adci report q1 2016

TRANSCRIPT

sewellsgroup.com

April 2016

sewellsgroup.comPage 1

About Sewells GroupAutomotive Dealer ConfidenceIndex

ADCI Survey Methodology Summary of Respondents

GAUTOMOTIVEDEALERCONFIDENCE

SEWELLS GROUP

INDEXThe automotive industry in India contributes a significant share to country’s GDP. A healthy domestic market, an active involvement of the government, growth of domestic auto manufacturers and presence of global brands in the country have made sure that this industry has come of age. With everything else being executed on a global scale and with global vision, the Indian auto industry also needs a dealer confidence index.

Globally, confidence indices are viewed as reliable precursors to business performance. Such indices aim to capture and quantify the sentiment of various industry stakeholders – be it CXOs, suppliers, vendors or distribution partners who usually are in the middle of the action. People within the industry typically use these indices to get a sense of stakeholder sentiment and optimize their actions in line with the sentiment. Market analysts, on the other hand, interpret theses indices as ‘lead indicators’ of the performance of a particular industry or sector. An accurately constructed index usually demonstrates a high correlation with actual business performance.

Ssewellsgroup.comPage 2

About Sewells GroupAutomotive Dealer ConfidenceIndex

ADCI Survey Methodology Summary of Respondents

In the automotive industry, dealers enjoy a unique position which keeps them close to the customers. They are also in constant touch with factory staff, other dealers, financiers and market intermediaries. Consequently, each dealer has exposure to a plethora of information that in turn shapes his / her views about the future of his business in short / medium term.

The Sewells Group Automotive Dealer Confidence Index (ADCI) captures and quantifies this sentiment from across the length and breadth of the country. The movement of this collective sentiment in the form of an index indicates the direction of the wholesale and the retail sales in the industry. It is published by Sewells India on a quarterly basis.

ADCI allows the stakeholders in the automotive industry to have meaningful conversations well in time, which in turn helps them put together strategies for a superior performance in the market place.

sewellsgroup.comPage 3

About Sewells GroupAutomotive Dealer ConfidenceIndex

ADCI Survey Methodology Summary of Respondents

TThe Sewells Group ADCI is computed on the basis of responses received to a structured questionnaire from the automotive dealers. The questionnaire attempts to capture their sentiment about economy in general and their business in particular on a six month horizon.

As per the design, the ADCI’s range is between -100 and +100, where an index score of -100 represents the most pessimistic outlook, and +100 indicates the most optimistic outlook. The index is based on how dealers see the overall market and their businesses performing in next six months

The Sewells Group tracks the trend of the index which offers an insight into the future direction of the market. We believe that it is the movement of the index that offers greater insights than its absolute value in a particular quarter.

In this ninth edition of the ADCI, we have captured the sentiment of the dealer fraternity at the end of Jan-March quarter of 2016. The findings of this survey are compared with the findings of the previous eight editions to map the trend.

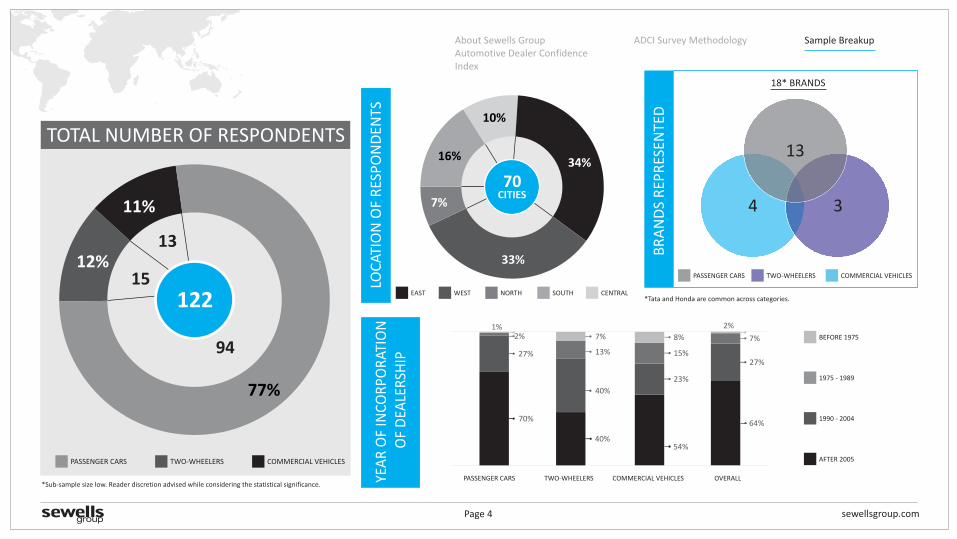

As always, a questionnaire was sent to the automotive dealers across India. A total of 122 responses were received, from dealers, representing 18 brands. These were used to compute the index. Every effort has been made to ensure that the index is meaningful and representative of the dealer sentiment. However, we advise reader discretion in using the results considering the low sample in some cases.

sewellsgroup.comPage 4

ADCI Survey Methodology Sample Breakup

PASSENGER CARS TWO-WHEELERS COMMERCIAL VEHICLES

TOTAL NUMBER OF RESPONDENTS13

34

EAST

PASSENGER CARS TWO-WHEELERS COMMERCIAL VEHICLES

PASSENGER CARS TWO-WHEELERS COMMERCIAL VEHICLES OVERALL

70%

27%

BEFORE 1975

1975 - 1989

1990 - 2004

AFTER 2005

LOC

ATI

ON

OF

RES

PO

ND

ENTS

BR

AN

DS

REP

RES

ENTE

D

18* BRANDS

40%

13%

40%

54%

23%

64%

27%

7%

*Sub-sample size low. Reader discretion advised while considering the statistical significance.

1% 2%

8%

YEA

R O

F IN

CO

RPO

RAT

ION

OF

DEA

LER

SHIP

WEST NORTH SOUTH CENTRAL

2%

About Sewells GroupAutomotive Dealer ConfidenceIndex

34%

7%

16%

10%

70CITIES

33%12%

11%

77%

13

15122

947%

15%

12%

*Tata and Honda are common across categories.

sewellsgroup.comPage 5

AUTOMOTIVEDEALERCONFIDENCE

JAN 16 – MAR 16QUARTER INDIA

INDEX

SEWELLS GROUP

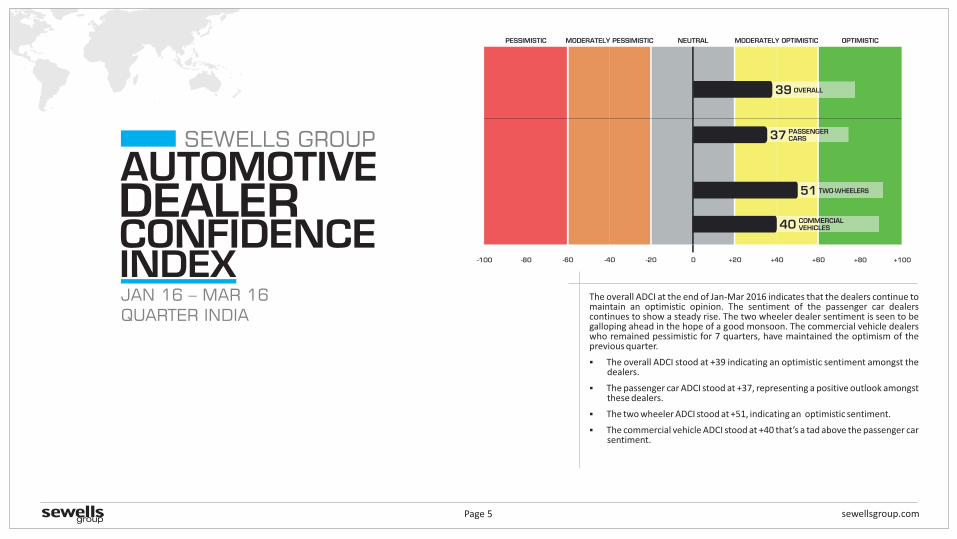

The overall ADCI at the end of Jan-Mar 2016 indicates that the dealers continue to maintain an optimistic opinion. The sentiment of the passenger car dealers continues to show a steady rise. The two wheeler dealer sentiment is seen to be galloping ahead in the hope of a good monsoon. The commercial vehicle dealers who remained pessimistic for 7 quarters, have maintained the optimism of the previous quarter.

