q1 2017 waterloo region office market report

TRANSCRIPT

Research & Forecast Report

WATERLOO REGIONOFFICE First Quarter 2017

2 Research & Forecast Report | First Quarter 2017 | Waterloo Region / Office | Colliers International

Market Summaries

City of Cambridge ..........................................................................................................4 City of Kitchener ..................................................................................................... 5 City of Waterloo ...................................................................................................... 6

Glossary ............................................................................................................................... 7

Table of Contents

3 Research & Forecast Report | First Quarter 2017 | Waterloo Region / Office | Colliers International

Waterloo Region Market Overview

The Waterloo Region office leasing market has seen many showings, but few leases over the past two quarters. A number of companies have been actively looking to fulfill their space requirements, but only a few have made firm commitments. New or newly renovated buildings are generating the most activity and attracting tenancies. There is significant demand for Class A office space; many companies insist that their primary real estate requirement is high quality office space.

The impact on the regional market is demand for new development. New development continues to pursue and secure tenants for currently un-built projects. The long-term outcome of this will be an overall increase in the quality of office space in the market along with a very competitive market to backfill space that is being left by exiting companies.

The City of Waterloo continues to attract companies looking for high quality buildings, big blocks of space, and favourable demographics. Waterloo has a striking advantage for large blocks of available space and high quality buildings over Kitchener and Cambridge.

The City of Kitchener continues to be the busiest node in the Region with the highest number of transactions, however tenant demand continues to be for new or newly updated space. The downtown market’s competitive advantage over the rest of the Region is its broad

Market IndicatorsRelative to prior period

Waterloo RegionQ4 2016

Waterloo RegionQ1 2017 Trend

VACANCY 15.34% 15.66%

NET ABSORPTION -70,283 -28,708

CONSTRUCTION 363,637 227,912

RENTAL RATE* $13.32 $13.54

* Rental rates for current quarter are asking weighted averages for all submarkets.

selection of prices, sizes, types of space, and overall quality. The tech sector is robust, and with the current political climate in the United States, Canadian companies and locations will benefit from the new “push” factors. The light rail transit tracks are largely completed and there is a sense of anticipation as the downtown community awaits the arrival and operation of the new rail cars.

The Cambridge market continues to show positive signs. For several quarters, the lack of Class A space available in the City of Cambridge has been noted, and in span of this bi-annual report, a large piece of Class A space has come to market and leased before the existing tenant has vacated the premises. Demand for high quality office space along the Highway 401 corridor is present and new vacancies will continue to lease as they come available.

Investment Market

There were two office investment sales within the last two quarters: 236-264 Victoria Street North (53,960 square feet mixed-use property consisting of a fitness centre and a 22,360 square feet fully leased office building) which sold for $11,000,000. The DREAM portfolio, consisting of eight buildings, sold in December 2016 for $138,000,000 or $128 per square foot. Due to a high vacancy rate within the portfolio, the cap rate was uncharacteristically high.

Regional Historical Performance and Forecast

(600,000)

(500,000)

(400,000)

(300,000)

(200,000)

(100,000)

0

100,000

200,000

300,000

400,000

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

2012

Q1

2012

Q2

2012

Q3

2012

Q4

2013

Q1

2013

Q2

2013

Q3

2013

Q4

2014

Q1

2014

Q2

2014

Q3

2014

Q4

2015

Q1

2015

Q2

2015

Q3

2015

Q4

2016

Q1

2016

Q2

2016

Q3

2016

Q4

2017

Q1

2017

Q2

2017

Q3

2017

Q4

2018

Q1

Net Absorption New Supply Vacancy Rate

4 Research & Forecast Report | First Quarter 2017 | Waterloo Region / Office | Colliers International

Notable Lease TransactionsTENANT NAME & ADDRESS TYPE APPROXIMATE

SIZE (SF)

