2014.05.20_oecd-eclac-pse forum_miotti

TRANSCRIPT

DIVERSIFICATION PRODUCTIVE :

SCIENCE, TECHNOLOGIE, INNOVATION

… ÉDUCATION?

Egidio Luis Miotti

Université de Paris Nord (CEPN-CNRS)Directeur Scientifique (Adj.) –

Ministère de l’Enseignement Supérieur et de la Recherche

(MESR)Direction générale de la recherche et de l’innovation

– Politiques d'incitation à la R&D des entreprises

02 Session : Global change, labour market dynamics and the sectoral

structure of production

Europe and Latin America in the wake on global paradigm shifts and

new trends in the world economy

Paris, OCDE Headquarters, 20-21 May 2014

LA PROBLEMATIQUE

o Most countries in Europe and Latin America and the Caribbean

have been very much affected by competition from emerging

Asian countries in manufacturing. This raises the following

questions: What policies can governments adopt to reduce

vulnerability and improve the competitiveness of their

economies in this new scenario? To want extent have these

global trends redefined production and technological leads and

lags and created imbalances?

o The optimal policy emphasis might not be on industry per se, but

more generally on the diversification of the sectoral structure of

production …

Science, technologie, production

LOCALISATION DES ACTIVITÉS

LOCALISATION DES ACTIVITÉS PRODUCTIVES(AVANTAGES COMPARATIVES RÉVÉLÉS – 2009)

SIMILARITÉS DES SPÉCIALISATIONS SCIENTIFIQUES (2011)

BREVETS ET PUBLICATIONS SCIENTIFIQUES(AXES 1 ET 2 – ANALYSE EN COMPOSANTES PRINCIPALES)

BREVETS ET PUBLICATIONS SCIENTIFIQUES(VAGUES SCIENTIFIQUES ET TECHNOLOGIQUES ET PAYS CONCERNÉS)

DEMANDES DE BREVETS AUPRÈS D’EPO(1978-2013, NOMBRE ET %0)

1978-1990 1990-2000 2000-2013 TOTAL 1978-1990 1990-2000 2000-2013 TOTAL

MONDE 493 643 811 031 1 426 021 2 730 695 1 000.000 1 000.000 1 000.000 1 000.000

Argentine 57 249 454 760 0.115 0.307 0.318 0.278

Brésil 177 538 2 023 2 738 0.359 0.663 1.419 1.003

Chili 14 44 296 354 0.028 0.054 0.208 0.130

Colombie 21 28 103 152 0.043 0.035 0.072 0.056

Mexico 60 181 582 823 0.122 0.223 0.408 0.301

Pérou 2 3 14 19 0.004 0.004 0.010 0.007

Amérique Latine 374 1 165 3 568 5 107 0.758 1.436 2.502 1.870

Australie 4 099 5 804 10 664 20 567 8.304 7.156 7.478 7.532

Canada 4 502 10 548 23 463 38 513 9.120 13.006 16.453 14.104

Nouvelle Zélande 428 822 1 872 3 122 0.867 1.014 1.313 1.143

Corée du Sud 199 5 620 46 038 51 857 0.403 6.929 32.284 18.990

Taiwan 54 324 8 156 8 534 0.109 0.399 5.719 3.125

DEMANDES DE BREVETS AUPRÈS D’EPO (NOMBRE)

