investor presentation - arescapitalcorp-ir.com · overview of ares management 1. as of december 31,...

TRANSCRIPT

Ares Capital Corporation - Not for Publication or Distribution

Investor Presentation

March 2018

Ares Capital Corporation - Not for Publication or Distribution 2

Disclaimer

IMPORTANT NOTICE:

Statements included herein may constitute “forward-looking statements,” which may relate to future events or the future performance or financial condition of Ares Capital Corporation (“ARCC”), its investment adviser Ares Capital Management LLC (“ACM”), a subsidiary of Ares Management, L.P. (“Ares Management”), or of Ares Management. These statements are not guarantees of future results or financial condition and involve a number of risks and uncertainties. Actual results and conditions may differ materially from those in the forward-looking statements as a result of a number of factors, including those described from time to time in the filings of ARCC and Ares Management with the Securities and Exchange Commission (“SEC”).

The information contained in this presentation is summary information that is intended to be considered in the context of the SEC filings of ARCC and Ares Management and other public announcements that ARCC or Ares Management may make, by press release or otherwise, from time to time. Neither ARCC nor Ares Management undertakes any duty or obligation to publicly update or revise the forward-looking statements or other information contained in this presentation. These materials contain information about ARCC, ACM and Ares Management, and certain of their respective personnel and affiliates, information about their respective historical performance and general information about the market. You should not view information related to the past performance of ARCC, ACM or Ares Management or information about the market, as indicative of future results, the achievement of which cannot be assured.

Nothing in these materials should be construed as a recommendation to invest in any securities that may be issued by ARCC or Ares Management or as legal, accounting or tax advice. None of ARCC, ACM, Ares Management or any affiliate of ARCC, ACM or Ares Management makes any representation or warranty, express or implied, as to the accuracy or completeness of the information contained herein and nothing contained herein shall be relied upon as a promise or representation whether as to the past or future performance. Certain information set forth herein includes estimates and projections and involves significant elements of subjective judgment and analysis. Further, such information, unless otherwise stated, is before giving effect to management and incentive fees and deductions for taxes. No representations are made as to the accuracy of such estimates or projections or that all assumptions relating to such estimates or projections have been considered or stated or that such estimates or projections will be realized.

These materials may contain confidential and proprietary information, and their distribution or the divulgence of any of their contents to any person, other than the person to whom they were originally delivered and such person’s advisers, without the prior consent of ARCC, ACM or Ares Management, as applicable, is prohibited. You are advised that United States securities laws restrict any person who has material, non-public information about a company from purchasing or selling securities of such company (and options, warrants and rights relating thereto) and from communicating such information to any other person under circumstances in which it is reasonably foreseeable that such person is likely to purchase or sell such securities. You agree not to purchase or sell such securities in violation of any such laws.

These materials are not intended as an offer to sell, or the solicitation of an offer to purchase, any security, the offer and/or sale of which can only be made by definitive offering documentation. Any offer or solicitation with respect to any securities that may be issued by ARCC, Ares Management or any of their affiliates will be made only by means of definitive offering memoranda or prospectus, which will be provided to prospective investors and will contain material information that is not set forth herein, including risk factors relating to any such investment.

S&P Disclaimer NoticeThis may contain information obtained from third parties, including ratings from credit ratings agencies such as Standard & Poor’s. Reproduction and distribution of third party content in any form is prohibited except with the prior written permission of the related third party. Third party content providers do not guarantee the accuracy, completeness, timeliness or availability of any information, including ratings, and are not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, or for the results obtained from the use of such content. THIRD PARTY CONTENT PROVIDERS GIVE NO EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE. THIRD PARTY CONTENT PROVIDERS SHALL NOT BE LIABLE FOR ANY DIRECT, INDIRECT, INCIDENTAL, EXEMPLARY, COMPENSATORY, PUNITIVE, SPECIAL OR CONSEQUENTIAL DAMAGES, COSTS, EXPENSES, LEGAL FEES, OR LOSSES (INCLUDING LOST INCOME OR PROFITS AND OPPORTUNITY COSTS OR LOSSES CAUSED BY NEGLIGENCE) IN CONNECTION WITH ANY USE OF THEIR CONTENT, INCLUDING RATINGS. Credit ratings are statements of opinions and are not statements of fact or recommendations to purchase, hold or sell securities. They do not address the suitability of securities or the suitability of securities for investment purposes, and should not be relied on as investment advice.

Ares Capital Corporation - Not for Publication or Distribution 3

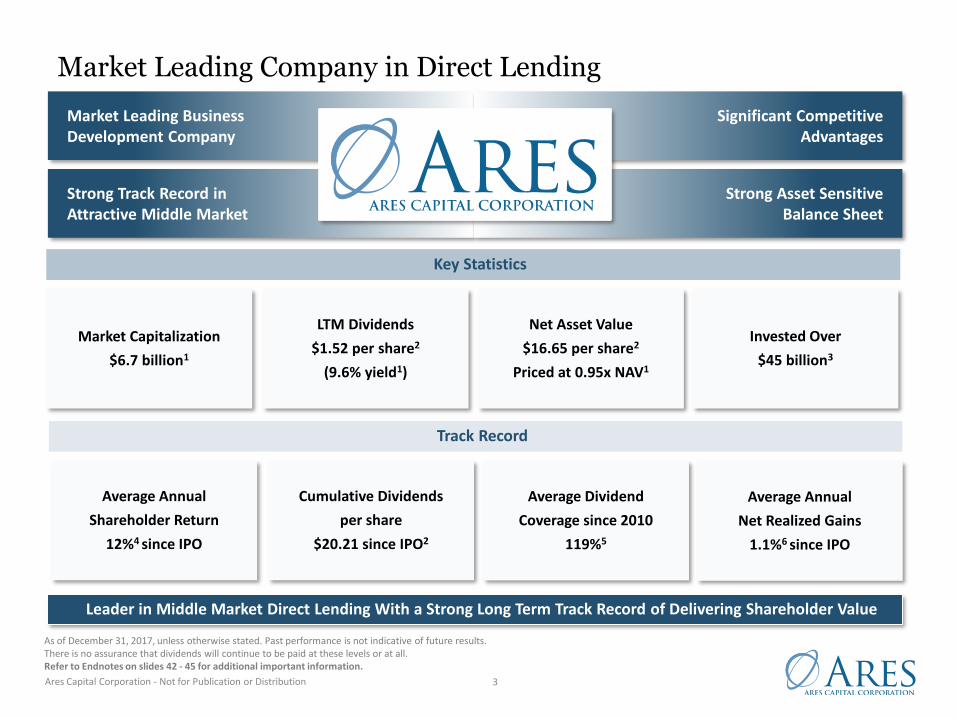

Market Leading Company in Direct Lending

$16.47

Market Leading Business Development Company

Strong Track Record in Attractive Middle Market

Significant CompetitiveAdvantages

Strong Asset Sensitive Balance Sheet

Cumulative Dividends

per share

$20.21 since IPO2

Invested Over

$45 billion3

Track Record

Leader in Middle Market Direct Lending With a Strong Long Term Track Record of Delivering Shareholder Value

Average Dividend

Coverage since 2010

119%5

Average Annual

Net Realized Gains

1.1%6 since IPO

Average Annual

Shareholder Return

12%4 since IPO

Net Asset Value

$16.65 per share2

Priced at 0.95x NAV1

Market Capitalization

$6.7 billion1

LTM Dividends

$1.52 per share2

(9.6% yield1)

Key Statistics

As of December 31, 2017, unless otherwise stated. Past performance is not indicative of future results. There is no assurance that dividends will continue to be paid at these levels or at all.Refer to Endnotes on slides 42 - 45 for additional important information.

Ares Capital Corporation - Not for Publication or Distribution 4

CREDIT

5%8%

10%14%

17%

SyndicatedLoans

High YieldBonds

Europe DirectLending

U.S. DirectLending

StructuredCredit

Overview of Ares Management

1. As of December 31, 2017, AUM amounts include funds managed by Ivy Hill Asset Management, L.P., a wholly owned portfolio company of Ares Capital Corporation and a registered investment adviser.

Please refer to the Performance Notes on slides 47 – 49 for additional definitions, information and notes.

Ares Management, L.P. is a leading global alternative asset manager with three distinct but complementary investment groups

NET PERFORMANCE RETURNS. Credit: 5% for U.S. Syndicated Loan funds, 7% for U.S. High Yield funds, and 13% for Structured Credit. Private Equity: 17% for ACOF I-IV Aggregate, 9% for EIF Aggregate and 8% for Special Situations. Real Estate: 10% for U.S. Equity, 7% for U.S. Debt and 8% for Europe Equity

REAL ESTATE

7%

15% 15%

Debt U.S. Equity Europe Equity

PRIVATE EQUITY

Global FootprintAres ProfileAs of December 31st, 2017

Founded: 1997

AUM(1): $106bn

Employees: 1,000+

Investment Professionals: ~400

Global Offices: 15+

Listing: NYSE – Market Capitalization $5bn

24%

14% 13%

ACOF I-IV Aggregate EIF Aggregate Special Situations

Gross Annualized Returns Since Inception except Europe and U.S. Direct Lending Asset Level Realized Gross IRRs ITD

Net Annual Return On Equity for ACRE since IPO

Gross IRRs Based on Actual and Projected Cash Flows

Gross Asset Level IRRs Since Inception

Gross Annualized IRR Since Inception

Assets Under Management

$71.7 billion $24.5 billion $10.2 billion

Strategies

High Yield Bonds

Syndicated Loans

Structured Credit

Direct Lending/ARCC

Corporate Private Equity

U.S. Power & Energy Infrastructure

Special Situations

Real Estate Private Equity

Real Estate Debt

Historical Returns

Ares Capital Corporation - Not for Publication or Distribution 5

We have experienced teams across the platform that are positioned for excellence in investing and client service

Advantages

Syndication, Trading & Servicing

6 traders in the U.S. and Europe6 dedicated capital markets professionals

~30 direct lending professionals focused solely on asset management

Origination, Research & Investment Management

14 portfolio managers~55 industry research and structured credit professionals

~120 direct origination professionals11 distressed and restructuring specialists(2)

$71.7 billion AUM(1)

25+ Partners averaging 24 years of experience

~235 dedicated investment professionals

Investor Relations & Business Operations

Established investor relations and client service across the Americas,Europe, Asia, Australia and the Middle East

Note: As of December 31, 2017, unless otherwise noted.1. As of December 31, 2017 AUM amounts include funds managed by Ivy Hill Asset Management, L.P., a wholly owned portfolio company of Ares Capital

Corporation and a registered investment adviser. 2. The performance, awards/ratings noted herein relate only to selected funds/strategies and may not be representative of any given client’s experience and

should not be viewed as indicative of Ares’ past performance or its funds’ future performance. All investments involve risk, including possible loss of principal.Please refer to the Performance Notes on slide 50 for additional information on accolades.

