antologia maestra contabilidad internacional

TRANSCRIPT

ANTOLOGÍA DE CONTABILIDAD INTERNACIONAL

MAESTRA: CP. MARÍA DE LOS ÁNGELES MÉNDEZ CEJA

GRADO: 8° GRUPO: “C”

ALUMNOS

RENDÓN GARCÍA GUADALUPE NATALHI

RANGEL SÁNCHEZ LILIANA MANELY

RODRÍGUEZ DEHARA JORDÁN ISAI

ZAVALETA LANDA GUADALUPE

POLÍTICAS DEL SALÓN

Puntualidad

Respeto a mi maestro y compañeros

No celulares ni audífonos ( si me cacha la maestra me lo quita y al termino

periodo de clases me lo regresa en presencia papas u esposo)

No chicles ni dulces ni nada que se le parezca ( si me cacha me

comprometo al dia siguiente traer una bolsa de kisses almendra para

repartir a mis compañeros)

No palabras altisonantes ( si me cacha me impondrá una sanción que ella

considere necesaria).

Compromiso de trabajo en equipo

Hombres no gorras bien peinados uñas

Mujeres bien peinadas uñas limpias

Criterios de evaluación

Examen 50%

Tarea 10%

Trabajo en eq. 40%

El trabajo en equipo se entregara una semana antes del término del periodo con

las sig. Características:

En una Usb letra arial 14 para título con hoja de presentación texto normal arial 12

interlineado normal justificado sin faltas de ortografía y en un sobre sellado.

Unidad 1

Normas internacionales de información financiera

1.1Antecedentes

1.2Países que ya adoptaron las NIIF

1.3Quienes están obligados

1.4A partir de cuando se aplican las NIIF

1.5Quien emitió la obligación en México

1.6Requisitos para adoptar las NIIF en México

1.7Quien regula internacionalmente las NIIF

1.8Políticas contables de acuerdo a las NIIF

1.9 Situación actual de las NIIF

Unidad 2

Proceso de transición de las NIF a las NIIF

2.1 Adopción a las NIF

2.2 Quienes están obligados

2.3 NIIF. Adopción por primera vez a las NIF

2.4 Implicaciones del balance de apertura según las NIIF

2.5 Combinación de negocios y alcance de consolidación de estados financieros

2.6 Consolidación y revelación en los primeros estados contables según las NIIF

Unidad 3

Normas y principios internacionales para registro y presentación de información contables

3.1 Introducción

3.2 Características de la contabilidad internacional

3.3 Normas y principios de la contabilidad internacional

3.4 Estados financieros básicos

3.5 Casos prácticos

Unidad 4

Registro de operaciones en moneda extranjera

4.1 Introducción

4.2 Técnicas de registro, conversión de moneda extranjera

4.3 Distintos tipos de cambio de moneda extranjera

4.4 Casos prácticos

Unidad 5

Problemas de contabilidad internacional en las practicas de reporte y registro alrededor del mundo

5.1 Introducción

5.2 Practicas de reporte y registro sobre crédito mercantil, activos intangibles, precios de transferencia y operadora por áreas

Unidad 6

Análisis de los estados financieros y comparabilidad de la información entre los países

6.1 Introducción

6.2 Medidas de ejecución de compañías japonesas

6.3 Aplicación de normas Internacionales de información financiera en Estados Unidos, Japón y Reino Unido

6.4 Casos prácticos (Se pide el uso de estados financieros en ingles)

Unidad 1

Normas internacionales de información financiera

1.1 Antecedentes

Debido a los cambios que se han dado en torno a la Globalización convirtiendo el

mundo en tan solo una aldea global electrónica, donde todo se encuentra

interconectado a través de una red mundial, y es por ello, que en Estados Unidos

de Norteamérica, caracterizado como primera potencia económica donde se

concentran las grandes empresas, que muchas de ellas cotizan en las bolsas de

valores, presentándose una controversia del mal manejo que se le da a la

información financiera para fines particulares de algunos grupos, debido a que no

existe una norma estándar que regule la práctica contable a nivel mundial.

1.2 Países que ya adoptaron las NIIF

Las NIIF son usadas en muchas partes del mundo, entre los que se incluye la

Unión Europea, Hong Kong, Australia, Malasia, Pakistán, India, Panamá,

Guatemala, Perú, Rusia, Sudáfrica, Singapur y Turquía. Al 28 de marzo de 2008,

alrededor de 75 países obligaran el uso de las NIIF, o parte de ellas. Otros

muchos países han decidido adoptar las normas en el futuro, bien mediante su

aplicación directa o mediante su adaptación a las legislaciones nacionales de los

distintos países.

Desde 2002 se ha producido también un acercamiento entre el IASB "

International Accounting Standards Board y el FASB "Financial Accounting

Standards Board", entidad encargada de la elaboración de las normas contables

en Estados Unidos para tratar de armonizar las normas internacionales con las

norteamericanas. En Estados Unidos las entidades cotizadas en bolsa tendrán la

posibilidad de elegir si presentan sus estados financieros bajo US GAAP (el

estándar nacional) o bajo NICs.

1.3 Quienes están obligados

-Empresas grandes que cotizan en bolsa, captan y colocan recursos

-Cuando su matriz o subsidiaria aplican NIIF plenas

-Cuando sus importaciones y exportaciones superan el 50% de operaciones

1.4 A parir de cuando se aplican las NIIF

No se debe esperar la fecha para iniciar la fase de planificación de la adopción,

porque la exigencia de presentar las cuentas anuales según las normas

internacionales se fija a partir del 2013, esas incluirán información comparativa.

por lo que al menos efectos internos, sera necesario adelantar un año de las NIC

1.5 Quien emitió la obligación

El Consejo mexicanos de Normas de Información Financiera

1.6 Requisitos para adoptar las NIIF

La gerencia debe estar conciente que la adopción e implementación inicial de las

NIIF debe concebirse como un proceso o proyecto el cual debe ser

adecuadamente planificado y gestionado. La implementación de NIIF no debe

concebirse Como un simple cambio del catalogo de cuentas ola elaboración de un

nuevo manual contable. Por el contario es un proyecto que implica la toma de

decisiones estratégicas por parte de la gerencia de la entidad adoptante en el que

deben establecerse fechas y actividades especificas

1.7 Quien regula internacionalmente las NIIF

El consejo internacional (Estados Unidos, Canadá y Europa)

1.8 Políticas contables de acuerdo a las NIIF

Son políticas que de acuerdo con los principios bases convenciones, reglas y

procedimientos específicos adoptados por la entidad al preparar y presentar

estados financieros.

UNIDAD II

PROCESO DE TRANSICIÓN DE LAS NIF A LAS NIIF

2.1 ADOPCIÓN DE LAS NIIF

Constituye un proceso de aplicación mundial, dicho de otro modo, una tendencia

que involucra la globalización de la profesión contable, vista bajo el paradigma de

la eliminación de fronteras en cuanto a la prestación de servicios.

2.2 QUIENES ESTÁN OBLIGADOS

NIFF PLENAS ( Grupo 1)

Empresas grandes que cotizan en bolsa y captan y colocan recursos. Cuando su

matriz o subsidiaria aplica NIIF plenas y cuando importaciones y exportaciones

superan el 50% de operaciones.

NIIF PARA PYMES ( Grupo 2)

Empresas grandes que no estan en el grupo 1 Todas empresas medianas y

pequeñas las microempresas .

2.3 Adopción por primera vez de las NIIF

NIIF A-1 Es la que nos habla de la adopción por primera vez.

El balance de apertura conforme a las NIIF de una entidad es el punto de partida

para su contabilidad según las NIIF

2.3 ADOPCIÓN POR PRIMERA VEZ DE LAS NIIF

La regla general es que a la fecha efectiva de reporte de la transición, los

principios de contabilidad deben ser aplicados retrospectivamente en la hoja de

balance de apertura.

Algunos aspectos de el balance de apertura:

*La entidad reconocerá todos los activos y pasivos de acuerdo con los

requerimientos de las IFRS, y eliminará los activos y pasivos que no cumplen los

requerimientos de las IFRS

Los efectos de los cambios en políticas contables serán reconocidos en el

patrimonio en el balance general de apertura, excepto por reclasificaciones entre

plusvalía mercantil (goodwill) y activos intangibles.

*La NIIF 1 expande los requerimientos de revelación comparados con los

requerimientos de la primera adopción incluidos previamente en la normas

internacionales de contabilidad, específicamente la interpretación SIC 8 Aplicación

por Primera Vez de las NICs como Base primaria para la Contabilidad.

2.4 IMPLICACIONES DEL BALANCE DE APERTURA SEGÚN LAS NIIF

EL BALANCE DE APERTURA SEGÚN LAS NIIF

Las compañías deben preparar un balance general de apertura según las niif en

“la fecha de transición a las niif”s el punto de inicio para la contabilidad posterior a

la aplicación de las niif

No es necesario publicar el balance general de apertura en los primeros estados

financieros siguiendo las niiff al balance inicial del primer periodo para el cual se

presenta información comparativa completa de acuerdo con las niif.

