welcome to asia pacific - aon benfieldthoughtleadership.aonbenfield.com/documents/201503...welcome...

TRANSCRIPT

1Risk. Reinsurance. Human Resources.

Aon Benfield

Welcome to Asia PacificA journey through the region’s insurance and reinsurance markets

2 3

The Asia Pacific region is home to more than half the world’s population, with diverse societies, cultures, economies and regulatory regimes. As rapid economic development, population growth and urbanisation lead to increased insurance penetration, Asia Pacific represents a key area of growth in the global marketplace.

In fact, in Aon Benfield’s 2015 Insurance Risk Study, three Asian markets make the top 3 of the Country Opportunity Index (COI), which identifies the world’s most promising property and casualty markets. They were chosen by analysts owing to their profitability, growth potential and relatively stable political environments. Indonesia, Malaysia, and Singapore tied this year for the number one position in the list of 50 countries. They were also the top quartile performer in both 2013 and 2014.

With many insurance and reinsurance companies already investing in this region and seeking to take advantage of the growth opportunities, an expert insight into these markets is crucial. Aon Benfield’s local teams have produced this guide as both an introduction to and exploration of sixteen key markets in Asia Pacific.

Data has been collated from major rating agencies, industry associations and regulatory bodies, IMF, World Bank, AXCO, Aon Risk Solutions, Aon Hewitt, and Aon Benfield. In addition, we have included our own views of each market’s major risks, regulatory & market updates, and market outlook.

With a global fact base and broad access to local market practitioners, Aon Benfield is equipped to provide insight across a spectrum of lines, products, and geographies. Inpoint, the consulting division of Aon Benfield, helps insurers and reinsurers address these challenges, from sizing market opportunities to identifying distribution channel dynamics, assessing competitor behaviour, and understanding what it takes to compete and win. Our approach leverages Aon Benfield’s 130mn USD annual investment in analytics, data and modelling to help our clients grow profitably.

Combined with Aon Benfield’s expertise and commitment to the region, we hope the guide will boost your understanding of the region and the available growth opportunities.

Wherever available, or unless otherwise stated, premiums include numbers for non-life and personal accident & healthcare business written by non-life companies.

Wherever Incurred Losses were not available, Loss Ratio was calculated on the basis of Paid Losses.

Demographics refer to 2015 estimates.

2014 GDP for Guam was not available, hence, excluded from the APAC insurance penetration calculation.

To calculate Y/Y Growth, restated numbers from prior year are used, wherever available.

The premiums information put together ranges from gross to direct and net basis; depending upon whatever was best available for each of the countries.

Australia

Pakistan

Malaysia

Thailand

Singapore

Indonesia

Brunei

Philippines

New Zealand

China

Hong Kong

Korea (Republic of)

Taiwan

Vietnam

Japan

India

Introduction Markets Topics

• Demographics

• Political & Terror Risk

• Sovereign Rating and Outlook

• Major Risks

• Top 5 Insurers

• Non-life Insurance Penetration Rate

• Industry Premiums Split by Line of Business

• Industry Aggregate Premium and Trends

• Capital Requirements

• Regulatory Updates

• Foreign Ownership

• Aon Benfield Outlook

4 5

AustraliaGold Coast

6 7

20,000

25,000

30,000

35,000

40,000

2010 2011 2012 2013 2014

Total Premiums AUD million Total Premiums USD million

Entity

GEP

USD mn

GEP

AUD mn

Inc claims

AUD mn

UW result

AUD mn

QBE Insurance Group Ltd. 16,606.9 18,423.7 11,515.6 609.5

Insurance Australia

Group Ltd. 8,762.1 9,720.6 6,791.8 1,139.6

Suncorp Insurance

Holdings Ltd. 7,919.7 8,786.1 6,600.9 665.7

Allianz Australia Ltd. 3,533.4 3,920.0 3,090.6 -8.5

Zurich Financial Services

Australia Ltd. 1,140.0 1,264.7 905.8 -115.9

Australia

Capital Requirements

Minimum capital requirement of 5mn AUD is effective from 1 July 2002. Prudential Standards GPS 110 specifies that a regulated institution must ensure that it has a capital base, at all times, in excess of its Prudential Capital Requirement (PCR) which is intended to take account of the full range of risks to which a regulated institution is exposed, including insurance risk, insurance concentration risk, asset risk, asset concentration risk, and operational risk.

Foreign Ownership

There are no material restrictions on foreign ownership. Subject to regulatory approval, foreign companies may acquire any percentage of a domestic company’s equity or may establish wholly owned subsidiaries or branches.

Foreign investments in Australia above a certain size must be approved by the Foreign Investment Review Board (FIRB).

For investors from the US, Chile, Japan, Korea and New Zealand, they need approval from FIRB for acquiring a domestic company with assets in excess of 1.09bn AUD. For investors from other countries, the approval limit is 252mn AUD.

Regulatory Updates

Australian Prudential Regulation Authority (APRA) released a package that harmonizes and enhances its current risk management requirements. The package includes the final cross-industry Prudential Standard CPS 220 Risk Management, a proposed prudential practice guide on risk management, and a response paper that addresses submissions received by APRA on the CPS 220 consultation package released in May 2013. APRA also released an amended Prudential Standard CPA 510 Governance (CPS 510) to ensure that governance requirements related to risk management was aligned with those of CPS 220. The new Prudential Standard CPS 220 Risk Management (CPS 220) and amended Prudential Standard CPS 510 Governance (CPS 510) have been in effect since 1 January 2015.

Major Risks

Underwriting Risk

Given the consolidation of the insurance market in Australia, and a highly competitive environment, most insurers are heavily focused on underwriting and risk selection. Increasingly the market is utilising external data sources to help refine underwriting decisions, with many companies exploring the use of Big Data analytics in their processes.

Regulatory Risk

Since LAGIC was introduced in 2013, the Australian market has quickly adapted to the horizontal as well as vertical requirement of the solvency standard, resulting in the Australian market developing an equitable working relationship with the regulation as it currently stands. In 2016 however, the Reserve Bank of New Zealand will have fully implemented its solvency regime, requiring (at an upper level) a 1 in 1000 year capitalisation for earthquake risk in Wellington. The ramifications of this requirement are already being seen, with some Trans Tasman insurers already setting reinsurance needs based on their New Zealand exposure.

Top 5 Insurers

Industry Premiums Split by Lines of Business

Industry Aggregate Premium 2010 to 2014

Credit Rating and Outlook

Rating Outlook

S&P AAA Stable

Fitch AAA Stable

Moody's Aaa Stable

AM Best CRT-1

Aon Benfield Outlook

Growth in the insurance market is relatively stable and broadly in line with natural inflation. With regards to reinsurance, catastrophe limits are increasing at a low single digit rate each year. Following the 2010/11 events, the market moved away from proportional business, however as reinsurers are searching for growth, there is an increased appetite to move back into proportional solutions.

Reducing premium rates are putting margins under pressure and forcing firms to have a clear focus on expense management going forward. For insurers, the biggest challenge is the static market and the pressure to grow. Exacerbating this pressure, over recent years various international underwriters have entered the Australian market, utilising global balance sheets to make the market even more competitive. These forces have forced many insurers to revisit and (re)define their value proposition and their “reason for being”.

The biggest challenge for reinsurers in Australia is to try and remain relevant to the well capitalised main reinsurance purchasers, as well as keeping their diversifying exposures in Australia aligned to the capacity they are deploying in the peak zone globally. Over recent years, the more successful of these have viewed their insurance clients on a holistic basis, viewing capital needs of their clients in totality rather than trying to underwrite selective placements.

Political Risk

Terror Risk

World Bank relative ease of doing business

GDP – PPP (USD bn)

1,136.9

GDP Per Capita – PPP (USD)

47,318

Population (mn)

24.0

5yr Real GDP Growth (%)

4.4

Unemployment Rate (%)

6.3

Inflation Rate (%)

1.8

Ranking based on Gross Earned Premiums, includes domestic and overseas Non-Life + PA & Healthcare premiums

*Growth % is based on premiums in local currency Break-up by line of business reflects written premiums within this market sector

Lines of

business USD mn AUD mn

Inc claims

AUD mn

Loss

ratio %

Comb

ratio %

*Y/Y

growth %

Property 10,156.3 11,267.0 5,613.0 47.4 68.8 -0.2

Motor 12,235.0 13,573.0 10,388.0 77.1 94.1 1.9

Workers Comp 1,486.4 1,649.0 1,614.0 97.3 112.4 -6.1

Liability 3,411.0 3,784.0 2,561.0 68.2 90.4 2.0

Miscellaneous 4,943.4 5,484.0 2,018.0 39.3 63.7 4.5

Industry-wide

Non-Life 32,232.0 35,757.0 22,194.0 61.9 81.9 1.2

2014 DWPLow High

Easiest Hardest

Data Source: IMF, AXCO, SNL, S&P, Fitch, Moody’s, A.M. Best, Australian Prudential Regulatory Authority, Aon, and Aon Benfield.

2014 GEP

2014 Insurance Penetration - Non-life and PA & Healthcare GWP vs. GDP

Australia Prem: GDP = 2.2%; APAC Prem: GDP = 1.5%

(2015 est.)

8 9

BruneiSultan Omar Ali Saifuddin Mosque in Bandar Seri Begawan

10 11

Brunei

Major Risks

Litigation Risk

The Legal Profession (Contingency Fee) Act 1994 has incentivised law firms to encourage clients to go to court to seek compensation for motor vehicle or occupational injury accidents. A contentious motor liability case is more likely to go to court in Brunei than in any other country in South-East Asia, many of which at grossly inflated compensation demands.

