indonesia’s e-commerce - cccs.gov.sg · •e-commerce in indonesia is growing and taking larger...

TRANSCRIPT

Indonesia’s E-Commerce: A New Engine of Growth?

Yose Rizal Damuri (CSIS)

Siwage Dharma Negara & Kathleen Azali (ISEAS-Yusof Ishak Institute)

Symposium on E-Commerce, ASEAN Economic Integration, and Competition Policy & Law

Singapore, 16 March 2017

Key Messages

• E-commerce in Indonesia is growing and taking larger portion of sales• Several factors have boosted e-commerce performance in Indonesia, e.g.

massive development of related infrastructures• E-commerce is perceived as an alternative marketing channel for SMEs• The government remains ambivalent towards the development of e-

commerce• Want to see it growing with a very high target, while expecting e-commerce to foster

SMEs• But remain cautious to its impact on traditional retails, international trade, industrial

development, and taxation

• Challenges are still abundant for future development• Consumer and data protection, lacks of reliable payment system• SMEs access to various enabling factors remain limited, e.g. access to financing

Rapid growth but still relatively small

• Retail e-commerce in Indonesia has been growing rapidly• While it is still small compared

to other countries, it grew by around 30% annually during the last five years

• The proportion to retail sales is still small but increasing

• The government targeted the online transactions to reach US$130 billion (2020)• More than 30 times increase

of 2015 figures

Source: Statista

Factors Supporting E-Commerce Development: Demography

• Largest market in SEA

• A growing middle class (135 mill by 2020)

• Young population: 70 per cent of the population is under the age of 40

• Big share of population aged 15-34

Source: CIA World Factbook

Factors Supporting E-Commerce Development: Growing Internet Penetration

32.0

22.0

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

2010 2011 2012 2013 2014 2015

Percentage of Population using internet

Urban Rural National

18.40%

24.40%29.20%

18.00%

10.00%

75.80% 75.80%

54.70%

17.20%

2%0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

10 - 24 yo 25 - 34 yo 34 - 44 yo 45 - 54 yo 55 + yo

Age Composition & Penetration (2016)

2016 Composition 2016 Penetration

Source: Susenas 2014 Source: APJII

Rising internet penetration (36 million in 2010, 93 million in 2015)

Supported by growing number of mobile internet and payment tools

6578

93105

122146

8 14 2236 36 4336

47 5568

85 93.4

9.4 8.7 7.7 10.1 9.9 10.4

243.8

279.8

312.3331.7 341.9 341.5

0

50

100

150

200

250

300

350

400

2010 2011 2012 2013 2014 2015

ATM Debit Credit Cards E Money Cards Internet User Fixed Line Subscribers Cell phone subscribers

