brazil monthly chart pack | february 2017

TRANSCRIPT

February 2017

Gabriela Morales

Brazil Monthly Chart Pack:

The credit market

OFFICIAL

1

2

1. Credit once helped pushing us down here

OFFICIAL

OFFICIAL

Despite the history of high inflation, a cheap credit spree marked Brazil’s recent past

Source: Central Bank of Brazil (BCB).

25

27

29

31

33

35

37

39

41

43

45

% Average interest rate for Households

OFFICIAL

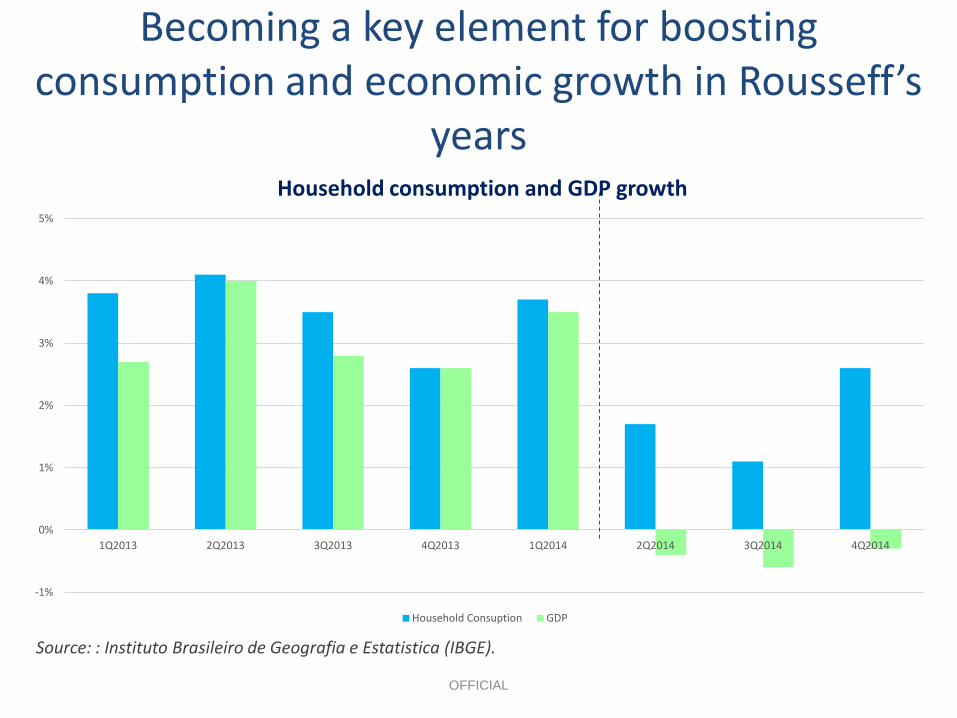

Becoming a key element for boosting consumption and economic growth in Rousseff’s

years

Source: : Instituto Brasileiro de Geografia e Estatistica (IBGE).

-1%

0%

1%

2%

3%

4%

5%

1Q2013 2Q2013 3Q2013 4Q2013 1Q2014 2Q2014 3Q2014 4Q2014

Household consumption and GDP growth

Household Consuption GDP

OFFICIAL

However, soon the bill had to come. Brazilians felt it hard, as interest rates climbed at the same

pace as they before were pushed down

Source: Instituto Brasileiro de Geografia e Estatistica (IBGE); Central Bank of Brazil (BCB).

0

2

4

6

8

10

12

0

2

4

6

8

10

12

14

16

Jan

-13

Feb

-13

Mar

-13

Ap

r-1

3

May

-13

Jun

-13

Jul-

13

Au

g-1

3

Sep

-13

Oct

-13

No

v-1

3

Dec

-13

Jan

-14

Feb

-14

Mar

-14

Ap

r-1

4

May

-14

Jun

-14

Jul-

14

Au

g-1

4

Sep

-14

Oct

-14

No

v-1

4

Dec

-14

Jan

-15

Feb

-15

Mar

-15

Ap

r-1

5

May

-15

Jun

-15

Jul-

15

Au

g-1

5

Sep

-15

Oct

-15

No

v-1

5

Dec

-15

% % Inflation and Interest rate

IPCA SELIC

OFFICIAL

Which restricted the credit market…

Source: Central Bank of Brazil (BCB).