§ The overall ADCI stood at +39 indicating an optimistic sentiment amongst the dealers.

§ The passenger car ADCI stood at +37, representing a positive outlook amongst these dealers.

§ The two wheeler ADCI stood at +51, indicating an optimistic sentiment.

§ The commercial vehicle ADCI stood at +40 that’s a tad above the passenger car sentiment.

0-80-100 -40-60 -20 +80 +100+40 +60+20

PESSIMISTIC NEUTRAL MODERATELY PESSIMISTIC MODERATELY OPTIMISTIC OPTIMISTIC

OVERALL

PASSENGERCARS

39

51

37

COMMERCIALVEHICLES40

sewellsgroup.comPage 6

AUTOMOTIVEDEALERCONFIDENCEINDEX-TREND

SEWELLS GROUP

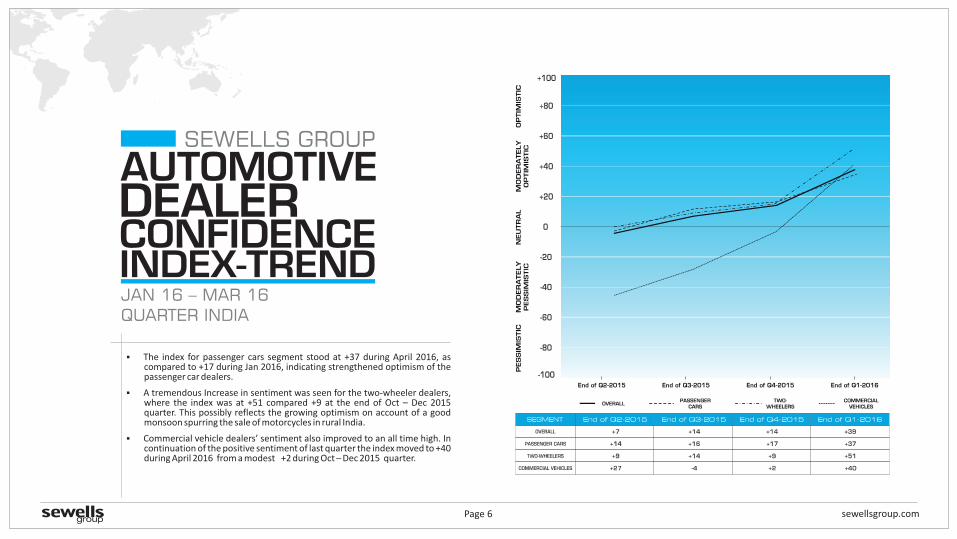

§ The index for passenger cars segment stood at +37 during April 2016, as compared to +17 during Jan 2016, indicating strengthened optimism of the passenger car dealers.

§ A tremendous Increase in sentiment was seen for the two-wheeler dealers, where the index was at +51 compared +9 at the end of Oct – Dec 2015 quarter. This possibly reflects the growing optimism on account of a good monsoon spurring the sale of motorcycles in rural India.

§ Commercial vehicle dealers’ sentiment also improved to an all time high. In continuation of the positive sentiment of last quarter the index moved to +40 during April 2016 from a modest +2 during Oct – Dec 2015 quarter.

JAN 16 – MAR 16QUARTER INDIA

End of Q -2011 6End of Q -20154End of Q -20152 End of Q -20153

sewellsgroup.com

Future view of manpower strength of the business

Expected performance of the market as well as the

dealership over the next six months

Expected levels of sales, inventory and profits over the

next six months

View on the current situation of sales, inventory and profits vis-à-vis same period last year

Impact of the current economic scenario on the

market, as well as the dealership business

View on the current situation of sales, inventory and profits

vis-à-vis previous quarter

Page 7

DETAILED ANALYSIS

The ADCI survey delves into the following areas:

AUTOMOTIVEDEALERCONFIDENCEINDEX

SEWELLS GROUP

§ The following pages carry details of responses received during the ninth edition of the survey for questions covering the above areas.

§ To map the trend, the findings of this survey are compared with the findings of the previous three editions which captured the sentiments of the dealer fraternity in the last three quarters.

§ This section presents the distribution of responses across multiple questions and compared with the findings of the previous surveys.

020403

01Impact of Current Economic Environment on the Local Market

Dealership Performance this Quarter vis-a -vis same Period Previous Year

Impact of the Current Economic Environment on the Dealership

Dealership Performance this Quarter vis-a-vis Previous Quarter

page 8 page 9

page 10 page 13

060807

05Expected Dealership Performance Over Next Six Months Compared to Present Level

Expected Manpower Strength Over Next Six Months

page 18 page 21

Expected Market Performance Over Next Six Months

Overall Expected Dealership Performance Over Next Six Months page 16 page 17

09Dealers Opinion on Odd-Even Plan of Delhi Govt.

page 22

11%

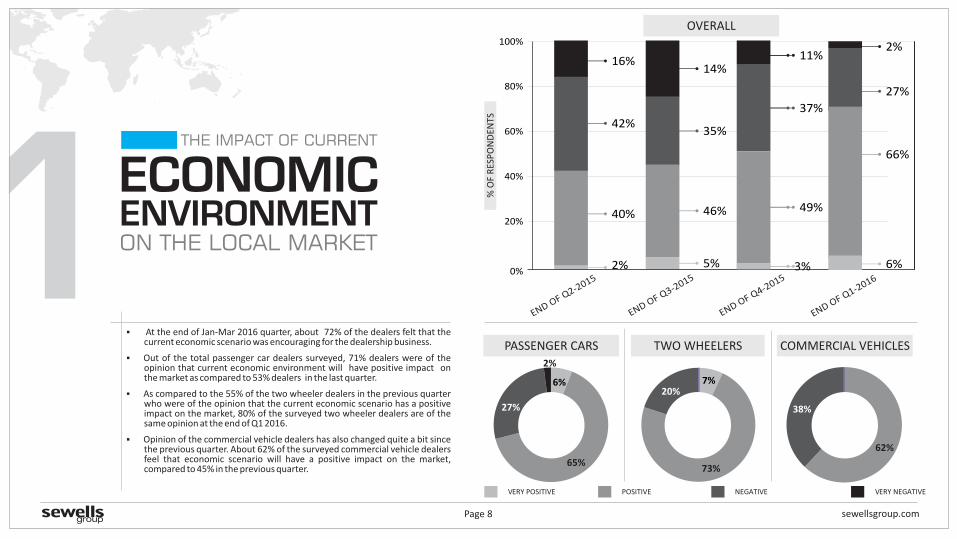

§ At the end of Jan-Mar 2016 quarter, about 72% of the dealers felt that the current economic scenario was encouraging for the dealership business.

