mercer capital's value focus: construction industry | q3 2015

TRANSCRIPT

BUSINESS VALUATION & FINANCIAL ADVISORY SERVICES

Construction Overview Construction & National GDP 1Construction & National Unemployment 2Value of Construction Put-in-Place 3

Sector Focus Roads, Bridges, & Highways 4

Government Funding for Highways and Local and State Government Investment 5Price of Cement 6Yield on 10-Year Treasury 7

Sector Round-up Residential Construction 8Building Materials 10Nonresidential 11

Mergers and Acquisitions 12

Bellwether Stocks & Industry Participants 13

About Mercer Capital 16

VALUE FOCUS

Third Quarter 2015

Construction & Building Materials

SEGMENT FOCUS Roads, Bridges, & Highways

EXECUTIVE INDUSTRY TRENDS

• Federal infrastructure funding is in the works as the House

passes 6 year, $340 billion bill

• Public funding has declined year-over-year, though this trend

should soon reverse with the passing of the new bill

• LafargeHolcim completes its merger, becoming the largest

player in the industry

• Falling treasury yields indicate low financing costs for new

construction projects

www.mercercapital.com

© 2015 Mercer Capital // www.mercercapital.com 1

Mercer Capital’s Value Focus: Construction & Building Materials Third Quarter 2015

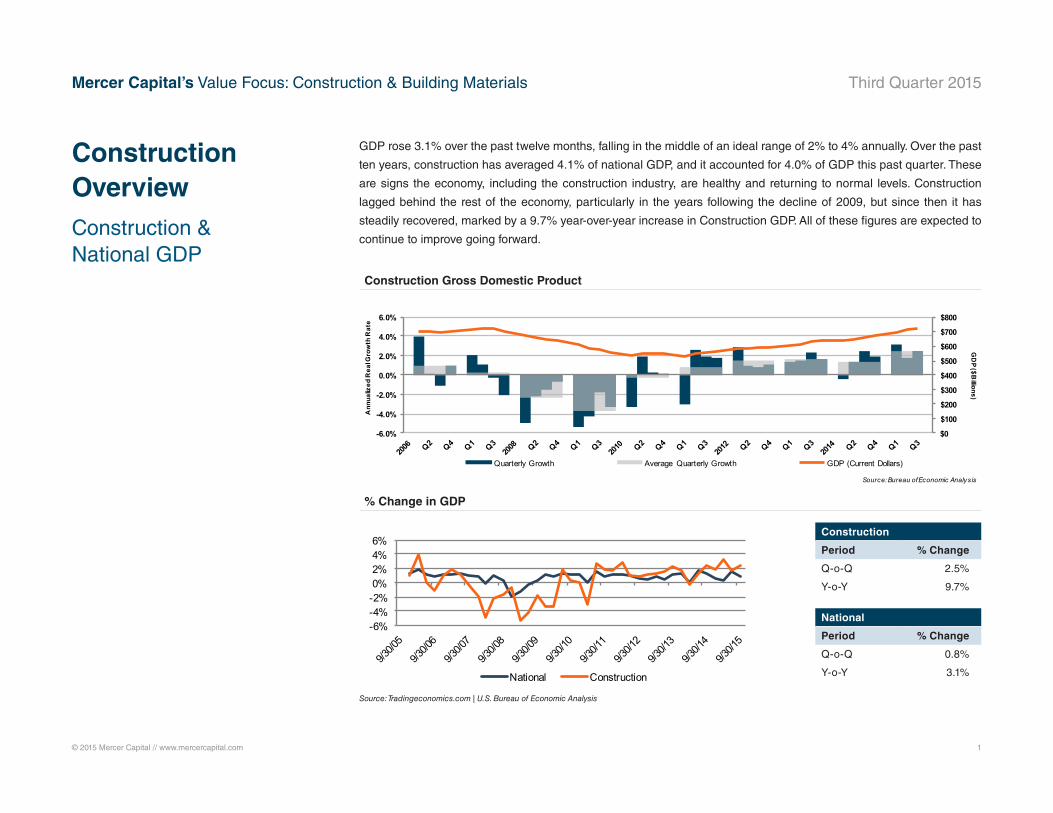

GDP rose 3.1% over the past twelve months, falling in the middle of an ideal range of 2% to 4% annually. Over the past

ten years, construction has averaged 4.1% of national GDP, and it accounted for 4.0% of GDP this past quarter. These

are signs the economy, including the construction industry, are healthy and returning to normal levels. Construction

lagged behind the rest of the economy, particularly in the years following the decline of 2009, but since then it has

steadily recovered, marked by a 9.7% year-over-year increase in Construction GDP. All of these figures are expected to

continue to improve going forward.

$0

$100

$200

$300

$400

$500

$600

$700

$800

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

GD

P ($Billions)

Ann

ualiz

ed R

eal G

row

th R

ate

Quarterly Growth Average Quarterly Growth GDP (Current Dollars)

Source: Bureau of Economic Analysis

-6%-4%-2%0%2%4%6%

National Construction

Construction OverviewConstruction & National GDP

Construction Gross Domestic Product

% Change in GDP

Source: Tradingeconomics.com | U.S. Bureau of Economic Analysis

Construction

Period % Change

Q-o-Q 2.5%

Y-o-Y 9.7%

National

Period % Change

Q-o-Q 0.8%

Y-o-Y 3.1%

© 2015 Mercer Capital // www.mercercapital.com 2

Mercer Capital’s Value Focus: Construction & Building Materials Third Quarter 2015

According to the Federal Reserve, a healthy economy typically has an unemployment rate between 4.5% and 6.0%. The

current level of 5.1% represents strength in the economy, after decreasing steadily from 6.0% a year ago.

