policy & legal implications of implementing renewable energy at scale

TRANSCRIPT

Mintz Levin. Not your standard practice.

Policy and Legal Implications ofImplementing Renewable Energy at Scale

Thomas R. Burton III, Chair, Energy Technology Practice

August 2015

12th Annual AREDAY Summit

2

• Supply and Demand GeographicMismatch

• Finance Gap for Innovation Deployment

• To DG or Not to DG – That's the Question

• Intermittent Power GenerationCharacteristics

Key Barriers to Adoption of Renewable Energy At Scale

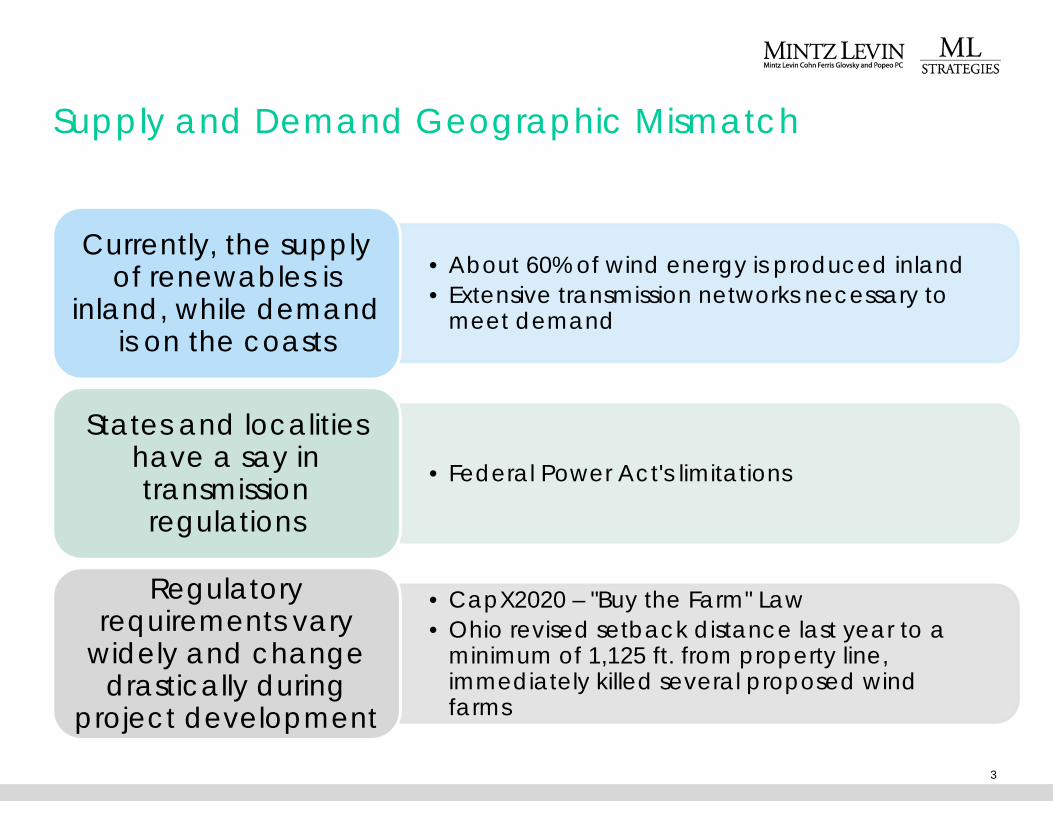

Supply and Demand Geographic Mismatch

3

• About 60% of wind energy is produced inland

• Extensive transmission networks necessary tomeet demand

Currently, the supplyof renewables is

inland, while demandis on the coasts

• Federal Power Act's limitations

States and localitieshave a say intransmissionregulations

• CapX2020 – "Buy the Farm" Law

• Ohio revised setback distance last year to aminimum of 1,125 ft. from property line,immediately killed several proposed windfarms

