support total revenue if mineral production is sustained and commodity prices hold on their current levels in 2012. However, the oversized wage bill will rise on the back of the increase in civil servants salaries after the 2011 strike. The improved outlook gen-erally depends on sustained global growth, which is in-creasingly looking more doubtful.

The MPC is likely to keep the bank rate at current levels of 9.5% for the next 6-m. It continues to expect that infla-tion will drop to within the 3-6% objective range in H2:12. We expect inflation to average 7.9% y/y in 2012, from an estimated 8.5% y/y in 2011. Consumer inflation surged in Nov 11, to 9.2% y/y, the highest print in 2011, and aver-aged 8.4% from Jan to Nov 11. Nevertheless, we expect headline inflation to ease as base effects are likely to impact the two main CPI groups from Q1:12. Transport inflation (CPI weight of 18.9%) was high and averaged 13.0% y/y, but food inflation (CPI weight of 21.8%) re-mained low at 6.7% y/y from Jan to Nov 11. Lower im-ported inflation from South Africa, which is expected to average 6.0% y/y in 2012, is also likely to moderate prices pressures. The weaker BWP is a risk to the out-look.

Balance of payments: trade deficit likely Current account developments

Fiscal policy: fiscal pressures subdued Central government budget

Monetary policy: neutral policy stance Inflation and interest rates

Sources: Bank of Botswana; IMF; Standard Bank Research

Source: Ministry of Finance

Sources: Bank of Botswana; CSO; Standard Bank Research

% of GDP 2010/11 2011/12

Total revenue 29.8 31.1

Total expenditure 39.9 37.5

- wages 11.7 10.6

- interest 0.5 0.5

- development 13.1 9.8

Overall balance (- grants) -9.5 -6.0

Overall balance (+ grants) -10.1 -6.3

Net external borrowing 19.1 19.0

Net domestic borrowing 6.4 8.0

Donor support (grants) 0.5 0.3

Botswana

-1,800

-550

700

1,950

3,200

2006 2008 2010 2012f

USD m

Trade Services IncomeTransfers C/A

0.0

4.5

9.0

13.5

18.0

Dec-05 Jun-07 Dec-08 Jun-10 Dec-11

Inflation Lower boundUpper bound Bank rate

%, y/y

African Markets Revealed — January 2012

22 Fixed Income Research

We expect that yields will remain largely unchanged over the coming 6-m period. Yields on BOBCs have been volatile over the past few weeks after the BOB unexpect-edly changed its conduct of monetary policy in mid-Nov. The BOB reduced the amount of BOBCs it issues as it needed to drain less excess liquidity from the money market on the back of lower BOP surpluses. The yield on the 91-d BOBC fell to 3.45% at the auction on 6 Dec from 6.62% previously, but rose to 5.29% on 30 Dec. The 14-d BOBC yield increased to 4.46% at the auction on 6 Dec compared to 2.69% the auction on 29 Nov, but is below the 6.48% level at earlier auctions. On 30 Dec the yield was 4.51%. Since 2006 only commercial banks have been permitted to hold BOBCs. The bank rate is also likely to remain at the current level of 9.5%. Bond auc-tions are only held in Mar and Sep.

We expect the USD/BWP to trade weaker in 2012. The USD/BWP is forecast to average 7.39 in 2012 and to trade at 7.27 in Dec 12, compared to an average of 6.84 in 2011. In 2010, the USD/BWP averaged 6.79. USD/BWP volatility is likely to persist and risks are to the up-side. Risk-off sentiment towards emerging markets drove the BWP sharply higher to 7.46 in Sep 11, from 6.68 in Aug 11. Ongoing concerns about the possible break-up of the Euro area, sovereign credit defaults in Greece and other Eurozone countries and heightened risks to US, Chinese and global growth will continue to depress inves-tor sentiment over the coming year. Given the ZAR’s dominant share in the BWP basket peg (estimated at 65%, with the SDR at about 35%), the USD/BWP is likely to continue to track the USD/ZAR higher. Since Sep, the USD/BWP has weakened in tandem with USD/ZAR.

