outlook on mexico so far, a tale of macro stability but ... · ... a tale of macro stability but...

TRANSCRIPT

Outlook on Mexico

So far, a tale of macro stability but still moderate growth: what is the outlook?

Monterrey, 1 February 2016

Jorge Sicilia, BBVA Research

GIC Meeting

Global Economic Scenario / 28 January 2016

1. A structural outlook of the Mexican economy: a journey trough strength and weaknesses

2. Recent developments: growth, markets, vulnerabilities

3. Second generation of economic reforms

Contents

Page 2

Global Economic Scenario / 28 January 2016

The long and winding road

Ruling party loses lower house majority

1993 1997 2000 2013 1994-95

Central bank autonomy

Flexible exchange rate

Ruling party loses presidency

Mexico joins GATT

1986 Structural reforms: Telecom, Labor Financial, Antitrust, Education

Inflation at an all-time low

USD at an all-

time high

Page 3

- 8.0

- 6.0

- 4.0

- 2.0 0.0 2.0 4.0 6.0 8.0

10.0

1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Debt crisis

Oil crisis Tequila crisis Lehman crisis

NAFTA Structural Reforms

Global Economic Scenario / 28 January 2016

Manufacturing (Annual percentage change, sa) Source: BBVA Research

Strengths: (i) highly integrated to the US economy Exports by destination in 2014 (structure, %) Source: BBVA Research

-1

0

1

2

3

4

5

6

7

Jan-11

Mar-11

May-11

Jul-11

Sep-11

Nov-11

Jan-12

Mar-12

May-12

Jul-12

Sep-12

Nov-12

Jan-13

Mar-13

May-13

Jul-13

Sep-13

Nov-13

Jan-14

Mar-14

May-14

Jul-14

Sep-14

Nov-14

Jan-15

U.S. Mexico

80.2

9.15.1 4.4 1.1

0

10

20

30

40

50

60

70

80

90

100

USA RestofAmerica EuropeaUnion Asia RestofCountries

Page 4

Global Economic Scenario / 28 January 2016

Mexican exports (% share in total exports) Source: BBVA Research with INEGI data.

Strengths: (ii) with an export structure relying less on petroleum and more on manufacturing

Mexican manufactured exports (% share in total exports) Source: BBVA Research with INEGI data.

0

10

20

30

40

50

60

70

80

90

100

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

Petroleum exports Non-petroleum exports

0

10

20

30

40

50

60

70

80

90

100

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Automotive Non-automotive

Page 5

Global Economic Scenario / 28 January 2016

Openness index and trade balance (% share in GDP) Source: BBVA Research with INEGI data.

Strengths: (iii) A very open economy (with free trade agreements with more than 50 countries)

Exports of light vehicles (units in millions, 12mma) Source: BBVA Research with AMIA data.

-6

-4

-2

0

2

4

6

8

10

0

10

20

30

40

50

60

70

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

Exports share in GDP Imports share in GDP

Trade balance - right axis

0

0.5

1

1.5

2

2.5

Jan-

95Ja

n-96

Jan-

97Ja

n-98

Jan-

99Ja

n-00

Jan-

01Ja

n-02

Jan-

03Ja

n-04

Jan-

05Ja

n-06

Jan-

07Ja

n-08

Jan-

09Ja

n-10

Jan-

11Ja

n-12

Jan-

13Ja

n-14

Jan-

15

Exports of light vehicles

Page 6

Global Economic Scenario / 28 January 2016

Strengths: (iv) A sound and solvent banking system

7

Bank's Capital Adequacy Ratio, % Source: CNBV

Non-performing loans (NPL) and Provision coverage (PC) ratios Source: CNBV

15,4

14,2

14,1

14,3

16,1

16,0

15,3

16,5

16,9

15,7

15,9

15,5

15,8

15,0

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

nov-

15

BIS minimum: 8%

CNBV minimum to avoid "early-warnings”: 10%

Basel III minimum: 10.5%

2,6

140,5

0

50

100

150

200

250

300

0

2

4

6

8

10

Dec

-00

Dec

-01

Dec

-02

Dec

-03

Dec

-04

Dec

-05

Dec

-06

Dec

-07

Dec

-08

Dec

-09

Dec

-10

Dec

-11

Dec

-12

Dec

-13

Dec

-14

Dec

-15

Non-Performing Loans Provision Coverage (PC)

PC

NPL

Global Economic Scenario / 28 January 2016

Potential GDP growth (%) Source: own estimation

Weaknesses: (i) Low GDP per capita (stable relative with the US) with no contribution from TFP

Page 8

- 2

- 1

0

1

2

3

4

5

6

7

- 2

- 1

0

1

2

3

4

5

6

7

1970 1972 1974 1976 1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Labor Capital Total Factor Productivity Potential GDP

