the study of excess returns of the liquidity risk of each sector in chinese stock market

DESCRIPTION

The Study of Excess Returns of the Liquidity Risk of each Sector in Chinese Stock Market. 李莉莉,张玉兰 LI Lili,ZHANG Yulan. I. Introduction. Foreign studies: Liquidity risk can lead to excess returns on the stock market. Chinese stock market: - PowerPoint PPT PresentationTRANSCRIPT

The Study of Excess Returns of the Liquidity Risk of each

Sector in Chinese Stock Market 李莉莉,张玉兰LI Lili,ZHANG Yulan

I. Introduction

Foreign studies:

Liquidity risk can lead to excess returns on the stock market.

Chinese stock market:Researchers cannot agree with each other on excess returns coming from liquidity risk.

II. Empirical Analysis

A. Liquidity indicator:

1/h l ct t t

tt

P P PNL

T

II. Empirical Analysis

B. Data selection:Bull phase: July 1, 2006 - October 16,2007 (the Shanghai A-share Index rose to 6395.76 points from 1784.46 points)

Bear phase: October 16, 2007 - December 31, 2008 (the Shanghai A-share Index fell to 1911.79 points from 6395.76 points)

II. Empirical Analysis

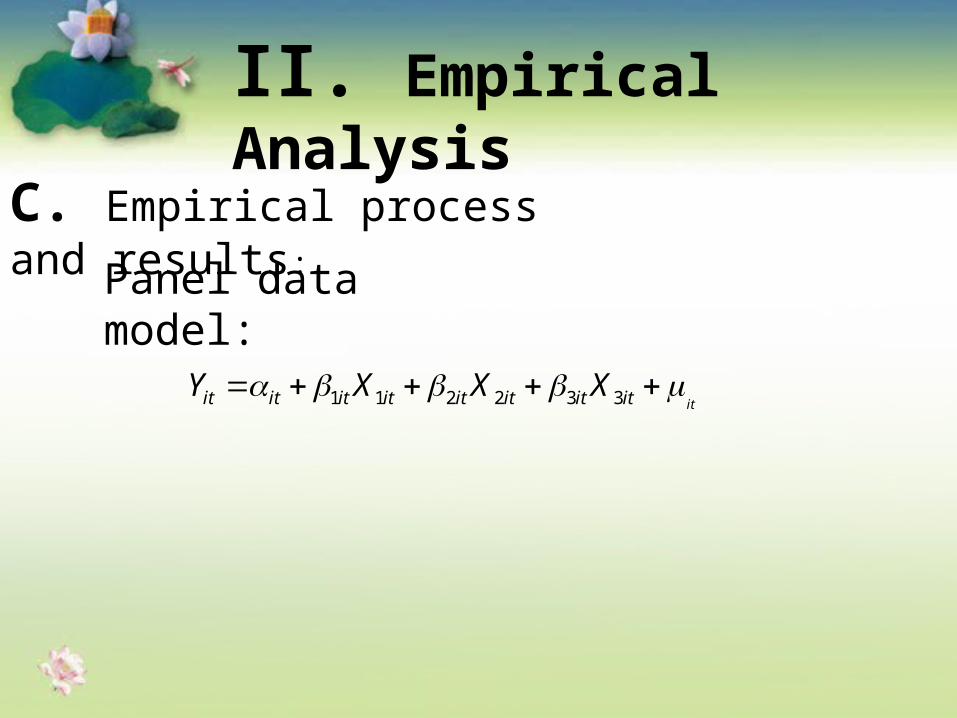

C. Empirical process and results:

Panel data model:

1 1 2 2 3 3 itit it it it it it it itY X X X

II. Empirical Analysis

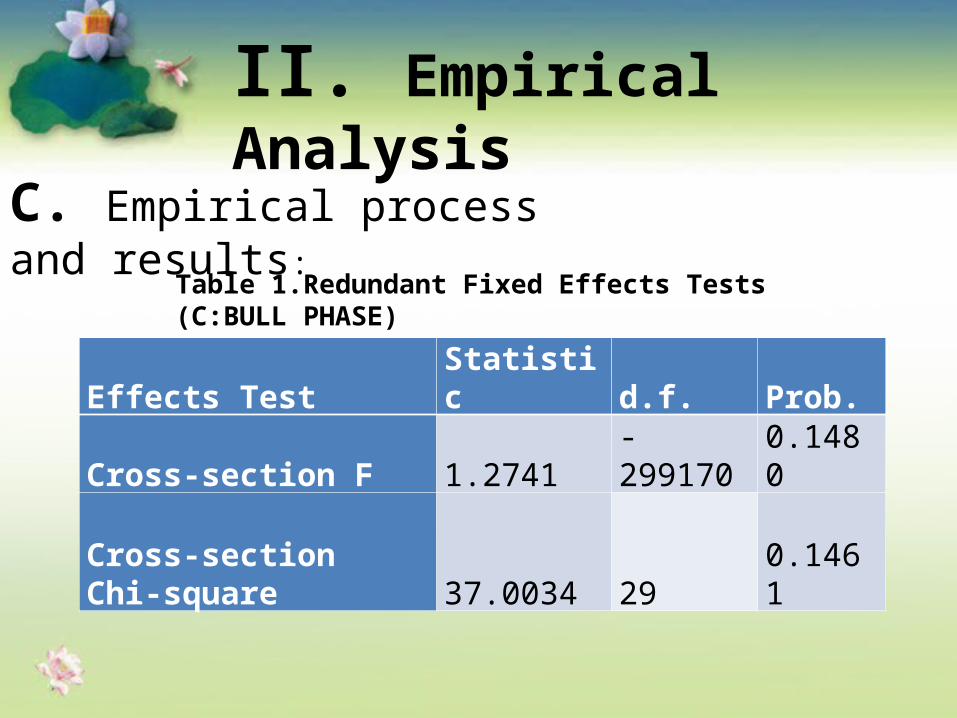

C. Empirical process and results:

Effects Test Statistic d.f. Prob.

Cross-section F 1.2741 -299170 0.1480

Cross-section Chi-square 37.0034 29 0.1461

Table 1.Redundant Fixed Effects Tests (C:BULL PHASE)

II. Empirical Analysis

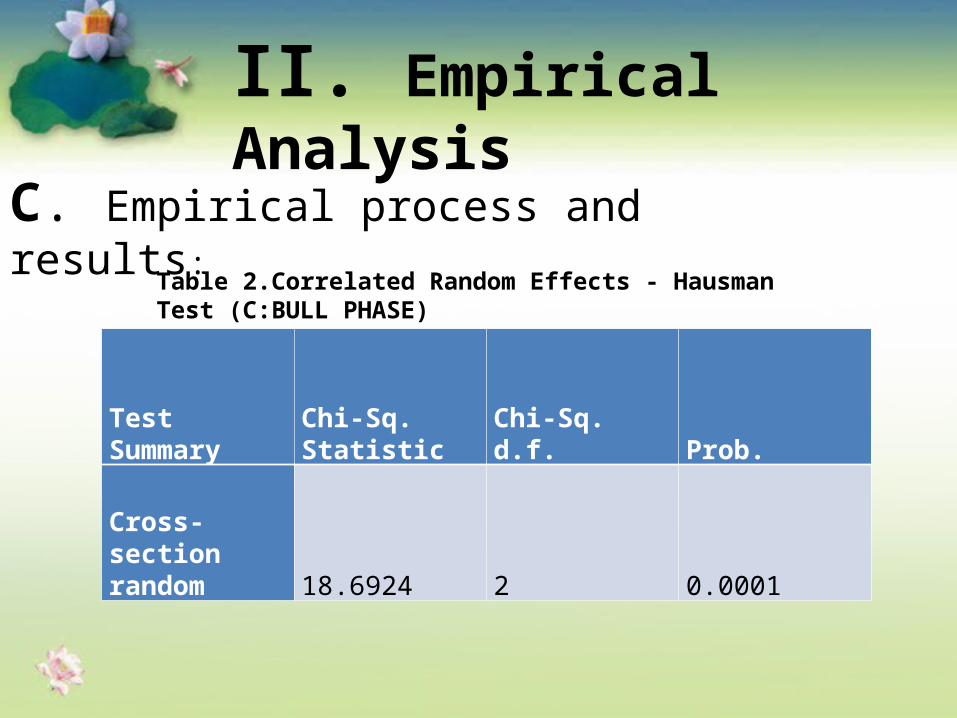

C. Empirical process and results:

Table 2.Correlated Random Effects - Hausman Test (C:BULL PHASE)

Test Summary Chi-Sq. Statistic Chi-Sq. d.f. Prob.

