section 179d: leveraging the energy efficiency...

TRANSCRIPT

Section 179D: Leveraging the Energy Efficiency

Deduction for Commercial Buildings Navigating Details of Full or Partial Tax Breaks on New or Improved Structures and Systems

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

For this program, attendees must listen to the audio over the telephone.

Please refer to the instructions emailed to the registrant for the dial-in information.

Attendees can still view the presentation slides online. If you have any questions, please

contact Customer Service at1-800-926-7926 ext. 10.

WEDNESDAY, JULY 18, 2012

Presenting a live 110-minute teleconference with interactive Q&A

Ronald Wainwright, Jr., Partner, Cherry Bekaert & Holland, Raleigh, N.C.

C.J. Aberin, Principal, KBKG, Denver

Julio Gonzalez, Founder and CEO, Engineered Tax Services, West Palm Beach, Fla.

Eric Smith, Tax Partner, Beene Garter, Grand Rapids, Mich.

Conference Materials

If you have not printed the conference materials for this program, please

complete the following steps:

• Click on the + sign next to “Conference Materials” in the middle of the left-

hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a

PDF of the slides for today's program.

• Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

Continuing Education Credits

Attendees must listen to the audio over the telephone. Attendees can still view

the presentation slides online but there is no online audio for this program.

Attendees must stay on the line for at least 100 minutes in order to qualify for

a full 2 credits of CPE. Attendance is monitored as required by NASBA.

Please refer to the instructions emailed to the registrant for additional

information. If you have any questions, please contact Customer Service

at 1-800-926-7926 ext. 10.

FOR LIVE EVENT ONLY

Tips for Optimal Quality

Sound Quality

For this program, you must listen via the telephone by dialing 1-866-873-1442

and entering your PIN when prompted. There will be no sound over the web

connection.

If you dialed in and have any difficulties during the call, press *0 for assistance.

You may also send us a chat or e-mail [email protected] immediately so

we can address the problem.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

Section 179D: Leveraging the Energy Efficiency Deduction for Commercial Buildings Seminar

C.J. Aberin, KBKG

Eric Smith, Beene Garter

July 18, 2012

Ronald Wainwright Jr., Cherry Bekaert & Holland

Julio Gonzalez, Engineered Tax Services

Today’s Program

Evolution Of The 179D Deduction, And Future Outlook

[Ron Wainwright]

Material Terms Of The 179D Deduction

[C.J. Aberin, Julio Gonzalez and Eric Smith]

Placed-In-Service Issues And IRS Guidance

[Eric Smith]

The Role Of Energy Studies

[Julio Gonzalez]

Slide 7 – Slide 14

Slide 15 – Slide 46

Slide 47 – Slide 55

Slide 56 – Slide 69

EVOLUTION OF THE 179D DEDUCTION, AND FUTURE OUTLOOK

Ronald Wainwright Jr., Cherry Bekaert & Holland

Energy Policy Act Of 2005

• What is EPACT ?

• What was congressional intent ?

• Impact of President Obama’s Better Building Initiative

• Current volleying around by Congress and White House,

coupled with AIA

• Current White House stand

• Possibility of REIT

• Current legislation update

8

Energy Policy Act Of 2005 (Cont.)

• Congress passed legislation in August 2005 to encourage property owners to build energy efficient real estate properties, in order to promote reduction in energy consumption. Service dates were from 1/1/06 through 12/31/08.

• The Emergency Economic Stabilization Act of 2008 (HR-1424), approved and signed on Oct. 3, 2008, extended the benefits of the Energy Policy Act of 2005 through December 31, 2013.

• The ruling allows a tax deduction of up to $1.80 per sq. ft.

• The entity that funds the investment on a private property, or the designer on a government-owned property, is eligible for the deduction.

9

Public Buildings And Tax Deductions?

For commercial buildings 2006-2013 (new buildings and renovations)

- Private buildings (benefits - owner/tenant)

- Public buildings (benefits - architect/engineer/contractor)

- Lighting/HVAC/envelope (roof/windows/insulation)

$.60 $.60 $.60 = $1.80 per SF

$100k SF = $180,000

- Model vs. ASHRAE 2001 90.1 (see slide - % - improvement)

- Business strategy (federal and state subsidy)

10

Attention: Architects, Engineers And Contractors

For energy-efficient commercial building improvements (new build or

renovations) made by a public or government entity ...