-

500

1,000

1,500

2,000

2,500

3,000

19

78

19

79

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

Amérique Latine Australie Canada

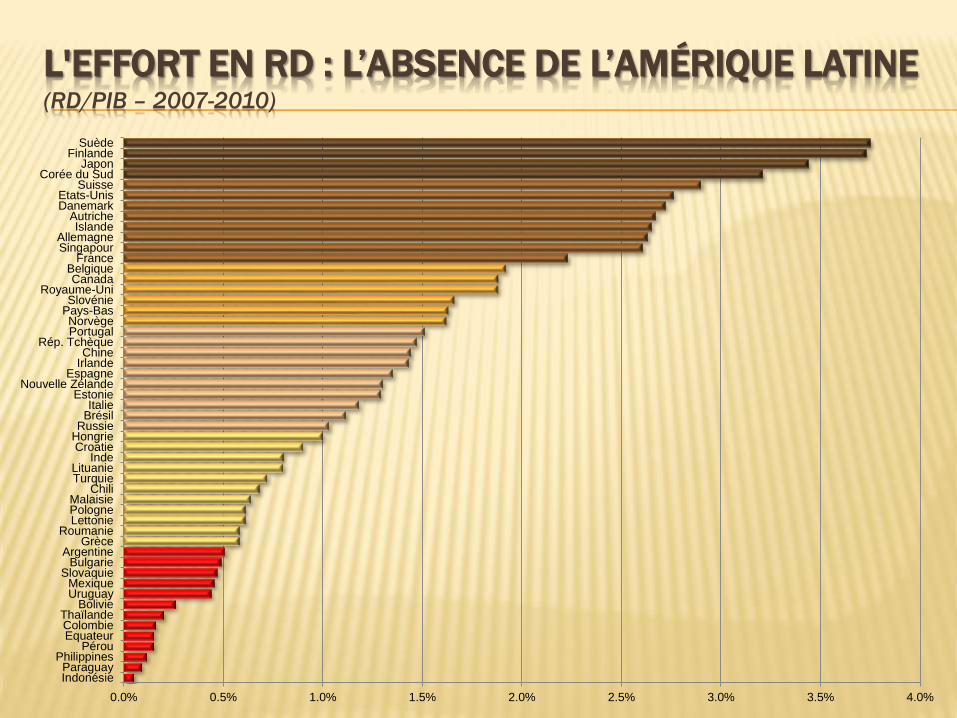

L'EFFORT EN RD : L’ABSENCE DE L’AMÉRIQUE LATINE (RD/PIB – 2007-2010)

0.0% 0.5% 1.0% 1.5% 2.0% 2.5% 3.0% 3.5% 4.0%

IndonésieParaguay

PhilippinesPérou

EquateurColombieThaïlande

BolivieUruguayMexique

SlovaquieBulgarie

ArgentineGrèce

RoumanieLettoniePologneMalaisie

ChiliTurquieLituanie

IndeCroatieHongrieRussieBrésilItalie

EstonieNouvelle Zélande

EspagneIrlandeChine

Rép. TchèquePortugalNorvège

Pays-BasSlovénie

Royaume-UniCanada

BelgiqueFrance

SingapourAllemagne

IslandeAutriche

DanemarkEtats-Unis

SuisseCorée du Sud

JaponFinlande

Suède

L’INNOVATION COMME MODELE DE CATCHING-UP

L’ÉVOLUTION DES POLITIQUES STRUCTURELLES

Période Légitimité Ampleur InstrumentsHiérarchie des politiques

structurelles

1950-1970Monde fermé avec rareté dans la disponibilité des devises

Sectoriel Droits de douane Politiques industrielles

Guerre froide Verticales Politiques fiscales/subventions Politiques de la concurrence

Régimes de croissance autocentrés Infrastructure (parcs industriels)

Grands programmes (Nucléaire, Aéronautique, Télécommunications, Industrie lourde)

1980-1990 Perte de légitimité Démantèlement des procédures et barrières Politiques de la concurrence

Globalisation commerciale et financière

Politiques de compétitivité

1990-2000Nouvelle légitimité dans les politiques d'innovation

Globales Politiques fiscales/subventions Politiques de la concurrence

"Nouvelle économie" Horizontales Infrastructure (pôles technologiques) Politiques de compétitivité

Industries et services

Politiques scientifiques et technologiques

2010 - … Accélération des délocalisations .. Secteurs émergents Politiques fiscales/subventionsPolitiques scientifiques et technologiques

Ré-industrialisation ? …Le retour des Grands programmes ? (Santé, Economie verte, dénucléarisation, …)

Politiques de compétitivité

Politiques de la concurrence

LES RISQUES DE L’INTERVENTION

o Il ne s’agit pas uniquement d’un problème d’évaluation d’impact des politiquespubliques, même si celui-ci est un sujet d’importance cruciale. Il s’agit deminimiser les risques que telle politique peut engendrer en termes declientélisme, corruption et de recherche des rentes (Rodrick, 2004).