1. Undisclosed73 Water Street North Headlease 32,240

2. exactEarth Inc.260 Holiday Inn Drive Headlease 8,961

1

Notable Lease Notable Sale New Supply

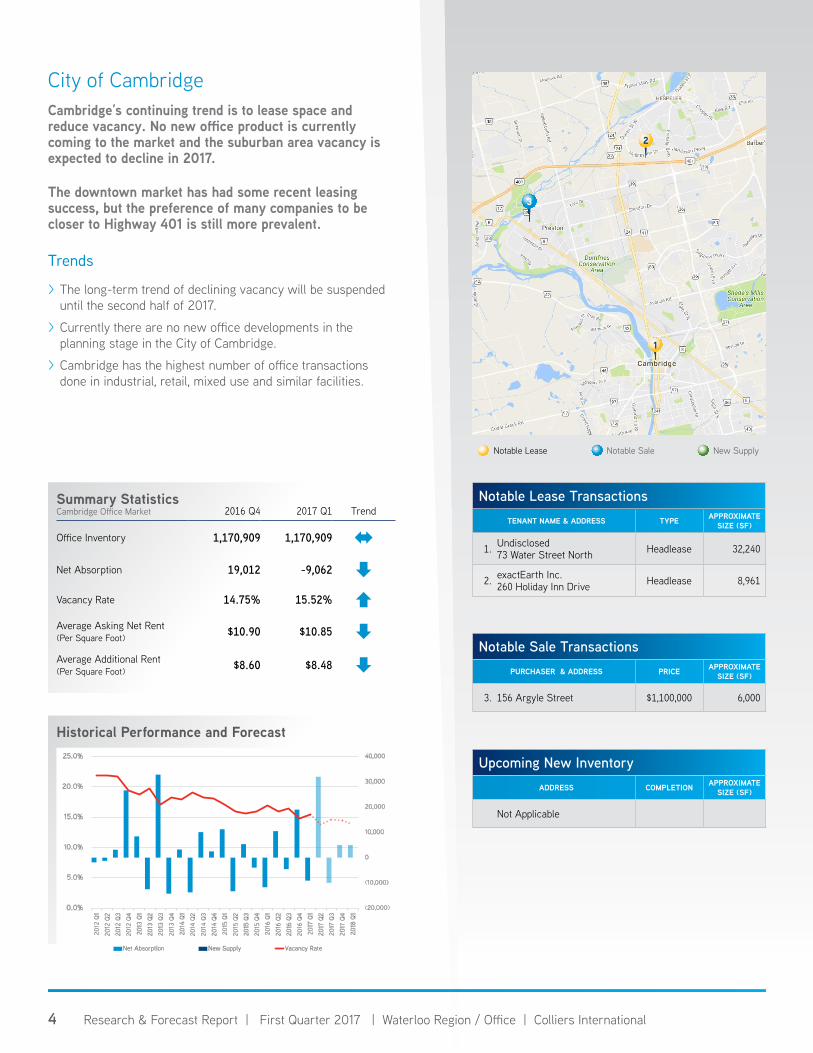

City of CambridgeCambridge’s continuing trend is to lease space and reduce vacancy. No new office product is currently coming to the market and the suburban area vacancy is expected to decline in 2017.

The downtown market has had some recent leasing success, but the preference of many companies to be closer to Highway 401 is still more prevalent.

Trends

> The long-term trend of declining vacancy will be suspended until the second half of 2017.

> Currently there are no new office developments in the planning stage in the City of Cambridge.

> Cambridge has the highest number of office transactions done in industrial, retail, mixed use and similar facilities.

Notable Sale TransactionsPURCHASER & ADDRESS PRICE APPROXIMATE

SIZE (SF)

3. 156 Argyle Street $1,100,000 6,000

Upcoming New InventoryADDRESS COMPLETION APPROXIMATE

SIZE (SF)

Not Applicable

Summary Statistics Cambridge Office Market 2016 Q4 2017 Q1 Trend

Office Inventory 1,170,909 1,170,909

Net Absorption 19,012 -9,062

Vacancy Rate 14.75% 15.52%

Average Asking Net Rent(Per Square Foot) $10.90 $10.85

Average Additional Rent(Per Square Foot) $8.60 $8.48

Historical Performance and Forecast

(20,000)

(10,000)

0

10,000

20,000

30,000

40,000

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

2012

Q1

2012

Q2

2012

Q3

2012

Q4

2013

Q1

2013

Q2

2013

Q3

2013

Q4

2014

Q1

2014

Q2

2014

Q3

2014

Q4

2015

Q1

2015

Q2

2015

Q3

2015

Q4

2016

Q1

2016

Q2

2016

Q3

2016

Q4

2017

Q1

2017

Q2

2017

Q3

2017

Q4

2018

Q1

Net Absorption New Supply Vacancy Rate

2

3

5 Research & Forecast Report | First Quarter 2017 | Waterloo Region / Office | Colliers International

Notable Lease TransactionsTENANT NAME & ADDRESS TYPE APPROXIMATE

SIZE (SF)