We expect the BSE to generally disappoint in 2012. Risk aversion towards emerging markets is likely to have a negative influence on the local equity market as well as emerging markets in general. The BSE is likely to per-form broadly in line with the MSCI EM index. Both the Foreign Companies Index (FCI) and the Domestic Com-panies Index (DCI) are strongly correlated with the MSCI EM index, the FCI by a coefficient of 0.76 and the DCI by 0.68. Nevertheless, both the FCI and DCI outperformed the MSCI EM index in 2011, supported by buoyant do-mestic economic growth. The MSCI EM index dropped by 19.2% y/y in 2011, from an increase of 13.3% y/y in 2010. The FCI rose by 1.8% y/y, compared to 16.2% y/y in 2010, and the DCI rose by 8.7% y/y in 2011, against a drop of 11.7% y/y in 2010.

Bond curve outlook: stable yields expected Changes in yield curve

FX outlook: further weakness in sight USD/BWP: forwards versus forecast

Equity market: lacklustre performance ahead Botswana Stock Exchange

Sources: Bank of Botswana; Standard Bank Research

Sources: Reuters; Standard Bank Research

Sources: Reuters; Standard Bank Research

Botswana

3.0

4.5

6.0

7.5

9.0

91-d 182-d 2-y 5-y 8-y 9-y 15-y

6-m forcast 12-Dec-11 12-Jul-11

YTM

2,000

4,250

6,500

8,750

11,000

400

1,050

1,700

2,350

3,000

Jan-05 Oct-06 Jun-08 Mar-10 Dec-11

FCI (lh) MSCI EM (lh) DCI (rh)

FCI & MSCI EM DCI

5.0

6.0

7.0

8.0

9.0

Dec-06 Mar-08 Jun-09 Aug-10 Nov-11 Feb-13

USD/BWP

History Forw ards Forecast

23 Fixed Income Research

African Markets Revealed — January 2012

Botswana: annual indicators

2007 2008 2009 2010 2011e 2012f 2013f

Output Population (million) 1.736 1.755 1.798 1.802 1.806 1.809 1.813

Nominal GDP (BWPbn) 76.0 92.0 82.1 100.9 102.4 103.9 105.3

Nominal GDP (USDbn) 12.4 13.5 11.6 14.9 15.0 14.1 13.9

GDP / capita (USD) 7,153 7,673 6,447 8,248 8,286 7,767 7,660

Real GDP growth (%) 4.8 2.9 -4.9 7.2 6.2 6.3 6.1

Diamond production (’000 carats) 33.6 32.6 17.7 23.8 26.0 27.5 28.9

Copper-nickel production (tons) 49,121 52,086 53,425 48,375 49,343 50,329 51,336

Central Government Operations

Budget balance / GDP (%) 4.8 -5.4 -10.7 -10.1 -6.3 0.0 1.1 Domestic debt / GDP (%) 2.9 2.2 4.0 4.1 6.3 7.1 6.3 External debt / GDP (%) 2.3 2.4 2.3 10.5 10.9 10.0 9.1

Balance Of Payments

Exports (USDbn) 5.17 4.81 3.47 4.65 4.97 4.93 4.56 Imports (USDbn) 3.47 4.38 4.04 4.89 5.05 5.07 4.68 Trade balance (USDbn) 1.71 0.44 -0.57 -0.24 -0.08 -0.14 -0.13 Current account (USDbn) 2.02 0.93 -0.55 -0.76 -0.78 -0.75 -0.76 - % of GDP 16.3 6.9 -4.7 -5.1 -5.2 -5.4 -5.5 Financial account (USDbn) 0.09 0.08 0.09 0.02 0.14 0.13 0.12 - FDI (USDbn) 0.49 0.53 0.58 0.53 0.55 0.60 0.65 Basic balance / GDP (%) 20.27 10.81 0.26 -1.53 -1.56 -1.09 -0.79 FX reserves (USDbn) pe 9.79 9.12 8.70 7.89 8.80 9.00 9.20

- Import cover (months) pe 33.9 25.0 25.8 19.4 20.9 21.3 23.6

Sovereign Credit Rating

S&P A A A A- A- A1 A1

Moody’s A2 A2 A2 A2 A2 A2 A2

Fitch nr nr nr nr nr nr nr

Monetary & Financial Indicators Consumer inflation (%) pa 7.1 12.6 8.2 6.9 8.5 7.9 7.1 Consumer inflation (%) pe 8.1 13.7 5.8 7.4 9.0 7.5 6.8