Deep Investment Opportunity Set

Leading Platform of Liquid and Direct Lending Strategies

Ares’ Extensive Credit Group Provides Many Benefits to ARCC

Integrated scaled global platform combines direct origination, deep fundamental credit research and broad perspective of relative value

Access to Differentiated Information to Inform

Credit Decisions

Ability to Express Relative Value

Accolades (2)

Global SponsoredDeal of the Year -

2016

Lender of the YearNorth America

2014, 2015 & 2016

ARCC Received Most Honored Designation & Highest

Rankings for Best CEO, CFO, IR Professional and Investor

Relations Program

Top Quartile Rankings for Several Funds

Syndicated Loans

High Yield

Structured Credit / CMBS

Asset Based Lending

Middle Market Cash Flow Loans

Liquid Credit Illiquid Credit

Project Finance

Private Mezz/ Opportunistic

Ares Capital Corporation - Not for Publication or Distribution 6

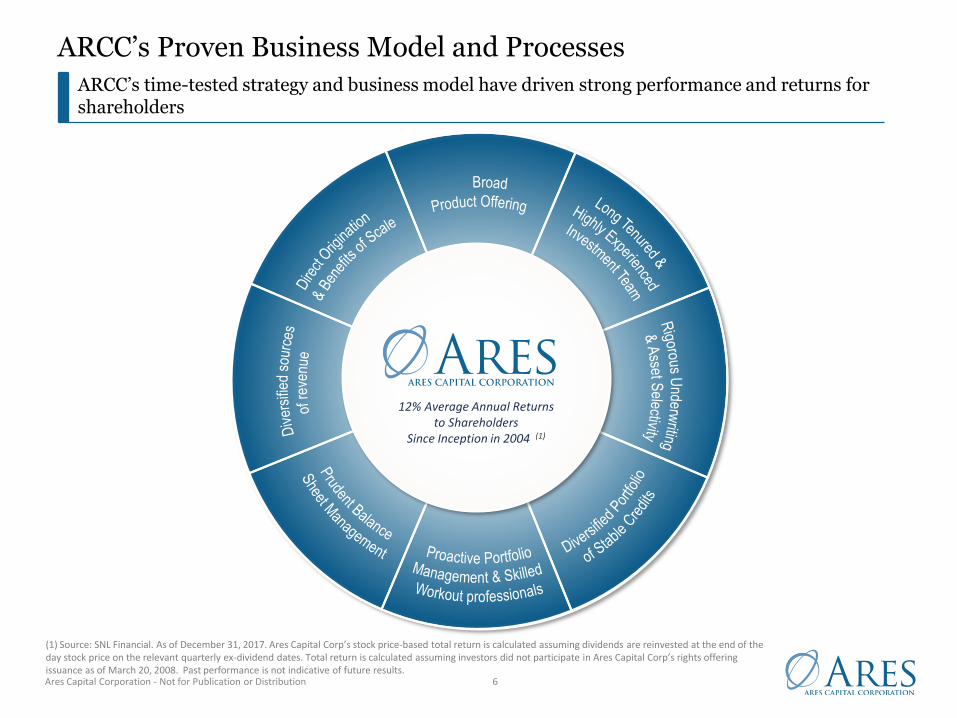

ARCC’s Proven Business Model and Processes

ARCC’s time-tested strategy and business model have driven strong performance and returns for shareholders

(1) Source: SNL Financial. As of December 31, 2017. Ares Capital Corp’s stock price-based total return is calculated assuming dividends are reinvested at the end of the day stock price on the relevant quarterly ex-dividend dates. Total return is calculated assuming investors did not participate in Ares Capital Corp’s rights offering issuance as of March 20, 2008. Past performance is not indicative of future results.

12% Average Annual Returns to Shareholders

Since Inception in 2004 (1)

Ares Capital Corporation - Not for Publication or Distribution 7

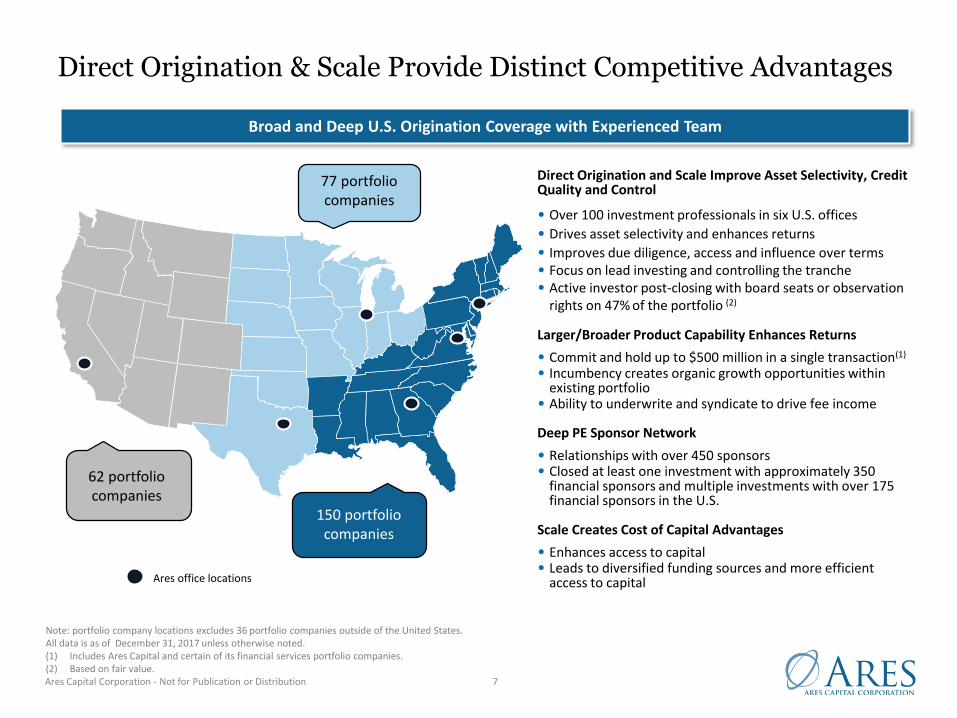

Broad and Deep U.S. Origination Coverage with Experienced Team

Direct Origination & Scale Provide Distinct Competitive Advantages

Direct Origination and Scale Improve Asset Selectivity, Credit Quality and Control

• Over 100 investment professionals in six U.S. offices

• Drives asset selectivity and enhances returns

• Improves due diligence, access and influence over terms• Focus on lead investing and controlling the tranche• Active investor post-closing with board seats or observation

rights on 47% of the portfolio (2)

Larger/Broader Product Capability Enhances Returns

• Commit and hold up to $500 million in a single transaction(1)

• Incumbency creates organic growth opportunities within existing portfolio

• Ability to underwrite and syndicate to drive fee income

Deep PE Sponsor Network

• Relationships with over 450 sponsors• Closed at least one investment with approximately 350

financial sponsors and multiple investments with over 175 financial sponsors in the U.S.

Scale Creates Cost of Capital Advantages

• Enhances access to capital• Leads to diversified funding sources and more efficient

access to capital

Note: portfolio company locations excludes 36 portfolio companies outside of the United States. All data is as of December 31, 2017 unless otherwise noted.(1) Includes Ares Capital and certain of its financial services portfolio companies.(2) Based on fair value.

Ares office locations

77 portfolio companies

150 portfolio companies

62 portfolio companies

Ares Capital Corporation - Not for Publication or Distribution 8

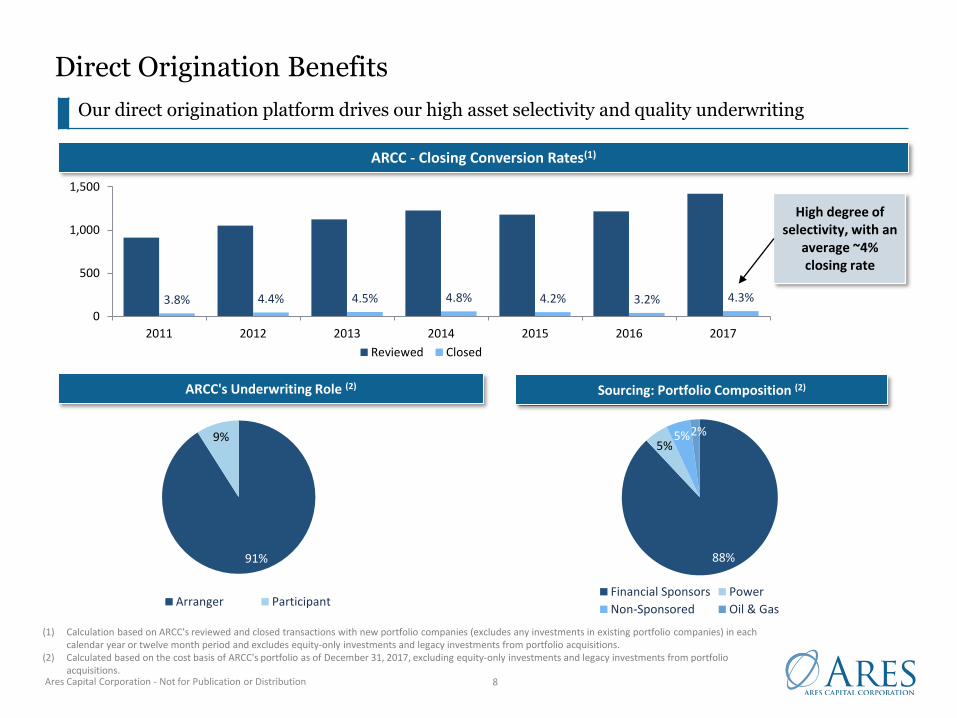

Direct Origination Benefits

Our direct origination platform drives our high asset selectivity and quality underwriting

ARCC - Closing Conversion Rates(1)

High degree of selectivity, with an

average ~4% closing rate

(1) Calculation based on ARCC's reviewed and closed transactions with new portfolio companies (excludes any investments in existing portfolio companies) in each calendar year or twelve month period and excludes equity-only investments and legacy investments from portfolio acquisitions.

(2) Calculated based on the cost basis of ARCC's portfolio as of December 31, 2017, excluding equity-only investments and legacy investments from portfolio acquisitions.

ARCC's Underwriting Role (2) Sourcing: Portfolio Composition (2)

91%

9%

Arranger Participant

3.8% 4.4% 4.5% 4.8% 4.2% 3.2% 4.3%

0

500

1,000

1,500

2011 2012 2013 2014 2015 2016 2017

Reviewed Closed

88%

5%5%2%

Financial Sponsors Power

Non-Sponsored Oil & Gas

Ares Capital Corporation - Not for Publication or Distribution 9

TARGETEDINVESTMENT HOLD SIZES

TRANSACTION TYPES

PRODUCTS

PARTNERS

ARCC Benefits from Broad and Flexible Product Offerings

Corporate:Project Finance:EBITDA Range:

$30 - $250 million$10 - $200 millionGenerally under $100 million

Leveraged BuyoutsAcquisitions

Recapitalizations

RestructuringsGeneral Refinancing

Rescue FinancingGrowth Capital

Power GenerationOil & Gas

RevolversFirst Lien LoansStretch Senior

Unitranche LoansSecond Lien LoansMezzanine Debt

Junior CapitalMinority Equity

Private Equity SponsorsManagement Teams

Intermediaries

Project DevelopersFamily Offices

EntrepreneursOther Lenders

Going to market as a total solution provider to our prospective and existing borrowers allows us to see a broad view of market opportunity

Ares Capital Corporation - Not for Publication or Distribution 10

Long Tenured & Highly Experienced Investment Team

ARCC benefits from a long tenured and highly experienced team with significant expertise in direct lending and extensive middle market knowledge

• ARCC’s investment team has invested over $45 billion across more than 950 transactions since 2004(1)

• 75% of senior investment professionals in our direct lending team have been with Ares for at least 5 years(2)

• The members of the investment committee possess an average of 22 years of investing experience and every member has been with Ares more than 10 years

• ARCC receives referrals from other teams across the Ares Platform

U.S. Direct Lending Investment Committee

PartnersMark

AffolterMichael

AroughetiKipp

deVeerMitch

GoldsteinJim Miller

Kort Schnabel

Dave Schwartz

Michael Smith

Average

Industry Experience

28 Years 25 Years 22 Years 23 Years 18 Years 20 Years 17 Years 22 Years 22 Years

Years with Ares

10 Years 14 Years 14 Years 13 Years 11 Years 16 Years 13 Years 14 Years 13 Years

Direct Lending Commercial Finance

No. Investment Professionals 100+ 50+

No. Senior Investment Professionals (2) 40 13

Average Industry Experience of Sr. Professionals

18 years 20 years

No. of Offices 6 6

As of December 31, 2017.(1) Includes invested capital from inception on October 8, 2014 through December 31, 2017. Excludes syndications within one year of origination, $1.8 billion of investments acquired from Allied Capital on April 1, 2010 and $2.5 billion of investments acquired from American Capital on January 3, 2017.(2) Includes principals, managing directors and partners.

