green diesel_final report

TRANSCRIPT

Methods and Economics of Renewable Diesel Production

12 May 2016

Group O: Michael P. Letterio, Robert McNew, Nickolas

Martin

1

Abstract

The hydrodeoxygenation of triglyceride feedstocks has been shown in the literature

to be a viable alternative to the production of diesel fuel. Renewable diesel boasts a high

cetane number along with decreased carbon emissions. However renewable diesel suffers

from poor cold flow properties. Using soybean oil as a feedstock we have developed a two-

reactor process, hydrodeoxygenation (HDO) employing a sulfided NiMo catalyst followed

by isomerization to ensure suitable diesel properties using a Pt/SAPO11 catalst.1,2 Capital

investment of renewable diesel plants can run as high as $1 billion with high feedstock

costs. Current diesel prices make it impossible for a profitable renewable diesel business

to be developed currently. However it has shown promise to be fairly profitable if the

market turns around. To promote the use of renewable fuels, US policy makers have

currently allowed for a $1/gallon tax credit. Renewable diesel has been shown to lower

CO2 emissions by 60% on a per energy basis compared to conventional diesel production.

Government intervention and changing markets could help make this process feasible in

the future.

2

Table of Contents

Introduction ................................................................................................................... 5

Feedstock Choice ........................................................................................................... 6

Current Renewable Diesel facilities ................................................................................... 7

Process Development ...................................................................................................... 9

ASPEN Modeling ......................................................................................................... 10

Heat Integration ............................................................................................................ 12

Haz Ops ...................................................................................................................... 14

Market Analysis ........................................................................................................... 16

Government Policies ..................................................................................................... 19

Economics ................................................................................................................... 20

Life Cycle Analysis....................................................................................................... 23

Appendix A: Economics ................................................................................................ 30

Appendix B: Aspen Data ............................................................................................... 32

Appendix C: Market Analysis ......................................................................................... 43

Appendix D: ASTM Diesel Standards .............................................................................. 48

3

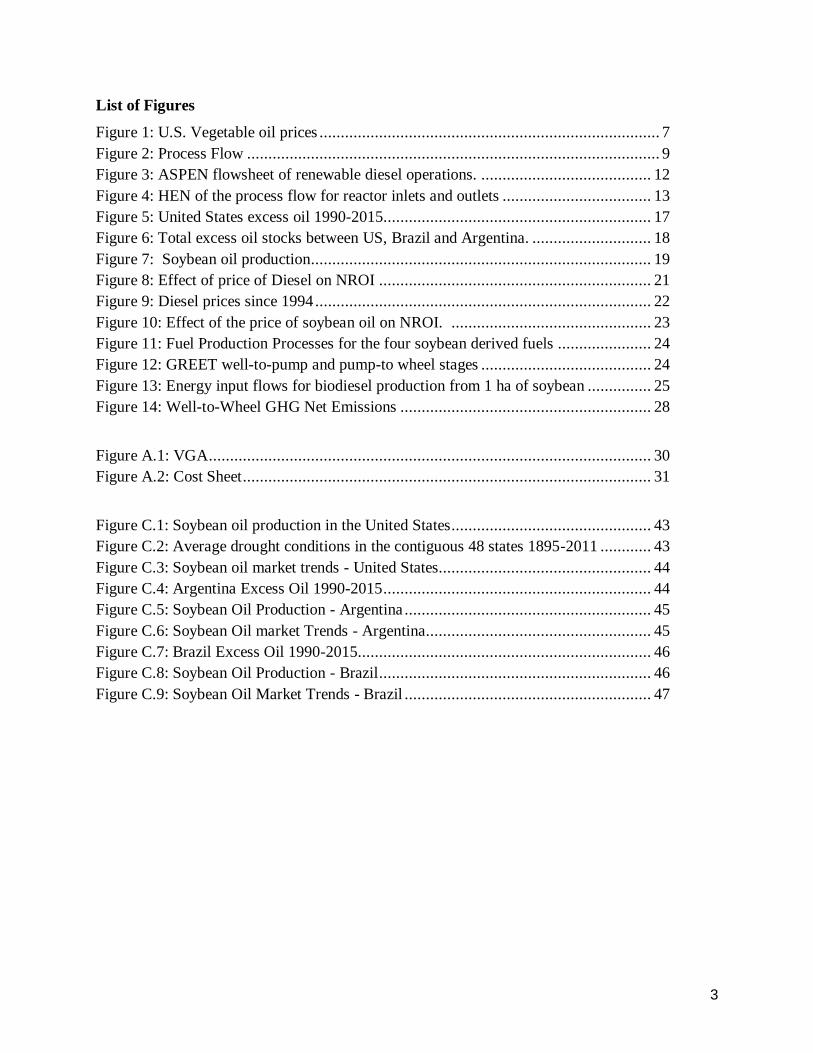

List of Figures

Figure 1: U.S. Vegetable oil prices ................................................................................ 7

Figure 2: Process Flow ................................................................................................. 9

Figure 3: ASPEN flowsheet of renewable diesel operations. ........................................ 12

Figure 4: HEN of the process flow for reactor inlets and outlets ................................... 13

Figure 5: United States excess oil 1990-2015............................................................... 17

Figure 6: Total excess oil stocks between US, Brazil and Argentina. ............................ 18

Figure 7: Soybean oil production................................................................................ 19

Figure 8: Effect of price of Diesel on NROI ................................................................ 21

Figure 9: Diesel prices since 1994 ............................................................................... 22

Figure 10: Effect of the price of soybean oil on NROI. ............................................... 23

Figure 11: Fuel Production Processes for the four soybean derived fuels ...................... 24

Figure 12: GREET well-to-pump and pump-to wheel stages ........................................ 24

Figure 13: Energy input flows for biodiesel production from 1 ha of soybean ............... 25

Figure 14: Well-to-Wheel GHG Net Emissions ........................................................... 28

Figure A.1: VGA ........................................................................................................ 30

Figure A.2: Cost Sheet ................................................................................................ 31

Figure C.1: Soybean oil production in the United States ............................................... 43

Figure C.2: Average drought conditions in the contiguous 48 states 1895-2011 ............ 43

Figure C.3: Soybean oil market trends - United States.................................................. 44

Figure C.4: Argentina Excess Oil 1990-2015 ............................................................... 44

Figure C.5: Soybean Oil Production - Argentina .......................................................... 45

Figure C.6: Soybean Oil market Trends - Argentina..................................................... 45

Figure C.7: Brazil Excess Oil 1990-2015 ..................................................................... 46

Figure C.8: Soybean Oil Production - Brazil ................................................................ 46

Figure C.9: Soybean Oil Market Trends - Brazil .......................................................... 47

4

List of Tables

Table 1: A comparison of carbon structure composition of various candidates for

renewable diesel feedstock. ........................................................................................... 6

Table 2: Current Renewable Diesel Production .............................................................. 8

Table 3: Haz Ops ........................................................................................................ 14

Table 4: Potential carbon tax savings........................................................................... 20

Table 5: Economics of Current Design ........................................................................ 20

Table 6: Land Requirement for fuel production ........................................................... 25

Table 7: Energy Use for Soybean Farming in the United States (USDA 2007b) ............ 26

Table 8: Energy Use and Amount of Fuel Prodcut and Co-Products from One Ton of

Soybeans .................................................................................................................... 27

Table B.1: Cases for Flash 1 ....................................................................................... 32

Table B.2: Cases for Table 2 ....................................................................................... 33

Table B.3: Aspen Block Summary .............................................................................. 34

Table B.4: Aspen Stream Tables ................................................................................. 39

5

Introduction

As anthropogenic CO2 emissions continue to rise there has been an increasing

desire to develop biofuels from a variety of different sources, including biomass and

triglycerides. The use of biofuels creates a closed carbon cycle theoretically preventing

any carbon addition to the atmosphere. Currently much of the biofuels industries employ

first generation (edible) feedstock. The processing of triglycerides to either biodiesel or

renewable diesel production. Biodiesel is produced by the transesterification of

triglycerides to produce fatty acid methyl esters (FAME). Biodiesel has come under

substantial criticism due to its expensive separation structure and oxygenate content that

would require current diesel engines to be modified. An alternative to this is the HDO of

triglycerides to produce hydrocarbons.4-7 The HDO of triglyceride feedstock produces n-

chain hydrocarbons in the diesel range that can be used without blending in the diesel

engines used. The HDO process produces diesel fuel with a much higher cetane number

than conventional diesel fuel due to the higher purity of diesel products. The major concern

of renewable diesel is the cold flow properties of the diesel fuel. By employing an

isomerization process the cold flow properties of renewable diesel can be greatly improved

while maintaining a high cetane number. Current possible feedstock include soybean,

palm, and rapeseed oils as first generation fuels along while jatropha and waste oils can be

used as second-generation fuels (non-edible).

