embedded value miroslav petkov director standard&poor’s

DESCRIPTION

Embedded Value Miroslav Petkov Director Standard&Poor’s. Embedded Value Setting the Scene. Origins of Embedded Value. Developed as a concept in the UK in 1980’s Origins in valuing life companies (appraisal values) Introduced widely in the equity markets in 1990’s - PowerPoint PPT PresentationTRANSCRIPT

CONFIDENTIAL AND PROPRIETARY.

Permission to reprint or distribute any content from this presentation requires the written approval of Standard & Poor’s.

Copyright (c) 2006 Standard & Poor’s, a subsidiary of The McGraw-Hill Companies, Inc. All rights reserved.

Embedded Value

Miroslav PetkovDirectorStandard&Poor’s

CONFIDENTIAL AND PROPRIETARY.

Permission to reprint or distribute any content from this presentation requires the written approval of Standard & Poor’s.

Copyright (c) 2006 Standard & Poor’s, a subsidiary of The McGraw-Hill Companies, Inc. All rights reserved.

Embedded Value Setting the Scene

3.

CONFIDENTIAL AND PROPRIETARY.

Permission to reprint or distribute any content from this presentation requires the written approval of Standard & Poor’s.August 2005

Developed as a concept in the UK in 1980’s

Origins in valuing life companies (appraisal values)

Introduced widely in the equity markets in 1990’s

Embedded Value is gaining global acceptance e.g.

Europe, Australia, Canada, South Africa

US companies stand out as the exception

Embedded Value initially drove a re-rating in the UK sector

Flaws in methodology have seen price/EV’s collapse

Origins of Embedded Value

4.

CONFIDENTIAL AND PROPRIETARY.

Permission to reprint or distribute any content from this presentation requires the written approval of Standard & Poor’s.August 2005

In the UK, achieved profit (EV) guidance notes first issued in July 1995

Appraisal values rose as embedded value methodology gained wide acceptance

Appraisal Value = Embedded Value + Goodwill

Association of British Insurers issued guidance notes on EV reporting in 2001 to improve consistency in reporting

From 2002, all companies use active economic assumptions (investment returns and discount rates)

Development in the UK

5.

CONFIDENTIAL AND PROPRIETARY.

Permission to reprint or distribute any content from this presentation requires the written approval of Standard & Poor’s.August 2005

0

0.5

1

1.5

2

2.5

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Pri

ce /

EV

UK Life Sector

Emergence of

E.V. Reporting

6.

CONFIDENTIAL AND PROPRIETARY.

Permission to reprint or distribute any content from this presentation requires the written approval of Standard & Poor’s.August 2005

Myriad of local statutory solvency accounting bases around Europe

Continental Europe were slower to embrace EV, but implemented following pressure from investment community

Companies were already using EV internally for many years as a product-pricing tool.

Unlike UK, European companies often saw share price fall as disclosure coincided with de-rating of the insurance sector.

EEV Principles were introduced in 2004 by the CFO Forum

Development in Continental Europe

7.

CONFIDENTIAL AND PROPRIETARY.

Permission to reprint or distribute any content from this presentation requires the written approval of Standard & Poor’s.August 2005

US companies have stuck with US GAAP

Signs this may be changing

Many large US life companies have European parents eg.

AEGON, AXA, ING & Prudential

These US subsidiaries report embedded values

US life businesses viewed as under-valued in some quarters

Perceived valuation arbitrage may encourage US life companies down EV route

Development in the US ?

8.

CONFIDENTIAL AND PROPRIETARY.

Permission to reprint or distribute any content from this presentation requires the written approval of Standard & Poor’s.August 2005

Overview of Embedded Value

9.

CONFIDENTIAL AND PROPRIETARY.

Permission to reprint or distribute any content from this presentation requires the written approval of Standard & Poor’s.August 2005

Value of a Life Company In most sectors, a companies value is equal to net assets

Net Asset Value (NAV) = Assets minus Liabilities

Life insurance is different

By design contracts are written for the long-term

Additional value is taken for “guaranteed” future income

Many (traditional) life insurance contracts have exit penalties

Consequently, they tend to be maintained for long periods of time

Expected profits from life insurance contracts are referred to as value in force (VIF)

VIF = NPV of future profits from contracts already written (sold)

The actual value and intangible value are jointly referred to as Embedded Value (EV)

EV = NAV + VIF

10.