Construction is a cyclical and seasonal industry, so its unemployment rate is more volatile. The major contributing

factor to the seasonal nature of the construction industry is the weather. Production of materials and projects in general

decrease during the cold, winter months. Construction unemployment is currently 5.5%, down from 7.0% a year ago.

This number will likely continue to fall during the fourth quarter before inevitably increasing during the cold first quarter

of next calendar year. Lower unemployment rates suggest an increase of activity within the industry.

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

National Construction

Note: In the above graph, the national unemployment rate is seasonally adjusted, but the construction unemployment rate is not in order to show seasonality and recent trends. Source: U.S. Bureau of Labor Statistics

Construction OverviewConstruction & National Unemployment

Unemployment Rate

© 2015 Mercer Capital // www.mercercapital.com 3

Mercer Capital’s Value Focus: Construction & Building Materials Third Quarter 2015

The value of construction put-in-place is the total cost of construction on a job site for a particular period. The U.S.

Census Bureau tracks this data and reports the total monthly. These costs include, but are not limited to, the building

materials, labor, profit, engineering, interest, and taxes.

Year-over-year put-in-place construction has surged, up 21.8% for residential and 10.4% for nonresidential. Despite

rapid yearly growth, both seem to be slowing down this quarter with residential construction increasing by 3.5%, which

is still quite strong, and nonresidential construction increasing by just 0.9%. Higher levels of put-in-place construction

suggest an increase of activity within the industry.

Construction OverviewValue of Construction Put-in-Place

$0

$100

$200

$300

$400

$500

$600

$700

$800

$Billions

Residential Nonresidential

Source: U.S. Census Bureau

Value of Construction Put-in-Place

Residential

Period % Change

Q-o-Q 3.5%

Y-o-Y 21.8%

Nonresidential

Period % Change

Q-o-Q 0.9%

Y-o-Y 10.4%

© 2015 Mercer Capital // www.mercercapital.com 4

Mercer Capital’s Value Focus: Construction & Building Materials Third Quarter 2015

A long-awaited congressional bill for federal highway funding appears imminent, which should provide a boost to the

industry. There has been discussion for months about the potential for such a deal, yet it now seems more likely than

ever. The House passed a six year bill for about $340 billion in funding for highways. The Senate must now reconcile

a similar bill from June; while the bills are similar, funding over the life of the bill is a crucial detail to be finalized. One

potential source of funding is increased gas taxes, which typically fund transportation costs. In the current climate of

depressed oil prices, this seems increasingly palatable.

Duration will likely be a more important aspect of this bill than the final dollar amount. A long-term bill will finally allow

larger projects to be completed. Large, complex projects typically demand long-term funding to get off the ground. This

bill would alleviate pent-up demand and would jumpstart the road construction industry. It should also be noted that it

will take time for this bill to affect revenues. Jobs benefitting from this funding will be commissioned and enter companies’

backlogs, likely becoming revenue towards the latter half of 2016.

Despite the significant strides made for federal funding, local and state governments are taking it upon themselves to

do their part. Texas Proposition 7 is a particularly notable bill as it recently passed and will provide $3 billion annually to

Texas’ Department of Transportation. While the federal funds will help with larger jobs, Proposition 7 targets smaller jobs

focusing on areas where traffic congestion is common.

With funding playing such a critical role in the industry, companies focus a considerable amount of effort on future bids

and winning contracts. Contracts are won by the company who provides the lowest bid, and these projects get added

to their backlogs. This stimulates future revenue, so companies frequently point to their backlogs and pipeline of bids

as an indicator of future revenue as opposed to current revenue. While companies have experienced varying levels of

revenue recently, the outlook is positive for the whole industry as funding is increasing the amount of projects to bid on.

Despite the importance of future growth, companies are focused on current profitability, so they are not sacrificing

margins in order to drive up wins and backlogs. Especially, given the increase in projects to bid on, firms are willing

to lose some bids if it means maintaining margin expectations. It should be noted that larger projects typically build in

margin contingencies, which allows increases over the life of a project, given all goes according to plan. This means

margins stand to increase even further as these new projects entering the pipeline mature.

Sector FocusRoads, Bridges, & Highways

© 2015 Mercer Capital // www.mercercapital.com 5

Mercer Capital’s Value Focus: Construction & Building Materials Third Quarter 2015

Companies that build roads, bridges, and highways largely depend on public funding and clearly benefit from any

increases in public investment or spending. Most projects are funded through local and state governments which spend

their own money or use funds allocated to them by the federal government. Both government funding and local and state

investment are poised to increase moving forward, which represents a strengthening climate for companies in the road,

bridge, and highway construction industry.