1. Atomic Labs119 King Street West Sublease 10,940

2. Overlap Associates305 King Street West Headlease 6,439

3. Laurentian Bank305 King Street West Headlease 5,520

Notable Lease Notable Sale New Supply

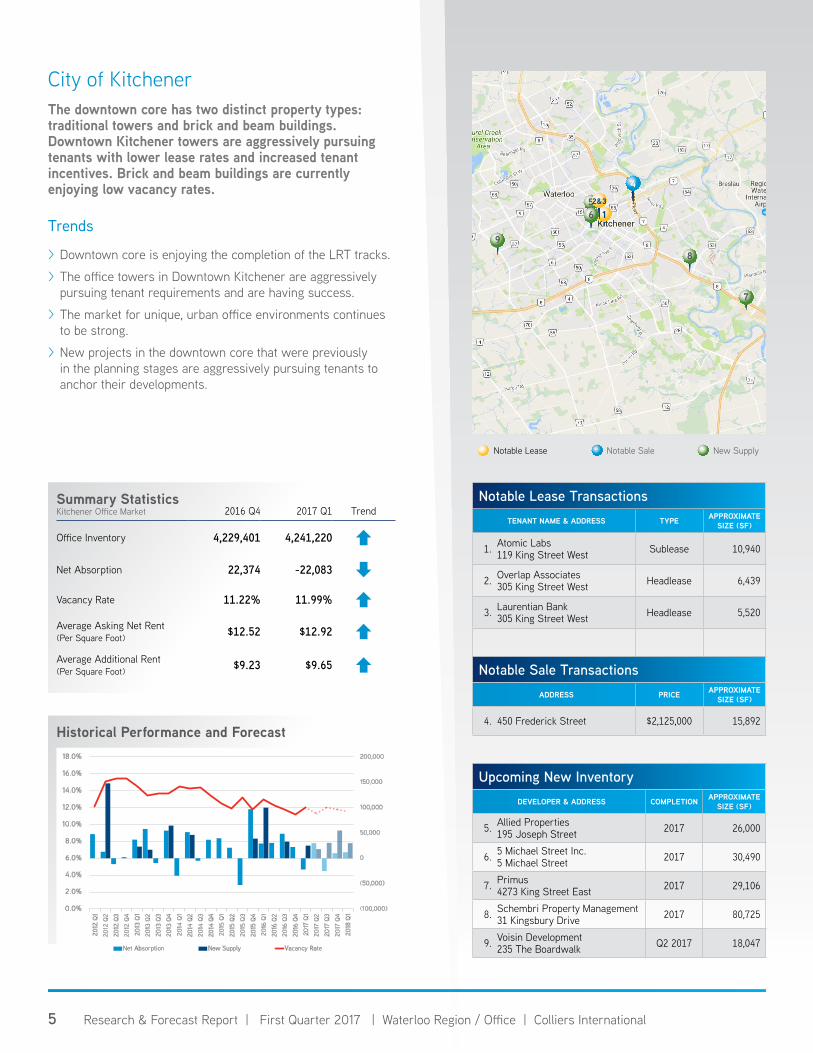

City of KitchenerThe downtown core has two distinct property types: traditional towers and brick and beam buildings. Downtown Kitchener towers are aggressively pursuing tenants with lower lease rates and increased tenant incentives. Brick and beam buildings are currently enjoying low vacancy rates.

Trends

> Downtown core is enjoying the completion of the LRT tracks.

> The office towers in Downtown Kitchener are aggressively pursuing tenant requirements and are having success.

> The market for unique, urban office environments continues to be strong.

> New projects in the downtown core that were previously in the planning stages are aggressively pursuing tenants to anchor their developments.

Summary Statistics Kitchener Office Market 2016 Q4 2017 Q1 Trend

Office Inventory 4,229,401 4,241,220

Net Absorption 22,374 -22,083

Vacancy Rate 11.22% 11.99%

Average Asking Net Rent(Per Square Foot) $12.52 $12.92

Average Additional Rent(Per Square Foot) $9.23 $9.65 Notable Sale Transactions

ADDRESS PRICE APPROXIMATE SIZE (SF)

4. 450 Frederick Street $2,125,000 15,892

Upcoming New InventoryDEVELOPER & ADDRESS COMPLETION APPROXIMATE

SIZE (SF)

5. Allied Properties195 Joseph Street 2017 26,000

6. 5 Michael Street Inc.5 Michael Street 2017 30,490

7. Primus4273 King Street East 2017 29,106

8. Schembri Property Management31 Kingsbury Drive 2017 80,725

9. Voisin Development235 The Boardwalk Q2 2017 18,047

Historical Performance and Forecast

(100,000)