Global diesel demand is expected to increase from 27 MMB/D to 33 MMB/D by

2030, leaving an opportunity for other methods of diesel production to fill the demand gap.8 The

development of renewable diesel facilities has been limited by the high capital cost of

plants and price fluctuations in the feedstock and final product markets. Here we provide

a process design and economic analysis of a potential renewable diesel facility.

6

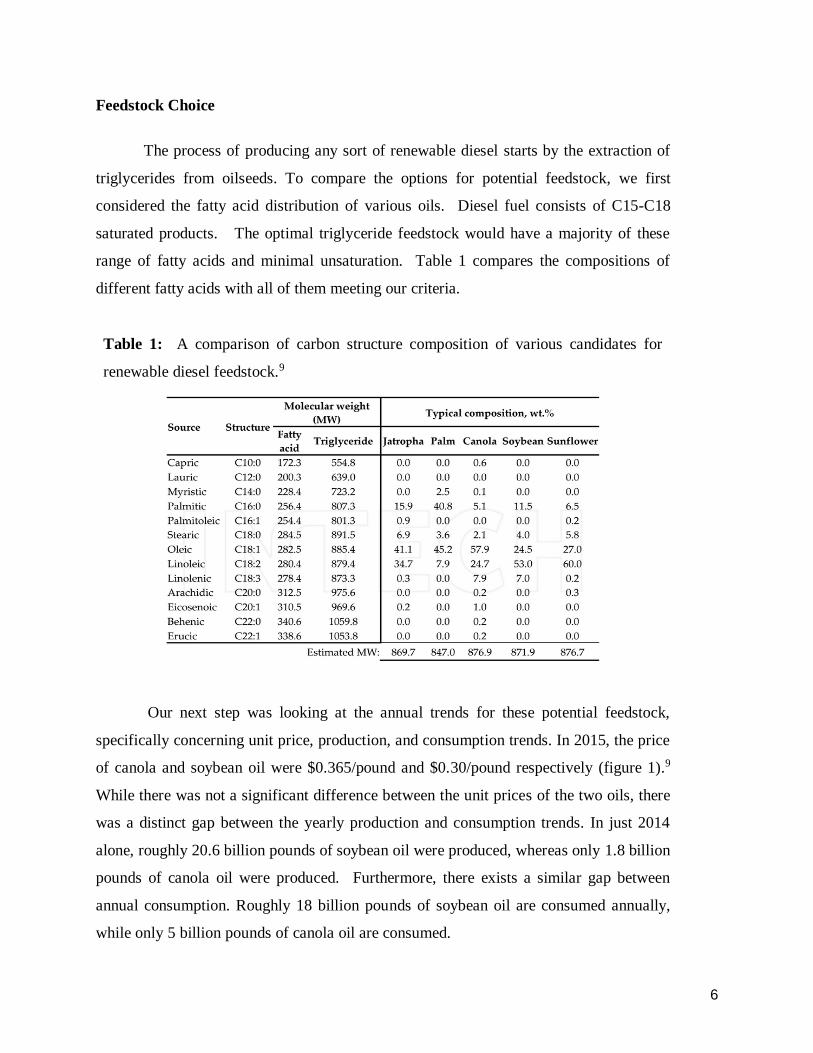

Feedstock Choice

The process of producing any sort of renewable diesel starts by the extraction of

triglycerides from oilseeds. To compare the options for potential feedstock, we first

considered the fatty acid distribution of various oils. Diesel fuel consists of C15-C18

saturated products. The optimal triglyceride feedstock would have a majority of these

range of fatty acids and minimal unsaturation. Table 1 compares the compositions of

different fatty acids with all of them meeting our criteria.

Table 1: A comparison of carbon structure composition of various candidates for

renewable diesel feedstock.9

Our next step was looking at the annual trends for these potential feedstock,

specifically concerning unit price, production, and consumption trends. In 2015, the price

of canola and soybean oil were $0.365/pound and $0.30/pound respectively (figure 1).9

While there was not a significant difference between the unit prices of the two oils, there

was a distinct gap between the yearly production and consumption trends. In just 2014

alone, roughly 20.6 billion pounds of soybean oil were produced, whereas only 1.8 billion

pounds of canola oil were produced. Furthermore, there exists a similar gap between

annual consumption. Roughly 18 billion pounds of soybean oil are consumed annually,

while only 5 billion pounds of canola oil are consumed.

7

Figure 1: U.S. Vegetable oil prices3

With this data, it becomes clear that soybean oil is the most abundant and therefore

our recommended renewable diesel feedstock. Based on the current market growth and

consumption of soybean oil as our feedstock, we expect to produce 131 MMgal/yr of

renewable diesel from a 600 MTonnes/yr feedstock.

Current Renewable Diesel facilities

To develop the scope of our project we first wanted to obtain an idea of the global

renewable diesel production we compared our proposed facility show in Table 2. As can

be seen from the table the current market for renewable diesel is still relatively small,

with most plants starting up some time between 2008 and 2013. The exception to this

data is the Delaware City Refinery which produces conventional diesel oil at a capacity

much larger than any renewable diesel facility. ASTM diesel standards are provided in

the appendix for reference.

8

Table 2: Current Renewable Diesel Production10

Company Size (bpd) Location Feedstock

ConocoPhillips 1,000 Ireland Soybean Oil, Animal Fats

ConocoPhillips 12,000 United States Soybean Oil

Diamond Green Diesel

(Valero) a

17,000 United States Soybean Oil, Animal fats

Delaware City Refinery b 52,000 United States Petroleum

Neste 2 x 3,400 Finland Palm, Rapeseed, animal fats

Neste 13,600 Singapore Palm Oil

Neste 13,600 Netherlands Palm, Rapeseed, animal fats

Petrobras c 4 x 4000 Brazil

British Petroleum c 1,900 Australia

UOP/Eni 6,500 Italy Soybean Oil

Our Proposed Facility 9,800 United States Soybean Oil

a Currently producing 10000 bpd expected expansion of approximately 7000 bpd Q1 2018

b Conventional Diesel Production c Co-processing plants

9

Process Development

Our proposed process flow diagram is shown in Figure 2. The oil will first enter a

reactor and undergo HDO, with a flash tank used to separate the oil from water and syngas.

The liquid stream goes through a second reactor to isomerize the n-alkanes to achieve

desired physical properties. Another flash tank is used to again separate our product oil

from syngas and water. The vapor streams from the flash tanks undergo hydrogen

separation with the use of a ceramic membrane with near 100% hydrogen selectivity.11

Figure 2: Process Flow

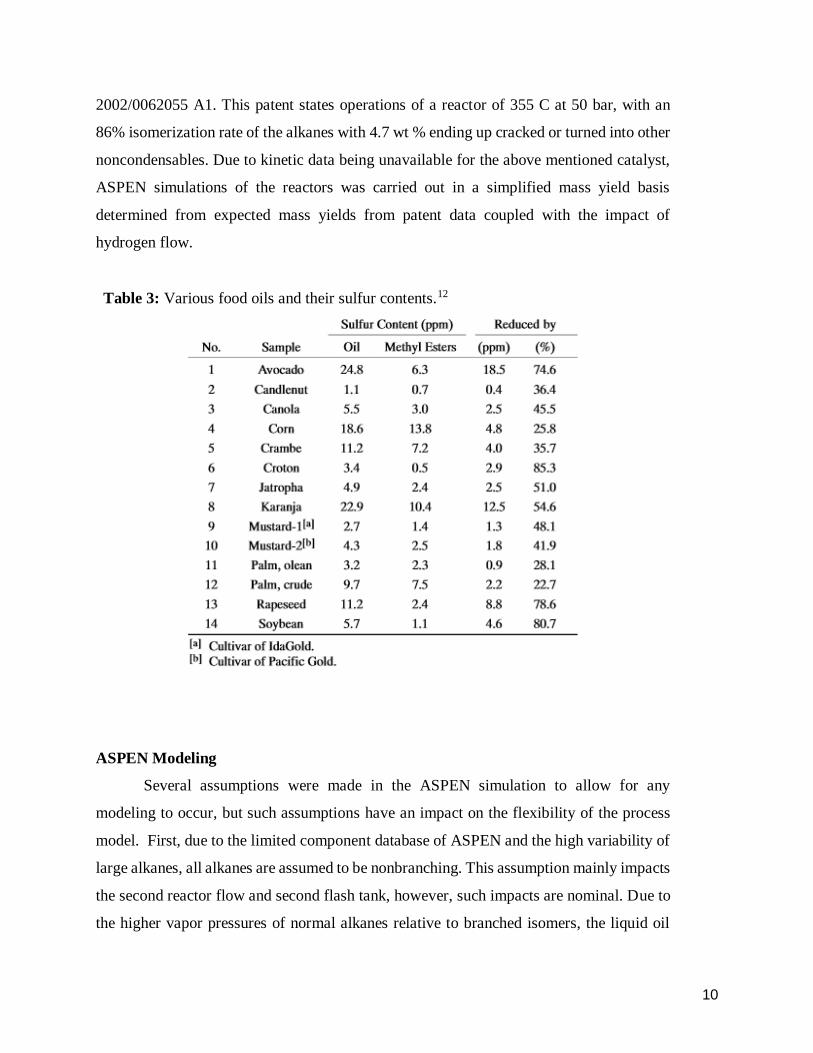

For consideration on catalyst, patent US 9,266,802 by Chevron U.S.A. Inc. example