20.57

18.76

16.44

14.48

11.29

6.69

-3.51 -5

0

5

10

15

20

25

2010 2011 2012 2013 2014 2015 2016

Credit Growth (%)

OFFICIAL

…Affecting economic activity and supporting the country’s path into a vicious cycle

Source: Instituto Brasileiro de Geografia e Estatistica (IBGE); Central Bank of Brazil (BCB).

-10%

-5%

0%

5%

10%

15%

2010 2011 2012 2013 2014 2015 2016

Industrial activity growth

-8%

-4%

0%

4%

8%

12%

2010 2011 2012 2013 2014 2015 2016

Retail sales growth

OFFICIAL

As unemployment skyrocketed, households struggled to cover debts contracted during the

“good old days”

Source: Central Bank of Brazil (BCB).

40

41

42

43

44

45

46

47

0

2

4

6

8

10

12

14

Jan

-14

Feb

-14

Mar

-14

Ap

r-1

4

May

-14

Jun

-14

Jul-

14

Au

g-1

4

Sep

-14

Oct

-14

No

v-1

4

Dec

-14

Jan

-15

Feb

-15

Mar

-15

Ap

r-1

5

May

-15

Jun

-15

Jul-

15

Au

g-1

5

Sep

-15

Oct

-15

No

v-1

5

Dec

-15

Jan

-16

Feb

-16

Mar

-16

Ap

r-1

6

May

-16

Jun

-16

Jul-

16

Au

g-1

6

Sep

-16

Oct

-16

No

v-1

6

Dec

-16

Ho

useh

old

deb

t (%) U

ne

mp

loym

ent

(%)

Unemployment and Household Debt

OFFICIAL

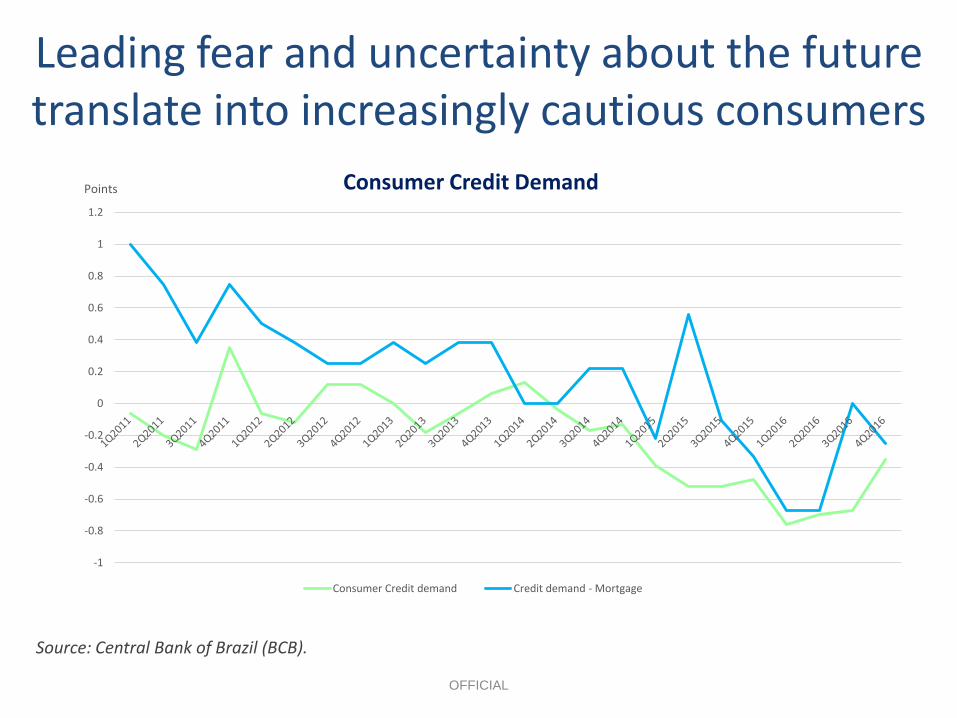

Leading fear and uncertainty about the future translate into increasingly cautious consumers

Source: Central Bank of Brazil (BCB).