Roads, Bridges, & HighwaysGovernment Funding for Highways and Local and State Government Investment

Government Funding for Highways

Local and State Government Investment

$0

$50

$100

$150

$200

$250

$300

$Billions

Source: IBIS World | Bureau of Economic Analysis

$0

$50

$100

$150

$200

$250

$300

$350

$400

$Billions

Source: IBIS World | Bureau of Economic Analysis

Government Funding

for Highways

Period % Change

Y-o-Y -2.1%

Local and State

Government Investment

Period % Change

Y-o-Y 2.6%

© 2015 Mercer Capital // www.mercercapital.com 6

Mercer Capital’s Value Focus: Construction & Building Materials Third Quarter 2015

Road contractors submit bids to local and state governments, and construction jobs are awarded to the lowest bidder.

Higher input costs, like cement, decrease both the volume of projects the government is willing to start and the profit

margins for contractors. Delivery is the most significant cost factor and proximity to a supplier plays a large role in price

because the product is relatively cheap and sold in large, heavy quantities, which makes it a regional product. Because

of these factors, cement, like other building materials, has largely avoided being commoditized. The U.S. Geological

Survey determines the trend of cement prices, and its increase represents a negative sign for the industry.

$0

$20

$40

$60

$80

$100

$120

$140

$ pe

r Ton

Roads, Bridges, & HighwaysPrice of Cement

Price of Cement

Price of Cement

Period % Change

Y-o-Y 5.0%

Source: IBIS World | U.S. Geological Survey

© 2015 Mercer Capital // www.mercercapital.com 7

Mercer Capital’s Value Focus: Construction & Building Materials Third Quarter 2015

The yield on 10-Year Treasury Bonds can indirectly affect the road contracting industry. Higher interest rates make

construction projects more expensive to undertake. When yields on the 10-Year Treasury are low and stable, the

construction industry experiences increased investments and volume. When interest rates are high, it is more expensive

for the public sector to finance industry projects such as road building. As seen in the chart below, the 10-Year yield

has decreased 36 basis points over the past year, more than half of which occurred in this quarter alone. This can

signal an increase in investment as projects remain relatively inexpensive to finance. Especially with an impending

congressional highway bill, all signs point to increased investment, which would greatly benefit the roadbuilding sector

of the construction industry.

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

Source: St. Louis Fed | Board of Governors of the Federal Reserve (US)

Roads, Bridges, & HighwaysYield on 10-Year Treasury

Yield on 10-Year Treasury

Yield on 10-Year Treasury

Period % Change

Q-o-Q -19 BPS

Y-o-Y -36 BPS

© 2015 Mercer Capital // www.mercercapital.com 8

Mercer Capital’s Value Focus: Construction & Building Materials Third Quarter 2015

The National Association of Home Builders uses surveys to produce two indices on the confidence level within the

homebuilding industry. For both surveys, respondents are asked to rate market conditions, with 50 being the index

average. Both indices show clear declines due to the housing crisis, but they have both increased and have been above

50 for over a year. HMI growth has slowed and RMI has actually declined. Crucially, they have both remained above 50.

While fluctuations will continue going forward, it is a positive sign as long as these indices are above average.

0

10

20

30

40

50

60

70

80

90

100

HMI RMI

Note: RMI is measured quarterly and approximated for a monthly basis using a straight-line approach. Source: National Association of Home Builders

Sector Round-upResidential Construction

NAHB Housing Market and Remodeling Market Indices

NAHB HMI

Period % Change

Q-o-Q 1.7%

Y-o-Y 3.4%

NAHB RMI

Period % Change

Q-o-Q -3.3%

Y-o-Y -0.9%

© 2015 Mercer Capital // www.mercercapital.com 9

Mercer Capital’s Value Focus: Construction & Building Materials Third Quarter 2015