CONFIDENTIAL AND PROPRIETARY.

Permission to reprint or distribute any content from this presentation requires the written approval of Standard & Poor’s.August 2005

Traditional accounting regimes provide a lagging indicator of current performance

Balance sheets give limited view on value ‘locked-in’ within life business

P&L reflect historic management performance/actions

Current actions will only emerge through earnings over time

Consequently, the traditional accounting methods provide little perspective on management efficacy

Traditional Accounting Methods

11.

CONFIDENTIAL AND PROPRIETARY.

Permission to reprint or distribute any content from this presentation requires the written approval of Standard & Poor’s.August 2005

Traditional Accounting Methods

Economic Value

Cash Profit

Statutory

GAAP

EV

Level of Conservatism

12.

CONFIDENTIAL AND PROPRIETARY.

Permission to reprint or distribute any content from this presentation requires the written approval of Standard & Poor’s.August 2005

-140

-120

-100

-80

-60

-40

-20

0

20

40

60

80

100

120

0 1 2 3 4 5 6 7 8 9 10

Regulatory GAAP EV

-

Profit Emergence – Take your pick !!

13.

CONFIDENTIAL AND PROPRIETARY.

Permission to reprint or distribute any content from this presentation requires the written approval of Standard & Poor’s.August 2005

All the reporting basis give the same total profits,

timing being the only difference

“In the end we’re all dead…….”

CONFIDENTIAL AND PROPRIETARY.

Permission to reprint or distribute any content from this presentation requires the written approval of Standard & Poor’s.

Copyright (c) 2006 Standard & Poor’s, a subsidiary of The McGraw-Hill Companies, Inc. All rights reserved.

Embedded ValueThe Weaknesses

15.

CONFIDENTIAL AND PROPRIETARY.

Permission to reprint or distribute any content from this presentation requires the written approval of Standard & Poor’s.August 2005

Embedded Value – The Weaknesses

Four areas analysts should be aware of :

Cash

Risk

Consistency

Subjectivity

16.

CONFIDENTIAL AND PROPRIETARY.

Permission to reprint or distribute any content from this presentation requires the written approval of Standard & Poor’s.August 2005

Traditional EV failed to flag impact from falling markets to asset liability mismatch and costly options and guarantees

Therefore, for full perspective of a company need to consider :

Embedded value – for value creation

Statutory earnings – for cash potential

Capital model – for assessment of capital generation and needs

Not all about Embedded Value !!

CONFIDENTIAL AND PROPRIETARY.

Permission to reprint or distribute any content from this presentation requires the written approval of Standard & Poor’s.

Copyright (c) 2006 Standard & Poor’s, a subsidiary of The McGraw-Hill Companies, Inc. All rights reserved.

European Embedded ValueNew Kid on the Block

18.

CONFIDENTIAL AND PROPRIETARY.

Permission to reprint or distribute any content from this presentation requires the written approval of Standard & Poor’s.August 2005

European Embedded Value (EEV) is the first set of financial reporting principles to be developed by the insurance industry.

A potential driver of EEV was to influence/provide solution for the IASB

It aims to provide supplementary disclosure, particularly in relation to long-term insurance business

It seeks to eradicate the different methodologies that have made EV comparison difficult

And address some of the inherent weaknesses of traditional EV

Goal is to build on strengths of existing EV methodologies

Background to EEV

19.

CONFIDENTIAL AND PROPRIETARY.

Permission to reprint or distribute any content from this presentation requires the written approval of Standard & Poor’s.August 2005