Regulatoryrequirements vary

widely and changedrastically during

project development

Solution: Federal Preemption to Simplify the Process

• Congress can and should have acomprehensive response

– On energy, the Supreme Court agrees

• Precedent: Telecommunications Act of1996, 1980 Comprehensive EnvironmentalResponse, Compensation, and Liability Act(CERCLA)

• For more, read Ann Klee, Jeffrey Porter, and KatyWard's analysis in Gas Lines to Pipelines: The Case forComprehensive Federal Energy Legislation

4

Solution: Clean Power Plan

5

Overview

•Building Block 3

•Federal Implementation Plan

Challenges

•Increased Generation Costs

•Infrastructure Gap

Opportunities

•Regional Partnerships – RGGI

•Corporate Leadership

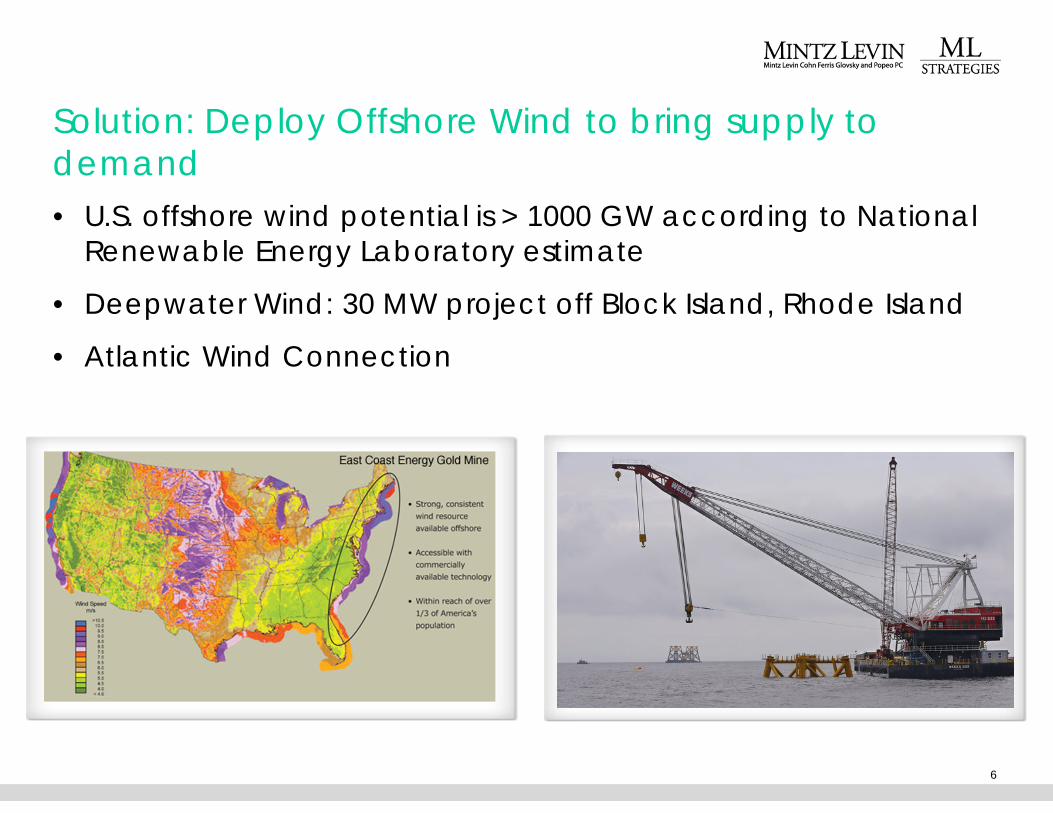

• U.S. offshore wind potential is > 1000 GW according to NationalRenewable Energy Laboratory estimate

