q1 2016 presentation - telia company · • estonia impacted by higher marketing costs ... •...

TRANSCRIPT

1

JOHAN DENNELIND,

PRESIDENT & CEO

INTERIM REPORT

JANUARY – MARCH 2016 Q1

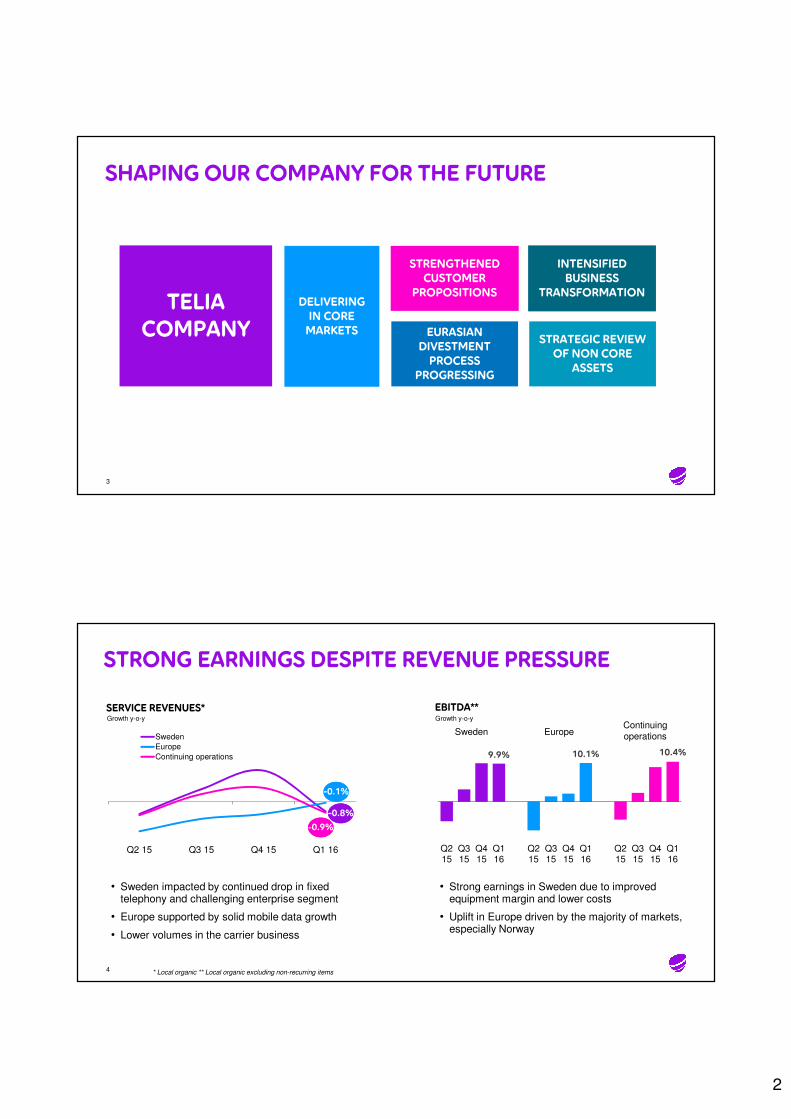

SUMMARY Q1 2016

2

S E RV I C E R E VENUE GROWTH

EB I TDA * G ROWTH

TOTA L F R E E CA SH F LOW

Reported -0.7%Organic -0.9%

Reported +10.4%Organic +10.4%

SEK 2.1 billion-16.0%

All figures refer to continuing operations *Excluding non-recurring items

2

SHAPING OUR COMPANY FOR THE FUTURE

3

TELIA

COMPANYSTRATEGIC REVIEW

OF NON CORE

ASSETS

INTENSIFIED

BUSINESS

TRANSFORMATION

EURASIAN

DIVESTMENT

PROCESS

PROGRESSING

STRENGTHENED

CUSTOMER

PROPOSITIONSDELIVERING

IN CORE

MARKETS

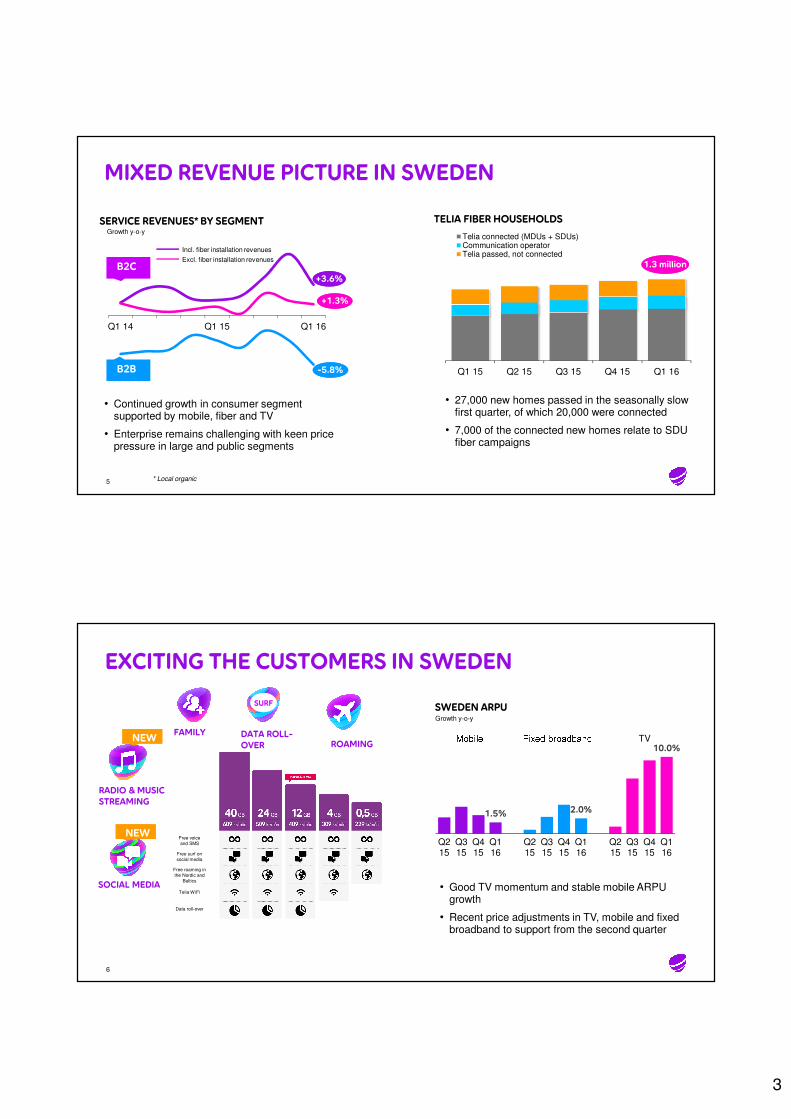

9.9% 10.1% 10.4%

Q215

Q315

Q415

Q116

Q215

Q315

Q415

Q116

Q215

Q315

Q415

Q116

4

Sweden EuropeContinuing

operations

Q2 15 Q3 15 Q4 15 Q1 16

Sweden

Europe

Continuing operations

* Local organic ** Local organic excluding non-recurring items

• Sweden impacted by continued drop in fixed telephony and challenging enterprise segment

• Europe supported by solid mobile data growth

• Lower volumes in the carrier business

• Strong earnings in Sweden due to improved equipment margin and lower costs

