opportunities and challenges of infrastructure financing in...

TRANSCRIPT

Opportunities and Challenges of Infrastructure Financing in Sub-

Saharan Africa IIIC Conference

Johannesburg, September 2014 Presentation by ECIC CEO,

Kutoane Kutoane

The Fact Sheet – what we know

• Infrastructure plays a key role in economic

growth and poverty reduction as well as in

regional integration.

• The lack of infrastructure affects productivity and

raises production and transaction costs, which

hinders growth by reducing the competitiveness

of businesses.

• The lack of infrastructure is a continental problem

that requires a continental solution.

2

The Fact Sheet – what we know

• Huge infrastructure deficits – some $90 bn pa. • Power Generation, Transmission and maintenance $40

– $45 bn pa followed by transportation, water supply and sanitation

• Funding falls short of demand – less than 15% • Governments in SSA have put infrastructure

development at top of policy agenda • Investment in SSA infrastructure remain elusive despite

high growth and returns offered. • Many challenges and risks (external and internal) • Unpredictable economic policy environment

3

The Fact Sheet – what we know

• Africa presents many investment opportunities in terms of:

1. Resources: - Africa has about 20% of the world’s land mass

- Africa is endowed with minerals and oil resources

2. Manpower: – With more than 1 billion people (2010) Africa has

about 16% of the world’s population

3. Sustained economic growth over the past decade – ranges 6 – 10%

4

The Fact Sheet – what we know

• Based on the statistics reported by PIDA: – the road access rate is only 34%, compared with 50% in

other parts of the developing world. –Transport costs are higher by up to 100%. –Only 30% of the population has access to electricity,

compared to up to 90% in other parts of the developing world.

–Water resources are underused, with only 4% of water resources developed for water supply, irrigation and hydropower use. Only about 18% of the continent’s irrigation potential being exploited. ]

5

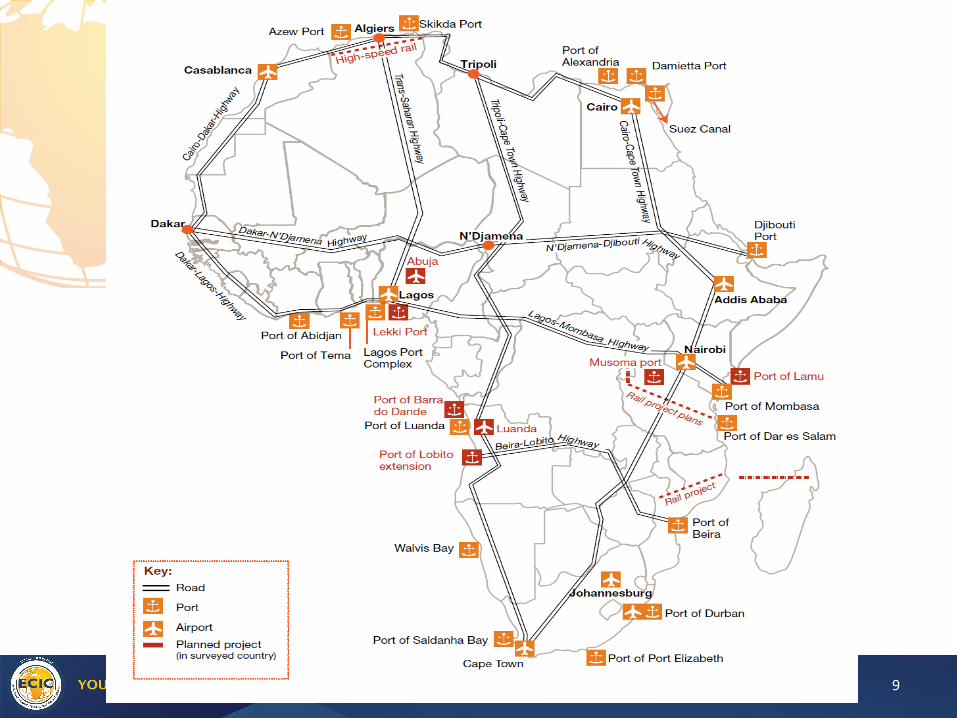

The Opportunity Space - Transport

• Future Freight transport and ports development tied to growth in intra-regional trade

