bulk to boutique: road to riches? · branding value add but so do many of our competitors! 4 has...

TRANSCRIPT

Australian Dairy Conference

Bulk to boutique: road to riches?

Michael HarveyRabobank Food & Agribusiness ResearchFebruary 2016

2

A dictionary definition of ‘value add’

“…an improvement or addition to

something that makes it worth more”

Extract value

• Country of origin branding

• Leveraging safety, quality and integrity of product

Add value

• Taking numerous forms

• Product, packaging and process innovation

3

Our industry has good credentials to ‘extract’ value

High quality/grass

fed

Sustainable production

TraceabilitySpeed and access to market

Country of origin

brandingValue add

But so do many of our competitors!

4

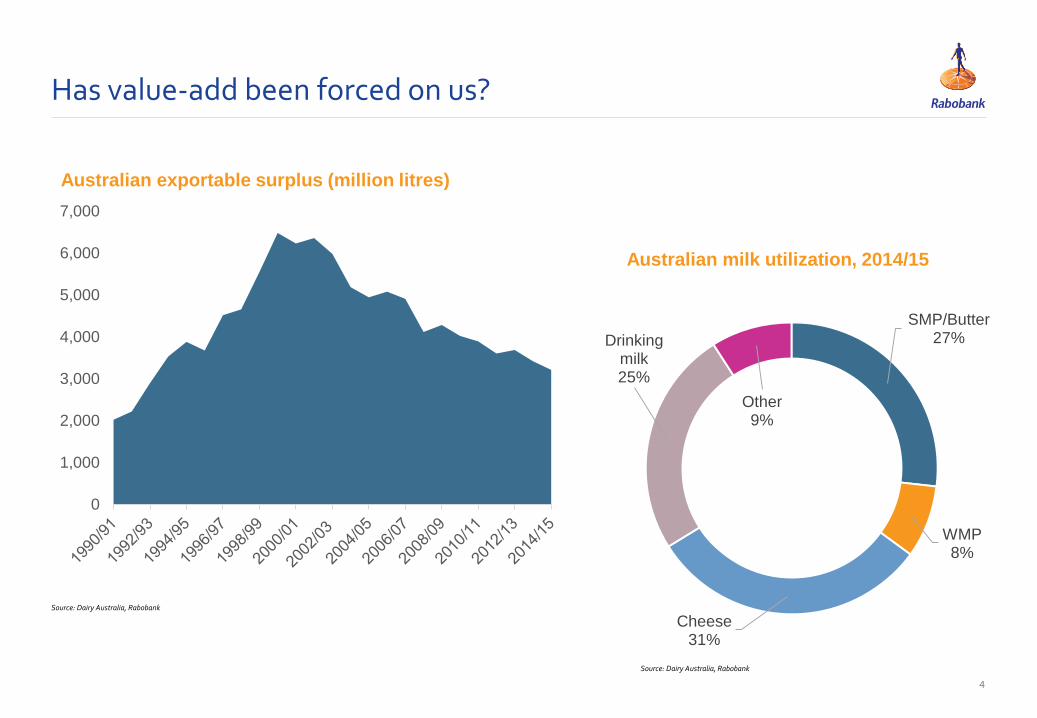

Has value-add been forced on us?

Source: Dairy Australia, Rabobank

Australian exportable surplus (million litres)

SMP/Butter27%

WMP8%

Cheese31%

Drinking milk25%

Other9%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Australian milk utilization, 2014/15

Source: Dairy Australia, Rabobank

5

Profit add is a common goal amongst dairy processors

2 key reasons:

Cost of doing business are higher here than global peers due to high labour and overhead costs