4 of a NiMoW maleate catalyst has the most desirable conversion of soybean oil to diesel

with a 99.5% conversion having 54.2 wt% nC18, 19.2 wt% nC17, 6.6 wt% nC16, and 2.3

wt% nC15. In addition, the sulfur content of the catalyst is 8 ppmw. The low sulfur content

of the catalyst prevents most of the sulfur leaching that can occur in hydrocracking and

limits the need for the addition of a hydrotreater to remove excess sulfur to meet ASTM

diesel specifications. Table 3 also shows the naturally low sulfur content of soybean oil

emphasizing the impact of sulfur content of the catalyst on the process. Due to sulfur

allowance of 15 ppmw, the process at hand is unlikely to ever reach that limit. The patent

specifies reactor operation at 500 °F, 1000 psig (260 °C at 70 bar) and a LHSV of 1 h-1. It

has also been shown that the reaction does not suffer from any internal or external transport

effects. A second patent was used to specify isomerization of the normal alkanes, US

10

2002/0062055 A1. This patent states operations of a reactor of 355 C at 50 bar, with an

86% isomerization rate of the alkanes with 4.7 wt % ending up cracked or turned into other

noncondensables. Due to kinetic data being unavailable for the above mentioned catalyst,

ASPEN simulations of the reactors was carried out in a simplified mass yield basis

determined from expected mass yields from patent data coupled with the impact of

hydrogen flow.

Table 3: Various food oils and their sulfur contents.12

ASPEN Modeling

Several assumptions were made in the ASPEN simulation to allow for any

modeling to occur, but such assumptions have an impact on the flexibility of the process

model. First, due to the limited component database of ASPEN and the high variability of

large alkanes, all alkanes are assumed to be nonbranching. This assumption mainly impacts

the second reactor flow and second flash tank, however, such impacts are nominal. Due to

the higher vapor pressures of normal alkanes relative to branched isomers, the liquid oil

11

composition of the second flash tank will be underestimates. Another key assumption is in

the reactor design. Due to lack of kinetic data, mass yield based reactor simulation was

used, thereby limiting each simulation to a specific mass flow to ensure accurate outlet

compositions. To simulate varying flow rates of either H2 or oil would require a

readjustment of the mass balance and subsequent changes expected in mass yields. Due to

the high mass flow rate of the process, a change of 0.4 % on yield will have a great impact

on yields of oil or H2 recycle. Membrane separation was also simplified to component splits

in the outlet flows.

Due to the inflexibility of modeling in the reactors and membrane separation of H2,

focus was put towards the separation setup and optimization. Due to high boiling points of

the alkanes, single flashes are sufficient for separation of the otherwise volatile <C5

alkanes, CO, CO2, H2O, and H2 (hereby referred to as noncondensables). Due to high H2

flows required for both reactors, effective recycle of H2 from the noncondensables stream

was important. With the membrane separation being determined to be nearly 100%

selective to H2 and highly resistant to poisoning, a single separation unit would suffice for

both noncondensable streams. Outlet flow of H2 can then be split to flow to either reactor

2 or to the front of the process for feed into reactor 1.

Process simulation is adjustable only in flashing conditions. To study the effects on

inlet temperature and flashing pressure on liquid composition and recovery was carried out

with 20 case studies being carried out, 4 temperature conditions per 5 flashing pressures,

full description of case scenarios can be seen in the appendix. The composition profiles

showed that lower inlet temperatures had higher product recovery, but also had higher H2

composition. Flashing at lower pressures also had lower product recovery, but had less H2

losses. Due to the relatively low H2 loss in comparison to H2 recovery, it was opted for

lower temperatures in flash inlet with higher operating pressure of the first flash tank. The

first flash was determined to have an inlet stream at 70 °C and to operate at 65 bar as to

allow high enough process pressures to naturally flow to reactor 2 that operates at 50 bar.

The second flash was to have an inlet temperature of 30 °C for high product recovery and

manageable downstream handling, and an operating pressure of 25 bar. The lower

temperature of the second flash would minimize product loss that would occur at the

lowering flashing pressure. Product loss changed minimally on 5 bar increments of

12

operating pressures will H2 recovery changed significantly. This led to the second flash

tank to be designed with higher H2 recovery in mind.

Figure 3: ASPEN flowsheet of renewable diesel operations.

Due to the high flow rates of the H2 the oil was considered to be in the vapor phase

after the reactors in the ASPEN simulation, requiring the whole stream to be cooled to at

least temperatures below 110 C to condense the oils. Due to the large mass flow rate of H2

this is not an unreasonable outcome of the simulation, however the required heat

exchangers are large, as noted in the next section, and are the major capital cost of the

project. More intensive research or experimentation would be beneficial to confirm the

simulation and the need for the heat exchangers as large as the ones required for the

designed process.

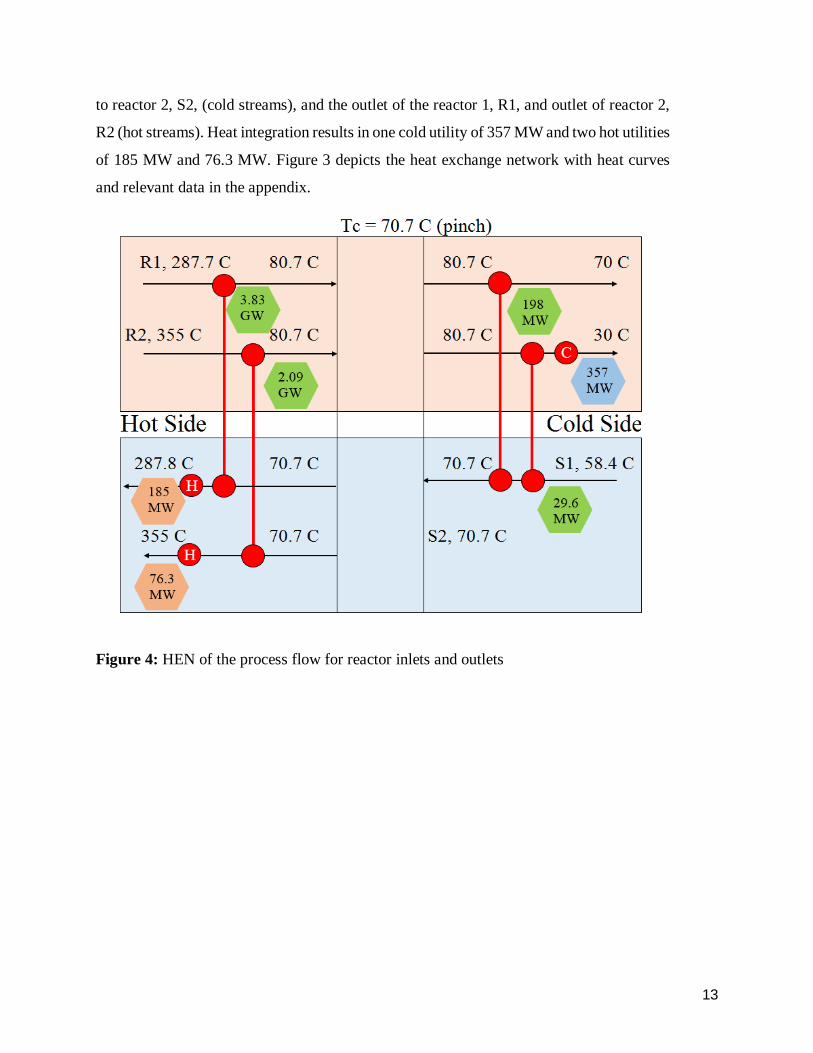

Heat Integration

With the process requiring high temperature swings on the flows for the flash tanks,

heat integration was imperative to reduce the roughly 14 gigawatt energy flow requirement.

ASPEN was used to find mass flow rates of the streams to be used and the average heat

capacity of the streams. The 4 streams to be considered are inlet to reactor 1, S1, and inlet

13

to reactor 2, S2, (cold streams), and the outlet of the reactor 1, R1, and outlet of reactor 2,

R2 (hot streams). Heat integration results in one cold utility of 357 MW and two hot utilities

of 185 MW and 76.3 MW. Figure 3 depicts the heat exchange network with heat curves

and relevant data in the appendix.