Global Economic Scenario / 28 January 2016

Weaknesses: (ii) relatively high informality and an improvable legal environment…

0

5

10

15

20

25

30

35

40

45

50

55

I-05 III

I-06 III

I-07 III

I-08 III

I-09 III

I-10 III

I-11 III

I-12 III

I-13 III

I-14 III

I-15 III

IMSS Employment Labor Force

1Q05Diference: Total-IMSS=30.3million

persons

3Q15Diference :Total-IMSS=35.4million

persons

Total and formal private employment (figures in millions of workers) Source: BBVA Research with data of INEGI

Page 9

Informal economy and legal environment (% of GDP and Index) Source: Schneider (2009) and Property Rights Alliance with World Bank data

Info

rmal

eco

nom

y (%

of G

DP)

Index of legal environment (max=10)

Brasil

China

Perú

México

España

EEUU

0

10

20

30

40

50

60

70

2 3 4 5 6 7 8 9

Global Economic Scenario / 28 January 2016

Info

rmal

eco

nom

y (%

of G

DP)

Productivity (relative to the US) Capital (relative to the US)

Informal economy (% of GDP) and … Capital Source: Schneider (2009) and Hall and Jones (1998)

Productivity Source: Schneider (2009) and Hall and Jones (1998)

Brazil

China

Peru

Mexico

Spain

US 0

10

20

30

40

50

60

70

0.2 0.4 0.6 0.8 1 1.2 1.4

Brazil

China

Peru

Mexico

Spain

US 0

10

20

30

40

50

60

70

0 0.2 0.4 0.6 0.8 1 1.2 1.4

Weaknesses: (ii) … keeps productivity and investment down

Page 10

Global Economic Scenario / 28 January 2016

2.8 2.6 2.83.9 3.7 3.8

4.9 4.7 4.8

6.1 6.0 5.9

7.5 7.2 7.2

9.4 9.0 9.1

12.1 11.8 11.4

16.6 16.4 16.1

35.3 37.2 37.4

05101520253035404550556065707580859095100

2010 2012 2014

I II III IV V VI VII VIII IX XIncomedeciles:

1.4 1.4 1.5

Quarterly monetary current income by decile (% of total income) Source: BBVA Research with data from INEGI

Page 11

0,00

0,05

0,10

0,15

0,20

0,25

0,30

0,35

0,40

0,45

0,50

Den

Slov Slvk Nor Cze

Ice

Fin

Bel

Swe

Austr

Neth

Swit

Ger

Hung Pol

Lux

Ire Fra

SKor

Can

Austr

Ita NZa Spa

Est

Por

Gree UK Isr

US Tur

MEX

ICO

Income Inequality, Gini Index. OECD countries Gini coefficient, 0 = complete equality; 1 = complete inequality, Source: OECD, 2012

Weaknesses: (iii) … and prevents wages from growing. At the same time, inequality is high

Global Economic Scenario / 28 January 2016

Traditional and total public sector balance (% of GDP) Source: BBVA Research with data of Ministry of Finance (SHCP)

Weaknesses: (iv) Traditional and total public sector balance has remained high as proportion of GDP

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

2009 2010 2011 2012 2013 2014 2015

TraditionalBalance TotalBalance

Total public sector gross debt (% of GDP) Source: BBVA Research with data of Ministry of Finance (SHCP)

34.6 34.9 35.336.4

38.8

41.0

45.7

30

32

34

36

38

40

42

44

46

48

2009 2010 2011 2012 2013 2014 2015

Page 12

Global Economic Scenario / 28 January 2016

High heterogeneity Regional and national economic activity over 2010-15e (2010=100) p/preliminary data; e/in-house estimates Source: BBVA Research with INEGI data

95

100

105

110

115

120

125

2010

2011

2012

2013

p

2014

e

2015

e

Touristic IndustrialHigh Development Medium DevelopmentLow Development National

Regional and national GDP per capita (Compounded annual growth rate %) Source: BBVA Research with INEGI data

Regions are divided by economic vocation and level of development: High Development: DF; Touristic: BCS and Q Roo; Industrial: Ags, BC, Coah, Chih, Jal, Méx, NL, Qro, Son, Tamps; Medium Development: Camp, Col, Dgo, Gto, Hgo, Mich, Mor, Nay, Pue, SLP, Sin, Tab, Tlax, Ver, Yuc, Zac; Low Development: Chis, Gro and Oax.