Credit Rating and Outlook

Rating Outlook

S&P NA —

Fitch NA —

Moody's NA —

AM Best CRT-4

Capital Requirements

The Insurance Order 2006 and Insurance Regulations 2006 require life and non-life insurers to keep the minimum paid-up capital of 8mn BND with a minimum deposit set at 1mn BND to be maintained with Monetary Authority of Brunei Darussalem. The capital requirements for Takaful operators are the same. Insurers established or incorporated outside Brunei who do not have local share capital are required to maintain in Brunei a surplus of assets over liabilities of an amount not less than the requirement for the minimum paid-up capital of an insurer incorporated in Brunei.

Foreign Ownership

Foreign ownership is not restricted or discriminated against under The Insurance Order 2006 and Insurance Regulations 2006.

Incorporated foreign companies wishing to establish a place of business in Brunei are required to register under Section 299 of the Companies Act.

Regulatory Updates

The new General Insurance and Takaful Agent Handbook (GAH) was introduced by the Monetary Authority of Brunei Darussalam (MABD) and Brunei Insurance and Takaful Association (BITA) with effect from 1 July 2014. A period of grace of six months was given to agents to implement the new guidelines, which have been in effect from 1 January 2015.

Industry Aggregate Premium 2009 to 2013

Aon Benfield Outlook

The potential for any significant growth in Brunei remains low due to a small economy, a heavy dependency on finite oil and gas reserves, and a small number of insurers in the market. In addition, the Monetary Authority of Brunei Darussalam (AMDB) has introduced new loan requirements including a loan cap aimed at reducing the debt burden among Bruneians. Motor is the main class of business but the outlook in the personal lines sector remains limited. Apart from the compulsory purchase of motor insurance, there is no culture of buying insurance in Brunei.

Demand is driven by bank lending requirements and culture of state welfare and religious concerns have affected the development of the industry. The contingency fee act remains to be an issue which has increased the number of motor third party bodily injury claims going to court, many of which are grossly inflated.

30

40

50

60

70

80

2009 2010 2011 2012 2013

Total Premiums BND million Total Premiums USD million

GDP – PPP (USD bn)

32.9

GDP Per Capita – PPP (USD)

78,475.6

Population (mn)

0.4

5yr Real GDP Growth (%)

1.4

Unemployment Rate (%)

2.7

Inflation Rate (%)

0.0

Entity USD mn BDN mn

Market share

%

National Insurance Co. BHD 20.3 25.5 35.0

Audley Insurance Co. SDN BHD 15.1 18.9 26.0

Standard Insurance SDN BHD 8.9 11.2 15.4

Tokio Marine Insurance

Singapore Ltd. 6.1 7.6 10.5

MBA Insurance Co. SDN BHD 4.4 5.5 7.6

Top 5 Insurers

Industry Premiums Split by Lines of Business

*Growth % is based on premiums in local currency Excludes PA & Healthcare premiums Statistics refer to conventional non-life business and do not include the Takaful business or companies 2014 statistics were not published by the regulator when preparing this report Break-up by line of business reflects written premiums within this market sector

Lines of

business USD mn BND mn

Paid

claims

BND mn

Loss

ratio

%

Comb

ratio

%

*Y/Y

growth

%

Property 9.5 11.9 7.7 64.9 105.7 -0.1

Construction

& Engineering 2.4 3.0 0.1 3.2 8.5 1234.5

Motor 11.2 14.1 4.2 29.5 48.4 15.4

Workers Comp 8.9 11.1 2.8 24.8 65.5 15.3

Liability 6.0 7.6 0.5 7.2 14.5 157.8

Surety, bonds

& credit 0.3 0.4 -0.0 -7.3 3.6 -9.4

Miscellaneous 14.0 17.6 1.0 5.8 16.6 -12.3

MAT 5.7 7.1 0.9 12.6 21.1 -15.9

Industry-wide

Non-Life 58.1 72.7 17.1 23.6 44.6 10.5

2013 GWP

2013 GWP

Political Risk

Terror Risk

World Bank relative ease of doing business

Low High

Easiest Hardest

Data Source: IMF, AXCO, SNL, S&P, Fitch, Moody’s, A.M. Best, the General Insurance Association of Brunei Darussalam, Aon, and Aon Benfield.

2013 Insurance Penetration - Non-life and PA & Healthcare (excl. Takaful) GWP vs. GDP

Brunei Prem: GDP = 0.4%; APAC Prem: GDP = 1.5%

Excludes PA & Healthcare Premiums Statistics refer to conventional non-life business and do not include the Takaful business or companies 2014 statistics were not published by the regulator when preparing this report Ranking based on total premiums written by an insurer within this market sector

(2015 est.)

12 13

ChinaThe Great Wall of China

14 15

Top 5 Insurers

Entity USD mn CNY mn

Market

share %

Loss

ratio %

Comb

ratio %

PICC Property & Casualty

Co. Ltd. 41,087.6 252,419.2 33.5 64.5 95.6

Ping An Property & Casualty

Insurance Co. Ltd. 23,253.7 142,857.3 18.9 57.6 90.6

China Pacific Property

Insurance Co. Ltd. 15,111.6 92,837.3 12.3 68.1 101.2

China Life Property & Casualty

Ins. Co. Ltd. 6,575.7 40,397.4 5.4 61.6 97.3

China United Property

Insurance Co. Ltd. 5,675.2 34,865.2 4.6 61.6 94.0

2014 GWP

Industry Premiums Split by Lines of Business

Lines of

business USD mn CNY mn

Paid claims

CNY mn

Loss

ratio %

*Y/Y

growth %

Property 11,629.6 72,054.0 42,367.4 58.8 15.5

Construction

& Engineering 1,264.0 7,831.6 3,123.6 39.9 24.5

Motor 76,294.6 472,702.8 272,080.4 57.6 17.9

Liability 3,470.5 21,502.1 8,914.8 41.5 18.9

Surety, bonds

& credit 4,384.4 27,164.8 8,515.6 31.4 8.6

Miscellaneous 200.5 1,242.0 817.9 65.9 11.0

MAT 3,106.1 19,244.7 8,872.4 46.1 1.0

Industry-wide

Non-Life 100,349.6 621,742.0 344,692.0 55.4 16.7

PA & Health 4,257.4 26,378.0 11,758.5 44.6 31.5

Grand Total 104,607.1 648,120.0 356,450.5 55.0 17.2

2013 GWP

*Growth % is based on premiums in local currencyBreak-up by line of business reflects premiums written within this market sector 2014 statistics were not published by the regulator when preparing this report

China

Credit Rating and Outlook

Rating Outlook

S&P AA- Stable

Fitch A+ Stable

Moody's Aa3 Stable

AM Best CRT-3

Capital Requirements

Minimum capital required is 200mn CNY and 20mn CNY increment for each new provincial branch, with total capital capped at 500mn CNY. Insurers should keep solvency ratio (actual capital divided by minimum capital) no lower than 100%. Actual capital is insurer’s admitted assets minus admitted liabilities. Minimum capital is the greater of 18% premium last year up to 100mn CNY plus 16% premium last year excess of 100mn CNY (no ceded reinsurance and business tax), or 26% average incurred claims last 3 year up to 70mn CNY plus 23% average incurred claims last 3 year excess of 70mn CNY (no reinsurance recoveries).

Foreign Ownership

If 25% or more of a Chinese insurance company’s shares are held by foreign entities, the firm is considered foreign funded and regulated by the Regulations on the Administration of Foreign-Invested Insurance Companies. Otherwise it is deemed to be domestic. To be eligible for a branch, joint venture, or subsidiary license, foreign insurers must has been in business for over 30 years, set representative office in mainland China for at least 2 years, and has total assets of at least 5bn USD.

Regulatory Updates

China Insurance Regulatory Commission (CIRC) published the final version of China Risk Oriented Solvency System (C-ROSS) in February 2015. The industry is in the transition toward C-ROSS with the formal implementation expected to be in 2016. For non-life insurers, the average solvency ratio under C-ROSS was 282.0% for 1Q 2015 and 286.3% for 2Q 2015.

In March 2015, CIRC formally issued the Notice on Implementing Reinsurance Registration System. Beginning 1 January 2016, all reinsurers (including primary insurers writing inward business) and reinsurance brokers must register on the platform built and maintained by CIRC. Cedants must select reinsurance counterparties from those valid in the registration system. Treaty reinsurers must have secure rating (“A-“ or above for leaders and “BBB” or above for followers). Certain exemptions may apply. In April 2015, China’s Residential EQ Pool was established in Beijing. In June 2015, motor de-tariff began in six provinces/cities. In August 2015, CIRC kicked off the pilot residential earthquake scheme in Da’li prefecture of Yunnan province. In October 2015, the State Council proposed to amend the Insurance Law. The current clause that “a P&C insurer’s net premium cannot exceed 4X its capital” will be removed.