Figure 4: HEN of the process flow for reactor inlets and outlets

14

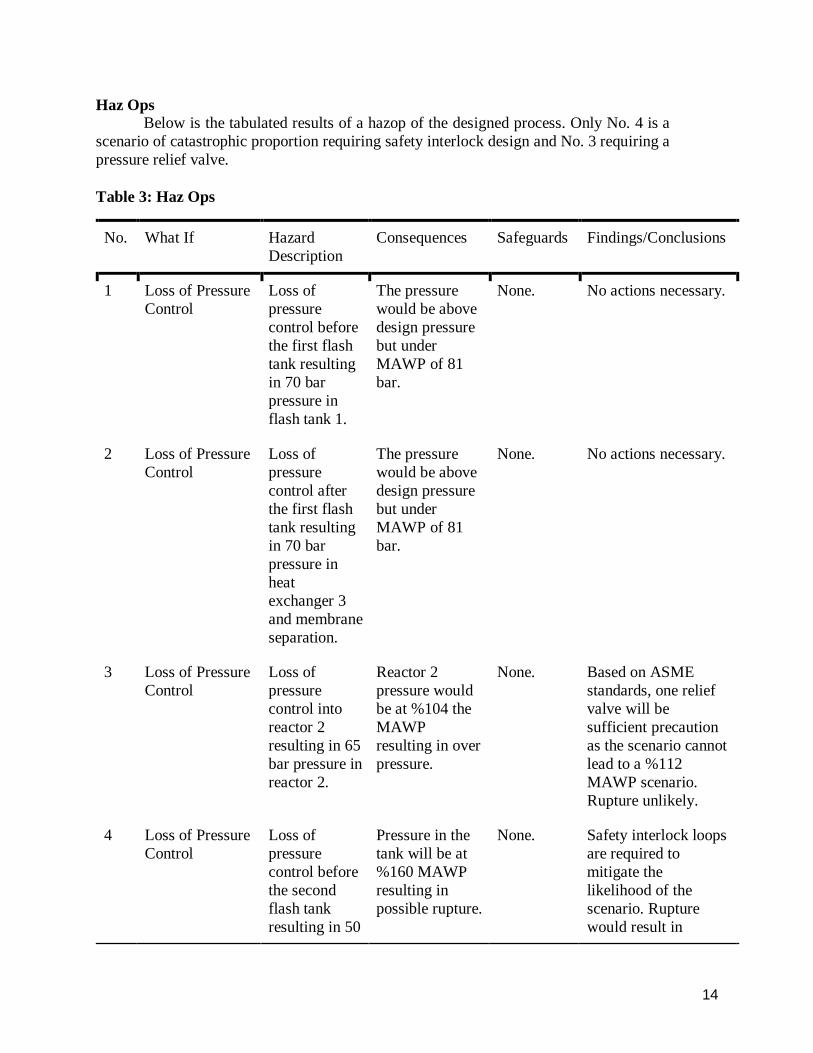

Haz Ops Below is the tabulated results of a hazop of the designed process. Only No. 4 is a

scenario of catastrophic proportion requiring safety interlock design and No. 3 requiring a

pressure relief valve.

Table 3: Haz Ops

No. What If Hazard

Description

Consequences Safeguards Findings/Conclusions

1 Loss of Pressure

Control

Loss of

pressure

control before

the first flash

tank resulting

in 70 bar

pressure in

flash tank 1.

The pressure

would be above

design pressure

but under

MAWP of 81

bar.

None. No actions necessary.

2 Loss of Pressure

Control

Loss of

pressure

control after

the first flash

tank resulting

in 70 bar

pressure in

heat

exchanger 3

and membrane

separation.

The pressure

would be above

design pressure

but under

MAWP of 81

bar.

None. No actions necessary.

3 Loss of Pressure

Control

Loss of

pressure

control into

reactor 2

resulting in 65

bar pressure in

reactor 2.

Reactor 2

pressure would

be at %104 the

MAWP

resulting in over

pressure.

None. Based on ASME

standards, one relief

valve will be

sufficient precaution

as the scenario cannot

lead to a %112

MAWP scenario.

Rupture unlikely.

4 Loss of Pressure

Control

Loss of

pressure

control before

the second

flash tank

resulting in 50

Pressure in the

tank will be at

%160 MAWP

resulting in

possible rupture.

None. Safety interlock loops

are required to

mitigate the

likelihood of the

scenario. Rupture

would result in

15

bar pressure in

the flash tank.

catastrophic spillage

and fire hazard.

5 Loss of Cooling Heat

exchanger 2

fails resulting

in high

temperature

on flash tank 1

inlet.

Higher than

anticipated

vapor flow

would occur,

but impact

minimal due to

already high

hydrogen flows.

None. No actions necessary.

6 Loss of Cooling Heat

exchanger 4

fails resulting

in high

temperature

on flash tank 2

inlet.

See No. 5. See No. 5. See No. 5.

7 Loss of Heating Heat exchange

1 fails

resulting in

low feed

temperature

into reactor 1.

Reaction in

reactor 1 would

most likely be

quenched

thereby having

triglycerides in

product stream.

None. Operability issues, no

actions required.

8 Loss of Heating Heat

exchanger 3

fails resulting

in low feed

temperature

into reactor 2.

Reaction in

reactor 2 would

most likely be

quenched

thereby

reducing

isomerization

rate.

None. Operability issues, no

actions required.

9 Hydrogen Split

Fails

Stream split of

hydrogen in

not having

proper flows

to target units.

Either reactor 1

or reactor 2

could have

reactions

proceed less

than expected.

Reaction cannot

proceed further

due to near

None. Operability issues, no

actions required.

16

completion in

reactors.

10 Loss of Feed Oil feed is

reduced or

stopped.

Reactor feed

temperature

may rise too

high resulting in

high pressure.

None. Unlikely due to high

mass composition of

hydrogen to reactor.

No actions necessary.

11 Loss of Feed Hydrogen

feed is

reduced or

stopped.

Hydrogen is

eventually

consumed in the

process.

None. Due to high process

flows, time to

consume all hydrogen

is long enough for

operators to react to

scenario. No actions

necessary.

12 High Feed Rate Oil feed is

higher than

expected.

Reactions may

not occur to

completion due

to increased

flow rate of oil.

None. Operability issues, no

actions required.

13 High Feed Rate Hydrogen

feed is higher

than expected.

Due to low feed

rate relative to

process flow,

impact likely to

be insignificant.

None. No actions necessary.

Market Analysis

Initially, our choice of feedstock was between soybean oil, cottonseed oil,

sunflower seed oil, and corn oil based on their production volumes in the United States. In

order to not pressure any of the crop markets, while still meeting our annual feedstock

demand of 600 MTonnes, it became clear that we would have to seek additional markets

internationally. What follows is an analysis of the market trends for these four oils in the

United States, Brazil, and Argentina. Brazil and Argentina were selected because of their

1) annual production volumes of the aforementioned oils, and 2) geographical proximity

to the United States.

17

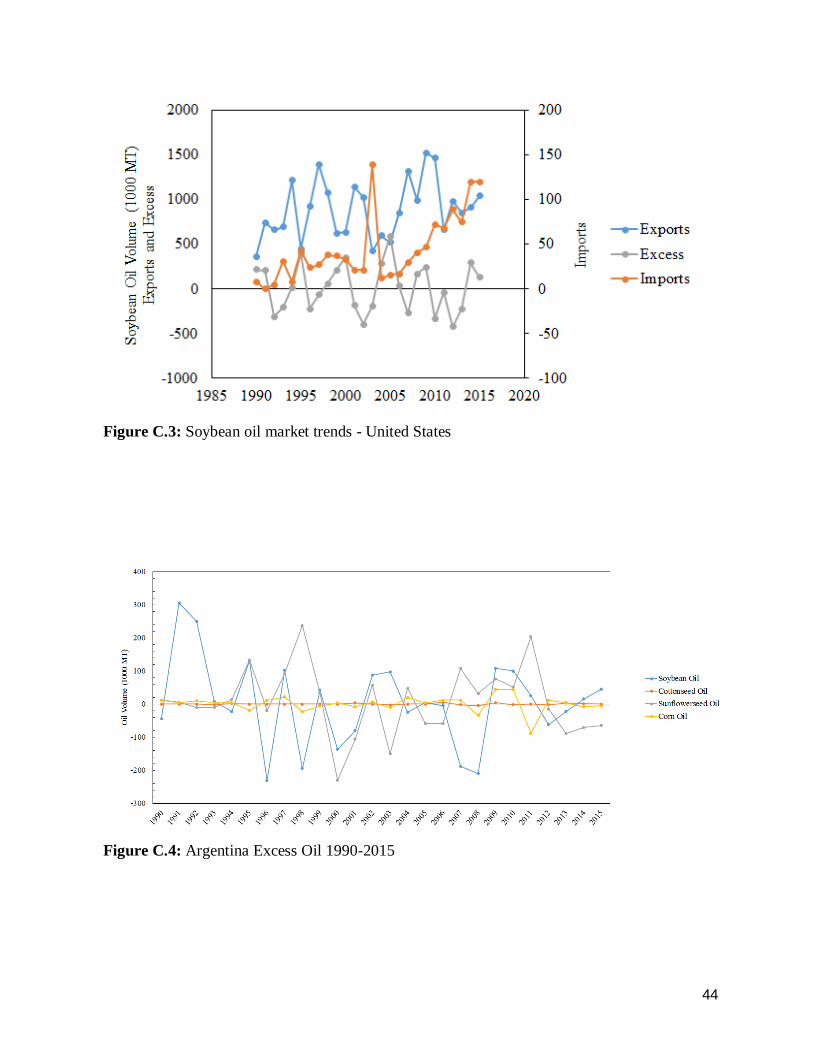

In general the United States appears to have much more soybean oil in excess

annually than the other potential feedstock. The United States soybean oil excess has the

general cyclic trend with large swings in the stocks of soybean oil. While the general trend

of soybean oil production increases overtime (figure C.8) increases over time, there are

years with less than expected production volume (i.e. 2003, 2008, 2010). For example,

2008 and 2010 were years of recession in the U.S. These three years indicated in the chart

above generally correspond with periods of negative excess oil. The trend of domestic

soybean production is also expressed in Table C.1.