0

0.5

1

1.5

2

2.5

3

Hig

h D

evel

opm

ent

Indu

stria

l

Nat

iona

l

Tour

istic

Low

Dev

elop

men

t

Med

ium

Dev

elop

men

t

GDP per capita compounded annual growth rate 2003-2014 (%)

Page 13

Global Economic Scenario / 28 January 2016

Contents

Page 14

1. A structural outlook of the Mexican economy: a journey trough strength and weaknesses

2. Recent developments: growth, markets, vulnerabilities

3. Second generation of economic reforms

Global Economic Scenario / 28 January 2016

GDP’s contribution to growth by component (percentage points of total growth Source: BBVA Research with data of INEGI)

In this recovery, GDP growth has been lower than expected and relied mainly on consumption

Page 15

4.7

- 5.8

5.9

7.0 4.7 2.7

5.3

- 0.6

0.1 1.4

4.3 3.0

5.0

3.1 1.4

- 4.7

5.1 4.0 4.0

1.3 2.3

2.5

- 12.0 - 11.0 - 10.0

- 9.0 - 8.0 - 7.0 - 6.0 - 5.0 - 4.0 - 3.0 - 2.0 - 1.0 0.0 1.0 2.0 3.0 4.0 5.0 6.0 7.0 8.0

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 Avg Qs15

Consumption Fixed Investment Net Exports GDP

Consumption has been the main driver

of GDP growth

Global Economic Scenario / 28 January 2016

Page 16

Recent developments in financial markets: higher financial stress in EM BBVA Research Financial Stress Index (normalized index) Source: BBVA Research

BBVA Research Financial Stress Index regional map for EM. Source: BBVA Research

Jan-

16

# # # # # # # #EMU # # # # # # # #

# # # # # # # #Brazil # # # # # # # #Chile # # # # # # # #Colombia # # # # # # # #Mexico # # # # # # # #Peru # # # # # # # #

# # # # # # # #Czech Republic # # # # # # # #Hungary # # # # # # # #Poland # # # # # # # #Russia # # # # # # # #Turkey # # # # # # # #

# # # # # # # #China # # # # # # # #India # # # # # # # #Indonesia # # # # # # # #Korea # # # # # # # #Malaysia # # # # # # # #Philippines # # # # # # # #Taiwan # # # # # # # #

Thailand # # # # # # # #

May

-15

Apr

-15

Mar

-15

Feb-

15

Jun-

15

Nov

-15

Jan-

15

Sep

-15

Dec

-14

Dec

-15

Oct

-15

Jul-1

5

Aug

-15

US

Latam

EMEA

Asia

Very high Low

High Very low

Neutral No data

-1,5

0,0

1,5

3,0

4,5

Jan-08

Jan-09

Jan-10

Jan-11

Jan-12

Jan-13

Jan-14

Jan-15

Jan-16

Developed Emerging

Focus on

Global Economic Scenario / 28 January 2016

Page 17

EM BBVA footprint FX performance vs USD (Base 100 January 2015) Source: Bloomberg and BBVA Research

Recent developments in financial markets: evolving like other “crisis”

