Mintz Levin. Not your standard practice.

Policy and Legal Implications ofImplementing Renewable Energy at Scale

Thomas R. Burton III, Chair, Energy Technology Practice

August 2015

12th Annual AREDAY Summit

2

• Supply and Demand GeographicMismatch

• Finance Gap for Innovation Deployment

• To DG or Not to DG – That's the Question

• Intermittent Power GenerationCharacteristics

Key Barriers to Adoption of Renewable Energy At Scale

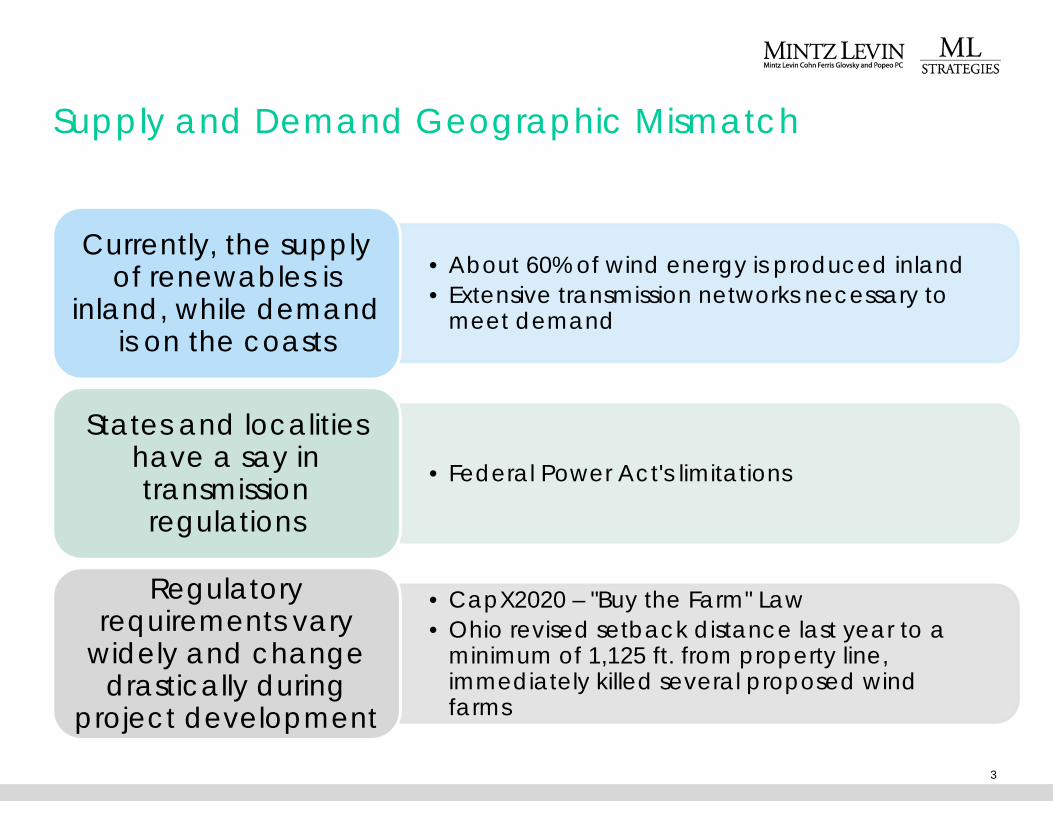

Supply and Demand Geographic Mismatch

3

• About 60% of wind energy is produced inland

• Extensive transmission networks necessary tomeet demand

Currently, the supplyof renewables is

inland, while demandis on the coasts

• Federal Power Act's limitations

States and localitieshave a say intransmissionregulations

• CapX2020 – "Buy the Farm" Law

• Ohio revised setback distance last year to aminimum of 1,125 ft. from property line,immediately killed several proposed windfarms