• Deepwater Wind: 30 MW project off Block Island, Rhode Island

• Atlantic Wind Connection

Solution: Deploy Offshore Wind to bring supply todemand

6

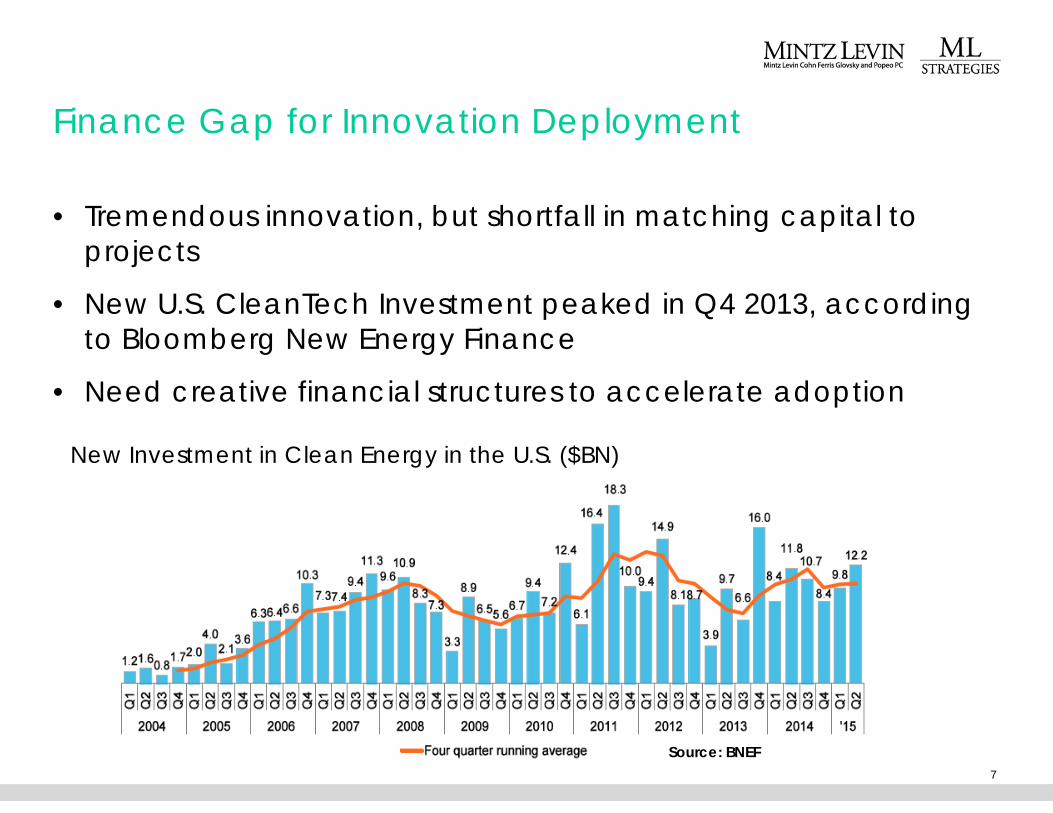

Finance Gap for Innovation Deployment

• Tremendous innovation, but shortfall in matching capital toprojects

• New U.S. CleanTech Investment peaked in Q4 2013, accordingto Bloomberg New Energy Finance

• Need creative financial structures to accelerate adoption

7

New Investment in Clean Energy in the U.S. ($BN)

Source: BNEF

Solution: Consistent Financial Policy

• Congress extends tax credits, but offers little certainty

– PTC: Senate approved extension July 21st through 2016

– ITC: Likely addressed via a tax reform negotiation in 2017

– Sustainable proposals to sunset may be a solution

• Grow More Green Banks

– Connecticut: Attracted $225 million last year

– New York: Initial commitment of over $800 million

– PACE

• For renewable solutions to scale, government must lead the wayas an early adopter, which can unlock financing