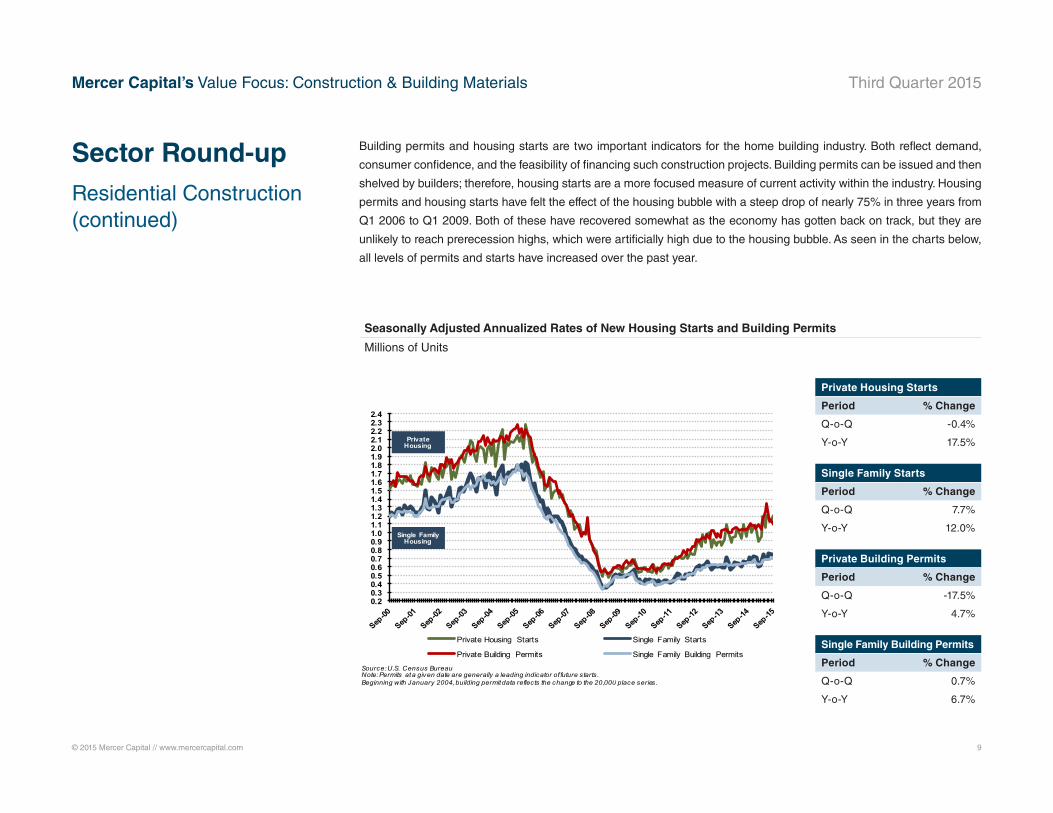

Building permits and housing starts are two important indicators for the home building industry. Both reflect demand,

consumer confidence, and the feasibility of financing such construction projects. Building permits can be issued and then

shelved by builders; therefore, housing starts are a more focused measure of current activity within the industry. Housing

permits and housing starts have felt the effect of the housing bubble with a steep drop of nearly 75% in three years from

Q1 2006 to Q1 2009. Both of these have recovered somewhat as the economy has gotten back on track, but they are

unlikely to reach prerecession highs, which were artificially high due to the housing bubble. As seen in the charts below,

all levels of permits and starts have increased over the past year.

Sector Round-upResidential Construction(continued)

Seasonally Adjusted Annualized Rates of New Housing Starts and Building Permits

Millions of Units

Private Housing Starts

Period % Change

Q-o-Q -0.4%

Y-o-Y 17.5%

Single Family Starts

Period % Change

Q-o-Q 7.7%

Y-o-Y 12.0%

Private Building Permits

Period % Change

Q-o-Q -17.5%

Y-o-Y 4.7%

Single Family Building Permits

Period % Change

Q-o-Q 0.7%

Y-o-Y 6.7%

0.20.30.40.50.60.70.80.91.01.11.21.31.41.51.61.71.81.92.02.12.22.32.4

Private Housing Starts Single Family Starts

Private Building Permits Single Family Building Permits

Source: U.S. Census BureauNote: Permits at a given date are generally a leading indicator of future starts. Beginning with January 2004, building permit data reflects the change to the 20,000 place series.

Private Housing

Single Family Housing

© 2015 Mercer Capital // www.mercercapital.com 10

Mercer Capital’s Value Focus: Construction & Building Materials Third Quarter 2015

Construction aggregates, asphalt, cement, and ready-mix concrete are all essential elements to building and maintaining

roads and highways. Companies that deal in building materials sell a sizeable amount of their products to publicly

funded projects. Therefore, government funding is an important driver for the industry, and companies benefit when

public spending increases. According to the chart below, GCI has increased modestly by 0.4% over the last quarter and

just 0.7% over the past year. If government spending remains low, the industry will feel the negative effects. This is not

expected to persist, however, with a large highway bill hopefully being completed soon.

$2,650

$2,700

$2,750

$2,800

$2,850

$2,900

$2,950

$3,000

$3,050

$3,100

$3,150

$Billions

Source: St. Louis Fed | U.S. Bureau of Economic Analysis

Sector Round-upBuilding Materials

Government Consumption and Investment

Government Consumption

and Investment

Period % Change

Q-o-Q 0.4%

Y-o-Y 0.7%

Source: St. Louis Fed | U.S. Bureau of Economic Analysis

© 2015 Mercer Capital // www.mercercapital.com 11

Mercer Capital’s Value Focus: Construction & Building Materials Third Quarter 2015