Figure 5: United States excess oil 1990-2015

One thought for this deviation was believed to be drought. If not enough soybean

crop for example is produced, than the excess would not be expected to be as high.

According to Figure C.2, there appears to be a correlation between United States drought

patterns and annual volume of soybean oil produced.

Another correlation is discovered when comparing the annual soybean oil exports

to the annual excess. In general, when the United States exports more oil, there is less in

excess and vice versa (see Figure C.3). Argentina typically has soybean and sunflower seed

oil in excess as shown in Figure C.4. Based on the annual production trends (Figure C.5),

there have been variations in the anticipated trend in the years 2008 and 2012. This

generally corresponds to decreased amounts of soybean oil in excess. For the Argentine

18

markets, the export and import trends of soybean oil appear to be less sensitive to the annual

excess (Figure C.6).

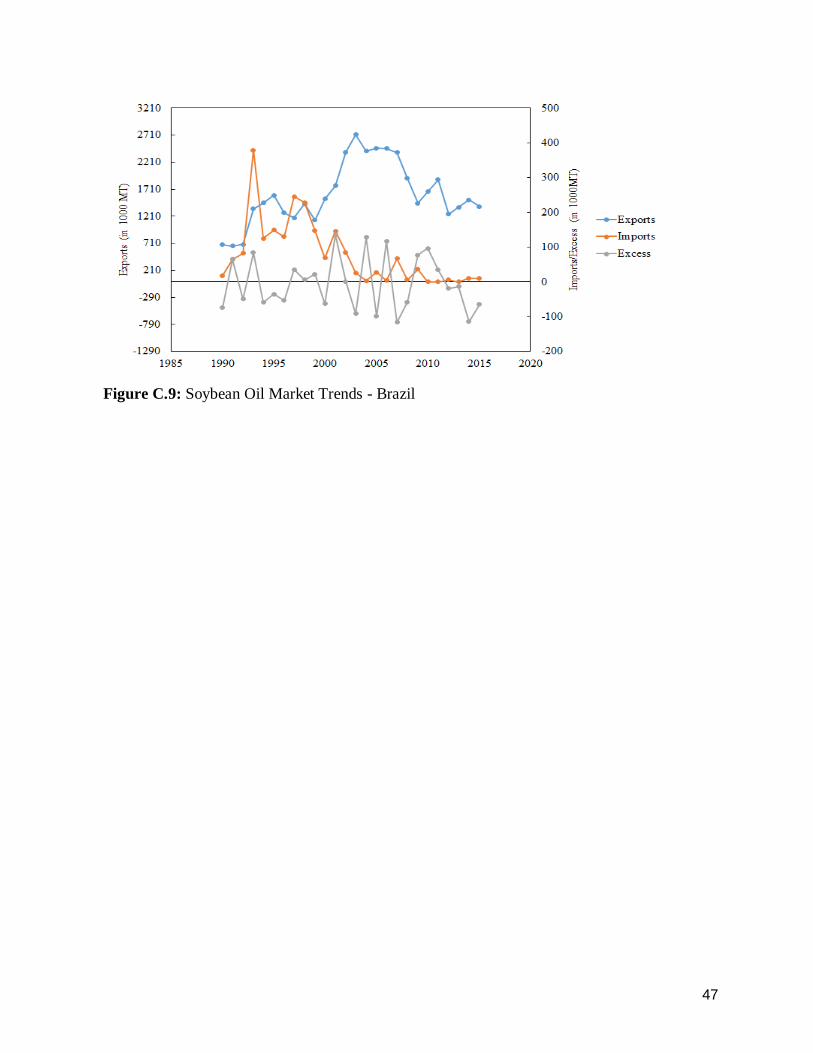

Finally, the excess of soybean and corn oil seem to be the most volatile depending

on the year in the Brazil (Figure C.7). Based on the annual production trends, there has

recently been variations in the anticipated trend in the years 2005 and 2012 (Figure C.8).

This generally corresponds to decreased amounts of soybean oil in excess. For the Brazilian

markets, the export and import trends of soybean oil appear to be less sensitive to the annual

excess (Figure C.9).

Our group made the decision to get our soybean oil from both the United States and

South America. The reason for doing so was to avoid pressuring one market too much. The

excess soybean oil stock for the top 3 producers of soybean oil (the United States,

Argentina, and Brazil) is shown in the figure below, from 1990-2015.

Figure 6: Total excess oil stocks between US, Brazil and Argentina.

It appears as though the global soybean oil excess has periods of increase and decrease, for

3-4 years at a time. At the moment, it appears that all three markets have a net positive

amount of soybean oil at the end of year. Because our plant will not be built immediately,

19

we also wanted to consider what the average excess for these three countries has looked

like for the past 15 years.

Figure 7: Soybean oil production

While all three countries under investigation have a positive trend over time,

Brazil’s exports have been decreasing in the past few years, which is the category our

feedstock would come from. For the purposes of our project moving forward, we will only

consider the United States and Argentinean markets. They hold the most promise for

increased production capacity, excess supply, and export capacity of soybean oil moving

forward. Because of this, we do not believe that we will be pressuring either market in a

significant manner. We will assume that 50% of our soybean oil feedstock will come from

the United States and 50% will come from Argentina.

Government Policies

Two policy issues will have a large part in whether the renewable diesel process

can be profitable. The current tax credit in the US is $1.00/gallon is from bill H.R. 2029

which expires December 31, 2016.3 As will be shown in the next section this bill is critical

for building the renewable diesel industry. If the bill is not renewed it is unlikely that the

renewable diesel industry will be able to continue in the United States

The other policy that can also help develop the renewable diesel industry is the

implementation of a carbon tax. One of the main reasons to look towards renewable diesel

facilities is because substantially less CO2 emissions compared to conventional plants. A

20

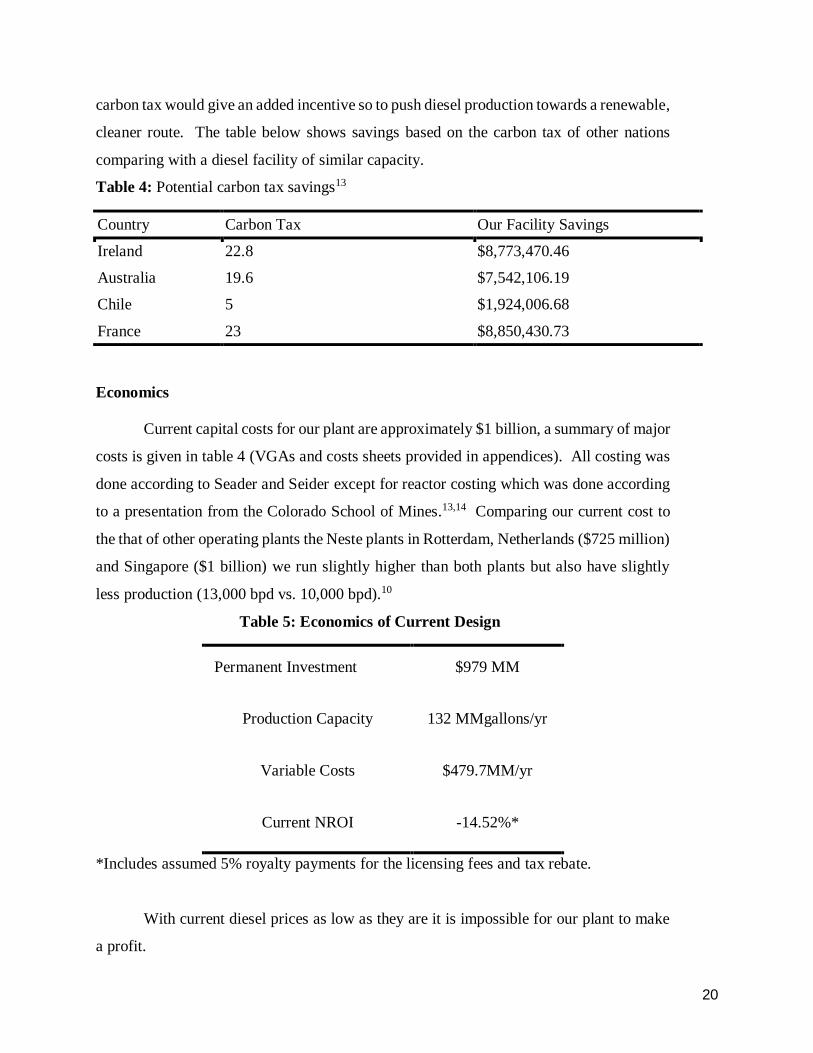

carbon tax would give an added incentive so to push diesel production towards a renewable,

cleaner route. The table below shows savings based on the carbon tax of other nations

comparing with a diesel facility of similar capacity.