• Uplift in Europe driven by the majority of markets, especially Norway

STRONG EARNINGS DESPITE REVENUE PRESSURE

SERVICE REVENUES* EBITDA**Growth y-o-y Growth y-o-y

-0.8%-0.8%

-0.9%-0.9%

-0.1%-0.1%

3

Q1 15 Q2 15 Q3 15 Q4 15 Q1 16

Telia connected (MDUs + SDUs)Communication operatorTelia passed, not connected

MIXED REVENUE PICTURE IN SWEDEN

5

Q1 14 Q1 15 Q1 16

+1.3%+1.3%

-5.8%-5.8%

+3.6%+3.6%

B2B

B2C

• Continued growth in consumer segment supported by mobile, fiber and TV

• Enterprise remains challenging with keen price pressure in large and public segments

SERVICE REVENUES* BY SEGMENT

* Local organic

Excl. fiber installation revenues

Incl. fiber installation revenues

1.3 million1.3 million

TELIA FIBER HOUSEHOLDS

• 27,000 new homes passed in the seasonally slow first quarter, of which 20,000 were connected

• 7,000 of the connected new homes relate to SDU fiber campaigns

Growth y-o-y

EXCITING THE CUSTOMERS IN SWEDEN

6

SWEDEN ARPU

1.5% 2.0%

10.0%

Q215

Q315

Q415

Q116

Q215

Q315

Q415

Q116

Q215

Q315

Q415

Q116

TV

• Good TV momentum and stable mobile ARPU growth

• Recent price adjustments in TV, mobile and fixed broadband to support from the second quarter