Ejemplo:

Cuando una compañía prepare sus primeros estados financieros para el año que

finaliza el 31 de diciembre del 2005 con una año comparativo, la fecha de

transición a las NIIF sería el 1º de enero de 2004, y el balance general de

apertura según las NIIF se preparar en esa fecha.

Una compañía que requiera presentar dos años de información comparativa

completa, tendría que preparar un balance general de apertura el 1º de enero del

2003.

Incluye todos los activos y pasivos que s e requieren en las niif.

Excluye cualquier activo y pasivo que no esten permitidos por las niif.

Clasifica todos los activos, pasivos y patrimonio de conformidad con las niif; y mide

todas las partidas de acuerdo a las niif.

FECHA DE ADOPCIÓN

La fecha de adopción de una compañía es la del inicio de 1 año financiero cuyos

estados financieros se preparan según las NIIF por primera vez.

Los ajustes realizados como resultado de la adopción de las NIIF por primera vez

se registran en las ganancias retenidas o en otra cuenta del patrimonio.

LAS IMPLICAIONES EN EL BALANCE GENERAL DE APERTURA

La preparación del balance general de apertura según las NIIF puede recurrir el

cálculo o recolección de información que no se calculó o no se recolecto bajo los

PCGA anteriores de la compañía. en las primeras etapas, las compañías deben

planificar su transición e identificar las diferencias que existen entre las NIIF y sus

PCGA anteriores, para así poder recolectar toda la información requerida.

NIIF 3 Combinaciones de negocios.

El objetivo de esta NIIF es mejorar la relevancia, la fiabilidad y la comparabilidad

de la información sobre las combinaciones de negocios y sus efectos, que una

entidad informante proporciona a través de sus estados financieros.

Se lleva a cabo mediante el establecimiento de principios y requerimientos sobre

la forma en que una adquirente:

(a) reconocerá y medirá en sus estados financieros los activos identificables

adquiridos, los pasivos asumidos y cualquier participación no controladora en la

entidad adquirida.

(b) reconocerá y medirá la plusvalía adquirida en la combinación de negocios o

una ganancia procedente de una compra en condiciones muy ventajosas.

(c) determinará qué información revelará para permitir que los usuarios de los

estados financieros evalúen la naturaleza y los efectos financieros de la

combinación de negocios.

Cualquier clasificación o designación realizada al reconocer estas partidas debe

realizarse de acuerdo con los términos contractuales, condiciones económicas,

políticas contables y de operación de la adquirente y otros factores que existan en

la fecha de la adquisición.

Cada activo y pasivo identificables se medirá al valor razonable en la fecha de su

adquisición. Cualquier participación no controladora en una adquirida se medirá al

valor razonable o como la parte proporcional de la participación no controladora de

los activos identificables netos de la adquirida.

La NIIF proporciona excepciones limitadas a estos principios de reconocimiento y

medición:

(a) Los contratos de arrendamiento y de seguro se requiere que se clasifiquen

sobre la base de los términos contractuales y otros factores existentes al

inicio del contrato (o cuando los términos hayan cambiado) en lugar de

sobre la base de los factores que existan en la fecha de adquisición.

(b) Solo se reconocerán aquellos pasivos contingentes asumidos en una

combinación de negocios que sean una obligación presente y puedan

medirse con fiabilidad.

(c) Se requiere que algunos activos y pasivo se reconozcan o midan de

acuerdo con otras NIIF, en lugar de al valor razonable.

(d) Existen requerimientos especiales para medir un derecho readquirido.

(e) Los activos por indemnización se reconocerán y medirán sobre una base

que sea coherente con la partida objeto de indemnización, incluso si esa

medida no es el valor razonable.

La NIIF requiere que la adquirente, que tenga reconocidos los activos

identificables, los pasivos y las participaciones no controladoras, identifique

cualquier diferencia entre:

La suma de la contraprestación transferida, cualquier participación no controladora

en la adquirida y, en una combinación de negocios realizada por etapas, el valor

razonable de la fecha de adquisición de la participación de la adquirente

mantenida con anterioridad en el patrimonio de la adquirida.

(b) los activos identificables netos adquiridos.

NIIF 1 ADOPCIÓN POR PRIMERA VEZ

Cuando se adoptan por primera vez, las normas internacionales de información

financiera NIIF, la empresa necesita realizar una serie de acciones como por

ejemplo un análisis comparativo de los estados financieros.

Si una empresa necesita entregar sus estados financieros con arreglo a NIIF o

IFRS, al 31 de Diciembre, entonces necesita preparar la siguiente información:

Balance de apertura con arreglo a las NIIF el 1ro de Enero

Balance según NIIF del 31 de diciembre, estado de resultados, Estado de Flujo de

Efectivo, Estado de cambios en el patrimonio.

Comparativos de saldos con el año anterior.

Los primeros estados financieros conforme a las NIIF son los primeros estados

financieros anuales en los cuales la entidad adopta las NIIF, mediante una

declaración, explícita y sin reservas, contenida en tales estados financieros, del

cumplimiento con las NIIF.

Una entidad usará las mismas políticas contables en su estado de situación

financiera de apertura conforme a las NIIF y a lo largo de todos los periodos que

se presenten en sus primeros estados financieros conforme a las NIIF. Estas

políticas contables cumplirán con cada NIIF vigente al final del primer periodo

sobre el que informe según las NIIF

UNIDAD3

NORMAS Y PRINCIPIOS INTERNACIONALES PARA REGISTRO Y

PRESENTACION DE LA INFORMACION CONTABLE

Los Principios de Contabilidad Generalmente Aceptados (PCGA) o Normas de

Información Financiera conocidos como (PCGA) son un conjunto de reglas

generales y normas que sirven de guía contable para formular criterios referidos a

la medición del patrimonio y a la información de los elementos patrimoniales y

económicos de un ente. Los PCGA constituyen parámetros para que la confección

de los estados financieros sea sobre la base de métodos uniformes de técnica

contable.

Se aprobaron durante la 7ª Conferencia Interamericana de Contabilidad y la 7ª

Asamblea Nacional de Graduados en Ciencias Económicas, que se celebraron en

Mar del Plata en 1965.

Los principios de la “partida doble” es un principio contable establecido por Fray

Luca Paccioli (1445-510 E. C.) en 1494.

Su enunciado básico dice: .

A una o más cuentas deudoras corresponden siempre una o más cuentas

acreedoras por el mismo importe.

En todo momento las sumas del debe deben ser igual a las del haber.

Las pérdidas se debitan y las ganancias se acreditan.

El patrimonio del ente es distinto al de su/s propietario/s.

El principio de los recursos de un ente es igual al valor de las participaciones que

recaen sobre él.

Los componentes patrimoniales y las causas de sus resultados se representan por

medio de cuentas en las que se registran notas o asientan las variaciones al

concepto que representan.

El saldo de una cuenta es el valor monetario de la misma en un momento dado.

Este saldo se modifica cada vez que una operación tiene efecto sobre los

componentes que ella representa.

Las cuentas de activo y gasto son deudoras, y las de pasivo, ganancia y

patrimonio neto son acreedoras.

En toda anotación (asiento), cualquiera sea el número de débitos y créditos, la

suma de los saldos debe ser igual.

Para dar de baja un importe previamente registrado, la cuenta a registrar debe ser

la que lo representa y el importe debe ser el mismo previamente registrado

.Toda cuenta posee 2 secciones: DEBE Y HABER.

NORMAS INTERNACIONALES DE INFORMACIÓN FINANCIERA

Cuando hablamos de IFRS nos estamos refiriendo a:

NIC + IFRS + SIC + IFRIC

NIC (International Accounting Standards)= NIC (Normas Internacionales de

Contabilidad)

IFRS (International Financial Reporting Standards)= NIIF (Normas Internacionales

de Información Financiera)

SIC (Standards Interpretation Committee)= Comité de Interpretaciones de las NIC

IFRIC (International Financial Reporting Interpretation Committee)= CINIIF

(Comité de Interpretación de las Normas Internacionales de Información

Financiera)

Características de Las Normas Internacionales

de Información Financiera (NIIF/IFRS)

Es una normativa amplia que provee de modelos sistémicos para la generación de

información para el usuario

Se basan en la confiabilidad de los datos, la independencia de los métodos de

valoración y en la calidad de la información

No es regulatoria (como lo son los USGAAP)

La libertad de interpretación es un factor de riesgo en nuestra cultura contable.

Se aleja de los conceptos tributarios pues es netamente financiera.

CARACTERISTICAS DE LA CONTABILIDAD INTERNACIONAL

Esta contabilidad se debe principalmente a las transacciones de empresas

multinacionales, ya que maneja sus recursos a escala mundial.

Mucho se ha escrito acerca de la naturaleza multinacional de la economía mundial

actual. Ejemplo de empresas tenemos: la coca cola, Toyota, etc.

La primera aparición de una empresa en el campo de la Contaduría Internacional

generalmente ocurre como resultado de una importación y una exportación ( dos

actividades importantes que se están dando en todo el mundo).

Una complicación en la actualidad para el manejo de la contabilidad internacional,

es el idioma, ya que los estados financieros se elaboran con el lenguaje

predominante en dicho país, por tal razón muchas empresas piden apoyos a

instituciones de crédito o agencias especializadas.