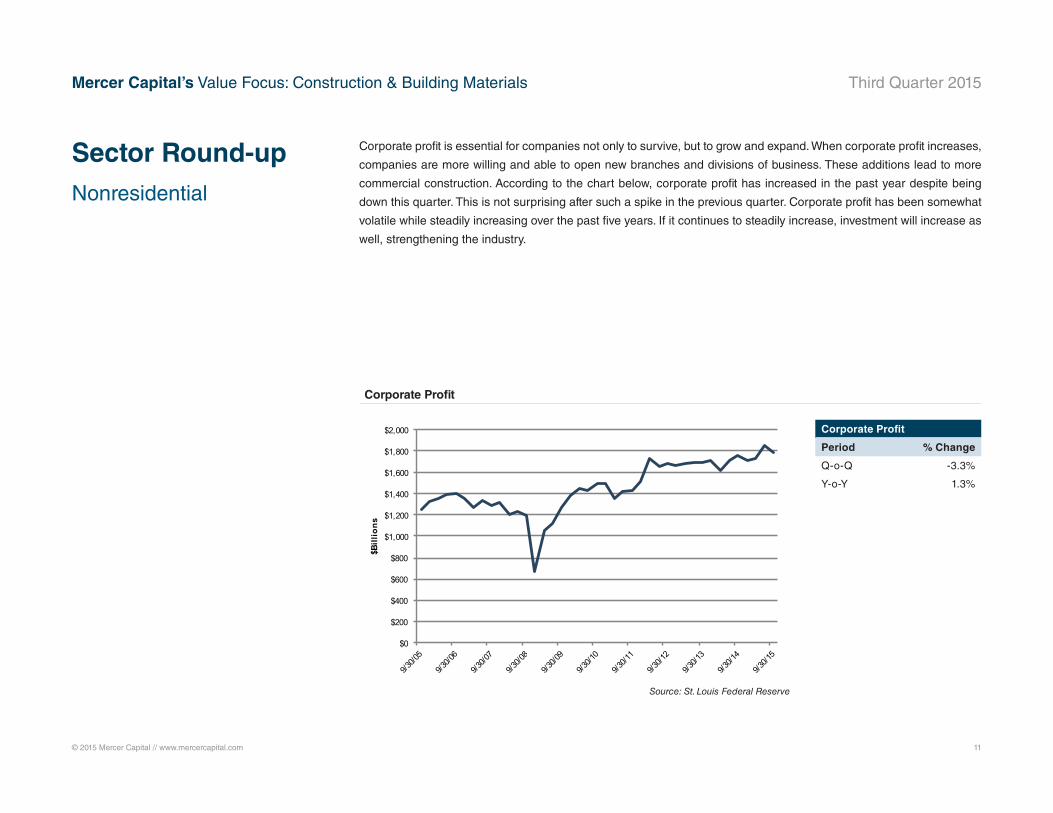

Corporate profit is essential for companies not only to survive, but to grow and expand. When corporate profit increases,

companies are more willing and able to open new branches and divisions of business. These additions lead to more

commercial construction. According to the chart below, corporate profit has increased in the past year despite being

down this quarter. This is not surprising after such a spike in the previous quarter. Corporate profit has been somewhat

volatile while steadily increasing over the past five years. If it continues to steadily increase, investment will increase as

well, strengthening the industry.

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

$2,000

$Billions

Sector Round-upNonresidential

Corporate Profit

Corporate Profit

Period % Change

Q-o-Q -3.3%

Y-o-Y 1.3%

Source: St. Louis Federal Reserve

© 2015 Mercer Capital // www.mercercapital.com 12

Mercer Capital’s Value Focus: Construction & Building Materials Third Quarter 2015

Announce

Date

Industry

Subsector Target/Issuer Buyers/Investors Seller Description

September 25Building

MaterialsCemex, Inc., Gypsum Wallboard

U.S. LBM Holdings,

LLCCEMEX, Inc.

Divestiture of division comprising a cement

manufacturing plant in the U.S.

August 28Building

Materials

E&A Materials, Inc.,

Select AssetsU.S. Concrete, Inc.

E & A Materials

Inc.

Divestiture of some sand and gravel operations in the

U.S.

August 28Building

Materials

Pitts Sand & Gravel, Inc.,

Select AssetsU.S. Concrete, Inc.

Pitts Sand &

Gravel, Inc.Divestiture of 2 sand and gravel operations in the U.S.

August 26 Nonresidential Moll's Utility Services, LLC Dycom Industries Provides construction services based in Hammond, WI.

August 25 Nonresidential TelCom Construction Inc. Dycom Industries Provides utility contractor services across the U.S.

August 18 NonresidentialAecon Group Inc., Atlantic Buildings

Divisions's Construction ActivitiesPomerleau Inc. Aecon Group Inc.

Divestiture of division that provides construction and

engineering services.

August 4Building

Materials

Martin Marietta Materials, Inc.,

California Cement Business Assets

CalPortland

Company, Inc.

Martin Marietta

Materials, Inc.

Divestiture of division business operations in California

manufacturing cement.

August 4Building

Materials

3 aggregates facilities and 7 ready mixed-

concrete operations in AZ and NM

Vulcan Materials

Company Not Stated

Aggregate and ready-mix concrete operations in NM and

AZ.

July 21 Home BuildingCharlotte, Raleigh, and Chicago

Operations and Homebuliding Assets

Taylor Morrison

Home Corporation

Orleans

Homebuilders, Inc.

Divestiture of certain operations and homebuilding

assets in Charlotte, Raleigh, and Chicago.

July 13 Nonresidential AECOM., Quality Programs BusinessSystem One Holdings,

LLCAECOM

Divestiture of division comprising workforce solutions,

quality engineering, product assurance, asset integrity, etc.

Source: Capital IQ

Mergers and Acquisitions

In recent M&A news, U.S. Concrete acquired sand and gravel operations again this quarter, Vulcan Materials added

aggregate and ready-mix facilities, and Martin Marietta sold their California cement business to CalPortland Com-

pany. The big move in building materials, however, was the close of the LafargeHolcim merger. They put the finishing

touches on their deal on July 10th after spending the last quarter announcing divestitures of certain assets to avoid

anti-trust regulation issues. Both sides called it a merger of equals, though the exchange favored Holcim with nine

of their shares going for 10 Lafarge shares. The headquarters of the new company will also be based in Switzerland,

Holcim’s native country. The giant corporation now services 90 countries, has combined net sales of €27 billion, and

can manufacture 368.5 million tons annually.