Regulatoryrequirements vary

widely and changedrastically during

project development

Solution: Federal Preemption to Simplify the Process

• Congress can and should have acomprehensive response

– On energy, the Supreme Court agrees

• Precedent: Telecommunications Act of1996, 1980 Comprehensive EnvironmentalResponse, Compensation, and Liability Act(CERCLA)

• For more, read Ann Klee, Jeffrey Porter, and KatyWard's analysis in Gas Lines to Pipelines: The Case forComprehensive Federal Energy Legislation

4

Solution: Clean Power Plan

5

Overview

•Building Block 3

•Federal Implementation Plan

Challenges

•Increased Generation Costs

•Infrastructure Gap

Opportunities

•Regional Partnerships – RGGI

•Corporate Leadership

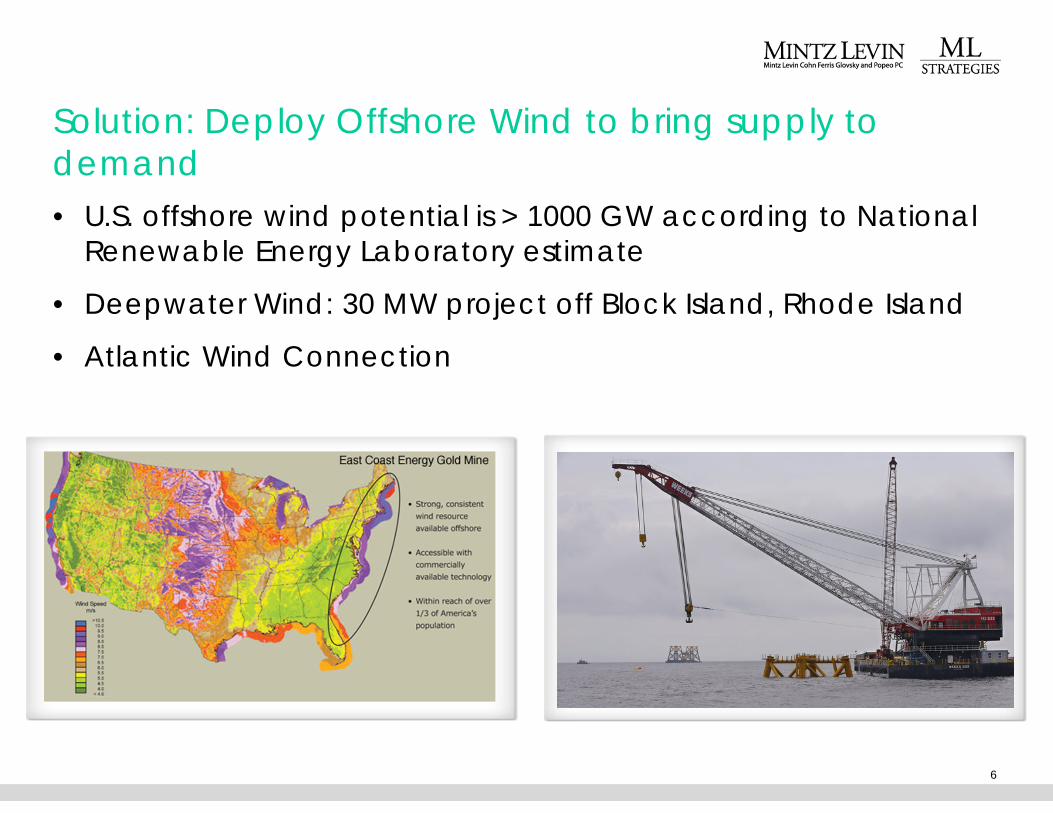

• U.S. offshore wind potential is > 1000 GW according to NationalRenewable Energy Laboratory estimate