-1

-0.8

-0.6

-0.4

-0.2

0

0.2

0.4

0.6

0.8

1

1.2

Points Consumer Credit Demand

Consumer Credit demand Credit demand - Mortgage

OFFICIAL

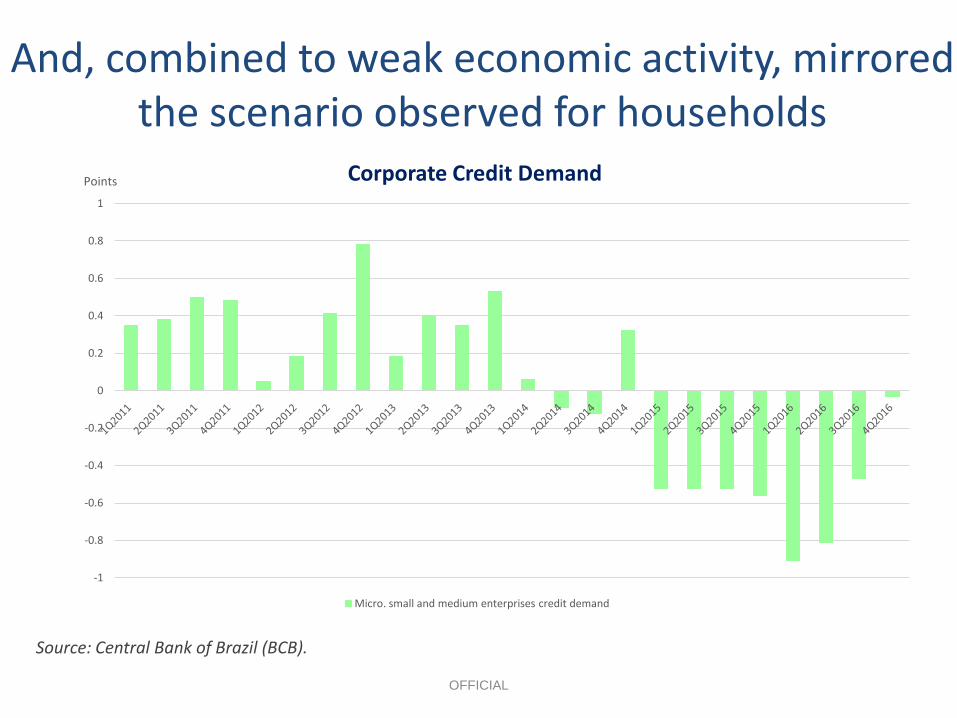

Meanwhile, corporate credit followed the same path

Source: Central Bank of Brazil (BCB).

12

14

16

18

20

22

24 %

Average interest rate for Non-financial corporations

OFFICIAL

And, combined to weak economic activity, mirrored the scenario observed for households

Source: Central Bank of Brazil (BCB).

-1

-0.8

-0.6

-0.4

-0.2

0

0.2

0.4

0.6

0.8

1

Points Corporate Credit Demand

Micro. small and medium enterprises credit demand

12

2. Now, credit will be key for driving us from here

OFFICIAL

OFFICIAL

As inflation cedes, monetary easing is finally a reality for a new confidence boosted Central Bank

Source: Instituto Brasileiro de Geografia e Estatistica (IBGE); Central Bank of Brazil (BCB).