Examples: Schools K-12, colleges, universities, civil, municipal,

government, jails, military buildings, etc.

… The IRS now allows the deduction to be allocated to the “person

primarily” responsible for designing the property and systems, in

lieu of the public entity.

― Fewer than 3% of taxpayers or design firms are aware of

opportunity - AIA Journals

― Did your accountant tell you about this?

11

Who Benefits?

Owners or tenants who pay for new or improved, energy efficient

commercial buildings since 2006 and through 2013

Designers of energy efficient properties or retrofits/installed

efficiency in publicly owned buildings

Building and real estate communities indirectly benefit.

12

Candidates

• New construction

• Upgrades, renovations and retrofits, improvements to lighting, HVAC, envelope (roof , insulation, windows), energy performance contracting, CRA redevelopment

• LEED-certified buildings

• Green/energy-efficient buildings

• Commercial and residential (4-plus stories)

• Private and public sectors

• Types: Schools, government, office, retail, hospitality, industrial, manufacturing, healthcare, parking garages

• Architects, engineers and contractors

Placed in service since Jan. 1, 2006

13

In Summary, Maximizing The Benefits Of The Energy Policy Act

Generates money for investments

Increase cash flow through minimizing tax liabilities and

reducing insurance premiums

Increases ROI and reduces payback periods on investments

Important: Planning and execution

14

MATERIAL TERMS OF THE 179D DEDUCTION

C.J. Aberin, KBKG

Julio Gonzalez, Engineered Tax Services

Eric Smith, Beene Garter

NATIONWIDE SERVICE Tax Credits · Incentives · Cost Recovery

© KBKG inc 2012 16

IRC Sect. 179D allows for an immediate deduction of up to

$1.80/sq. ft. for “commercial buildings” that achieve a 50%

reduction in total energy and power costs for lighting, HVAC and

hot water systems, in comparison to 2001 energy standards.

Building envelope

HVAC and hot water

Interior lighting

§179D Tax Deduction Energy Efficient Commercial Building

NATIONWIDE SERVICE Tax Credits · Incentives · Cost Recovery

© KBKG inc 2012 17

Whoever makes investment and places in service for first use

Building owner or landlord

Tenant

OR

Designers of government buildings

§179D Tax Deduction: Who Benefits?

NATIONWIDE SERVICE Tax Credits · Incentives · Cost Recovery

© KBKG inc 2012 18

“Commercial buildings” includes

Public and government buildings (e.g., schools, prisons)

Typical commercial buildings (e.g., office, retail, industrial)

Housing that is 4 stories or higher

Must be situated in the U.S.

§179D Tax Deduction: What Building Types Are Eligible?

NATIONWIDE SERVICE Tax Credits · Incentives · Cost Recovery

© KBKG inc 2012 19

Ground-up construction

Renovations and retrofits

Applies to affected square footages (rate x sq. ft.)

PIS from 2006 through 2013

§179D Tax Deduction: What Types

Of Construction Are Eligible?

NATIONWIDE SERVICE Tax Credits · Incentives · Cost Recovery

© KBKG inc 2012 20

§179D Tax Deduction: Various Ways To Achieve Deduction

Fully

qualifying

property

Partially qualifying property

Envelope HVAC Lighting

(permanent

rule)

Interim lighting rule

(PIS before publication of

final 179D regs)

1/1/06 to 12/31/08:

Energy cost savings*

50%

16-2/3% 16-2/3% 16-2/3%

25% to 40% LPD reduction

(50% LPD reduction for

warehouse) + other factors

1/1/06 to 12/31/13:

Energy cost savings*

10% 20% 20%

3/12/12 to 12/31/13:

Energy cost savings*

10% 15% 25%

Tax deduction $1.80/sf $0.60/sf $0.60/sf $0.60/sf $0.30 to $0.60/sf (using

applicable % from 2006-52)

