the german energiewende and implications for · pdf filethe german energiewende and...

TRANSCRIPT

RWE AG PAGE 1

The German Energiewende and Implications for Utilities

Graham Weale, Chief Economist – RWE AGUC Davis IAEE Seminar 3rd June 2014

24/05/2014

RWE AG PAGE 2

Contents

1. What is the position of the German utilities?

2. What has brought them there?

3. What changes are underway in Berlin?

4. What will be the utilities’ role in the future?

24/05/2014

RWE AG PAGE 3

The position of the German utilities – high capital invested in conventional plants…

24/05/2014

0

20

40

60

80

100

GW

OtherBig-4

Other non-RES

RES (incl.hydro)

Nuclear

Lignite

Hard Coal

Gas

0

10

20

30

40

50

60

70

€ bn

OtherBig-4

Net Capacity End 2012 Indicative capital employed based on 50% new value

Peak demand

Source: BMWi

RWE AG PAGE 4

… but making a low EBIT with declining market value and reduced investments

24/05/2014

EBIT Market Value

Investments Cumulative impairments

0

5

10

15

20

25

€ bn

-35%

2013201220112010200920082007

Vattenfall

RWE

EnBW

E.ON

0

50

100

150

200 -70%

2013201220112010200920082007

€ bn

50

160

2010200920082007 20122011

€ bn

20

15

10

5

02013

0

5

10

15

20

25

30

€ bn

2007 20122011201020092008

-45%

2015*2014*2013

Source: Company annual reports

Page 5RWE AG – CEA 01/04/2014

€ 000 / MW

20142010 2013 201520122009

0

10

20

30

40

50

60

70

80

90

2011

80

90

30

2013

10

2015

€ 000 / MW

0

2014

20

2012

40

70

60

50

2009 2010 2011

Gas plants never recovered their full costs; from2011/2012 failed to cover depreciation then O&M

New plants Old (fully amortised) plants

Normal return on capital

Depreciation

Staff & Maintenance

Annual proceeds

Annual proceeds Staff & Maintenance

Page 6RWE AG – CEA 01/04/2014

2009 2011 2012 2013 2014

100

150

€ 000 / MW

2010

0

2015

50

2013

0

20152010 201220112009 2014

50

100

150

€ 000 / MW

…but new coal plants not earning a return on capital whilst old plants covering fixed costs

New plants Old (fully amortised) plants

Normal return on capital

Depreciation

Staff & Maintenance

Annual proceedsAnnual proceeds

Staff & Maintenance

RWE AG PAGE 7

Contents

1. What is the position of the German utilities?

2. What has brought them there?

3. What changes are underway in Berlin and Brussels?

4. What will be the utilities’ role in the future?

24/05/2014

RWE AG PAGE 8

Energiewende

2010 20122011

The Energiewende – a plan to move from nuclearand coal to renewables: milestones from 1991