Source: Susenas 2014

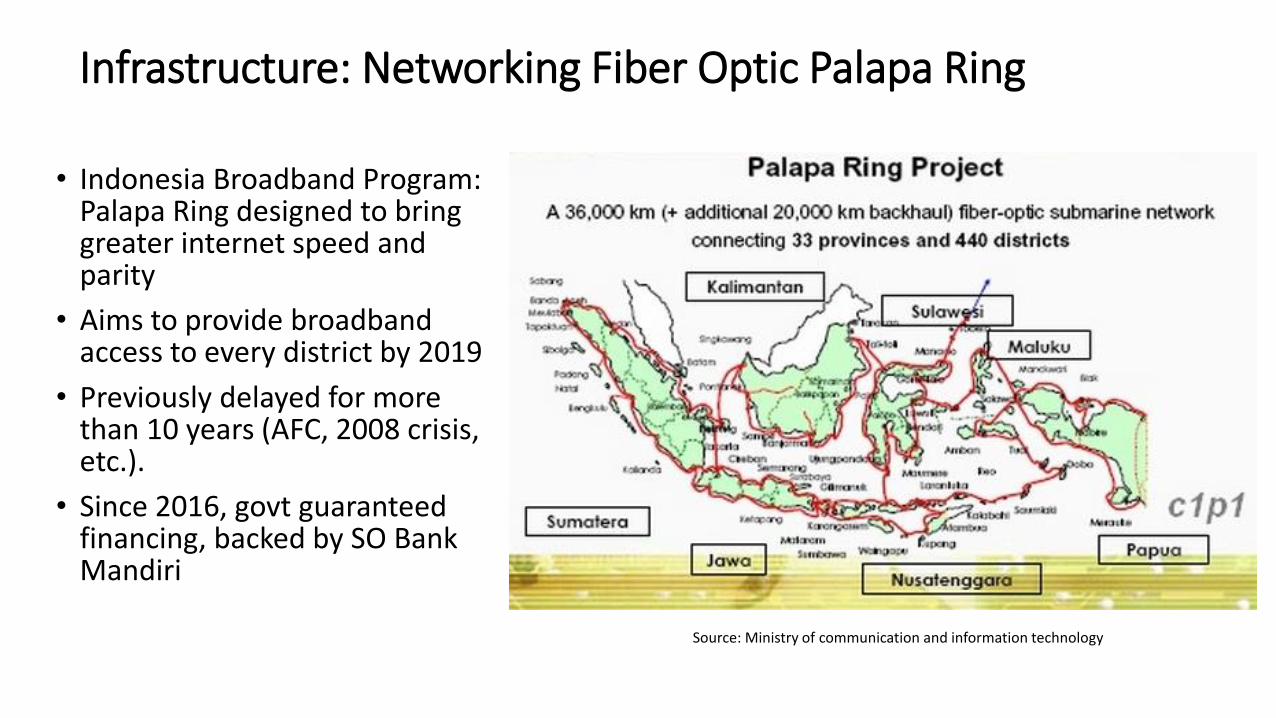

Infrastructure: Networking Fiber Optic Palapa Ring

• Indonesia Broadband Program: Palapa Ring designed to bring greater internet speed and parity

• Aims to provide broadband access to every district by 2019

• Previously delayed for more than 10 years (AFC, 2008 crisis, etc.).