© 2015 Mercer Capital // www.mercercapital.com 13

Mercer Capital’s Value Focus: Construction & Building Materials Third Quarter 2015

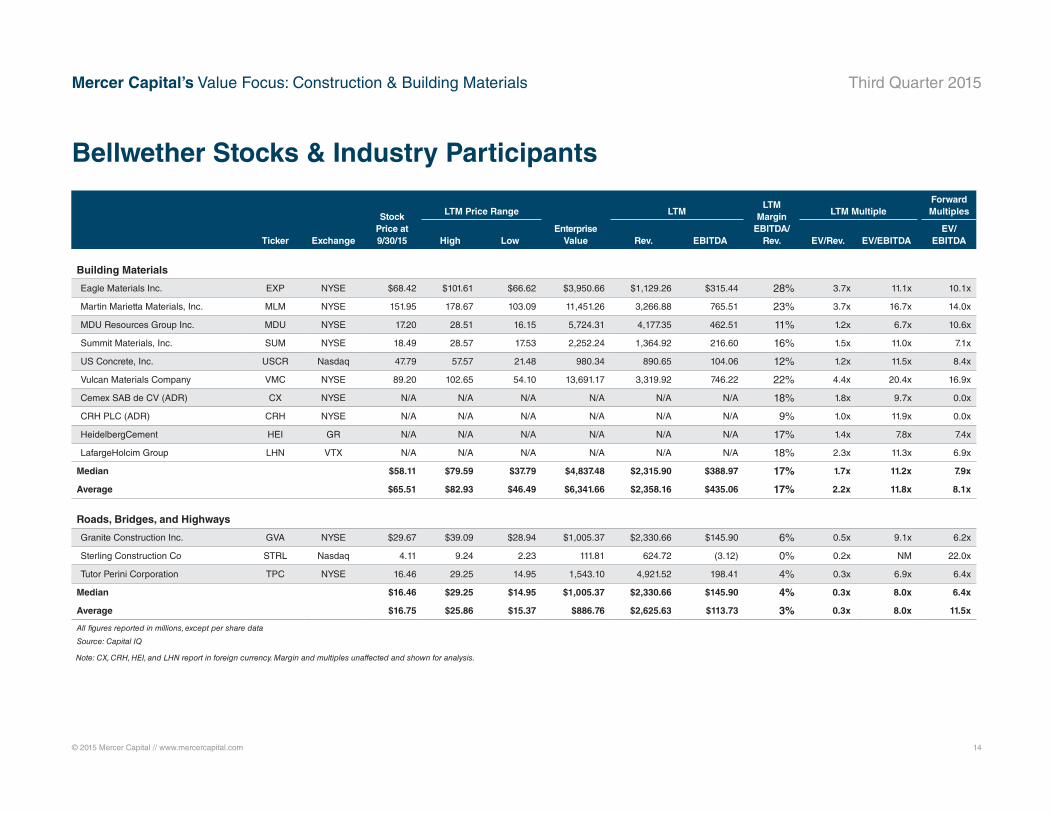

Ticker Exchange

Stock Price at 9/30/15

LTM Price Range

Enterprise Value

LTMLTM

Margin EBITDA/

Rev.

LTM MultipleForward Multiples

High Low Rev. EBITDA EV/Rev. EV/EBITDAEV/

EBITDA

Residential

Beazer Homes USA Inc. BZH NYSE $13.33 $21.19 $13.01 $1,699.23 $1,627.41 $49.13 3% 1.2x 36.8x 12.6x

Comstock Holding Companies, Inc. CHCI Nasdaq 3.54 8.84 2.45 62.96 45.01 (2.06) -5% 1.2x NM 0.0x

DR Horton Inc. DHI NYSE 29.36 33.06 19.29 13,225.31 10,824.00 1,229.20 11% 1.4x 12.3x 10.9x

Hovnanian Enterprises Inc. HOV NYSE 1.77 4.42 1.37 2,363.35 2,153.67 34.93 2% 1.1x 57.1x 16.3x

KB Home KBH NYSE 13.55 18.10 11.76 3,524.61 2,842.29 151.27 5% 1.2x 23.0x 18.4x

Lennar Corporation LEN NYSE 48.13 56.04 37.50 16,466.65 9,112.38 1,135.29 12% 1.8x 13.1x 11.8x

LGI Homes, Inc. LGIH Nasdaq 27.19 30.17 12.21 752.66 561.89 72.22 13% 1.5x 12.3x 9.4x

MDC Holdings Inc. MDC NYSE 26.18 31.23 23.67 2,010.89 1,835.80 107.50 6% 1.1x 19.0x 11.9x

NVR, Inc. NVR NYSE 1,525.22 1,610.00 1,050.95 6,417.56 4,940.67 591.68 12% 1.3x 11.5x 10.6x

PulteGroup, Inc. PHM NYSE 18.87 23.36 16.56 8,176.66 5,742.89 754.20 13% 1.4x 10.1x 9.2x

Toll Brothers Inc. TOL NYSE 34.24 42.19 28.92 8,957.97 4,084.74 484.84 12% 2.2x 17.7x 15.6x