• Deepwater Wind: 30 MW project off Block Island, Rhode Island

• Atlantic Wind Connection

Solution: Deploy Offshore Wind to bring supply todemand

6

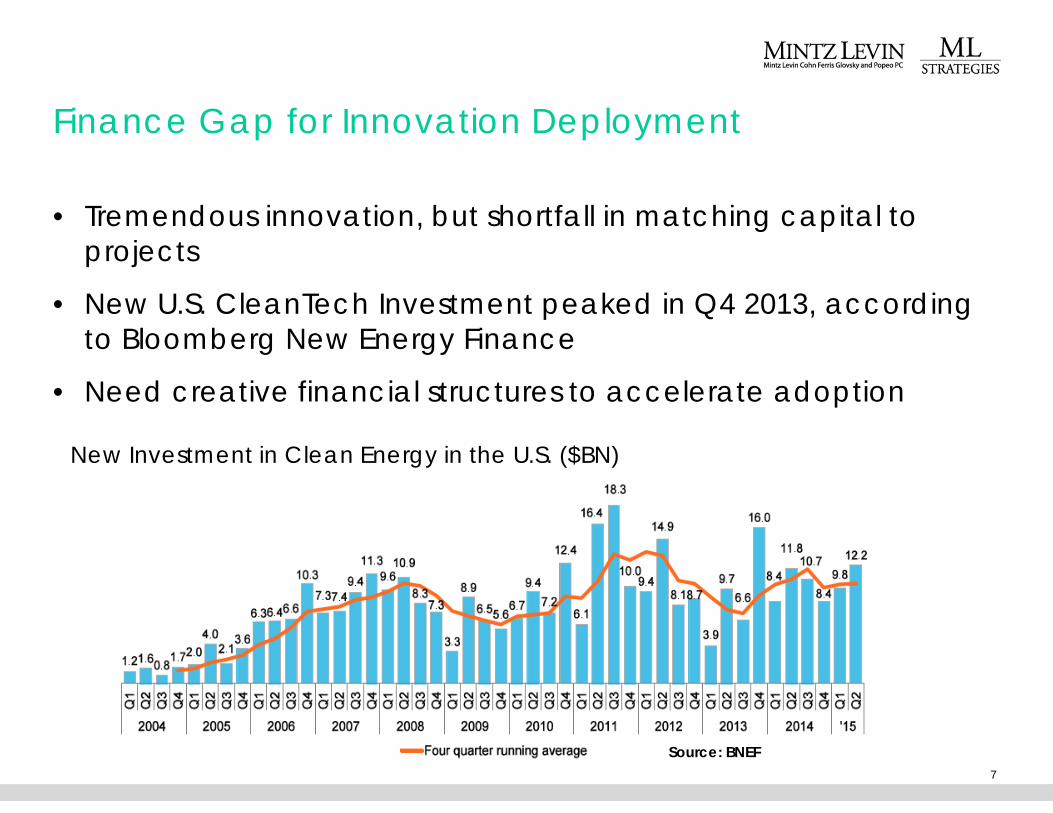

Finance Gap for Innovation Deployment

• Tremendous innovation, but shortfall in matching capital toprojects

• New U.S. CleanTech Investment peaked in Q4 2013, accordingto Bloomberg New Energy Finance

• Need creative financial structures to accelerate adoption

7

New Investment in Clean Energy in the U.S. ($BN)