• Since 2016, govt guaranteed financing, backed by SO Bank Mandiri

Source: Ministry of communication and information technology

Existing submarine cables, facing geographical challenges

Source: submarinecablemap

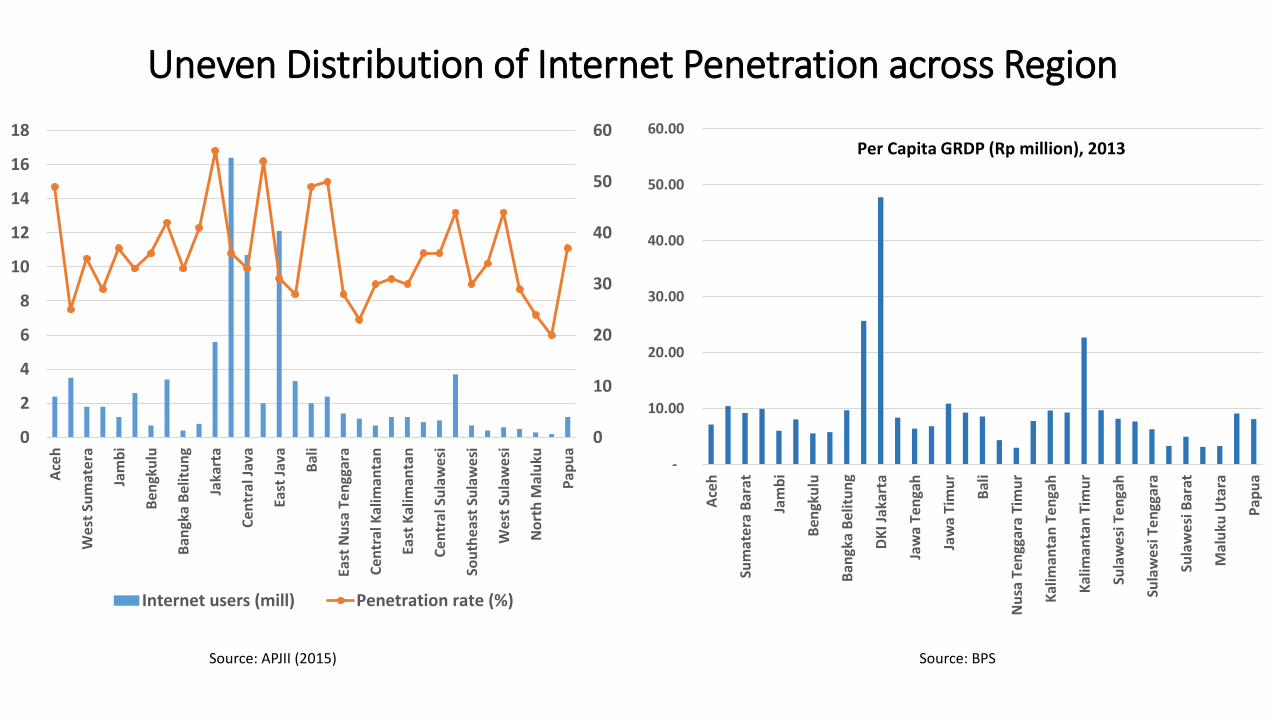

Uneven Distribution of Internet Penetration across Region

0

10

20

30

40

50

60

0

2

4

6

8

10

12

14

16

18

Ace

h

Wes

t Su

mat

era

Jam

bi

Ben

gku

lu

Ban

gka

Bel

itu

ng

Jaka

rta

Ce

ntr

al J

ava

East

Jav

a

Bal

i

East

Nu

sa T

en

ggar

a

Ce

ntr

al K

alim

anta

n

East

Kal

iman

tan

Ce

ntr

al S

ula

wes

i

Sou

thea

st S

ula

we

si

Wes

t Su

law

esi

No

rth

Mal

uku

Pap

ua

Internet users (mill) Penetration rate (%)

Source: APJII (2015)

-

10.00

20.00

30.00

40.00

50.00

60.00

Ace

h

Sum

ate

ra B

arat

Jam

bi

Ben

gku

lu

Ban

gka

Be

litu

ng

DK

I Jak

arta

Jaw

a Te

nga

h

Jaw

a Ti

mu

r

Bal

i

Nu

sa T

engg

ara

Tim

ur

Kal

iman

tan

Te

nga

h

Kal

iman

tan

Tim

ur

Sula

we

si T

en

gah

Sula

we

si T

en

ggar

a

Sula

we

si B

arat

Mal

uku

Uta

ra

Pap

ua

Per Capita GRDP (Rp million), 2013

Source: BPS

The Landscape of E-commerce in Indonesia

• E-commerce has just recently developed in Indonesia

• It started with simple marketplaces/classifieds where sellers can only advertise their products• Buyers and sellers make contact

directly• The transactions is normally conducted

through e-mails, phone calls or messaging

• Several integrated platforms started to grow by early 2010s• Especially when some big providers

offer integrated services of online transactions

• Turning point in the development of e-commerce in Indonesia

Source: Bede Moore, Lazada Indonesia (2016)

VC firms mostly linked to major conglomeratesLaunch date Backing Significant investments in

Venturra Mid 2015 Riady (re-incarnation of Lippo Digital Ventures)

GrabTaxi, HappyFresh, Bridestory, Munchery, RuangGuru, First Media ISPLippo also invested in MatahariMall, Lazada

SMDV Mid 2015 Widjaja (Sinar Mas Digital Ventures)

HappyFresh, aCommerce, FemaleDaily, MyRepublicISP

Convergence Ventures

Nov 2014 Bakrie Path, Qraved, YesBoos, MBDC media

Emtek Nov 2014 Sariaatmadja Bukalapak, PropertyGuru, Kudo, Hijup, BoboBobo

2010 Hartono (Djarum) BliBli, Kaskus, Daily Social, InfoKost

Skystar Capital Dec 2013 Kompas Gramedia Group SCOOP, Bridestory, Hijup

Source: Bede Moore, Lazada Indonesia (2016)

E-commerce and SMEs

• The development of e-commerce is believed to offer significant chances in retail and distribution for SMEs

• New potentials for the creation of networks, and cross-border activities• Enabling companies to compete with

larger firms, while encouraging the creation of new businesses and to the innovation

• But the proportion of firms using email and have websites is still small• Necessary conditions to be connected to

the network and to take advantages of e-commerce

32.27%

17.11%

46.21%

35.83%

Used email Had Website

Firms using Internet and e-mail, Indonesia 2009 & 2015

2009 20092015 2015

Source: World Bank Enterprise Survey

Despite all the development… only 7% of Indonesian buys online

51%

82% 87%

58%75%

58% 64% 68%

6%

3% 2%

5%

4%

4%

12% 6%38%

11% 7%

30%10%

33%14% 18%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

China India Indonesia Malaysia Philippines Singapore Thailand Vietnam

Consumers purchase behavior (2014)

Offline Store Phone Online

Source: Google Barometer

Most people use internet for social media….