Competition for milk supply among these processors is intense

Source: Bloomberg, Rabobank

Financial performance of selected dairy processors

0

2

4

6

8

10

12

14

16

18

South EastAsia

NorthAmerica

Europe China Brazil Africa Oceania Japan

Ave

rag

e E

BIT

DA

ma

rgin

20

08

-14

f

2008-2014 average 2008-2014f average Top 30 listed companies

6

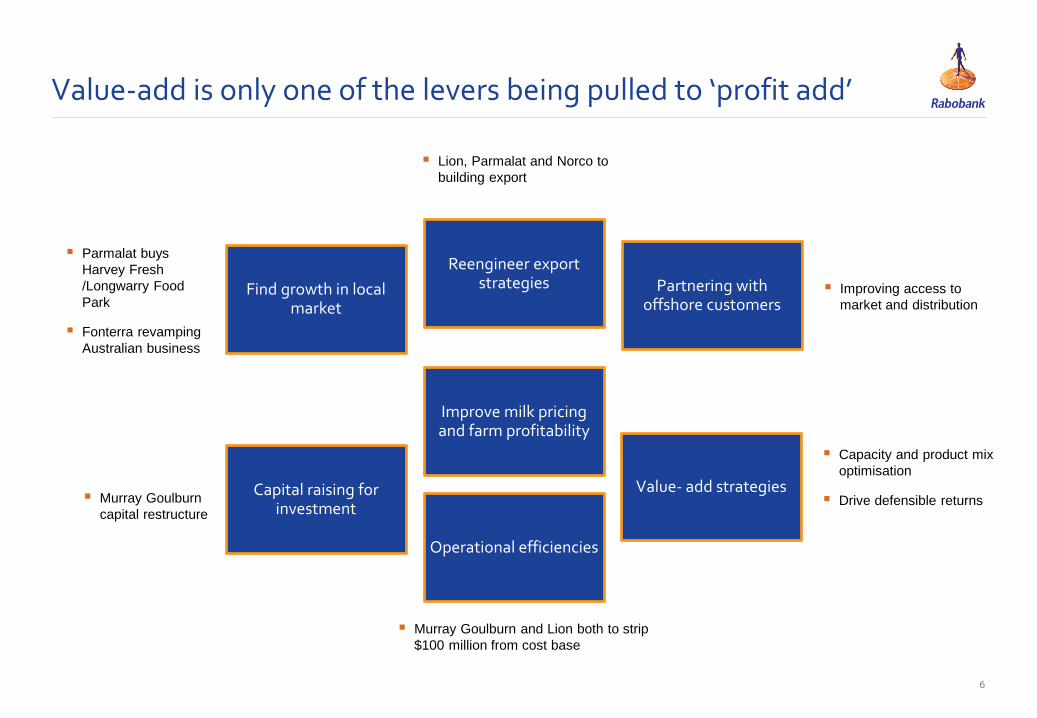

Value-add is only one of the levers being pulled to ‘profit add’

Find growth in local market

Reengineer export strategies Partnering with

offshore customers

Capital raising for investment

Improve milk pricing and farm profitability

Value- add strategies

Operational efficiencies

Parmalat buys

Harvey Fresh

/Longwarry Food

Park

Fonterra revamping

Australian business

Improving access to

market and distribution

Murray Goulburn

capital restructure

Lion, Parmalat and Norco to

building export

Capacity and product mix

optimisation

Drive defensible returns

Murray Goulburn and Lion both to strip

$100 million from cost base New entrants

7

Value add can be quite niche … or quite simple?

FrieslandCampina pay suppliers a premium

who graze herds outdoors for at least 6hrs a

day, 120 days per year

iNdream is made from melatonin-rich milk

collected at night when cows naturally

produce increased concentrations of

melatonin

8

Volume vs value – bulk comes before boutique

Source: Rabobank

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Mill

ion

s lit

res

LM

E

WMP Liquid milk

Chinese import volumes, milk powder and liquid milk

9

On the surface export margins look very lucrative

Source: Coles Online, Rabobank

Indicative retail price of 1 litre of UHT milk (AUD/litre)

0.00

1.00

2.00

3.00

4.00

5.00

Coles private label Devondale Local China brand Imported brand inChina

10

But value-add products attach a layer of cost to the business

Source: PC, Rabobank

Cost structure comparison, % of operating costs, bulk milk powder vs branded fresh milk

Raw milk71%

Other29%

Raw milk54%

Other46%

11

There are risks and barriers to entry

Lack of scale / supply capacity

Regulatory/certification hurdles

Capital outlay

Product development churn

Protecting IP/counterfeit

12

-200

0

200

400

600

800

1000

Net

her

lan

ds

Irel

and

UK

Po

lan

d

Ger

man

y

Fran

ce

Den

mar

k

Sp

ain

Bel

giu

m

Au

stri

a

CZ

Po

rtu

gal

Ital

y

Fin

lan

d

Hu

ng

ary

Slo

ven

ia

Slo

vaki

a

Gre

ece

Bu

lgar

ia

Bal

tic

Sta

tes

Cro

atia

Sw

eden

Ro

man

ia

‘00

0 t

on

nes

EU growth accelerating in the post-quota era

Growth in milk production versus pervious year (April-December)

Source: Rabobank analysis

Ireland and the Netherlands account for 50%

13

We aren’t alone in our quest to value add

Powders79%

Cheese17% Fresh

4%

Planned investment in new EU processing capacity

China liquid milk imports, 2009-2015

0

100,000

200,000

300,000

400,000

500,000

2009 2010 2011 2012 2013 2014 2015

Germany Australia New Zealand Other

Source: Rabobank

Source: Rabobank

So how do you measure success?

15

We are seeing a decoupling of farmgate milk returns from volatile commodities….