BBVA Research Volatility Index: by assets Source: BBVA Research

Fixed income

Credit

FX

Equity

August 2013, 2nd taperging talksAugust 2015 episodeCurrent

60

65

70

75

80

85

90

95

100

105

110

Jan-15 Mar-15 May-15 Jul-15 Sep-15 Nov-15 Jan-16

ARS CLP COP MXN PEN BRL

Depreciationvs.USD

Global Economic Scenario / 28 January 2016

-6

-5

-4

-3

-2

-1

0

1

2

3

4

5

6

USA UK

Norway

Swed

en

Austria

Germany

France

Nethe

rland

s

Italy

Spain

Belgium

Greece

Portug

al

Ireland

Turkey

Russia

Poland

CzechRe

p

Hun

gary

Bulgaria

Roman

ia

Croatia

Mexico

Brazil

Chile

Colombia

Peru

Arge

ntina

China

Korea

Thailand

Indo

nesia

Malaysia

Philip

pine

s

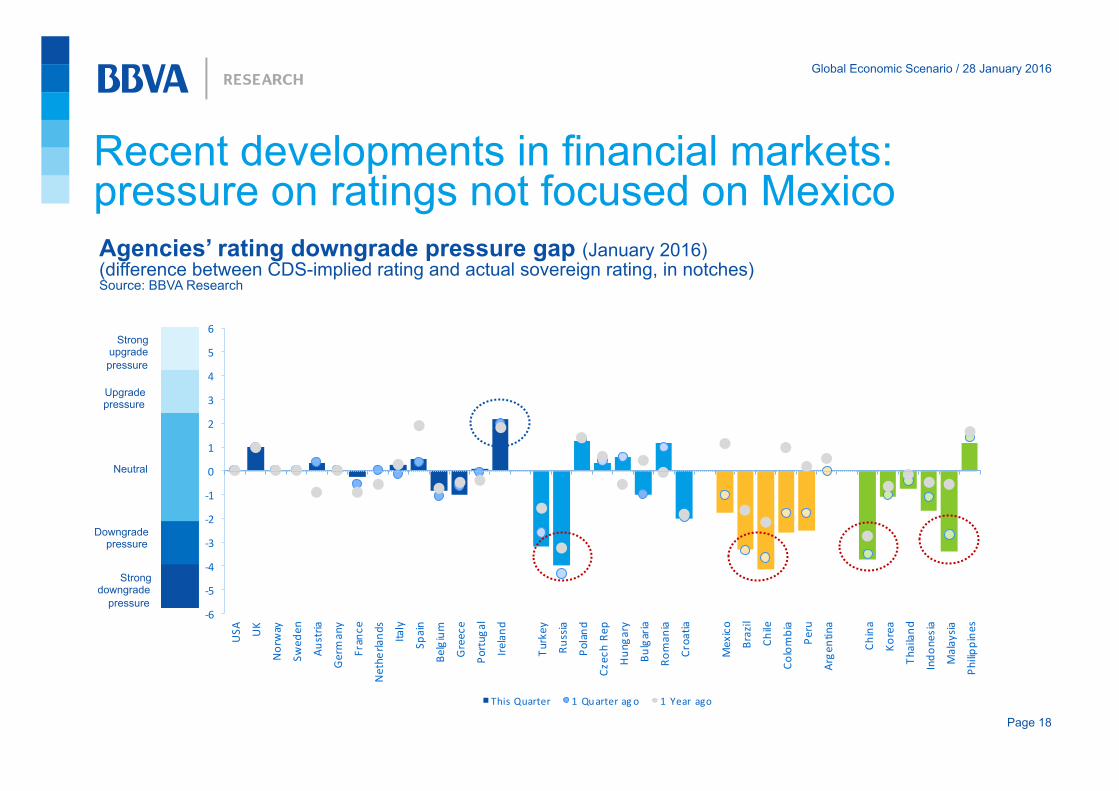

ThisQuarter 1Quarterag o 1 Year ago

Strong downgrade

pressure

Strong upgrade pressure

Downgrade pressure

Neutral

Upgrade pressure

Agencies’ rating downgrade pressure gap (January 2016) (difference between CDS-implied rating and actual sovereign rating, in notches) Source: BBVA Research

-6.0-5.0-4.0-3.0-2.0-1.00.01.02.03.04.05.06.0

Page 18

Recent developments in financial markets: pressure on ratings not focused on Mexico

Global Economic Scenario / 28 January 2016

But risk perception is starting to rise Emerging-markets CDS bp Source: BBVA Research, Bloomberg

Emeging markets CDS change Year-to-date, bp Source: BBVA Research, Bloomberg

050

100150200250300350400450500

Brz(Baa3)

Col(Ba

a2)

Tur(Ba

a3)

Per(A3

)

Mal(A

3)

Mx(A3)

Thai(B

aa1)

Chil(Aa3

)

SKo

r(Aa3

)

215

0

10

20

30

40

50

60

Col(Ba

a2)

Mx(A3)

Per(A3

)

Mal(A

3)

Thai(B

aa1)

Tur(Ba

a3)

Chil(Aa3

)

SKo

r(Aa3

)

Brz(Baa3)

Page 19

Global Economic Scenario / 28 January 2016

Very recent developments show little impact on long term rates also at the start of the year M10 and 10yT yields % Source: BBVA Research, Bloomberg

M10 and 10yT yields Last two months, % Source: BBVA Research, Bloomberg

1.5

1 .7

1 .9

2 .1

2 .3

2 .5

2 .7

2 .9

3 .1

5 .1

5 .3

5 .5

5 .7

5 .9

6 .1

6 .3

6 .5

6 .7

Jan-14

Mar-14

May-14

Jul-1

4

Sep-14

Nov

-14

Jan-15

Mar-15

May-15

Jul-1

5

Sep-15

Nov

-15

Jan-16

M10 ,lhs 10yT, rhs

1.952.002.052.10

2.152.202.252.302.35

6.10

6.15

6.20

6.25

6.30

6.35

6.40

1-Dec

4-Dec

7-Dec

10-Dec

13-Dec

16-Dec

19-Dec

22-Dec

25-Dec

28-Dec

31-Dec

3-Jan

6-Jan

9-Jan

12-Ja

n15

-Jan

18-Ja

n21

-Jan

M10 ,lhs 10yT, rhs

Page 20

Global Economic Scenario / 28 January 2016

Exchange rate and Mexican oil price (ppd and USD per barrel) Source: BBVA Research and Bloomberg

High liquidity currencies. Currencies from oil-exporting countries and MXN * (Index 12/1/2015 = 100) Source: BBVA Research and Bloomberg

Very recent developments show too high volatility in the MXN depreciation: no fear of floating?