Industry Aggregate Premium 2010 to 2014

Aon Benfield Outlook

The China insurance and reinsurance market potential remains high given low insurance penetration, continued economy growth, and clearly stated government desire for market growth and product diversity. Significant growth has been achieved in recent years in non-life sector such as Agriculture, Liability, and Credit – mostly due to government incentives and guidance. Personal lines continue to be untapped, except Motor. CIRC recently launched a liberalization of motor tariff for selected regions in China, aiming to expand nationwide shortly. Immediate impacts on the market have mainly been centered on reduced written premium with stable loss ratios. As motor contributes more than 70% GWP, the industry will continue to monitor developments closely. Specialty lines performed better than Property and Engineering which continues to be very competitive. The impact of C-ROSS to date has been limited to specific cedants and placements. However, C-ROSS marks a significant change in how regulatory capital is quantified in China and may result in significant changes in the local market in the future. Discussions regarding the upcoming January 1 renewals have centered around the impact of CROSS on signings for offshore reinsurers and the impact of the Tianjin Port Explosion on renewal terms and conditions. Early expectations are for onshore reinsurers to continue enjoying more favourable signings on placements. This trend will likely be accelerated due to the rapid increase in the number of Llyod’s Syndicates writing business via the Chinese Platform. Aon Benfield remains confident however that offshore reinsurers will still play an important role in the market. In the absence of clarity on loss positions for 2015, predictions on renewal conditions remain subject to significant uncertainty. Early expectations are for a moderate impact on renewal terms for the market given favourable loss activity in recent years and the continued strong interest in China from a strategic long term perspective. Corrections on the worst affected programs may be more significant however.

Major Risks

Catastrophe Risk

China is one of the most exposed countries to natural catastrophe perils. Earthquake risk of insurers portfolio is mainly driven by growing exposures in and around the capital of Beijing. Tropical Cyclone exposures are driven by accumulations along the Eastern Coast from Shanghai to Guangdong, which are the manufacturing and trading centers of China. Catastrophe risk continues to be a focus of the Regulator and Industry. Catastrophe risk insurance is still in an embryonic stage. Pilot catastrophe schemes have been launched in Shenzhen, Yunnan and Ningbo, Zhejiang province.

However, at the country level, catastrophe insurance for residential risk is still not in place. Data and modelling continue to improve for these two major perils.

Regulatory Risk

Regulators have introduced many new regulations. The most important ones are China Risk Oriented System (C-ROSS), motor de-tariff pilot programs in six regions, the Agriculture Reinsurance Pool, the Reinsurance Registration System, and amendment of the China Insurance Law. These new regulations may have many implications, e.g. changing the cedant’s retention level, increasing demand of non-proportional reinsurance, pushing reinsurers to get (better) international rating, etc.

Financial Risk

GDP growth rate is slowing down in light of the government’s intention to bring structural changes to the economy. Reform of the financial sector, particularly regulating the “shadow banks”, is increasingly attracting more attention and debate.

40,000

60,000

80,000

100,000

120,000

140,000

350,000

450,000

550,000

650,000

750,000

850,000

2010 2011 2012 2013 2014

Total Premiums CNY million Total Premiums USD million

GDP – PPP (USD bn)

19,510.0

GDP Per Capita – PPP (USD)

14,189.50

Population (mn)

1,375.0

5yr Real GDP Growth (%)

9.6

Unemployment Rate (%)

4.1

Inflation Rate (%)

1.5

Political Risk

Terror Risk

World Bank relative ease of doing business

Low High

Easiest Hardest

Data Source: IMF, SNL, S&P, Fitch, Moody’s, A.M. Best, China Insurance Regulatory Comission, Aon, and Aon Benfield.

2014 Insurance Penetration - Non-life and PA & Healthcare GWP vs. GDP

China Prem: GDP = 1.2%; APAC Prem: GDP = 1.5%

Includes Non-Life + PA & Healthcare premiums Ranking based on total premiums written by an insurer within this market sector

(2015 est.)

16 17

Hong KongSkyline of Hong Kong

18 19

Top 5 Insurers

Entity

USD

mn

HKD

mn

Market

share %

Net

claims

incurred

Underwriting

profit / (Loss)

*Y/Y

growth

%

AXA General 470.8 3,650.9 8.4 1,840.46 187.32 4.3

Zurich Insurance 342.7 2,657.0 6.1 603.75 71.21 1.6

Bupa 303.3 2,351.7 5.4 1,390.86 92.65 12.3

China Taiping (HK) 263.6 2,043.6 4.7 779.30 46.92 14.7

BOC Group Ins. 237.6 1,842.6 4.2 1,041.23 63.46 3.3

2014 GWP

Industry Premiums Split by Lines of Business

Lines of

business USD mn HKD mn

Inc. claims

HKD mn

Loss

ratio %

**Comb

ratio %

*Y/Y

growth %

Motor 624.5 4,842.1 2,296.4 58.0 90.9 6.5

Aircraft 2.1 16.1 8.5 119.7 132.8 -27.1

Ships 260.6 2,020.5 835.7 64.7 82.6 7.7

Goods in Transit 221.9 1,720.5 378.3 43.2 59.4 23.9

Property 1,155.5 8,959.9 1,168.6 29.9 49.0 -0.2

General Liability 1,429.2 11,082.4 5,271.1 62.0 86.7 0.7

Pecuniary Loss 369.2 2,862.9 354.5 24.7 48.2 13.9

Non-Prop Treaty 26.2 202.8 91.8 47.8 58.3 12.1

Prop Treaty 51.6 400.3 190.0 50.5 86.8 -4.4

Industry-Wide

Non-Life 4,140.7 32,107.5 10,594.9 51.6 75.0 3.8

PA & Health 1,487.5 11,534.0 6,090.6 67.5 87.9 6.2

Grand Total 5,628.2 43,641.5 16,685.5 56.4 79.0 4.4

2014 GWP

*Growth % is based on premiums in local currency **Expense ratio computation includes “Net Commissions Payable/Receivable” & “Management Expenses” Break-up by line of business reflects total written premiums (domestic + overseas)

Hong Kong

Capital Requirements

Minimum paid-up capital requirements are 10mn HKD for a non-life company, 20mn HKD for a non-life company writing the statutory class of business, 20mn HKD for a compositive, and 2mn HKD for a captive. Insurance companies must submit a three or five-year plan when they apply for authorisation. The applicant and the regulator agree how much capital they will need based on the business plan. This is normally much higher than the statutory minimum.

An insurer shall maintain an excess of assets over liabilities of not less than a required solvency margin which is the greater of 1/5 of the relevant premium income up to 200mn HKD plus 1/10 of the amount by which the relevant premium income exceeds 200mn HKD, or 1/5 of the relevant claims outstanding up to 200mn HKD, plus 1/10 of the amount by which the relevant claims outstanding exceeds 200mn HKD, subject to the minimum paid-up capital requirements.

Foreign Ownership

There are no restrictions on foreign ownership. Foreign companies may acquire any percentage of the shares in an existing insurance company or establish branches or locally incorporated subsidiaries.

Any person who intends to acquire control of 15% or more of the voting power of a locally incorporated insurer must seek the regulator’s approval before making the acquisition.

Regulatory Updates

The Insurance Authority (IA) conducted a three-month consultation exercise from September to December 2014 to solicit views on the proposed Risk-based Capital (RBC) framework for Hong Kong. In September 2015, IA issued the consultation conclusions. There is general support from the insurance industry for the move towards a risk-sensitive capital framework and the enhancement of risk management. There is general agreement on the high level principles of the conceptual framework, although there are mixed views on some of the technical aspects. IA decided to proceed to the next phase which involves developing the detailed rules and carrying out the QIS. After that, another consultation exercise will be conducted.

Major Risks

Catastrophe Risk

Hong Kong is generally considered as low catastrophe-prone region with no proximity to earthquake fault line. Despite the frequent visit of typhoon, Hong Kong is saved from major losses as a result of strict regulations on building code. Owing to much increase in property value (insured value) as well as the extreme high concentration of risks, we can never underestimate potential major losses arising from those “un-modelled” perils such as landslide, terrorism and other man-made hazards. Insurance coverage for catastrophe perils in Hong Kong is almost free for the time being, something, that needs immediate attention.

Underwriting Risk

There is fierce competition among insurers on all lines particularly for those premium-rich classes such as EC/EL and Motor and unfortunately, there is no sign of possible rebound in the near future.

Market Risk

Hong Kong by all means is closely adhering to the Chinese economy in various arenas – investment, tourism, import/export, etc. Slowing down of the Chinese economy is to drive weaker demand on insurance particular for SME sector and therefore profound impact onto Hong Kong insurance industry.

Industry Aggregate Premium 2010 to 2014

Credit Rating and Outlook

Rating Outlook

S&P AAA Stable

Fitch AA+ Stable

Moody's Aa1 Stable

AM Best CRT-2

Aon Benfield Outlook

Hong Kong insurance industry will also embrace the implementation of Risk-Based Capital regulatory framework in a matter of few years’ time. And insurers would have to prepare for the potential impact arising hereunder: 1) potentially to trigger a wave of consolidation and to drive smaller carriers out of business; 2) more holistic/stringent approach on risk management and capital requirement by direct insurers and reinsurers operating in Hong Kong; 3) Additional burden onto insurers in regard to the compliance of myriad of risks – underwriting risk, credit risk, market risk, operational risk, liquidity risk, counter-party risk plus other non-quantifiable risks.

Voluntary Health Insurance Scheme (VHIS): Hong Kong Government is proposing an alternative to those who are able and willing to use private healthcare services through the collaboration with local insurance industry by providing insurance to general public, with potential key challenges to medical insurance carriers including: 1) Guaranteed renewal for life; 2) Covering pre-existing conditions subject to a waiting period; 3) Accepting high-risk groups through a high-risk pool; 4) Standardization of policy terms/conditions. Medical insurance is an important sector in the Hong Kong insurance industry – for 2014, it captured 20.4% of overall premium income to the non-life market. Yet operating margin was under severe pressure due to escalating insurance payment and ended up being 4%. Challenges emanating from VHIS are to pose major uncertainty onto Hong Kong medical insurance carriers.