§ Out of the total passenger car dealers surveyed, 71% dealers were of the opinion that current economic environment will have positive impact on the market as compared to 53% dealers in the last quarter.

§ As compared to the 55% of the two wheeler dealers in the previous quarter who were of the opinion that the current economic scenario has a positive impact on the market, 80% of the surveyed two wheeler dealers are of the same opinion at the end of Q1 2016.

§ Opinion of the commercial vehicle dealers has also changed quite a bit since the previous quarter. About 62% of the surveyed commercial vehicle dealers feel that economic scenario will have a positive impact on the market, compared to 45% in the previous quarter.

sewellsgroup.com

TWO WHEELERS COMMERCIAL VEHICLES

1VERY POSITIVE POSITIVE NEGATIVE VERY NEGATIVE

0%

20%

40%

60%

80%

100%

% O

F R

ESP

ON

DEN

TS

OVERALL

END OF Q3-2015

END OF Q2-2015

2%

40%

42%

16%

PASSENGER CARS

35%

5%

46%

14%

END OF Q4-2015

37%

49%

3%

Page 8

12% 6%

65%

27%

2%

7%

73%

20%

62%

38%

END OF Q1-2016

27%

6%

66%

2%

ECONOMIC

ON THE LOCAL MARKET

THE IMPACT OF CURRENT

ENVIRONMENT

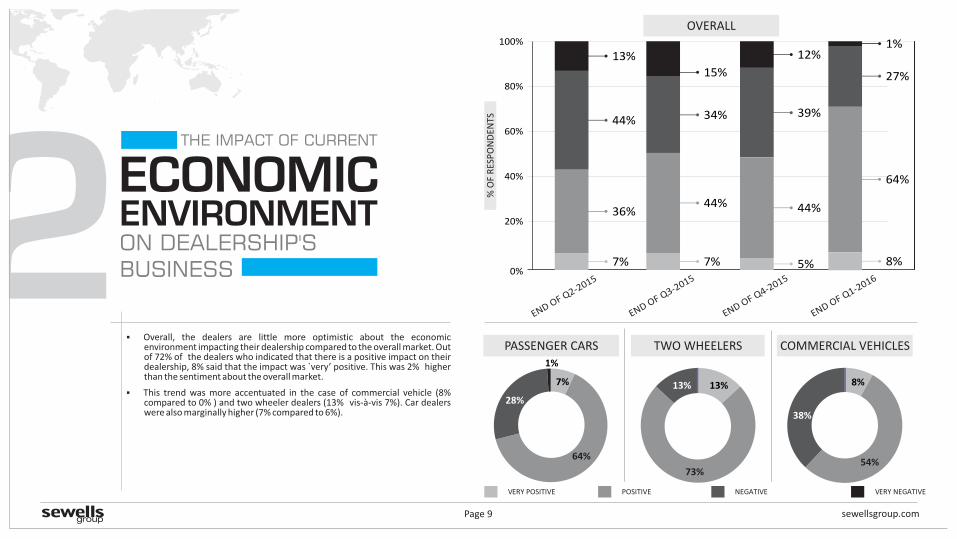

2§ Overall, the dealers are little more optimistic about the economic

environment impacting their dealership compared to the overall market. Out of 72% of the dealers who indicated that there is a positive impact on their dealership, 8% said that the impact was `very’ positive. This was 2% higher than the sentiment about the overall market.

§ This trend was more accentuated in the case of commercial vehicle (8% compared to 0% ) and two wheeler dealers (13% vis-à-vis 7%). Car dealers were also marginally higher (7% compared to 6%).

sewellsgroup.comPage 9

0%

20%

40%

60%

80%

100%

% O

F R

ESP

ON

DEN

TS

OVERALL

7%

36%

44%

13%

TWO WHEELERSPASSENGER CARS

34%

7%

44%

15%

END OF Q3-2015

END OF Q2-2015

END OF Q4-2015

39%

5%

44%

12%

END OF Q1-2016

27%

8%

64%

1%

8%

54%

38%

7%

64%

28%

1%

13%

73%

13%

ECONOMIC

ON DEALERSHIP'S BUSINESS

THE IMPACT OF CURRENT

ENVIRONMENT

VERY POSITIVE POSITIVE NEGATIVE VERY NEGATIVE

COMMERCIAL VEHICLES

sewellsgroup.comPage 10

3PERFORMANCE

YEAR

DEALERSHIP

VIS-À-VIS SAME PERIOD

PREVIOUSSALES INVENTORY PROFITS

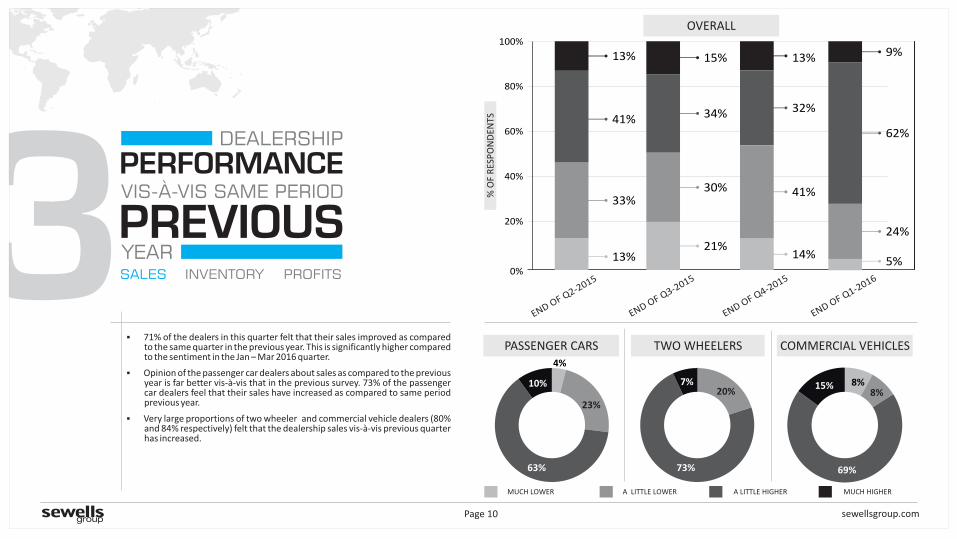

§ 71% of the dealers in this quarter felt that their sales improved as compared to the same quarter in the previous year. This is significantly higher compared to the sentiment in the Jan – Mar 2016 quarter.

§ Opinion of the passenger car dealers about sales as compared to the previous year is far better vis-à-vis that in the previous survey. 73% of the passenger car dealers feel that their sales have increased as compared to same period previous year.

§ Very large proportions of two wheeler and commercial vehicle dealers (80% and 84% respectively) felt that the dealership sales vis-à-vis previous quarter has increased.