* Oil exporting countries: Brazil, Colombia, Russia, Norway, Canada. High liquidity currencies: South Korean Won, Singapore dollar, Taiwan dollar and Hong Kong dollar.

98

100

102

104

106

108

110

112

114

1-Dec 8-Dec 15-Dec 22-Dec 29-Dec 5-Jan 12-Jan 19-Jan

OilExporting HighLiquidity MXN

14.0

14.5

15.0

15.5

16.0

16.5

17.0

17.5

18.0

Jan-15

Feb-15

Mar-15

Apr-15

May-15

Jun-15

Jul-1

5

Aug-15

Sep-15

Oct-15

Nov-15

Dec-15

FED-leduncertainty

FED-leduncertainty

ConcernsoverChina'scycle

OPEPdeniesoilproduction cut

Page 21

Global Economic Scenario / 28 January 2016

Inflation in inflation-targeting (IT) countries %YoY Source: BBVA Research, Bloomberg, Central Banks

So far, so good: as opposed to peers, inflation in Mexico is likely to remain comfortably on target

Page 22

0

2

4

6

8

10

12

BRA CHI COL PER MEX CB's target range Current inflation (Jan - 16) Forecast (Dec - 16)

Inflation in IT countries %YoY Source: BBVA Research, Bloomberg, Central Banks

0

2

4

6

8

10

12

Jun-15

Dec-15

Jun-16

Dec-16

Jun-17

Dec-17

Jun-15

Dec-15

Jun-16

Dec-16

Jun-17

Dec-17

Jun-15

Dec-15

Jun-16

Dec-16

Jun-17

Dec-17

Jun-15

Dec-15

Jun-16

Dec-16

Jun-17

Dec-17

Jun-15

Dec-15

Jun-16

Dec-16

Jun-17

Dec-17

Brasil Chile Colombia Perú México

ForecastInflation target

Global Economic Scenario / 28 January 2016

In Mexico the pass-through is limited and the peso seems to have overreacted compared to fair value

Page 23

Pass through to inflation from a 1% depreciation of the exchange rate to the USD Source: BBVA Research

Exchange rate vs USD: over-undervaluation (%) Source: BBVA Research

-30

-20

-10

0

10

20

30

ARG BRA CHI COL MEX PER

Jan-16 Oct-15

unde

rval

uatio

n ov

erva

luat

ion

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

BRA CHI COL MEX PER URU

may-15 may-14

Global Economic Scenario / 28 January 2016

Page 24

Financial markets: What can we read from recent developments and if so, how does Mexico fare?

Unlikely! Not likely yet!

Probably! Uncertainty about China (growth, rebalancing and FX policy) and persistently low oil prices raise the risk of second round effects (higher vulnerabilities in corporates affecting banks and sovereigns, especially in the oil sector) that could become self-fulfilling.

Is it a downward revision of the

baseline global outlook?

Is it the threat of risk scenarios going

forward in this new world?

Is it a belated

re-pricing of the Fed´s liftoff?

Is it a belated re-pricing of the

Fed´s liftoff?

Global Economic Scenario / 28 January 2016

Page 25

Financial markets: Are they pricing a 2nd round of tail risks on corporates, sovereign & quasi-sovereign?

EM Corporate bond index (spread bp) Source: JP Morgan, BBVA Research

EM Corporate debt index (spread bp) Source: JP Morgan BBVA Research,

0,0

200,0

400,0

600,0

800,0

1.000,0

1.200,0

Jan-07 Jan-09 Jan-11 Jan-13 Jan-15

CEMBI Mexico CEMBI Brazil CEMBI Colombia

CEMBI Chile CEMBI Peru

0

200

400

600

800

1.000

1.200

1.400

1.600

1.800

2.000

May-07 May-09 May-11 May-13 May-15

CEMBI Asia CEMBI Latam CEMBI EM Europe

US: estimated probability of default in the Oil and Gas sector Source: Bloomberg and BBVA Research

(*) S&P 500 subsector default probability (weigthed average of default probability implied in CDS of S&P500 enery companies). Assumning rate of recovery of 70%

0%

20%

40%

60%

80%

100%

Drilling

Expl. &

Prod.

Stor. &

Transp.

Refining &

M.

Equip. &

Serv.

