2015 employer health benefits chart pack

TRANSCRIPT

Employer Health Benefit Survey 2015

Release SlidesSeptember 22, 2015

$4,955

$4,823

$4,565

$4,316

$4,129

$3,997*

$3,515

$3,354

$3,281*

$2,973*

$2,713

$2,661*

$2,412*

$2,137*

$1,787*

$1,619

$1,543

$12,591*

$12,011

$11,786

$11,429*

$10,944*

$9,773

$9,860*

$9,325*

$8,824

$8,508*

$8,167*

$7,289*

$6,657*

$5,866*

$5,274*

$4,819*

$4,247

2015

2014

2013

2012

2011

2010

2009

2008

2007

2006

2005

2004

2003

2002

2001

2000

1999Worker Contribution

Employer Contribution

Average Annual Worker and Employer Contributions to Premiums and Total Premiums for Family Coverage, 1999‐2015

* Estimate is statistically different from estimate for the previous year shown (p<.05).

SOURCE: Kaiser/HRET Survey of Employer‐Sponsored Health Benefits, 1999‐2015.

$5,791

$6,438*

$7,061*

$8,003*

$9,068*

$9,950*

$10,880*

$11,480*

$12,106*

$12,680*

$13,375*

$13,770*

$15,073*

$15,745*

$16,351*

$16,834*

$17,545*

11%

5% 5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

1999 to 2005 2005 to 2010 2010 to 2015

SOURCE: Kaiser/HRET Survey of Employer‐Sponsored Health Benefits, 1999‐2015

Average Annual Premium Increases for Family Coverage, 1999‐2015

Cumulative Increases in Health Insurance Premiums, Workers’ Contributions to Premiums, Inflation, and Workers’ Earnings, 1999‐2015

88%

138%

203%

75%

158%

221%

20%

42%56%

17%

31% 42%

0%

50%

100%

150%

200%

250%

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Health Insurance PremiumsWorkers' Contribution to PremiumsWorkers' EarningsOverall Inflation

SOURCE: Kaiser/HRET Survey of Employer‐Sponsored Health Benefits, 1999‐2015. Bureau of Labor Statistics, Consumer Price Index, U.S. City Average of Annual Inflation (April to April), 1999‐2015; Bureau of Labor Statistics, Seasonally Adjusted Data from the Current Employment Statistics Survey, 1999‐2015 (April to April).

* Estimate is statistically different between All Large Firms and All Small Firms estimate (p<.05).

SOURCE: Kaiser/HRET Survey of Employer‐Sponsored Health Benefits, 2015.

Average Annual Worker and Employer Contributions to Premiums and Total Premiums for Single and Family Coverage, by Firm Size, 2015

$899* $1,146* $1,071

$5,904*$4,549* $4,955

$5,264 $5,142 $5,179

$10,720* $13,390* $12,591

Small Firms(3 to 199Workers)

Large Firms(200 or MoreWorkers)

All Firms Small Firms(3 to 199Workers)

Large Firms(200 or MoreWorkers)

All Firms

Employer Contribution

Worker Contribution

$16,625*$17,983* $17,545

$6,163 $6,289 $6,251

Single Coverage Family Coverage

* Estimate is statistically different between All Large Firms and All Small Firms estimate (p<.05).

NOTE: Lower‐wage level is $23,000 annually or less, the 25th percentile for workers earnings nationally.

SOURCE: Kaiser/HRET Survey of Employer‐Sponsored Health Benefits, 2015.

Average Annual Worker and Employer Contributions to Premiums and Total Premiums for Single and Family Coverage, by Firm Wage Level, 2015

$1,069 $1,099 $1,071

$4,829*$6,382*

$4,955$5,238* $4,507* $5,179

$12,835* $9,801* $12,591

Less Than 35%are Lower‐Wage

Level

35% or More areLower‐Wage

Level

All Firms Less Than 35%are Lower‐Wage

Level

35% or More areLower‐Wage

Level

All Firms

Employer Contribution

Worker Contribution

$17,665*

$16,182*$17,545

$6,307*$5,606*

$6,251

Single Coverage Family Coverage

55%59%* 59%

63%

70%*74%

72%

78%*80% 81%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

* Estimate is statistically different from estimate for the previous year shown (p<.05).