3.9%

8.4%

11.3%

27.8%

35.1%

45.1%

73.5%

82.0%

Others

Financial facility (e-banking)

Online trading

Sending and receiving e-mail

Doing school assignments

Entertainment/games

Searching information/news

Social Media

Source: Susenas (2014)

Some infrastructures are just not sufficient….

36.70%

14.20%

7.50%

2.50%

1.60%

0.70%

0.00% 10.00% 20.00% 30.00% 40.00%

via ATM

Cash on Delivery (COD)

Internet banking

Credit cards

SMS banking

E-money

Payment methods

0%

20%

40%

60%

80%

100%

120%

0

2

4

6

8

10

12

14

16

18

Singapore Thailand Malaysia Vietnam Indonesia

Speed (Mbps) Q1-2016

Proportion of IP Address with Speed > 4Mbps

Source: APJII (2016) Source: Akamai – State of the Internet Connectivity Report 2016

And consumers still don’t trust online shopping…

56

36

35

35

34

30

22

9

8

8

0 10 20 30 40 50 60

Online shopping has a fraudulent image

I cannot try/test the product

Payment is not safe/convenient

Price is higher

Product quality is not reliable

Unsatisfactory sales support

I don't know how

Online shopping has a low-end image

Products are not available online

Poor after-sales service

Source: McKinsey (2013)

Current regulations

• Law No 8/1999 on consumer protection• Law No 11/2008 on information and electronic transaction• Government Regulation No 82/2012 on electronic system and transactions• Law No 7/2014 on trade (Article 65 and 66 on e-commerce)• Presidential regulation No 44/2016 opens e-commerce business for foreign

investment • DG Tax circular No 6/2015 which sets the taxes to be paid by e-commerce

business• Financial Services Authority (OJK) regulation no. 77/2016 regarding

Information Technology-Based Money Lending Services, e.g. peer-to-peer lending (P2P lending)

• Draft government regulation on e-commerce

Policy IssuesPolicy Areas Possible Issues Illustrative Cases

Competition-related - Definition of relevant market- Winner takes all- Definition of anti-competitive

behavior

- Web-based vs traditional transport services- Acquisition of platforms to increase market share- Some e-commerce platforms might use