NORMAS Y PRINCIPIOS DE LA CONTABILIDAD

La Comisión de Principios y Normas de Contabilidad tiene como objetivos el

análisis y emisión de las Normas Contables, es decir, Boletines técnicos y Normas

de Información Financiera. Así también, representa al Colegio de Contadores en

destinas instancias sociales, y frente a los organismos fiscalizadores nacionales e

internacionales.

La Comisión está integrada por 11 miembros colegiados, entre los que se incluye

profesores de diversas universidades, socios y exsocios de las principales firmas

de auditoría, representantes de la Confederación de la Producción y del Comercio.

Las Normas Internacionales de Contabilidad NIC Son un conjunto de estándares

que establecen la información que deben presentarse en los estados financieros y

la forma en que esa información debe aparecer, en dichos estados.

Estos principios han sido elaborados tomando en cuenta los postulados o

principios básicos para que la información financiera de la contabilidad logre el

objetivo de ser útil al momento de tomar decisiones, se dividen en tres categorías

distintas:

Supuestos derivados del ambiente económico: entidad, énfasis en el aspecto

económico, cuantificación y unidad de medida

Principios generales que debe reunir la información: objetividad, importancia

relativa, comparabilidad, y revelación suficiente.

Principios que establecen la base para cuantificar las operaciones de la entidad y

los eventos económicos que la afectan: valor histórico original, dualidad

económica, negocio en marcha o continuidad, realización contable, periodo

contable y conservatismo.

Las normas se conocen con las siglas NIC y NIIF dependiendo de cuándo fueron

aprobadas y se matizan a través de las "interpretaciones"

ESTADOS FINANCIEROS BÁSICOS

¿Que son?

Los estados financieros, también denominados estados contables , informes

financieros o cuentas anuales, son informes que utilizan las instituciones para dar

a conocer la situación económica y financiera y los cambios que experimenta la

misma a una fecha o periodo determinado.

Objetivo

El objetivo de los estados financieros es proveer información sobre el patrimonio

del emisor a una fecha y su evolución económica y financiera en el período que

abarcan, para facilitar la toma de decisiones económicas.

Características cualitativas de los estados financieros:

BALANCE GENERAL

El estado de situación financiera, también llamado estado de posición financiera o

balance general, muestra relativa a fecha determinada sobre los recursos y

obligaciones financieros de la entidad: por lo consiguiente, los activos en orden de

su disponibilidad, revelando sus restricciones; los pasivos atendiendo a su

exigibilidad, revelando sus riesgos financieros, así como el capital contable

patrimonio a dicha fecha

Activo: Es un recurso controlado por la entidad, identificado y cuantificado en

términos monetarios, del que se esperan fundadamente beneficios económicos

futuros, derivado de operaciones ocurridas en el pasado, que han afectado

económicamente a dicha entidad

Pasivo: Es una obligación presente virtualmente ineludible, identificada,

cuantificada en términos monetarios y que representa una disminución futura de

beneficios económicos, derivada de operaciones ocurridas en el pasado que han

afectado a dicha entidad

Capital contable: Es el valor residual de los activos de la entidad, una vez

deducidos todos sus pasivos

EL ESTADO DE RESULTADOS INTEGRAL

El estado de resultados integral para entidades lucrativas o, en su caso, estado de

actividades, para entidades con propósitos no lucrativos, que muestra información

relativa al resultado de sus operaciones en un periodo y, por ende, de los

ingresos, gastos; así como de la utilidad (perdida) neta o cambio neto o cambio en

le patrimonio contable resultante en el periodo.

EL ESTADO DE FLUJOS DE EFECTIVO

El estado de flujos de efectivo o, en su caso, el estado de cambios en la situación

financiera, que indica información acerca de los cambios en los recursos y las

fuentes de financiamiento de la entidad del periodo, clasificados por actividades,

de operación, de inversión y de financiamiento

Actividades de operación: Son las que constituyen la fuente principal de ingresos

por la entidad

Actividades de inversión: Son las relacionadas con la adquisición y la disposición

de: propiedades, planta y equipo activos intangibles y otros activos destinados al

uso, a la producción de bienes o la prestación de servicios

Actividades de Financiamiento: Son las relacionadas con la obtención, así como la

retribución y resarcimiento de fondos provenientes: los propietarios de la entidad,

acreedores otorgantes de financiamiento que no estén relacionados con las

operaciones habituales de suministro de bienes y servicios.

EL ESTADO DE CAMBIOS EN EL CAPITAL CONTABLE

El estado de cambios en el capital contable, en el caso de entidades lucrativas,

que muestra los cambios en la inversión de los propietarios durante el periodo, y

se conforman por los siguientes elementos básicos:

-Movimientos de propietarios

-Movimientos de reserva

-Resultado integral

UNIDAD IV. REGISTRO DE OPERACIÓN EN MONEDA EXTRANJERA.

INTRODUCCION

MONEDA EXTRANJERA:

Moneda extranjera o divisa, se refiere a los billetes o monedas de países

extranjeros. Es cualquier moneda distinta a la de registro, a la funcional o a la de

informe de la entidad, según las circunstancias.

Moneda de registro: es aquella a la cual la entidad mantiene sus registros

contables, ya sea para fines legales o de información.

Moneda de informe: es aquella elegida y utilizada por una entidad para presentar

sus estados financieros.

Moneda funcional: es aquella con la que opera una entidad en su entorno

económico.

Tipo de cambio: es la relación de cambio entre dos monedas a una fecha

determinada.

Tipos de cambio de contado: es el utilizado en transacciones con entrega

inmediata.

Tipo de cambio de cierre:

Es el de contado a la

Fecha de balance general.

Tipo de cambio histórico: es el de contado a la fecha de transacción.

Partidas monetarias: son aquellas que se encuentran expresadas en unidades

monetarias nominales sin tener relación con precios futuros de determinados

bienes o servicios.

Partidas no monetarias: son aquellas cuyo valor nominal varía de acuerdo

con el movimiento de la inflación.

Valor razonable: es el monto de efectivo o equivalentes que participantes en el

mercado estarían dispuestos a intercambiar para la venta de un activo o transferir

un pasivo.

¿Quien debe hacer el registro de operaciones con moneda extranjera?

Todas aquellas empresas que realizan transacciones en moneda extranjera.

Entre las operaciones en moneda extranjera se incluye:

a)Compra o vende bienes o servicios cuyo precio se denomina en moneda

extranjera.

b) Presta o toma prestados fondos, si los importes correspondientes se

establecen a cobrar o pagar en moneda extranjera; o

Adquiere o dispone de activos, o bien, incurre, transfiere o liquida pasivos, siempre

que estas transacciones se hayan denominado en moneda extranjera.

Toda transacción en moneda extranjera debe reconocerse inicialmente en la

moneda de registro aplicando el tipo de cambio histórico.

La fecha de alguna transacción es aquella en la cual dicha operación se devenga

y cumple sus condiciones para su reconocimiento de acuerdo a las NIF.

A la fecha de cierre de los estados financieros los saldos de partidas monetarias

derivados de transacciones en monedas extranjeras deben convertirse al tipo de

cambio de cierre. Así mismo a la fecha de realización (cobro o pago) de dichas

transacciones.

La diferencia en cambios debe reconocerse como ingreso o gasto en la utilidad

o perdida neta en el estado de resultados integral.

TECNICAS DE REGISTRO Y CONVERSION DE MONEDA EXTRANJERA

Conversión implica transformar, re expresar o trasladar los estados contables

elaborados originalmente en una moneda A, en otra moneda B.

Una conversión es una re expresión monetaria en la cual: el objeto (lo que se

expresa) es una medición en moneda de origen; el producto es una medición

(equivalente a la anterior) en una moneda de conversión; la segunda medición se

obtiene a partir de la primera y de algún tipo de cambio que indica la cantidad de

unidades de la moneda de origen por las que se puede cambiar una unidad de la

moneda de conversión, o viceversa.

Operaciones extranjeras

Una operación extranjera es una entidad cuyas actividades se llevan a cabo en un

país con una moneda distinta a los de la entidad informante. La NIF B-15

establece que los estados financieros de este tipo de entidades deben convertirse

a la moneda de informe, por lo que debe atenderse lo siguiente:

Proceso de conversión:

1. Convertir la moneda de registro a la moneda funcional.

2. Convertir la moneda funcional a la moneda de informe.

1.-Conversión de la moneda de registro a la funcional:

Activos y Pasivos monetarios. TC de cierre.

Activos y Pasivos no monetarios y capital contable. TC histórico.

Ingresos, Costos y Gastos. TC histórico.

Diferencias en cambios. Deben reconocerse como ingreso o gasto, dentro del RIF

en el estado de resultados.

2.-Conversión de la moneda funcional a la de informe:

cuando el entorno es o no inflacionario: Las variaciones entre el capital contable y

la inversión de la operación extranjera deben reconocerse en el capital contable.

Conversión de la moneda funcional a la de informe, cuando el entorno es

inflacionario:

Activos, Pasivos y capital contable. TC de cierre.