SOURCE: Kaiser/HRET Survey of Employer‐Sponsored Health Benefits, 2006‐2015.

Percentage of Covered Workers With a General Annual Deductible for Single Coverage, 2006‐2015

$584 $616

$735*

$826*

$917*

$991

$1,097*$1,135

$1,217

$1,318

$303 $343

$433*

$533*

$646*

$747*$802

$883

$989*$1,077

$275

$375

$475

$575

$675

$775

$875

$975

$1,075

$1,175

$1,275

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Average Deductible Among CoveredWorkers With a Deductible

Average Deductible Among All CoveredWorkers

* Estimate is statistically different from estimate for the previous year shown (p<.05).

NOTES: Average general annual deductible is among all covered workers. Workers in plans without a general annual deductible for in‐network services are assigned a value of zero. SOURCE: Kaiser/HRET Survey of Employer‐Sponsored Health Benefits, 2006‐2015.

Average General Annual Deductible for Covered Workers Enrolled in Single Coverage, 2006‐2015

Cumulative Increases in Health Insurance Premiums, General Annual Deductibles, Inflation, and Workers’ Earnings, 2010‐2015

9%10%

67%

24%

0%

10%

20%

30%

40%

50%

60%

70%

80%

2010 2011 2012 2013 2014 2015

Overall Inflation

Workers Earnings

Single Coverage Deductibles, all Workers

Single Coverage Premiums

NOTE: Average general annual deductible is among all covered workers. Workers in plans without a general annual deductible for in‐network services are assigned a value of zero. SOURCE: Kaiser/HRET Survey of Employer‐Sponsored Health Benefits, 2010‐2015. Bureau of Labor Statistics, Consumer Price Index, U.S. City Average of Annual Inflation (April to April), 2010‐2015; Bureau of Labor Statistics, Seasonally Adjusted Data from the Current Employment Statistics Survey, 2010‐2015 (April to April).

16%21%*

35%*40%

46%50% 49%

58%*61% 63%

6% 8% 9%13%*

17%22%*

26% 28%32%

39%*

10% 12%*

18%*22%*

27%*31%

34%38%

41%46%

0%

10%

20%

30%

40%

50%

60%

70%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

All Small Firms (3‐199 Workers)

All Large Firms (200 or More Workers)

All Firms

* Estimate is statistically different from estimate for the previous year shown (p<.05).

NOTE: These estimates include workers enrolled in HDHP/SOs and other plan types. Average general annual health plan deductibles for PPOs, POS plans, and HDHP/SOs are for in‐network services.

SOURCE: Kaiser/HRET Survey of Employer‐Sponsored Health Benefits, 2006‐2015.

Percentage of Covered Workers Enrolled in a Plan with a General Annual Deductible of $1,000 or More for Single Coverage, By Firm Size, 2006‐2015

1%<1%1%1%1%

1%1%2%3%3%3%5%5%4%7%8%10%

27%46%

73%

14%13%14%16%17%19%20%20%21%20%21%

25%24%27%24%

29%28%

31%21%

16%

52%58%57%56%55%

58%60%58%

57%60%61%

55%54%52%

46%42%

39%28%

26%11%

10%8%9%9%10%

8%10%

12%13%13%

15%15%

17%18%

23%21%

24%14%

7%

24%20%20%19%17%

13%8%8%5%4%

20152014201320122011201020092008200720062005200420032002200120001999199619931988

Conventional HMO PPO POS HDHP/SO

NOTE: Information was not obtained for POS plans in 1988. A portion of the change in plan type enrollment for 2005 is likely attributable to incorporating more recent Census Bureau estimates of the number of state and local government workers and removing federal workers from the weights. See the Survey Design and Methods section from the 2005 Kaiser/HRET Survey of Employer‐Sponsored Health Benefits for additional information.

SOURCE: Kaiser/HRET Survey of Employer‐Sponsored Health Benefits, 1999‐2015; KPMG Survey of Employer‐Sponsored Health Benefits, 1993, 1996; The Health Insurance Association of America (HIAA), 1988.