• Current planned ports and terminal expansion projects include:

- Tema in Ghana - Lagos in Nigeria - Mombasa in Kenya - Lobito in Angola - Da-e-Salam port - All Mozambique ports upgrade

6

The Opportunity Space - Transport

• Traffic growth on roads/railways corridors will depend on mineral development, particularly iron ore, bauxite, coal, copper mining projects.

• There are opportunities in multimodal development corridors (e.g. North South Corridor, maritime corridors)

• Airports: Most airports’ capacity will be exceeded by 2020 under the current forecasts.

7

The Opportunity Space - Transport

• Johannesburg and Cairo, for example, will have to expand their capacity to face the increase number of passengers per year by 2040

• Most air-traffic control systems will reach saturation between 2020 and 2030 and will need to be replaced with satellite-based air traffic control system.

8

9

The Opportunity Space - Energy

• Modernization of Africa’s economies, social progress and a commitment to widening access to electricity, will boost energy demand in Africa by an average 5.7% annually through 2040, a 6 fold increase.

• Based on PIDA’s report, Africa’s demand for primary energy is expected to increase by 8.9% annually through 2040.

• For that reason, gas, nuclear and renewables power need to be explored and developed to meet increasing demand.

10

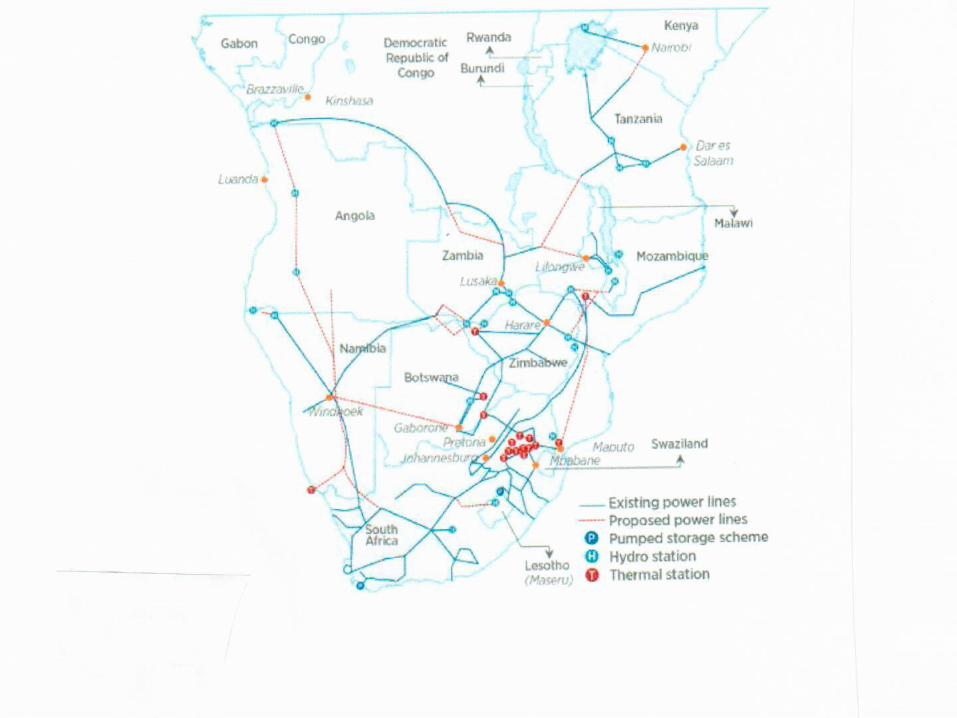

The Opportunity Space - Energy

• Grand Inga with a potential for 40,000MW which can provide power for most of the Southern Africa

• Recent discovery of LNG gas in Mozambique can provide gas, petroleum products and electricity to various countries within and outside the region.