(50,000)

0

50,000

100,000

150,000

200,000

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

2012

Q1

2012

Q2

2012

Q3

2012

Q4

2013

Q1

2013

Q2

2013

Q3

2013

Q4

2014

Q1

2014

Q2

2014

Q3

2014

Q4

2015

Q1

2015

Q2

2015

Q3

2015

Q4

2016

Q1

2016

Q2

2016

Q3

2016

Q4

2017

Q1

2017

Q2

2017

Q3

2017

Q4

2018

Q1

Net Absorption New Supply Vacancy Rate

8

51

7

9

4

62&3

6 Research & Forecast Report | First Quarter 2017 | Waterloo Region / Office | Colliers International

Notable Lease Notable Sale New Supply

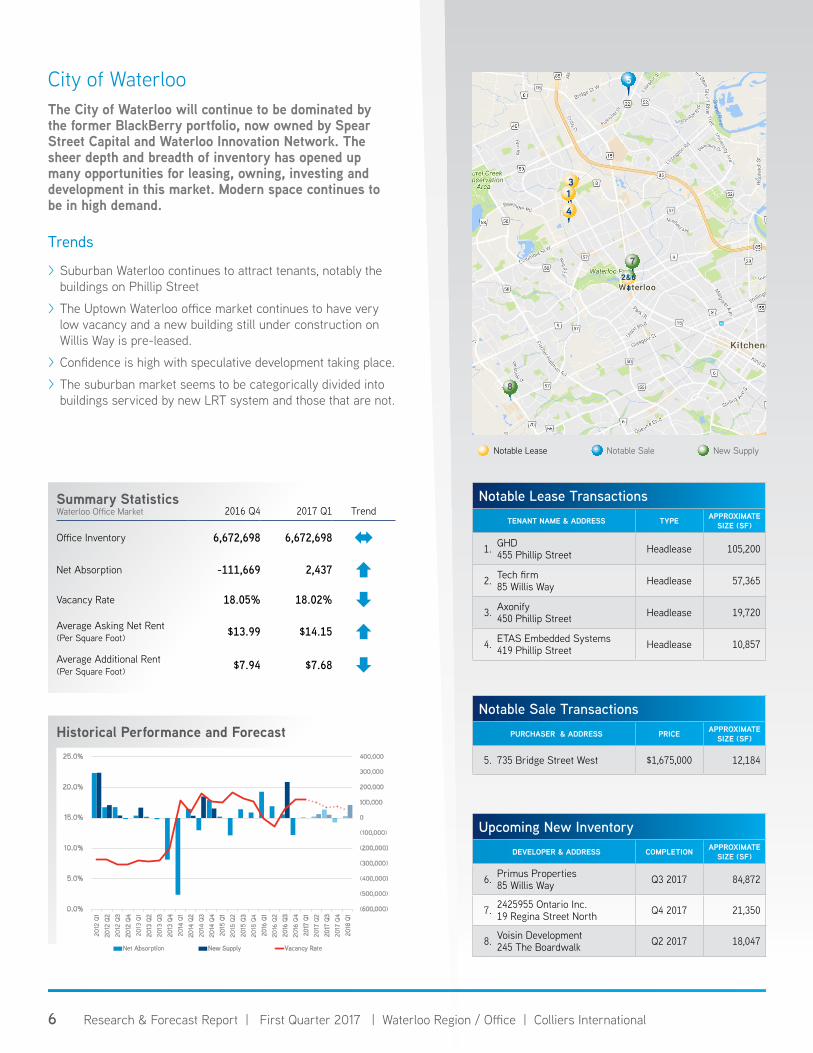

City of WaterlooThe City of Waterloo will continue to be dominated by the former BlackBerry portfolio, now owned by Spear Street Capital and Waterloo Innovation Network. The sheer depth and breadth of inventory has opened up many opportunities for leasing, owning, investing and development in this market. Modern space continues to be in high demand.

Trends

> Suburban Waterloo continues to attract tenants, notably the buildings on Phillip Street

> The Uptown Waterloo office market continues to have very low vacancy and a new building still under construction on Willis Way is pre-leased.

> Confidence is high with speculative development taking place.

> The suburban market seems to be categorically divided into buildings serviced by new LRT system and those that are not.