Cross-section random 18.6924 2 0.0001

II. Empirical Analysis

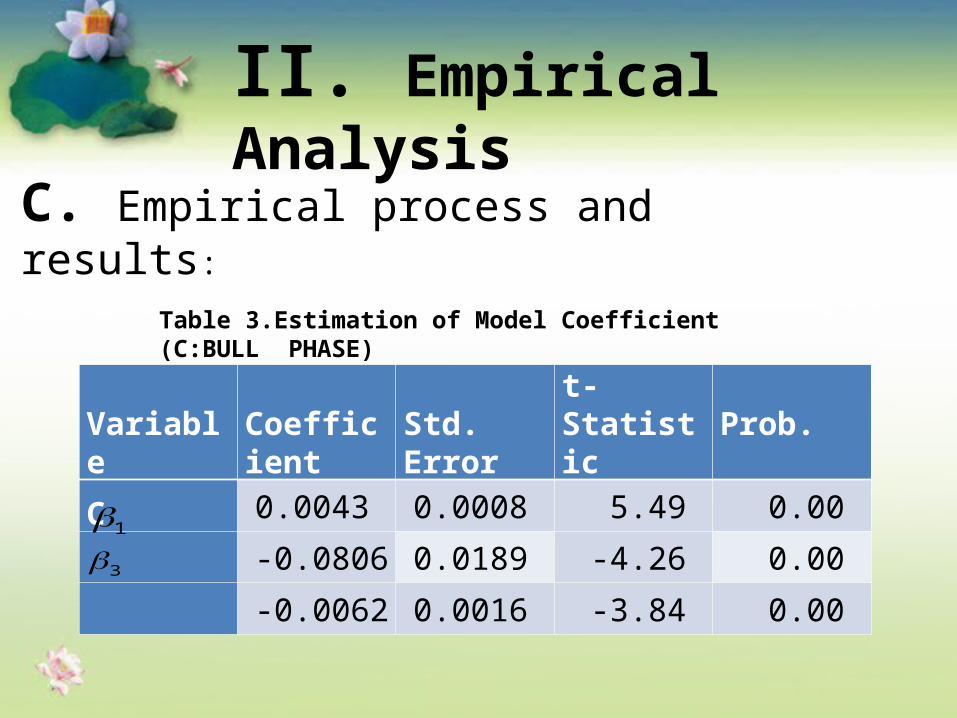

C. Empirical process and results:

Table 3.Estimation of Model Coefficient (C:BULL PHASE)

Variable Coefficient Std. Error t-Statistic Prob.

C 0.0043 0.0008 5.49 0.00

-0.0806 0.0189 -4.26 0.00

-0.0062 0.0016 -3.84 0.00 13

II. Empirical Analysis

C. Empirical process and results:

We find :

1.Individual fixed effects

2.Liquidity premium does not exist.

3.Value effect does not exist.