* Compared to a reference building that meets 2001 energy standards

NATIONWIDE SERVICE Tax Credits · Incentives · Cost Recovery

© KBKG inc 2012 21

§179D Tax Deduction: Various Ways To Achieve Deduction

Fully

qualifying

property

Partially qualifying property

Envelope HVAC Lighting

(permanent

rule)

Interim lighting rule

(PIS before publication of

final 179D regs)

1/1/06 to 12/31/08:

Energy cost savings*

50%

16-2/3% 16-2/3% 16-2/3%

25% to 40% LPD reduction

(50% LPD reduction for

warehouse) + other factors

1/1/06 to 12/31/13:

Energy cost savings*

10% 20% 20%

3/12/12 to 12/31/13:

Energy cost savings*

10% 15% 25%

Tax deduction $1.80/sf $0.60/sf $0.60/sf $0.60/sf $0.30 to $0.60/sf (using

applicable % from 2006-52)

* Compared to a reference building that meets 2001 energy standards

NATIONWIDE SERVICE Tax Credits · Incentives · Cost Recovery

© KBKG inc 2012 22

§179D Tax Deduction: Various Ways To Achieve Deduction

Fully

qualifying

property

Partially qualifying property

Envelope HVAC Lighting

(permanent

rule)

Interim lighting rule

(PIS before publication of

final 179D regs)

1/1/06 to 12/31/08:

Energy cost savings*

50%

16-2/3% 16-2/3% 16-2/3%

25% to 40% LPD reduction

(50% LPD reduction for

warehouse) + other factors

1/1/06 to 12/31/13:

Energy cost savings*

10% 20% 20%

3/12/12 to 12/31/13:

Energy cost savings*

10% 15% 25%

Tax deduction $1.80/sf $0.60/sf $0.60/sf $0.60/sf $0.30 to $0.60/sf (using

applicable % from 2006-52)

* Compared to a reference building that meets 2001 energy standards

NATIONWIDE SERVICE Tax Credits · Incentives · Cost Recovery

© KBKG inc 2012 23

§179D Tax Deduction: Various Ways To Achieve Deduction

Fully

qualifying

property

Partially qualifying property

Envelope HVAC Lighting

(permanent

rule)

Interim lighting rule

(PIS before publication of

final 179D regs)

1/1/06 to 12/31/08:

Energy cost savings*

50%

16-2/3% 16-2/3% 16-2/3%

25% to 40% LPD reduction

(50% LPD reduction for

warehouse) + other factors

1/1/06 to 12/31/13:

Energy cost savings*

10% 20% 20%

3/12/12 to 12/31/13:

Energy cost savings*

10% 15% 25%

Tax deduction $1.80/sf $0.60/sf $0.60/sf $0.60/sf $0.30 to $0.60/sf (using

applicable % from 2006-52)

* Compared to a reference building that meets 2001 energy standards

NATIONWIDE SERVICE Tax Credits · Incentives · Cost Recovery

© KBKG inc 2012 24

Assume federal tax rate = 35%

** Discount rate = 8%

1 system

$0.60 / sf

2 systems

$1.20 / sf

3 systems

$1.80 / sf

Tax deduction $60,000 $120,000 $180,000

NPV benefit **

(owners) $14,348 $28,696 $43,044

§179D Tax Deduction: Benefit, Example Of 100,000 sf Building

NATIONWIDE SERVICE Tax Credits · Incentives · Cost Recovery

© KBKG inc 2012 25

Building type

Building size and number of stories

Physical orientation

Climate zone

Utility rates

§179D Tax Deduction: Key Variables

NATIONWIDE SERVICE Tax Credits · Incentives · Cost Recovery

© KBKG inc 2012 26

Process:

Obtain certification package

No special form required

Reported on the “Other Deduction” line with a description of “Section 179D Deduction

Reduce depreciable basis

Considerations:

Deduction can reduce AMTI.