Distribution of Health Plan Enrollment for Covered Workers, by Plan Type, 1988‐2015

63%

66% 66%64% 63%

61%

57% 58%56%

60%

57%

66%*

57%*59%

55%

52%54%

96%

99%*

94%*

91%93%

87%

91%

88%

94%

91% 92% 93% 92% 93%91% 90% 89%

98%

96%

98% 98% 97% 98% 97% 97% 96%99% 98% 99%

96%* 96% 95% 94%

97%

66%68% 68%

66% 66%

63%

60% 61%59%

63%

59%

69%*

60%* 61%

57%55%

57%

40%

50%

60%

70%

80%

90%

100%

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

3 to 49 Workers

50 to 99 Workers

100 or more

ALL FIRMS

Percentage of Firms Offering Health Benefits, by Firm Size, 1999‐2015

*Estimate is statistically different from estimate for the previous year shown (p<.05).

NOTE: Estimates presented in this exhibit are based on the sample of both firms that completed the entire survey and those that answered just one question. For more information, see the Survey Methods Section.

SOURCE: Kaiser/HRET Survey of Employer‐Sponsored Health Benefits, 1999‐2015.

79%81%

83%81%* 81% 80% 80%

78% 79% 80% 79% 79% 79%77% 77% 77%

79%

85% 84% 84% 85% 84% 83% 83% 83% 82% 82% 81% 80%81% 81% 80% 80% 79%

66%68%

70%68% 68% 67% 66% 65% 65% 65% 65%

63%65%

62% 62% 62% 63%

50%

60%

70%

80%

90%

100%

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Percentage Eligible

Percentage of Eligible That Take Up

Percentage Covered

Eligibility, Take‐Up Rate, and Coverage for Workers in Firms Offering Health Benefits, 1999‐2015

* Estimate is statistically different from estimate for the previous year shown (p<.05).

SOURCE: Kaiser/HRET Survey of Employer‐Sponsored Health Benefits, 1999‐2014.

Among Firms with More Than 50 Employees and Who Offer Health Benefits, The Percentage of Firms Considering Offering Benefits Through a Private Exchange, 2015

ǂ These questions were not asked of firms that already offer health benefits through a private exchange.

NOTE: A private exchange is one created by a consulting company, not by a state or federal government. Private exchanges allow employees to choose from several health benefit options offered on the exchange. A defined premium contribution is a set dollar amount offered to the employee. Employees may then select one of several plans and the employee pays the difference between the defined contribution and the cost of the health insurance option they choose.

SOURCE: Kaiser/HRET Survey of Employer‐Sponsored Health Benefits, 2015.

17%26%

2% 3%

76%68%

7% 7%

0%

20%

40%

60%

80%

100%

Considering Offering Benefits Through a Private Exchangeǂ

Considering a Defined Contributionǂ

Percentage of CoveredWorkers Enrolled at a

Firm That Offers BenefitsThrough a Private orCorporate Exchange

Percentage of Firmsoffering Health BenefitsWhich Offer CoverageThrough a Private orCorporate Exchange

Yes

No

Don't Know

ǂ Firms which offer either “Programs to Help Employees Stop Smoking”, “Programs to Help Employees Lose Weight”, or “Other Lifestyle or Behavioral Coaching“.

SOURCE: Kaiser/HRET Survey of Employer‐Sponsored Health Benefits, 2015.

Among Large Firms (200 or More Workers) Offering Health Benefits, Percentage of Firms Offering Incentives for Various Wellness and Health Promotion Activities, 2015

50%

31%

50%

28%

81%

31%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Offers orRequires HealthRisk Assessment

Also has anIncentive to

Complete HealthRisk Assessment

Offers or AsksEmployees toCompleteBiometericScreening

Also has anIncentive ToCompleteBiometricScreening

Offers Specific Wellness Programǂ

Also has anIncentive orPenalty to

Participate inWellnessPrograms

Health Risk Assessments

Biometric Screening Wellness Programs

* Estimate is statistically different between All Small Firms and All Large Firms (p<.05).

NOTE: “Other Lifestyle or Behavioral Coaching” can include health education classes, stress management, or substance abuse counseling.

SOURCE: Kaiser/HRET Survey of Employer‐Sponsored Health Benefits, 2015.