2050

Start ofEU

EmissionsTrading Scheme

Nuclear phase-out by 2022

Energyconcept

Nuclear operatinglifetime extension

1st Feed-in Law

Last nuclearreactor will

be shut down

80% to 90% reduction in

emissions, and 80% renewables share in

power

EEG 2012

Closure of 8 nuclear plants andchange to nuclear law to close

all plants by 2022

Eckpunkte-papier

Market Liberalization

19981991 20022000 2005 202220142004 2009

EEG 2004 12.5% / 20% power sharein 2010 / 2020

EEG 2009 35% power

share by2020

EEG Reform

1st EEG

Double RES share of

total energyby 2010

Page 9RWE AG – CEA : 01/04/2014

Further targets introduced in 2011…

W1

Currently only loosely defined goals

C

C

Limit renewables surcharge to 3.5 cents/kWh

Reduce heat demand of buildings compared to 2008

Annual rate of energy-saving renovation in housing of 2%

V Additional construction of firm fossil fuel power p lant capacity

Not availabe

- - EnEV

- - Only indirect – loanprogramme

10 GW - Not available

V1 Supply security - Strategic Reserve

C1

C2

C3

C4

C5

C6

C7

C8

N1

Increase proportion of renewables (RES) in gross fi nal energy consumption to

Increase the proportion of RES in gross elec. consu mption to

Reduce primary energy consumption compared to 2008 to

Reduce electricity consumption compared to 2008 by

Increase energy efficiency compared to 2007 by

Reduce heat demand of buildings compared to 2008 by

Increase number of electric vehicles to

Reduce final energy consumption in transport vs.200 8 by

Grid expansion according to ENLAG

35% 50% EEG

20% - Environmental tax, EnEV

10% - Environmental tax

20% - Environmental tax and otherlaws

20% - EnEV

1 Mio. 6 Mio. Energy and climate funds

10% - Reform car tax

- - EnLAG

Firm goals 2020 2030 Instruments 1

C0 Reduce greenhouse gas emissions compared to 1990 by 40% 55% ETS with German version

18% 30% Renewable heating, andBiomass laws,

N2 Punctuality of the grid connection of offshore wind farms - - EnWG

N3 Increase installed capacity of offshore wind to 10 GW 25 GW EEG

-

K1 Phase out nuclear power by 2022 2011 Nuclear Power Law

Slide 10RWE AG – 01/04/2014

1. Achievement of federal government‘s CO2 reduction target (-40 %) increasingly unrealistic2. Share of renewables rising in the case of electricity – stagnation in the transport and heating sectors3. Due to first results from coalition talks the watering down of heating efficiecy targets is likely

1. More than 80% of expansion projects still delayed2. By 2015 a number of offshore wind farms will be completed, but key grid expansion projects for

overland transmission of electricty will not be ready until that time3. At least there is some improvement in sight for offshore wind power connections to the grid

Grid expansion

… which were badly off track after just two years, except for renewables growth

Source: own calculations

78%

Sustainability

Security of supply

Costs/EEG levy

15%

50%

22%1. With 6.2 ct /kwh the EEG levy has exceeded the government‘s own threshold of 3.5 ct / kWh by far2. With the new government at least modest reforms that are targeting at limiting the costs are to

expect, so we come to an neutral outlook for the next years, but situation will not improve quickly

1. Increasing intervention by transmission system operators in the market to avoid critical situations with the power grid. The situation continued in whole 2013.

2. End of March 2013 there were some severe situations in the German grid due to very high wind feed-in.

= 41%Adherence to target path:

RWE AG PAGE 11

The implications of the Energiewende together with the 2007 global recession1. Renewables subsidy system without

any cap

– annual support originally expected to be € 0,6 bn, not € 22 bn

– has its origins in the 2000 EEG, rather than the 2011 “Energiewende”

– costs (esp. PV) continually lower than subsidies = strong incentive

2. Recession

3. Low CO2 prices

4. Low coal prices

5. Over-investment in conventional plant based on trend from early 2000’s

24/05/2014

0

5

10

15

20

25

0

1

2

3

4

5

6

2002

€ bn

201220102008200620042000

€cts/kWh

EEG levy

EEG Surcharge

CHP

Levy based on §§§§19

Offshore charges

0

50

100

150

2000 2002 2004 2006 2008 2010 2012

GW

PV

Total

Water (exc. PS)

Biomass

Wind

Renewables capacity build-up

Subsidies for the Energiewende

2000 2004 2009

RWE AG PAGE 12

Generators suffered from two effects cutting volume by 15% vs. expected level...