COMMERCIAL VEHICLES

MUCH LOWER A LITTLE LOWER A LITTLE HIGHER MUCH HIGHER

0%

20%

40%

60%

80%

100%

% O

F R

ESP

ON

DEN

TS 41%

13%

33%

13%

TWO WHEELERSPASSENGER CARS

34%

21%

30%

15%

END OF Q3-2015

END OF Q2-2015

END OF Q4-2015

32%

14%

41%

13%

8%8%

69%

15%

4%

23%

63%

10%20%

73%

7%

END OF Q1-2016

62%

5%

24%

9%

OVERALL

SALES INVENTORY PROFITS

COMMERCIAL VEHICLES

3PERFORMANCE

YEAR

DEALERSHIP

VIS-À-VIS SAME PERIOD

PREVIOUS

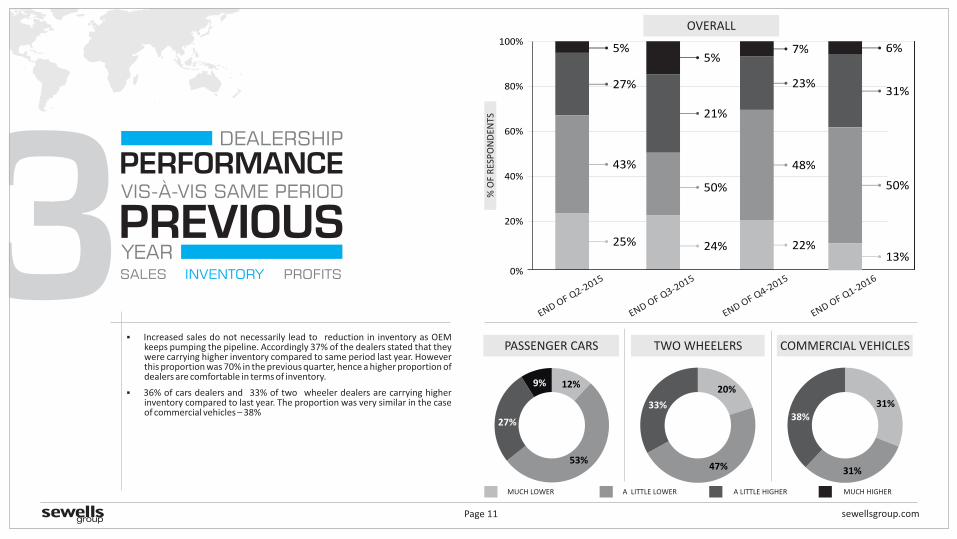

§ Increased sales do not necessarily lead to reduction in inventory as OEM keeps pumping the pipeline. Accordingly 37% of the dealers stated that they were carrying higher inventory compared to same period last year. However this proportion was 70% in the previous quarter, hence a higher proportion of dealers are comfortable in terms of inventory.

§ 36% of cars dealers and 33% of two wheeler dealers are carrying higher inventory compared to last year. The proportion was very similar in the case of commercial vehicles – 38%

sewellsgroup.comPage 11

0%

20%

40%

60%

80%

100%

% O

F R

ESP

ON

DEN

TS

OVERALL

TWO WHEELERSPASSENGER CARS

27%

25%

43%

5%

END OF Q2-2015

21%

24%

50%

5%

END OF Q3-2015

END OF Q4-2015

23%

22%

48%

7%

END OF Q1-2016

31%

13%

50%

6%

12%

53%

27%

9%20%

47%

33% 31%

31%

38%

MUCH LOWER A LITTLE LOWER A LITTLE HIGHER MUCH HIGHER

COMMERCIAL VEHICLES

3PERFORMANCE

YEAR

DEALERSHIP

VIS-À-VIS SAME PERIOD

PREVIOUSSALES INVENTORY PROFITS

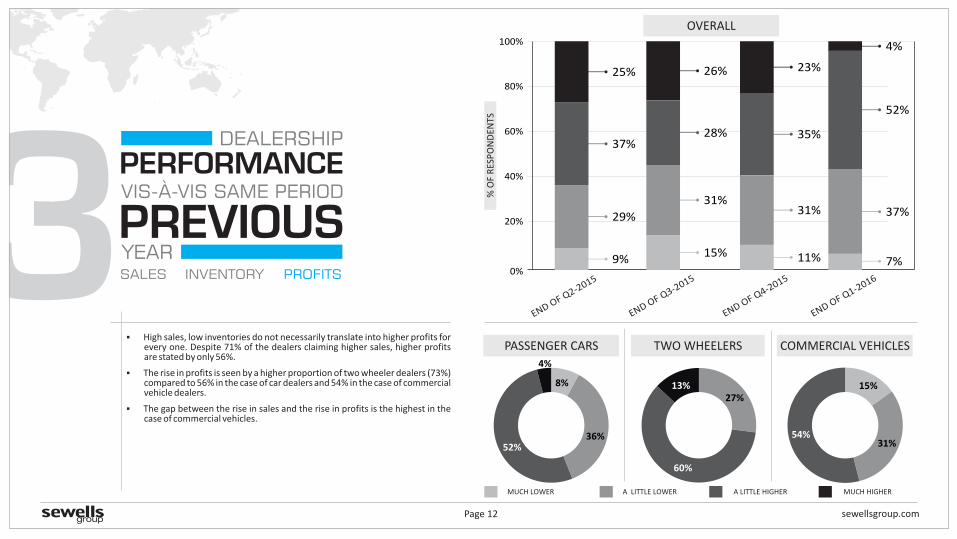

§ High sales, low inventories do not necessarily translate into higher profits for every one. Despite 71% of the dealers claiming higher sales, higher profits are stated by only 56%.

§ The rise in profits is seen by a higher proportion of two wheeler dealers (73%) compared to 56% in the case of car dealers and 54% in the case of commercial vehicle dealers.

§ The gap between the rise in sales and the rise in profits is the highest in the case of commercial vehicles.

sewellsgroup.comPage 12

0%

20%

40%

60%

80%

100%

% O

F R

ESP

ON

DEN

TS

OVERALL

37%

9%

29%

25%

TWO WHEELERSPASSENGER CARS

28%

15%

31%

26%

END OF Q3-2015

END OF Q2-2015

END OF Q4-2015

35%

11%

31%

23%

END OF Q1-2016

52%

7%

37%

4%

8%

36%52%

4%

27%

60%

13% 15%

31%54%

MUCH LOWER A LITTLE LOWER A LITTLE HIGHER MUCH HIGHER

4PERFORMANCE

QUARTER

VIS-À-VIS

PREVIOUS

DEALERSHIP

SALES INVENTORY PROFITS

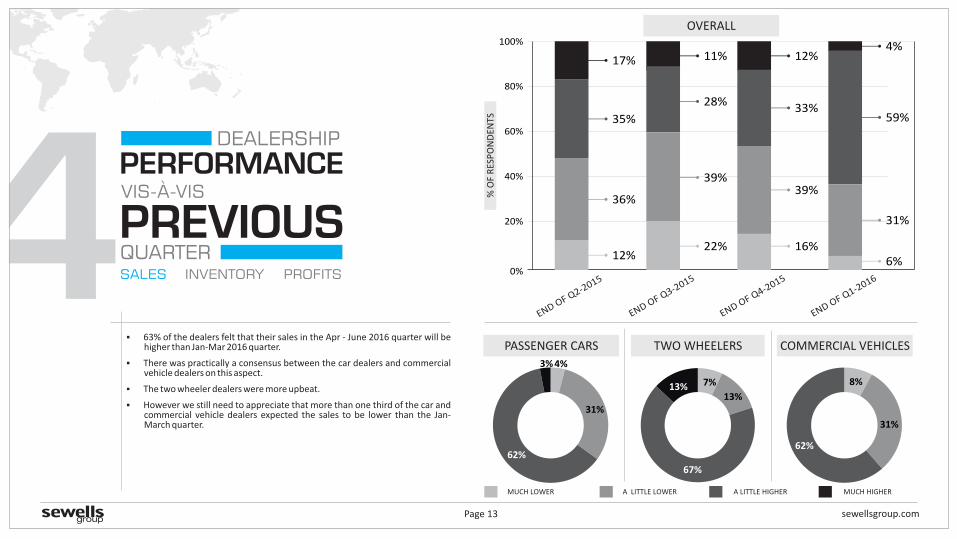

§ 63% of the dealers felt that their sales in the Apr - June 2016 quarter will be higher than Jan-Mar 2016 quarter.