Integrated

Current porbability of default 01/07/2015

+29%

+36% +32%

+10%

+5% +7%

Global Economic Scenario / 28 January 2016

The direct impact of China’s slowdown on Mexico should be quite small

Source: BBVA Research, WEO

Mexico, exports of goods to its partners (Top 10 trade partners, millions, US dollars)

FDI to Mexico by country (% of total, 2014)

US

Canada

China

Spain

Brazil

Colombia

Germany

India

Japan

Netherlands

US

Spain

Canada

Germany

Netherlands

Japan

France

Other

China

Source: BBVA Research, SE

Page 26

Global Economic Scenario / 28 January 2016

Monthly oil trade balance (figures in USD millions) Source: BBVA Research with data of INEGI

Is Mexico too dependent on oil?… a deficit in oil trade balance, a higher current account deficit

-3.2

-2.4

-2.7

-2.4

-2.0

-1.1

-0.8-1.1

-0.8

-1.4

-1.9

-0.9

-0.4

-1.1-1.3

-2.4

-1.9

-3.1

-3.5

-3.0

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Current account balance (% of GDP) Source: BBVA Research with data of INEGI and Bank of Mexico

-1,500

-1,000

-500

0

500

1,000

1,500

2,000

2,500

Jan-93

Jan-94

Jan-95

Jan-96

Jan-97

Jan-98

Jan-99

Jan-00

Jan-01

Jan-02

Jan-03

Jan-04

Jan-05

Jan-06

Jan-07

Jan-08

Jan-09

Jan-10

Jan-11

Jan-12

Jan-13

Jan-14

Jan-15

Page 27

Global Economic Scenario / 28 January 2016

Is Mexico too dependent on oil?… importance in fiscal revenues Fiscal revenues (% GDP) Source: BBVA Research with data from the Ministry of Finance

Page 28

0

2

4

6

8

10

12

14

16

18

20

22

24

2009 2010 2011 2012 2013 2014 2015

Total Revenues Total Oil Revenues

Federal Government Oil Revenues Pemex Oil Revenues

Global Economic Scenario / 28 January 2016

How vulnerable are emerging countries?

Page 29

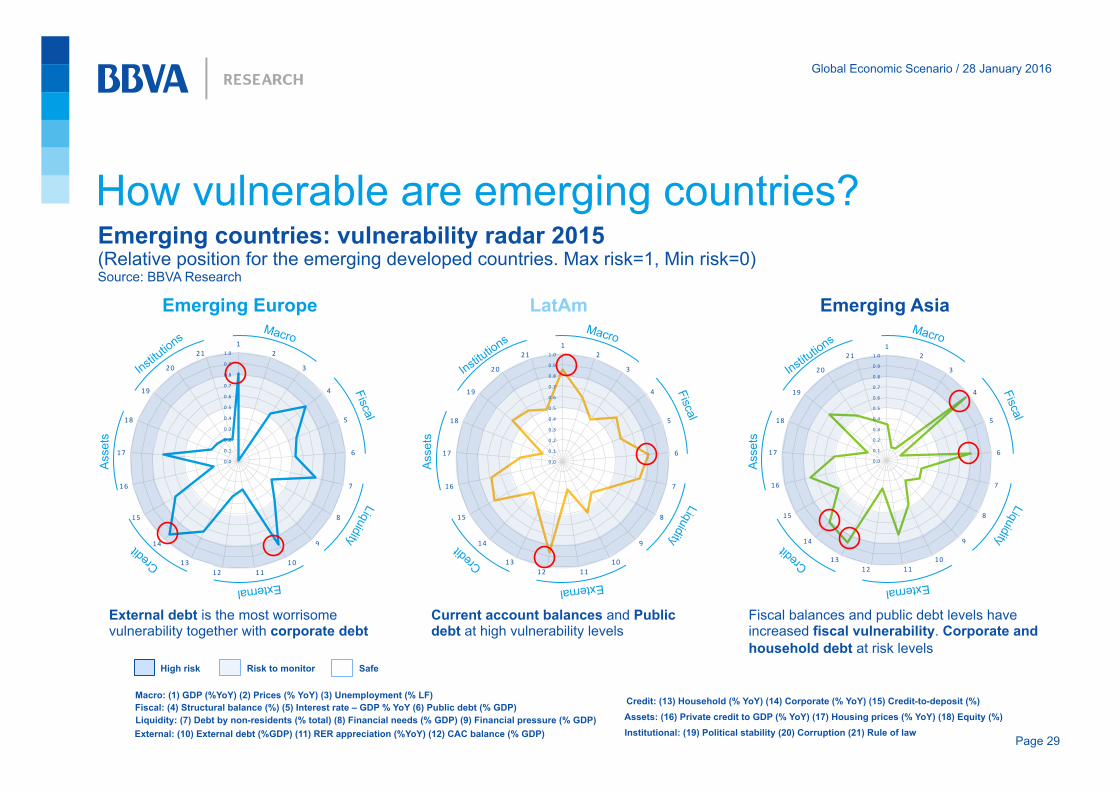

Macro: (1) GDP (%YoY) (2) Prices (% YoY) (3) Unemployment (% LF) Fiscal: (4) Structural balance (%) (5) Interest rate – GDP % YoY (6) Public debt (% GDP) Liquidity: (7) Debt by non-residents (% total) (8) Financial needs (% GDP) (9) Financial pressure (% GDP) External: (10) External debt (%GDP) (11) RER appreciation (%YoY) (12) CAC balance (% GDP)