Subject to 1245 recapture

Can either amend or file Form 3115 to retroactively claim deduction

Deduction limited to amount invested in energy efficient property

§179D Tax Deduction:

Tax Process & Considerations

NATIONWIDE SERVICE Tax Credits · Incentives · Cost Recovery

© KBKG inc 2012 27

Analysis of drawings and as-built specifications

Energy simulation modeling or lighting analysis, using DOE-

approved software

On-site verification

Signed certification by qualified third party that meets all IRS

requirements

§179D Tax Deduction: Certification Process

Practical taxpayer experiences in claiming the deduction for different types of improvements

28

How Does The 179D Affect The Value Of A Design Firm?

A design firm with $10 Million per annum revenue

Designs 500,000 sq. ft. of public buildings a year

• Generating $750,000 a year in tax deductions

• $250,000 in cash (cash in hand, taxes paid)

Assuming a 10-to-1 multiple, these deductions equate to $2.5

million in sales.

As a one-times-earnings multiple, this is an increase in the firm’s

value.

29

Over $290,000 Energy Tax Deductions Claimed By Building Owner

Sq. Ft. 179D/sf Total 179D

San Jose, CA 47,939 $1.20 $57,526.80

Petaluma, CA 65,580 $1.10 $72,138.00

Sparks, NV 64,744 $1.10 $71,218.40

Modesto, CA 74,969 $1.20 $89,962.80

30

Over $119,390 Energy Tax Deductions Claimed By Owner

Hampton Inn, Gainesville: 66,328 square feet •Envelope: Insulated glass, double-pane thermal-break windows and doors, white reflective single-ply roofing system

•Lighting: Low-voltage fluorescent

•HVAC: Natural gas units, split-unit systems, motion-activated room thermostat, continuous-flow

hot water service

31

Over $45,691 Energy Tax Deductions Claimed By Building Owner

Canyon Stone Inc. HVAC 76,153 square feet

(Direct gas-fired industrial heater)