0

2

4

6

8

10

12

11

11.5

12

12.5

13

13.5

14

14.5

Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jun-16 Jul-16 Aug-16 Sep-16 Oct-16 Nov-16 Dec-16 Jan-17 Feb-17

% %

Inflation and Interest rate

IPCA SELIC

OFFICIAL

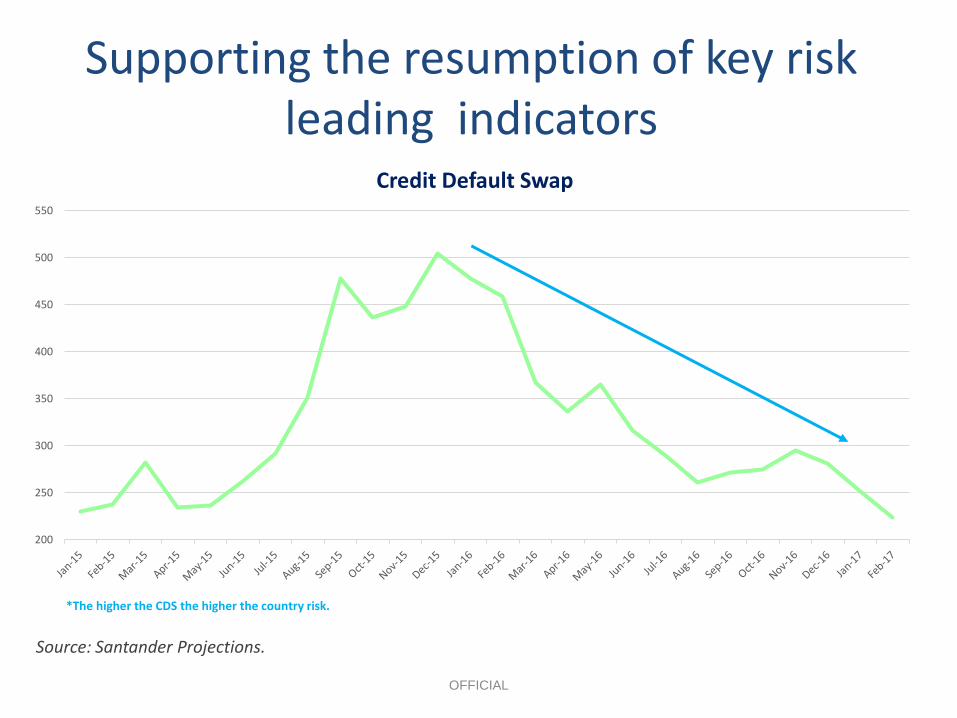

Supporting the resumption of key risk leading indicators

Source: Santander Projections.

200

250

300

350

400

450

500

550

Credit Default Swap

*The higher the CDS the higher the country risk.

OFFICIAL

Alongside its confidence peers

Source: Confederacao Nacional da Industria (CNI).

63.40

44.50

59.80

40

45

50

55

60

65

70

0-100 points Industry Confidence Index

Confidence

Lack of Confidence

OFFICIAL

Meanwhile, banks are well capitalized and the financial market remains solid

Source: IMF.

3.8%

1.7%

37.0%

7.6%

9.2%

3.2%

0.0% 5.0% 10.0% 15.0% 20.0% 25.0% 30.0% 35.0% 40.0%

Brazil

China

Greece

India

Russian Federation

South Africa

IMF Financial Soundness Indicator (Bank non-performing loans to total gross loans 2016)

OFFICIAL

And ready for a fresh start

Source: Central Bank of Brazil (BCB); Santander Projections.

Projections

7.9%

-3.9%

9.8%

24.0%

-2.3%

8.5%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

2013 2014 2015 2016 2017 2018 2019

Directed and non-directed credit

Non-directed credit Directed credit

OFFICIAL

Driving what may hopefully look something like that: credit supply + confidence + uncertainty =

investments

Source: Instituto Brasileiro de Geografia e Estatistica (IBGE); Santander Projections.

Projections

11.29

6.69

-3.55

3.2

8.9 9.6

10.5

-5

0

5

10

15

2014 2015 2016 2017 2018 2019 2020

Credit growth (%)

Projections

Source: Central Bank of Brazil (BCB); Santander Projections.