Extensive Direct Lending Team

Ares Capital Corporation - Not for Publication or Distribution 11

44%

32%

4%

8%

1%4%

7%

Portfolio by Asset Class (1)

First Lien Senior Secured Loans Second Lien Senior Secured Loans

Senior Direct Lending Program Senior Subordinated Debt

Collateralized Loan Obligations Preferred Equity

Other Equity and Other

Portfolio Diversification and Industry Selection

Attractively positioned portfolio, diversified by asset class, industry and borrower size

(1) At fair value as of December 31, 2017.(2) Including First Lien Senior Secured Loans, Second Lien Senior Secured Loans and investments in the subordinated certificates of the Senior Direct Lending Program.

Well diversified portfolio –

314 companies

Focus on high free cash flow businesses

Strong investment discipline and focus on downside production

Senior oriented portfolio: 80% senior secured loans(2)

Focus on defensively positioned, attractive

industries

23%

19%

7%6%6%

4%

4%

4%

4%

3%

3%

3%3%

2%2%

7%

Portfolio by Industry (1)

Healthcare-Services Business ServicesConsumer Products Services-OtherManufacturing Financial ServicesFood and Beverage SDLPPower Generation Restaurants and Food ServicesAutomotive Services EducationWholesale Distribution Oil and GasContainers-Packaging Remaining

Ares Capital Corporation - Not for Publication or Distribution 12

Prudent Balance Sheet Management

We manage our balance sheet conservatively, which provides us with flexible, low cost funding and allows us to be opportunistic throughout the cycle

• Target and maintain leverage of 0.65x to 0.75x, well below regulatory requirements(1)

o As of December 31, 2017, our leverage ratio was 0.66x net of available cash

Relatively Low Leverage

As of December 31, 2017, unless otherwise noted.(1) The use of leverage magnifies the potential for gain or loss on the amount invested and may increase the risk of investment.(2) Weighted average maturity of outstanding liabilities of 4.3 years vs. weighted average maturity of investments at fair value of 4.2 years. The weighted average maturity of investments at fair value excludes the investment in the subordinated certificates of the SDLP. The weighted average maturity of investments within the SDLP portfolio was 4.1 years.

• Maintain significant undrawn revolving capacity

• Accessed the debt and equity markets over 30 times since inception

• Significant annual cash flows from portfolio repayments and sales

Strong Liquidity

• We have liability duration that is equal to or longer than our asset duration(2)

• No “mark to market” financing

• Staggered debt maturity ladder

Long Duration and Flexible Funding

• Secured revolvers provided by 27 different banks

• Over 100 investors have invested in ARCC’s convertible and investment grade notes

• Significant permanent equity base of $7.1 billion

Diversity of Funding Sources

• Diversified $11.8 billion portfolio with 314 companies

• Our investments are spread across the country and 25+ industriesDiversified Portfolio

Ares Capital Corporation - Not for Publication or Distribution

Financial and Portfolio Performance

Ares Capital Corporation - Not for Publication or Distribution 14

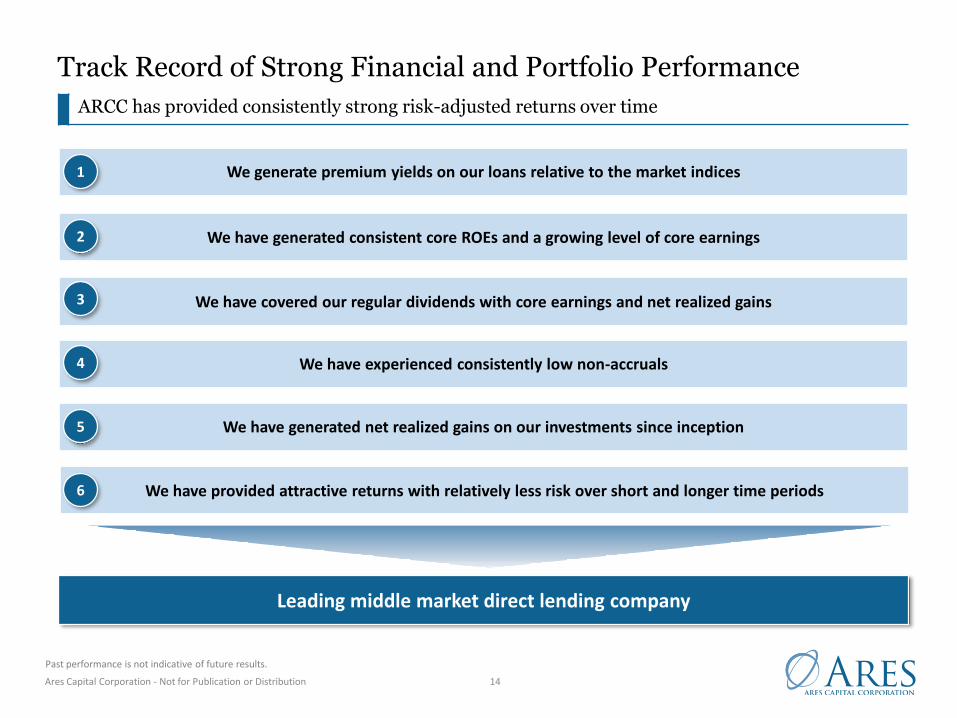

Track Record of Strong Financial and Portfolio Performance

ARCC has provided consistently strong risk-adjusted returns over time

We generate premium yields on our loans relative to the market indices

We have generated consistent core ROEs and a growing level of core earnings

We have covered our regular dividends with core earnings and net realized gains

We have experienced consistently low non-accruals

Leading middle market direct lending company

We have generated net realized gains on our investments since inception

Past performance is not indicative of future results.

We have provided attractive returns with relatively less risk over short and longer time periods

1

2

3

4

5

6

Ares Capital Corporation - Not for Publication or Distribution 15

Sustained Market Premium for ARCC Yields with Lower Losses

ARCC’s portfolio has historically generated premium performance to middle market and syndicated bank loans and high yield bonds

Premium yields... ...with lower loss rates

ARCC’s Portfolio Yield vs. Leveraged Loans & High Yield Bonds

5%

7%

9%

11%

2013 2014 2015 2016 2017

ARCC Yield on Debt and Income Producing Securities (1) S&P LSTA Leveraged Loan Yields (2)

S&P LSTA Middle Market Leveraged Loan Yields (3) ICE BofAML US HY Master II (4)

Note: Past performance is not indicative of future results. Refer to Endnotes on slides 42 - 45 for additional important information.

Non-Accrual Rate/

Default Rate

Average ARCC Non-Accrual Rate

at Amortized Cost (5)2.8%

High Yield Bond Default Rate (6) 5.1%

Average Annual

Gain/(Loss) Rate

ARCC (7) 1.1%

High Yield Bonds (8) (2.7)%

Yield

12/31/17

ARCC

Premium

ARCC Yield on Debt and Income Producing

Securities (1)9.8%

ICE BofAML U.S. High Yield Master II 6.2% 3.6%

S&P LSTA Leveraged Loan Yields 5.2% 4.6%

S&P LSTA Middle Market Leveraged Loan

Yields7.3% 2.5%

3-month LIBOR 1.7% 8.1%

Premium to Middle Market Leveraged Loans

1

Ares Capital Corporation - Not for Publication or Distribution 16

Long standing track record of stable core ROE ranging from ~9% to ~12% annually over the past 10 years

Growing level of core earnings since inception generated from diverse revenue sources and prudent liability management

Consistent Core Return on Equity (2) Compelling Core Earnings (1)

0%

2%

4%

6%

8%

10%

12%

14%

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Q1

-17

Q2

-17

Q3

-17

Q4

-17

Core Earnings ROE 10 Yr US T-Note

0

100

200

300

400

500

600

700

Co

re E

arn

ings

($

M)

Core Earnings

Note: Past performance is not indicative of future results. Refer to Endnotes on slides 42 - 45 for additional important information.

Annualized

2

ARCC has generated a compelling and growing level of core earnings(1) and stable core ROE(2)

Compelling Core Earnings and Return on Equity

Ares Capital Corporation - Not for Publication or Distribution 17

Dividend and Core Earnings Plus Net Realized Gains Track Record

ARCC has generated cumulative core earnings and net realized gains in excess of our dividends paid since our IPO

Note: As of December 31, 2017. There can be no assurance that dividends will continue to be paid at historic levels or at all. Past performance is not indicative of future results. Refer to Endnotes on slides 42 - 45 for additional important information.