consumers’ profiles and characteristics for other services they offer

Consumer protection - Fraudulent activities in C2C and B2C marketplaces

- Risky payment mechanism

- Complaints about quality of goods, or delivery time

- Especially in using credit cards on unsecured services

International trade - Cross-border e-commerce- Impact to domestic industry and

start-up services

- Tariff application for such imported goods

Taxation - Taxing internet-based economic activities

- Problems if the services is supplied cross-border,e.g. Google case, Amazon

Data protection and traffic

- Freedom of data flow and privacy

- Requirement for localization of data centers

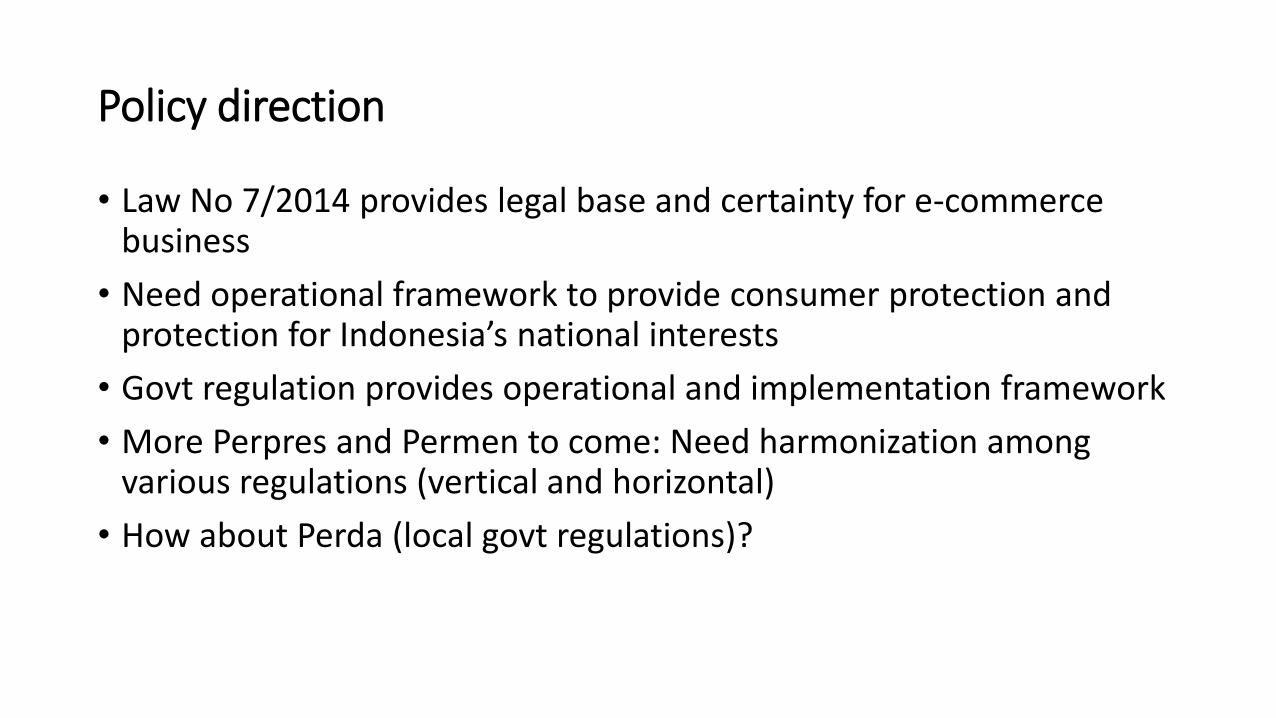

Policy direction

• Law No 7/2014 provides legal base and certainty for e-commerce business

• Need operational framework to provide consumer protection and protection for Indonesia’s national interests

• Govt regulation provides operational and implementation framework

• More Perpres and Permen to come: Need harmonization among various regulations (vertical and horizontal)

• How about Perda (local govt regulations)?

Government departments & regulators

1. Coordinating Ministry of Economic

Affairs

2. Ministry of Communication and

Information

3. Ministry of Trade

4. Ministry of Industry

5. Head of Creative Economy (Bekraf)

6. Ministry of Finance

7. Bank Indonesia

8. OJK (Financial Service Authority)

Enforcement? Coordination across ministries and govt agencies remains challenging