§ There was practically a consensus between the car dealers and commercial vehicle dealers on this aspect.

§ The two wheeler dealers were more upbeat.

§ However we still need to appreciate that more than one third of the car and commercial vehicle dealers expected the sales to be lower than the Jan- March quarter.

0%

20%

40%

60%

80%

100%

% O

F R

ESP

ON

DEN

TS 35%

12%

36%

17%

28%

22%

39%

11%

END OF Q3-2015

END OF Q2-2015

33%

16%

39%

12%

END OF Q4-2015

COMMERCIAL VEHICLES

sewellsgroup.comPage 13

TWO WHEELERSPASSENGER CARS

END OF Q1-2016

59%

6%

31%

4%

4%

31%

62%

3%

7%

13%

67%

13% 8%

31%

62%

MUCH LOWER A LITTLE LOWER A LITTLE HIGHER MUCH HIGHER

OVERALL

COMMERCIAL VEHICLES

sewellsgroup.comPage 14

4PERFORMANCE

QUARTER

VIS-À-VIS

PREVIOUS

DEALERSHIP

SALES INVENTORY PROFITS

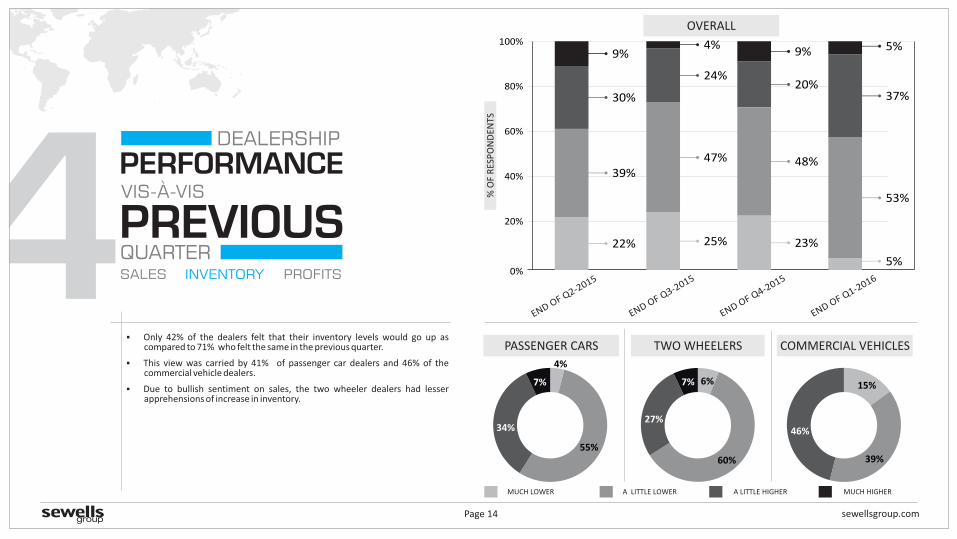

§ Only 42% of the dealers felt that their inventory levels would go up as compared to 71% who felt the same in the previous quarter.

§ This view was carried by 41% of passenger car dealers and 46% of the commercial vehicle dealers.

§ Due to bullish sentiment on sales, the two wheeler dealers had lesser apprehensions of increase in inventory.

0%

20%

40%

60%

80%

100%

% O

F R

ESP

ON

DEN

TS

OVERALL

30%

22%

39%

9%

TWO WHEELERSPASSENGER CARS

24%

25%

47%

4%

END OF Q3-2015

END OF Q2-2015

20%

23%

48%

9%

END OF Q4-2015

END OF Q1-2016

37%

5%

53%

5%

4%

55%

34%

7% 6%

60%

27%

7% 15%

39%

46%

MUCH LOWER A LITTLE LOWER A LITTLE HIGHER MUCH HIGHER

COMMERCIAL VEHICLES

4PERFORMANCE

QUARTER

VIS-À-VIS

PREVIOUS

DEALERSHIP

SALES INVENTORY PROFITS

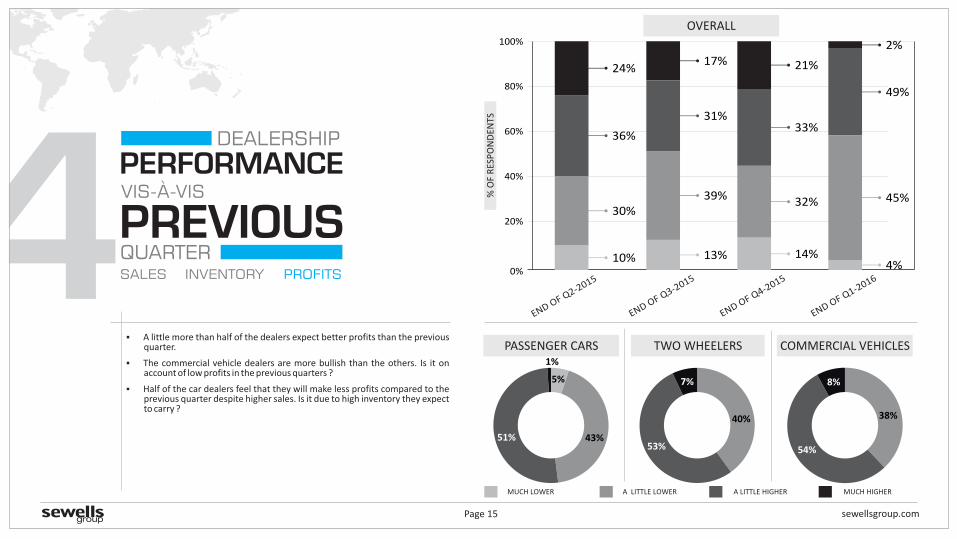

§ A little more than half of the dealers expect better profits than the previous quarter.

§ The commercial vehicle dealers are more bullish than the others. Is it on account of low profits in the previous quarters ?