GDP – PPP (USD bn)

414.5

GDP Per Capita – PPP (USD)

56,689.1

Population (mn)

7.3

5yr Real GDP Growth (%)

4.6

Unemployment Rate (%)

3.2

Inflation Rate (%)

2.9

Political Risk

Terror Risk

World Bank relative ease of doing business

Low High

Easiest Hardest

Data Source: IMF, SNL, S&P, Fitch, Moody’s, A.M. Best, Office of the Comissioner of Insurance, Aon, and Aon Benfield.

3,500

4,500

5,500

6,500

30,000

35,000

40,000

45,000

2010 2011 2012 2013 2014

Total Premiums HKD million Total Premiums USD million

2014 Insurance Penetration - Non-life and PA & Healthcare GWP vs. GDP

Hong Kong Prem: GDP = 1.9%; APAC Prem: GDP = 1.5%

*Growth % is based on premiums in local currencyIncludes Non-life + PA & Healthcare premiumsRanking based on total premiums written by an insurer (domestic + overseas)

(2015 est.)

20 21

IndiaTaj Mahal in Agra, Uttar Pradesh

22 23

India

Capital Requirements

Minimum capital for direct insurance companies (life and non-life) of 1bn INR and 2bn INR for professional reinsurers.

The “Required Solvency Margin” (RSM) shall be the maximum of the following amounts:

a) 500mn INR for direct non-life insurers, (1bn INR for reinsurers), or b) a sum equivalent to 20% of net premium income, or c) a sum equivalent to 30% of net incurred claims.

Foreign Ownership

In March 2015, the Indian Parliament passed the Insurance Laws (Amendment) Bill raising the ceiling for foreign investment in the insurance sector. The foreign direct investment cap in an Indian insurance company will be increased from 26% to 49% but ownership and “control” of the Indian insurance company will remain with Indian residents.

The Bill amends the definition of ‘foreign company’, which will now include a company or body established under a law of any country outside India, and includes Lloyd’s of London, established under the Lloyd’s Act, 1871, or any of its members. Foreign reinsurers will be permitted to conduct reinsurance business through setting up branch offices in India.

Regulatory Updates

A bill is currently under consideration in Parliament which will impose a cap on motor third party bodily injury damages per person of 1mn INR. The bill has already been approved by the lower house and is currently being debated by the upper house. If ultimately passed into an Act of Parliament, this legislation would have a beneficial effect on the market’s motor third party insurance future loss ratios.

Major Risks

Regulatory Risk

The Indian Insurance market re-opened its doors to privatisation in 1999 and the first set of regulations came into effect in 2001, with Broker Regulations being announced in October 2002.

There were very few changes made to regulations for the next 10 years or so until the new set of regulations were announced by the Insurance Regulatory and Development Authority of India (IRDAI) in December 2013. These regulations were announced after the IRDAI had meetings with Insurance Companies, Brokers, Agents, Loss Adjusters, Third Party Administrators and the General Insurance Corporation of India.

In 2014, the new Government of India introduced an amended Insurance Bill to Parliament to allow 49% Foreign Direct Investment in insurance and also for reinsurers to set up branches in India. After much debate, the government got the Bill passed through an Ordinance in 2015 and the IRDAI is now in the process of finalising new regulations to incorporate into the existing ones. The IRDAI is trying to get these regulations finalised by October 2015 but it may well take them till the end of the calendar year to announce them.

As such, there is little Regulatory Risk involved except that any amendments to Bills have to receive Parliamentary support and that can take time.

Litigation Risk

As a rule, individuals accept an offer of a claim made by an insurer although in the past couple of years, people are getting more aware of their rights. Group Companies generally drives a hard bargain at the time of taking insurance and also is not averse to litigate a claim if they feel that they are not being given a fair deal by their insurer. The process of litigation is a long drawn out one with cases usually taking a minimum of 10 years to get settled.

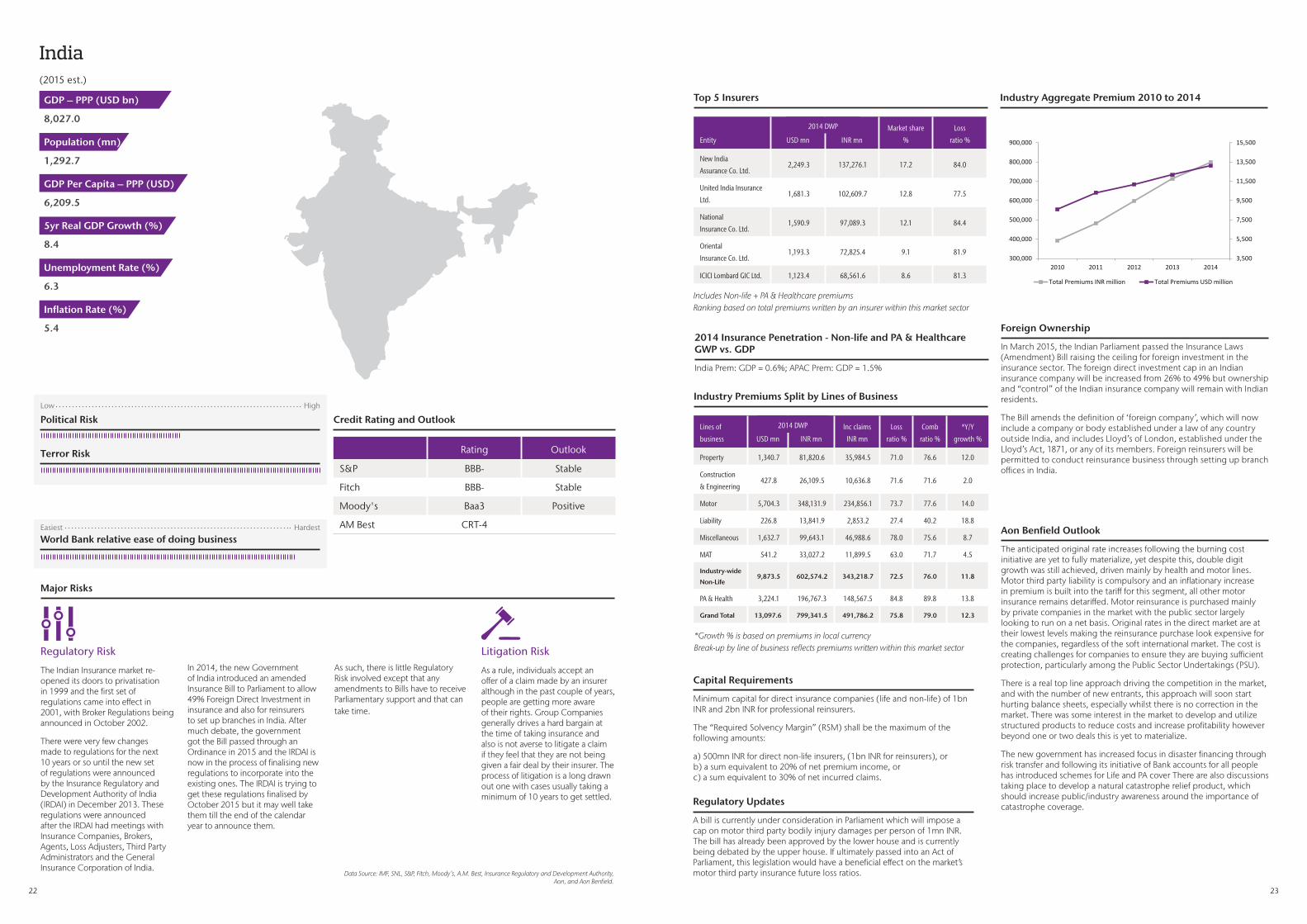

Industry Aggregate Premium 2010 to 2014

Credit Rating and Outlook

Rating Outlook

S&P BBB- Stable

Fitch BBB- Stable

Moody's Baa3 Positive

AM Best CRT-4 Aon Benfield Outlook

The anticipated original rate increases following the burning cost initiative are yet to fully materialize, yet despite this, double digit growth was still achieved, driven mainly by health and motor lines. Motor third party liability is compulsory and an inflationary increase in premium is built into the tariff for this segment, all other motor insurance remains detariffed. Motor reinsurance is purchased mainly by private companies in the market with the public sector largely looking to run on a net basis. Original rates in the direct market are at their lowest levels making the reinsurance purchase look expensive for the companies, regardless of the soft international market. The cost is creating challenges for companies to ensure they are buying sufficient protection, particularly among the Public Sector Undertakings (PSU).

There is a real top line approach driving the competition in the market, and with the number of new entrants, this approach will soon start hurting balance sheets, especially whilst there is no correction in the market. There was some interest in the market to develop and utilize structured products to reduce costs and increase profitability however beyond one or two deals this is yet to materialize.

The new government has increased focus in disaster financing through risk transfer and following its initiative of Bank accounts for all people has introduced schemes for Life and PA cover There are also discussions taking place to develop a natural catastrophe relief product, which should increase public/industry awareness around the importance of catastrophe coverage.