Growth y-o-y

FAMILY DATA ROLL-

OVER ROAMING

SOCIAL MEDIA

RADIO & MUSIC

STREAMING

SURF

NEW

Free voice

and SMS

Free surf on

social media

Free roaming in

the Nordic and

Baltics

Telia WiFi

Data roll-over

NEW

4

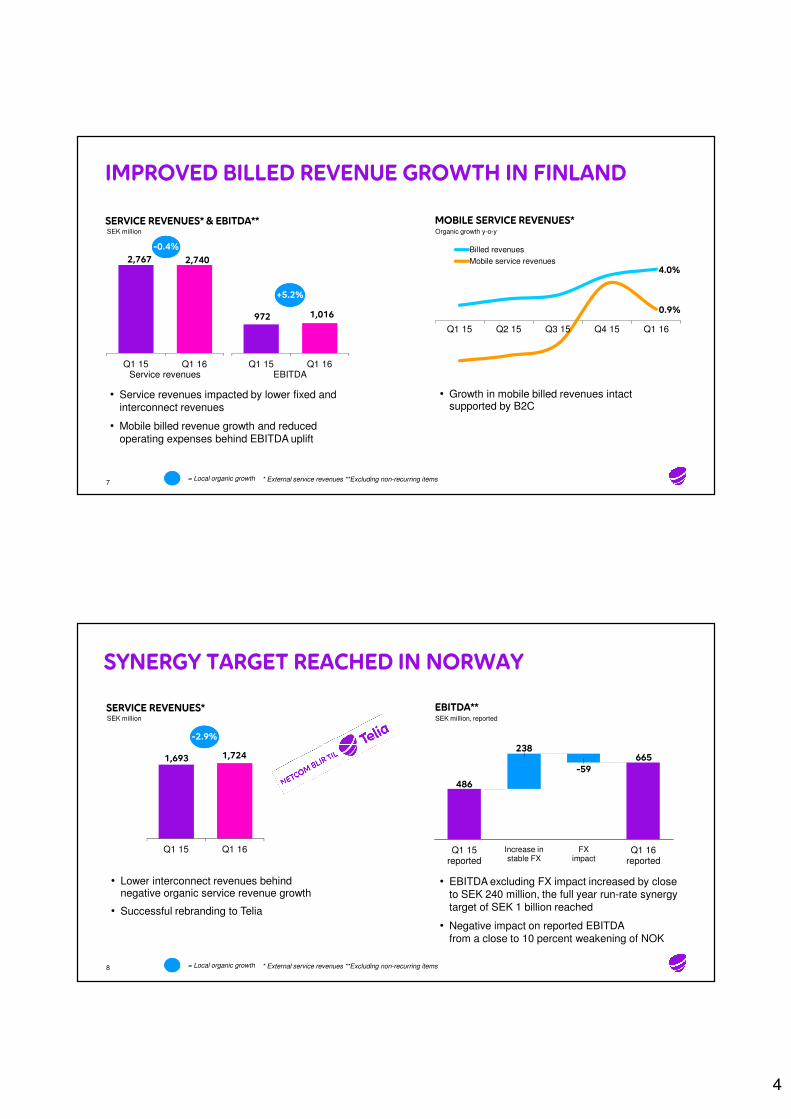

2,767 2,740

Q1 15 Q1 16

-0.4%-0.4%

4.0%

0.9%

Q1 15 Q2 15 Q3 15 Q4 15 Q1 16

Billed revenues

Mobile service revenues

IMPROVED BILLED REVENUE GROWTH IN FINLAND

• Growth in mobile billed revenues intact supported by B2C

7

• Service revenues impacted by lower fixed and interconnect revenues

• Mobile billed revenue growth and reduced operating expenses behind EBITDA uplift

* External service revenues **Excluding non-recurring items

972 1,016

Q1 15 Q1 16

+5.2%+5.2%

Service revenues EBITDA

= Local organic growth

MOBILE SERVICE REVENUES*SERVICE REVENUES* & EBITDA**SEK million Organic growth y-o-y

1,693 1,724

Q1 15 Q1 16

SYNERGY TARGET REACHED IN NORWAY

• Lower interconnect revenues behind negative organic service revenue growth

• Successful rebranding to Telia

8

• EBITDA excluding FX impact increased by close to SEK 240 million, the full year run-rate synergy target of SEK 1 billion reached

• Negative impact on reported EBITDA from a close to 10 percent weakening of NOK

-2.9%-2.9%

* External service revenues **Excluding non-recurring items = Local organic growth

665238

486

FXimpact

Increase in stable FX

Q1 15reported

-59

Q1 16reported

SERVICE REVENUES* EBITDA**SEK million SEK million, reported

5

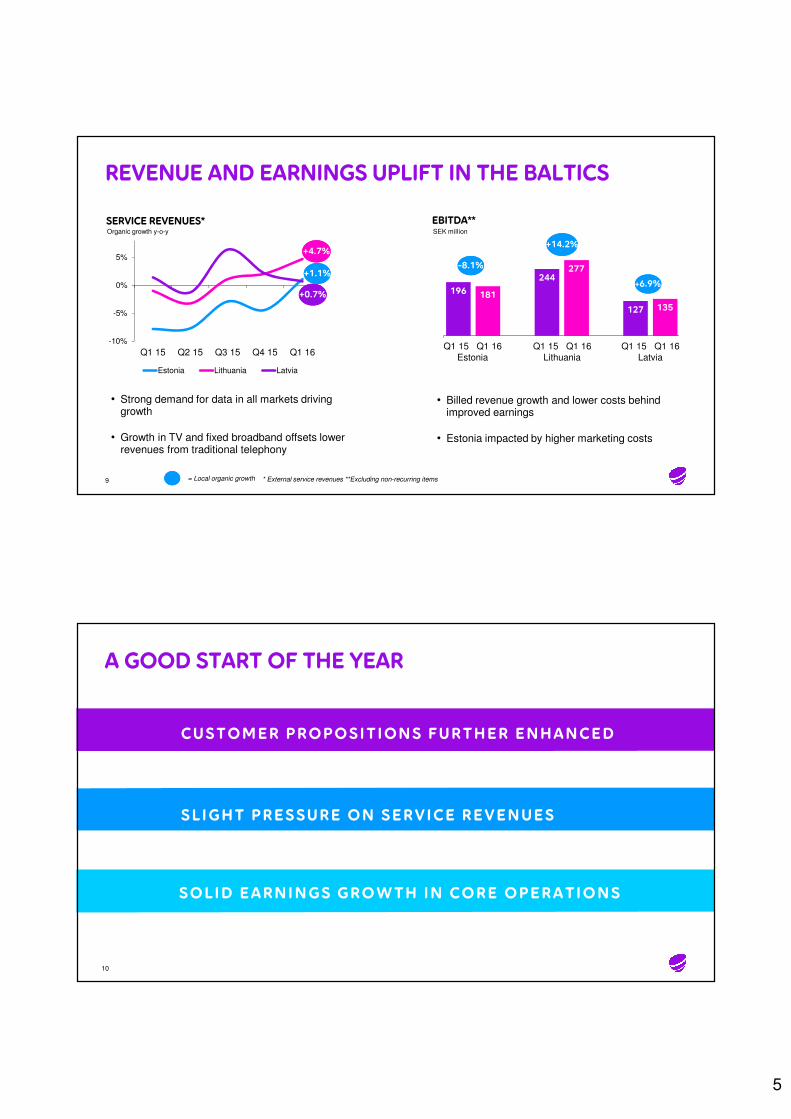

9

196 181

244277

127 135

-10%

-5%

0%

5%

Q1 15 Q2 15 Q3 15 Q4 15 Q1 16

Estonia Lithuania Latvia

• Strong demand for data in all markets driving growth

• Growth in TV and fixed broadband offsets lower revenues from traditional telephony