32

Over $124,813 Energy Tax Deductions Claimed By Owner

Renaissance Plaza - San Antonio – Texas – 208,022 Square Feet

•HVAC: Full $0.60 for HVAC and chiller unit

33

Over $292,137 Energy Tax Deductions Claimed By Architect

Sq. Ft. 179D/sf Total

Fern Hill School 54,637 $1.10 $60,101

Auburn Mountainville 183,676 $ .90 $165,308

Capital High School 127,440 $ .40 $50,976

Meeker Elementary 39,382 $ .40 $15,752

34

Over $46,710 Energy Tax Deductions Claimed By Architect

Conference Center, Texas – 77,851 Square Feet

•HVAC: Full $0.60, includes HVAC and chiller units

35

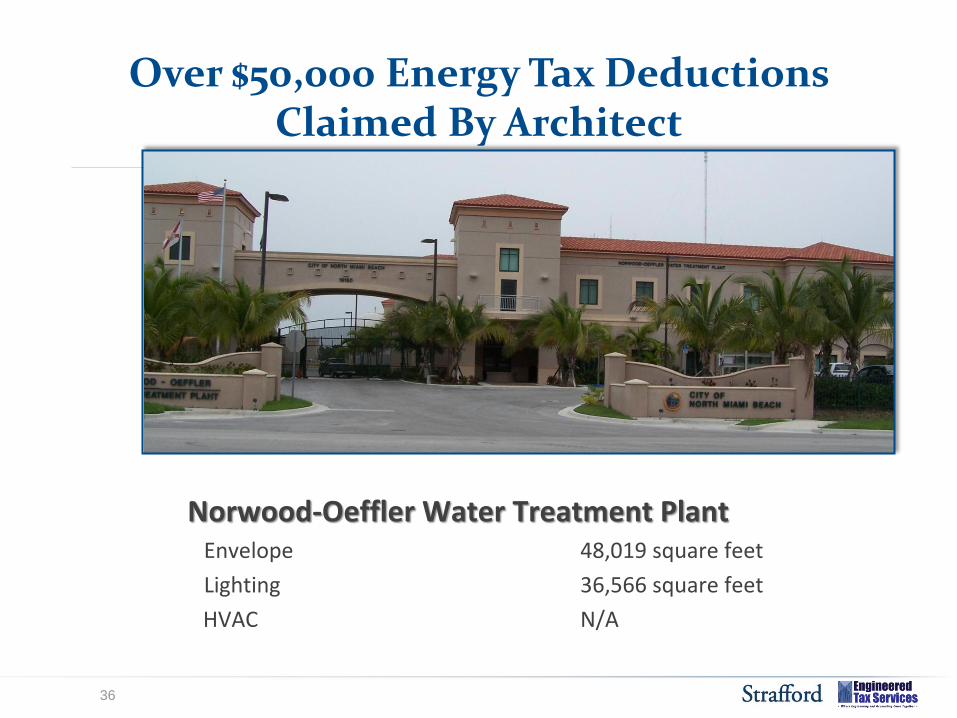

Over $50,000 Energy Tax Deductions Claimed By Architect

Norwood-Oeffler Water Treatment Plant Envelope 48,019 square feet

Lighting 36,566 square feet

HVAC N/A

36

Over $118,680 Energy Tax Deductions Claimed By Owner

Other HVAC Examples – Wyoming, Mich.

•Manufacturing complex - HVAC: Full $0.60 , 105,000 sq. ft., $63,000 tax benefit

•Government building - HVAC: Full $0.60 , 92,801 sq. ft., $55,680 tax benefit

37

Summary Of Tax Deductions

179D Rules

Permanent/Fully Qualifying Property

Permanent/Partially Qualifying Property Interim/Partially Qualifying Property (Lighting Only)

IRS Notice

2006-52, 2008-40 and 2012-22 2006-52 2008-40 2012-22

2006-52, 2008-40 and 2012-22

Requirement Percent reduction in energy cost

Percent reduction in lighting power reduction (LPD)

Building Envelope 50% 16 2/3 % 10% 10% N/A

HVAC 50% 16 2/3 % 20% 15% N/A

Interior Lighting 50% 16 2/3 % 20% 25%

25% to 40% (50% for Warehouses)

Tax Deduction Per Square Foot

$1.80 $0.60 $0.60 $0.60

$.30 to $.60 times the applicable percentage, based on the reduction in LPD (100% - (3-1/3 x [40% - x%]))

Effective For Property Placed In Service

Jan. 1, 2006 through Dec. 31, 2013

Jan. 1, 2006 through Dec. 31, 2008

Jan. 1, 2006 through Dec. 31, 2013

Feb. 24, 2012 through Dec. 31, 2013

Jan. 1, 2006 through Dec. 31, 2013

38

Public Buildings And The 179D Tax Deduction

§179D(d)(4): In the case of energy efficient commercial building property installed on or in property owned by a Federal, State, or local government or a political subdivision thereof, the Secretary shall promulgate a regulation to allow the allocation of the deduction to the person primarily responsible for designing the property in lieu of the owner of such property. Such person shall be treated as the taxpayer for purposes of this section.

39

Who Qualifies As The Designer?

• Sect. 3.02 of Notice 2008-40 defines a designer of government-owned buildings as:

• A person who creates the technical specifications for installation of energy efficient property

• May include architect, engineer, contractor, environmental consultant or energy services provider

• It does not include a person that merely installs, repairs or maintains the property.

40

What If There Are Multiple Designers?

• Sect. 3.03 of Notice 2008-40 provides guidance on allocating the deduction.

• If more than one designer is responsible for creating the technical specifications for installation of energy efficient commercial building property , the owner of the building shall:

• Determine which designer is primarily responsible and allocate the full deduction to that designer, or

• At the owner's discretion, allocate the deduction among several designers.

41

How Does The Designer Obtain The Deduction?

• Sect. 3.04 of Notice 2008-40 provides guidance on obtaining the allocation from the public entity.

• The allocation must be in writing and contain all of the required information set out in this section.

• Name, address and telephone number of authorized representative of the owner of the building

• Name, address and telephone number of authorized representative of the designer

• Address of building, cost of property, date property was placed in service, and amount of deduction being allocated to the designer

• Signatures by both parties, including a declaration signed under penalties of perjury by authorized representative of the owner of the government-owned building

42

Example Of An Allocation Letter

43

How Much Of A Deduction Can The Designer Get?

• Sect. 3.06 of Notice 2008-40 provides guidance on the tax consequences of the allocation.