We’ve out-earned our dividend with cumulative core earnings plus net realized gains

Cumulative Core Earnings Plus Net Realized Gains vs. Cumulative Dividends (1)

$226 $360 $447

$726

$1,136

$1,552

$2,074

$2,635

$3,244

$3,855

$4,472

$192 $301

$490 $720

$997

$1,355

$1,766

$2,231

$2,718

$3,195

$3,837

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

$ M

illio

ns

Cumulative Core Earnings Plus Net Realized Gains Cumulative Dividends Paid

3

Ares Capital Corporation - Not for Publication or Distribution 18

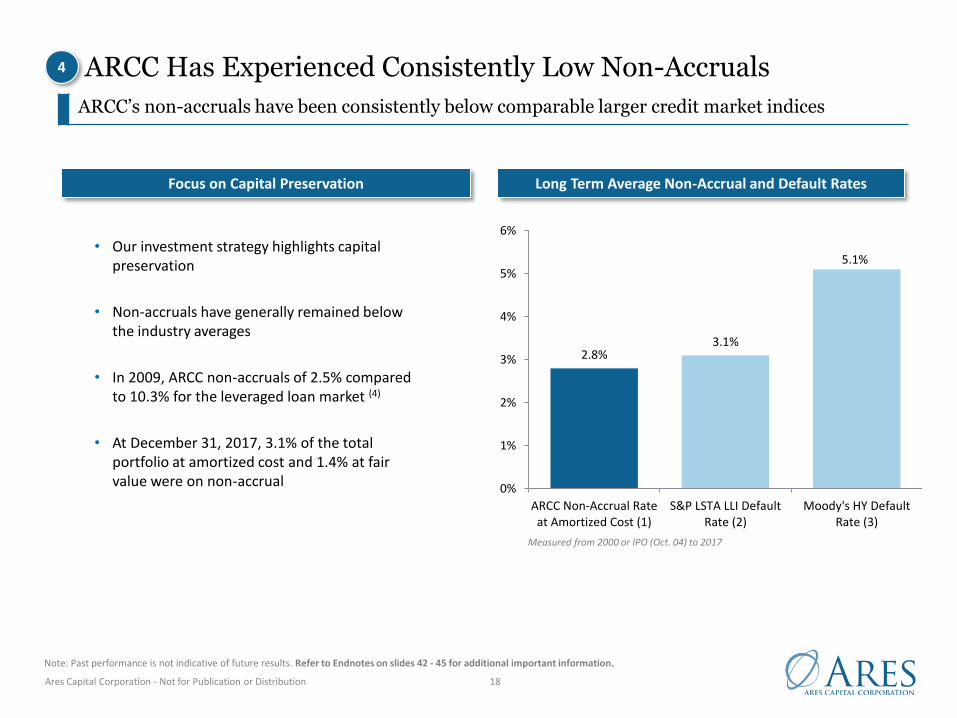

ARCC Has Experienced Consistently Low Non-Accruals

ARCC’s non-accruals have been consistently below comparable larger credit market indices

Long Term Average Non-Accrual and Default Rates

• Our investment strategy highlights capital preservation

• Non-accruals have generally remained below the industry averages

• In 2009, ARCC non-accruals of 2.5% compared to 10.3% for the leveraged loan market (4)

• At December 31, 2017, 3.1% of the total portfolio at amortized cost and 1.4% at fair value were on non-accrual

Note: Past performance is not indicative of future results. Refer to Endnotes on slides 42 - 45 for additional important information.

2.8%3.1%

5.1%

0%

1%

2%

3%

4%

5%

6%

ARCC Non-Accrual Rateat Amortized Cost (1)

S&P LSTA LLI DefaultRate (2)

Moody's HY DefaultRate (3)

4

Focus on Capital Preservation

Measured from 2000 or IPO (Oct. 04) to 2017

Ares Capital Corporation - Not for Publication or Distribution 19

ARCC Has Generated Net Realized Gains to Offset Losses

Active portfolio management and internal resources seek to protect downside and have generated net returns on the principal amount of investments across a variety of methods

Our ability to successfully invest equity, acquire companies, structure loans and work out troubled investments has created ~$610 mm of net realized gains since our inception (1)

Note: Past performance is not indicative of future results. (1) From inception on October 8, 2004 through December 31, 2017, excludes $196 million one‐time gain on the acquisition of Allied Capital Corporation in Q2‐10 and gains/losses from extinguishment of debt and sale of other assets.

Sources of Cumulative Net Realized Gains Since Inception(1)

Source Nature of Gains / Losses $ in mm Annual Rate %

ARCC Restructuring Gains Primarily equity received in workouts ~$255 +0.4%

Acquired Portfolio Net Gains Effective monetization of controlled buyouts, CLOs and other investments ~$210 +0.4%

ARCC Equity Net Gains Primarily equity tags and minority equity investments ~$220 +0.4%

ARCC Other Debt Gains Primarily call protection and discount accretion ~$190 +0.3%

ARCC Debt Losses Relatively minimal losses through credit selection & loss avoidance once in deals ~($265) (0.5%)

Total Net Realized Gains ~$610 +1.1%

~$255

~$210

~$220

~$190

~$265

~$610

$0

$200

$400

$600

$800

$1,000

ARCC RestructuringGains

Allied/ACAS Net Gains ARCC Equity Net Gains ARCC Other Debt Gains ARCC Debt Losses Cumulative NetRealized Gains

$ M

illio

ns

5

Ares Capital Corporation - Not for Publication or Distribution 20

Strong Investment Performance

ARCC’s net realized gain and loss rates have consistently outperformed the BDC peer group

Note: Past performance is not indicative of future results. Refer to Endnotes on slides 42 - 45 for additional important information.* As of 12/31/17 for ARCC. As of 9/30/17 for BDC Peer Group since not all peers have reported as of 2/26/18.

ARCC and BDC Peers Net Realized Gain (Loss) Rate

CY2007 CY2008 CY2009 CY2010 CY2011 CY2012 CY2013 CY2014 CY2015 CY2016 LTM * Avg(6)

ARCC(3) 0.4% 0.3% (2.0)% 1.3% 2.1% 0.9% 1.0% 1.2% 1.5% 1.2% 0.2% 1.1%

BDC Peer Group Average(5) 0.3% 0.3% (7.6)% (4.3)% (1.4)% (0.5)% (0.9)% 0.7% (0.1)% (1.4)% (2.5)% (1.2)%

Outperformance (%) 0.1% —% 5.6% 5.6% 3.5% 1.4% 1.9% 0.5% 1.6% 2.6% 2.7% 2.3%

ARCC

BDC Peers

-1.20%

-0.80%

-0.40%

0.00%

0.40%

0.80%

1.20%

ARCC BDC Peers

Net

rea

lized

gai

n/(

loss

) ra

te (

5)

ARCC generated 230 bps of average annual incremental gain differential

vs. peers since 200414% IRR (1)(2) Cumulative internal rate of return on ~$21

billion of exited investments

~$610 million Net Realized

Gains(3)(4)

Cumulative net realized gains generated

1.1% Net Realized Gain Rate%(3)

Average annualized net realized gain rate on the principal amount of its investments. ARCC had a net realized loss in only one fiscal year since inception(3)

Since IPO in October 2004 through December 31, 2017:

5

Ares Capital Corporation - Not for Publication or Distribution 21

ARCC’s Portfolio Has Generated Higher Returns with Less Risk

Our investment strategy and competitive advantages have led to attractive returns with lower volatility

Annual Returns (Dividends & Change in NAV)(1)

3 Years (2)(3) 5 Years (2)(3) 10 Years(2)(3)

Volatility of Annual Returns (Standard Deviation of Dividends & Change in NAV)(1)

5 Years (2)(3) 10 Years (2)(3)3 Years(2)(3)

Note: Past performance is not indicative of future results. Refer to Endnotes on slides 42 - 45 for additional important information.

6

9.1%

6.3% 5.9%

3.9%

0%

5%

10%

15%

ARCC BDCComparable

Universe

High YieldIndex

Loan Index

10.9%

8.8%

6.4%

4.1%

ARCC BDCComparable

Universe

High YieldIndex

Loan Index

11.2%

6.9%7.7%

4.7%

ARCC BDCComparable

Universe

High YieldIndex

Loan Index

1.5%

4.4%5.9%

3.1%

0%

5%

10%

15%

ARCC BDCComparable

Universe

High YieldIndex

Loan Index

1.8%

4.4%5.2%

2.6%

ARCC BDCComparable

Universe

High YieldIndex

Loan Index

8.9%9.7%

12.2% 11.6%

ARCC BDCComparable

Universe

High YieldIndex

Loan Index

Ares Capital Corporation - Not for Publication or Distribution 22

ARCC (2)

S&P 500 Index

ML HY Master II index

SNL U.S. RICs

CSLLISP LSTA LLI

BKX TR Index

-100%

-50%

0%

50%

100%

150%

200%

250%

300%

350%

400%

Dec-04 Dec-05 Dec-06 Dec-07 Dec-08 Dec-09 Dec-10 Dec-11 Dec-12 Dec-13 Dec-14 Dec-15 Dec-16 Dec-17

ARCC’s Stock Has Generated Strong Returns to Investors

ARCC has outperformed major indices through a variety of market environments since IPO in 2004

Cumulative Total Return since Inception 10/7/04 - 12/31/17 (1)

Note: Past performance not indicative of future results.(1) Time period selected to include Ares Capital IPO in October 2004. The benchmarks included represent investments in either the U.S. non-investment grade credit or equity market. The ICE BofAML US HY Master II is a broad index tracking high-yield corporate bonds, the S&P 500 Index is a broad index tracking the U.S. equity markets, the S&P LSTA LLI is a broad index tracking the U.S. loan market and the Credit Suisse Leveraged Loan Index is a broad index tracking the non-investment grade bank loans.(2) Ares Capital's stock price-based total return is calculated assuming dividends are reinvested at the end of day stock price on the relevant quarterly ex-dividend dates, and assuming investors did not participate in Ares Capital's rights offering issuance as of March 20, 2008.

Allied Capital Acquisition provided scaleApril 1, 2010

American Capital Acquisition provided additional scale

January 3, 2017

6

Ares Capital Corporation - Not for Publication or Distribution

Current Market Opportunities& Strategic Initiatives

Ares Capital Corporation - Not for Publication or Distribution 24

Long Term Structural Positives

Ares Capital’s Approach

Seek to invest in leading, non-cyclical businesses with attractive growth prospects and high free cash flows

Use direct origination and scale to provide greater influence on loan structures to maintain high selectivity

Seek to be the lead lender with voting control to have the ability to impact outcomes

Use incumbent positions to support growth of leading portfolio companies and enhance credit quality

Be proactive managing investments and use our robust process to preserve capital and create value

• Healthy demand trends from vibrant middle market companies

• Continued bank retrenchment

• Substantial private equity dry powder(~8x direct lending dry powder)

• Significant level of equity contributions in structures

Near Term Challenges in Current Environment

• Spreads have compressed

• Debt to EBITDA multiples are elevated

• Covenants and documentation are weaker

• Significant new capital has formed, including new entrants with need to deploy capital in a limited timeframe

ARCC’s Approach to Managing Current Market Conditions

Ares Capital Corporation - Not for Publication or Distribution 25

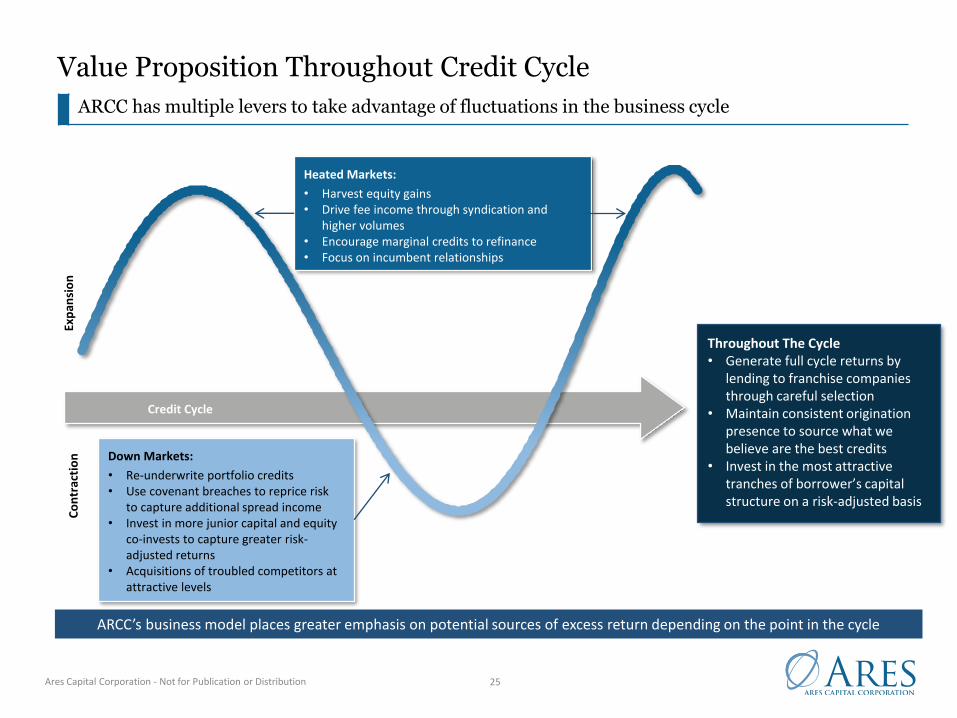

Value Proposition Throughout Credit Cycle

ARCC has multiple levers to take advantage of fluctuations in the business cycle

Heated Markets:

• Harvest equity gains• Drive fee income through syndication and

higher volumes• Encourage marginal credits to refinance• Focus on incumbent relationships

Down Markets:

• Re-underwrite portfolio credits• Use covenant breaches to reprice risk

to capture additional spread income • Invest in more junior capital and equity

co-invests to capture greater risk-adjusted returns

• Acquisitions of troubled competitors at attractive levels

Credit Cycle

Exp

ansi

on

Co

ntr

acti

on

Throughout The Cycle• Generate full cycle returns by

lending to franchise companies through careful selection

• Maintain consistent origination presence to source what we believe are the best credits

• Invest in the most attractive tranches of borrower’s capital structure on a risk-adjusted basis

ARCC’s business model places greater emphasis on potential sources of excess return depending on the point in the cycle

Ares Capital Corporation - Not for Publication or Distribution 26

ARCC’s Earnings Will Likely Benefit from Higher LIBOR Rates

ARCC has an asset sensitive balance sheet that we believe will benefit from an expected rise in base interest rates

3 Month LIBOR Forward Rates (1) Enhanced Ability to Benefit from Rising Rates (2)

(1) Source: Chatham Financial. Reflects the current and forward 3 month LIBOR rates for February 26, 2018 through 2022, all as of February 26, 2018.(2) As of December 31, 2017.(3) Remaining 2% consists of non-accruals and non-coupon bearing loans.(4) In January 2018, Ares Capital issued $600 million aggregate principal amount of unsecured notes that mature on March 1, 2025 (the “2025 Notes”). The 2025 Notes bear interest at a rate of 4.25%

per year, payable semi-annually on March 1 and September 1 of each year, commencing on September 1, 2018. The 2025 Notes may be redeemed in whole or in part at the Company’s option at any time at the redemption prices as determined pursuant to the indenture governing the 2025 Notes.

(5) Includes the $395 million term loan tranche of Ares Capital's Revolving Credit Facility which Ares Capital effectively fixed the interest rate at 3.8% through an interest rate swap agreement. (6) Marginal EPS contributions include the impact of income-based fees.

• Heavily weighted to floating-rate loans (3)

o 90% floating rate loan portfolio

o 8% fixed rate loan portfolio

• Heavily weighted to fixed-rate borrowings (4)

o 87% fixed rate (5)

o 13% floating rate

• Conservative Leverage

o 0.66x net debt to equity

Increase in LIBOR Annual Per Share Impact (2)(6)

100 bps $0.17 per share

200 bps $0.34 per share

300 bps $0.51 per share

1.80%

2.00%

2.20%

2.40%

2.60%

2.80%

3.00%

3.20%

Feb. 2018 Feb. 2019 Feb. 2020 Feb. 2021 Feb. 2022

Ares Capital Corporation - Not for Publication or Distribution 27

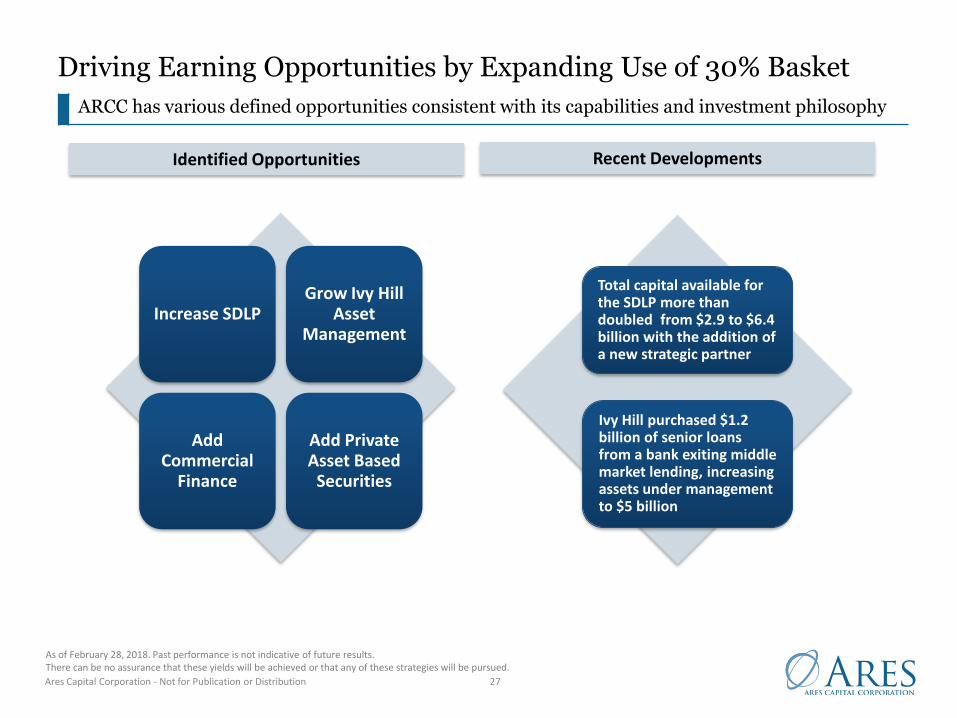

Driving Earning Opportunities by Expanding Use of 30% Basket

As of February 28, 2018. Past performance is not indicative of future results. There can be no assurance that these yields will be achieved or that any of these strategies will be pursued.

ARCC has various defined opportunities consistent with its capabilities and investment philosophy

Total capital available for the SDLP more than doubled from $2.9 to $6.4 billion with the addition of a new strategic partner

Identified Opportunities

Increase SDLPGrow Ivy Hill

Asset Management

Add Commercial

Finance

Add Private Asset Based

Securities

Ivy Hill purchased $1.2 billion of senior loans from a bank exiting middle market lending, increasing assets under management to $5 billion

Recent Developments

Ares Capital Corporation - Not for Publication or Distribution 28

Rotation of American Capital Portfolio Should Help Provide Incremental Returns

We have ~$900 million of remaining non-core investments acquired in the American Capital Acquisition, with a blended yield of 6.7%, which are targeted for reinvestment into higher yields

As of December 31, 2017, unless otherwise noted. There is no guarantee that performance objectives will be achieved.

47%

24%

44%

32%

32%

32%

5%4%

7%

15%

8%

7%

1%3%

13%

4%6% 9% 7%

$10.1 billion $1.7 billion $11.8 billion

0%

20%

40%

60%

80%

100%

Ares Capital ExcludingInvestments Acquired

in the AmericanCapital Acquisition

RemainingInvestments Acquired

in the AmericanCapital Acquisition

Total Ares Capital

Other Equity and Other

Preferred Equity

Collateralized Loan Obligations

Senior Subordinated Loans

Senior Direct Lending Program

Second Lien Senior Secured Loans

First Lien Senior Secured Loans

Progress on ACAS Portfolio

$85 million in net realized gains

$184 million in net unrealized appreciation

Exited over $1.0 billion of lower yielding

investments

Acquired Portfolio Rotation 1/3/17 to 12/31/17

Yield at fair value on remaining investments

acquired increased from 7.4% to 7.8%

Ares Capital Corporation - Not for Publication or Distribution 29

Conclusion

Distinct Competitive Advantages

• Market leading company with long tenured management team

• Benefits from Ares Platform

• Competitive advantages of scale

• Portfolio of larger companies in defensive industries

• Conservatively funded balance sheet with efficient capital

Note: As of December 31, 2017. Past performance is not indicative of future results.1. Source: SNL Financial. As of December 31, 2017. Ares Capital Corp's stock price-based total return is calculated assuming dividends are reinvested at the end of

the day stock price on the relevant quarterly ex-dividend dates. Total return is calculated assuming investors did not participate in Ares Capital Corp's rights offering issuance as of March 20, 2008. Past performance is not indicative of future results.

2. Refer to slide 21 for further details.

We believe these factors lead to a company well positioned to continue to generate attractive future financial performance and benefit from rising LIBOR

Track Record of Outperformance

• Compelling performance

• Generated 12% average annual shareholder return since IPO (1)

• Long term track of strong and stable core ROEs

• Strong coverage of dividends from earnings sources

• Higher risk adjusted returns vs. the BDC comparable universe, leveraged loans and high yield bonds over 3, 5, and 10 year periods (2)

Ares Capital Corporation - Not for Publication or Distribution

Appendix A: Market and Other Investment Considerations

Ares Capital Corporation - Not for Publication or Distribution 31

Drivers of Market Demand

Dry powder statistics suggest plenty of additional capacity for direct lending strategy

Source: Preqin. As of January 2018.

• Direct lending dry powder in North America is currently $52 billion, which represents 14% of buyout dry powder

• We believe scaled providers will benefit from the available capacity

North America Dry Powder – Direct Lending and Buyout

Direct Lending Dry Powder as a % of Buyout Dry Powder

0

50

100

150

200

250

300

350

400

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 Feb-18

Dry

Po

wd

er

($B

)

Direct Lending Dry Powder Buyout Dry Powder

2% 4% 7% 5% 7% 9% 11% 20% 15% 13% 13% 13%2%2% 14%

Ares Capital Corporation - Not for Publication or Distribution 32

Supply Constraints Create an Attractive Market Opportunity

We believe supply constraints in the middle market have resulted in attractive risk adjusted returns for direct lenders

Total Number of U.S. Banks Continues to Decline (1)

(1) Source: Federal Deposit Insurance Corp Quarterly Banking Profile Q4-17.(2) Source: S&P LCD Leveraged Lending Review Q4-17. Amounts are based on administrative, syndication and documentation agent as well as arranger roles.

Banks' Share of the U.S. Leveraged Loan Market Continues to Shrink (2)

5,000

6,000

7,000

8,000

9,000

10,000

11,000

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

71%

45%

18%12% 9%

29%

55%

82%88% 91%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1994 2000 2006 2012 2017

Foreign/Domestic Banks Non-Bank Companies/Funds

Ares Capital Corporation - Not for Publication or Distribution 33

Rigorous Underwriting and Credit Management

Our in-depth process often spans several months, allowing for thoughtful decision making

Key Attributes of ARCC Borrowers (1)

Franchise businesses

High free cash flow

Above market growth prospects

Premier financial sponsors with meaningful “skin in the game”

Leading management teams

ARCC has lead role

Appropriate capital structure

Diverse sources of profitability

Ares’ Approach:

• Seek to invest in leading, non-cyclical businesses with attractive growth prospects and high free cash flows

• Use direct origination and scale to provide greater influence on loan structures to maintain high selectivity

• Seek to be the lead lender with voting control to have the ability to impact outcomes

• Use incumbent positions to support growth of leading portfolio companies and to help enhance credit quality

• Be proactive managing investments and use our robust process to preserve capital and create value

(1) Not every investment meets each of the criteria.