Q1 15 Q1 16

Lithuania

Q1 15 Q1 16

Latvia

+14.2%+14.2%

Q1 15 Q1 16

Estonia

• Billed revenue growth and lower costs behind improved earnings

• Estonia impacted by higher marketing costs

* External service revenues **Excluding non-recurring items = Local organic growth

REVENUE AND EARNINGS UPLIFT IN THE BALTICS

EBITDA**

-8.1%-8.1%

+6.9%+6.9%

Organic growth y-o-y

SERVICE REVENUES*SEK million

+0.7%+0.7%

+4.7%+4.7%

+1.1%+1.1%

A GOOD START OF THE YEAR

10

CUSTOMER PROPOSIT IONS FURTHER ENHANCED

SL IGHT PRESSURE ON SERV ICE REVENUES

SOLID EARNINGS GROWTH IN CORE OPERATIONS

6

SAVE THE DATE JUNE 21, 2016

11

ANALYST AND INVESTOR BRIEFING IN STOCKHOLM - FOCUS ON TELIA SWEDEN

CHRISTIAN LUIGA,

SENIOR VICE PRESIDENT & CFO

INTERIM REPORT

JANUARY – MARCH 2016 Q1

7

NET SALES DECLINE DUE TO FIXED AND EQUIPMENT

NET SALES* EQUIPMENT SALES**

* Local organic ** Reported currency

• Mobile growth impacted by lower interconnect

• Traditional telephony decline only partly compensated by fiber installation revenues, TV and fixed broadband

EquipmentOtherservice

revenues

Fixedservice

revenues

Mobile service

revenues

Q1 15

-1.1%

Q1 16-40%

-20%

0%

20%

40%

Q1 14 Q1 15 Q1 16

Sweden Europe

• Equipment sales decline in Sweden due to lack of major handset releases

• Still equipment sales growth in Europe due to successful Christmas campaign in Spain and continued strong growth in Latvia

Growth y-o-y Growth y-o-y

13

EBITDA GROWTH SUPPORTED BY LOWER COSTS

14

EBITDA*Growth y-o-y

OtherEurope Q1 16SwedenQ1 15

+10.4%

• Sweden supported by improved sales mix together with lower resource and field maintenance costs

• Improvements in Europe driven by Norway and reduced resource costs in the Nordics