• Uranium mining which can be utilized to produce nuclear power.

• Wind and solar power potential for renewable power generation.

11

12

The Opportunity Space - Water

• Africa’s trans boundary water resources - unevenly distributed, but potential to contribute to food and energy production and to poverty reduction

• With a flow of 3,931km3 of water, Africa count for 9.2% of the world’s total internal water resources.

• However, Africa has the lowest level of irrigated agriculture of any world region. About half the African continent faces water scarcity and large part of the population does not have access to clean water.

• Additional capacity to seize opportunities in hydropower is still lacking

13

Challenges

• Africa faces multiple challenges:

- The continent is highly fragmented; it is home to over two-thirds of the world’s least developed countries, many of are landlocked.

- Financial capacity to execute mega-infrastructure projects is still lacking

- Technical know-how has to be imported

- Infrastructure regulatory and policy frameworks at regional levels are not harmonized

14

Challenges

• Lack of alignment with national and regional priorities is a primary failure factor in terms of the execution of infrastructure projects.

• Raising finance and reaching financial closure are for complex infrastructure projects is challenging

• Lack of experienced project promoters • Conflict of interest of different parties involved in

project execution often affects the commitment of all partners.

• Insufficient revenue collection on infrastructure projects affect the coverage of operating expenses, maintenance or expansion.

15

Key Investment Challenges

• Shortage of private sector investors willing to risk capital on long term complex projects

• No capital market sources of long term funding for Greenfields.

• Poor investment climate in many countries – public debt rising in most high growth countries

• Regional/cross-border projects endure high cost of preparation and lack of regional institutional drivers

• Risk of border closures, contract cancellations, political interference and regional conflicts.

16

Key Investment Challenges

• Tariffs do not cover costs – arbitrary setting • Poor public investment framework leading to

poor public infrastructure spending in PPPs • Lack of infrastructure maintenance capacity • Frequent delays in licensing and permitting • Poor and costly tendering and procurement

procedures. • Lack of credit worthiness of SSA countries • Cost overruns due to lack of adequate planning

and lengthy contract negotiation

17

Many Political Risks

• Lack of established constitutional democracy in some countries

• Arbitrary review of mineral contracts or concessions

• Instability and civil disturbances in certain African countries

• Terrorism activities (Al-Shabab and Boko Haram) • Negative perception associated with resources

nationalism • Breach of contractual obligations by governments

18

ECAs and Risk Solutions

• Many private investors and financiers need ECA backing for SSA projects

• ECAs provide investors with comfort of official insurance and guarantees support enabling bankability

• In SA many cross-border investment companies should benefit from using ECIC support

• ECIC can help mitigate risks (PRI and CRI)

19

Benefits of ECIC-backed Financing

• For SA government, increased exports and export-led industrialization, growth and employment.

• Banks able to limit or remove credit risk – view ECIC backing as SA government’s commitment and support for export of capital goods and services.

• Buyers(importers) able to secure long-term financing at competitive rates (CIRR guided)

• Better assessment of risk and ability to provide cover in particularly risky SSA jurisdictions.

20

Risks underwritten by ECIC

• Provide 100% PRI and 85% CRI cover to enable long term financing where risks are particularly high as in many SSA countries. – State interference in projects – Breach of underlying contract or concession – Cancellation or non-renewal of supply

contract – Currency inconvertibility (transfer risk) – Expropriation or creeping expropriation,

confiscation and nationalization.

21

Risks underwritten by ECIC

– Acts of war, civil unrest, sabotage or terrorism

– Fair and unfair calling of contractual bonds

– Non-honoring of bank guarantees or LCs

– Protracted default on the side of buyer/ borrower

22

ECIC Product Offerings

• Buyers credit insurance cover

• Supplier’s credit insurance cover

• Equity investment insurance

• Performance bond insurance

• Small and Medium Transactions (SMT) support

• Currently exploring shorter term working capital support products.