o Tel que signalé par Rodrick et Hausmann (2003), l’une des grandes différencesentre les politiques industrielles asiatiques et latino-américaines est que lespremières ont utilisé tant le bâton que la carotte, tandis que les dernières ontprivilégié uniquement la carotte. Ainsi, en Amérique latine, à côté de quelquesrares “champions”, on trouve un grand nombre de choix qui se sont avérésinefficaces, donnant lieu à l’idée du “protectionnisme frivole” de Fanjnzylber(1983).

o En effet, l’idée de base est que la véritable difficulté de la mise en œuvre d’unepolitique structurelle d’intervention ne se trouve pas dans la détection de“champions” (tout en demeurant difficile pour certains, impossible pour d’autres),sinon dans la capacité d’abandonner, plus ou moins rapidement, les perdants,en évitant des transferts inutiles (coûts sociaux et d’opportunité pour lesressources publiques) et l’inefficacité en termes productifs.

LES POLITIQUES D’INCITATION À LA R&D

POURQUOI FAUT IL UNE POLITIQUE D’INCITATION À LA

R&D ?

Firms cannot fully appropriate the benefits of their R&D investments: Patents

are circumvented in different ways, and valuable process and product

innovations are emulated more or less quickly. Even when intellectual property

rights are enforced effectively, R&D generates positive externalities that spill

over to other firms and benefit the economy at large. Firms thus tend to invest

less in R&D projects than they should since they know that other firms will

capture part of the returns, or they tend to wait for other firms to engage in R&D

projects rather than doing so themselves. As a result firms will normally tend to

increase their R&D expenditures to the size where their expected private

returns and marginal costs will match, but they will not increase them further to

the level that would equalize marginal social costs and marginal social returns

and maximize economic efficiency and social welfare. This market failure can

be corrected by direct public funding of research activities performed by public

research organizations and universities and by economic policies supporting

private R&D.

Damien Ientile et Jacques Mairesse - 2009

POURQUOI VOULOIR INTERVENIR?

• The closer an economy is to the world technology frontier, the higher the

relative importance of innovation relative to imitation as a source of

productivity growth.

• Because the selection of high-skill entrepreneurs and firms is more

important for innovation than for adoption, firms in countries that are far from

the technology frontier pursue an investment-based strategy, which features

long-term relationships, high average size and age of firms, large

investments, but little selection.

• Closer to the technology frontier, there is less room for copying and adoption

of well-established technologies; consequently, there is an equilibrium

switch to an innovation-based strategy with short-term relationships,

younger firms, less investment, and better selection of entrepreneurs.

POURQUOI VOULOIR INTERVENIR?

• We showed that economies may switch out of the investment-based

strategy too soon or too late. A standard appropriability effect, resulting from

the fact that firms do not internalize the greater consumer surplus they

create by investing more, implies that the switch may occur too soon.

• In contrast, the presence of retained earnings that incumbent entrepreneurs

can use to shield themselves from competition makes the investment-based

strategy persist for too long.

• When the switch is too soon, government intervention in the form of policies

limiting product market competition or providing subsidies to investment may

be useful because it encourages the investment-based strategy.

• Nevertheless, anticompetitive policies can also lead to a non convergence

trap whereby the economy never switches out of the investment-based

strategy and fails to converge to the world technology frontier.

Daron Acemoglu (MIT) Philippe Aghion (Harvard) Fabrizio Zilibotti (IIES) - 2006

COMMENT INTERVENIR?

o Les subventions à la R&D et les aides fiscales de type crédit d'impôt recherche (CIR)

sont deux modes privilégiés d’aides qui sont supposés complémentaires. La

combinaison de ces outils est cependant hétérogène.

o La popularité croissante des systèmes fiscaux d’aide à la R&D repose d’une part sur

leur généralité, d’autre part sur leur malléabilité. En théorie, toutes les entreprises

peuvent bénéficier d’un tel système, quelles que soient leurs caractéristiques. Dans la

pratique, les aides fiscales à la R&D peuvent être ciblées sur des groupes spécifiques

d'entreprises selon leur secteur, leur taille, leur âge, leur emplacement, leurs liens avec

les laboratoires universitaires et leur technologie (voir Lhuillery, 1996; OCDE, 2010).