10.4%

Q1 15 Q2 15 Q3 15 Q4 15 Q1 16

EBITDA*Growth y-o-y

• Comparisons to become gradually tougher throughout the year

• Main challenges remains the B2B segment primarily in Sweden and Finland

* Local organic, excluding non-recurring items

8

15

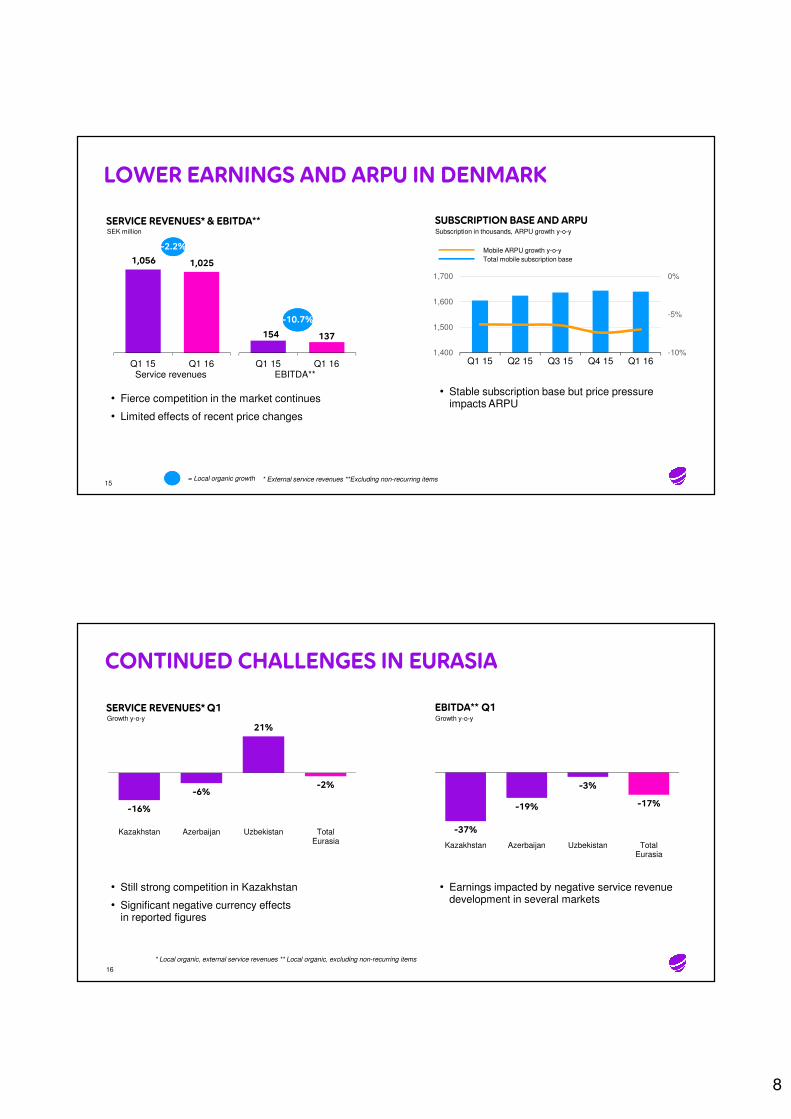

1,056 1,025

Q1 15 Q1 16

-2.2%-2.2%

154 137

Q1 15 Q1 16

-10.7%-10.7%

Service revenues EBITDA**

-10%

-5%

0%

1,400

1,500

1,600

1,700

Q1 15 Q2 15 Q3 15 Q4 15 Q1 16

• Fierce competition in the market continues

• Limited effects of recent price changes

Mobile ARPU growth y-o-y

Total mobile subscription base

• Stable subscription base but price pressure impacts ARPU

LOWER EARNINGS AND ARPU IN DENMARK

SUBSCRIPTION BASE AND ARPUSERVICE REVENUES* & EBITDA**SEK million Subscription in thousands, ARPU growth y-o-y

* External service revenues **Excluding non-recurring items = Local organic growth

CONTINUED CHALLENGES IN EURASIA

• Still strong competition in Kazakhstan

• Significant negative currency effects in reported figures

-16%

-6%

21%

-2%

Kazakhstan Azerbaijan Uzbekistan TotalEurasia

16

* Local organic, external service revenues ** Local organic, excluding non-recurring items

• Earnings impacted by negative service revenue development in several markets

-37%

-19%

-3%

-17%

Kazakhstan Azerbaijan Uzbekistan TotalEurasia

SERVICE REVENUES* Q1 EBITDA** Q1Growth y-o-y Growth y-o-y

9

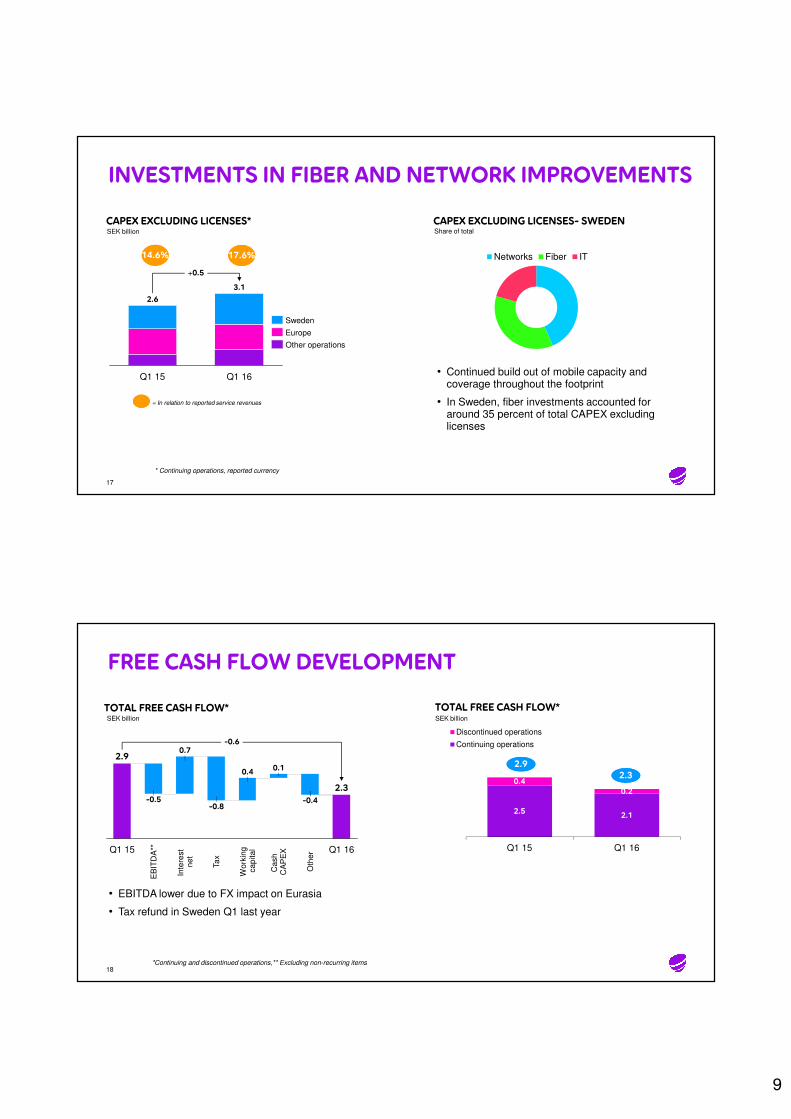

INVESTMENTS IN FIBER AND NETWORK IMPROVEMENTS

17

2.6

3.1

Q1 16

+0.5

Q1 15

Other operations

Europe

Sweden

• Continued build out of mobile capacity and coverage throughout the footprint

• In Sweden, fiber investments accounted for around 35 percent of total CAPEX excluding licenses