Median $26.18 $30.17 $16.56 $3,524.61 $2,842.29 $151.27 11% 1.3x 15.4x 11.8x

Average $158.31 $170.78 $110.70 $5,787.08 $3,979.16 $418.93 8% 1.4x 21.3x 11.5x

All figures reported in millions, except per share data

Source: Capital IQ

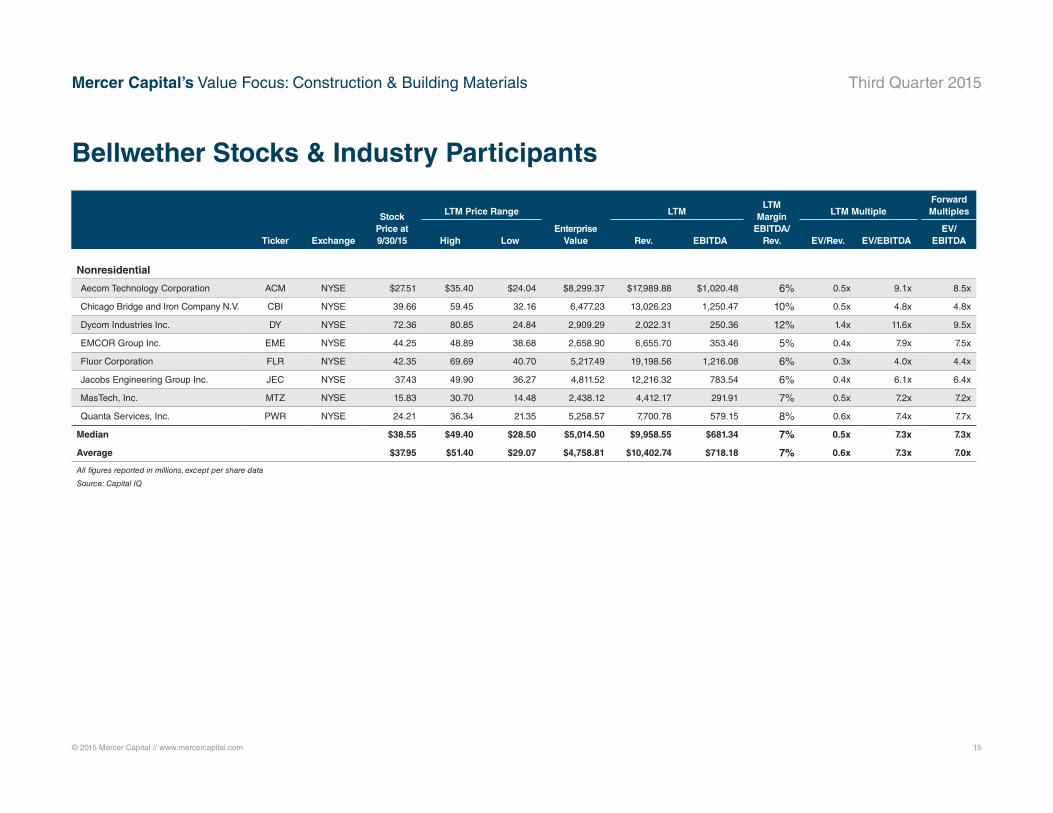

Bellwether Stocks & Industry Participants

© 2015 Mercer Capital // www.mercercapital.com 14

Mercer Capital’s Value Focus: Construction & Building Materials Third Quarter 2015

Ticker Exchange

Stock Price at 9/30/15

LTM Price Range

Enterprise Value

LTMLTM

Margin EBITDA/

Rev.

LTM MultipleForward Multiples

High Low Rev. EBITDA EV/Rev. EV/EBITDAEV/

EBITDA

Building Materials

Eagle Materials Inc. EXP NYSE $68.42 $101.61 $66.62 $3,950.66 $1,129.26 $315.44 28% 3.7x 11.1x 10.1x

Martin Marietta Materials, Inc. MLM NYSE 151.95 178.67 103.09 11,451.26 3,266.88 765.51 23% 3.7x 16.7x 14.0x

MDU Resources Group Inc. MDU NYSE 17.20 28.51 16.15 5,724.31 4,177.35 462.51 11% 1.2x 6.7x 10.6x

Summit Materials, Inc. SUM NYSE 18.49 28.57 17.53 2,252.24 1,364.92 216.60 16% 1.5x 11.0x 7.1x

US Concrete, Inc. USCR Nasdaq 47.79 57.57 21.48 980.34 890.65 104.06 12% 1.2x 11.5x 8.4x

Vulcan Materials Company VMC NYSE 89.20 102.65 54.10 13,691.17 3,319.92 746.22 22% 4.4x 20.4x 16.9x

Cemex SAB de CV (ADR) CX NYSE N/A N/A N/A N/A N/A N/A 18% 1.8x 9.7x 0.0x

CRH PLC (ADR) CRH NYSE N/A N/A N/A N/A N/A N/A 9% 1.0x 11.9x 0.0x

HeidelbergCement HEI GR N/A N/A N/A N/A N/A N/A 17% 1.4x 7.8x 7.4x

LafargeHolcim Group LHN VTX N/A N/A N/A N/A N/A N/A 18% 2.3x 11.3x 6.9x

Median $58.11 $79.59 $37.79 $4,837.48 $2,315.90 $388.97 17% 1.7x 11.2x 7.9x

Average $65.51 $82.93 $46.49 $6,341.66 $2,358.16 $435.06 17% 2.2x 11.8x 8.1x

Roads, Bridges, and Highways

Granite Construction Inc. GVA NYSE $29.67 $39.09 $28.94 $1,005.37 $2,330.66 $145.90 6% 0.5x 9.1x 6.2x