Among Firms Offering Health Benefits, Percentage of Firms Offering Specific Wellness Program to Their Employees, by Firm Size, 2015

41%* 39%* 39%*

49%*

71%*

61%*

68%*

81%*

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Programs to Help EmployeesStop Smoking

Programs to Help EmployeesLose Weight

Other Lifestyle or BehavioralCoaching

At Least Oneof These Programs

All Small Firms (3‐199 Workers)All Large Firms (200 or More Workers)

Among Large Firms Offering Incentives for Workers Who Participate In or Complete Wellness Programs, Maximum Annual Value of the Reward for Wellness and Health Promotion Programs, Including Incentives for Health Risk Assessment and Biometric Screening, 2015

22%

41%

21%

11%5%

0%

20%

40%

60%

80%

100%

$150 or Less >$150 to $500 >$500 to $1,000 >$1,000 to $2,000 Greater than $2,000

Maximum Annual Value of the Reward for Wellness and Health Promotion Programs Altogether (All Large Firms‐200 or More Workers)

NOTE: Firms with at least one of the listed wellness programs were asked to report the maximum reward or penalty an employee could earn for all of the firm's health promotion activities combined. For some employers, the maximum incentive may include rewards or penalties for activities related to health risk assessments and biometric screening. Listed programs include: “Programs to Help Employees Stop Smoking”, “Programs to Help Employees Lose Weight”, or “Other Lifestyle or Behavioral Coaching”.

SOURCE: Kaiser/HRET Survey of Employer‐Sponsored Health Benefits, 2015.

Note: A high performance network is one that groups providers within the network based on quality, cost, and/or efficiency of care they deliver.

SOURCE: Kaiser/HRET Survey of Employer‐Sponsored Health Benefits, 2015.

Among Firms Offering Health Benefits, Percentage of Firms Who Have Incorporated Various Features into Their Provider Networks, by Firm Size, 2015

17%

9%8%

24%

6%5%

0%

10%

20%

30%

Largest Plan Includes a High‐Performance orTiered Provider Network

Firm/Insurer Eliminated Hospitals or HealthSystems from Network to Reduce Cost

Firm Offers a Plan Considered a NarrowNetwork Plan

All Small Firms (3‐199 Workers)

All Large Firms (200 or More Workers)

Among Firms Whose Plan with the Largest Enrollment Covers Specialty Drugs, Percentage of Firms Which Use the Following Strategies to Contain Specialty Drug Cost, by Firm Size, 2015

8% 7%4%

7% 6% 7%2%

20%

14%* 14%

30%25%

31%

10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Separate Cost SharingTier

Specialty Drug CarveOut

Specialty PharmacyDispensing Program

Step Therapies Tight Limits on theNumber of UnitsAdministeredat a Single Time

UtilizationManagementPrograms

Other

All Small Firms (3‐199 Workers) All Large Firms (200 or More Workers)

SOURCE: Kaiser/HRET Survey of Employer‐Sponsored Health Benefits, 2015.

Among Firms Offering Health Benefits with 50 or More Full‐Time‐Equivalentsǂ, Percentage of Firms That Took Various Actions, by Firm Size, 2015

ǂ Firms were asked if they took the relevant action in response to the Employer‐Shared Responsibility Provisions. Firms with 50 or more full‐time equivalents were asked these questions. A significant number of employers, mostly large employers did not know how many FTEs they employed. In these cases, firms with 50 or more workers were asked these questions.

Source: Kaiser/HRET Survey of Employer‐Sponsored Health Benefits, 2015.

4%

10%

4%

2%

3%

13%

5%

3%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Changed some job classifications fromfull time to part time so employees

would NOT be eligible

Changed some job classificationsfrom part time to full time so that

employees would be eligible

Reduced the number of full time employeesthe firm intended to hire because of the cost

of providing health benefits

Increased the waiting period beforenew employees are eligible for health benefits