= In relation to reported service revenues

CAPEX EXCLUDING LICENSES*SEK billion

14.6%14.6% 17.6%17.6%

* Continuing operations, reported currency

Networks Fiber IT

CAPEX EXCLUDING LICENSES- SWEDENShare of total

FREE CASH FLOW DEVELOPMENT

• EBITDA lower due to FX impact on Eurasia

• Tax refund in Sweden Q1 last year

*Continuing and discontinued operations,** Excluding non-recurring items 18

-0.4

Oth

er

0.1

Wo

rkin

gca

pita

l

0.4

Ta

x

-0.8

Inte

rest

ne

t

0.7

EB

ITD

A**

-0.5

Q1 15

2.9

Q1 16

2.3

Ca

sh

C

AP

EX

-0.6

2.52.1

0.4

0.2

Q1 15 Q1 16

Discontinued operations

Continuing operations

2.32.3

2.92.9

TOTAL FREE CASH FLOW* TOTAL FREE CASH FLOW*SEK billion SEK billion

10

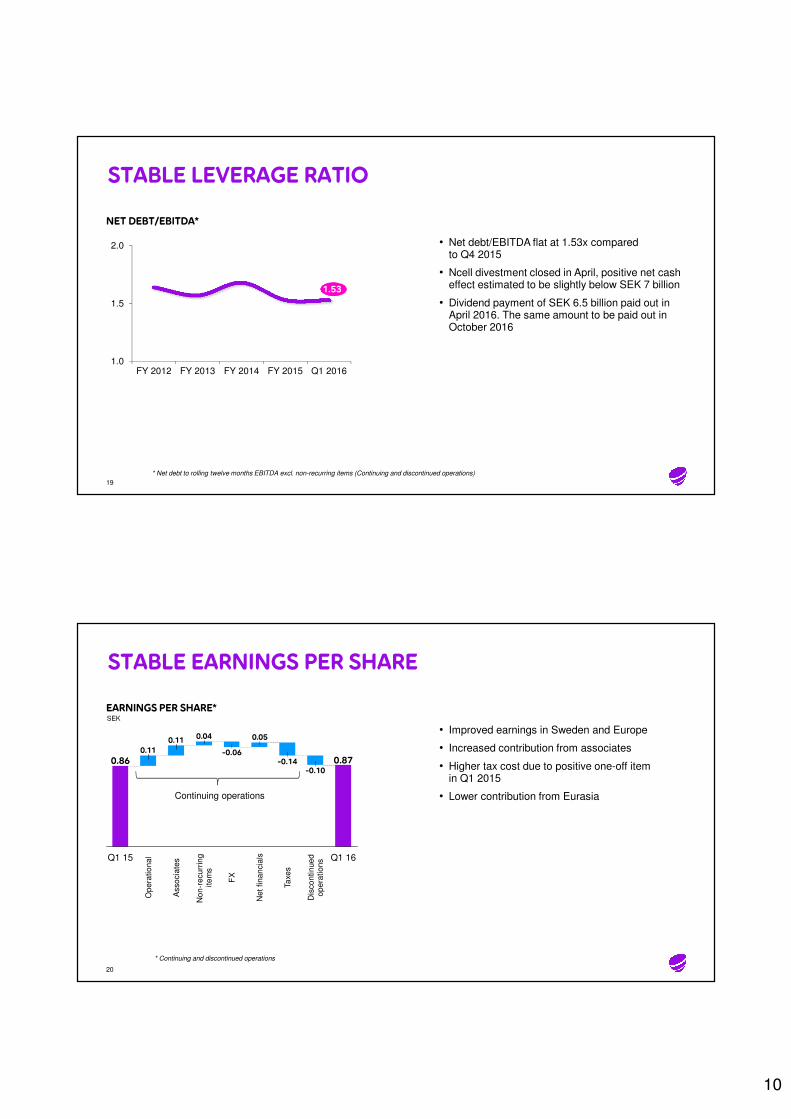

STABLE LEVERAGE RATIO

19

* Net debt to rolling twelve months EBITDA excl. non-recurring items (Continuing and discontinued operations)

• Net debt/EBITDA flat at 1.53x compared to Q4 2015

• Ncell divestment closed in April, positive net cash effect estimated to be slightly below SEK 7 billion

• Dividend payment of SEK 6.5 billion paid out in April 2016. The same amount to be paid out in October 2016