3,500

5,500

7,500

9,500

11,500

13,500

15,500

300,000

400,000

500,000

600,000

700,000

800,000

900,000

2010 2011 2012 2013 2014

Total Premiums INR million Total Premiums USD million

Top 5 Insurers

Entity USD mn INR mn

Market share

%

Loss

ratio %

New India

Assurance Co. Ltd. 2,249.3 137,276.1 17.2 84.0

United India Insurance

Ltd. 1,681.3 102,609.7 12.8 77.5

National

Insurance Co. Ltd. 1,590.9 97,089.3 12.1 84.4

Oriental

Insurance Co. Ltd. 1,193.3 72,825.4 9.1 81.9

ICICI Lombard GIC Ltd. 1,123.4 68,561.6 8.6 81.3

2014 DWP

Industry Premiums Split by Lines of Business

Lines of

business USD mn INR mn

Inc claims

INR mn

Loss

ratio %

Comb

ratio %

*Y/Y

growth %

Property 1,340.7 81,820.6 35,984.5 71.0 76.6 12.0

Construction

& Engineering 427.8 26,109.5 10,636.8 71.6 71.6 2.0

Motor 5,704.3 348,131.9 234,856.1 73.7 77.6 14.0

Liability 226.8 13,841.9 2,853.2 27.4 40.2 18.8

Miscellaneous 1,632.7 99,643.1 46,988.6 78.0 75.6 8.7

MAT 541.2 33,027.2 11,899.5 63.0 71.7 4.5

Industry-wide

Non-Life 9,873.5 602,574.2 343,218.7 72.5 76.0 11.8

PA & Health 3,224.1 196,767.3 148,567.5 84.8 89.8 13.8

Grand Total 13,097.6 799,341.5 491,786.2 75.8 79.0 12.3

2014 DWP

*Growth % is based on premiums in local currency Break-up by line of business reflects premiums written within this market sector

GDP – PPP (USD bn)

8,027.0

GDP Per Capita – PPP (USD)

6,209.5

Population (mn)

1,292.7

5yr Real GDP Growth (%)

8.4

Unemployment Rate (%)

6.3

Inflation Rate (%)

5.4

Political Risk

Terror Risk

World Bank relative ease of doing business

Low High

Easiest Hardest

Data Source: IMF, SNL, S&P, Fitch, Moody’s, A.M. Best, Insurance Regulatory and Development Authority, Aon, and Aon Benfield.

2014 Insurance Penetration - Non-life and PA & Healthcare GWP vs. GDP

India Prem: GDP = 0.6%; APAC Prem: GDP = 1.5%

Includes Non-life + PA & Healthcare premiums Ranking based on total premiums written by an insurer within this market sector

(2015 est.)

24 25

IndonesiaBorobudur Temple in Yogyakarta, Java

26 27

Indonesia

Capital Requirements

Insurance companies’ minimum capital has to increase to 100bn IDR in 2014. The requirements for reinsurance companies are 200bn IDR in 2014. Both insurers and reinsurers are required to maintain a minimum guarantee funds as policyholder protection in the event of bankruptcy. The requirement is the greater of 20% of paid-up capital or equity benchmark and 1% of net premium plus 0.25% of reinsurance premium.

Foreign Ownership

Foreign ownership in joint ventures are capped at 80%. This level is flexible, however, provided that the Indonesian partner’s aggregated paid-up capital is maintained. Then, the foreign insurer can increase its stake beyond 80%. This is a much higher level than in other countries in the region. Foreign ownership is still lower due to the highly competitive nature of the market.

Regulatory Updates

In October 2015, President Joko Widodo signed a presidential regulation on the formation of PT Reasuransi Indonesia Utama, also known as Indonesia Re. The company is formed through the merger of state-owned PT Asei Reasuransi Indonesia (Persero) and PT Reasuransi Umum Indonesia (Persero). The establishment of Indonesia Re is aimed at creating a large-scale national reinsurance company that can help promote domestic retention.

In September 2015, OJK mentioned that it would temporarily lower insurers’ required solvency margin as part of a stimulus policy package to help local insurance industry weather the impact of volatile currency and capital market by relaxing some criteria for computation of insurers’ risk-based capital requirement, including the evaluation of securities investments, particularly those companies that suffered investment losses as a result of weakening local financial conditions. Overall, the OJK said it will allow insurance companies to meet only 50% of the minimum capital requirement, instead of 100%, until such time the markets have recovered. The new measures are applicable to conventional insurers and reinsurers and Shariah insurance and reinsurance companies.

Major Risks

Catastrophe Risk

Volcanic Eruption and Flood remain the dominant catastrophe risk factors in Indonesia. In 2015 alone, Indonesia experienced eruption of Mt. Sinabung, Mt. Raung and Mt. Gamalama, although for the last two incidents, the social & economic losses are not significant. Floods, in many cities in Indonesia are considered a man-made loss due to poor maintenance of water ways infrastructure.

Regulatory Risk

With enforced regulation systems by OJK, the business operation of insurance & reinsurance companies in Indonesia can be considered improved than in the past. The implementation of Enterprise Risk Management for insurance & reinsurance companies also monitored by OJK with special supervision for the Board of Directors. Failure to maintain level of reporting or implementing risk management could be resulted in penalty not only for the company but also to the Directors.

Financial Risk

The current exchange rate between Indonesia Rupiah (IDR) and United States Dollar (USD) has wider impact in insurance & reinsurance transactions as most of commercial policies in Indonesia are using USD. The Central Bank of Indonesia (Bank Indonesia) this year issued law that minimized transaction in USD and to use IDR as the main currency. Specific for insurance & reinsurance business, OJK has discretion but encourages industry to maximise the use of IDR in making the payment, moreover in direct side.

Litigation Risk

The Indonesia government put special effort to strengthening the litigation system especially in financial sector. The impact of KPK has been significantly changed the way people or industry doing transactions with more clarity on business procedure and optimising electronic or online system for tender, procurement including taxation. If this mechanism has been fully adopted by all industry, the business process would be more productive, transparent and time effective. The litigation risk at this stage can be considered lower than in the past.

Industry Aggregate Premium 2009 to 2013

Credit Rating and Outlook

Rating Outlook

S&P BB+ Positive

Fitch BBB- Stable

Moody's Baa3 Stable

AM Best CRT-4

Aon Benfield Outlook

The insurance market in Indonesia is growing through the increase in the number of automobiles and scooters, micro financing schemes, large scale commercial projects, and infrastructure development. The impact on reinsurance is largely around Commercial lines, specifically the development of infrastructure and public utilities. The new government has assigned the infrastructure and public utilities sector as a key area of focus, after a lack of any significant investment for decades. Insurance rates have been growing to optimum levels since early 2014 with the introduction of the motor tariff which is expected to be maintained for at least the next three years. However it is expected that earthquake and flood rates are likely to be reviewed and changed in the near future due to the recent losses on these programs.

There is over-supply in the reinsurance market as reinsurers look to support the local cedants and benefit from the growth in premiums from the new tariff. Main themes in the market are around consolidation with reinsurers looking to increase scale and establish more flag positions and multinationals looking to set-up joint ventures on the direct side. How the OJK-proposed regulatory change is to impact the reinsurance industry is to be observed.

There is an increased emphasis on developing mobile technology as a distribution for retail products.

Top 5 Insurers

Entity USD mn IDR mn

Market

share %

Loss

ratio %

Comb

ratio %

*Y/Y

growth %

Asuransi Astra

Buana 361.3 3,779,889.0 8.7 49.2 85.1 26.3

Asuransi Sinar

Mas 341.1 3,568,439.0 8.2 60.2 96.9 3.6

Asuransi Jasa

Indonesia 269.7 2,821,370.0 6.5 51.2 71.5 -1.6

Asuransi Central

Asia 220.4 2,305,945.0 5.3 76.0 103.7 14.5

PT. Tugu Pratama

Indonesia 198.4 2,075,843.0 4.8 43.4 70.2 38.3

2013 DWP

Industry Premiums Split by Lines of Business

Lines of

business USD mn IDR mn

Inc claims IDR

mn

Loss

ratio %

*Y/Y

growth %

Property 1,040.4 10,883,507.0 4,759,477.0 56.9 16.8

Construction &

Engineering 132.8 1,388,778.0 675,218.0 59.8 19.9

Motor 1,235.5 12,924,531.0 6,390,310.0 64.9 15.1

Liability 84.2 881,234.0 79,043.0 10.7 34.8

Surety, Bonds &

Credit 300.8 3,146,440.0 967,768.0 50.8 108.0

Miscellaneous 227.0 2,375,072.0 787,885.0 49.8 -1.1

Marine, Aviation

& Transit 608.5 6,365,945.0 380,110,058.0 N/A 12.1

Industry-Wide

Non-Life 3,629.2 37,965,507.0 393,769,759.0 58.0 18.8

Personal

Accident &

Healthcare

503.8 5,270,155.0 3,264,813.0 74.8 14.4

Grand Total 4,132.9 43,235,662.0 397,034,572.0 N/A 18.3

2013 DWP

*Growth % is based on premiums in local currency 2013 information is updated based on the revised numbers now available 2014 statistics were not published by the regulator when preparing this reportBreak-up by line of business reflects premiums written within this market sector

GDP – PPP (USD bn)

2,838.6

GDP Per Capita – PPP (USD)

11,111.8

Population (mn)

255.5

5yr Real GDP Growth (%)

7.2

Unemployment Rate (%)

5.8

Inflation Rate (%)

6.8

Political Risk

Terror Risk

World Bank relative ease of doing business

Low High

Easiest Hardest

Data Source: IMF, SNL, S&P, Fitch, Moody’s, A.M. Best, Otoritas Jasa Keuangan, Aon, and Aon Benfield.