Sterling Construction Co STRL Nasdaq 4.11 9.24 2.23 111.81 624.72 (3.12) 0% 0.2x NM 22.0x

Tutor Perini Corporation TPC NYSE 16.46 29.25 14.95 1,543.10 4,921.52 198.41 4% 0.3x 6.9x 6.4x

Median $16.46 $29.25 $14.95 $1,005.37 $2,330.66 $145.90 4% 0.3x 8.0x 6.4x

Average $16.75 $25.86 $15.37 $886.76 $2,625.63 $113.73 3% 0.3x 8.0x 11.5x

All figures reported in millions, except per share data

Source: Capital IQ

Bellwether Stocks & Industry Participants

Note: CX, CRH, HEI, and LHN report in foreign currency. Margin and multiples unaffected and shown for analysis.

© 2015 Mercer Capital // www.mercercapital.com 15

Mercer Capital’s Value Focus: Construction & Building Materials Third Quarter 2015

Ticker Exchange

Stock Price at 9/30/15

LTM Price Range

Enterprise Value

LTMLTM

Margin EBITDA/

Rev.

LTM MultipleForward Multiples

High Low Rev. EBITDA EV/Rev. EV/EBITDAEV/

EBITDA

Nonresidential

Aecom Technology Corporation ACM NYSE $27.51 $35.40 $24.04 $8,299.37 $17,989.88 $1,020.48 6% 0.5x 9.1x 8.5x

Chicago Bridge and Iron Company N.V. CBI NYSE 39.66 59.45 32.16 6,477.23 13,026.23 1,250.47 10% 0.5x 4.8x 4.8x

Dycom Industries Inc. DY NYSE 72.36 80.85 24.84 2,909.29 2,022.31 250.36 12% 1.4x 11.6x 9.5x

EMCOR Group Inc. EME NYSE 44.25 48.89 38.68 2,658.90 6,655.70 353.46 5% 0.4x 7.9x 7.5x

Fluor Corporation FLR NYSE 42.35 69.69 40.70 5,217.49 19,198.56 1,216.08 6% 0.3x 4.0x 4.4x

Jacobs Engineering Group Inc. JEC NYSE 37.43 49.90 36.27 4,811.52 12,216.32 783.54 6% 0.4x 6.1x 6.4x

MasTech, Inc. MTZ NYSE 15.83 30.70 14.48 2,438.12 4,412.17 291.91 7% 0.5x 7.2x 7.2x

Quanta Services, Inc. PWR NYSE 24.21 36.34 21.35 5,258.57 7,700.78 579.15 8% 0.6x 7.4x 7.7x

Median $38.55 $49.40 $28.50 $5,014.50 $9,958.55 $681.34 7% 0.5x 7.3x 7.3x

Average $37.95 $51.40 $29.07 $4,758.81 $10,402.74 $718.18 7% 0.6x 7.3x 7.0x

All figures reported in millions, except per share data

Source: Capital IQ

Bellwether Stocks & Industry Participants

Mercer CapitalConstruction & Building Materials Industry Services

Contact Us

Copyright © 2015 Mercer Capital Management, Inc. All rights reserved. It is illegal under Federal law to reproduce this publication or any portion of its contents without the publisher’s permission. Media quotations with source attribution are encouraged.

Reporters requesting additional information or editorial comment should contact Barbara Walters Price at 901.685.2120. Mercer Capital’s Industry Focus is published quarterly and does not constitute legal or financial consulting advice. It is offered as an

information service to our clients and friends. Those interested in specific guidance for legal or accounting matters should seek competent professional advice. Inquiries to discuss specific valuation matters are welcomed. To add your name to our mailing list

to receive this complimentary publication, visit our web site at www.mercercapital.com.

Mercer Capital provides valuation and transaction advisory services to the construction and building materials industries.

Industry Segments

Mercer Capital serves construction industry segments from to commercial and civil to residential. We also serve the

building materials sector from aluminum and steel to brick, glass, and lumber.

Mercer Capital Experience

• Family and management succession planning

• Buy-side and sell-side transaction advisory assistance

• Conflict resolution and litigation support

• Trust and estate planning

• Buy-sell agreement valuation, design, and funding advisory

Contact a Mercer Capital professional to discuss your needs in confidence.

Timothy R. Lee, ASA

901.322.9740

Nicholas J. Heinz

901.685.2120

MERCER CAPITAL

Memphis

5100 Poplar Avenue, Suite 2600

Memphis, Tennessee 38137

901.685.2120

Dallas

12201 Merit Drive, Suite 480

Dallas, Texas 75251

214.468.8400

Nashville

102 Woodmont Blvd., Suite 231

Nashville, Tennessee 37205

615.345.0350

www.mercercapital.com

BUSINESS VALUATION & FINANCIAL ADVISORY SERVICES