All Large Firms (200 or more Workers)ǂ

All Firms (50 or More FTEs)ǂ

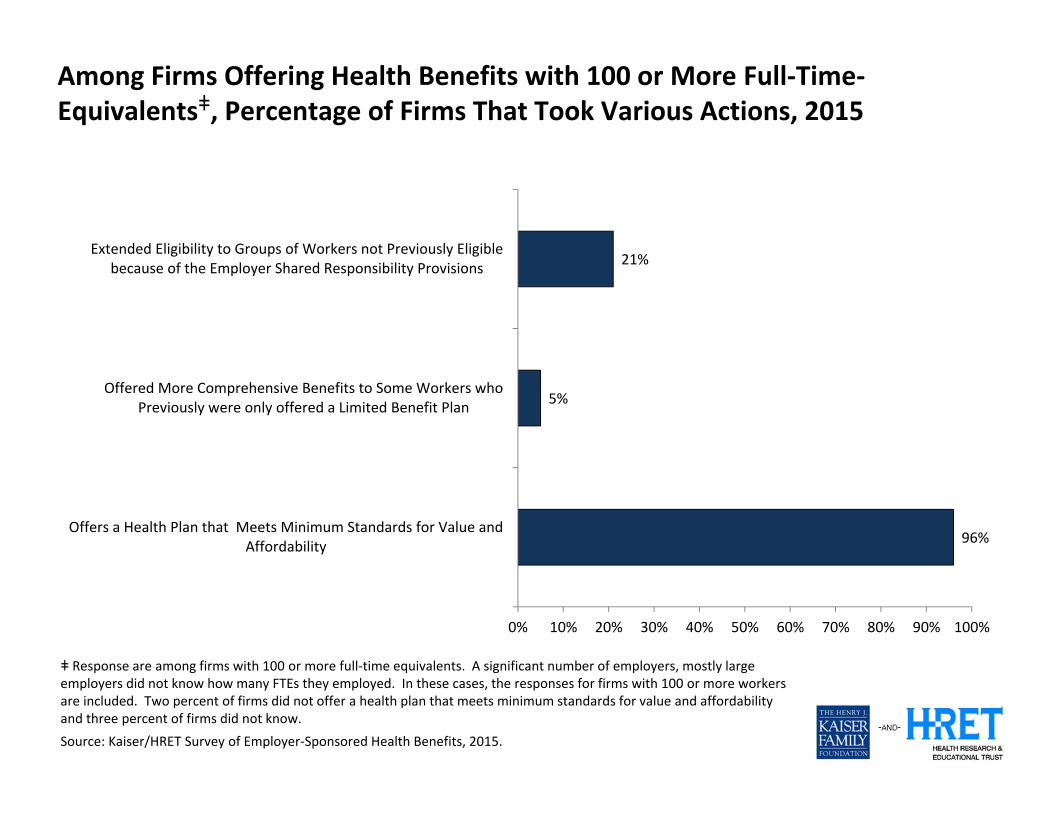

Among Firms Offering Health Benefits with 100 or More Full‐Time‐Equivalentsǂ, Percentage of Firms That Took Various Actions, 2015

ǂ Response are among firms with 100 or more full‐time equivalents. A significant number of employers, mostly large employers did not know how many FTEs they employed. In these cases, the responses for firms with 100 or more workers are included. Two percent of firms did not offer a health plan that meets minimum standards for value and affordability and three percent of firms did not know.

Source: Kaiser/HRET Survey of Employer‐Sponsored Health Benefits, 2015.

96%

5%

21%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Offers a Health Plan that Meets Minimum Standards for Value andAffordability

Offered More Comprehensive Benefits to Some Workers whoPreviously were only offered a Limited Benefit Plan

Extended Eligibility to Groups of Workers not Previously Eligiblebecause of the Employer Shared Responsibility Provisions

SOURCE: Kaiser/HRET Survey of Employer‐Sponsored Health Benefits, 2015.