• The maximum amount of the deduction that can be allocated is equal to the lesser of the cost of the property to the owner, or the $1.80 per square foot (if all three systems qualify).

• The designer has no requirement to include any amounts in income for future years, or reduce any future years’ deductions by an amount equal to the 179D deduction received.

44

What Types Of Projects Are Good Candidates?

• New construction

• Upgrades, renovations or retrofits

• LEED-certified buildings

• Currently must be a government-owned building; non-profit entities currently not allowed

• Public schools, public universities, federal, state, city, township owned properties

45

How Far Back In Time Can A Designer Look For Projects?

• §6511 limits the statute for filing refund claims generally to three years from the time the return was filed.

• For a calendar-year taxpayer that filed its 2008 tax return at the extended due date of Sept. 15, 2009, there are still a few months to amend and claim any projects placed in service during 2008.

• There may be an opportunity to use Rev. Proc. 2011-14 to claim the deduction for projects that were placed in service during a year when the statute is closed.

46

PLACED-IN-SERVICE ISSUES, AND IRS GUIDANCE

Eric Smith, Beene Garter

What If I Did Not Take The 179D Deduction On My Original Return?

Example: An automotive parts manufacturing company built a new 400,000-square-foot, state-of-the-art facility on Jan. 1, 2007. No 179D study was performed, and the lighting, HVAC and envelope were set up on a 39-year depreciable life. The taxpayer filed its 2007 return on Sept. 15, 2008. The company could have received the maximum deduction under Sect. 179D of $720,000 ($1.80 X 400,000) had the study been performed in 2007. Instead, it has taken $73,846 of depreciation ($720,000/39 years X 4 tax years) through 2010. The statute is closed to amend the 2007 return. Are there any options available to this company?

48

Revenue Procedure 2011-14

• Prior to Rev. Proc. 2011-14, this company would have been out of luck. The only option was to claim the deduction on an amended tax return at the time.

• §6511 generally only allows returns to be amended to claim a refund for three years after the date of filing a return.

• In our example, the automotive parts manufacturer would not have had any means to go back and take the 179D deduction, since the project was placed in service during 2007 and the statute for filing a refund claim expired on Sept. 15, 2011.

49

Revenue Procedure 2011-14 (Cont.)

• Rev. Proc. 2011-14 was issued on Jan. 10, 2011 and now makes it possible to claim a 179D deduction for years closed by statute under designated automatic accounting method change No. 152.

• This, in effect, allows a taxpayer to catch up the deduction in the current year, using a change in accounting under appendix Sect. 8.04 of the Rev. Proc. 2011-14.

• Under our original example, the 481(a) adjustment would have been a negative adjustment of $646,154 ($720,000 - $73,846).

50

Revenue Procedure 2011-14 (Cont.)

• Requirements of Rev. Proc. 2011-14

• Sect. 5.04 requires a §481(a) adjustment which, in the case of a 179D deduction, should be a negative adjustment that can be taken completely in the year of change.

• Sect. 6.02 requires that ordinarily, a Form 3115 be filed to apply for a change in accounting method. However, this Rev. Proc. allows certain changes to be made with a statement in lieu of a Form 3115. The 179D change under appendix Sect. 8.04(3) is one such change.

51

Revenue Procedure 2011-14 (Cont.)

• Requirements of Rev. Proc. 2011-14 (Cont.)

• Sect. 6.02(4) provides guidance on what is required in the statement to be filed in lieu of Form 3115. It provides that the automatic change number of 152 be included on the top of the first page, directly above the taxpayer’s name and federal EIN. It also requires a detailed description of the tax treatment of the property under the present and proposed methods of accounting.

• Also, no duplicate copy is required to be sent to the national office.

52

Revenue Procedure 2011-14 (Cont.)

• Requirements of Rev. Proc. 2011-14 (Cont.)

• Appendix Sect. 8.04(4) also requests a copy of the independent certification required under Notice 2006-52 and Notice 2008-40 be attached to the application statement.

• Sect. 7.01 provides audit protection under this Rev. Proc. except as otherwise provided.