o L'attractivité des régimes fiscaux à la R&D repose également sur leur facilité de mise

en œuvre, de modification ou de suppression. Contrairement aux subventions, ils ne

rencontrent pas les problèmes liés au manque d'information sur les innovateurs, les

coûts de procédures bureaucratiques ou de suppression, ou les pressions potentielles

de lobbying. En revanche, les subventions à la R&D peuvent être préférées aux crédits

d'impôt recherche en raison de la possible discrimination entre projets et l’opportunité

de financer uniquement les entreprises les plus innovantes, celles dont l’impact sur le

bien-être social est supérieur. En outre, les subventions à la R&D semblent plus

appropriées que les crédits d'impôt, en particulier ceux en accroissement, pour contrer

les cycles économiques et leurs effets, en particulier dans la phase de ralentissement

(lorsque les entreprises ayant des contraintes budgétaires sévères coupent dans leur

budget de R&D).

DIRECT GOVERNMENT FUNDING OF BERD (2011, EN % DU PIB)

0.00 0.04 0.08 0.12 0.16 0.20 0.24 0.28 0.32 0.36 0.40

MexicoChile (2010)

Australia (2010)Poland

Switzerland (2008)Slovak Republic

TurkeyJapan

PortugalLuxembourg (2009)

ItalySouth Africa (2009)

NetherlandsCanada

China (2009)Denmark

Ireland (2010)New Zealand

FinlandNorway

GermanyUnited KingdomBelgium (2010)

EstoniaBrazil (2010)

AustriaHungarySweden

Spain (2010)France

Czech RepublicIsrael (2010)

KoreaUnited States

SloveniaRussian Federation

INDIRECT GOVERNMENT SUPPORT THROUGH R&D

TAX INCENTIVES (2011, EN % DU PIB)

0.00 0.04 0.08 0.12 0.16 0.20 0.24 0.28

MexicoPoland

Switzerland (2008)Luxembourg (2009)

New ZealandFinland

GermanyEstoniaSweden

Slovak RepublicChile (2010)

ItalySouth Africa (2009)Russian Federation

Spain (2010)Turkey

China (2009)Denmark

NorwayBrazil (2010)

Czech RepublicUnited States

SloveniaJapan

United KingdomHungaryPortugal

Australia (2010)Austria

Ireland (2010)Netherlands

Belgium (2010)Korea

CanadaFrance

TOTAL GOVERNMENT SUPPORT (DIRECT AND TAX) TO

BUSINESS R&D (2011, EN % DU PIB)

0.00 0.04 0.08 0.12 0.16 0.20 0.24 0.28 0.32 0.36 0.40 0.44

MexicoChile (2010)

PolandSwitzerland (2008)

Slovak RepublicLuxembourg (2009)

ItalySouth Africa (2009)

TurkeyNew Zealand

FinlandGermany

JapanChina (2009)

DenmarkEstonia

PortugalSweden

Australia (2010)Norway

Spain (2010)Brazil (2010)

United KingdomNetherlands

Ireland (2010)Hungary

Czech RepublicAustria

CanadaBelgium (2010)

United StatesSloveniaFranceKorea

Russian Federation

Direct government funding of BERD

Indirect government support through R&D tax incentives

MAIS …

o Le problème de l’opportunité de passer à un modèle intensif en

technologie n’est pas de facile …

o … sur tout en présence des comportements rentiers et absence relative

d’entrepreneurs schumpetériens …

o … ou de fortes volatilités macroéconomiques

o Pas toute R&D / innovation est à la portée de tout le monde.

o Exemple des nanotechnologies qui se trouvent très concentrées du

point de vue géographique

DEUX EXEMPLES DE STRATÉGIES OPPOSÉES

o Mexique (R&D/PIB = 0.34) : localisation de segments productifs

intensifs en main d’œuvre et en économies d’échelle d’entreprises

américaines (maquila).

o Corée du Sud (R&D/PIB = 2.50) : «remontée de filière» et système

endogène d’apprentissage technologique. (Voir : Miotti L. et F. Sachwald,

"Foreign Direct Investment as a Technology Sourcing Strategy. The Case of Korean

Multinationals", En Robert Lipsey and Jean-Louis Mucchielli (eds), Multinational Firms'

Strategies, Edward Elgar, 2001.)