Ingresos, Costos y Gastos. TC de cierre.

Las variaciones entre el capital contable y la inversión de la operación extranjera

deben reconocerse como efecto acumulado por conversión en el capital contable.

Cambios de moneda de registro, funcional y de informe:

Cambio de moneda de registro o funcional. Debe reconocerse de forma

prospectiva a partir de la fecha del cambio.

Cambio de moneda de informe. Debe reconocerse con base en el método

retrospectivo conforme

DISTINTOS TIPOS DE CAMBIO DE MONEDA EXTRANJERA

¿QUE ES TIPO DE CAMBIO?

El tipo o tasa de cambio es el precio de una divisa. Ahora en el 2014 con otras

palabras, es el número de unidades de la moneda nacional que hay que entregar,

en un momento dado, a cambio de una unidad de moneda extranjera (divisa).

El nacimiento de un sistema de tipos de cambio proviene de la existencia de un

comercio internacional entre distintos países que poseen diferentes monedas.

Tipo de cambio fijo: es determinado rígidamente por el Banco central.

Tipo de cambio flexible: se determina en un mercado libre, por el juego de la oferta

y la demanda de divisas.

Tipo de cambio real: Se define como la relación a la que una persona puede

intercambiar los bienes y servicios de un país por los de otro.

Tipo de cambio nominal: es la relación a la que una persona puede intercambiar

la moneda de país por los de otro, es decir, el número de unidades que necesito

de una moneda X para conseguir una unidad de la moneda Y. Este último es el

que se usa más frecuentemente.

EN PLAZOS

El tiempo de liquidación de las transacciones realizadas con divisas puede ser:

Tipo de cambio spot: El tipo de cambio spot se refiere al tipo de cambio corriente,

es decir, transacciones realizadas al contado.

El precio spot o precio corriente de un producto, de un bono o de una divisa es el

precio que es pactado para transacciones (compras o ventas) de manera

inmediata.

Tipo de cambio futuro: el tipo de cambio futuro indica el precio de la divisa en

operaciones realizadas en el presente, pero cuya fecha de liquidación es en el

futuro, a un determinado precio fijado entre las partes, por ejemplo, dentro de 180

días.

UNIDAD VI

ANALISIS DE LOS ESTADOS FINANCIEROS Y COMPARABILIDAD DE LA

INFORMACION ENTRE LOS PAISES

INTRODUCCION

Conocer los Estados Financieros es saber hacia donde marcha nuestro negocio,

es tener el detalle de la estructura financiera de la empresa, es entender la

evolución de las operaciones y las cuentas de manera que se pueda analizar la

tendencia positiva o negativa de la situación y los resultados financieros.

El análisis financiero requiere de un conocimiento completo de la esencia de los

Estados Financieros, las partidas que la conforman, sus problemas y

limitaciones. Con esta base, quien analice los estados financieros podrá lograr

mejores recomendaciones o tomar óptimas decisiones.

Naturaleza de los Estados Financieros

Los Estados Financieros se preparan para presentar un informe periódico acerca

de la situación del negocio, los progresos de la administración y los resultados

obtenidos durante el periodo que se estudia, constituyendo una combinación de

hechos registrados, convenciones contables y juicios personales.

Los hechos registrados se refieren a los datos sacados de los registros contables,

tales como la cantidad de efectivo o el valor de las obligaciones.

Las relaciones contables se relacionan con ciertos procedimientos supuestos,

tales como la forma de valorizar los activos, la capitalización de los gastos

financieros, etc.

El juicio personal hace referencia a las decisiones que puede tomar el contador

en cuanto a utilizar tal o cual método de depreciación o valoración de inventarios,

amortización de diferidos en un término más corto o más largo .

Se denomina análisis de estados financieros al tratamiento de la información que

esta suministra con objeto de permitir la toma de decisiones con su uso. Esta labor

irá enfocada al objetivo que se persiga y al usuario que haga uso de ella por lo que

no existe un único tipo de análisis.

Para interpretar en forma adecuada las cifras contenidas en los estados

financieros, estudiaremos los siguientes métodos de análisis:

Método de porcientos integrales razones financieras punto de equilibrio flujo de

efectivo

El conocimiento de estos métodos de análisis le permitirá una mejor interpretación

de los estados financieros, lo cual hará posible la obtención de conclusiones sobre

los resultados obtenidos y en su caso tomar las medidas correctivas necesarias.

EL BALANCE GENERAL

Es un resumen claro y sencillo sobre la situación financiera de la empresa a una

fecha determinada. Muestra todos los bienes propiedad de la empresa (activo), así

como todas sus deudas (pasivo) y por último el patrimonio de la empresa (capital).

Su elaboración podrá ser mensual, semestral o anual.

EL ESTADO DE RESULTADOS

Es un informe que permite determinar si la empresa registró utilidades o pérdidas,

en un periodo determinado.

Análisis de estados financieros por compañías extranjeras

Describe varias razones que justifican el análisis de estados financieros

extranjeros.

Describe los problemas potenciales relacionados con el análisis de los estados

financieros extranjeros y discute las posibles soluciones a esos problemas

MEDIDAS DE EJECUCION DE COMPAÑIAS JAPONESAS

Regulación contable

En Japón la información contable y la información financiera están reguladas

principalmente a través de un triangulo de leyes:

El código comercial

La ley de valores y de cambios

La ley del impuesto al ingreso corporativo

Código comercial

Esta ley requiere que las kabushiki kaisha(las corporaciones de acciones

conjuntas) preparen un informe anual para la aprobación de la junta general de

accionistas.

Ley de valores y de cambios

(Security and Exchangue Law)

Japón tiene seis bolsas de valores, siendo la mas importante la bolsa de valores

de Tokio. Las SEL para las compañías inscritas en bolsa se promulgo en 1948 y

es administrado por el MoF.En 1951 la SEL requirió que los estados financieros de

dichas compañías que estuvieran inscritas en bolsa fueran auditadas por CPC.

Ley del impuesto al ingreso corporativo

Proporciona métodos para calcular del ingreso gravable y requiere que los

ingresos y los gastos se reconozcan en los libros de cuentas de acuerdo con las

leyes fiscales.

Balance general

Estado de resultados

Estado de aplicaciones propuestas de las utilidades

Se considera que las leyes fiscales son menos vagas que el código comercial y la

SEL; por lo tanto, frecuentemente se hace referencia a ellas cuando se requieren

regulaciones mas detalladas

Las normas de contabilidad de los negocios consisten en un conjunto de 7

lineamientos que forman un marco conceptual del Japón

Las normas de contabilidad de los negocios son desarrollados por el

BADC(Business Accounting Deliberation Council).

Los miembros del BADC tiene un amplia variedad de antecedentes. Incluyen a

contadores que trabajan en la industria , en la contabilidad publica, en el gobierno

y en la educación mas alta.

En el mes de noviembre de 1966, el gobierno japonés anuncio su estrategia para

las reformas financieras y el primer ministro comisiono a BADC para reformar el

sistema de información financiera de Japón.

Estos cambios han recibido el nombre de Big Bang

Las compañías de Japón están actualmente obligadas a:

Una perspectiva verdadera y justa

Una teneduría de libros ordenada

La distinción entre el capital y las utilidades

Una presentación clara

La continuidad

El conservadurismo

La consistencia

Publicar cuentas consolidadas, incluyendo las de todas las asociadas sobre las

cuales tengan influencia

Revelar el valor mercado de los pasivos por pensiones y el hecho de tener

inconvenientes o no.

Reportar los valores financieros negociables, como los instrumentos derivativos y

las acciones ordinarias, a los valores de mercado y no al costo histórico.

UNIDAD VI PROBLEMAS DE REGISTROS Y REPORTE ALREDEDOR DEL

MUNDO

Es una estructura universal, que busca crear unas determinadas condiciones para que las empresas tengan como objetivo principal, acrecentar su nivel de ganancias por la venta de bienes y servicios en el ámbito mundial

MODELOS CONTABLES EN EL MUNDO

Cada país posee una mezcla única de variables ambientales (economía,

importaciones, exportaciones de las empresas, empleos, oferta, demanda, leyes.),

que en conjunto influyen en el desarrollo de un sistema contable.

MODELO ANGLO-AMERICANO

La orientación de este modelo se encuentra fijada por gran Bretaña, Estados

Unidos y Holanda.

La contabilidad se define en base a sus usuarios, en este caso los inversionistas y

los proveedores.

Los países que integran este modelo, tenemos: Australia, Bahamas, India,

Irlanda, Islas Caimán, Pakistán, Puerto Rico, Israel, Sudáfrica, Venezuela,

Filipinas, Canadá, Inglaterra, Holanda, Estados Unidos y México

MODELO CONTINENTAL

En su mayoría se integran países de Europa y Japón

Aquí se mantienen lazos estrechos con los bancos, los cuales proveen el Capital

necesario y el Sistema Contable

Se enfoca a satisfacer las necesidades de información del gobierno y los bancos,

en cumplimiento de políticas macroeconómicas.

Los países que integran este modelo son: Alemania, Austria, Egipto, España,

Francia, Italia, Japón, Marruecos, Senegal, Suecia y Suiza.