23

Current ECIC footprint

• Tolled road Zimbabwe

• Tolled road Nigeria

• Power (SHEP 4) Ghana

• Power distribution Ghana

• Locomotives Sierra Leone

• Locomotives DR Congo

• Railways Zambia

24

Enquires received and reviewed

• ECIC has received a number of enquiries, among which:

Ghana Power IPP

Kenya Wind farm

Nigeria Hydro power plant

Mozambique Port expansion

Mozambique Supply of Locomotives

Zimbabwe Supply of locomotives

Guinea Port expansion

DRC Airport expansion

South Sudan Fibre Optic network and power

25

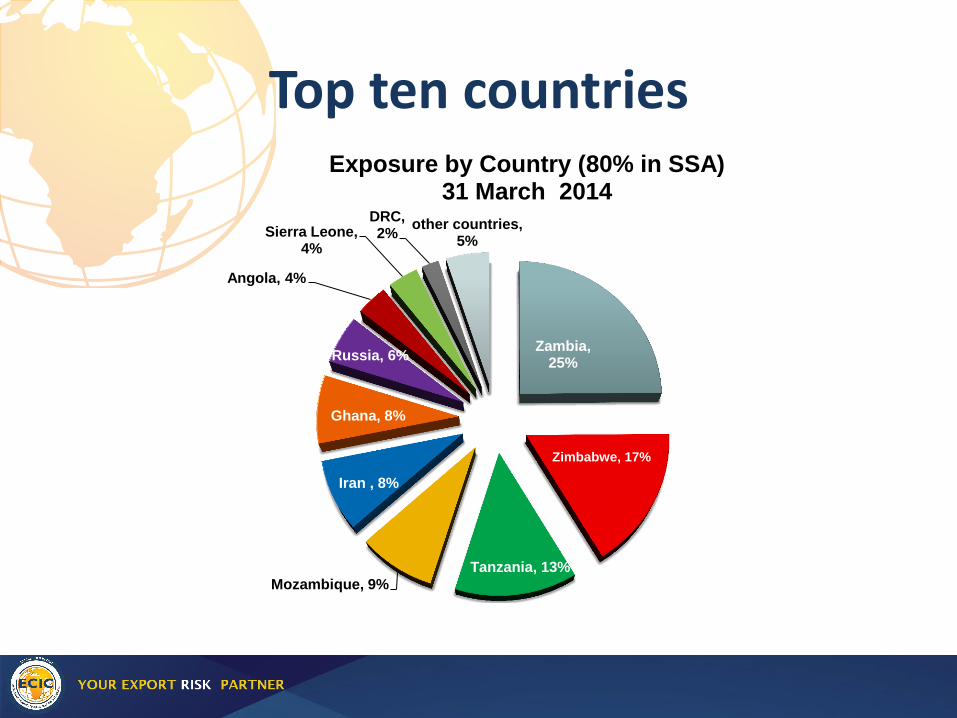

Top ten countries

Zambia, 25%

Zimbabwe, 17%

Tanzania, 13%

Mozambique, 9%

Iran , 8%

Ghana, 8%

Russia, 6%

Angola, 4%

Sierra Leone, 4%

DRC, 2%

other countries, 5%

Exposure by Country (80% in SSA) 31 March 2014

What is to be done

1. Ensure the preparation of viable/development-oriented and bankable projects

2. Financial sustainability of project funding - develop transparent and user friendly investment environment

3. Commitment by the leadership and sense of ownership. 4. Appropriate policy, institutional and regulatory

framework. 5. Partnership with private sector in infrastructure

development (as a result of fiscal limitations and competing needs from other urgent socio-economic sectors)

6. Adoption of the user pay principle (for quick rehabilitation of infrastructure) and instill the culture in the population.

27

Finally

For SA cross-border investors and exporters of capital goods and services make ECIC your trusted risk partner.

Corporate Boards and banks MUST INSIST ON ECIC INSURANCE COVER as a condition of approval for SA companies undertaking projects in SSA. This will improve bankability and unlock long term funding for infrastructure.

28