– Federal

– Local8

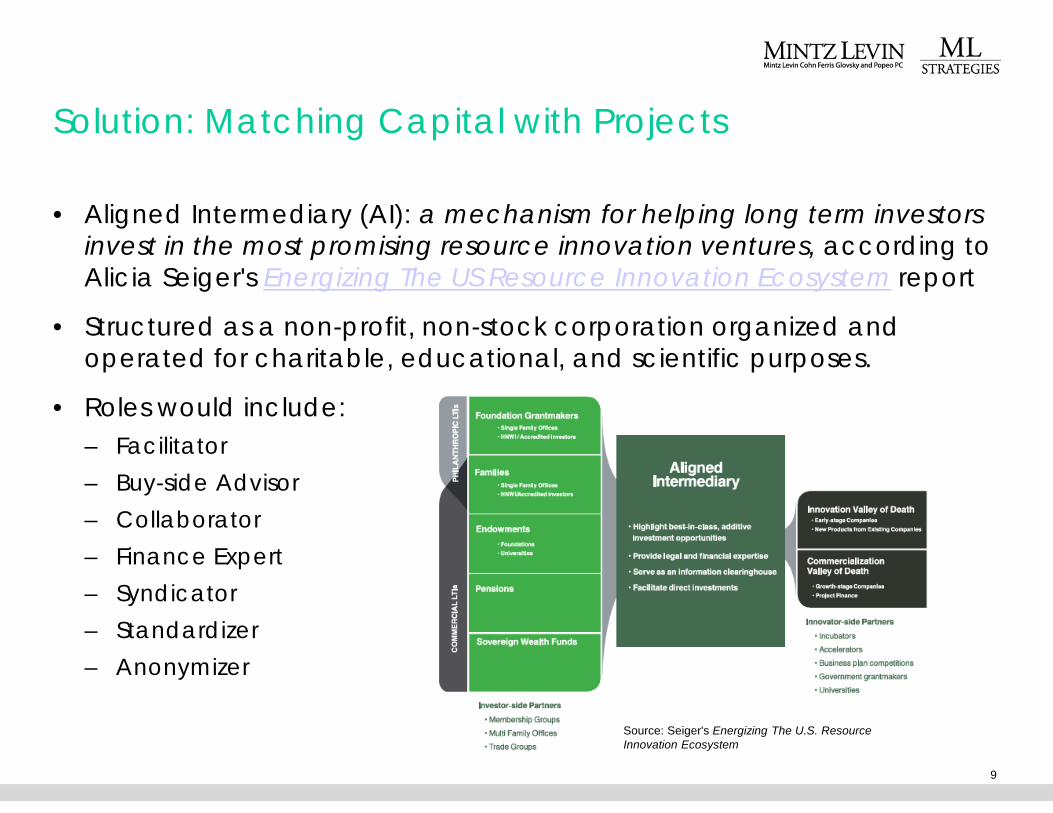

Solution: Matching Capital with Projects

• Aligned Intermediary (AI): a mechanism for helping long term investorsinvest in the most promising resource innovation ventures, according toAlicia Seiger's Energizing The US Resource Innovation Ecosystem report

• Structured as a non-profit, non-stock corporation organized andoperated for charitable, educational, and scientific purposes.

• Roles would include:

– Facilitator

– Buy-side Advisor

– Collaborator

– Finance Expert

– Syndicator

– Standardizer

– Anonymizer

9

Source: Seiger's Energizing The U.S. ResourceInnovation Ecosystem

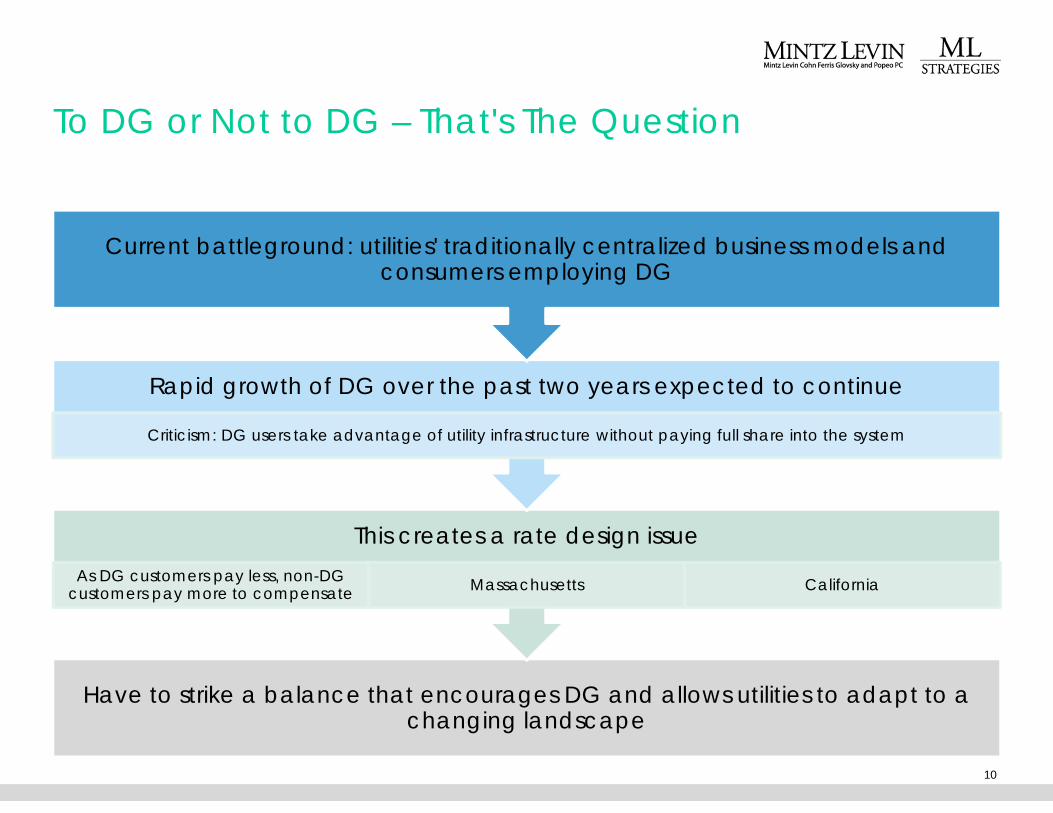

To DG or Not to DG – That's The Question

10

Have to strike a balance that encourages DG and allows utilities to adapt to achanging landscape

This creates a rate design issue

As DG customers pay less, non-DGcustomers pay more to compensate

Massachusetts California

Rapid growth of DG over the past two years expected to continue

Criticism: DG users take advantage of utility infrastructure without paying full share into the system

Current battleground: utilities' traditionally centralized business models andconsumers employing DG