II. Empirical Analysis

C. Empirical process and results:

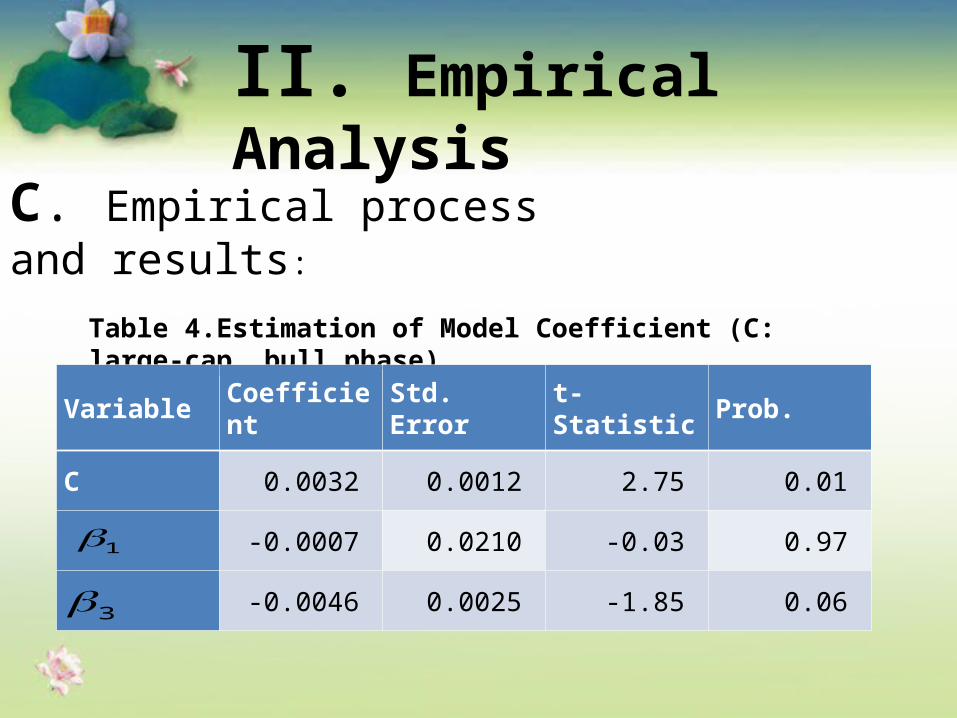

Table 4.Estimation of Model Coefficient (C: large-cap, bull phase)

Variable Coefficient Std. Error t-Statistic Prob.

C 0.0032 0.0012 2.75 0.01

-0.0007 0.0210 -0.03 0.97

-0.0046 0.0025 -1.85 0.06

1

3

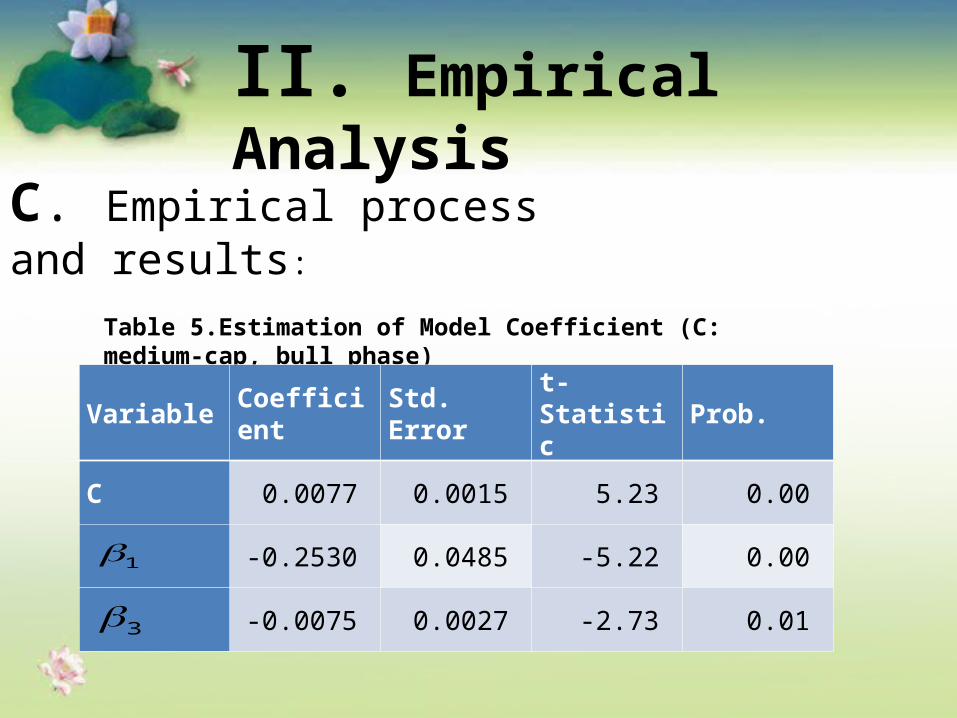

II. Empirical Analysis

C. Empirical process and results:

Table 5.Estimation of Model Coefficient (C: medium-cap, bull phase)

Variable Coefficient Std. Error t-Statistic Prob.