M3 money supply (% y/y) pa 26.7 21.5 3.6 7.2 9.8 10.3 10.1

M3 money supply (% y/y) pe 29.0 22.7 -0.8 10.8 10.8 9.3 10.3 Policy interest rate (%) pa 14.7 15.1 12.2 10.0 9.5 9.4 8.8 Policy interest rate (%) pe 14.5 15.0 10.0 9.5 9.5 9.0 8.5

3-m rate (%) pe 12.0 13.1 8.2 7.2 3.5 3.5 3.5

1-y rate (%) pe 11.4 na na na na na na

2-y rate (%) pe na na 7.4 7.0 7.3 7.5 7.4

5-y rate (%) pe 10.8 10.3 7.5 7.7 7.8 7.6 7.5

USD/BWP pa 6.12 6.83 7.08 6.79 6.84 7.39 7.58

USD/BWP pe 6.03 7.56 6.61 6.45 7.47 7.27 7.76

REER pa 98.1 100.7 101.1 101.9 103.7 106.5 107.0 NEER pa 96.9 95.9 93.5 89.9 87.8 90.0 92.0

Notes: pe — period end; pa — period average; nr — not rated; na — not available

Sources: Bank of Botswana; Bloomberg; CSO; Standard Bank Research

Botswana

African Markets Revealed — January 2012

24 Fixed Income Research

Côte d’Ivoire: strong post-crisis rebound

The parties supporting President Alassane Ouattara won the 11 Dec 11 parliamentary elections by a landslide, confirming their political dominance and benefiting from the opposition FPI’s decision to boycott the contest. Ouattara’s own party (RDR) secured 127 of 254 declared seats, while the PDCI won 77 seats. These smooth legis-lative elections are a major step in the normalisation of the country’s institutional framework, which will be com-pleted when mayoral and regional elections take place in early 2012. Whether Prime Minister Guillaume Soro will retain his position is still unclear, although this could cre-ate some friction within the ruling coalition. While the formation of an integrated army remains a priority, the policy focus is shifting to the economy and structural re-forms, especially in the cocoa sector, which is a pre-requisite for reaching the HIPC completion point.

GDP contracted by an estimated 4.2% in 2011, because of the political disquiet in Jan-Apr, but appeared to be recovering rapidly in H2:11. Industrial production in Jul 11 was only down 2.0% y/y, while agricultural and mining production improved further in Q3:11. We expect growth to rebound to 7.5% y/y in 2012, assisted by the low base in 2011. The improving political-economy, coupled with a resumption of bank lending, will support private sector consumption. Higher investment in infrastructure and development projects, after nearly a decade of stagna-tion, will also underpin the pick-up in GDP growth. Fi-nally, the net export position will probably deteriorate, although the unfavourable base effects in cocoa vol-umes, higher aggregate demand and the effects of a weaker XOF will be offset by a recovery in non-cocoa exports.

Quarterly indicators

Political risk: pro-Ouattara legislative majority Election results

GDP growth: strong economic rebound Composition of GDP

Notes: pe — period end; pa — period average Sources: IMF; Ministere de l’economie et des finances; Institut National de la Statistique; Standard Bank Research; Bloomberg

Sources: IMF; Standard Bank Research

Source: Independent Electoral Commission

Q1:10 Q2:10 Q3:10 Q4:10 Q1:11 Q2:11 Q3:11e Q4:11f Q1:12f Q2:12f Q3:12f Q4:12f

GDP (% y/y) pa 3.0 2.6 2.6 1.5 -13.6 -6.5 0.2 3.1 9.6 7.6 6.5 6.4

CPI (% y/y) pa -0.1 1.0 1.8 3.9 5.2 6.7 4.6 3.1 2.0 0.3 3.2 4.7

M2 (% y/y) pe 16.0 20.6 32.2 28.4 15.1 15.3 18.0 13.7 14.6 16.3 12.5 18.0

CA/GDP (%) pa 2.1 1.5 1.4 2.2 4.0 2.8 3.7 1.9 -0.5 -2.6 -1.9 -1.7

FX reserves (USD bn) pe 3.1 3.0 3.3 3.6 3.5 4.0 4.4 4.5 4.6 4.6 4.7 4.7

Import cover (mths) pe 5.0 4.7 5.2 5.8 5.6 6.4 7.0 7.2 7.2 7.2 7.3 7.3

Marginal lending facility (%) pe 4.25 4.25 4.25 4.25 4.25 4.25 4.25 4.25 4.25 4.25 4.25 4.25