Ares Capital Corporation - Not for Publication or Distribution 34

-6%

-5%

-4%

-3%

-2%

-1%

0%

1%

2%

ARCC BDC 1 BDC 2 BDC 3 BDC 4 BDC 5 BDC 6 BDC 7 BDC 8 BDC 9 BDC 10 BDC 11 BDC 12 BDC 13 BDC 14 BDC 15 BDC 16

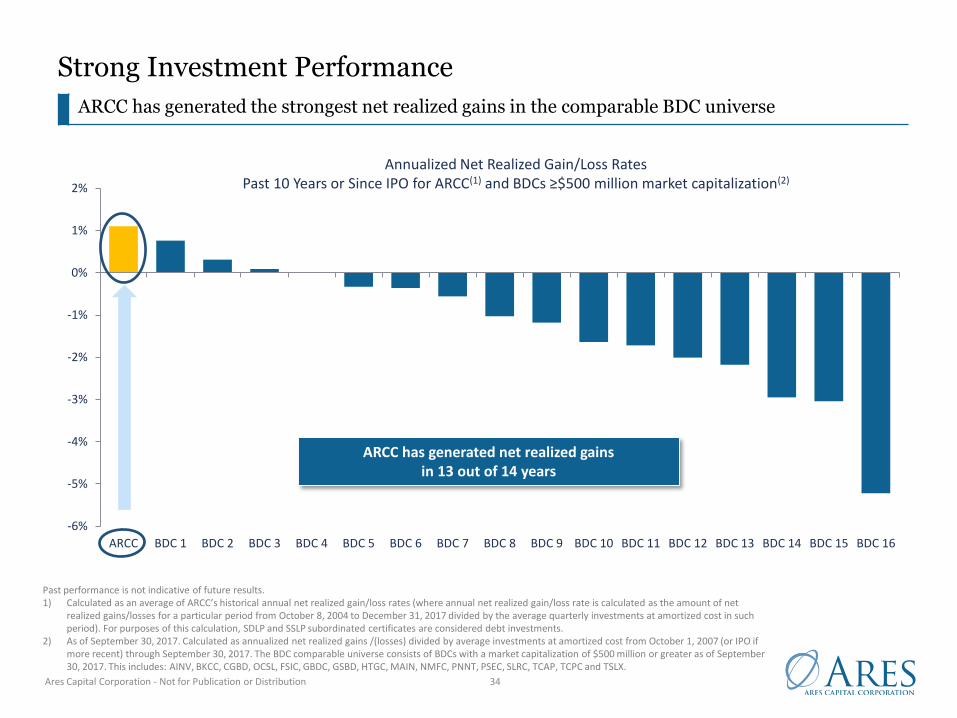

Strong Investment Performance

ARCC has generated the strongest net realized gains in the comparable BDC universe

Past performance is not indicative of future results. 1) Calculated as an average of ARCC’s historical annual net realized gain/loss rates (where annual net realized gain/loss rate is calculated as the amount of net

realized gains/losses for a particular period from October 8, 2004 to December 31, 2017 divided by the average quarterly investments at amortized cost in such period). For purposes of this calculation, SDLP and SSLP subordinated certificates are considered debt investments.

2) As of September 30, 2017. Calculated as annualized net realized gains /(losses) divided by average investments at amortized cost from October 1, 2007 (or IPO if more recent) through September 30, 2017. The BDC comparable universe consists of BDCs with a market capitalization of $500 million or greater as of September 30, 2017. This includes: AINV, BKCC, CGBD, OCSL, FSIC, GBDC, GSBD, HTGC, MAIN, NMFC, PNNT, PSEC, SLRC, TCAP, TCPC and TSLX.

Annualized Net Realized Gain/Loss RatesPast 10 Years or Since IPO for ARCC(1) and BDCs ≥$500 million market capitalization(2)

ARCC has generated net realized gains in 13 out of 14 years

Ares Capital Corporation - Not for Publication or Distribution 35

Deep and Diverse Access to Low Cost Debt Financing

We believe that ARCC is one of the most efficient issuers of liabilities amongst BDCs

• Significant access to long-dated, lower cost revolving debt facilities

• No “mark to market” financing• Reduced pricing over time and continue to periodically

extend maturities (5-7 year terms)

• Seasoned issuer in the institutional unsecured debt market

• More than 100 investors have invested in ARCC’s Convertible and Investment Grade Notes

• Raised over $5.7 billion in unsecured notes since 2011 (5)

(including January 2018 issuance)

($ in millions)

Total Aggregate Principal Amount of

Commitments Outstanding (1)

Principal Amount Outstanding (2)

Weighted Average Stated Interest Rate (3)

Secured Revolving Facilities (4)

Revolving Credit Facility $2,108 $395 3.814%

Revolving Funding Facility 1,000 600 3.714%

SMBC Funding Facility 400 60 3.569%

Subtotal $3,508 $1,055 3.743%

SBA Debentures $50 $— —%

Unsecured Notes Payable (5)

2018 Convertible Notes $270 $270 4.750%

2018 Notes 750 750 4.875%

2019 Convertible Notes 300 300 4.375%

2020 Notes 600 600 3.875%

January 2022 Notes 600 600 3.625%

2022 Convertible Notes 388 388 3.750%

2023 Notes 750 750 3.500%

2047 Notes 230 230 6.875%

Subtotal $3,888 $3,888 4.221%

Total $7,446 $4,943 4.119%

Weighted Average Stated Interest Rate

3.87%(6) 4.12%

All data as of December 31, 2017, unless otherwise noted. Refer to Endnotes on slides 42 - 45 for additional important information.

Ares Capital Corporation - Not for Publication or Distribution 36

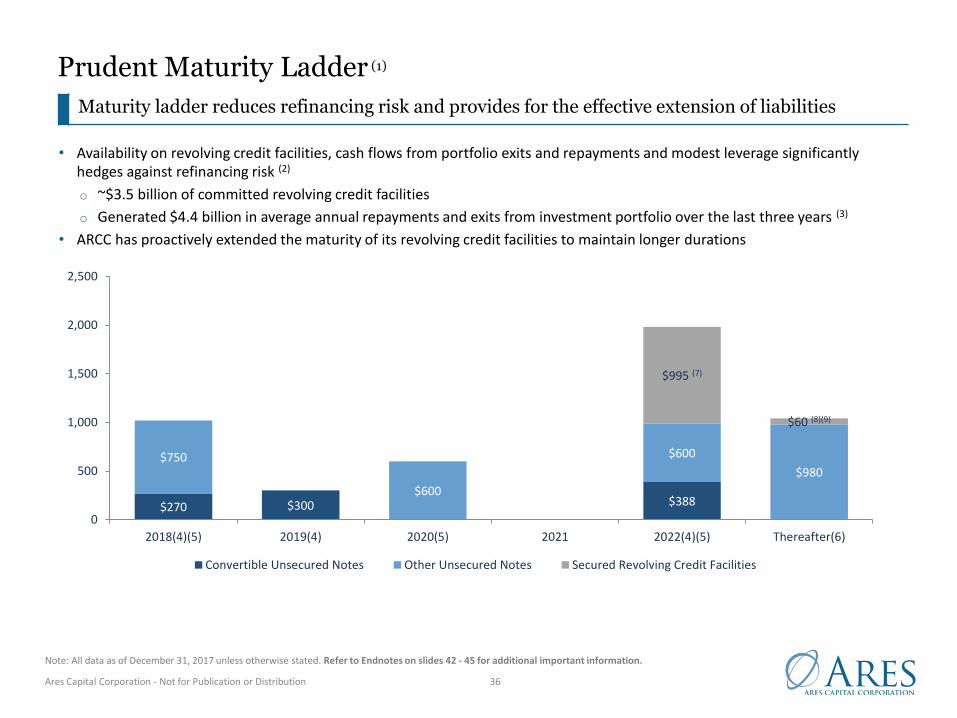

Prudent Maturity Ladder (1)

Maturity ladder reduces refinancing risk and provides for the effective extension of liabilities

• Availability on revolving credit facilities, cash flows from portfolio exits and repayments and modest leverage significantly hedges against refinancing risk (2)

o ~$3.5 billion of committed revolving credit facilities

o Generated $4.4 billion in average annual repayments and exits from investment portfolio over the last three years (3)

• ARCC has proactively extended the maturity of its revolving credit facilities to maintain longer durations

Note: All data as of December 31, 2017 unless otherwise stated. Refer to Endnotes on slides 42 - 45 for additional important information.

$270 $300 $388

$750

$600

$600

$980

$995 (7)

$60 (8)(9)

0

500

1,000

1,500

2,000

2,500

2018(4)(5) 2019(4) 2020(5) 2021 2022(4)(5) Thereafter(6)

Convertible Unsecured Notes Other Unsecured Notes Secured Revolving Credit Facilities

Ares Capital Corporation - Not for Publication or Distribution

Appendix B: Management and Core Earnings Reconciliation

Ares Capital Corporation - Not for Publication or Distribution 38

Members of Investment CommitteeYears of Relevant

Experience

Years atAres

Background

Michael AroughetiAres Capital Corporation – Co-Chairman of the Board of Directors and Executive Vice PresidentAres – Co-Founder, Chief Executive Officer, President and Partner

25 14 RBC Capital Partners – Managing PartnerIndosuez Capital – Principal

Kipp deVeerAres Capital Corporation – Director and Chief Executive OfficerAres – Partner and Head of Credit Group

22 14 RBC Capital Partners – PartnerIndosuez Capital – Vice President

Mitch GoldsteinAres Capital Corporation – Co-PresidentAres – Partner and Co-Head of Credit Group

23 13 Credit Suisse First Boston – Managing DirectorIndosuez Capital – PrincipalBankers Trust – Vice President

Michael SmithAres Capital Corporation – Co-PresidentAres – Partner and Co-Head of Credit Group

22 14 RBC Capital Partners – PartnerIndosuez Capital – Vice President

Mark AffolterAres – Partner of Credit Group

28 10 CIT – Managing DirectorGE Capital – Senior Managing DirectorHeller Financial – Senior Vice President

Jim MillerAres – Partner of Credit Group

18 11 Silver Point Capital – Vice PresidentGE Commercial Finance – Vice President

Kort SchnabelAres – Partner of Credit Group

20 16 Walker Digital Corporation – Corporate Development GroupMorgan Stanley Dean Witter – Corporate Finance Group

Dave SchwartzAres – Partner of Credit Group

17 13 RBC Capital Partners – AssociateIndosuez Capital – Analyst

Other Senior ProfessionalsScott Lem – Chief Accounting Officer, Vice President and TreasurerJana Markowicz – Partner / Head of Product Management, U.S. Direct LendingPenni Roll – Chief Financial OfficerJohn Stilmar – Principal, Public IRMichael Weiner – Vice PresidentRaymond L. Wright – Managing Director and Chief Administrative Officer

Joshua M. Bloomstein – Partner, General Counsel and SecretaryMichael Dieber – Partner / Co-Head of Portfolio ManagementCarl Drake – Partner / Head of Public IR, Ares ManagementIan Fitzgerald – Managing Director/Associate General CounselDaniel Katz – Partner / Co-Head of Portfolio ManagementMiriam Krieger – Chief Compliance Officer

Note: As of December 31, 2017.