MODELO SUDAMERICANO

Incluye a la mayoría de naciones de América del Sur

Principalmente se enfocan al manejo contable de la inflación, la contabilidad esta

orientada a planes del gobierno y prácticas establecidas en las empresas.

Los países que conforman este modelo son: Argentina, Bolivia, Brasil, Chile,

Ecuador, Perú y Uruguay.

BASES PARA LA PRESENTACIÓN Y REVELACIÓN DE INFORMACIÓN

NIF: La NIF A-3 “Necesidades de los usuarios y objetivos de los estados

financieros” (“NIF A-3”)

Requiere la presentación de un “Estado de Resultados” y la utilidad integral se

presenta en el Estado de variaciones en el capital contable, según el Boletín B-4

“Utilidad Integral” (B-4).

En diciembre de 2011 el Consejo Emisor del CINIF aprobó la NIF B-3 Estado de

resultado integral la cual entra en vigor a partir del 1 de enero de 2013 – Esta NIF

establece la presentación de la utilidad integrales (en uno o dos estados

financieros) por lo que con dicho cambio se elimina esta diferencia.

2. RECONOCIMIENTO DE LOS EFECTOS DE LA INFLACIÓN

De conformidad con la IAS 29 “Financial Reporting in Hyperinflationary

Economies” (“IAS 29”), los efectos de la inflación en la información financiera se

reconocerán en los estados financieros de una entidad cuya moneda funcional sea

la moneda de una economía hiperinflacionaria

Uno de los parámetros másrelevantes a considerar para que una economía sea

considerada como hiperinflacionaria, es cuando la inflación acumulada de tres

años se aproxima o es superior al 100%. [IAS29.3].

NIF: Para fines de la NIF B-10 “Efectos de la Inflación” (“NIF B-10”)

Los efectos de la inflación en la información financiera deben reconocerse al

momento en que el ambiente económico de la entidad se reconoce como

inflacionario

la inflación acumulada de los tres años fiscales anteriores es igual o mayor a 26%.

Por lo tanto, los efectos de la inflación en la información financiera se reconocen

con un nivel de inflación menor que cuando se aplica la IAS 29.

ACTIVO INTANGIBLE

Un activo identificable, de carácter no monetario y sin apariencia física

Ejemplos de activos intangibles: programas informáticos, patentes, derechos de

autor, películas, listas de clientes, licencias y permisos, cuotas de importación,

franquicias.

Respecto al criterio de amortización, observamos la ausencia de homogeneidad

en el período establecido.

Las regulaciones de los diferentes países establecen como periodo de

amortización la vida útil del bien, señalando la normativa argentina, chilena y

mexicana un período máximo de veinte años

En Brasil se reduce a diez.

EjercicioS

Consolidación

La CIA. “C” posee el 85% de las acciones de CIA. “Y”. La CIA. Controladora pago exactamente el valor contable de las acciones cuando adquirió las de las subsidiarias. A continuación se presentan la información financiera de las dos compañías:

Se pide:

1.-Asientos de eliminación de inversión en acciones

2.-Contabilización del interés minoritario

3.-Estados de resultados individuales y consolidados

4.-Estados de utilidades retenidas consolidado

5.-Balance Consolidado

6.-Compruebe el saldo de la cuenta de participación de las utilidades retenidas de la subsidiaria.

Concepto CIA “C” CIA “Y”Ventas 350000 180000Costo de ventas 240000 103400Gastos de ventas 43660 30320Gastos de administración 29840 28080Participación en la subsidiaria 15470 0Utilidades retenidas al 1 de enero 61550 26400Dividendos pagados 20000 8000Efectivo 26990 11840Cuentas por cobrar 40720 24240Inventarios 55100 48320Inversión en acciones de la subsidiaria 90610 0Activos fijos 80600 77500Depreciación acumulada 38700 25000Cuentas por pagar 62000 30300Capital social 100000 70000

Ejercicio

La sociedad anónima Guerra a obtenido un préstamo al 1 de Junio 2013 en dólares.

Un préstamo de Citibank por 10000dolares a reembolsarse en 2 años único vencimiento, interés 11% anual y liquidación semestral los dias:

31 de Diciembre $13.5

31 de Enero $13.6

31 de Diciembre $13.7

31 de Enero $13.8

Elaborar asientos contables

-----------------------------------------------------1--------------------------------------------------------------Bancos $130000

Doc. Por pagar(Citibank) $130000Préstamo de Citibank

-----------------------------------------------------2--------------------------------------------------------------Intereses $28600

Doc. Por pagar(Citibank) $28600Registro de intereses

-----------------------------------------------------3-------------------------------------------------------------- Doc. Por pagar(Citibank)

$33750

Bancos $33750

Ejercicio 1 Apott S.A.

La empresa de laboratorios Apott S.A. ha iniciado en 2X09 el proyecto denominado antivirus con el objetivo de elaborar una vacuna que logre la inmunización contra el virus. La empresa cuenta con los medios humanos, materiales y equipos para desarrollar dicho proyecto.

La primera fase es propia de investigación para descubrir posibles antigenos, ya que las mezclas de fármacos retrovirales no logran alcanzar la eliminación del virus

La etapa de desarrollo se inicia en marzo del 2011 cuando se logra aislar al antigeno tras pruebas realizadas en roedores con bastante éxito y se opta por dicho antigeno

A la vista de los análisis técnicos y del proyecto , la gerencia de la empresa considero desde el inicio del ejercicio 2011 existían razones suficientes para asegurar el éxito científico del proyecto que existían recursos suficientes para iniciar la explotación y en cuanto al éxito económico-comercial y su distribución que no iban a existir dificultades ya que los grandes distribuidores mayoristas se han ofrecido para suministro.

EUROSConcepto 2009(I) 2010(I) 2011(I) 2011(D) 2012(D)Consumo de Mat. Div. 100 130 40 95 100Gto. De personal 400 400 120 360 520Serv. Exteriores 40 45 15 30 30Amort. De Inmov. Mat. 20 20 5 25 30Amort. De act. Intang.(patente) 60 60 15 45 60Gtos por reg. De mueva patente

0 0 0 0 6

Total 620 655 195 555 746

Elaborar el tratamiento de los gastos incurridos en cada uno de los periodos descritos

-----------------------------------------------------1--------------------------------------------------------------Gtos de desarrollo 127500 euros

Trab. Realizados por inm. Intan. 127500 euros

Por los gastos de investigación del año 2009 y 2010

-----------------------------------------------------2--------------------------------------------------------------Gtos de desarrollo 19500 euros

Trab. Realizados por inm. Intan 19500 eurosPor los gastos de los 3 meses de investigación

-----------------------------------------------------3--------------------------------------------------------------Propiedad industrial(patente)

130100 euros

Gtos de desarrollo 130100 eurosDesarrollo de la patente antivirus

-----------------------------------------------------4--------------------------------------------------------------Trabajos realizados 147000 euros

Bancos 147000 eurosPor los gastos incurridos por la patente

Ejercicio Caso 2 El corral

Una empresa petrolera inicia la exploración de un pozo petrolífero denominado “el sitio” en el año 1987. La exploración es una fase de “investigación” que implica costosos estudios y otras erogaciones

El pozo “el corral” inicio su fase de exploración (investigación) en 1980, pero para 1987 ya esta en fase de desarrollo porque se encontraron “reservas probadas”, es decir se tiene suficiente evidencia y seguridad razonable de que se producirán ingresos en forma de beneficios económicos futuros sobre las cuales la compañía tendrá el control. Por esta razón, algunas erogaciones del pozo “el corral” se podrán capitalizar aunque aun no se estén produciendo los ingresos respectivos

Un ingeniero que trabaja en la compañía devenga $10 millones de pesos mensuales

El 80% de su tiempo lo dedica al pozo “El sitio” el 10% al pozo “el corral” y el otro 10% a labores administrativas

Los pagos a proveedores por concepto de compra de facilidades fueron de $20000. Estos recursos se midieron confiablemente mediante una distribución de los costos de manera que se determino que para el pozo “el sitio” se usaría el 70% de tales facilidades y el 30% para el pozo denominado “el corral”

En Colombia el registro podría hacerse la columna cuenta puede variar según el sector o país, no es importante.

-----------------------------------------------------1--------------------------------------------------------------Gtos administrativos $1000000Activo intangible”El sitio” $8000000Activo intangible”El corral”

$1000000

Obligaciones laborales por pagar

$1000000

Por $10000000 que se devengan mensualmente por el “sitio y el corral”

-----------------------------------------------------2--------------------------------------------------------------Activo intangible”El sitio” $14000000Activo intangible”El corral”

$6000000

Bancos $20000000Pago a proveedores

-----------------------------------------------------3--------------------------------------------------------------Obligaciones laborales por pagar

$10000000

Bancos $10000000Pago de obligaciones laborales

Ejercicio Caso 3 Cristodopoulos SHA.