§ Half of the car dealers feel that they will make less profits compared to the previous quarter despite higher sales. Is it due to high inventory they expect to carry ?

sewellsgroup.comPage 15

0%

20%

40%

60%

80%

100%

% O

F R

ESP

ON

DEN

TS

OVERALL

36%

10%

30%

24%

TWO WHEELERSPASSENGER CARS

31%

13%

39%

17%

END OF Q3-2015

END OF Q2-2015

33%

14%

32%

21%

END OF Q4-2015

END OF Q1-2016

4%

2%

49%

45%

5%

43%51%

1%

40%

53%

7%

38%

54%

8%

MUCH LOWER A LITTLE LOWER A LITTLE HIGHER MUCH HIGHER

5MARKET OVER NEXT SIX MONTHS

PERFORMANCE

sewellsgroup.comPage 16

COMMERCIAL VEHICLES

QUITE GOOD SOMEWHAT GOOD SOMEWHAT POOR QUITE POOR

0%

20%

40%

60%

80%

100%

% O

F R

ESP

ON

DEN

TS

OVERALL

27%

10%

61%

2%

TWO WHEELERSPASSENGER CARS

22%

12%

62%

4%

END OF Q3-2015

END OF Q2-2015

END OF Q4-2015

18%

10%

68%

4%

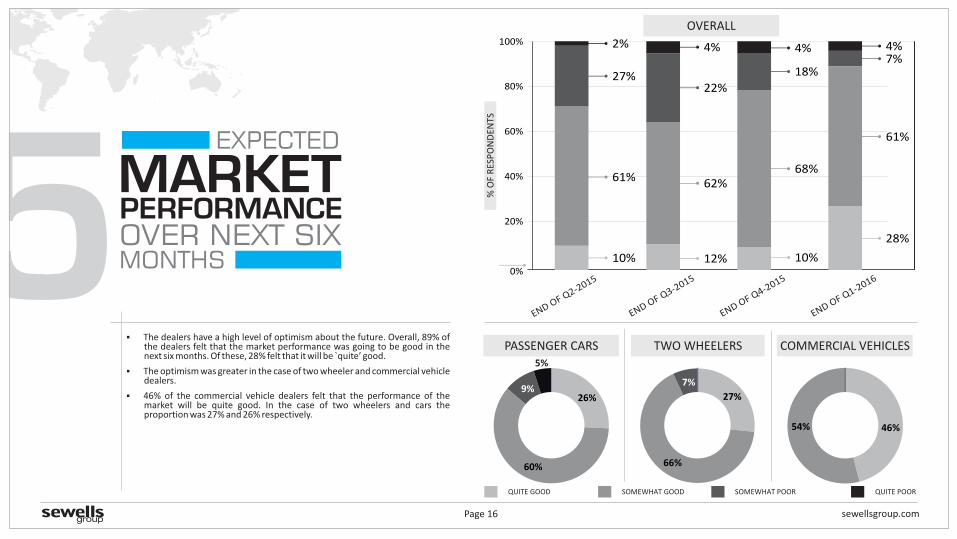

§ The dealers have a high level of optimism about the future. Overall, 89% of the dealers felt that the market performance was going to be good in the next six months. Of these, 28% felt that it will be ̀ quite’ good.

§ The optimism was greater in the case of two wheeler and commercial vehicle dealers.

§ 46% of the commercial vehicle dealers felt that the performance of the market will be quite good. In the case of two wheelers and cars the proportion was 27% and 26% respectively.

END OF Q1-2016

28%

4%7%

61%EXPECTED

26%

60%

9%

5%

27%

66%

7%

46%54%

6DEALERSHIP

OVER NEXT SIX MONTHS

OVERALL EXPECTED

PERFORMANCE

COMMERCIAL VEHICLES

sewellsgroup.comPage 17

0%

20%

40%

60%

80%

100%

% O

F R

ESP

ON

DEN

TS

OVERALL

20%

11%

65%

4%

TWO WHEELERSPASSENGER CARS

15%

19%

60%

6%

END OF Q3-2015

END OF Q2-2015

END OF Q4-2015

14%

16%

63%

7%

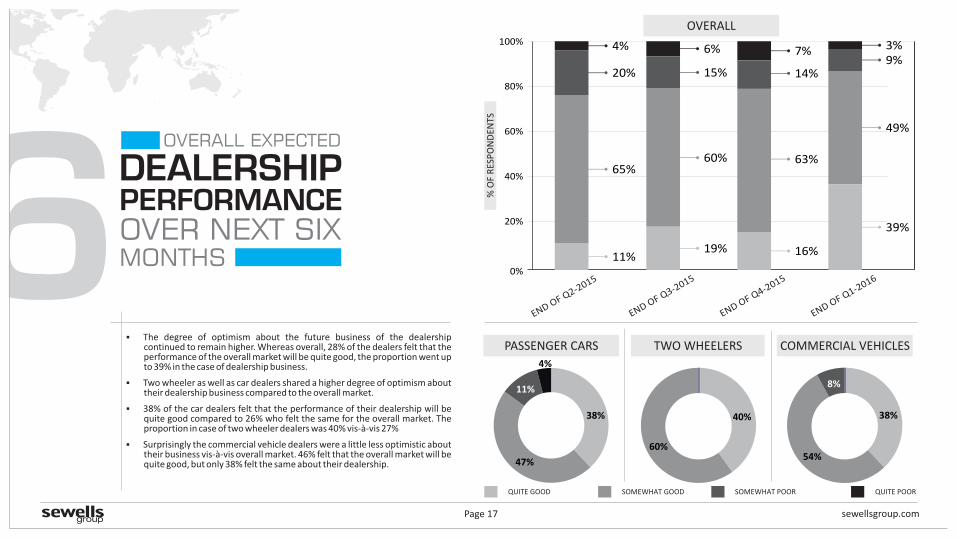

§ The degree of optimism about the future business of the dealership continued to remain higher. Whereas overall, 28% of the dealers felt that the performance of the overall market will be quite good, the proportion went up to 39% in the case of dealership business.

§ Two wheeler as well as car dealers shared a higher degree of optimism about their dealership business compared to the overall market.

§ 38% of the car dealers felt that the performance of their dealership will be quite good compared to 26% who felt the same for the overall market. The proportion in case of two wheeler dealers was 40% vis-à-vis 27%

§ Surprisingly the commercial vehicle dealers were a little less optimistic about their business vis-à-vis overall market. 46% felt that the overall market will be quite good, but only 38% felt the same about their dealership.

END OF Q1-2016

39%

3%9%

49%

38%

47%

11%

4%

40%

60%

38%

54%

8%

QUITE GOOD SOMEWHAT GOOD SOMEWHAT POOR QUITE POOR

7COMMERCIAL VEHICLES

DEALERSHIP

COMPARED TO THE

EXPECTED

PERFORMANCEOVER NEXT SIX MONTHS

SALES INVENTORY PROFITS

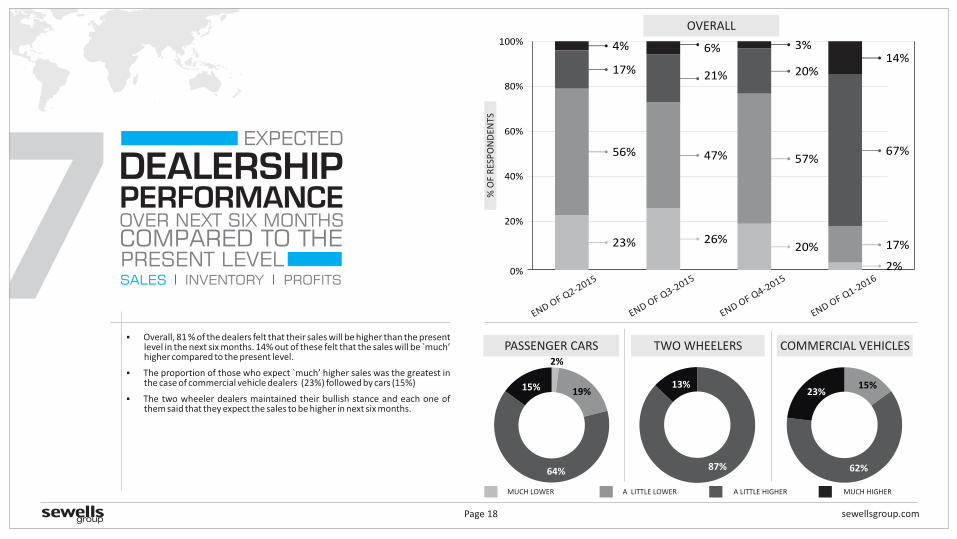

§ Overall, 81 % of the dealers felt that their sales will be higher than the present level in the next six months. 14% out of these felt that the sales will be ̀ much’ higher compared to the present level.