USD/XOF pe 482 537 483 491 466 452 492 509 519 536 548 525

REER (Q4:05=100) pe 102 98 99 102 104 107 106 101 98 95 97 99 NEER (Q4:05=100) pe 103 99 100 101 102 104 104 100 98 96 96 97

Presidential election (run-off), Nov 10 Party % of votes

Alassane Ouattara RHDP 54.1

Laurent Gbagbo LMP 45.9

Presidential election, Dec 11 Party % of votes

Rally of Republicans 127 49.8

Democratic Party of Côte d’Ivoire 77 30.2 Union for Democracy and Peace in Côte d’Ivoire 7 2.7

Rally of Houphouetists for Democracy/Peace 4 1.6

Movement of the Forces of the Future 3 1.2

Union for Côte d’Ivoire 1 0.4

Independents 35 13.7

-8

-4

0

4

8

2007 2008 2009 2010 2011e 2012f 2013f

%

PCE GCE GFCF Netex GDP

25 Fixed Income Research

African Markets Revealed — January 2012

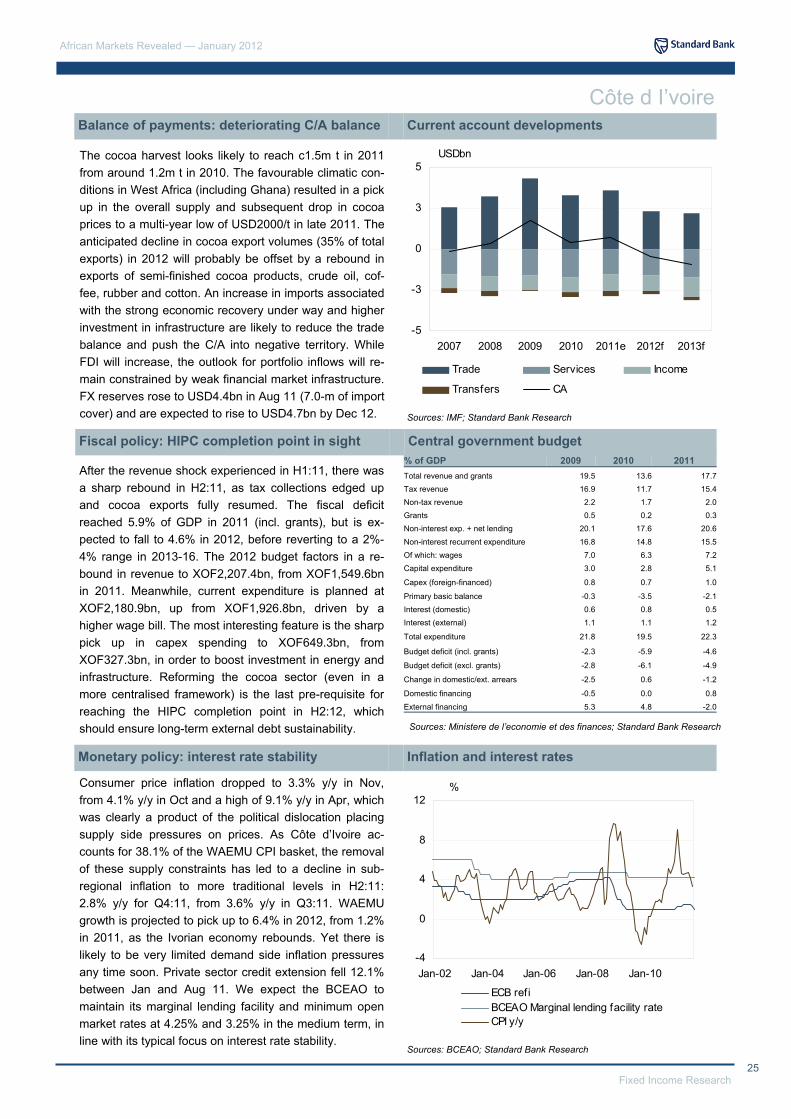

The cocoa harvest looks likely to reach c1.5m t in 2011 from around 1.2m t in 2010. The favourable climatic con-ditions in West Africa (including Ghana) resulted in a pick up in the overall supply and subsequent drop in cocoa prices to a multi-year low of USD2000/t in late 2011. The anticipated decline in cocoa export volumes (35% of total exports) in 2012 will probably be offset by a rebound in exports of semi-finished cocoa products, crude oil, cof-fee, rubber and cotton. An increase in imports associated with the strong economic recovery under way and higher investment in infrastructure are likely to reduce the trade balance and push the C/A into negative territory. While FDI will increase, the outlook for portfolio inflows will re-main constrained by weak financial market infrastructure. FX reserves rose to USD4.4bn in Aug 11 (7.0-m of import cover) and are expected to rise to USD4.7bn by Dec 12.