La empresa armadora Cristodopoulos S.A., a adquirido un buque de nombre “Egeo” construido por astilleros novanta S.A. siendo el coste de adquisición 6000000 euros

La propia empresa constructora Astilleros Novanta comunica que debe someter el buque a una gran reparación consistente en neutralizar la futura corrosión con una secuencia de 5 años. El costeo que se supondría dicha gran reparación en el momento de “botar” el buque o momento inicial ascendería a 900000 euros

Fecha de inicio de la actividad 01-01-2X10

La empresa armadora aplica como criterio de amortización el lineal. La vida útil de buque se estima en 40 años. No se prevé ningún valor residual ni costeos futuros a asumir por desguace

Se pide:

Contabilizar los asientos hasta la fecha de la realización de la reparación teniendo en cuenta que en 30-06-2X014 el barco ataca en los astilleros para acometer la gran reparación y revisión ya que se han detectado desperfectos en el casco y la cubierta que merecen ser subsanadas sin mas demora.

-----------------------------------------------------1--------------------------------------------------------------Inmovilizado (Buque) 6000000 euros

Bancos 6000000 eurosAdquisición del buque “El GEO”

-----------------------------------------------------2--------------------------------------------------------------Amortización 127500 euros

Amortización acumulada 127500eurosRegistro de amortización

-----------------------------------------------------3--------------------------------------------------------------Inmovilizado (Buque) 900000 eurosIVA acreditable 144000 euros

Bancos 1044000 eurosReparación de Buque

-----------------------------------------------------4--------------------------------------------------------------Amortización 200000 euros

Amortización acumulada 200000 eurosRegistro de amortización de reparación

ENGLISH

SALON POLICIES

• Punctuality

• Respect my teacher and classmates

• No cell phones or headphones (if I grip the master me to finish it off and class

period you back me in presence potatoes or husband)

• No gum or candy or anything like it (if I commit myself handle the next day bring a

bag of almond kisses to distribute to my classmates)

• No bad words (if I grip me impose a sanction that it deems necessary).

• Commitment to teamwork

• no hats Men well groomed nails

• Women clean well groomed nails

Evaluation Criteria

Examination 50%

Task 10%

Teamwork. 40%

Teamwork will be delivered a week before the end of the period to the next.

features:

In a Usb Arial 14 for title display sheet text Arial 12 Normal Normal line spacing

justified without spelling mistakes and in a sealed envelope.

Unit 1

International Financial Reporting Standards

1.1 Background

1.2 Countries that have already adopted IFRS

1.3 Who are required

1.4 From when applied IFRS

1.5 Who obligation issued in Mexico

1.6 Requirements to adopt IFRS in Mexico

1.7 Who regulates internationally IFRS

1.8 Accounting policies according to IFRS

1.9 Current status of IFRS

unit 2

Transition from FRS to IFRS

2.1 Adoption of FRS

2.2 Who are required

IFRS 2.3 . First-time adoption of FRS

2.4 Implications of the opening balance sheet under IFRS

2.5 Business combinations and scope of consolidation of financial statements

2.6 Consolidation and revelation in the first financial statements under IFRS

Unit 3

International norms and standards for registration and presentation of financial

information

3.1 Introduction

3.2 Characteristics of international accounting

3.3 Rules and principles of international accounting

3.4 Basic Financial Statements

3.5 Case Studies

unit 4

Registration of foreign currency transactions

4.1 Introduction

4.2 Techniques of registration, foreign currency

4.3 Different types of foreign currency exchange

4.4 Case Studies

Unit 5

Problems of international accounting practices in reporting and recording around

the world

5.1 Introduction

5.2 Reporting Practices and registration on goodwill, intangible assets , transfer

pricing and operated by area

unit 6

Analysis of the financial statements and comparability of information between

countries

6.1 Introduction

6.2 Measures for compliance with Japanese companies

6.3 Application of International Financial Reporting Standards in the United States,

Japan and the UK

6.4 Case Studies ( the use of financial statements in English are requested )

Unit 1

International Financial Reporting Standards

1.1 Background

Due to the changes that have occurred around Globalisation making the world just

an electronic global village , where everything is interconnected through a global

network , and is therefore in the United States, characterized as economic power

where large companies , many of them listed on the stock exchange , presenting a

dispute mismanagement that is given to the financial information for particular

purposes of certain groups , because there is no standard rule concentrate

regulating the accounting practice worldwide.

1.2 Countries that have already adopted IFRS

IFRS are used in many parts of the world, including the European Union , Hong

Kong , Australia , Malaysia, Pakistan , India, Panama , Guatemala , Peru , Russia,

South Africa , Singapore and Turkey is included . At March 28, 2008 , about 75

countries forced to use IFRS, or part thereof . Many other countries have decided

to adopt the rules in the future, either by direct or by adapting national laws of the

various countries application.

Since 2002 there has also been a rapprochement between the IASB " International

Accounting Standards Board and the FASB " Financial Accounting Standards

Board " , in charge of the development of accounting standards in the United

States to try to harmonize international standards with U.S. . In U.S. publicly traded

entities will be able to choose whether present their financial statements under

U.S. GAAP (the national standard) or low NICs.

1.3 Who are required

Large - traded companies , captan and place resources

- When your parent or subsidiary apply full IFRS

- When imports and exports over 50% of operations

1.4 A calving when IFRS are applied

Do not expect the date to begin the planning phase of adoption, because the

requirement to submit annual accounts to international standards is set in 2013 ,

these include comparative information.

so that at least internal purposes will be necessary to advance one year of the NIC

1.5 Who issued the obligation

The Mexican Council of Financial Reporting Standards

1.6 Requirements to adopt IFRS

Management should be aware that the adoption and initial implementation of IFRS

should be seen as a process or project which must be properly planned and

managed . The implementation of IFRS should not be conceived as a simple

change of wave accounts Catalog developing a new accounting manual. On the

contrary it is a project that involves making strategic decisions by management of

the adopting entity in which dates and specific activities should be established

1.7 Who regulates internationally IFRS

The International Council (United States, Canada and Europe)

1.8 Accounting policies according to IFRS

Policies are in accordance with the principles freely conventions, rules and

practices applied by an entity in preparing and presenting financial statements.

UNIT II

PROCESS OF TRANSITION TO IFRS NIF

2.1 ADOPTION OF IFRS

It is a process of global application , in other words , a trend that involves the

globalization of the accounting profession, view the paradigm of removing borders

in terms of service delivery.

2.2 WHO ARE REQUIRED

Full IFRS ( Group 1)

Large publicly traded companies and pick and place resources. When its parent or

subsidiary apply full IFRS as imports and exports over 50% of operations.

IFRS for SMEs ( Group 2)

Large companies that are not in Group 1 Each micro small and medium

enterprises.

2.3 First time adoption of IFRS

Is IFRS A-1 which speaks of the first time adoption .

The opening balance sheet under IFRS an entity is the starting point for its

accounting under IFRSs

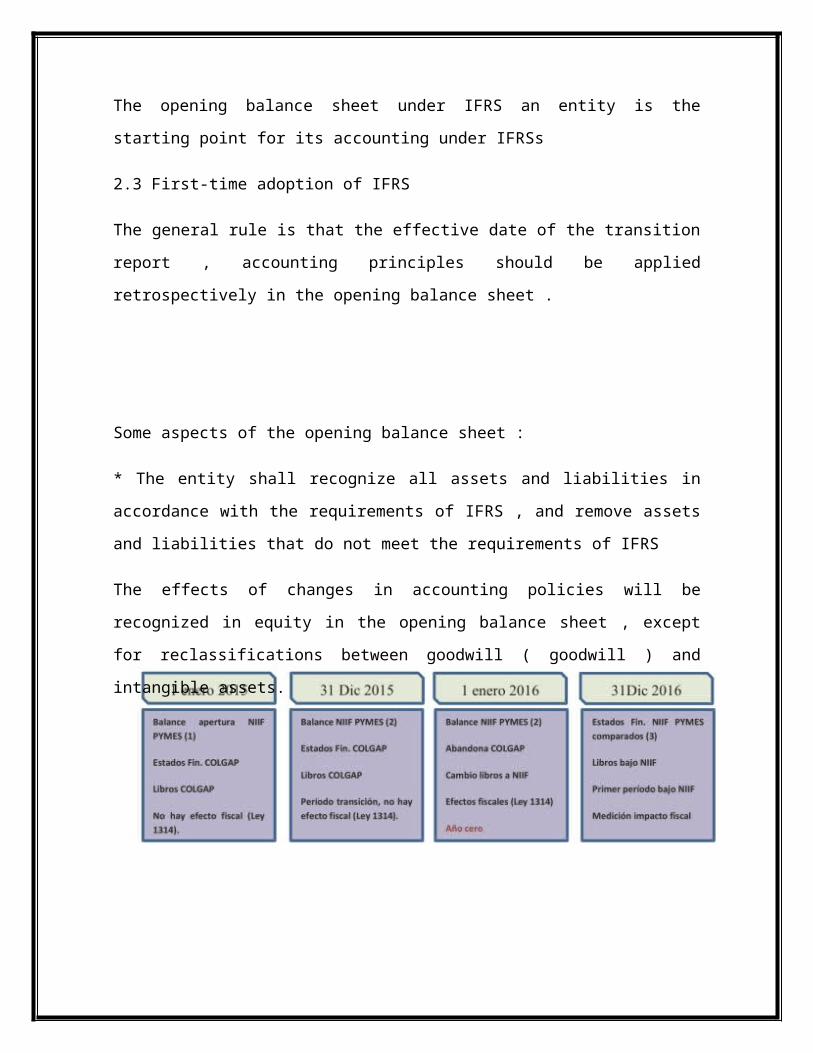

2.3 First-time adoption of IFRS

The general rule is that the effective date of the transition report , accounting

principles should be applied retrospectively in the opening balance sheet .