Source: Rabobank analysis

World WMP vs MG vs Fonterra FMP, (A$/kgMS and USD/t)

0

1,000

2,000

3,000

4,000

5,000

0.00

2.00

4.00

6.00

8.00

2009/10 2010/11 2011/12 2012/13 2013/14 2014/15 2015/16f

MGC AUD/kgMS Fonterra AUD/kgMS WMP

16

Summary and conclusion

Australia has good credentials to play the ‘value add’ game

Playing the game requires investment, comes with risk and presents hurdles

The competitive environment in ‘value add’ is intensifying

A strong point of difference is critical to defensibility – quality and brand strength is key!

Profit gains for successful value adding will be shared along the supply chain

And there is no guarantees of success…

But early evidence suggests strategies are working to de-commoditize farmgate returns

17

Important notice

This document is issued by Rabobank Australia Limited incorporated in Australia (“Rabobank”). The information and opinions contained in this document have been

compiled or arrived at from sources believed to be reliable, but no representation or warranty, express or implied, is made as to their accuracy, completeness or

correctness. This document is for information purposes only and is not, and should not be construed as, an offer or a commitment by Rabobank or any of its affiliates to

enter into a transaction. This information is not professional advice and has not been prepared to be used as the basis for, and should not be used as the basis for, any

financial or strategic decisions. This information is general in nature only and does not take into account an individual’s personal circumstances. All opinions expressed in

this document are subject to change without notice. Neither Rabobank, nor other legal entities in the group to which it belongs, accept any liability whatsoever for any

direct, indirect, consequential or other loss or damage howsoever arising from any use of this document or its contents or otherwise arising in connection therewith. This

document may not be reproduced, distributed or published, in whole or in part, for any purpose, except with the prior written consent of Rabobank. All copyrights,

including those within the meaning of the Copyright Act 1968 (Cth), are reserved. Australian law shall apply. By accepting this document you agree to be bound by the

foregoing restrictions. © Rabobank Australia Limited, Level 16 Darling Park Tower 3, 201 Sussex Street Sydney Australia, +61 2 8115 4000

18

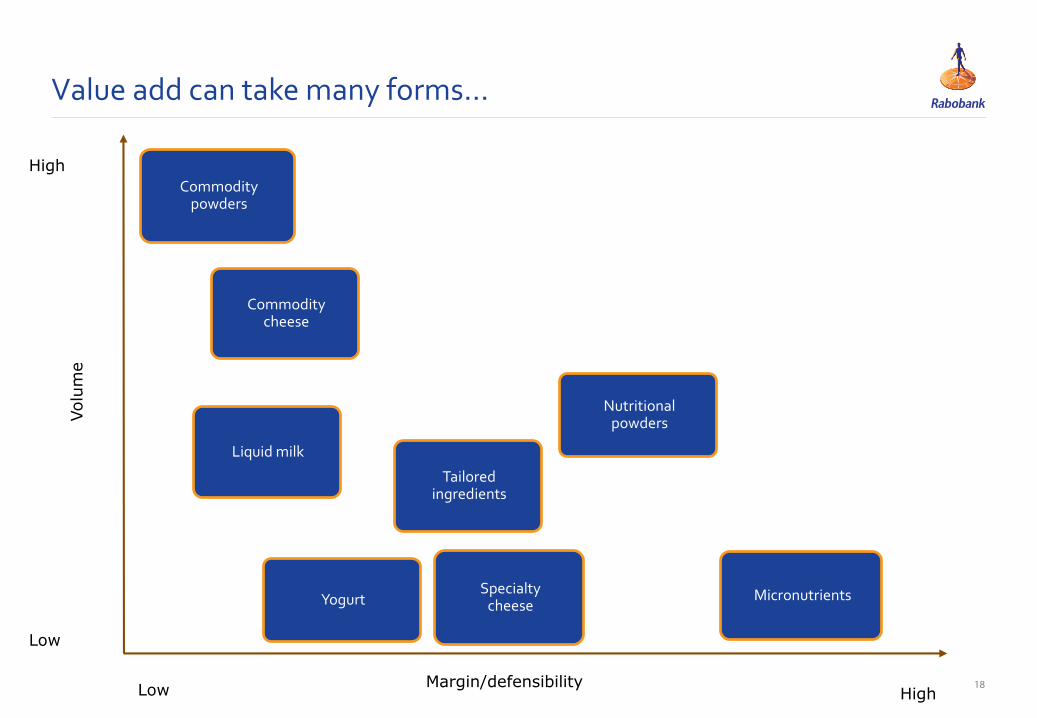

Value add can take many forms…

ACE Farms

Superannuation fundsVolume

High

Low

Margin/defensibilityHighLow

Nutritional powders

Tailored ingredients

Commodity powders

Regional brand owner

Micronutrients

Liquid milk

Commodity cheese

Specialty cheeseYogurt