2,000

2,500

3,000

3,500

4,000

4,500

20,000,000

25,000,000

30,000,000

35,000,000

40,000,000

45,000,000

2009 2010 2011 2012 2013

Total Premiums IDR million Total Premiums USD million

2013 Insurance Penetration - Non-life GWP vs. GDP

Indonesia Prem: GDP = 0.3%; APAC Prem: GDP = 1.5%

*Growth % is based on premiums in local currencyIncludes Non-life + PA & Healthcare premiumsRanking based on total premiums written by an insurer within this market sector2013 information is updated based on the revised numbers now available2014 statistics were not published by the regulator when preparing this report

(2015 est.)

28 29

JapanMount Fuji

30 31

Industry Premiums Split by Lines of Business

Lines of

business USD mn JPY mn

Inc claims

JPY mn

Loss ratio

%

*Y/Y

growth %

Property 13,461.1 1,426,141.0 744,307.0 52.2 0.5

Construction

& Engineering 796.1 84,347.0 41,029.0 48.6 9.2

Motor 46,182.9 4,892,843.0 2,910,732.0 59.5 1.2

Workers Comp 531.7 56,330.0 19,299.0 34.3 -45.3

Liability 4,938.6 523,217.0 236,775.0 45.3 -5.5

Surety, bonds,

& credit 401.1 42,493.0 10,478.0 24.7 -7.5

Miscellaneous 7,395.6 783,525.0 200,964.0 25.6 3.0

MAT 2,877.5 304,854.0 145,218.0 47.6 -1.5

Industry-Wide

Non-Life 76,584.6 8,113,750.0 4,308,802.0 53.1 0.1

PA & Health 6,680.9 707,807.0 354,200.0 50.0 -7.9

Grand Total 83,265.4 8,821,557.0 4,663,002.0 52.9 -0.1

2014 DWP

*Growth % is based on premiums in local currencyBreak-up by line of business reflects direct net premiums written (net ofcancellations) within this market sector

Japan

Capital Requirements

The minimum capital requirement for both the stock insurance company and the mutual insurance association is 1bn JPY.

Foreign branches are required to deposit normally minimum 200mn JPY in cash or securities and must hold assets in Japan in equivalence to the total of their underwriting reserves and outstanding loss reserves.

Foreign Ownership

Foreign companies are allowed to establish wholly owned subsidiaries or branches in Japan or to acquire any percentage of a Japanese company’s equity.

Regulatory Updates

In June 2015 the Japan Financial Services Agency (JFSA) disclosed the results of the second field tests which covered all insurance companies with the aim of introducing economic value-based solvency regime. JFSA summarizes the direction of future examinations as follows:

1. A variety of issues and challenges were recognized in the field tests, as in the previous tests. Based on the results, JFSA needs to conduct further examination toward establishing a specific framework.

2. There are ongoing movements in the economic value-based solvency regime and accounting system, such as the IAIS’s ICS field tests, Solvency II in Europe and examination of IFRS 4 “Insurance Contracts”. Under such circumstances, it is considered to be important to establish a regulatory framework suitable to Japan, paying attention to the nature of the Japanese insurance market.

3. Introducing the economic value-based solvency regime requires some revisions to the business management and risk management methods used by insurance companies. Therefore, the JFSA will make steady efforts to establish a new framework through dialogue with relevant parties in various situations, so as to ensure a smooth introduction.

Major Risks

Catastrophe Risk

Japan is exposed to multiple catastrophe risks including earthquake and weather related events which are a significant challenge to insureds and insurers alike. For insurers both frequency and severity must be carefully managed in accordance with heightened ERM governance requirements. Profitability is heavily dependent on frequency and severity of natural catastrophe losses in any given year.

Regulatory Risk

In March 2015, Japan FSA requested all the insurance companies to submit an ORSA report on an annual basis. The aim is to enhance and speed implementation of ERM within Japanese insurers. There are potential implications for how insurers view and therefore purchase reinsurance with an increased focus and accountability on decision-making for the reinsurance purchase.

Underwriting Risk

Revised fire base rates will be introduced in October 2015 reflecting recent loss experience due to weather related exposures (e.g. snow, freeze). On average the rates are increased by 3.5% although there is variation across the different rating zones depending on loss experience. As part of this base rate change, the maximum duration of the long-term dwelling policies will be capped at 10 years.

Market Risk

Japanese insurers typically hold a relatively high percentage of assets in equity. While this has led significant increases in financial strength over the past couple of years driven by the NIKKEI, it was also a major challenge during the Global Financial Crisis. Volatile financial market therefore remains a risk factor. A number of companies have active strategies to change the shift in their asset bases within their published mid-term plans.

Industry Aggregate Premium 2010 to 2014

Credit Rating and Outlook

Rating Outlook

S&P A+ Stable

Fitch A Stable

Moody's A1 Stable

AM Best CRT-2

Aon Benfield Outlook

With a challenging growth environment in Japan for a number of years the merger activity of the mega insurance groups looks almost complete on the domestic front. Once all the mega-mergers are completed in 2015 the three largest insurance groups will have a combined market share of over 90%, with concentration being close to 100% in certain specialist lines. Published mid-term plans point to further M&A activity outside of Japan as insurers look to reduce exposure to the Japanese equity market and use the proceeds to build on the successful strategy of M&A driven growth outside of Japan in both life and non-life lines of business.

Domestically, profitability has rebounded following the recent revision of Motor rates which has led to improved underwriting performance in the dominant Motor line of business. However, some concern remains over the impact of the consumption tax rate increase to 8% and how it will affect both claims and acquisition costs. Japan is exposed to multiple catastrophe risks include earthquake and weather related events. These remain a significant challenge to insured’s and insurers alike. Profitability of domestic insurance remains heavily dependent on frequency and severity of natural catastrophe losses in any given year.

Reinsurance rates have reduced towards the pre-Tohoku levels follow a combination of softening market conditions and in some cases payback being achieved from the events of 2011. Barring a significant shock the softening market looks set to continue.

40,000

50,000

60,000

70,000

80,000

90,000

100,000

110,000

7,600,000

7,800,000

8,000,000

8,200,000

8,400,000

8,600,000

8,800,000

9,000,000

2010 2011 2012 2013 2014

Total Premiums JPY million Total Premiums USD million

GDP – PPP (USD bn)

4,842.4

GDP Per Capita – PPP (USD)

38,210.6

Population (mn)

126.7

5yr Real GDP Growth (%)

2.3

Unemployment Rate (%)

3.5

Inflation Rate (%)

0.7

Top 5 Insurers

Entity USD mn JPY mn

Market

share %

Loss

ratio %

Comb

ratio %

Sompo Japan Insurance

+ NIPPONKOA Insurance 20,589.0 2,181,300.0 27.0 65.6 97.4

Tokio Marine & Nichido

Fire Insurance Co. Ltd. 19,225.0 2,036,790.0 25.2 61.3 91.5

Mitsui Sumitomo

Insurance Co. Ltd. 13,646.9 1,445,819.0 17.9 62.2 94.0

Aioi Nissay Dowa

Insurance Co. Ltd. 10,957.3 1,160,867.0 14.4 63.2 96.9

The Fuji Fire & Marine

Insurance Co. Ltd.2,632.5 278,898 3.5 54.8 92.4

2014 NWP

Political Risk

Terror Risk

World Bank relative ease of doing business

Low High

Easiest Hardest

Data Source: IMF, SNL, S&P, Fitch, Moody’s, A.M. Best, Financial Services Agency, Aon, and Aon Benfield.

2014 Insurance Penetration - Non-life and PA & Healthcare GWP vs. GDP

Japan Prem: GDP = 1.8%; APAC Prem: GDP = 1.5%

Includes Non-life + PA & Healthcare premiums Excludes Zenkyoren, that has a significant market share and other cooperative mutual insurers e.g., KyosaiRanking based on total premiums written by an insurer within this market sector

(2015 est.)

32 33

Korea (Republic of)Boats at Haeundae in Busan

34 35

Korea (Republic of)

Capital Requirements

Minimum capital requirements have been set by line of business.

For insurance companies, minimum capital requirements depend on the complexity of their business portfolio. The minimum capital for a mono-line insurer writing only engineering or title insurance is 5bn KRW. The minimum capital for a multiline insurer is the sum total of the capital requirements applicable to each of its authorized business lines, subject to a maximum of 30bn KRW. For application of a reinsurance license, the minimum capital is at 30bn KRW.

The RBC ratio is based on available capital divided by the required capital. The ratio which has to be maintained by all insurers is to be more than 100%.

Foreign Ownership

Foreign insurers are allowed to establish branches or wholly owned subsidiaries in Korea or to buy any percentage of a domestic company’s equity.

Foreign insurers must hold an investment grade rating from an international rating agency.

Regulatory Updates

FSS is moving towards a more evolved version of the RBC with strengthening of the confidence level of capital sufficiency for all risk factors from 95% to 99% and this is being implemented at different times for different risk factors.

Insurers will be required to prepare and implement an Own Risk and Solvency Assessment (ORSA) policy in 2017, based on 2016 financial data. ORSA guidelines, a manual to the guidelines and an FSS reporting template will be published towards the end of 2015.

Major Risks

Catastrophe Risk

Typhoon season in Korea is normally during summer which is May to September and looks like typhoon season is mostly over now. That means it will be another clean cat year and we will be able to expect modest rate deduction continuously.