Source: BNEF

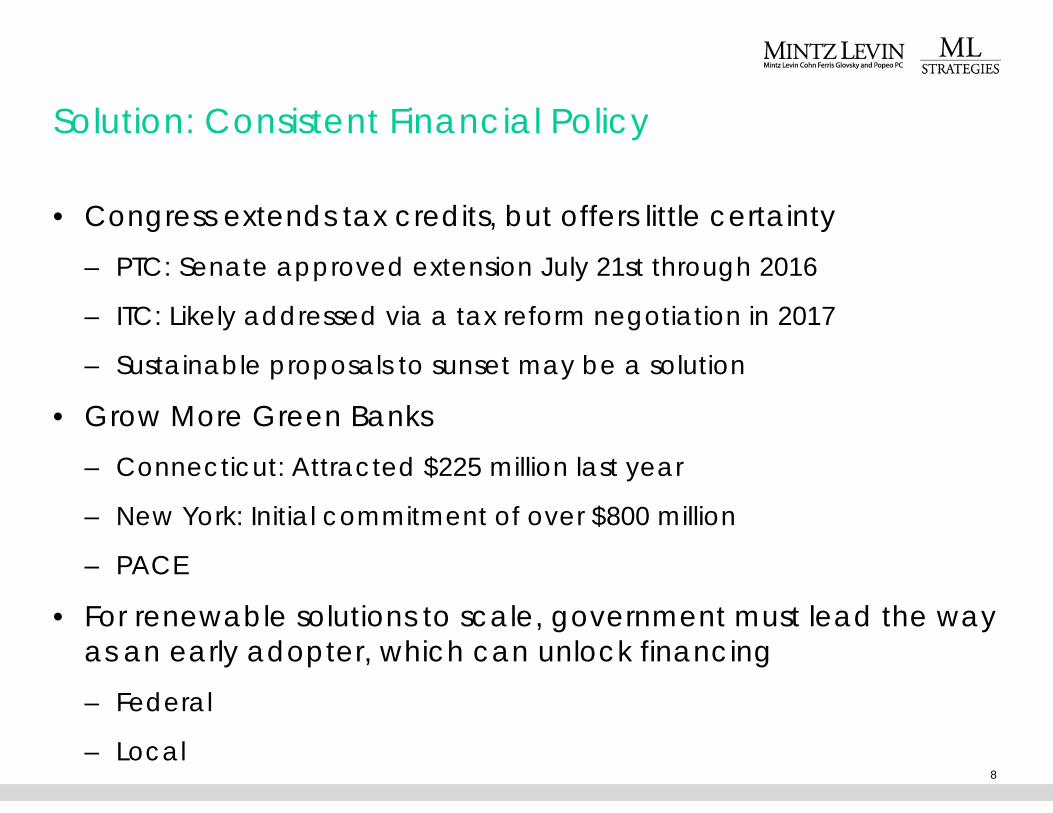

Solution: Consistent Financial Policy

• Congress extends tax credits, but offers little certainty

– PTC: Senate approved extension July 21st through 2016

– ITC: Likely addressed via a tax reform negotiation in 2017

– Sustainable proposals to sunset may be a solution

• Grow More Green Banks

– Connecticut: Attracted $225 million last year

– New York: Initial commitment of over $800 million

– PACE

• For renewable solutions to scale, government must lead the wayas an early adopter, which can unlock financing