Table 4: Potential carbon tax savings13

Country Carbon Tax Our Facility Savings

Ireland 22.8 $8,773,470.46

Australia 19.6 $7,542,106.19

Chile 5 $1,924,006.68

France 23 $8,850,430.73

Economics

Current capital costs for our plant are approximately $1 billion, a summary of major

costs is given in table 4 (VGAs and costs sheets provided in appendices). All costing was

done according to Seader and Seider except for reactor costing which was done according

to a presentation from the Colorado School of Mines.13,14 Comparing our current cost to

the that of other operating plants the Neste plants in Rotterdam, Netherlands ($725 million)

and Singapore ($1 billion) we run slightly higher than both plants but also have slightly

less production (13,000 bpd vs. 10,000 bpd).10

Table 5: Economics of Current Design

Permanent Investment $979 MM

Production Capacity 132 MMgallons/yr

Variable Costs $479.7MM/yr

Current NROI -14.52%*

*Includes assumed 5% royalty payments for the licensing fees and tax rebate.

With current diesel prices as low as they are it is impossible for our plant to make

a profit.

21

The purchase cost of hydrogen and soybean oil outweighs the value of the diesel fuel

making it impossible for any plant working on soybean oil to be profitable at the current

prices. As can be seen from figure 2 it would take an increase in diesel price to

$4.20/gallon before an NROI of 0% is achieved. In the last ten years the max price of

diesel was $4.72/gallon in July 2008 at this price of diesel our project plant would still only

have an NROI of 3.78% making it barely profitable.15 Figure 17 also shows demonstrates

the importance of the government subsidy. Without the subsidy it would be near

impossible to make a profit unless soybean oil and capital costs dropped dramatically.

Figure 8: Effect of price of Diesel on NROI

In order to determine if this business could be profitable at all we calculated the

NROI of the DGD based on their capital cost of $330 million, their output of 134 million

gallons a year, and our utility costs as a close approximation. In the early part of the decade

when many of the renewable diesel facilities were being built diesel averaged around

$4/gallon while soybean prices were also higher at approximately $0.85/kg. However it

appears the DGD facility was able to achieve an NROI of approximately 13%.

-20.00%

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

2 2.5 3 3.5 4 4.5

NR

OI

Price of Diesel ($/gallon)

NROI

NROI noroyaltiesNROI norebate

22

Figure 9: Diesel prices since 1994

Estimating the profitability of the other plants in the Netherlands and Singapore is

more difficult due to other government policies on the taxing of fossil fuels and rebates

being unclear however diesel prices are significantly higher (2.96 USD/gallon in

Singapore, 5.10 USD/gallon in the Netherlands) which could easily lead to a large profit

margin as palm oil and soybean oil have similar prices to soybean oil in the US.16,17

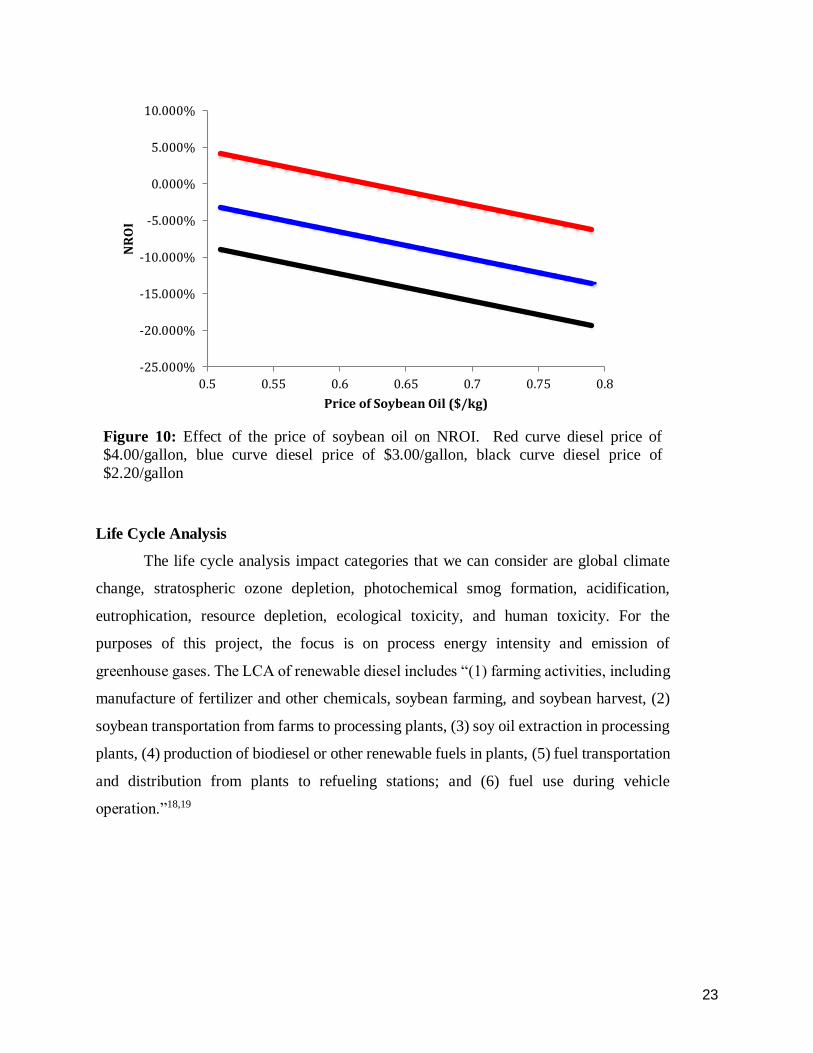

Although the soybean oil price has steadily decreased over the last three years there

has still be a large degree of variability over the last ten years that makes it difficult to tell

the direction of the soybean market. The price of soybean has been shown to shift enough

to dramatically shift the profitability of the plant. Figure 19 shows how the price of

soybean oil can affect the NROI of our projected plant. However although about $0.51/kg

of soybean oil has been the lowest observed for soybean oil the highest price seen over the

past 10 years has been $1.17/kg which would be catastrophic to the industry.9

23

Figure 10: Effect of the price of soybean oil on NROI. Red curve diesel price of $4.00/gallon, blue curve diesel price of $3.00/gallon, black curve diesel price of

$2.20/gallon

Life Cycle Analysis

The life cycle analysis impact categories that we can consider are global climate

change, stratospheric ozone depletion, photochemical smog formation, acidification,

eutrophication, resource depletion, ecological toxicity, and human toxicity. For the

purposes of this project, the focus is on process energy intensity and emission of

greenhouse gases. The LCA of renewable diesel includes “(1) farming activities, including

manufacture of fertilizer and other chemicals, soybean farming, and soybean harvest, (2)

soybean transportation from farms to processing plants, (3) soy oil extraction in processing

plants, (4) production of biodiesel or other renewable fuels in plants, (5) fuel transportation

and distribution from plants to refueling stations; and (6) fuel use during vehicle

operation.”18,19

-25.000%

-20.000%

-15.000%

-10.000%

-5.000%

0.000%

5.000%

10.000%

0.5 0.55 0.6 0.65 0.7 0.75 0.8

NR

OI

Price of Soybean Oil ($/kg)

24

Figure 11: Fuel Production Processes for the four soybean derived fuels18

The GREET (Greenhouse gases, Regulated Emissions, and Energy Use in Transportation)

model is used in our life cycle analysis, as we consider this process from well to wheel (see

Figure below).

Figure 12: GREET well-to-pump and pump-to wheel stages18

A majority (about ~65%) of the energy intensity in the lifecycle of renewable diesel comes

from the agricultural soybean production, soybean transportation, and soybean crushing.