� 15% lower than expected demand due 60% to recession and 40% to renewables

24/05/2014

0

100

200

300

400

500

600

700

2000 2002 2004 2006 2008 2010 2012

TWh

Lower residual demand

Renewables expected base on trend to 2005

Renewables actual

Gross demand actual

Gross demand expected

Thermal power supplied by large generators

Actual and expected (as of 2005) demand and renewab les

RWE AG PAGE 13

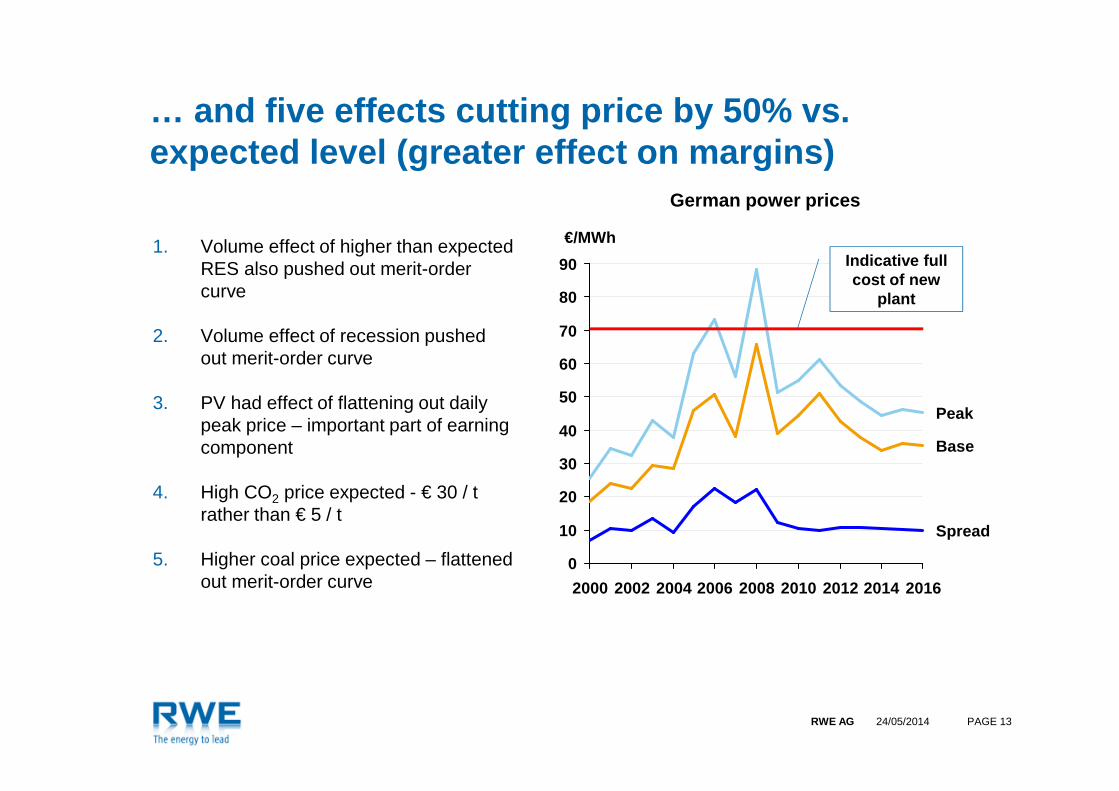

… and five effects cutting price by 50% vs. expected level (greater effect on margins)

1. Volume effect of higher than expected RES also pushed out merit-order curve

2. Volume effect of recession pushed out merit-order curve

3. PV had effect of flattening out daily peak price – important part of earning component

4. High CO2 price expected - € 30 / t rather than € 5 / t

5. Higher coal price expected – flattened out merit-order curve

24/05/2014

0

10

20

30

40

50

60

70

80

90

201620082002 2012 20142000

Base

2006

Peak

2010

Spread

2004

€/MWhIndicative fullcost of new

plant

German power prices

Page 14RWE AG – 01/04/2014

0

20

40

60

80

100

120

140

160

180

200

Peak loadMin load

MW

Germany: Merit Order 2009 (€ / MWh)

Average available

Wind / PV / Hydro / other Renew.

Renewables / CHP

Nuclear

Hard Coal

Gas

Oil / Gasoil

Lignite

Thermal plant Merit-Order 2009: new gas andhard coal plants competing strongly

Page 15RWE AG – 01/04/2014

Germany: Merit Order 2012 (€ / MWh)

0

20

40

60

80

100

120

140

160

180

200

Peak loadMin load

Thermal plant Merit Order 2012: hard coal plantswith high utilisation but gas weakening

Average available

Wind / PV / Hydro / other Renew.