23

0

2500

5000

7500

10000

12500

15000

17500

20000

22500

25000

19

60

19

62

19

64

19

66

19

68

19

70

19

72

19

74

19

76

19

78

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

Mexique Corée du Sud

CORÉE ET MEXIQUE : PERFORMANCES COMPARÉESPIB PAR HABITANT, U$ CONSTANTS EN PPA

Bas salaires contre intensité en technologie

DEMANDES DE BREVETS AUPRÈS D’EPO (NOMBRE)

-

1,000

2,000

3,000

4,000

5,000

6,000

19

78

19

79

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

Mexique Corée du Sud Taiwan

Argentine, Mexique, Brésil, Espagne, France et Suisse

UNE ANALYSE MICROÉCONOMIQUE

COMPARATIVE DE 6 PAYS

STATISTIQUES DESCRIPTIVES

Variables Argentine Mexique Brésil Espagne Suisse France

Surveyed period 1998-2001 1999-2000 1998-2000 2002-2004 1998-2001 1998-2000

Observations 1 308 1 515 6 840 3 559 925 4 618

Internal R&D engagement 29.1% 18.1% 30.5% 64.7% 54.7% 44.7%

Innovator 63.3% 34.4% 68.6% 75.3% 79.4% 54.3%

Product innovator 51.8% 27.3% 33.8% 59.4% 72.1% 47.3%

Process innovator 53.7% 23.8% 48.5% 58.8% 59.4% 32.9%

Exporter 57.3% 57.2% 46.5% 80.9% 78.8% 84.1%

Exports share 12.4% 16.4% 8.7% 25.2% 36.9% 22.8%

Public funding 2.0% 1.3% 8.6% 24.6% 5.3% 17.7%

Cooperating with national partner 9.9% 6.7% 10.1% 29.6% 3.8% 22.5%

Cooperating with international partner 8.2% 4.8% 5.1% 13.8% 13.9% 17.6%

R&D ENGAGEMENT AND EXPORTS(SHARE IN TOTAL SAMPLE)

29.1%

18.1%

30.5%

64.7%

54.7%

44.7%

57.3% 57.2%

46.5%

80.9%78.8%

84.1%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Argentina Mexico Brazil Spain Switzerland France

Internal R&D engagement

Exporter

R&D ENGAGEMENT AND EXPORTS SHARE

29.1%

18.1%

30.5%

64.7%

54.7%

44.7%

12.4%

16.4%

8.7%

25.2%

36.9%

22.8%

0%

10%

20%

30%

40%

50%

60%

70%

Argentina Mexico Brazil Spain Switzerland France

Internal R&D engagement

Exports share

COOPERATION EN R&D / INNOVATION

9.9%

6.7%

10.1%

29.6%

3.8%

22.5%

8.2%

4.8% 5.1%

13.8% 13.9%

17.6%

0%

5%

10%

15%

20%

25%

30%

35%

Argentine Mexique Brésil Espagne Suisse France

Coopération avecpartenaires nationaux

Coopération avecpartenaires étrangers

LA CAPACITÉ DES SNI A CRÉER DES RÉSEAUX

0%

3%

6%

9%

12%

15%

18%

21%

0% 5% 10% 15% 20% 25% 30%

Co

op

éra

tio

n a

ve

c d

es

pa

rte

na

ire

s

étr

an

ge

rs

Coopération avec des partenaires nationaux

France

Espagne

Suisse

Argentine

BrésilMexique

SNI avec faible développement de la coopération pour l’innovation

La taille des bulles représente la part d’entreprises qui s’engagent dans des activités de R&D

LES RÉSULTATS

o We find evidences revealing structural differences between regions,

but also presence of heterogeneity within regions. In particular,

firms tend to face innovation activities to achieve a better economic

performance in similar terms along regions, but their interaction

with national systems and environments is weaker in

developing countries. A heterogeneous effect of MNEs is found

regarding innovativity whereas it induces better productivity in

every country.