25

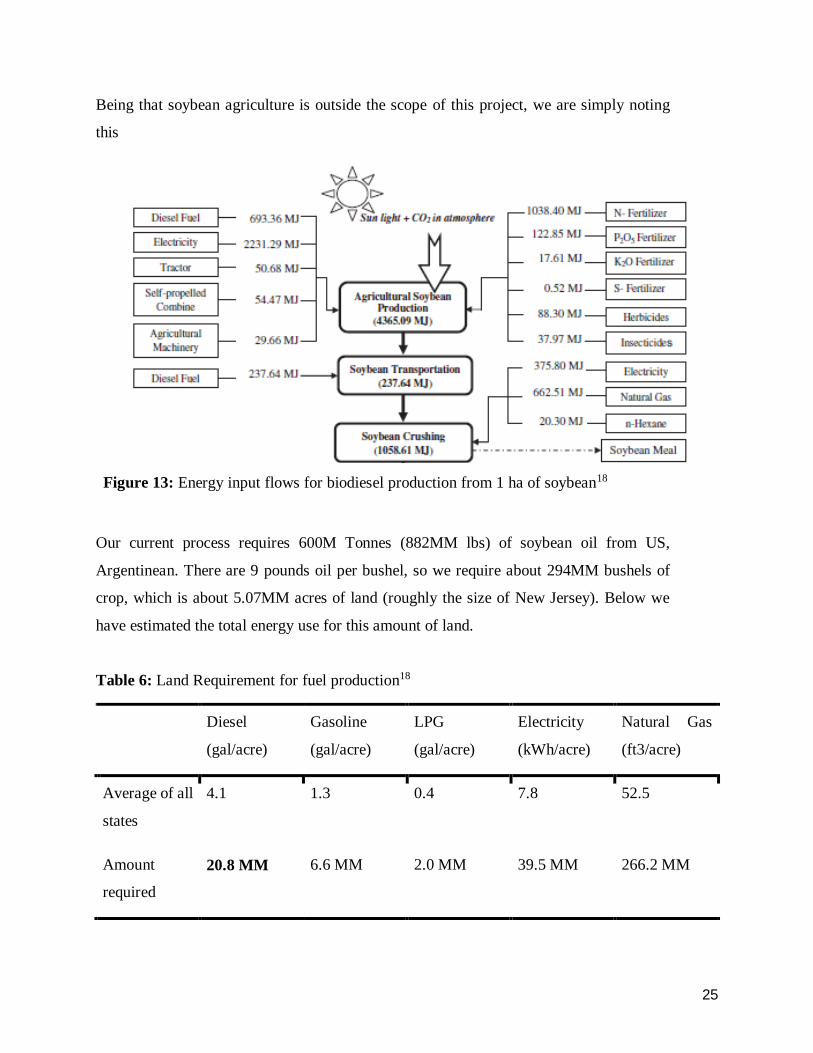

Being that soybean agriculture is outside the scope of this project, we are simply noting

this

Figure 13: Energy input flows for biodiesel production from 1 ha of soybean18

Our current process requires 600M Tonnes (882MM lbs) of soybean oil from US,

Argentinean. There are 9 pounds oil per bushel, so we require about 294MM bushels of

crop, which is about 5.07MM acres of land (roughly the size of New Jersey). Below we

have estimated the total energy use for this amount of land.

Table 6: Land Requirement for fuel production18

Diesel

(gal/acre)

Gasoline

(gal/acre)

LPG

(gal/acre)

Electricity

(kWh/acre)

Natural Gas

(ft3/acre)

Average of all

states

4.1 1.3 0.4 7.8 52.5

Amount

required

20.8 MM 6.6 MM 2.0 MM 39.5 MM 266.2 MM

26

Our preliminary process produces 131 MM gallons of green diesel annually. To be a more

sustainable venture, we propose using our renewable diesel to power the machinery and

equipment used the harvest the soybean crop.

Table 7: Energy Use for Soybean Farming in the United States (USDA 2007b)18

Based on our desired annual production rate of renewable diesel (1.323 MM tons),

the required input of hydrogen to the process is approximately 10.6MM lbs. Using the one-

to-one hydrogen-carbon dioxide ratio in the hydrogen production process via reforming,

this equates to an annual carbon footprint of 234MM lbs CO2. It was assumed from the

table below that 0.49mmBtu hydrogen was required per ton of soybean.18

27

Table 8: Energy Use and Amount of Fuel Prodcut and Co-Products from One Ton of Soybeans18

The group also wanted to check that shipping half of our feedstock from a foreign market

would not have a negative impact on the life cycle analysis, specifically in regards to the

greenhouse gas emissions. The figure below shows the Well-to-Wheel GHG Emissions if

we get 50% of our feedstock from international soybean oil production plants. We will

assume for now that our plant will be built in Virginia. This is for several reasons: (1)

Virginia is on the coast, so rail costs will be low, (2) there is already a significant amount

of soybean grown in the state, and (3) the Port of Norfolk is a major shipping port on the

East Coast. The largest port in Argentina is in Buenos Aires, so we determined the optimal

route to be 6169 nautical miles (~11,000km). Based on this distance, a large container

vessel (carrying 20,000 tonnes on general) would need to make roughly 15 trips during the

year. A vessel this size burns 11.5 g CO2/tonne-km.

28

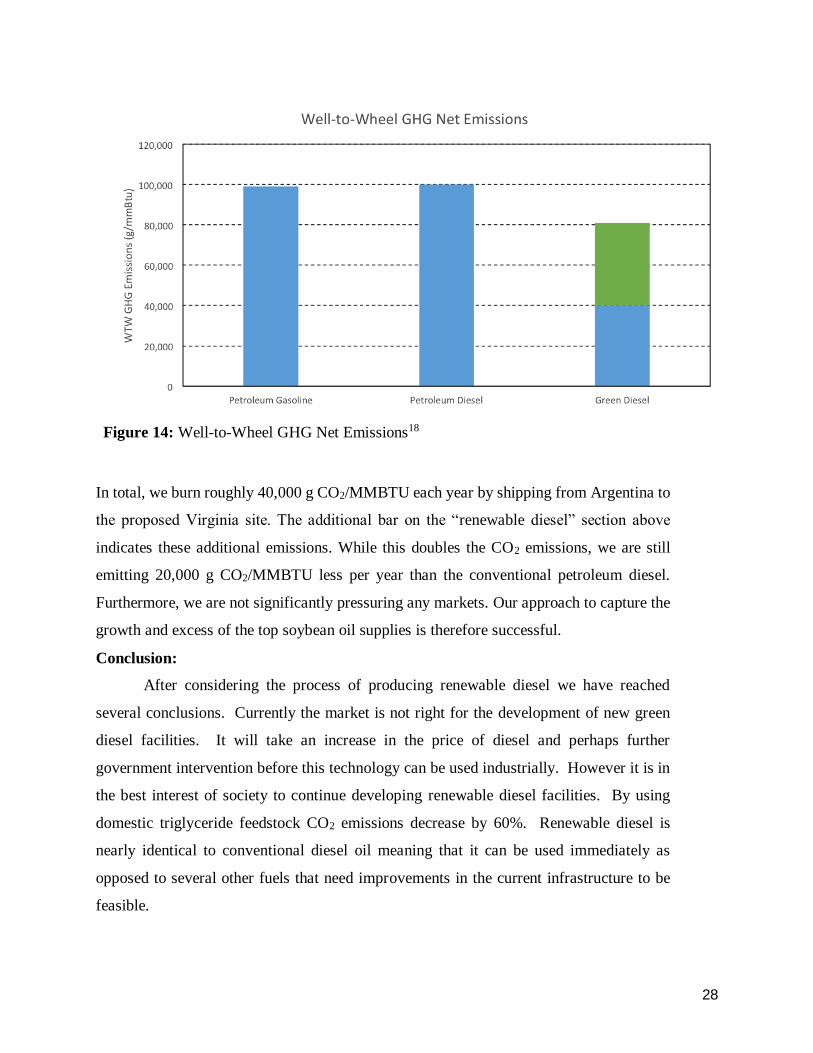

Figure 14: Well-to-Wheel GHG Net Emissions18

In total, we burn roughly 40,000 g CO2/MMBTU each year by shipping from Argentina to

the proposed Virginia site. The additional bar on the “renewable diesel” section above

indicates these additional emissions. While this doubles the CO2 emissions, we are still

emitting 20,000 g CO2/MMBTU less per year than the conventional petroleum diesel.

Furthermore, we are not significantly pressuring any markets. Our approach to capture the

growth and excess of the top soybean oil supplies is therefore successful.

Conclusion:

After considering the process of producing renewable diesel we have reached

several conclusions. Currently the market is not right for the development of new green

diesel facilities. It will take an increase in the price of diesel and perhaps further

government intervention before this technology can be used industrially. However it is in

the best interest of society to continue developing renewable diesel facilities. By using

domestic triglyceride feedstock CO2 emissions decrease by 60%. Renewable diesel is

nearly identical to conventional diesel oil meaning that it can be used immediately as

opposed to several other fuels that need improvements in the current infrastructure to be

feasible.

29

Works Cited: 1. (Patent US 9,266,802)

2. (Patent US 2002/0062055 A1).