Members of Investment Committee & Other Senior Professionals

Ares Capital Corporation - Not for Publication or Distribution 39

As of December 31, 2017.* Represents positions held previously.

Director Title Experience

Michael J Arougheti Co-Chairman/Director

Ares Capital Corporation – Co-Chairman and Executive Vice PresidentAres – Co-Founder, Chief Executive Officer, President and Partner Ares Management Limited - Management Committee Member

Ares Credit Group - Partner and Member of U.S. and European Direct Lending Investment CommitteesAres Commercial Real Estate Corporation – DirectorRBC Capital Partners – Managing Partner*Indosuez Capital – Principal*

Ann Torre Bates Director Chairperson –Audit Committee

Allied Capital Corporation – Director*Franklin Mutual Series and Recovery Funds – DirectorSLM Corporation – Director*

NHP, Inc. – Executive Vice President, CFO, Treasurer*U.S. Airways – Vice President, Treasurer*

Steven B. Bartlett Director BIPAC – Director*Financial Services Roundtable – President and CEO*Dallas, Texas – Mayor*

U.S. Congress – Member*Meridian Products – Founder*

Kipp deVeer Director Ares Capital Corporation – Chief Executive OfficerAres – Partner and Head of Credit Group

RBC Capital Partners – Partner*Indosuez Capital – Vice President*

Daniel G. Kelly, Jr. Director Davis Polk & Wardell LLP – Partner*

Steven B. McKeever Director Hidden Beach Recordings – Founder, CEOMotown Records – Executive Vice President*Irell & Manella LLP – Associate*

College Bound, African-Ancestry.com – DirectorThe Pacific Institute Spirit Board – Director

Robert L. Rosen Director Ares – Strategic Adviser to Private Equity GroupRLR Capital Partners, RLR Focus Fund – Managing Partner*RLR Partners LLC – CEO*

National Financial Partners – Founder, Chairman and CEO*Dolphin Domestic Fund II – Co-Managing Partner*Damon Corporation – Chairman and CEO*Maxxam Group – Vice Chairman*

Bennett Rosenthal Co-Chairman/Director

Ares – Co-Founder and Partner; Co-Head and Partner of Private Equity Group

National Bedding Company LLC – Co-Chairman/DirectorMerrill Lynch – Managing Director, Global Leveraged Finance*

Eric B. Siegel Director/Lead Independent Director

El Paso Electric Company – Director and Chairman of the Nominating and Governance CommitteeKerzner International – Director*

Apollo Advisors L.P. and Lion Advisors L.P. – Retired Limited Partner*

Board of Directors

Ares Capital Corporation - Not for Publication or Distribution 40

For the years ended

(in millions) 2012 2013 2014 2015 2016 2017

Core Earnings (1) $ 381 $ 442 $ 473 $ 486 $ 504 $ 592

Professional fees and other costs related to the American Capital Acquisition (2) — — — — (12) (40)

Net realized and unrealized gains (losses) 159 58 153 (129) (20) 156

Incentive fees attributable to net realized and unrealized gains and losses

(32) (11) (29) 27 5 (41)

Income tax and other expenses related to net realized and unrealized gains and losses

— — (6) (5) (3) —

GAAP Earnings $ 508 $ 489 $ 591 $ 379 $ 474 $ 667

(1) Core Earnings is a non-GAAP financial measure. Core Earnings is the net increase (decrease) in stockholders’ equity resulting from operations less professional fees and other costs related to the acquisition of American Capital, Ltd. (the "American Capital Acquisition"), net realized and unrealized gains and losses, any capital gains incentive fees attributable to such net realized and unrealized gains and losses and any income taxes related to such net realized gains and losses. Net increase (decrease) in stockholders’ equity is the most directly comparable GAAP financial measure. Ares Capital believes that Core Earnings provides useful information to investors regarding financial performance because it is one method Ares Capital uses to measure its financial condition and results of operations. The presentation of this additional information is not meant to be considered in isolation or as a substitute for financial results prepared in accordance with GAAP. (2) See Note 14 to Ares Capital's consolidated financial statements included in the annual report on Form 10-K for the year ended December 31, 2017 for information regarding the American Capital Acquisition.

Reconciliations of Core Earnings to GAAP Earnings

Reconciliation of Core Earnings

Ares Capital Corporation - Not for Publication or Distribution

Endnotes

Ares Capital Corporation - Not for Publication or Distribution 42

EndnotesSlide 3: Market Leading Company in Direct Lending1. Based on market prices as of February 28, 2018.

2. As of December 31, 2017.

3. Includes invested capital from inception on October 8, 2004 through December 31, 2017. Excludes syndications within one year of origination, $1.8 billion of investments acquired from Allied Capital on April 1, 2010 and $2.5 billion of investments acquired from American Capital on January 3, 2017.

4. Source: SNL Financial. As of December 31, 2017. Ares Capital Corp’s stock price-based total return is calculated assuming dividends are reinvested at the end of the day stock price on the relevant quarterly ex-dividend dates. Total return is calculated assuming investors did not participate in Ares Capital Corp’s rights offering issuance as of March 20, 2008. Past performance is not indicative of future results.

5. Dividend Coverage represents annual core earnings and net realized gains/losses as a percentage of the regular dividend (excluding additional dividends) from 2010 – 2017. Excludes $196 million one‐time gain from the acquisition of Allied Capital (the “Allied Acquisition”) in Q2-10, and gains/losses from extinguishment of debt and the sale of other assets. Net realized gains/losses are net of income tax expense related to realized gains and losses and capital gains incentive fees incurred and payable as calculated under the investment advisory and management agreement.

6. Calculated as an average of the historical annual net realized gain/loss rates (where annual net realized gain/loss rate is calculated as the amount of net realized gains/losses for a particular period from Ares Capital IPO in October 2004 to December 31, 2017 divided by the average quarterly investments at amortized cost in such period). For purposes of this calculation, SSLP and SDLP subordinated certificates are considered debt investments. Excludes $196 million one‐time gain on the Allied Acquisition in Q2‐10 and gains/losses from extinguishment of debt and sale of other assets.

Slide 15: Sustained Market Premium for ARCC Yields with Lower Losses1. The weighted average yield on debt and other income producing securities is computed as (a) annual stated interest rate or yield earned plus the net annual amortization of original issue discount

and market discount or premium earned on accruing debt and other income producing securities, divided by (b) total accruing debt and other income producing securities at fair value.

2. The S&P/LSTA Leveraged Loan Index is a market value-weighted index designed to measure the performance of the U.S. leveraged loan market based upon market weightings, spreads and interest payments. Term loans from syndicated credits must meet the following criteria at issuance in order to be eligible for inclusion in the index: senior secured, minimum initial term of one year, US dollar denominated, minimum initial spread of LIBOR + 125 basis points, $50M initially funded loans. Inception date: January 1, 1997.

3. The Middle Market Index consists of middle market facilities drawn from the larger S&P/LSTA (Loan Syndications and Trading Association) Leveraged Loan Index. It is designed to measure the performance of the U.S. leveraged loan market. S&P/LSTA defines the middle market as deals with an EBITDA of less than $50 million.

4. The ICE BofAML US High Yield Index ("H0A0") tracks the performance of US dollar denominated below investment grade corporate debt publicly issued in the US domestic market. Qualifying securities must have a below investment grade rating (based on an average of Moody’s, S&P and Fitch), at least 18 months to final maturity at the time of issuance, at least one year remaining term to final maturity as of the rebalancing date, a fixed coupon schedule and a minimum amount outstanding of $100 million. Index constituents are capitalization‐weighted based on their current amount outstanding times the market price plus accrued interest. Inception date: August 31, 1986.

5. Represents ARCC’s average non-accrual rate at amortized cost from inception in October 8, 2004 to December 31, 2017.

6. Source: Moody's U.S. Trailing 12-month issuer-weighted spec-grade default rate. Actual speculative grade default data taken from January 2000 to December 31, 2017.

7. Calculated as an average of the historical annual net realized gain/loss rates (where annual net realized gain/loss rate is calculated as the amount of net realized gains/losses for a particular period from Ares Capital IPO in October 2004 to December 31, 2017 divided by the average quarterly investments at amortized cost in such period). For purposes of this calculation, SSLP and SDLP subordinated certificates are considered debt investments. Excludes $196 million one‐time gain on the acquisition of Allied Capital Corporation in Q2‐10 and gains/losses from extinguishment of debt and sale of other assets.

8. Source: Moody’s 2017 Annual Default Study. Reflects average annual loss rate for speculative grade bonds from 2000-2017.

Ares Capital Corporation - Not for Publication or Distribution 43

Endnotes

Slide 16: Compelling Core Earnings and Return on Equity1. Core Earnings is a non-GAAP financial measure. Core Earnings is the net increase (decrease) in stockholders’ equity resulting from operations less professional fees and other costs related to

the American Capital Acquisition, net realized and unrealized gains and losses, any capital gains incentive fees attributable to such net realized and unrealized gains and losses and any income taxes related to such net realized gains and losses. Net increase (decrease) in stockholders’ equity is the most directly comparable GAAP financial measure. Ares Capital believes that Core Earnings provides useful information to investors regarding financial performance because it is one method Ares Capital uses to measure its financial condition and results of operations. The presentation of this additional information is not meant to be considered in isolation or as a substitute for financial results prepared in accordance with GAAP.

2. Core return on equity calculated as Core Earnings as defined in item (1) above divided by average equity over the relevant time period.

Slide 17: Dividend and Core Earnings Plus Net Realized Gains Track Record1. Core Earnings is a non-GAAP financial measure. Core Earnings is the net increase (decrease) in stockholders’ equity resulting from operations less professional fees and other costs related to

the American Capital Acquisition, net realized and unrealized gains and losses, any capital gains incentive fees attributable to such net realized and unrealized gains and losses and any income taxes related to such net realized gains and losses. Net increase (decrease) in stockholders’ equity is the most directly comparable GAAP financial measure. Ares Capital believes that Core Earnings provides useful information to investors regarding financial performance because it is one method Ares Capital uses to measure its financial condition and results of operations. The presentation of this additional information is not meant to be considered in isolation or as a substitute for financial results prepared in accordance with GAAP.

Slide 18: ARCC Has Experienced Consistently Low Non-Accruals1. Represents ARCC’s average non-accrual rate at amortized cost from inception in October 8, 2004 to December 31, 2017.

2. Source: S&P LCD data for LSTA Leveraged Loan Index (“LLI”). Calculated as average of rolling twelve month default rates for the LLI from January 2000 to December 31, 2017.

3. Source: Moody’s U.S. Trailing 12-month issuer-weighted speculative grade default rate. Actual speculative grade default data taken from January 2000 to December 31, 2017.

4. Source: S&P LCD data for LSTA Leveraged Loan Index (“LLI”).

Ares Capital Corporation - Not for Publication or Distribution 44

EndnotesSlide 20: Strong Investment Performance 1. Based on original cash invested, net of syndications, of approximately $19.3 billion and total proceeds from such exited investments of approximately $24.9 billion.