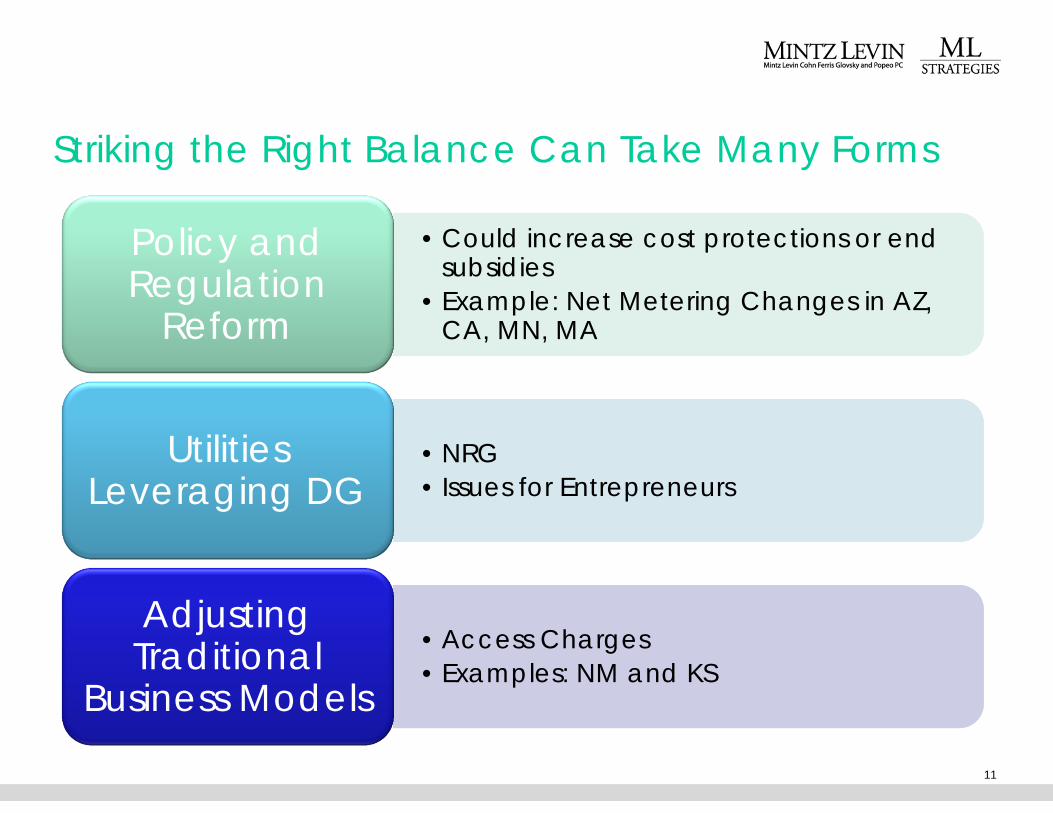

Striking the Right Balance Can Take Many Forms

11

• Could increase cost protections or endsubsidies

• Example: Net Metering Changes in AZ,CA, MN, MA

• Could increase cost protections or endsubsidies

• Example: Net Metering Changes in AZ,CA, MN, MA

Policy andRegulation

Reform

• NRG

• Issues for Entrepreneurs

• NRG

• Issues for Entrepreneurs

UtilitiesLeveraging DG

• Access Charges

• Examples: NM and KS

• Access Charges

• Examples: NM and KS

AdjustingTraditional

Business Models

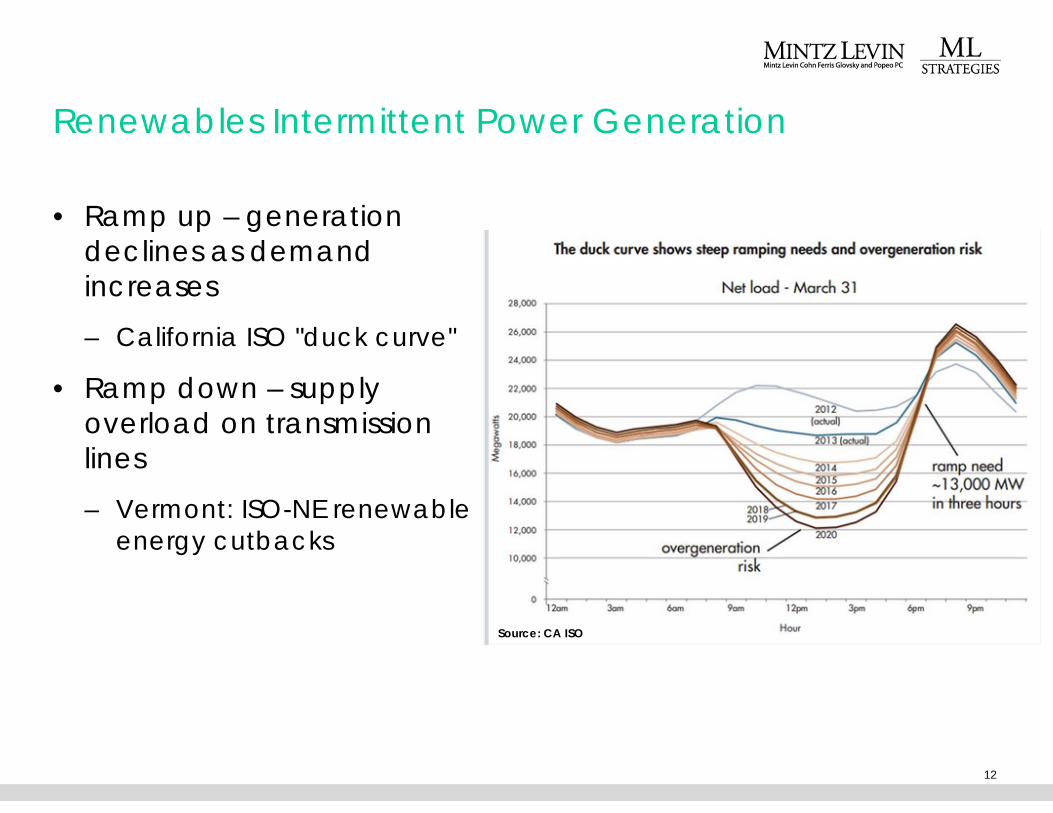

Renewables Intermittent Power Generation

• Ramp up – generationdeclines as demandincreases

– California ISO "duck curve"