Some aspects of the opening balance sheet :

* The entity shall recognize all assets and liabilities in accordance with the

requirements of IFRS , and remove assets and liabilities that do not meet the

requirements of IFRS

The effects of changes in accounting policies will be recognized in equity in the

opening balance sheet , except for reclassifications between goodwill ( goodwill )

and intangible assets.

* IFRS 1 expands the disclosure requirements compared to the first adoption

requirements previously included in the international accounting standards ,

specifically the interpretation SIC-8 First-time Application of IASs as the Primary

Basis of Accounting .

2.4 IMPLICATIONS OF BALANCE BY OPENING IFRS

OPENING BALANCE AS IFRS

Companies should prepare an opening balance sheet under IFRS on " the date of

transition to ifrs " s the starting point for the subsequent application of accounting

ifrs

No need to post the opening balance sheet in the first financial statements

following the niiff the initial balance of the first period for which full comparative

information is presented in accordance with IFRS.

example:

When a company prepares its first financial statements for the year ended

December 31, 2005 with comparative year, the date of transition to IFRSs would

be 1 January 2004 and the opening balance sheet under IFRS are prepared on

that date.

A company required to present two years of full comparative information should

prepare an opening balance sheet on 1 January 2003.

Includes all assets and liabilities that are required in the ifrs .

Excludes any assets and liabilities that are not allowed under ifrs .

Classify all assets , liabilities and equity in accordance with IFRS; and check all

items according to ifrs .

DATE OF ADOPTION

The date of adoption of a company is the financial year beginning 1 whose

financial statements are prepared under IFRS for the first time .

Adjustments made as a result of adopting IFRS for the first time are recorded in

retained earnings or other equity account .

IMPLICAIONES IN THE OPENING BALANCE SHEET

The preparation of the opening balance sheet under IFRS may appeal the

calculation or collection of information that was not calculated or was collected

under previous GAAP for the company. in the early stages , companies should

plan their transition and identify the differences between IFRS and previous

GAAP , in order to collect all the required information.

IFRS 3 Business Combinations.

The objective of this IFRS is to improve the relevance, reliability and comparability of the information about business combinations and their effects, that a reporting entity provides in its financial statements through.

Is carried out by establishing principles and requirements for how an acquirer:

(a) recognizes and measures in its identifiable assets acquired, the liabilities assumed and any noncontrolling interest in the acquiree financial statements.

(b) recognizes and measures the goodwill acquired in the business combination or a gain from a bargain purchase conditions.

( c ) determines what information to disclose to enable users of financial statements to evaluate the nature and financial effects of the business combination .

Any classifications or designations made in recognizing these items must be in accordance with the contractual terms , economic conditions, financial and operating policies of the acquirer and other factors that exist at the date of acquisition.

Each identifiable asset and liability is measured at fair value at the date of acquisition. Any non-controlling interest in an acquiree is measured at fair value or as the share of non-controlling share of the net identifiable assets acquired .

IFRS provides limited exceptions to these recognition and measurement principles of exceptions:

( a) Leases and insurance is required to be classified on the basis of the contractual terms and other factors at the inception of the contract (or when the terms have changed ) rather than on the basis of the factors exist in the acquisition date .

( b ) Only those contingent liabilities assumed are recognized in a business combination that are a present obligation and can be measured reliably.

( c) requires that certain assets and liabilities are recognized and measured in accordance with other IFRSs , rather than at fair value.

( d ) There are special requirements for measuring a reacquired right .

( e) Indemnification assets are recognized and measured on a basis that is consistent with the indemnified item , even if the measure is not fair value .

IFRS requires the acquirer , having recognized the identifiable assets , liabilities and non-controlling interests , identify any difference between:

The sum of the consideration transferred, any noncontrolling interest in the acquiree in a business combination achieved in stages, the fair value of the acquisition date the acquirer's previously held equity of the acquiree.

( b ) the net identifiable assets acquired.

IFRS 1 First-time adoption

When first-time adopters , international financial reporting standards IFRS , the company needs to perform a series of actions such as a comparative analysis of the financial statements.

If a company needs to deliver its financial statements under IFRS or IFRS with at December 31 , then you need to prepare the following information:

Opening balance sheet under IFRS on January 1

Balance as of December 31 IFRS , income statement , cash flow statement , statement of changes in equity.

Comparative balance with the previous year.

The first financial statements under IFRS are the first annual financial statements in which the entity adopts IFRSs, by an explicit and unreserved statement in those financial statements of compliance with IFRS.

An entity shall use the same accounting policies in its statement of financial position opening IFRS and throughout all periods presented in its first financial statements under IFRS . these accounting policies shall comply with each IFRS effective at the end of the first reporting period under IFRS report

UNIDAD3

INTERNATIONAL STANDARDS AND PRINCIPLES FOR REGISTRATION AND PRESENTATION OF ACCOUNTING INFORMATION

The Generally Accepted Accounting Principles ( GAAP ) and Financial Reporting Standards known as ( GAAP ) are a set of general rules and regulations that serve to formulate accounting guidance related to the measurement of assets and information criteria of assets and economic of an entity. GAAP are parameters for

the preparation of the financial statements is based on uniform methods of accounting techniques .

Were approved at the 7th Inter Accounting Conference and 7th National Assembly of Graduates in Economics , held in Mar del Plata in 1965.

The principles of " double entry " is an accounting principle established by Fra Luca Pacioli (1445-510 BCE) in 1494.

His basic statement says .

A debit one or more accounts are always one or more accounts payables for the same amount .

At all times the sums must be equal to the credit.

Losses are debited and credited earnings .

The assets of the entity is different from his / owner / s s .

The principle of the resources of a body is equal to the value of units levied on him.

Equity components and the causes of their results are represented by accounts that are recorded notes or settle the variations to the concept they represent.

The balance of an account is the monetary value of the same at any given time. This balance is modified each time an operation has no effect on the components it represents.

The asset accounts and expense are debtors, and liabilities , profit and net assets are creditor .

Throughout annotation ( seat) , whatever the number of debits and credits , the sum of the balances should be equal .

To unregister an amount previously registered, register the account should be that it represents and the amount should be the same previously registered

. Entire account has 2 sections: MUST AND HAVE .

INTERNATIONAL FINANCIAL REPORTING STANDARDS

When we speak of IFRS we are referring to:

SIC NIC + + + IFRS IFRIC

IAS (International Accounting Standards ) = IAS ( International Accounting Standards )

IFRS (International Financial Reporting Standards) = IFRS (International Financial Reporting Standards )

SIC ( Standards Interpretation Committee ) = Interpretations Committee IAS

IFRIC (International Financial Reporting Interpretation Committee ) = IFRIC

( Interpretations Committee International Financial Reporting Standards )

Features of International Standards

Financial Reporting Standards ( IFRS / IFRS )

It is a comprehensive legislation that provides systemic models for the generation of user information

They are based on the reliability of the data, regardless of the valuation methods and the quality of information

No regulatory (as are U.S. GAAP )

The freedom of interpretation is a risk factor in our accounting culture.

Away from tax concepts it is purely financial .

CHARACTERISTICS OF INTERNATIONAL ACCOUNTING

This is mainly due to accounting transactions of multinational companies as they manage their resources worldwide .

Much has been written about the multinational nature of today's global economy . Example companies are: coca cola , Toyota, etc. .

The first appearance of a company in the field of International Accounting usually occurs as a result of import and export (two important activities that are occurring around the world ) .

A complication at present for handling international accounting, the language , and that the financial statements are prepared using the dominant language in this country, that is why many companies ask support to lending institutions and specialized agencies.

RULES AND PRINCIPLES OF ACCOUNTING

The Committee on Accounting Principles and Standards aims analysis and issuance of the Accounting Standards , ie , Technical Bulletins and Financial Reporting Standards . Also, representing the Association of Accountants in social destine instances , and compared with national and international regulatory agencies .

The Commission is composed of 11 collegiate members , including professors from various universities , partners and exsocios major audit firms , representatives of the Confederation of Production and Trade included.

The International Accounting Standards IAS are a set of standards that establish the information should be presented in the financial statements and how this information should appear , in those states.

These principles have been developed taking into account the basic tenets or principles for financial accounting information to achieve the aim of being useful when making decisions , are divided into three categories :

Assumptions derived from the economic environment : entity , emphasis on the economic aspect , quantification and measurement unit

General principles should gather information: objectivity , materiality , comparability, and sufficient revelation.

Principles that form the basis for quantifying the operations of the entity and economic events that affect it : historical cost , economic duality , a going or continuity, accounting embodiment accounting period and conservatism.