– Federal

– Local8

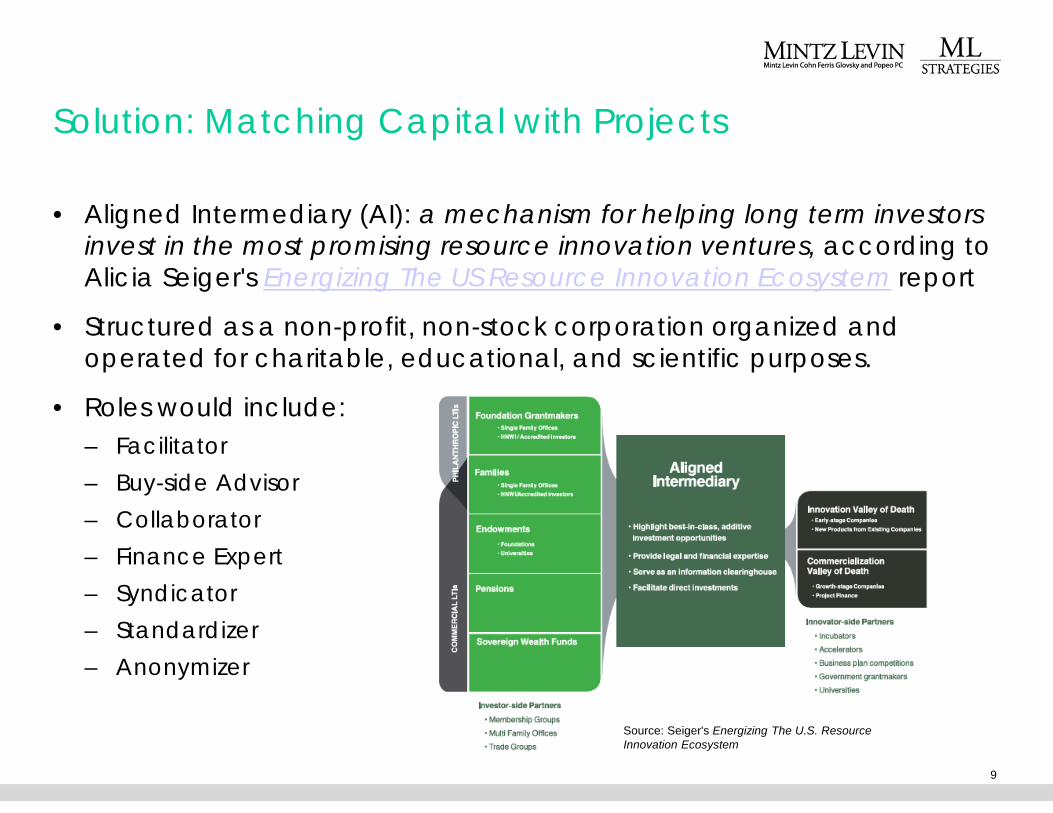

Solution: Matching Capital with Projects

• Aligned Intermediary (AI): a mechanism for helping long term investorsinvest in the most promising resource innovation ventures, according toAlicia Seiger's Energizing The US Resource Innovation Ecosystem report

• Structured as a non-profit, non-stock corporation organized andoperated for charitable, educational, and scientific purposes.

• Roles would include:

– Facilitator

– Buy-side Advisor

– Collaborator

– Finance Expert

– Syndicator

– Standardizer

– Anonymizer

9

Source: Seiger's Energizing The U.S. ResourceInnovation Ecosystem

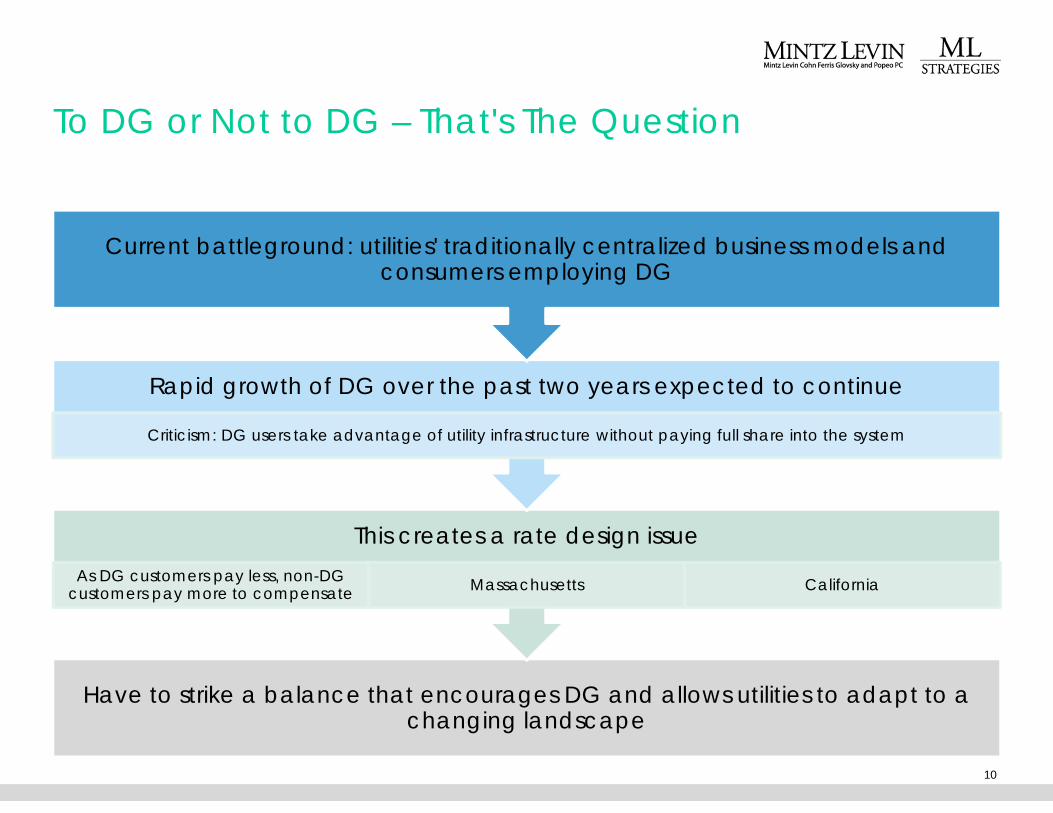

To DG or Not to DG – That's The Question

10

Have to strike a balance that encourages DG and allows utilities to adapt to achanging landscape

This creates a rate design issue

As DG customers pay less, non-DGcustomers pay more to compensate

Massachusetts California

Rapid growth of DG over the past two years expected to continue

Criticism: DG users take advantage of utility infrastructure without paying full share into the system

Current battleground: utilities' traditionally centralized business models andconsumers employing DG