• Appendix Sect. 8.04(5) states no audit protection is provided in connection with the 179D accounting method change.

53

Revenue Procedure 2011-14 (Cont.)

• Practical considerations

• Rev. Proc. 2011-14 is not mandatory if the return year the property is placed in service is not closed by statute. Meaning, you can choose to either amend the tax return or use the provision of Rev. Proc. 2011-14 to maximize your company’s tax benefit.

• Factors to consider:

• Tax rate in original return year vs. current year

• Carryback opportunities in original year versus current year

• Statute of limitations

54

Revenue Procedure 2011-14 (Cont.)

• Unsettled issue: What is a change in accounting?

• Under the §1.446 regulations, the accounting of an “item” is an accounting method.

• The question then becomes: Is each building an item, or should all qualifying buildings be a single item of accounting for purposes of §179D?

55

THE ROLE OF ENERGY STUDIES

Julio Gonzalez, Engineered Tax Services

Improve Building Value

Building size 1,000,000

Lighting watts/sq. ft. 1.5

Annual hours 3,500

Annual kWh 5,250,000

Cost at $0.10/kWh $525,000

% savings 30%

Annual savings $157,500

Savings per sq. ft. .157

Cost of equipment $400,000

Payback 2.5 yrs

Annual ROI 43.9%

Five-year net savings $387,000

Increase in asset value:

Increase in net operating income = Inc. asset

Capitalization rate value

Example:

$157,500 = $2,250,000

7%

57

Savings Increased With Complimentary Tax Strategies

Year Of Study 1 2 3 4 5

Cost of upgrades $ 130,000.00 $ 3,900.00 $ 3,900.00 $ 3,900.00

P/SF $ 3.25

% of total 1.30%

Cost savings w. ES* $ 20,300.00

Cost savings w.

CSS $ 185,000.00 $ 216,608.00 $ 132,210.00 $ 86,068.00 $ 80,931.00

Utility savings

(40%) $ 24,000.00 $ 24,720.00 $ 25,461.60 $ 26,225.45 $ 27,012.21

Less study cost $ 15,000.00

Totals savings $ (84,300) $ (241,328.00) $ (153,771.60) $(108,393) $ (104,043)

ROI % 158% 4042% 2897% 2767%

Payback time 0.6 0.0 0.0 0.0 0.0

* Energy saving of $58,000 @ 35% federal tax rate

58

Case Study Of Other Tax Benefits

• $450,000 IN COST TO RETROFIT THE BUILDING WITH NEW LEDs

• IN THE CASE EXAMPLE, THE OLD LIGHTING IS 5 YEARS OLD.

LET’S TAKE A PARKING STRUCTURE

59

This Will Provide …

EPAct WILL PROVIDE $0.60 PER SQUARE FOOT IN

TAX DEDUCTION

FOR THIS PROPERTY, THAT IS:

$300,000

60

Abandonment Deduction

Abandonment: When assets are retired or removed, they are

taken off a company’s books (when you re-light a facility, you

essentially remove the old lighting).

This tax incentive can be substantial!

61

Accelerated Deduction

WHEN YOU INSTALL THE NEW LED LIGHTING, YOU

ABANDONED OR REMOVED THE OLD CONVENTIONAL

LIGHTING.

THE LIGHTING HAD AN ESTIMATED CURRENT

NET BOOK VALUE OF:

$75,322 62

Accelerated Deduction (Cont.)

THE VALUE OF A CONVENTIONAL SYSTEM AND THE NEW

LED SYSTEM IN THE AMOUNT YOU CAN DEPRECIATE,

AND IN THIS CASE IN ONE YEAR

The VALUE IS:

$125,000

63

Total Tax Deductions

Deductions/depreciation

EPAct: $165,000

1245 property: $125,000

Abandonment: $ 75,322

Total: $365,322 64

Converted To N.A.T.

Net after tax

Remember: State benefits can equal or exceed the federal benefits, for EPAct.