NET DEBT/EBITDA*

1.53

1.0

1.5

2.0

FY 2012 FY 2013 FY 2014 FY 2015 Q1 2016

STABLE EARNINGS PER SHARE

20

0.050.040.11

0.11

0.870.86

Dis

co

ntin

ue

do

pe

ratio

ns

-0.10

Ta

xe

s

-0.14

Ne

t fin

an

cia

ls

FX

-0.06

No

n-r

ecu

rrin

g

ite

ms

Asso

cia

tes Q1 16

Op

era

tio

nalQ1 15

* Continuing and discontinued operations

Continuing operations

• Improved earnings in Sweden and Europe

• Increased contribution from associates

• Higher tax cost due to positive one-off item in Q1 2015

• Lower contribution from Eurasia

EARNINGS PER SHARE*SEK

11

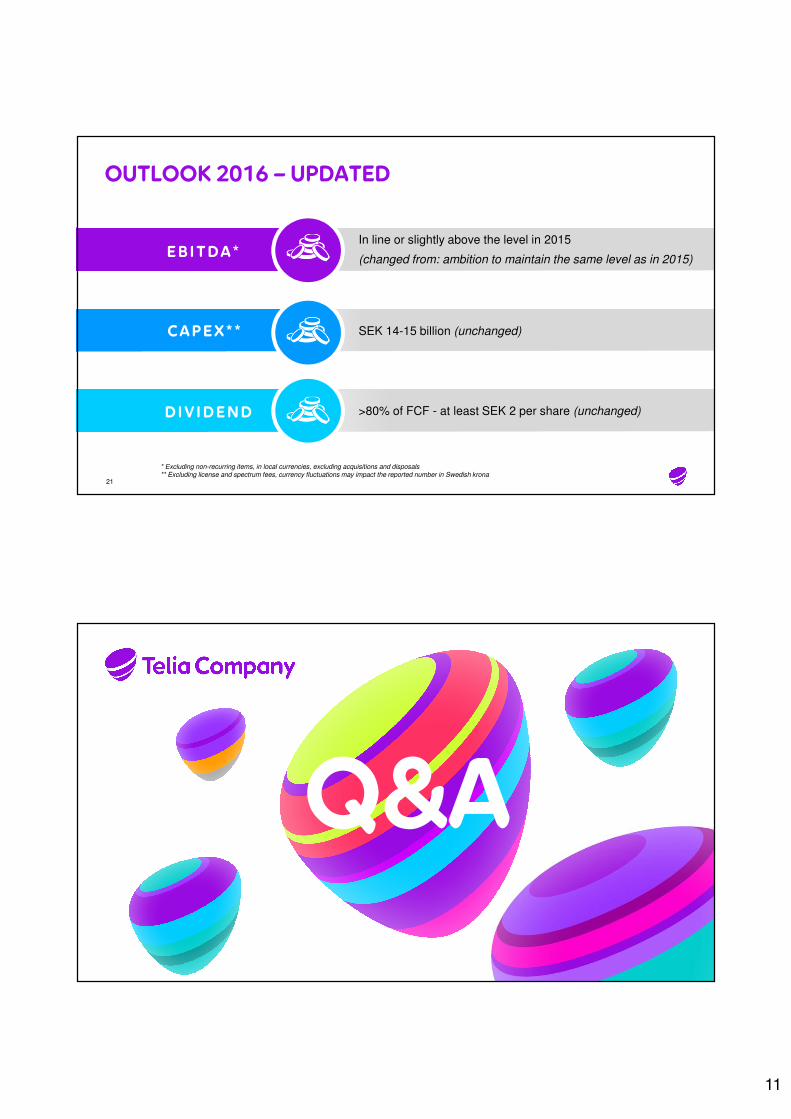

OUTLOOK 2016 – UPDATED

* Excluding non-recurring items, in local currencies, excluding acquisitions and disposals** Excluding license and spectrum fees, currency fluctuations may impact the reported number in Swedish krona

21

In line or slightly above the level in 2015

(changed from: ambition to maintain the same level as in 2015)EB ITDA *

SEK 14-15 billion (unchanged)

>80% of FCF - at least SEK 2 per share (unchanged)

CAPEX * *

DIV IDEND

Q&A

12

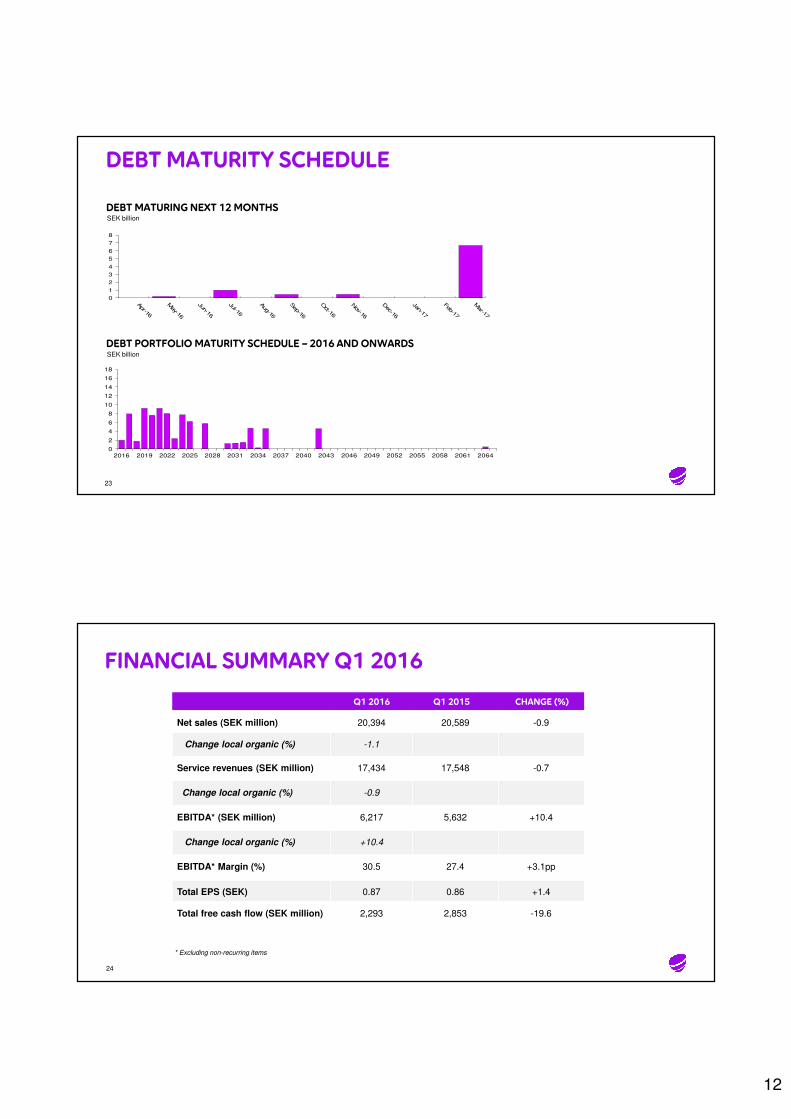

DEBT MATURITY SCHEDULE MMO

0

1

2

3

4

5

6

7

8

Apr-16

May-16

Jun-16

Jul-16

Aug-16

Sep-16

Oct-16

Nov-16

Dec-16

Jan-17

Feb-17

Mar-17

0

2

4

6

8

10

12

14

16

18

2016 2019 2022 2025 2028 2031 2034 2037 2040 2043 2046 2049 2052 2055 2058 2061 2064