« Innovation, productivité et exportation : une comparaison entre pays européens et latino-

américains » Fernando Freitas, Stéphane Lhuillery, João Alberto De Negri, Luis Miotti,

Julio Raffo. (Avril 2011)

« Innovativity in Northern and Southern countries: A comparison across European and

Latin-American countries ». LHUILLERY, Stéphane (EPFL); MIOTTI, Luis (MESR,CEPN)

and RAFFO, Julio (EPFL, CEPN) (2008)

LES RÉSULTATS (CONT.)

o A main conclusion is that there are difficulties for firms in developing countries to buildworking innovative systems where information and knowledge help them to invest intoR&D. A particular difficulty seems to be the link between academic research and industrywhereas some dynamics seems to occur in Brazil. Our results suggest that the lack ofR&D networking and especially interactions with academics may be a problem forinnovativity in these countries.

o It may however encounter some counterbalancing effects: a first one is the role of foreignMNEs being that a positive impact is found for innovativity in Brazil.

o Our results suggest that the bottleneck for developing countries seems to be theinnovativity stage considering that the productivity stage is found capable in the developingcountries to transform technological innovation into productivity and even exports. Ofcourse, investments and education are found important factors for performances. But still,our paper provides evidences that intermediate countries such as Argentina, Brazil andMexico are responsive to technological innovations.

o Last, public support stimulates developing country firms into engaging in innovativeactivities but the limited extent of policies – as in the cases of Argentina and Mexico –seems to prevent it from having an effect on the innovative intensity. Both results suggestthat there is still plenty of scope for policies stimulating firms’ innovative behavior and itsinteraction with the academic sector.

ET L’ÉDUCATION ?