• Ramp down – supplyoverload on transmissionlines

– Vermont: ISO-NE renewableenergy cutbacks

12

Source: CA ISO

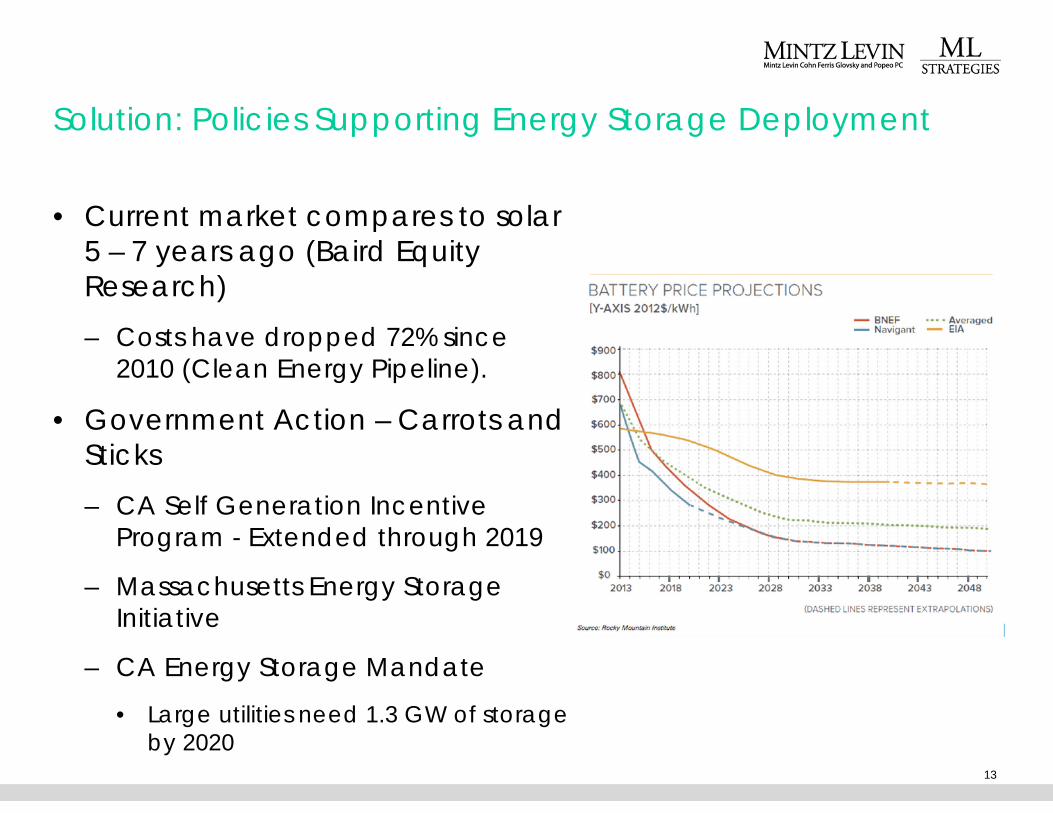

Solution: Policies Supporting Energy Storage Deployment

• Current market compares to solar5 – 7 years ago (Baird EquityResearch)

– Costs have dropped 72% since2010 (Clean Energy Pipeline).

• Government Action – Carrots andSticks

– CA Self Generation IncentiveProgram - Extended through 2019

– Massachusetts Energy StorageInitiative

– CA Energy Storage Mandate

• Large utilities need 1.3 GW of storageby 2020

13

14