After the revenue shock experienced in H1:11, there was a sharp rebound in H2:11, as tax collections edged up and cocoa exports fully resumed. The fiscal deficit reached 5.9% of GDP in 2011 (incl. grants), but is ex-pected to fall to 4.6% in 2012, before reverting to a 2%-4% range in 2013-16. The 2012 budget factors in a re-bound in revenue to XOF2,207.4bn, from XOF1,549.6bn in 2011. Meanwhile, current expenditure is planned at XOF2,180.9bn, up from XOF1,926.8bn, driven by a higher wage bill. The most interesting feature is the sharp pick up in capex spending to XOF649.3bn, from XOF327.3bn, in order to boost investment in energy and infrastructure. Reforming the cocoa sector (even in a more centralised framework) is the last pre-requisite for reaching the HIPC completion point in H2:12, which should ensure long-term external debt sustainability.

Consumer price inflation dropped to 3.3% y/y in Nov, from 4.1% y/y in Oct and a high of 9.1% y/y in Apr, which was clearly a product of the political dislocation placing supply side pressures on prices. As Côte d’Ivoire ac-counts for 38.1% of the WAEMU CPI basket, the removal of these supply constraints has led to a decline in sub-regional inflation to more traditional levels in H2:11: 2.8% y/y for Q4:11, from 3.6% y/y in Q3:11. WAEMU growth is projected to pick up to 6.4% in 2012, from 1.2% in 2011, as the Ivorian economy rebounds. Yet there is likely to be very limited demand side inflation pressures any time soon. Private sector credit extension fell 12.1% between Jan and Aug 11. We expect the BCEAO to maintain its marginal lending facility and minimum open market rates at 4.25% and 3.25% in the medium term, in line with its typical focus on interest rate stability.

Balance of payments: deteriorating C/A balance Current account developments

Fiscal policy: HIPC completion point in sight Central government budget

Monetary policy: interest rate stability Inflation and interest rates

Sources: IMF; Standard Bank Research

Sources: Ministere de l’economie et des finances; Standard Bank Research

Sources: BCEAO; Standard Bank Research

Côte d I’voire

% of GDP 2009 2010 Total revenue and grants 19.5 13.6 Tax revenue 16.9 11.7 Non-tax revenue 2.2 1.7

Non-interest exp. + net lending 20.1 17.6

Non-interest recurrent expenditure 16.8 14.8 Of which: wages 7.0 6.3 Capital expenditure 3.0 2.8

Capex (foreign-financed) 0.8 0.7

Grants 0.5 0.2

2011 17.7 15.4

2.0 0.3

20.6

15.5 7.2 5.1

1.0

Primary basic balance -0.3 -3.5 -2.1 Interest (domestic) 0.6 0.8 0.5 Interest (external) 1.1 1.1 1.2

Total expenditure 21.8 19.5 22.3

Budget deficit (incl. grants) -2.3 -5.9 -4.6

Budget deficit (excl. grants) -2.8 -6.1 -4.9

Change in domestic/ext. arrears -2.5 0.6 -1.2

Domestic financing -0.5 0.0 0.8

External financing 5.3 4.8 -2.0

-5

-3

0

3

5

2007 2008 2009 2010 2011e 2012f 2013f

USDbn

Trade Services Income

Transfers CA

-4

0

4

8

12

Jan-02 Jan-04 Jan-06 Jan-08 Jan-10

%

ECB refiBCEAO Marginal lending facility rateCPI y/y

African Markets Revealed — January 2012

26 Fixed Income Research

The USD2.3bn defaulted Eurobond (due in 2032) has continued to trade in a 50-55 range since Jun 11 (54 on 10 Jan 12), excepting a few outliers. This resilience re-flects the expected resumption of regular coupon pay-ments in 2012. The Finance Ministry confirmed in mid-Nov 11 that it would resume regular service payment from Jun 12’s coupon, but said it will only be able to make a good faith payment on the three missed coupons (Dec 10, Jun 11 and Dec 11). A more detailed schedule for the arrears clearance will probably be released in 2012 as the country heads for the HIPC completion point. Despite Côte d’Ivoire’s poor track record, the price risks look asymmetric, with a shift to 65 or beyond possible with a coupon payment in Jun. Meanwhile, the stock of local T-bills (XOF607bn) was restructured in Nov into 2-, 3- and 5-y bonds at marginally lower rates.