§ The proportion of those who expect `much’ higher sales was the greatest in the case of commercial vehicle dealers (23%) followed by cars (15%)

§ The two wheeler dealers maintained their bullish stance and each one of them said that they expect the sales to be higher in next six months.

sewellsgroup.comPage 18

0%

20%

40%

60%

80%

100%

% O

F R

ESP

ON

DEN

TS

OVERALL

TWO WHEELERSPASSENGER CARS

END OF Q3-2015

END OF Q2-2015

END OF Q4-2015

END OF Q1-20162%

14%

67%

17%

2%

19%

64%

15%

87%

13% 15%

62%

23%

MUCH LOWER A LITTLE LOWER A LITTLE HIGHER MUCH HIGHER

PRESENT LEVEL

17%

23%

56%

4%

21%

26%

47%

6%

20%

20%

57%

3%

7COMMERCIAL VEHICLES

sewellsgroup.comPage 19

0%

20%

40%

60%

80%

100%

% O

F R

ESP

ON

DEN

TS

OVERALL

TWO WHEELERSPASSENGER CARS

END OF Q3-2015

END OF Q2-2015

END OF Q4-2015

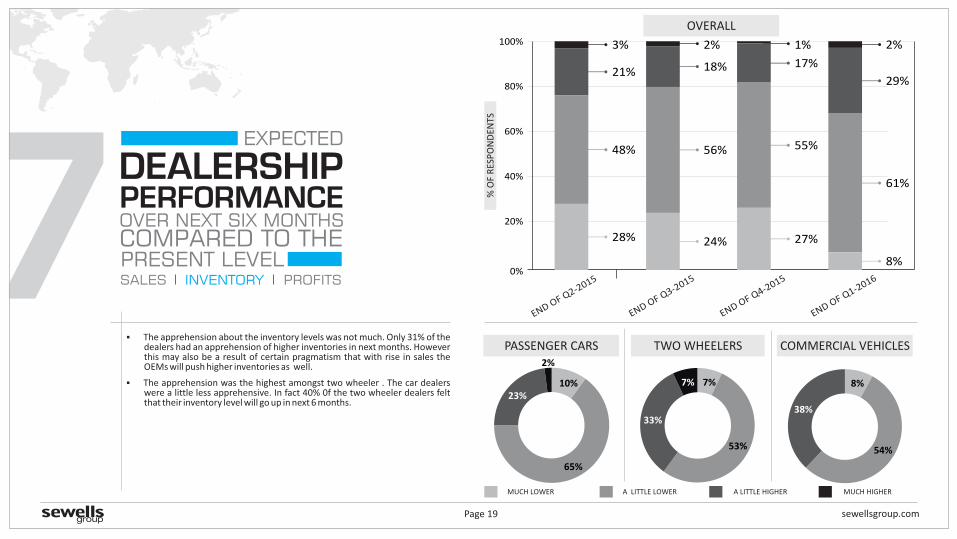

§ The apprehension about the inventory levels was not much. Only 31% of the dealers had an apprehension of higher inventories in next months. However this may also be a result of certain pragmatism that with rise in sales the OEMs will push higher inventories as well.

§ The apprehension was the highest amongst two wheeler . The car dealers were a little less apprehensive. In fact 40% 0f the two wheeler dealers felt that their inventory level will go up in next 6 months.

END OF Q1-2016

8%

2%

29%

61%

10%

65%

23%

2%

7%

53%

33%

7%

8%

54%

38%

MUCH LOWER A LITTLE LOWER A LITTLE HIGHER MUCH HIGHER

DEALERSHIP

COMPARED TO THE

EXPECTED

PERFORMANCEOVER NEXT SIX MONTHS

SALES INVENTORY PROFITS

PRESENT LEVEL

8%

21%

28%

48%

3%

18%

24%

56%

2%

17%

27%

55%

1%

7COMMERCIAL VEHICLES

sewellsgroup.comPage 20

0%

20%

40%

60%

80%

100%

% O

F R

ESP

ON

DEN

TS

OVERALL

23%

20%

47%

10%

TWO WHEELERSPASSENGER CARS

28%

20%

44%

8%

END OF Q3-2015

END OF Q2-2015

26%

20%

46%

8%

END OF Q4-2015

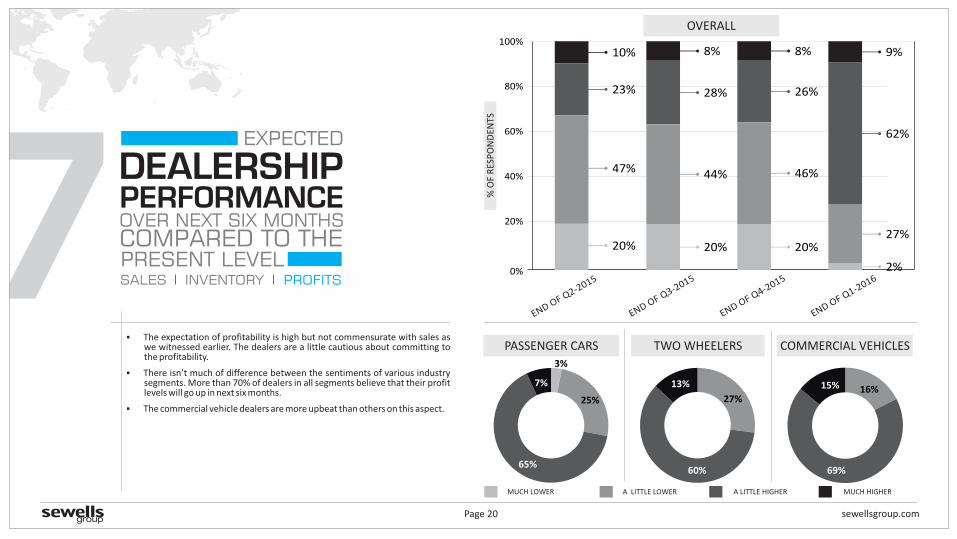

§ The expectation of profitability is high but not commensurate with sales as we witnessed earlier. The dealers are a little cautious about committing to the profitability.

§ There isn’t much of difference between the sentiments of various industry segments. More than 70% of dealers in all segments believe that their profit levels will go up in next six months.

§ The commercial vehicle dealers are more upbeat than others on this aspect.