The rules are known by the acronym IAS and IFRS depending on when they were approved and qualify through the "interpretations"

BASIC FINANCIAL STATEMENTS

What are they?

The financial statements , also called financial statements, financial reports or annual accounts , reports are used by institutions to publicize the economic and financial situation and the changes in it at a certain date or period.

target

The objective of financial statements is to provide information on the assets of the issuer as of a date and its economic and financial developments in the period covered , to facilitate economic decision making .

Qualitative characteristics of financial statements :

BALANCE SHEET

The statement of financial position, also called the statement of financial position or balance sheet shows on particular date on resources and financial obligations of the entity: so therefore the assets by their availability, revealing its restrictions; liabilities according to their enforceability, revealing their financial risks and stockholders' equity on that date

Active: A controlled entity, identified and quantified in monetary terms resource, which are reasonably expected future economic benefits arising from transactions occurred in the past, which have affected the entity financially

Liabilities: It is a virtually inescapable present obligation identified, quantified in monetary terms, which represents a decrease of future.

economic benefits derived from operations that occurred in the past that have affected the entity

Stockholders' equity: The residual value of the assets of the entity after deducting all of its liabilities.

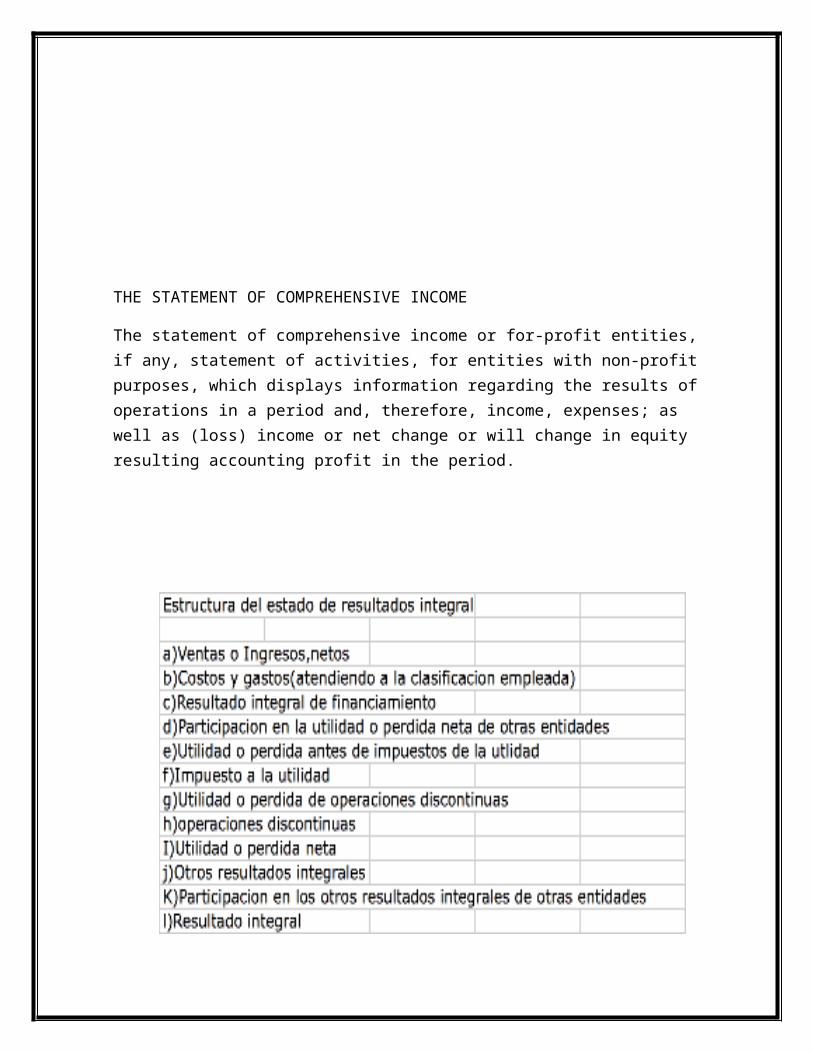

THE STATEMENT OF COMPREHENSIVE INCOME

The statement of comprehensive income or for-profit entities, if any, statement of activities, for entities with non-profit purposes, which displays information regarding the results of operations in a period and, therefore, income, expenses; as well as (loss) income or net change or will change in equity resulting accounting profit in the period.

THE STATEMENT OF CASH FLOWS

The cash flow statement or, where appropriate, the statement of changes in financial position, indicating about changes in resources and funding sources of the entity for the period, classified by activity, operating, investment and financing

Operating activities are those that are the main source of income for the entity

Investing activities are those related to the acquisition and disposition of: property, plant and equipment and intangible assets other assets intended for use in the production of goods or the provision of services.

Financing Activities: They are related to the procurement, as well as the remuneration and reimbursement of funds from: the owners of the entity funding grantors creditors unrelated to the normal operations of providing goods and services.

THE STATEMENT OF CHANGES IN STOCKHOLDERS 'EQUITY

The statement of changes in stockholders' equity, in the case of nonprofits, which shows changes in the investment of the owners during the period, and are made up of the following basic elements:

-Movements owners

-Movements of reserves

-Comprehensive income

UNIT IV. LOG IN FOREIGN CURRENCY TRANSACTION .

INTRODUCTION

FOREIGN CURRENCY :

Or foreign currency , currency refers to notes and coins of foreign countries. It is different to any registration , the functional or reporting entity in the circumstances currency.

Currency Registered: is one to which the entity maintains its accounting records , whether for legal purposes or information.

Reporting currency : that is chosen and used by an entity to present its financial statements .

Functional currency is the one with which an entity operates in its economic environment.

Exchange rate is the ratio for exchange of two currencies at a certain date.

Spot exchange rates : is used in transactions with immediate delivery.

Exchange rate at the end :

Is cash at

Balance sheet date .

Historical exchange rate : the cash at transaction date.

Monetary items are those that are expressed in nominal monetary units without reference to future prices of certain

goods or services.

Non-monetary items : those whose nominal value varies

with the movement of inflation.

Fair value : the amount of cash or cash equivalents that market participants would be willing to exchange for the sale of an asset or transfer a liability .

Who should make the registration of foreign currency transactions ?

All those companies that transact in foreign currency.

Among the foreign currency transactions include:

a) buy or sell goods or services whose price is denominated in foreign currency.

b ) borrows or lends funds when the amounts are established receivable or payable in foreign currency; or

Acquires or disposes of assets, or incurs , transferred or settles liabilities, these transactions have been denominated in foreign currency.

All foreign currency transaction should be recognized initially in the recording currency using the historical exchange rate .

The date of a transaction is one in which such transaction is chargeable and meets the conditions for recognition under FRS .

A closing date of the financial statements balances monetary items arising from transactions in foreign currencies are translated at the closing rate. Also the date of completion ( receipt or payment ) of such transactions.

The difference in changes should be recognized as income or expense in profit

or net loss in the statement of comprehensive income .

TECHNICAL REGISTRATION AND FOREIGN CURRENCY CONVERSION

Conversion involves transforming , or move restate financial statements originally made in a currency A in another currency B.

A conversion is a re monetary expression in which: the object ( what is expressed ) is a measurement currency of origin; the product is a measurement (equivalent to the previous one) in a currency conversion ; the second measurement is obtained from the first and some sort of change that indicates the number of units of the currency of origin which can change a unit of currency conversion , or vice versa.

foreign operations

A foreign subsidiary is an entity whose activities are conducted in a country with a currency other than the currency of the reporting entity . NIF B -15 establishes that the financial statements of such entities must be converted to the reporting currency , so that must be addressed as follows:

Conversion process :

1. Turning recording currency to the functional currency.

Two . Converting the functional currency to the reporting currency .

1.- Conversion of recording currency to the functional :

Monetary assets and liabilities . TC end .

Monetary assets and liabilities and stockholders' equity . Historical TC .

Revenues , Costs and Expenses . Historical TC .

Differences in changes. Should be recognized as income or expense in the RIF in the income statement .

2. -Conversion of the functional currency to the reporting :

when the environment is inflationary or not : Variations between equity and investment of the foreign operation are recognized in equity . Conversion of functional currency to the report , when the environment is inflationary :

Assets, Liabilities and stockholders' equity. TC end .

Revenues , Costs and Expenses . TC end .

Variations between equity and investment of the foreign operation should be recognized as a cumulative translation adjustment in stockholders ' equity.

Changes of accounting currency , functional and report :

Exchange log or functional . It should be recognized prospectively from the date of the change .

Currency Exchange report . Should be recognized using the retrospective method according

DIFFERENT TYPES OF FOREIGN CURRENCY EXCHANGE

WHAT IS EXCHANGE ?

The rate or exchange rate is the price of a currency. Now in 2014 , in other words , is the number of units of the national currency to be delivered in a given time , in exchange for one unit of foreign currency ( forex ) .

The birth of a system of exchange comes from the existence of international trade between different countries with different currencies.

Fixed exchange rate : it is rigidly determined by the Central Bank.

Flexible Exchange Rate : determined in a free market by the interaction of supply and demand for currencies.