2. Internal rate of return ("IRR") is the discount rate that makes the net present value of all cash flows related to a particular investment equal to zero. Internal rate of return is gross of management fees and expenses related to investments as these fees and expenses are not allocable to specific investments. The effect of such management and other expenses may reduce, maybe materially, the IRR’s shown herein. Investments are considered to be exited when the original investment objective has been achieved through the receipt of cash and/or non-cash consideration upon the repayment of Ares Capital’s debt investment or sale of an investment, or through the determination that no further consideration was collectible and, thus, a loss may have been realized. These IRR results are historical results relating to Ares Capital’s past performance and are not necessarily indicative of future results, the achievement of which cannot be assured.

3. Calculated as an average of the historical annual net realized gain/loss rates (where annual net realized gain/loss rate is calculated as the amount of net realized gains/losses for a particular period from Ares Capital IPO in October 2004 to December 31, 2017 divided by the average quarterly investments at amortized cost in such period). For purposes of this calculation, SDLP and SSLP subordinated certificates are considered debt investments.

4. As of December 31, 2017. Excludes $196 million one‐time gain on the acquisition of Allied Capital Corporation in Q2‐10 and gains/losses from extinguishment of debt and sale of other assets.

5. BDC peer group consists of BDCs with a market capitalization of $500 million or greater as of September 30, 2017 or who are under common management with a BDC that meets these criteria. Peers include: AINV, BKCC, CGBD, OCSL, OCSI, FSIC, GBDC, GSBD, HTGC, MAIN, NMFC, PFLT, PNNT, PSEC, SLRC, SUNS, TCAP, TCPC and TSLX.

6. Annual average from October 8, 2004 through December 31, 2016, and the last twelve month period ending September 30, 2017. For ARCC, the last twelve month period is as of December 31, 2017.

Slide 21: ARCC’s Portfolio Has Generated Higher Returns with Less Risk1. Returns are calculated as annualized average returns of dividends paid plus changes in net asset value over the time periods represented.

2. The High Yield Index represents the ICE BofAML Master II Index (“H0A0”) and the Loan Index represents the S&P/LSTA U.S. Leveraged Loan Index (“SPLLI”).

3. The BDC comparable universe consists of BDCs with a market capitalization of $500 million or greater as of September 30, 2017. This includes: AINV, BKCC, CGBD, FSIC, GBDC, GSBD, HTGC, MAIN, NMFC, OCSL, PNNT, PSEC, SLRC, TCAP, TCPC and TSLX. Of this universe, the following companies have been public for at least 3 years: AINV, BKCC, FSIC, GBDC, HTGC, MAIN, NMFC, OCSL, PNNT, PSEC, SLRC, TCAP, TCPC and TSLX. The following companies have been public for at least 5 years: AINV, BKCC, GBDC, HTGC, MAIN, NMFC, OCSL, PNNT, PSEC, SLRC, TCAP and TCPC. The following companies have been public for at least 10 years: AINV, BKCC, HTGC, PNNT, PSEC and TCAP. Data is presented as of September 30, 2017.

Ares Capital Corporation - Not for Publication or Distribution 45

EndnotesSlide 35: Deep and Diverse Access to Low Cost Debt Financing1. Subject to borrowing base, leverage and other restrictions. Represents total aggregate amount committed or outstanding, as applicable, under such instrument.

2. Represents the total aggregate principal amount outstanding as of December 31, 2017.

3. Effective stated rate as of December 31, 2017. In December 2017, Ares Capital entered into an interest rate swap agreement to effectively fix the interest rate in connection with the $395 million term loan tranche of the Revolving Credit Facility. The stated interest rate for the Revolving Credit Facility reflects the fixed interest rate of 2.064% plus the applicable spread of 1.75%, or 3.814% on the term loan tranche.

4. Requires periodic payments of interest and may require repayments of a portion of the outstanding principal once their respective reinvestment periods end but prior to the stated maturity.

5. In January 2018, Ares Capital issued $600 million aggregate principal amount of unsecured notes that mature on March 1, 2025 (the “2025 Notes”). The 2025 Notes bear interest at a rate of 4.25% per year, payable semi-annually on March 1 and September 1 of each year, commencing on September 1, 2018. The 2025 Notes may be redeemed in whole or in part at the Company’s option at any time at the redemption prices as determined pursuant to the indenture governing the 2025 Notes.

6. Assumes all committed capital is fully drawn. In December 2017, Ares Capital entered into an interest rate swap agreement to effectively fix the interest rate in connection with the $395 million term loan tranche of the Revolving Credit Facility. The stated interest rate for the Revolving Credit Facility reflects the fixed interest rate of 2.064% plus the applicable spread of 1.75%, or 3.814% on the term loan tranche.

Slide 36: Prudent Maturity Ladder1. Represents the total aggregate principal amount outstanding due on the stated maturity date.

2. The use of leverage magnifies the potential for gain or loss on the amount invested and may increase the risk of investment.

3. Represents an average of the three years ended December 31, 2017.

4. While Ares Capital expects to settle each of the 2019 Convertible Notes and 2022 Convertible Notes of $300.0 million and $388.00 million, respectively, in cash, Ares Capital has the option to settle each in cash, shares of common stock or a combination of cash and shares of common stock. The 2018 Convertible Notes of $270.0 million were repaid, in cash, at maturity in January 2018.

5. The 2018 High Grade Notes, the 2020 High Grade Notes, the 2022 High Grade Notes, the 2023 High Grade Notes may be redeemed in whole or in part at any time at Ares Capital’s option at a redemption price equal to par plus a “make whole” premium, as determined in the indenture governing the 2018 High Grade Notes, the 2020 High Grade Notes, the 2022 High Grade Notes, and the 2023 High Grade Notes and any accrued and unpaid interest.

6. The 2047 Notes with an aggregate principal amount of $230.0 million may be redeemed in whole or in part at any time or from time to time at Ares Capital's option at par redemption price of $25 per security plus accrued and unpaid interest.

7. As of December 31, 2017, the end of the reinvestment period for the Revolving Funding Facility is January 3, 2019. Subsequent to the end of this reinvestment period and prior to the stated maturity date of January 3, 2022, any principal proceeds from sales and repayments of loan assets held by Ares Capital CP Funding LLC will be used to repay the aggregate principal amount outstanding.

8. As of December 31, 2017, the end of the reinvestment period for the SMBC Funding Facility is September 14, 2018. Subsequent to the end of this reinvestment period and prior to the stated maturity date of September 14, 2023, any principal proceeds from sales and repayments of loan assets held by Ares Capital JB Funding LLC will be used to repay the aggregate principal amount outstanding.

9. In January 2018, Ares Capital issued the 2025 Notes. The 2025 Notes bear interest at a rate of 4.25% per year, payable semi-annually on March 1 and September 1 of each year, commencing on September 1, 2018. The 2025 Notes may be redeemed in whole or in part at Ares Capital’s option at any time at the redemption prices as determined pursuant to the indenture governing the 2025 Notes.

Ares Capital Corporation - Not for Publication or Distribution

Performance Notes

Ares Capital Corporation - Not for Publication or Distribution 47

Performance Notes to Overview of Ares Management SlideInformation respecting prior performance whether of a particular fund or investment strategy is not and should not be interpreted as a guaranty of future performance. Moreover, no assurancecan be given that unrealized, targeted or projected valuations or returns will be achieved. Future results are subject to any number of risks and factors, many of which are beyond the control ofAres. As with any investment, there is always the potential for gains as well as the possibility of losses.

Performance returns are as of December 31, 2017. Gross and net returns are rounded to the nearest whole number. Returns include the reinvestment of income and other earnings. Gross returnsdo not reflect the deduction of management fees, performance fees and carried interest, as applicable, or any other expenses that may be incurred in the management of the account. Net returnsfor the U.S. Bank Loan Aggregate and U.S. High Yield Composites are reduced by management fees; all other net returns are after giving effect to management fees, performance fees and carriedinterest, as applicable, and other expenses. The performance represented on this slide is considered representative of strategies currently available for investment. We believe aggregatedperformance returns reflect our overall performance returns in a strategy, but are not necessarily investable funds or products themselves. The performance does not represent all assets managedby Ares. The return earned by investors may vary materially from those presented. There can be no assurance that unrealized values or projected returns will be achieved.

Credit• Performance for U.S. Syndicated Loans is represented by the U.S. Bank Loan Aggregate Composite which includes all actual, fully discretionary, fee-paying, portfolios that are benchmarked to

the Credit Suisse Leveraged Loan Index and primarily invested in U.S. Dollar denominated banks loans. Portfolios may have limited allocations to high yield and structured securities. Portfoliosin the U.S. Bank Loan Aggregate Composite have an emphasis on capital appreciation and income. For periods prior to January 1, 2010 the U.S. Bank Loan Aggregate Composite included thebank loan segments of multi-asset class portfolios. The inception date of the U.S. Bank Loan Aggregate Composite is November 1997. From January 1, 2000 through January 1, 2010, cash wasallocated on a monthly basis to the bank loan segments based on relative assets. For periods prior to January 1, 2000 cash was not allocated to the bank loan segments. As of January 1, 2010the U.S. Bank Loan Aggregate Composite no longer includes bank loan segments of multi-asset class portfolios. The benchmark for the U.S. Bank Loan Aggregate Composite is the Credit SuisseLeveraged Loan Index. The index is designed to mirror the investable universe of the U.S. Dollar-denominated leveraged loan market. Investment track record of 15+ years dates prior tocomposite inception when Ares managed syndicated loans and high yield assets as part of its CLO strategy.

• Performance for U.S. High Yield is represented by the U.S. High Yield Composite, which includes all actual, fully discretionary, fee-paying, separately managed portfolios that primarily invest inU.S. high yield fixed income securities and are benchmarked to the ICE BofAML US High Yield Master II Constrained Index. Portfolios in the U.S. High Yield Composite have an emphasis oncapital appreciation and income. The benchmark for the U.S. High Yield Composite is the ICE BofAML US High Yield Master II Constrained Index, which tracks the performance of U.S. Dollar-denominated below investment grade corporate debt publicly issued in the U.S. domestic market with a maximum issuer exposure of 2%. The inception date of the U.S. High Yield Composite isMay 2007. Investment track record of 15+ years dates prior to composite inception when Ares managed syndicated loans and high yield assets as part of its CLO strategy.

• Gross performance for the Structured Product Core Composite is an annualized gross internal rate of return (“IRR”) that is calculated using the combined capital draw dates from the fee-paying limited partners in each fund for the composite and a combined fund valuation for the composite as of the period end date. The inception date of the IRRs for the Structured ProductCore Composite is August 11, 2008, which is the date of the first capital calls in the composite. IRRs include the reinvestment of income and other earnings and reflect the deduction of alltrading expenses. IRRs are presented as annualized returns. The gross IRR does not reflect the deduction of management fees, performance fees and carried interest, as applicable, andoperating and administrative expenses. Returns include the reinvestment of income and other earnings and reflect the deduction of all trading expenses. The net IRR reflects the deduction ofmanagement fees, performance fees and carried interest as if the composite was liquidated, and operating and administrative expenses. Actual expenses allocated to fee-paying limitedpartners are used in the net IRR calculation.

• Benchmark returns are provided to represent the investment environment existing during the time period shown. The returns for the ICE BofAML US High Yield Master II Constrained Index andthe Credit Suisse Leveraged Loan Index include the reinvestment of income and other earnings, but do not include transaction costs, management fees or other costs. Returns for the HFRIFund Weighted Composite Index are calculated using a time-weighted rate of return and are net of all fees.