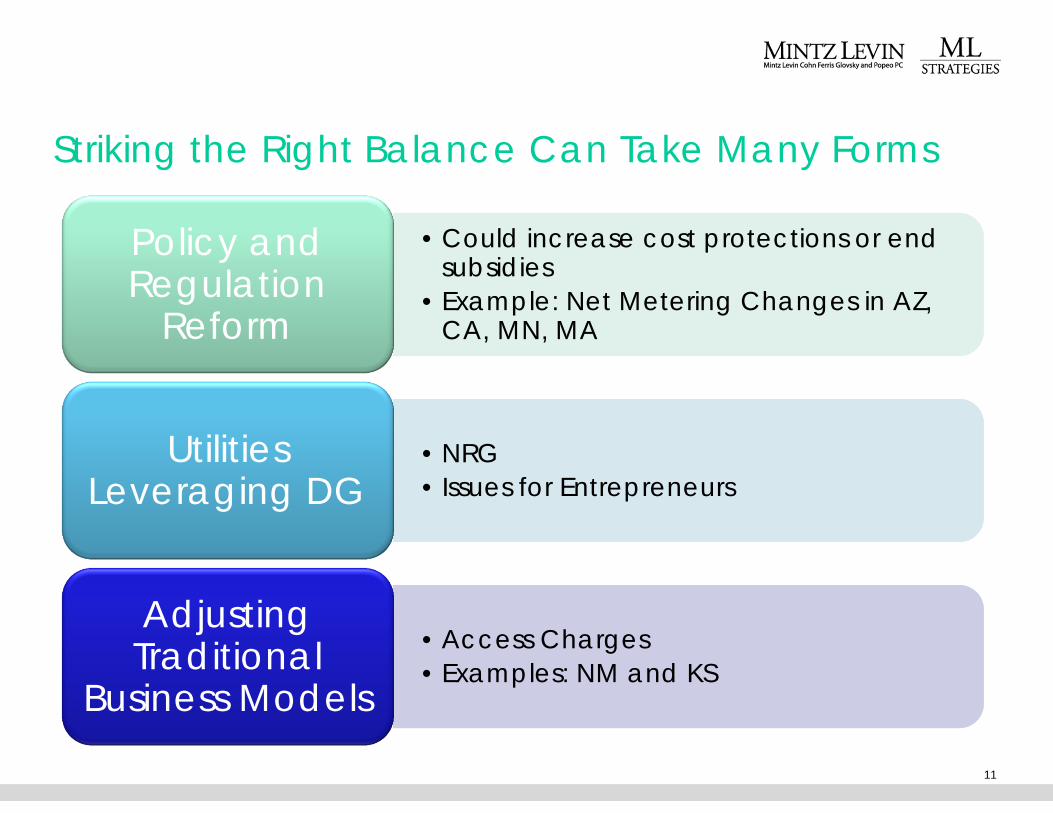

Striking the Right Balance Can Take Many Forms

11

• Could increase cost protections or endsubsidies

• Example: Net Metering Changes in AZ,CA, MN, MA

• Could increase cost protections or endsubsidies

• Example: Net Metering Changes in AZ,CA, MN, MA

Policy andRegulation

Reform

• NRG

• Issues for Entrepreneurs

• NRG

• Issues for Entrepreneurs

UtilitiesLeveraging DG

• Access Charges

• Examples: NM and KS

• Access Charges

• Examples: NM and KS

AdjustingTraditional

Business Models

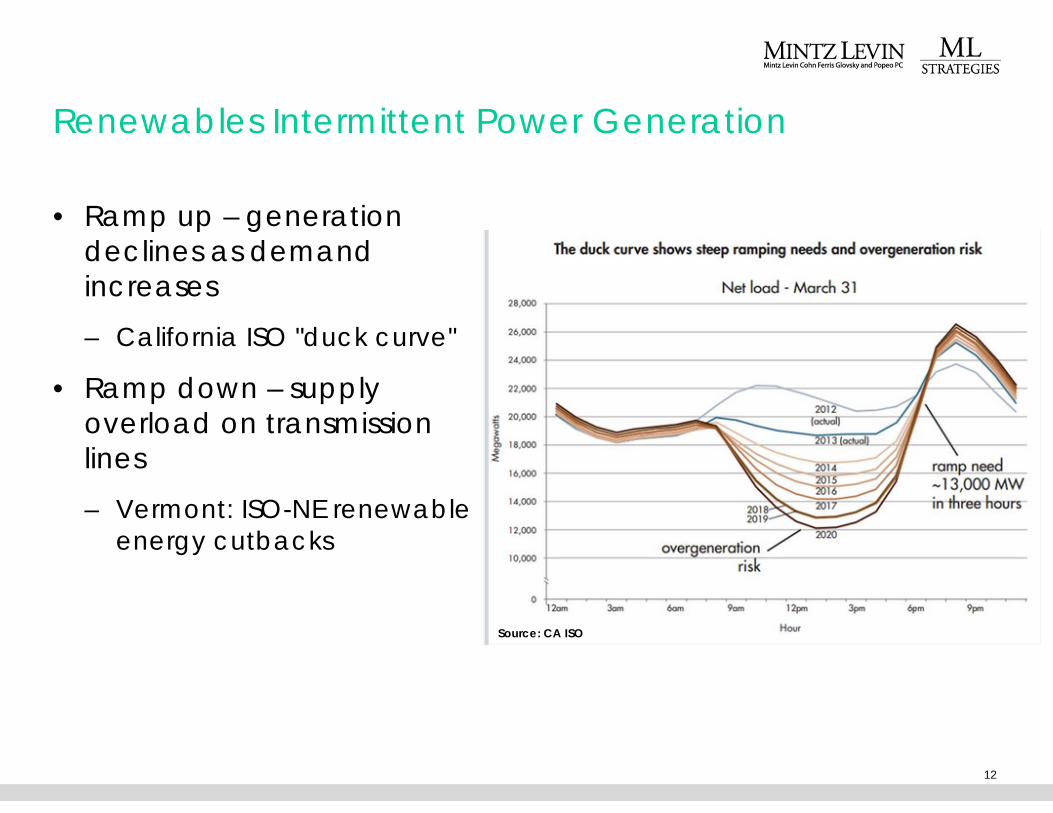

Renewables Intermittent Power Generation

• Ramp up – generationdeclines as demandincreases

– California ISO "duck curve"