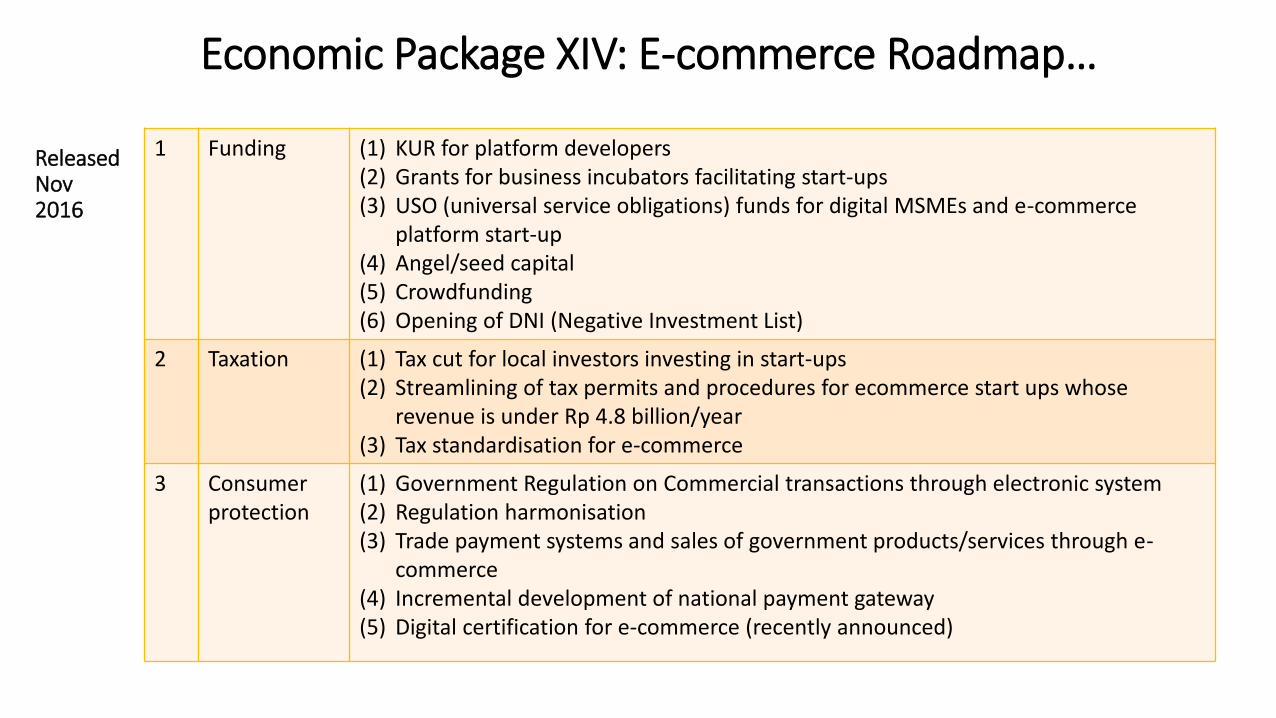

Economic Package XIV: E-commerce Roadmap…

Released Nov2016

1 Funding (1) KUR for platform developers(2) Grants for business incubators facilitating start-ups(3) USO (universal service obligations) funds for digital MSMEs and e-commerce

platform start-up(4) Angel/seed capital (5) Crowdfunding(6) Opening of DNI (Negative Investment List)

2 Taxation (1) Tax cut for local investors investing in start-ups(2) Streamlining of tax permits and procedures for ecommerce start ups whose

revenue is under Rp 4.8 billion/year(3) Tax standardisation for e-commerce

3 Consumer protection

(1) Government Regulation on Commercial transactions through electronic system(2) Regulation harmonisation(3) Trade payment systems and sales of government products/services through e-

commerce(4) Incremental development of national payment gateway(5) Digital certification for e-commerce (recently announced)

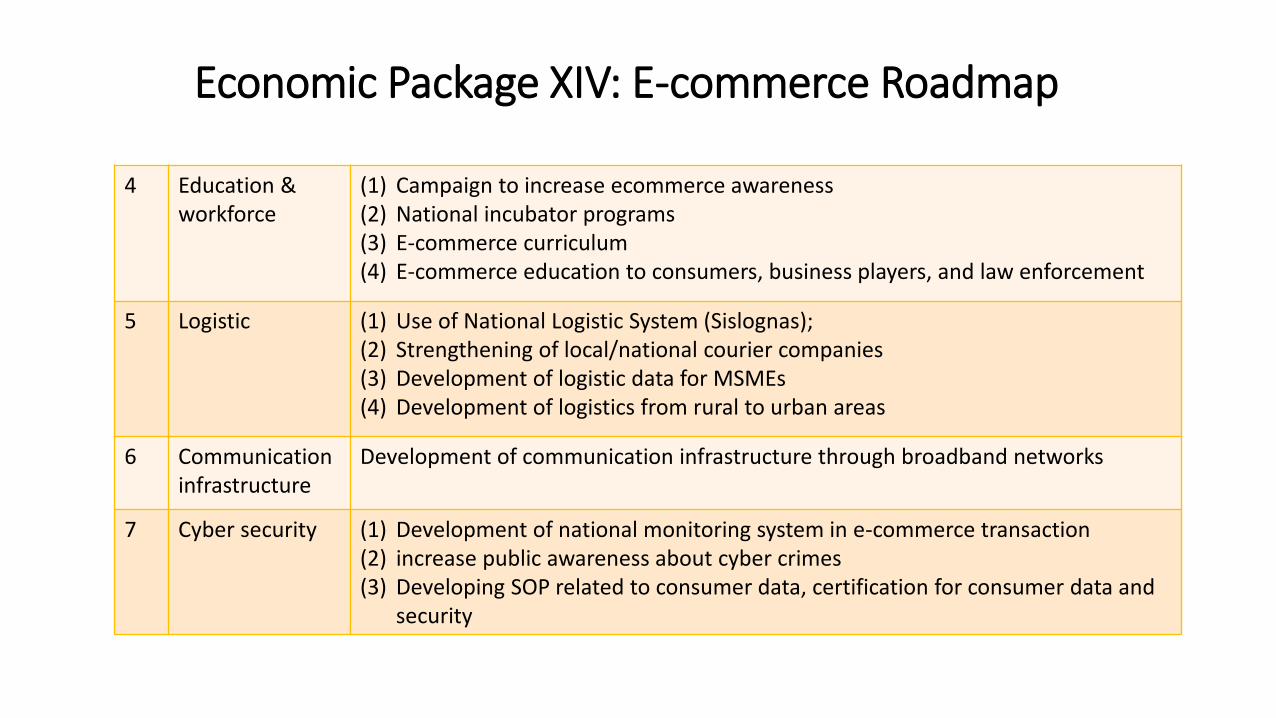

4 Education & workforce

(1) Campaign to increase ecommerce awareness(2) National incubator programs(3) E-commerce curriculum(4) E-commerce education to consumers, business players, and law enforcement