Total deductions after-tax (California, as an example)

Deductions/Depreciation Federal State

EPAct $165,000 $57,750 $ -

1245 property $125,000 $43,750 $12,500

Abandonment $75,322 $26,363 $ 7,532

TOTAL $365,322 $127,863 $20,032

$147,892 net after tax

65

Tax Reduced

Your $450,000 is reduced by $147,892, to:

And, this does not include other available rebates or discounts

$302,108

66

Clients Results Explained

Capital cost $124,000

N.A.T benefits $77,700

Cost year one $46,300

1st-year saving on energy $53,000

Consider the ROI going from 2.3 years to 9

months

67

Case Example

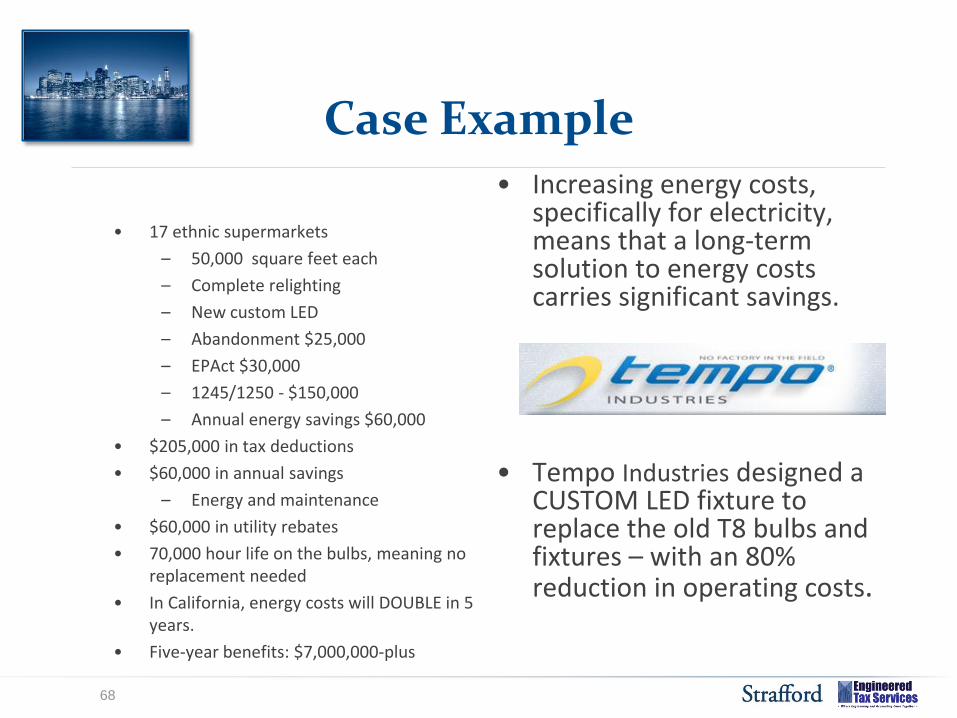

• 17 ethnic supermarkets

– 50,000 square feet each

– Complete relighting

– New custom LED

– Abandonment $25,000

– EPAct $30,000

– 1245/1250 - $150,000

– Annual energy savings $60,000

• $205,000 in tax deductions

• $60,000 in annual savings

– Energy and maintenance

• $60,000 in utility rebates

• 70,000 hour life on the bulbs, meaning no replacement needed

• In California, energy costs will DOUBLE in 5 years.

• Five-year benefits: $7,000,000-plus

• Increasing energy costs, specifically for electricity, means that a long-term solution to energy costs carries significant savings.

• Tempo Industries designed a CUSTOM LED fixture to replace the old T8 bulbs and fixtures – with an 80% reduction in operating costs.

68

Case Example (Cont.)

• The benefits from EPAct and abandonment were sufficient to turn the ROI on this project from thirty months to just under one year.

• Our partners at XYZ Company worked with the client to achieve the excellent return on investment.

Republic National Distributing Co.

– 250,000 –square-foot warehouse – Complete relighting – Cost $140,000 – EPAct $140,000 – Abandonment $90,000 – Annual energy savings $60,000

• $230,000 in tax deductions • $60,000 in annual energy savings • 1st-year NAT: $500-plus • Five-year benefits: $300,500-plus

– $450,000-plus with the increased cost of energy

– ZERO net cost the first year!

69