3. Tax Credit

4. Alonso, D. M., Bond, J. Q. & Dumesic, J. A. Catalytic conversion of biomass to biofuels. 1493–1513 (2010). doi:10.1039/c004654j

5. Ki, S. et al. Production of renewable diesel via catalytic deoxygenation of natural triglycerides :

Comprehensive understanding of reaction intermediates and hydrocarbons. Appl. Energy 116, 199–205

(2014).

6. Sinha, A. K. et al. Development of Hydroprocessing Route to Transportation Fuels from Non-Edible Plant-

Oils. 1–13 (2013). doi:10.1007/s10563-012-9148-x

7. Srivastava, A. & Prasad, R. Triglycerides-based diesel fuels. 4, (2000).

8. PIRA Energy Group. An Assessment of the Diesel Fuel Market: Demand, Supply, Trade, and Key Drivers.

Fuels Institute. 2014.

9. USDA. Oilseeds: World Markets and Trade. Oil Crops Yearbooks Economic Research Service. March 2014.

10. Eco Resources Consultants Study of Hydrogenation Derived Renewable Diesel as a Renewable Fuel Option

in North America: Final Report March 2012.

11. Oyama et al., Highly hydrogen selective ceramic membranes: application to the transformation of greenhouse

gases. J. Mem. Sci. 176, 233-248 (2000)

12. Zarchin, R. et. al. Hydroprocessing of soybean oil on nickel-phosphide supported catalysts. Fuel. 2014.

13. http://www.carbontax.org/where-carbon-is-taxed/

14. Seider, W. D., Seader, J. D., Lewin, D. R., Widagdo S., Product and Process Design Principles: Synthesis,

Analysis and Design, 3rd Ed. Wiley 2009

15. http://inside.mines.edu/~jjechura/Refining/08_Hydroprocessing.pdf

16. http://www.eia.gov/dnav/pet/hist/LeafHandler.ashx?n=PET&s=EMD_EPD2D_PTE_NUS_DPG&f=W

17. https://www.spc.com.sg/our-business/spc-service-station/latest-pump-price

18. Huo, H., M. Wang, C. Bloyd, and V. Putsche. Life-Cycle Assessment of Energy and Greenhouse Gas Effects

of Soybean-Derived Biodiesel and Renewable Fuels. Rep. Chicago: Argonne National Laboratory, 2008. Print.

19. Giroux, Robert "CHEG625 Class 15." 4 April 2016. Lecture

30

Appendix A: Economics

Figure A. 1: VGA

31

Figure A. 2: Cost Sheet

32

Appendix B: Aspen Data

ASPEN Tables:

Table B.1: Cases for Flash 1

Row/

Case

VARY 1 VARY 2

VARY

3

C18

LOSS

C17

LOSS

C16

LOSS

C15

LOSS H2 in Product

Reactor 1 H2

Feed

Reactor 2

Out

FLAS

H1

TEMP TEMP PRES TONNE/OPER-YEAR

C C BAR

CUM/OPER-

YEAR

1 100 100 65 1085 1284 604 676 8009

2 90 90 65 540 664 327 382 7755

3 80 80 65 256 328 170 206 7499

4 70 70 65 116 154 84 106 7246

5 100 100 60 1163 1377 647 724 7403

6 90 90 60 577 711 350 409 7170

7 80 80 60 273 350 182 221 6934

8 70 70 60 123 164 90 113 6701

9 100 100 55 1254 1486 698 780 6795

10 90 90 55 622 766 378 440 6583

11 80 80 55 294 377 195 237 6367

12 70 70 55 132 176 96 122 6153

13 100 100 50 1364 1616 759 847 6184

14 90 90 50 675 832 410 478 5993

15 80 80 50 318 408 212 257 5798

16 70 70 50 142 191 104 132 5604

17 100 100 45 1499 1776 833 929 5571

18 90 90 45 740 912 450 524 5402

19 80 80 45 348 447 232 282 5227

20 70 70 45 155 208 114 144 5052

33

Table B.2: Cases for Table 2

Row/

Case

VARY

1 VARY 2 VARY 3

VARY

4

C18

LOSS

C17

LOSS

C16

LOSS

C15

LOSS H2 In Product

Reactor

2 H2

Feed

Reactor 1

Contamin

-ants

Reactor 2

Outlet

FLAS

H2

TEMP TEMP TEMP PRES TONNE/OPER-YEAR

C C C BAR

CUM/OPER-

YEAR

1 60 60 60 45 303 415 208 237 4672

2 50 50 50 45 122 175 93 111 4518

3 40 40 40 45 46 69 39 49 4367

4 30 30 30 45 16 25 15 20 4220

5 60 60 60 40 334 459 230 262 4160

6 50 50 50 40 134 193 102 123 4024

7 40 40 40 40 50 76 43 54 3889

8 30 30 30 40 17 28 17 22 3759

9 60 60 60 35 375 514 258 294 3646

10 50 50 50 35 149 215 115 137 3527

11 40 40 40 35 56 84 48 60 3410

12 30 30 30 35 19 31 19 25 3296

13 60 60 60 30 428 589 295 336 3130

14 50 50 50 30 170 246 131 157 3029

15 40 40 40 30 63 96 54 69 2928

16 30 30 30 30 22 35 21 28 2830

17 60 60 60 25 504 693 347 395 2612

18 50 50 50 25 199 288 154 184 2528

19 40 40 40 25 74 112 64 81 2445

20 30 30 30 25 25 41 25 33 2363

34

Table B.3: Aspen Block Summary

35

36

37

38

39

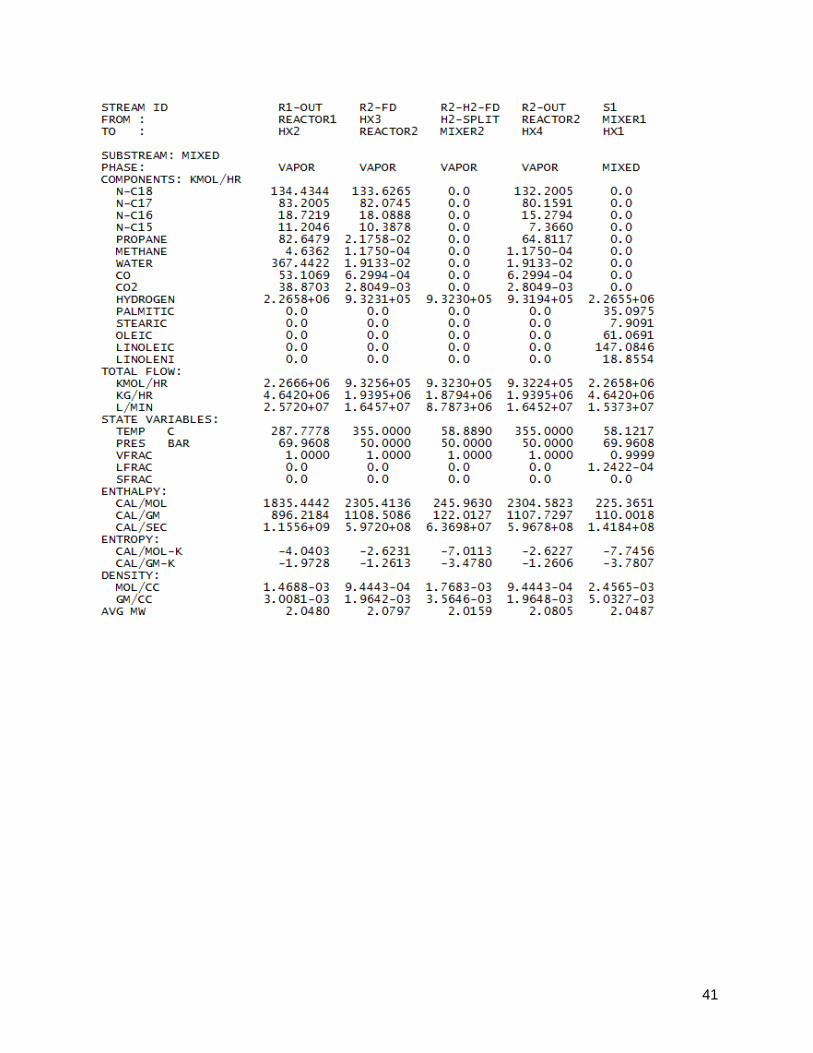

Table B.4: Aspen Stream Tables

40

41

42

43

Appendix C: Market Analysis

Figure C.1: Soybean oil production in the United States

Figure C.2: Average drought conditions in the contiguous 48 states 1895-2011

44

Figure C.3: Soybean oil market trends - United States

Figure C.4: Argentina Excess Oil 1990-2015

45

Figure C.5: Soybean Oil Production - Argentina

Figure C.6: Soybean Oil market Trends - Argentina

46

Figure C.7: Brazil Excess Oil 1990-2015

Figure C.8: Soybean Oil Production - Brazil

47

Figure C.9: Soybean Oil Market Trends - Brazil

48

Appendix D: ASTM Diesel Standards

Table D.1: ASTM Diesel Standards