Renewables / CHP

Nuclear

Hard Coal

Gas

Oil / Gasoil

Lignite

MW

Page 16RWE AG – 01/04/2014

Progressive reduction of mid-day price through PV-genera tion

The PV reduced the mid-day prices whichaccounted for high share of earnings

0

50

100

150

200

250[%]

Hour of day242322212019181716151413121110987654321

2011

2010

2009

2008

2007

PAGE 17RWE AG CEA - Weale

Power prices for industrial consumers (20-70 GWh) €ct/kWh excl. VAT

The Consumer Price has been driven up by the surcharge despite a falling wholesale price

0

2

4

6

8

10

12

2008 2009 2010 2011 2012

Base price

Consumer

Power prices for households(2.5-5 MWh) €ct/kWh incl. all taxes

0

5

10

15

20

25

30

2008 2009 2010 2011 2012

Peak price

Consumer

Source: BMWi Energiedaten 21.05.2013 and EEX

0

5

10

15

20

25

01

23

45

6€ bn

2012201020082006200420022000

€cts/kWh

EEG levy

CHP

Levy based on §§§§19

Offshore charges

EEG Surcharge

EEG Subsidies and Consumer Price Surcharge

PAGE 18RWE AG CEA - Weale

The renewables policy has led to work for 0.8% of the German workforce

� Earlier Red-Green Coalition had hopes that 500 T jobs would be created by 2020

– But loss of jobs (including growth prospects) in other sectors should be deducted

� Growing number of bankruptcies in renewables area since 2011, especially PV but also wind

100

150

200

250

300

1998 2004 2006 2007 2008 2009 2010 2011 2012 2013e

350

400000s

0

50

R&D / Admin

Hydropower

Geothermal

Biomass

Windpower

PV

Unclassified

Employees in the renewables sector

RWE AG PAGE 19

Contents

1. What is the position of the German utilities?

2. What has brought them there?

3. What changes are underway in Berlin?

4. What will be the utilities’ role in the future?

24/05/2014

Page 20RWE AG CEA - Weale

The proposal for revision of the EEG agreed in Cabinet on 8th April 2014

� Aim to reach 40-45% by 2025 then 55-60% by 2035 rene wables share of power but always ensuring affordability and supply security

� Reduce average RES cost level from €cts 17 / kWh to € 12 / kWh

� RES growth corridor will be legally fixed , with technology-specific instruments and focus on the most cost-efficient technologies

– Offshore wind 6.5 GW to 2020 and 15 GW to 2030 and afterwards 2 wind-parks p.a.

– Onshore wind and PV each a maximum growth of 2.5 GW p.a. (excluding repowering), with appropriate tariff adjustment

– Biomass maximum 100 MW p.a. (considered too expensive for more)

� Improved market integration through a market-premium approach and direct marketing

� New EEG (renewables law) will be fully EU-conform, including industry privileges

� Market design – a capacity market is envisaged medium-term

– not clear whether it will be technologically-neutral and all plants will be eligible

� Time-plan – Parliamentary process to be followed with am of entering into law 1st August 2014

Page 21RWE AG CEA - Weale

Renewables growth path proposed by new EEG compared with past…

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022 2024 2026

GW 8765

43210

Biomass

Wind Offshore

Wind Onshore

PV

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022 2024 2026

150GW

100

50

0

Total

PV

Wind Onshore

Wind Offshore

Biomass

Annual growth

Total capacity

Page 22RWE AG – CEA : 01/04/2014

The cost for power supply with a 35% RES share (target for 2020)

EE

G*

1.0

conventional generation

Price (ct/kWh)

0

4

12

17

20

60 TWh150 TWh

35 % RES 65 % Conventional

390 TWh

Ensure a cost efficient expansion of renewables

Capacity remuneration mechanism to ensure security of supply cost efficient

~600TWh

EE

G*

2.0

* EEG = German renewable energy act

Source: Federal Ministry of Economic Affairs and Energy

Page 23RWE AG – CEA : 01/04/2014

1 2 3 4 5 6 7 8 9 10

Power generation in TWh

20

18

16

14

12

10

8

6

4

2

Offshore wind

Bio

mas

s

PVOnshore wind

Average depends on technology mix

Remuneration ct/kWh

* EEG = German renewable energy act

Source: Federal Ministry of Economic Affairs and Energy

The plan to reduce the average cost forincremental RES to €cts 12 /kWh

Page 24RWE AG CEA - Weale

… and putting a limit on subsidies and the EEG surcharge even in a worst case

0

5

10

15

20

25€ bn

50% 40%

202520222020201820162014

0

Constant

Rising

2025202220202018

€cts/kWh

201620142012

8

7

6

5

4

Wholesale prices:

Subsidy costs by type

Onshore

Others

PV

Hydro

Biomass

Offshore

EEG-Surcharge

RWE AG PAGE 25

Contents

1. What is the position of the German utilities?

2. What has brought them there?

3. What changes are underway in Berlin?

4. What will be the utilities’ role in the future?

24/05/2014

RWE AG PAGE 26

Three essential elements to the supply

1. Affordability – the commodity (kWh) and service level must be delivered at lowest cost

– Use lowest cost fuels consistent with meeting EU carbon targets and most efficient plants

– Make use of existing thermal plants to provide service element

24/05/2014

2. Supply-security

– Achieved by the round-the-clock availability of conventional plants and their increasing flexibility

– Also by introduction of further flexibility along delivery chain –smart grids, smart meters etc

3. Carbon reduction

– Controlled by Emissions Trading Scheme – ensures targets are met

– Achieved by combination of renewables and fuel-switching

RWE AG PAGE 27

80

60

40

20

Mo Tu We Th Fr Sa Su

Demand

PV

Water

Thermal plants

Wind Onshore/Offshore

Biomass

GW Almost no thermal plant contribution

Some 20-30 GWcontribution

Indication of the role for thermal plants in August 2022

The integration of renewables will require a muchhigher „service“ component

� Wind and PV will become the basis for power supply; the remaining plants will optimisethemselves around this supply

� Most thermal plants will be only needed in the future at times of low wind / sun – there will be nolonger base-load plants

Source: Agora Energiewende (12 Thesen zur Energiewende, 2012)

RWE AG PAGE 28

Where are the utilities going? Shifting from kWh production to even higher emphasis on service

24/05/2014

0

100

200

300

400

500

600

700TWh

Therm - utilities

RES - utilities

Therm - other

RES - other

2035*2020*2013*2007

Less conventional production(indicative figures)

More effort on serviceQualititive Index vs. 2010

0

20

40

60

80

100

120

140

Therm. firm capacity

Therm. flexibility

Ren. firm capacity

Trading

Network

Retail

2030202020132007

RES. = renewables, Therm. = conventional thermal plants

RWE AG PAGE 29

What does flexibility mean for power plants?

1

2

Wholesale price vs. variable costs (€/MWh)

50

Power production (MW)-

0

Inflexible plant

Flexible plant

�

�400

800

600

EEX

Variable costs

� Dynamic performance

– High rate of changing load output

– Short-times for ramping up/down

� Operational flexibility

– Low minimum load with high efficiency

– High number of start p.a.

– Low costs for ramping up/down

– Short minimum load times

� Organisational flexibility

– Flexible shift models with wide range of staff qualifications

– Market-orientated maintenance plan

� Additional factors

– Permit restrictions, fuel quality and contract flexibility

RWE AG PAGE 30

Time (minutes)

600 MW - Block old position

600 MW - Blocknew position

Example Weisweiler Lignite Plant: renewal of theControl Technology increases the load rates

� Retrofitting of all 600-MW-Blocks withmodern digital control in combination withthe required technical adjustments to theplant

� Renewal of the control system is therequirement to improve the ramping

� Increasing the flexibility of the 600-MW Lignite blocks: ramping rate increased to 10 MW/ minute and minimum load to 170 MW.

� Contributes to life-time extension

� Allows the plant to operate in the secondarymarkets

0

100

200

300

400

500

600

MW

RWE AG 01/04/2014 31

RWE Contributions downstream - Smart grids

Quelle: ZSW

RWE AG 01/04/2014 32

Summary – examples RWE: future earnings shifting from production to service side

RWE develops towards an attractive stable downstrea m business profile with additional focus on renewables and upside potential from conven tional power generation

6.4

51%

48%

24%

55%

Operating result in € bn

5.9

4.5 – 4.9e

<20%

>60%

UpstreamGas & OilRenewables

Distribution andSupply

Conventionalpower generation

Trading GasMidstream 2012 2013 2014e

5%–10%

Of whichcirca40%-50%regulated

>70%

10%–15%

Mid-term

4

RWE AG PAGE 33

THANK YOU VERY MUCH FOR YOUR ATTENTION.

+ 49 201 17 17471 or + 49 162 254 4846