Credit: (13) Household (% YoY) (14) Corporate (% YoY) (15) Credit-to-deposit (%) Assets: (16) Private credit to GDP (% YoY) (17) Housing prices (% YoY) (18) Equity (%) Institutional: (19) Political stability (20) Corruption (21) Rule of law

0 .0

0 .1

0 .2

0 .3

0 .4

0 .5

0 .6

0 .7

0 .8

0 .9

1 .0

12

3

4

5

6

7

8

9

101112

13

14

15

16

17

18

19

20

21

0 .0

0 .1

0 .2

0 .3

0 .4

0 .5

0 .6

0 .7

0 .8

0 .9

1 .0

12

3

4

5

6

7

8

9

101112

13

14

15

16

17

18

19

20

21

0 .0

0 .1

0 .2

0 .3

0 .4

0 .5

0 .6

0 .7

0 .8

0 .9

1 .0

12

3

4

5

6

7

8

9

101112

13

14

15

16

17

18

19

20

21

High risk Risk to monitor Safe

Emerging Europe LatAm Emerging Asia

Ass

ets

Macro

External

External debt is the most worrisome vulnerability together with corporate debt

Current account balances and Public debt at high vulnerability levels

Fiscal balances and public debt levels have increased fiscal vulnerability. Corporate and household debt at risk levels

Emerging countries: vulnerability radar 2015 (Relative position for the emerging developed countries. Max risk=1, Min risk=0) Source: BBVA Research

Ass

ets

Macro

External

Ass

ets

Macro

External

Global Economic Scenario / 28 January 2016

0 .0

0 .1

0 .2

0 .3

0 .4

0 .5

0 .6

0 .7

0 .8

0 .9

1 .0

12

3

4

5

6

7

8

9

101112

13

14

15

16

17

18

19

20

21

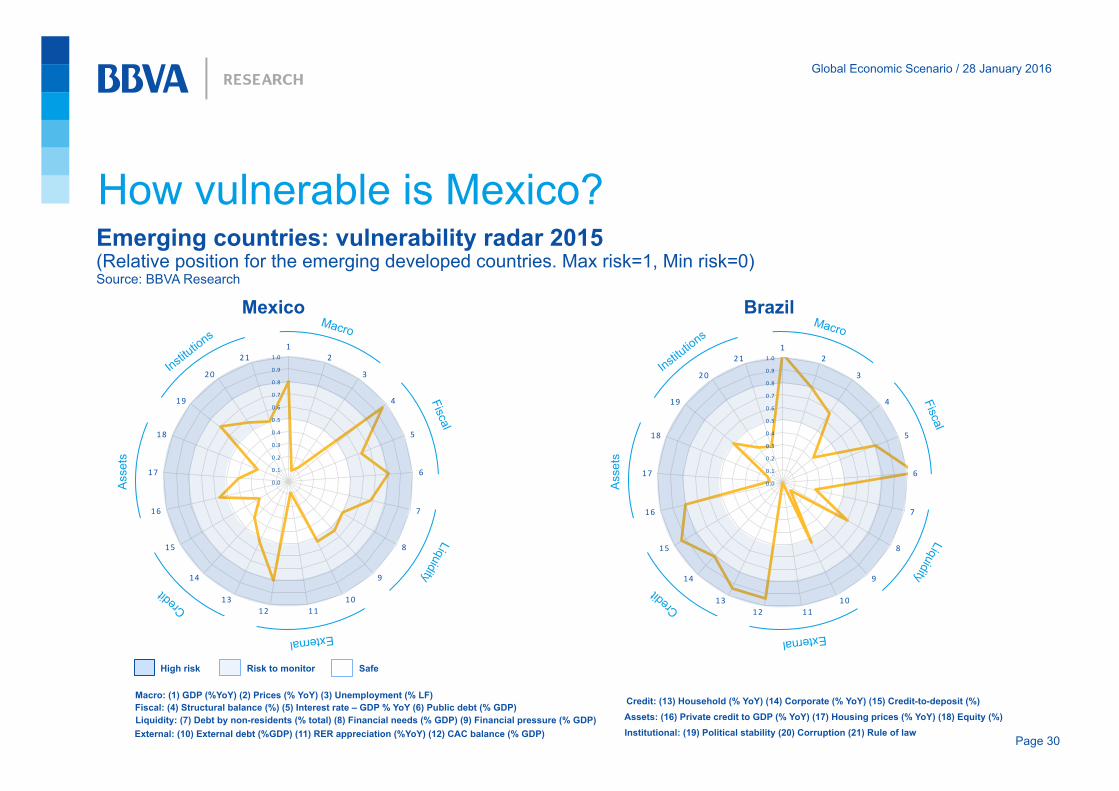

How vulnerable is Mexico?