USD/XOF tracks EUR/USD via the EUR/XOF peg (655.9), a mechanism that has been in place since 1960. The EUR/XOF peg was adjusted only once in 1994, at a time when CFA countries experienced significant fiscal and external distortions. Recent media speculation that XOF (XAF) would be devalued has been denied by the BCEAO (BEAC) as well as WAEMU (CEMAC) Finance Ministers and senior officials. We also believe that there will be no devaluation, which is after all consistent with relatively healthy fundamentals and the zone’s positive balance with its French counterparty (the BCEAO [BEAC] places 50% of its net foreign assets with the French Treasury). WAEMU’s external competitiveness is likely to improve further as the EUR weakens amid significant fiscal distortions. We see USD/XOF trending higher to 540 in 6-m, before recovering modestly in late 2012.

The BRVM index lost 12.7% in 2011, primarily due to the general risk aversion among international investors, a difficult post-electoral environment and sharp deteriora-tion in corporate results for H1:11. For example, Societe Generale’s Ivorian Unit (SGBCI) recorded a 53% y/y de-cline in profit over the period. Furthermore, Senegal-based telecoms operator SONATEL (c40% of market cap) also weighed negatively on the BRVM, as its stock fell 22.0% last year. In this context, one may argue that the performance of the Ivorian stocks was probably not as disastrous as might be expected, especially compared to the MSCI EM (-18.7%) and MSCI FM (-21.6%) indices. Despite the likely difficult global environment in 2012 (and EUR [XOF] weakness), BRVM stocks will be sup-ported by an economic rebound in Côte d’Ivoire and sub-sequent recovery in corporate results.

Eurobond: resuming regular coupon payments Côte d’Ivoire 2032

FX outlook: no devaluation in sight USD/XOF: forwards versus forecast

Equity market: recovery in corporate results Bourse Regionale Valuers Mobiliers

Sources: Reuters; Standard Bank Research

Sources: Bloomberg; Standard Bank Research

Sources: Bloomberg; Standard Bank Research

Côte d I’voire

30

40

50

60

70

Apr-10 Aug-10 Dec-10 Apr-11 Aug-11 Dec-11

Price

60

110

160

210

260

Jan-02 Nov-04 Sep-07 Jul-10

Index

400

440

480

520

560

Dec-06 Mar-08 Jun-09 Aug-10 Nov-11 Feb-13

USD/XOF

History Forw ards Forecast

27 Fixed Income Research

African Markets Revealed — January 2012

Côte d I’voire: annual indicators

Sources: Institut National de la Statistique, Ministere de l’economie et des finances; IMF; Standard Bank Research; Bloomberg

Notes: pe — period end; pa — period average; na — not available; nr — not rated

Côte d I’voire

2007 2008 2009 2010 2011e 2012f

Output

Population (million) 20.2 20.8 21.4 22.0 22.7 23.4

Nominal GDP (XOFbn) 9,487 10,485 10,999 11,443 11,523 12,687

Nominal GDP (USDbn) 19.8 23.4 23.8 23.1 23.2 23.8

GDP / capita (USD) 983 1,127 1,113 1,048 1,024 1,019

Real GDP growth (%) 1.6 2.3 3.8 2.4 -4.2 7.5

Oil Production ('000 bbl) 53,132 60,209 58,861 45,295 40,270 46,250

Central Government Operations

Budget balance (excl. Grants) / GDP (%) -1.9 -2.3 -2.1 -2.8 -6.1 -4.9

Budget balance (incl. Grants) / GDP (%) -1.3 -0.6 -1.6 -2.3 -5.9 -4.6

Domestic debt / GDP (%) 10.8 13.4 12.5 15.7 14.9 14.1

External debt / GDP (%) 64.8 61.9 53.3 50.2 52.0 48.0

Balance of Payments

Exports of goods and services (USDbn) 8.7 10.1 10.9 10.8 11.1 10.0

Imports of goods and services (USDbn) 6.1 6.9 6.6 7.5 7.5 7.7

Trade balance (USDbn) 2.6 3.2 4.3 3.3 3.6 2.3