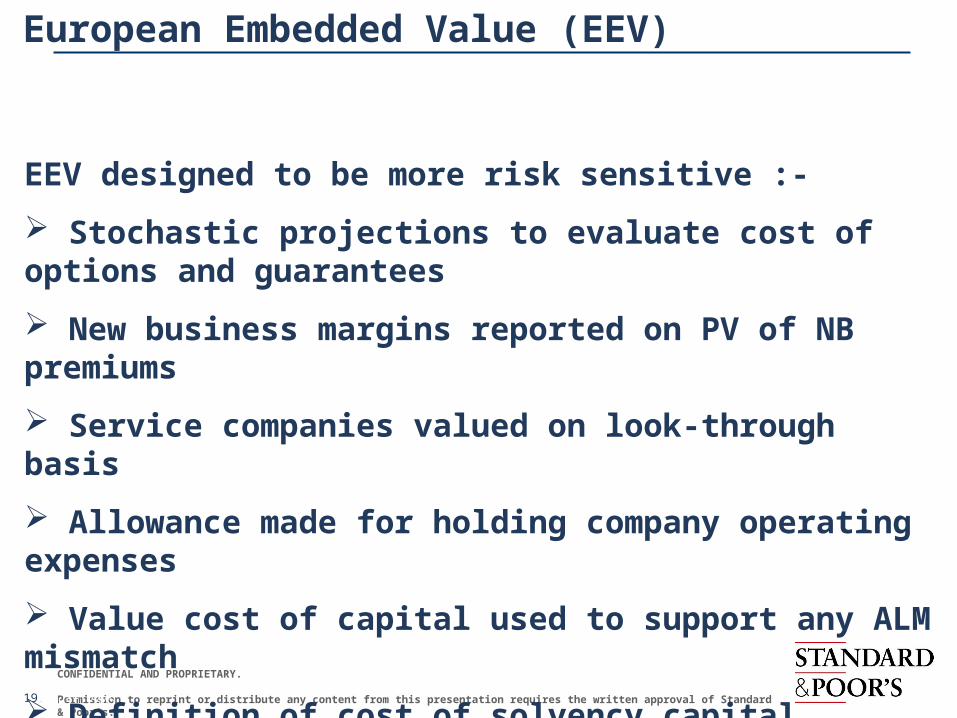

European Embedded Value (EEV)

EEV designed to be more risk sensitive :-

Stochastic projections to evaluate cost of options and guarantees

New business margins reported on PV of NB premiums

Service companies valued on look-through basis

Allowance made for holding company operating expenses

Value cost of capital used to support any ALM mismatch

Definition of cost of solvency capital widened

Risk discount rates may vary between product groups and territories – not prescriptive

Standardized set of sensitivities

20.

CONFIDENTIAL AND PROPRIETARY.

Permission to reprint or distribute any content from this presentation requires the written approval of Standard & Poor’s.August 2005

Criticisms of Traditional EV European Embedded Value

Deterministic approach to calculating options and guarantees

Capitalise market and credit risk premiums

Limited disclosure and lack of consistency

Variable economic assumptions and methodologies

Variable definition of required capital

Stochastic modelling of options and guarantees (not market consistent)

Discount rate set to capture remaining risks and may vary by product / territory

More detailed and consistent disclosure eg.sensitivities

Economic assumptions must be reliable, observable market data. No smoothing.

Required capital – preferred route is for economic rather than regulatory

Traditional EV vs. EEV

21.

CONFIDENTIAL AND PROPRIETARY.

Permission to reprint or distribute any content from this presentation requires the written approval of Standard & Poor’s.August 2005

Actuarial consultancies marketing MCEV that seeks to more fully allow for cost of risk and cost of capital

Cost of options and guarantees, priced on a basis consistent with that of the financial markets

Applies principle of no arbitrage re. asset risk premia

Expected cashflows valued using risk discount rate to reflect inherent product and ALM risks

Products that do best under MCEV are those that take no investment risk eg protection business.

Market value of assets – market-consistent value of liabilities –

cost of capital

Market Consistent Embedded Value

CONFIDENTIAL AND PROPRIETARY.

Permission to reprint or distribute any content from this presentation requires the written approval of Standard & Poor’s.

Copyright (c) 2006 Standard & Poor’s, a subsidiary of The McGraw-Hill Companies, Inc. All rights reserved.

S&P EV Analysis

23.

CONFIDENTIAL AND PROPRIETARY.

Permission to reprint or distribute any content from this presentation requires the written approval of Standard & Poor’s.August 2005

Advantages of EV for analysing operating performance

• Captures profits over the life of the portfolio rather over one year

• Contribution from new and existing business clearly defined

• Deviations in experience more transparent

• Options and guarantees quantified

24.

CONFIDENTIAL AND PROPRIETARY.

Permission to reprint or distribute any content from this presentation requires the written approval of Standard & Poor’s.August 2005

S&P Approach

• Establishing the credibility of EV Results

• Applying adjustments to EV Results

• Analysis of EV Results

25.

CONFIDENTIAL AND PROPRIETARY.