Page 30

Emerging countries: vulnerability radar 2015 (Relative position for the emerging developed countries. Max risk=1, Min risk=0) Source: BBVA Research

0 .0

0 .1

0 .2

0 .3

0 .4

0 .5

0 .6

0 .7

0 .8

0 .9

1 .0

12

3

4

5

6

7

8

9

101112

13

14

15

16

17

18

19

20

21

Mexico Brazil

Macro: (1) GDP (%YoY) (2) Prices (% YoY) (3) Unemployment (% LF) Fiscal: (4) Structural balance (%) (5) Interest rate – GDP % YoY (6) Public debt (% GDP) Liquidity: (7) Debt by non-residents (% total) (8) Financial needs (% GDP) (9) Financial pressure (% GDP) External: (10) External debt (%GDP) (11) RER appreciation (%YoY) (12) CAC balance (% GDP)

Credit: (13) Household (% YoY) (14) Corporate (% YoY) (15) Credit-to-deposit (%) Assets: (16) Private credit to GDP (% YoY) (17) Housing prices (% YoY) (18) Equity (%) Institutional: (19) Political stability (20) Corruption (21) Rule of law

High risk Risk to monitor Safe

Ass

ets

Macro

External

Ass

ets

Macro

External

Global Economic Scenario / 28 January 2016

Bank loans in foreign currency by term to maturity (3Q15) Thousand million real and % of total

Foreign currency debt by Mexican firms Corporte vulnerability is limited

Fuente: BBVA Research 31

18.5%

10.2%

15.3%

20.0%

12.2%

23.7%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

0

50

100

150

200

250

300

350

400

Menos de 1 año

Hasta 1 año

Hasta 2 años

Hasta 3 años

Hasta 4 años

5 años o más

Total

Nacional Extranjera Porcentaje del total

Pass due loans (IMOR) of corporates for local and foreign currencuy loans (%)

0.6

3.1

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

ene-

08ju

l-08

ene-

09ju

l-09

ene-

10ju

l-10

ene-

11ju

l-11

ene-

12ju

l-12

ene-

13ju

l-13

ene-

14ju

l-14

ene-

15ju

l-15

IMOR ME IMOR total (MN + ME)

Global Economic Scenario / 28 January 2016

1. A structural outlook of the Mexican economy: a journey trough strength and weaknesses

2. Recent developments: growth, markets, vulnerabilities

3. Second generation of economic reforms

Contents

Page 32

Global Economic Scenario / 28 January 2016

A few comments on the reforms

Page 33

Telecommunications and competition reform

Energy reform It is more than petroleum

New entrants and new benefits

Education Key but so many things to fix

What is missing?

Global Economic Scenario / 28 January 2016

Ease of doing business in Mexico (0-100 scale, 0= worst performance, 100 = the frontier) Source: BBVA Research with WB data.

69.5

70.0

70.5

71.0

71.5

72.0

72.5

73.0

73.5

74.0

2014 2015 2016

Distance to Frontier

01020304050607080

Mex

ico

Chi

le

Col

ombi

a

Chi

na

Reg

iona

l ave

rage

(LA

and

C

arib

bean

)

Bra

zil

Arg

entin

a

Indi

a

Distance to Frontier (2016)

Ease of doing business in various countries (0-100 scale, 0= worst performance, 100 = the frontier) Source: BBVA Research with WB data.

Page 34

The ease of doing business has improved with structural reforms

Global Economic Scenario / 28 January 2016

Where are we?

Page 35

Mexico has built a solid framework for macroeconomic stability in the past 20 years. It has helped to differentiate the country form other EM´s in these times of global turbulence, which does not mean that it is immune to the volatility.

However, the growth track-record has been poor. This is a consequence of stagnant productivity

Recent reforms will help with this, but…

Other reforms are needed, especially on Rule of Law, for the country to exploit its full potential

Outlook on Mexico

So far, a tale of macro stability but still moderate growth: what is the outlook?

Monterrey, 1 February 2016

Jorge Sicilia, BBVA Research

GIC Meeting