23

DEBT MATURING NEXT 12 MONTHS

DEBT PORTFOLIO MATURITY SCHEDULE – 2016 AND ONWARDS

SEK billion

SEK billion

FINANCIAL SUMMARY Q1 2016

24

* Excluding non-recurring items

Q1 2016 Q1 2015 CHANGE (%)

Net sales (SEK million) 20,394 20,589 -0.9

Change local organic (%) -1.1

Service revenues (SEK million) 17,434 17,548 -0.7

Change local organic (%) -0.9

EBITDA* (SEK million) 6,217 5,632 +10.4

Change local organic (%) +10.4

EBITDA* Margin (%) 30.5 27.4 +3.1pp

Total EPS (SEK) 0.87 0.86 +1.4

Total free cash flow (SEK million) 2,293 2,853 -19.6

13

25

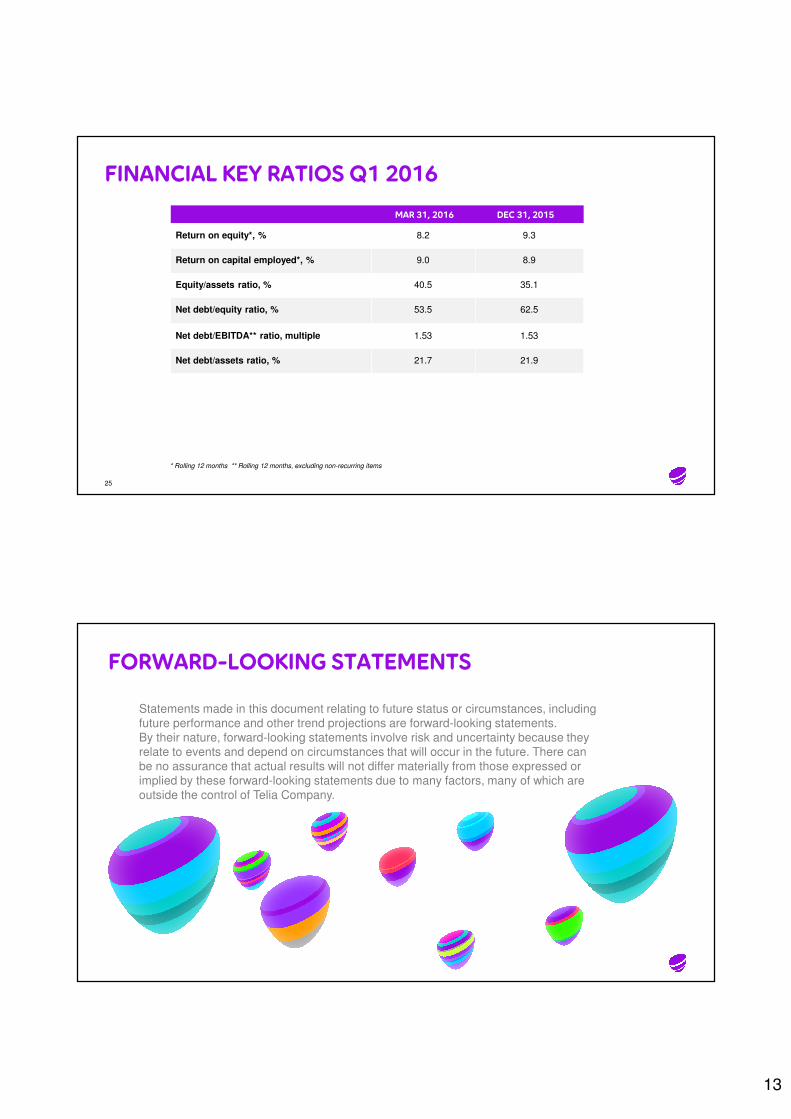

MAR 31, 2016 DEC 31, 2015

Return on equity*, % 8.2 9.3

Return on capital employed*, % 9.0 8.9

Equity/assets ratio, % 40.5 35.1

Net debt/equity ratio, % 53.5 62.5

Net debt/EBITDA** ratio, multiple 1.53 1.53

Net debt/assets ratio, % 21.7 21.9

* Rolling 12 months ** Rolling 12 months, excluding non-recurring items

FINANCIAL KEY RATIOS Q1 2016

FORWARD-LOOKING STATEMENTS

Statements made in this document relating to future status or circumstances, including

future performance and other trend projections are forward-looking statements.

By their nature, forward-looking statements involve risk and uncertainty because they

relate to events and depend on circumstances that will occur in the future. There can

be no assurance that actual results will not differ materially from those expressed or

implied by these forward-looking statements due to many factors, many of which are

outside the control of Telia Company.