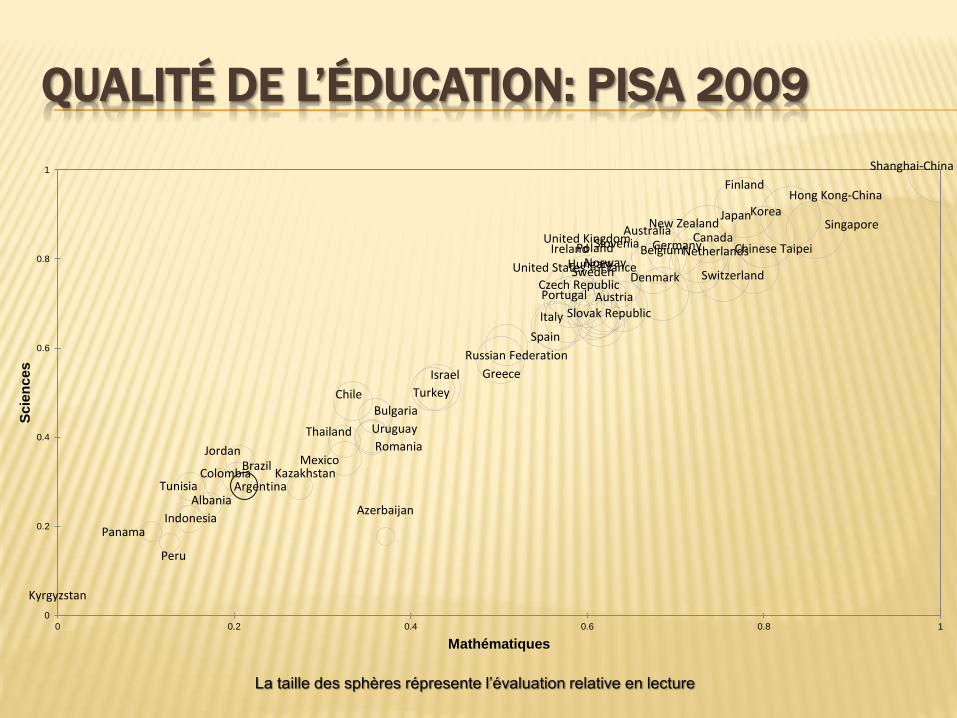

QUALITÉ DE L’ÉDUCATION: PISA 2009

Shanghai-China

Korea

FinlandHong Kong-China

SingaporeCanada

New ZealandJapan

Australia

NetherlandsBelgiumNorway

Switzerland

Poland

United StatesSweden

GermanyIreland

France

Chinese Taipei

Denmark

United Kingdom

Hungary

Portugal

Italy

Slovenia

Greece

Spain

Czech Republic

Slovak Republic

Israel

Austria

Turkey

Russian Federation

ChileBulgaria

Uruguay

MexicoRomania

Thailand

ColombiaBrazil

Jordan

Tunisia

Indonesia

ArgentinaKazakhstan

Albania

Panama

Peru

Azerbaijan

Kyrgyzstan

0

0.2

0.4

0.6

0.8

1

0 0.2 0.4 0.6 0.8 1

Sc

ien

ce

s

Mathématiques

La taille des sphères répresente l’évaluation relative en lecture

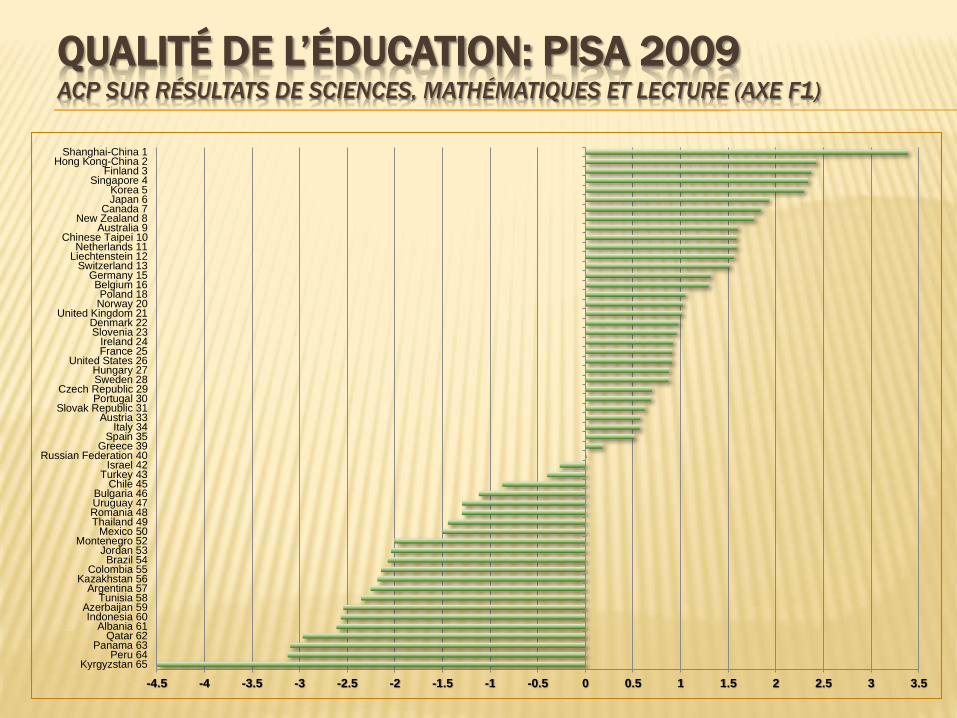

QUALITÉ DE L’ÉDUCATION: PISA 2009ACP SUR RÉSULTATS DE SCIENCES, MATHÉMATIQUES ET LECTURE (AXE F1)

-4.5 -4 -3.5 -3 -2.5 -2 -1.5 -1 -0.5 0 0.5 1 1.5 2 2.5 3 3.5

Kyrgyzstan 65Peru 64

Panama 63Qatar 62

Albania 61Indonesia 60

Azerbaijan 59Tunisia 58

Argentina 57Kazakhstan 56

Colombia 55Brazil 54

Jordan 53Montenegro 52

Mexico 50Thailand 49Romania 48Uruguay 47Bulgaria 46

Chile 45Turkey 43

Israel 42Russian Federation 40

Greece 39Spain 35

Italy 34Austria 33

Slovak Republic 31Portugal 30

Czech Republic 29Sweden 28Hungary 27

United States 26France 25Ireland 24

Slovenia 23Denmark 22

United Kingdom 21Norway 20Poland 18

Belgium 16Germany 15

Switzerland 13Liechtenstein 12Netherlands 11

Chinese Taipei 10Australia 9

New Zealand 8Canada 7

Japan 6Korea 5

Singapore 4Finland 3

Hong Kong-China 2Shanghai-China 1

CONCLUSION

CONCLUSION

o Maitrise de la rente, stabilité macroéconomique et bonne gouvernance sont

clé pour la mise en place des politiques structurelles.

o Et si l’unique politique industrielle possible était une politique structurelle

fondée sur l’éducation à tout niveaux?