5 Logistic (1) Use of National Logistic System (Sislognas); (2) Strengthening of local/national courier companies(3) Development of logistic data for MSMEs(4) Development of logistics from rural to urban areas

6 Communicationinfrastructure

Development of communication infrastructure through broadband networks

7 Cyber security (1) Development of national monitoring system in e-commerce transaction(2) increase public awareness about cyber crimes(3) Developing SOP related to consumer data, certification for consumer data and

security

Economic Package XIV: E-commerce Roadmap

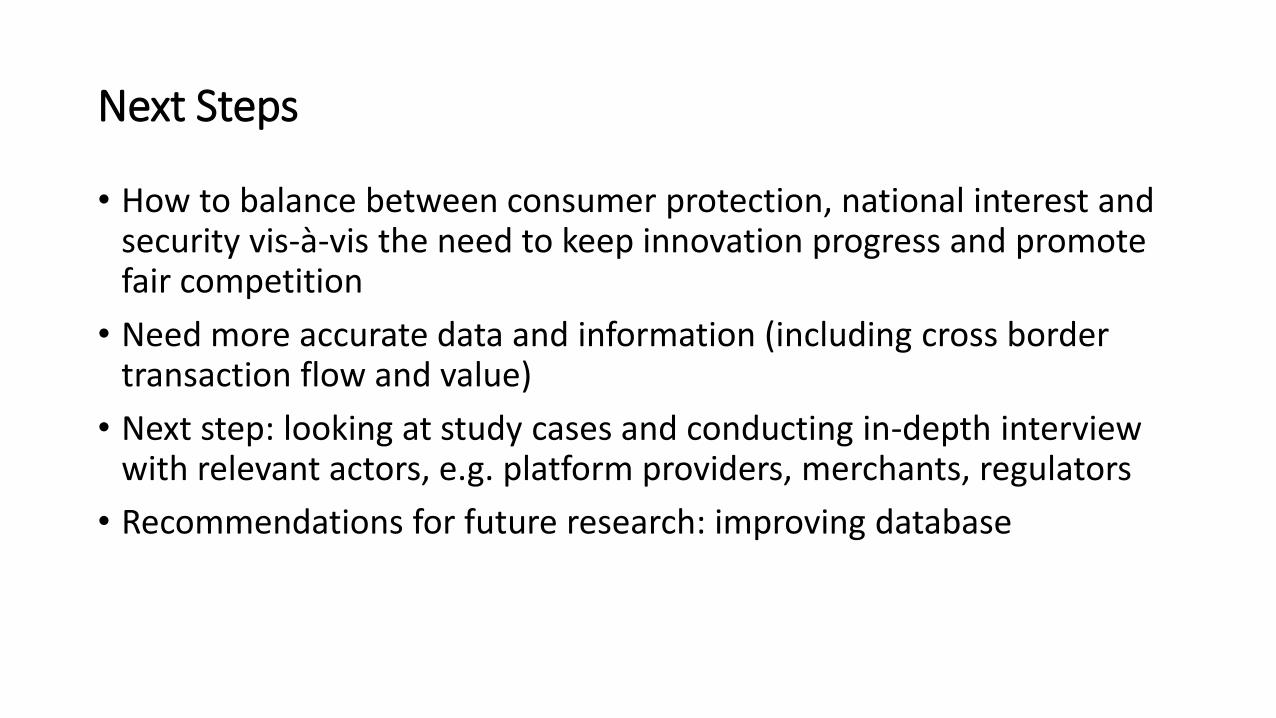

Next Steps

• How to balance between consumer protection, national interest and security vis-à-vis the need to keep innovation progress and promote fair competition

• Need more accurate data and information (including cross border transaction flow and value)

• Next step: looking at study cases and conducting in-depth interview with relevant actors, e.g. platform providers, merchants, regulators

• Recommendations for future research: improving database

THANK YOU