Underwriting Risk

2015 has proved to be a challenging year for Korean risk programmes with sizeable property losses emanating from the Middle East and China in addition to Korean domestic risk losses. We expect certain pro-rata treaties to be adversely affected and reinsurers would be looking for improved terms and/or limiting the coverage of certain overseas property types.

Regulatory Risk

With regards to reinsurers’ visit to Korea, overseas Reinsurers’ visit to Korean clients in Korea has been proceeding smoothly through the past year. We strongly recommend Reinsurers to arrange their meetings through a registered broker for their meetings with Korean cedants. Being one of the top reinsurance brokers in Korea, Aon Benfield is ready to assist all reinsurers to arrange for clients’ meeting in Korea.

Industry Aggregate Premium 2010 to 2014

Credit Rating and Outlook

Rating Outlook

S&P AA- Stable

Fitch AA- Stable

Moody's Aa3 Positive

AM Best CRT-2

Aon Benfield Outlook

There are currently no major changes occurring in the Korean market as direct rates remain flat and stable. There is excess capacity in the market and despite high loss ratios, reinsurance rates have not seen much increases. Most primary companies are focussed on increasing their market share in long-term A&H policy, as the majority of their portfolio is driven by this class of business. A large proportion of the A&H portfolios are reinsured through quota share directly with Korean Re and very little Excess of Loss (XOL) coverage is purchased. The development of new products has focussed on increasing coverage as opposed to investment products due to the low interest rate environment. Alternative capital is beginning to gain some real traction, causing insurers to think about consolidation in order to increase scale and competitive advantage. KB Financial Group has recently signed a contract with LIG to take control of the controlling stake of LIG insurance, stating the need for diversification as the main driver for the investment.

Following a change in the Insurance Business Law, the common fiscal year-end for the insurance industry has been changed from 31 March to 31 December, effective from 2013. Most major reinsurance programme renewal dates have been changed to 1 January.

GDP – PPP (USD bn)

1,894.4

GDP Per Capita – PPP (USD)

36,528.4

Population (mn)

50.6

5yr Real GDP Growth (%)

4.6

Unemployment Rate (%)

3.7

Inflation Rate (%)

0.7

Industry Premiums Split by Lines of Business

Break-up by line of business reflects premiums written within this market sector

Top 5 Insurers

Entity USD mn KRW mn

Market

share %

Loss

ratio %

Comb

ratio %

Samsung Fire & Marine

Insurance Co. Ltd. 18,850.0 19,848,346.3 26.2 85.5 103.7

Hyundai Marine & Fire

Insurance Co. Ltd. 11,588.2 12,201,961.9 16.1 85.2 102.5

Dongbu Insurance

Co. Ltd 10,363.4 10,912,234.2 14.4 86.8 105.0

*KB Insurance Co. Ltd. 9,245.2 9,734,845.8 12.9 87.5 106.7

Meritz Fire & Marine

Insurance Co. Ltd. 4,904.9 5,164,677.2 6.8 84.9 106.6

2014 DWP

Political Risk

Terror Risk

World Bank relative ease of doing business

Low High

Easiest Hardest

Data Source: IMF, SNL, S&P, Fitch, Moody’s, A.M. Best, Financial Services Commission, Aon, and Aon Benfield.

40,000

45,000

50,000

55,000

60,000

65,000

70,000

75,000

45,000,000

50,000,000

55,000,000

60,000,000

65,000,000

70,000,000

75,000,000

80,000,000

2010 2011 2012 2013 2014

Total Premiums KRW million Total Premiums USD million

2014 Insurance Penetration - Non-life and PA & Healthcare GWP vs. GDP

Korea Prem: GDP = 5.1%; APAC Prem: GDP = 1.5%

Excluding PA & Healthcare premiumsA dip in 2013 industry premiums is a result of financial year-end change in Korea (nine-month period from 1 April to 31 December 2013)

Lines of

business USD mn KRW mn

Inc claims

KRW mn

Loss ratio

%

Property 1,681.8 1,770,822.5 855,646.5 49.3

Construction

& Engineering 291.5 306,925.9 96,507.1 30.8

Motor 12,301.0 12,952,448.6 10,347,520.7 82.5

Workers Comp 100.0 105,344.4 80,637.5 77.0

Liability 598.9 630,650.4 360,038.8 58.0

Surety, bonds, & credit 1,207.4 1,271,352.8 588,524.9 46.1

Miscellaneous 53,558.1 56,394,574.7 48,622,978.9 86.4

MAT 711.3 749,006.2 604,235.6 78.4

Industry-Wide Non-Life 70,450.0 74,181,125.5 61,556,090.0 83.6

PA & Health 1,400.6 1,474,824.7 1,134,223.9 77.3

Grand Total 71,850.7 75,655,950.2 62,690,313.9 83.5

2014 DWP

*KB Insurance Co. Ltd. was previously LIG Insurance Co. Ltd.Includes Non-life + PA & Healthcare premiumsRanking based on total premiums written by an insurer within this market sector

(2015 est.)

36 37

MalaysiaKuala Lumpur is the capital and the largest city of Malaysia

38 39

Malaysia

Capital Requirements

Minimum paid-up capital for insurers / reinsurers since 1996 and Takaful operators since 2004 is 100mn MYR. For a life or general insurer operating as a Labuan company, the requirements are at least 7.5mn MYR or its equivalent in any foreign currency in the company’s first year of operation. In subsequent years, the requirement is the greater of 7.5mn MYR and 20 percent of net premium income. For a reinsurer operating as a Labuan company, the requirement is at least 10mn MYR in the first year, and the greater of 10mn MYR and the sum of 20 percent non-life net premiums and 3 percent of actuarial valuation of life liabilities in subsequent years.

Foreign Ownership

Foreign investment of up to 70% is permitted in insurance companies and Takaful operators. On a case-by-case basis, 100% foreign equity for insurance companies can be considered. If a foreign company plans to enter negotiations for 5+% of a Malaysian conventional insurer / Takaful operator, it must receive consent and approvals from the central bank, Malaysian minister of finance, government of BNM as a director general of Takaful, and the Foreign Investment Committee for proposed acquisitions of 15+% voting rights or with valuation of 10m MYR. A foreign insurer who acquires 33+% of a conventional insurer / Takaful operator or holds 33-50% of the voting shares of conventional insurer / Takaful operator and acquires or plans to acquire 2+% of voting shares of the company, must extend an MGO for the remaining shares.

Since 2009, locally incorporated foreign-owned insurance companies / Takaful operators can establish branches without restriction throughout Malaysia as well as enter into bancassurance arrangements. Greater flexibility with regards to hiring expatriates has also been employed, which has contributed to industry development and local talent / training improvement.

Regulatory Updates

The Malaysian market is moving towards the abolition of all rating tariffs, which is now expected to happen from 3rd Quarter 2016 or 1 January 2017.

Major Risks

Underwriting Risk

Malaysia has been experiencing favourable claim experience in most lines, except for Motor. An insurance pool (MMIP) for high-risk drivers was created that equally shares premium and losses among all licensed general and Takaful operators, putting added pressure on insurers’ operating results.

Regulatory Risk

The impending market liberalization which is now slated for 3rd Quarter 2016 or 1st January 2017 is a cause for concern among carriers as the additional competition expected from new market entrants would lead to a softening market. The regulator’s drive for financial liberalisation and detariffication has put an increased focus on profitability and cost management.

Catastrophe Risk

In 2014, Malaysia experienced the worst flood in 30 years. However, all the major reinsurance brokers are able to model this flood risk probabilistically resulting in greater confidence in the adequacy of the catastrophe cover being purchased.

Industry Aggregate Premium 2010 to 2014

Credit Rating and Outlook

Rating Outlook

S&P A- Stable

Fitch A- Stable

Moody's A3 Positive

AM Best CRT-3

Aon Benfield Outlook

The general insurance industry grew at a slower pace for 1st half 2015. General Insurance Association of Malaysia (PIAM) attributed the lower growth rate to a challenging business and operating environment. Contributing factors include a cautious outlook and a moderation in consumer spending as a result of the heightened economic uncertainties coupled with the rising cost of living which mainly affected the motor class being the dominant line of business overall. The reinsurance market remains relatively stable with excess capacity in the market but there is uncertainty around the prospect of detariffication slated for mid-2016. Bank Negara will most definitely incorporate premium bands to prevent the risk of under-pricing. In addition, detariffication will be a partial and gradual one and there could be slight margin erosion, although the risk of severe erosion in the industry due to irrational competition is eliminated. Pricing adequacy, segmentation analysis, product innovation, capital efficiency and cost management are key differentiators with firms fighting to gain market share.

With the recent memories of Sabah earthquake and 2014 Flood (the worst flooding in more than 30 years), market participants are more concerned with the impact of a natural catastrophe resulting in an increased interest in structured reinsurance solutions. Actuarial services, talent development and localisation of management remain high on the agenda for insurance firms. Above all, they are cautiously optimistic that the general insurance industry growth rates will go back to normality as it has proven its resilience and robust nature over time.