Summary Statistics Waterloo Office Market 2016 Q4 2017 Q1 Trend

Office Inventory 6,672,698 6,672,698

Net Absorption -111,669 2,437

Vacancy Rate 18.05% 18.02%

Average Asking Net Rent(Per Square Foot) $13.99 $14.15

Average Additional Rent(Per Square Foot) $7.94 $7.68

Historical Performance and Forecast

(600,000)

(500,000)

(400,000)

(300,000)

(200,000)

(100,000)

0

100,000

200,000

300,000

400,000

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

2012

Q1

2012

Q2

2012

Q3

2012

Q4

2013

Q1

2013

Q2

2013

Q3

2013

Q4

2014

Q1

2014

Q2

2014

Q3

2014

Q4

2015

Q1

2015

Q2

2015

Q3

2015

Q4

2016

Q1

2016

Q2

2016

Q3

2016

Q4

2017

Q1

2017

Q2

2017

Q3

2017

Q4

2018

Q1

Net Absorption New Supply Vacancy Rate

Notable Lease TransactionsTENANT NAME & ADDRESS TYPE APPROXIMATE

SIZE (SF)

1. GHD455 Phillip Street Headlease 105,200

2. Tech firm 85 Willis Way Headlease 57,365

3. Axonify450 Phillip Street Headlease 19,720

4. ETAS Embedded Systems419 Phillip Street Headlease 10,857

Notable Sale TransactionsPURCHASER & ADDRESS PRICE APPROXIMATE

SIZE (SF)

5. 735 Bridge Street West $1,675,000 12,184

Upcoming New InventoryDEVELOPER & ADDRESS COMPLETION APPROXIMATE

SIZE (SF)

6. Primus Properties85 Willis Way Q3 2017 84,872

7. 2425955 Ontario Inc.19 Regina Street North Q4 2017 21,350

8. Voisin Development245 The Boardwalk Q2 2017 18,047

5

3

7

8

1

2&6

4

7 Research & Forecast Report | First Quarter 2017 | Waterloo Region / Office | Colliers International

Glossary

Weighted Average Asking Net Rent The dollar amount requested by landlords for direct available space, not including subleases, expressed in dollars per square foot per year.

Availability The amount of available space and available space to be delivered to the market within six months, divided by the market’s inventory base including those future deliveries. Available space is space that is available for lease, and may or may not be vacant.

Net Absorption The net change in physically occupied space between the current measurement period, and the last measurement period. It can be either positive or negative.

Vacancy The amount of vacant space divided by the building inventory base. Vacant space is physically unoccupied, and it may or may not be available for lease or sublease. This is physical vacancy. It is not determined whether a tenant is paying rent on the space.

Copyright © 2017 Colliers International.

The information contained herein has been obtained from sources deemed reliable. While every reasonable effort has been made to ensure its accuracy, we cannot guarantee it. No responsibility is assumed for any inaccuracies. Readers are encouraged to consult their professional advisors prior to acting on any of the material contained in this report.

About Colliers International Group Inc.

Colliers International Group Inc. is an industry leading global real estate services company with more than 15,000 skilled professionals operating in 68 countries. With an enterprising culture and significant employee ownership, Colliers professionals provide a full range of services to real estate occupiers, owners and investors worldwide. Services include strategic advice and execution for property sales, leasing and finance; global corporate solutions; property, facility and project management; workplace solutions; appraisal, valuation and tax consulting; customized research; and thought leadership consulting.

Colliers professionals think differently, share great ideas and offer thoughtful and innovative advice that help clients accelerate their success. Colliers has been ranked among the top 100 outsourcing firms by the International Association of Outsourcing Professionals’ Global Outsourcing for 11 consecutive years, more than any other real estate services firm.

colliers.com

396 offices in 68 countries on 6 continentsUnited States: 153 Canada: 29 Latin America: 24 Asia Pacific: 79 EMEA: 111

$2.6BUS* in annual revenue

2Bsquare feet under management

15,000professionals and staff

*Based on 2016 results

MARKET CONTACT:Serguei Kaminski Market Intelligence Coordinator | Waterloo Region+1 519 904 [email protected]

REGIONAL AUTHORS:John Lind | Senior Sales RepresentativeKarl Innanen, CCIM | Managing Director, BrokerSerguei Kaminski | Market Intelligence CoordinatorJennie Ross | Client Project Coordinator

Colliers International | Waterloo Region305 King Street West, Suite 606Kitchener, ON N2G 1B9 | Canada

+1 519 570 1330