END OF Q1-20162%

9%

62%

27%

3%

25%

65%

7%

27%

60%

13%16%

69%

15%

MUCH LOWER A LITTLE LOWER A LITTLE HIGHER MUCH HIGHER

DEALERSHIP

COMPARED TO THE

EXPECTED

PERFORMANCEOVER NEXT SIX MONTHS

SALES INVENTORY PROFITS

PRESENT LEVEL

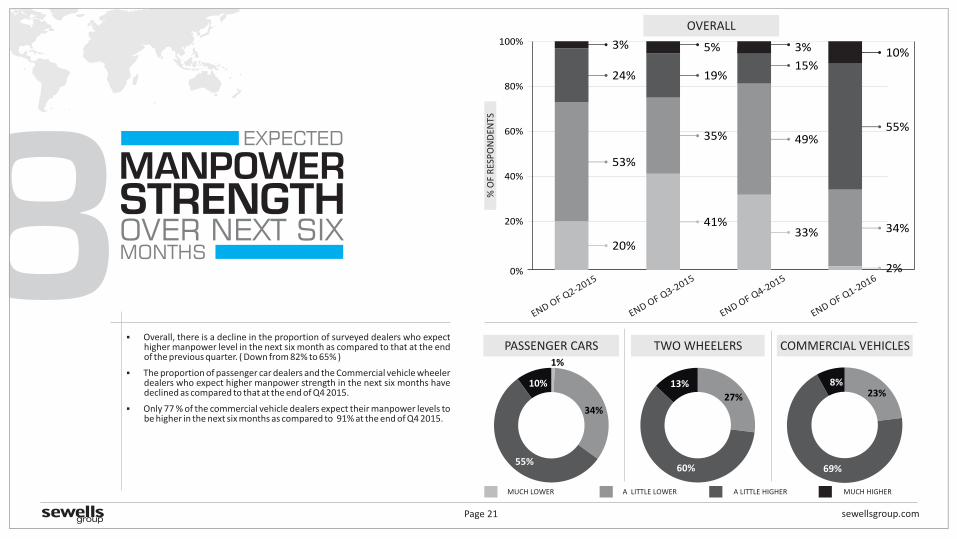

8sewellsgroup.comPage 21

MANPOWER

MONTHS

EXPECTED

STRENGTHOVER NEXT SIX

0%

20%

40%

60%

80%

100%

% O

F R

ESP

ON

DEN

TS

24%

20%

53%

3%

TWO WHEELERSPASSENGER CARS

19%

41%

35%

5%

END OF Q3-2015

END OF Q2-2015

15%

33%

49%

3%

END OF Q4-2015

§ Overall, there is a decline in the proportion of surveyed dealers who expect higher manpower level in the next six month as compared to that at the end of the previous quarter. ( Down from 82% to 65% )

§ The proportion of passenger car dealers and the Commercial vehicle wheeler dealers who expect higher manpower strength in the next six months have declined as compared to that at the end of Q4 2015.

§ Only 77 % of the commercial vehicle dealers expect their manpower levels to be higher in the next six months as compared to 91% at the end of Q4 2015.

END OF Q1-20162%

10%

55%

34%

1%

34%

55%

10%

27%

60%

13%

COMMERCIAL VEHICLES

23%

69%

8%

MUCH LOWER A LITTLE LOWER A LITTLE HIGHER MUCH HIGHER

OVERALL

9sewellsgroup.comPage 22

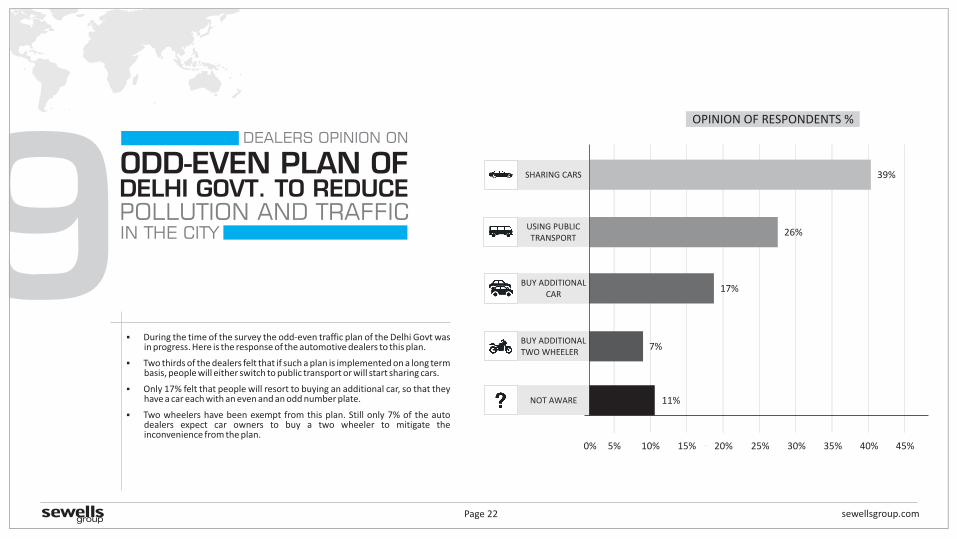

ODD-EVEN PLAN OF DEALERS OPINION ON

DELHI GOVT. TO REDUCE POLLUTION AND TRAFFIC

§ During the time of the survey the odd-even traffic plan of the Delhi Govt was in progress. Here is the response of the automotive dealers to this plan.

§ Two thirds of the dealers felt that if such a plan is implemented on a long term basis, people will either switch to public transport or will start sharing cars.

§ Only 17% felt that people will resort to buying an additional car, so that they have a car each with an even and an odd number plate.

§ Two wheelers have been exempt from this plan. Still only 7% of the auto dealers expect car owners to buy a two wheeler to mitigate the inconvenience from the plan.

OPINION OF RESPONDENTS %

BUY ADDITIONAL CAR

0% 5% 10% 15% 20% 25% 30% 35% 40% 45%

17%

SHARING CARS 39%

USING PUBLIC TRANSPORT

26% IN THE CITY

11%NOT AWARE

7%BUY ADDITIONALTWO WHEELER

sewellsgroup.comPage 23

SSEWELLSGROUP

ABOUT

Sewells Group is a global consulting and outsourcing firm which specializes in the automotive retail industry. Our very reason for being in the business is to improve the performance of individuals and organizations in the automotive retail industry. We operate across the Asia-Pacific, Africa and Middle East regions.

Our in-depth subject matter expertise in this area and our deep engagements with many leading automotive brands make us a leader in our business. Our Integrated Dealer Performance Management Model has delivered exceptional success to leading OEMs across the world. Through our proven business management model, demonstrated competence solutions and process efficacy initiatives, we contribute meaningfully to our clients’ businesses.

For more information, visit www.sewellsgroup.com

Sewells Group Contacts:

PRADEEP SAXENAChairman & CEO - Sewells Group IndiaE: [email protected]: +91 12 44681163, M: +91 9810305854

UNNIKRISHNAN NAIRManager- Solutions Operation, Sewells GroupE: [email protected]: +91 8689820043

sewellsgroup.comPage 24

DISCLAIMER

§ The contents of this report represent the opinion of survey respondents, and not that of Sewells Group, Sewells Group India, any of their subsidiary companies, or employees thereof.

§ The contents of this report and analysis of responses received in response to the quarterly Automotive Dealer Confidence Index (ADCI) survey are to be viewed as broad trends being observed, and not as definite commentary on the state of economy, state of business or policy framework of any automotive manufacturer and/or franchised automotive dealer group.

§ The contents of this report should not be viewed as commentary on the prospects of a particular manufacturer or brand as it is only intended to summarize the perceptions and opinions of respondents.

§ The contents of the report and analysis of responses should not be viewed in isolation, but in conjunction with the number of responses considered in the computation of the index and subsequent analysis.

§ This survey may have limitation in terms of sample size for some segments or overall. We advise reader discretion in interpretation of results.

§ Sewells Group does not take the responsibility of or does not indemnify any user of the study against the impact of the decisions made using the findings of this study.