• Ramp down – supplyoverload on transmissionlines

– Vermont: ISO-NE renewableenergy cutbacks

12

Source: CA ISO

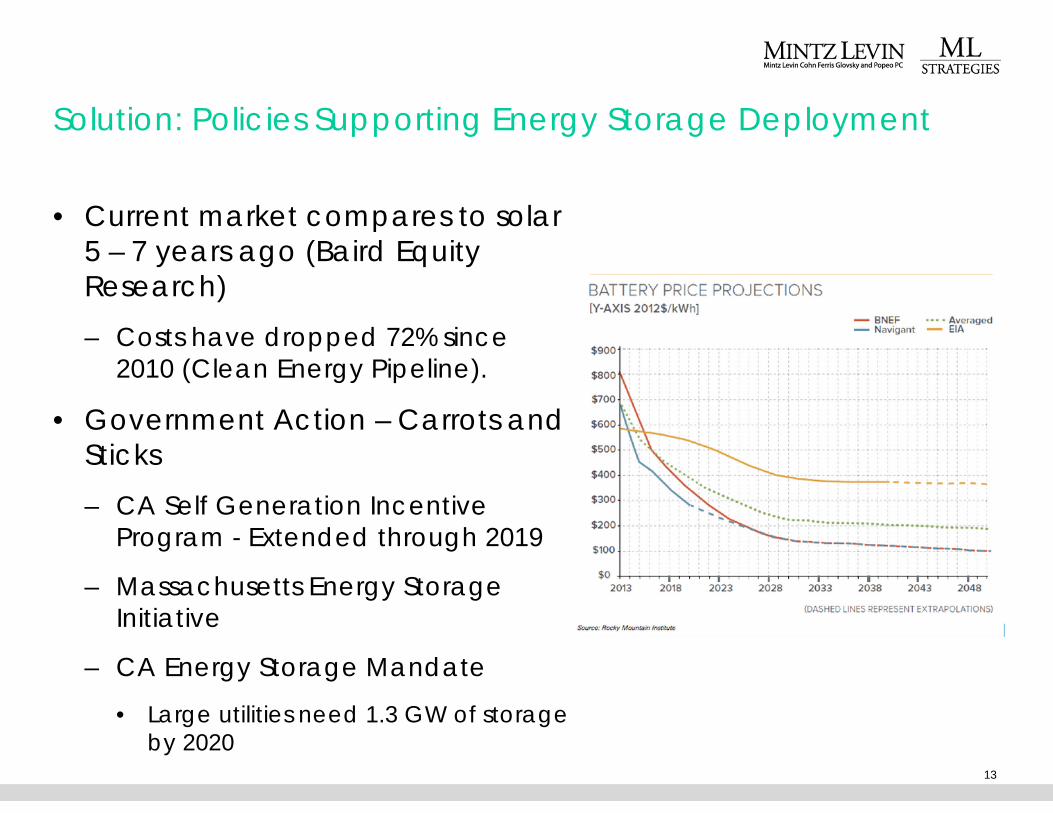

Solution: Policies Supporting Energy Storage Deployment

• Current market compares to solar5 – 7 years ago (Baird EquityResearch)

– Costs have dropped 72% since2010 (Clean Energy Pipeline).

• Government Action – Carrots andSticks

– CA Self Generation IncentiveProgram - Extended through 2019

– Massachusetts Energy StorageInitiative

– CA Energy Storage Mandate

• Large utilities need 1.3 GW of storageby 2020

13

14