-4.2%

-13.9%

-10.2%

3.5%

6.0% 5.0%

4.0%

-15%

-10%

-5%

0%

5%

10%

2014 2015 2016 2017 2018 2019 2020

Investment (FBKF)

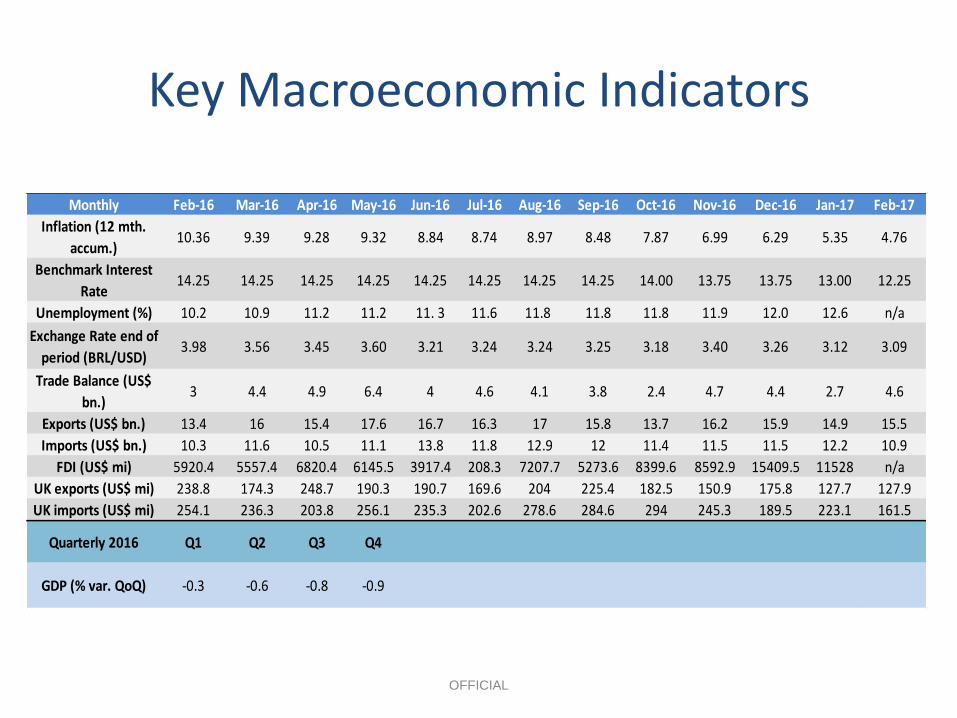

Key Macroeconomic Indicators

OFFICIAL

Monthly Feb-16 Mar-16 Apr-16 May-16 Jun-16 Jul-16 Aug-16 Sep-16 Oct-16 Nov-16 Dec-16 Jan-17 Feb-17

Inflation (12 mth.

accum.)10.36 9.39 9.28 9.32 8.84 8.74 8.97 8.48 7.87 6.99 6.29 5.35 4.76

Benchmark Interest

Rate14.25 14.25 14.25 14.25 14.25 14.25 14.25 14.25 14.00 13.75 13.75 13.00 12.25

Unemployment (%) 10.2 10.9 11.2 11.2 11. 3 11.6 11.8 11.8 11.8 11.9 12.0 12.6 n/a

Exchange Rate end of

period (BRL/USD)3.98 3.56 3.45 3.60 3.21 3.24 3.24 3.25 3.18 3.40 3.26 3.12 3.09

Trade Balance (US$

bn.)3 4.4 4.9 6.4 4 4.6 4.1 3.8 2.4 4.7 4.4 2.7 4.6

Exports (US$ bn.) 13.4 16 15.4 17.6 16.7 16.3 17 15.8 13.7 16.2 15.9 14.9 15.5

Imports (US$ bn.) 10.3 11.6 10.5 11.1 13.8 11.8 12.9 12 11.4 11.5 11.5 12.2 10.9

FDI (US$ mi) 5920.4 5557.4 6820.4 6145.5 3917.4 208.3 7207.7 5273.6 8399.6 8592.9 15409.5 11528 n/a

UK exports (US$ mi) 238.8 174.3 248.7 190.3 190.7 169.6 204 225.4 182.5 150.9 175.8 127.7 127.9

UK imports (US$ mi) 254.1 236.3 203.8 256.1 235.3 202.6 278.6 284.6 294 245.3 189.5 223.1 161.5

Quarterly 2016 Q1 Q2 Q3 Q4

GDP (% var. QoQ) -0.3 -0.6 -0.8 -0.9