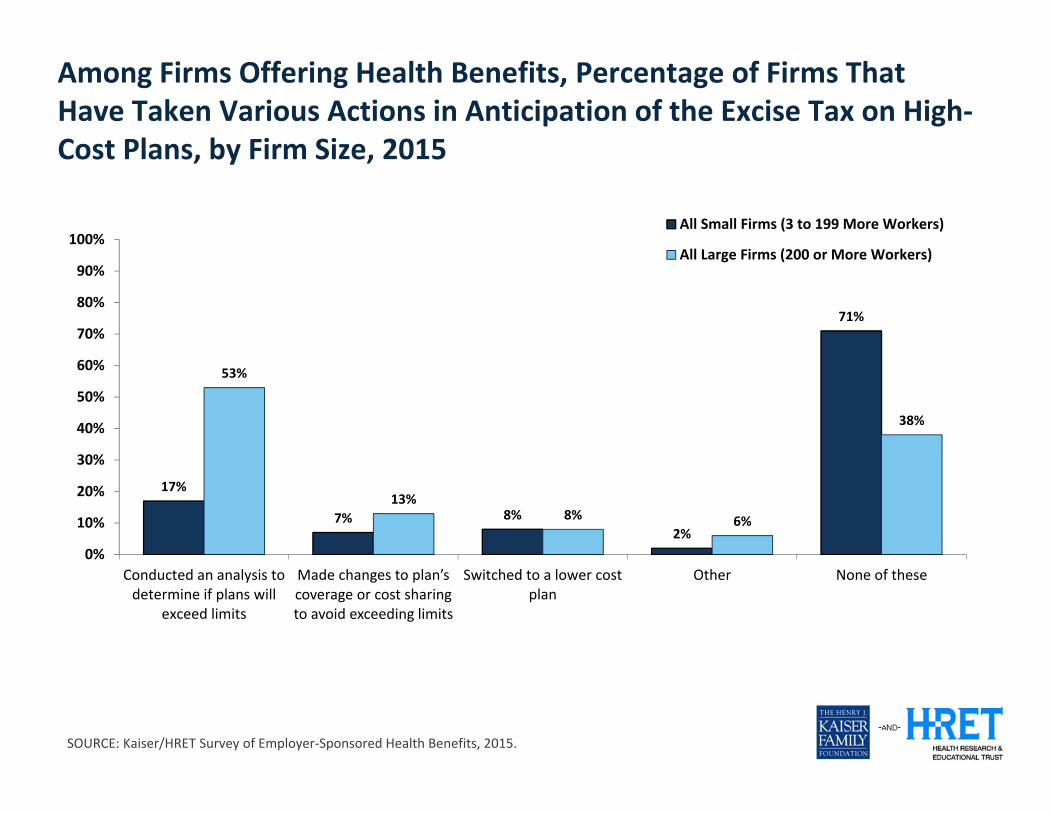

Among Firms Offering Health Benefits, Percentage of Firms That Have Taken Various Actions in Anticipation of the Excise Tax on High‐Cost Plans, by Firm Size, 2015

17%

7% 8%2%

71%

53%

13%8% 6%

38%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Conducted an analysis todetermine if plans will

exceed limits

Made changes to plan’s coverage or cost sharing to avoid exceeding limits

Switched to a lower costplan

Other None of these

All Small Firms (3 to 199 More Workers)

All Large Firms (200 or More Workers)

Among Large Firms (200 or More Workers) Offering Health Benefits Who Indicated That Have They Changed Their Plan or Switched Carriers In Anticipation of the Excise Tax on High‐Cost Health Plans, Percentage of Firms Which Have Taken Various Actions, 2015

‡ Among firms who offer either an HSA‐qualified plan or a high deductible plan paired with a health reimbursement arrangement.

Note: Sixteen percent of large firms offering health benefits report that they have changed their benefit plans or moved to lower cost plans in anticipation of the assessment

SOURCE: Kaiser/HRET Survey of Employer‐Sponsored Health Benefits, 2015.

64%

10%

34%

18% 16%24%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Increased costsharing

Reduced the scope ofcovered services

Moved benefit options to account‐based plans such as an HRA or HSA‡

Increase incentives touse less costlyproviders

Considered offeringhealth insurancethrough a private

exchange

Other

Actions Taken by Large Firms in Anticipation of the High Cost Plan Tax

SOURCE: Kaiser Family Foundation analysis of National Health Expenditure (NHE) data from Centers for Medicare and Medicaid Services, Office of the Actuary, National Health Statistics Group.

U.S. health care spending per capita has risen at historically low rates recently, but is expected to pick up

Average annual growth rate of health spending per capita for 1970’s – 1990’s;Annual change in actual health spending per capita 2000 – 2013 and projected health spending per capita (2014 – 2024)

12.0%

9.9%

5.5%6.1%

7.4%

8.6%

7.6%

6.2%5.8% 5.5% 5.3%

3.8%

2.9% 3.1% 3.2% 3.4%2.9%

4.7% 4.4%4.0%

4.5% 4.6%5.2% 5.3% 5.3% 5.3% 5.2% 5.1%

0%

2%

4%

6%

8%

10%

12%

14%

1970s

1980s

1990s

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

Actual Projected