Permission to reprint or distribute any content from this presentation requires the written approval of Standard & Poor’s.August 2005

Analysis of EV Results

• What S&P is seeking to analyse:• Value added as a result of management

actions

• Risk exposure of VIF

• Overall EV Performance

26.

CONFIDENTIAL AND PROPRIETARY.

Permission to reprint or distribute any content from this presentation requires the written approval of Standard & Poor’s.August 2005

EV Profit

• It considers EV Profit gross of tax• EV Profit breakdown:• Expected income (unwinding + expected income on NA)• VNB• Economic variances• Changes in economic assumptions• Operating variances• Changes in operating assumptions• Development costs• Currency movements• Modelling changes• Unexplained

27.

CONFIDENTIAL AND PROPRIETARY.

Permission to reprint or distribute any content from this presentation requires the written approval of Standard & Poor’s.August 2005

Value Added by Management

• Areas where management can influence results:

• VNB

• Some items among operational variances and change in assumptions, e.g.:

– Expenses

– Persistency

• Investment performance

28.

CONFIDENTIAL AND PROPRIETARY.

Permission to reprint or distribute any content from this presentation requires the written approval of Standard & Poor’s.August 2005

VNB

• Areas of new business to be analysed• Aggregate VNB

• Individual Product New Business Profitability

• VNB Exposed to Risk

29.

CONFIDENTIAL AND PROPRIETARY.

Permission to reprint or distribute any content from this presentation requires the written approval of Standard & Poor’s.August 2005

Aggregate VNB

• To assess the scale of the new business

• Key Ratios:• VNB / VIF (SOY)

• NB Margin

• IRR

30.

CONFIDENTIAL AND PROPRIETARY.

Permission to reprint or distribute any content from this presentation requires the written approval of Standard & Poor’s.August 2005

Individual Product New Business Profitability

• In order to understand Product Profitability, NB profit margins (and IRR) by product category, country and preferably by distribution channel are required.

• The aims of the analysis are:

• To establish NB margins (and IRR) on consistent basis

• To link NB margins (and IRR) with competitiveness and strategy of the company, e.g.:

– Higher margins consistent with competitive advantages?

– Lower margins as a result of aggressive strategy?

31.

CONFIDENTIAL AND PROPRIETARY.

Permission to reprint or distribute any content from this presentation requires the written approval of Standard & Poor’s.August 2005

Linking NB profitability and Competitive Position

• It is important to understand how company’s competitive position factors contribute to the new business profitability, i.e. how company competitive position translate into financial results.

32.

CONFIDENTIAL AND PROPRIETARY.

Permission to reprint or distribute any content from this presentation requires the written approval of Standard & Poor’s.August 2005

VNB to Exposed to Risk

• Ratios:

• PVNBER = NB Risk Exposure / VNB (overall and per product)

• NB Risk Exposure / NB Margin (overall and per product)

33.

CONFIDENTIAL AND PROPRIETARY.

Permission to reprint or distribute any content from this presentation requires the written approval of Standard & Poor’s.August 2005

Performance Related Value Added

• The analyst needs to decide whether credit should be given to the management in respect of value created (or destroyed) as a result of their particular actions, e.g:

• expense reduction

• persistency improvement

• outperforming investment benchmark (without assuming more risk)

34.

CONFIDENTIAL AND PROPRIETARY.

Permission to reprint or distribute any content from this presentation requires the written approval of Standard & Poor’s.August 2005

Total Value Added by the Management

• (VNB + Credit in respect of management actions) /

• VIF (SOY)

35.

CONFIDENTIAL AND PROPRIETARY.

Permission to reprint or distribute any content from this presentation requires the written approval of Standard & Poor’s.August 2005

VIF Exposed to Risk

• To analyse the robustness of VIF under adverse scenarios using sensitivities results.

• An indication of likely volatility of VIF.

• Ratio:• PVIFER = VIF Risk Exposure / VIF

36.

CONFIDENTIAL AND PROPRIETARY.

Permission to reprint or distribute any content from this presentation requires the written approval of Standard & Poor’s.August 2005

Overall EV Performance Assessment

“EV Return on capital” ratio – standardised industry measure:

• Adjusted EV Profit / BBB Risk Capital

• Return on Embedded Value (ROEV)

• EV Profit / ((EV (SOY) + EV (EOY))/2)