C 0.0077 0.0015 5.23 0.00

-0.2530 0.0485 -5.22 0.00

-0.0075 0.0027 -2.73 0.01

1

3

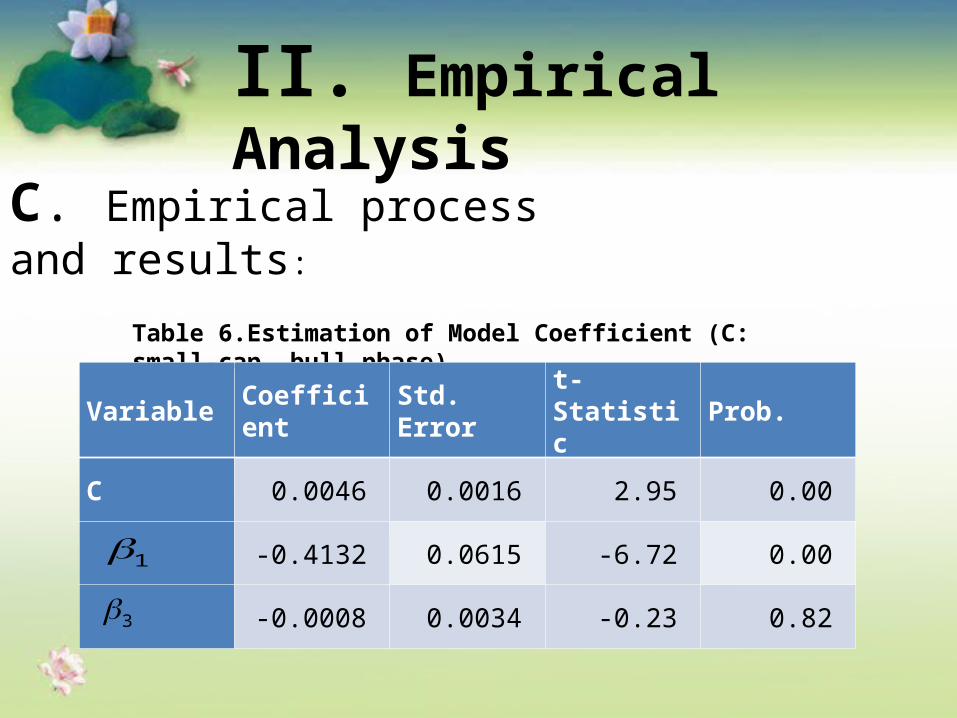

II. Empirical Analysis

C. Empirical process and results:

Table 6.Estimation of Model Coefficient (C: small-cap, bull phase)

Variable Coefficient Std. Error t-Statistic Prob.

C 0.0046 0.0016 2.95 0.00

-0.4132 0.0615 -6.72 0.00

-0.0008 0.0034 -0.23 0.82

1

3

II. Empirical Analysis

C. Empirical process and results:

Manufacturing sector (Bull phase):

There are no liquidity risk premium and value effects for the small-cap, medium-cap, large-cap stocks.

II. Empirical Analysis

C. Empirical process and results:

we similarly analyze other industry sectors, the large, medium and small cap both in the bull phase and the bear phase.

We find : The liquidity risk premium does not exist and there is a certain degree of negative correlati-on of the liquid risk and the excess return.

II. Empirical Analysis

A. Liquidity indicator:

1/h l ct t t

tt

P P PNL

T

Among them, refers to the highest stock price for the day, the lowest stock price, the closing stock price the day before, the turnover for the day.

htP

ltP

1ctP

T

III. Summary

More effective measures to manage liquidity risk:1. Further improve the trading mechanism ; 2. Strengthen the laws and regulations related to liquidity risk; 3. Nurture powerful institutional investors to improve risk control system; 4. Further build information disclosure system; 5. Develop the philosophy of rational investment and reduce the incidence of “herding”.

Thank you!