2,500

3,000

3,500

4,000

4,500

5,000

5,500

12,000

13,000

14,000

15,000

16,000

17,000

18,000

2010 2011 2012 2013 2014

Total Premiums MYR million Total Premiums USD million

GDP – PPP (USD bn)

813.5

GDP Per Capita – PPP (USD)

26,141.1

Population (mn)

31.1

5yr Real GDP Growth (%)

7.0

Unemployment Rate (%)

3.0

Inflation Rate (%)

2.4

Industry Premiums Split by Lines of Business

Lines of

business USD mn MYR mn

Inc claims

MYR mn

Loss

ratio %

Comb

ratio %

*Y/Y

growth %

Property 902.6 2,954.3 436.9 28.8 53.8 5.8

Construction &

Engineering 205.6 672.8 75.1 44.6 58.9 4.4

Motor 2,423.7 7,932.4 5,035.0 71.5 102.3 5.4

Workers Comp 73.5 240.6 21.5 9.6 46.0 3.2

Liability 167.4 548.0 45.9 20.1 54.6 10.5

Surety, bonds,

& credit 15.6 51.1 2.6 9.9 35.1 -3.7

Miscellaneous 237.1 776.0 227.1 49.8 91.3 6.1

MAT 504.5 1,651.2 123.7 33.9 54.8 8.7

Industry-Wide

Non-Life 4,530.0 14,826.2 5,967.8 59.5 89.5 5.9

PA & Health 693.8 2,270.8 822.2 42.0 77.8 5.3

Grand Total 5,223.8 17,097.0 6,790.0 56.7 78.3 5.9

2014 GWP

*Growth % is based on premiums in local currency Non-life premiums exclude General Takaful businessBreak-up by line of business reflects premiums written within this market sector

Top 5 Insurers

Entity USD mn MYR mn

Market

share %

Loss

ratio %

Comb

ratio %

Allianz General

Insurance Co. (MY) Bhd 650.1 2,127.8 11.8 59.3 86.6

AmGeneral Insurance

Bhd 620.4 2,030.4 11.3 N/A N/A

MSIG Insurance (MY)

Bhd 454.2 1,486.4 8.3 56.0 75.6

Etiga Insurance Bhd 425.2 1,391.6 7.7 54.4 88.6

AXA Affin General

Insurance Bhd 346.7 1,134.7 6.3 60.4 79.7

2014 GWP

Political Risk

Terror Risk

World Bank relative ease of doing business

Low High

Easiest Hardest

Data Source: IMF, SNL, S&P, Fitch, Moody’s, A.M. Best, Bank Negara Malaysia, Aon, and Aon Benfield.

2014 Insurance Penetration - Non-life and PA & Healthcare GWP vs. GDP

Malaysia Prem: GDP = 1.6%; APAC Prem: GDP = 1.5%

Includes Non-Life + PA & Healthcare premiums Ranking based on total premiums written by an insurer within this market sector

(2015 est.)

40 41

New ZealandMitre Peak in Fiordland National Park, South Island

42 43

New Zealand

Capital Requirements

An insurer must at all times maintain actual solvency capital in excess of minimum solvency capital (MSC) to the extent laid down by the solvency standard. Actual solvency capital is the difference between capital (as defined) and deductions from capital (as defined). Solvency capital for a licensed foreign insurer in New Zealand is the excess of the branch’s assets over its liabilities. The minimum amount of the MSC is 1mn NZD for a captive and 3mn NZD for any other type of insurer.

An insurer’s MSC is the sum of the capital charges appropriate for its insurance risk, catastrophe risk, asset risk, and reinsurance recovery risk.

Foreign Ownership

Foreign companies may acquire any percentage of a domestic insurer’s equity or may establish wholly owned subsidiaries or branches, subject to prudential approval. Foreign companies which are allowed to operate as branches should obtain a credit rating from an international rating agency.

Regulatory Updates

In December 2014 the Reserve Bank issued a set of Insurance Solvency Standards. The new standards commence on 1 January 2015, except for certain provisions relating to reinsurance within the Solvency Standard for Life Insurance Business 2014. The standards are reissued mainly for updated treatment of guarantees and enhanced disclosure of solvency margin information.

Beginning 8 September 2015, in the RBC model, the catastrophe risk capital charge on earthquake losses is calibrated at 1 in 750 years for insurance losses from earthquake. This will change to 1 in 1000 years starting 8 September 2016.

Major Risks

Catastrophe Risk

Exposure to earthquake continues to dominate private insurers catastrophe protection, particularly with the high earthquake insurance penetration rate for commercial and domestic (excess EQC) risk and the major fault lines running through the central region of New Zealand.

Regulatory Risk

The New Zealand Government has proposed changes to the EQC Act which are aimed at improving the claims management experience for EQC claimants and ensuring continued access to affordable, effective natural disaster insurance. Key proposed changes are earthquake claims being lodged and to a degree managed by private insurers, changes to land coverage and the current monetary cap on EQC building cover doubled to 200,000 NZD (plus GST). Any change to the EQC Act is not expected to come into effect before 2017, but if implemented in the current form may lead to EQC assuming a larger part of the exposure and therefore premium of the domestic natural perils market.

Underwriting Risk

While the number of outstanding Christchurch earthquake claims is decreasing, claims movement due to delayed settlements and increasing claims costs above current reserves will increase earnings risk for insurers as upper catastrophe limits have been tested during 2015.

Industry Aggregate Premium 2010 to 2014

Credit Rating and Outlook

Rating Outlook

S&P AA Stable

Fitch AA Positive

Moody's Aaa Stable

AM Best CRT-2

Aon Benfield Outlook

After expanding at a robust pace over 2014, the New Zealand economy is showing signs of coming off the boil in 2015. A dramatic downturn in dairy export markets is expected to result in export revenue declining by 3.5bn NZD (about 1.5% of annual GDP). Combined with an earlier than expected peak in Canterbury earthquake rebuild work, currently underpinning New Zealand construction activity, may result in annual GDP growth dropping below 2%. Some drivers of economic growth remain strong with the rapidly expanding population of Auckland propelling residential and infrastructure construction and a lower exchange rate boosting expansion of tourism and foreign education. Bodily injury risks (CTP, W/C, Med Mal) continue to be publically insured via a no-fault accident scheme (ACC) and domestic earthquake risk is largely insured with the EQC.

Private sector insurers are facing increased competition due to new entrants, market wide growth aspirations fuelled by a plentiful supply of (re)insurance capacity. Market consolidation should assist some players in maintaining current margins if efficiency gains can be achieved, however frequent weather related events continue to impact results (2015 to date reached 100mn NZD in insured losses). Favourable reinsurance market conditions continue to offer further expense savings or the opportunity to expand protection levels.

2,000

2,500

3,000

3,500

4,000

4,500

5,000

5,500

2010 2011 2012 2013 2014

Total Premiums NZD million Total Premiums USD million

GDP – PPP (USD bn)

166.0

GDP Per Capita – PPP (USD)

35,966.1

Population (mn)

4.6

5yr Real GDP Growth (%)

4.1

Unemployment Rate (%)

5.8

Inflation Rate (%)

0.2

Industry Premiums Split by Lines of Business

Lines of business USD mn NZD mn

Inc claims

NZD mn

Loss

ratio %

*Y/Y

growth %

Property 2,309.9 2,784.3 3,416.8 122.7 5.1

Motor 1,261.9 1,521.1 1,018.5 68.7 5.8

Workers’ Compensation 31.7 38.3 8.5 22.3 15.4

Liability 349.2 420.9 260.8 64.3 17.3

Surety, bonds, & credit 6.5 7.8 6.6 82.3 16.0

Miscellaneous 100.8 121.5 65.4 53.9 6.0

MAT 117.7 141.9 59.2 41.8 2.2

Industry-Wide Non-Life 4,177.7 5,035.8 4,835.8 97.1 6.3

PA & Health 190.5 229.7 107.7 48.3 18.3

Grand Total 4,368.3 5,265.5 4,943.6 95.0 6.7

2014 GWP

*Growth % is based on premiums in local currencyBreak-up by line of business reflects premiums written within this market sector

Top 5 Insurers

Entity USD mn NZD mn

Market

share %

Loss

ratio %

Comb

ratio %

IAG New Zealand 1,650.8 2,013.0 40.8 73.9 105.6

Vero Insurance 806.2 983.0 19.9 55.0 92.0

Lumley General

Insurance (NZ) 382.8 466.8 9.5 68.1 101.3

AA Insurance 201.9 246.2 5.0 67.4 100.6

Tower Insurance 187.5 228.7 4.6 70.6 102.8

2013 GWP

Political Risk

Terror Risk

World Bank relative ease of doing business

Low High

Easiest Hardest

Data Source: IMF, SNL, S&P, Fitch, Moody’s, A.M. Best, Financial Markets Authority, The Reserve Bank, Aon, and Aon Benfield.

2014 Insurance Penetration - Non-life and PA & Healthcare GWP vs. GDP

New Zealand Prem: GDP = 2.2%; APAC Prem: GDP = 1.5%

IAG completed acquisition of Wesfarmers/Lumley on July 30, 2014Ranking based on premiums written by an insurer within this market sector Includes Non-life + PA & Healthcare premiums 2014 statistics were not published by the regulator when preparing this report

(2015 est.)

44 45

PakistanBadshahi Mosque in Lahore

46 47

Pakistan

Capital Requirements

The minimum capital requirement is 300mn PKR for non-life companies and general Takaful operators. Each insurer shall make and maintain a deposit with the State Bank of Pakistan a specified minimum amount either in cash or approved securities, or a hybrid. Currently this specified amount is the higher of 10mn PKR and 10% of the insurer’s paid up capital or, such amount as may be prescribed by the regulator SECP.

The regulator has announced a planned increase in the minimum paid-up capital requirements which will take place incrementally in six-monthly intervals until December 2017. For non-life insurers and Takaful operators, the minimum paid-up capital has to be 300mn PKR by 31 December 2015, increasing by 50mn PKR at six-monthly intervals until it reaches 500mn PKR by 31 December 2017.