taxlab - deloitte us organising the tax function april 17, ... increased access to internal tax risk...

TRANSCRIPT

TaxLab

Organising the tax function

April 17, 2014

Robbert Hoyng

© 2014 Deloitte The Netherlands

Denying the future

Agenda

• Tax function model

• Tax transformation

• Approach

• Q&A

Tax function model

© 2014 Deloitte The Netherlands

Roadmap

2014 2015 2016 2017

2018

© 2014 Deloitte The Netherlands

Poll Question #1

Wat zijn de belangrijkste uitdagingen van jouw tax functie?

1. Budget druk

2. Personeelsmanagement & resourcing

3. Korte closing periode

4. Bijhouden van nieuwe wet- en regelgeving

5. Data kwaliteit en beschikbaarheid

6. Andere

© 2014 Deloitte The Netherlands

Poll Question #2

Wat kost de organisatie van de tax processen,

per 100mio revenue ?

1. 25.000 euro

2. 100.000 euro

3. 200.000 euro

© 2014 Deloitte The Netherlands

Case studyGlobal tax management challenges

US• Sarbanes-Oxley regulations• Schedule M3 reporting requirement• Uncertain tax position disclosures

Europe

• Trend is to move to e-audits and deliver standard audit file (i.e. new German E-Filing requirements)

Australia• Businesses are assigned a risk rating

by the Australian Tax Office. • Derived from data analytics and risk

profiling techniques

China• Authorities granted

increased access to internal tax risk control systems

India• More audit-based controls • Introduction of strict penalty

provisions including prosecutionBrazil• Elimination of corporate tax return

filings due to large amounts of data maintained by authorities

© 2014 Deloitte The Netherlands

Case studyGlobal tax management challenges

© 2014 Deloitte The Netherlands

Poll Question #2

Welke activiteit kost het meeste tijd van de tax functie gedurende het

jaar?

1. Algemeen management (tax function)

2. Tax planning

3. ‘Business partnering’

4. Jaarlijkse compliance & reporting

5. Transactionele compliance

6. Transfer pricing

7. Vragen en audits

8. Andere

© 2014 Deloitte The Netherlands

European Tax Directors

© 2014 Deloitte The Netherlands

What is necessary for a world-class Tax Function

Effectiveness

Efficiency

Transparency

Strategy

Order 2

Cash

Procure 2

Pay

Record 2

Report

Roles and Responsibilities

Governance

Group Tax SSCFinance Business

Tax processes

Stakeholder Management

Strategic

direction

Key tax and

reporting

activities

Business

Inquiries &

auditsAnnual

CompliancePlanning

Transaction

Compliance

ReportingTransfer

PricingOther

Organisation People Data Systems RiskSupporting

infrastructure

© 2014 Deloitte The Netherlands

EffectivenessTax strategy in line with the business

© 2014 Deloitte The Netherlands

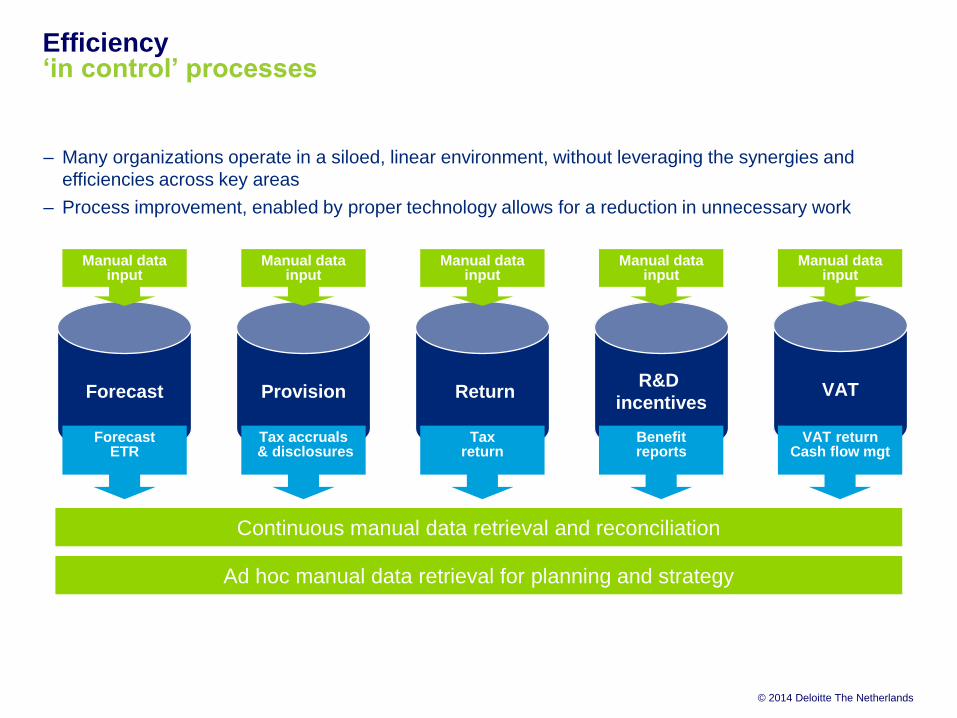

Efficiency‘in control’ processes

– Many organizations operate in a siloed, linear environment, without leveraging the synergies and

efficiencies across key areas

– Process improvement, enabled by proper technology allows for a reduction in unnecessary work

Continuous manual data retrieval and reconciliation

Ad hoc manual data retrieval for planning and strategy

Forecast

Manual data input

Forecast ETR

Provision

Manual data input

Tax accruals& disclosures

Return

Manual data input

Taxreturn

R&D

incentives

Manual data input

Benefit reports

VAT

Manual data input

VAT returnCash flow mgt

© 2014 Deloitte The Netherlands

Efficiency (cont’d)Record-to-report cycle

Tax process

Output

Reports

IFRS taxDisclosures

HFM, SAP BPC, and IBM Cognos.

Co-only

Manual

ERP

Excel

Input

Source data Data collection Consolidation

Process

Co-only

Local GAAPTax

Disclosures

Manual data

Webform

Tax Data

IFRS Data

Local GAAP data

Calculation

Tax Forecasting

CIT or VATtax return

© 2014 Deloitte The Netherlands

© 2014 Deloitte The Netherlands

TransparancyStakeholder management

© 2014 Deloitte The Netherlands

Transparancy (cont’d)Stakeholder management

Tax transformation

© 2014 Deloitte The Netherlands

Poll Question #3

Welke van de volgende gebieden hebben de grootste impact op

transformatie binnen jouw tax functie?

1. Beschikbare resources / mensen / capaciteit

2. Ons technologie landschap

3. Waardering voor tax van ons management (CFO/CEO etc.)

4. Koppeling corporate strategie met de tax strategie

5. Andere

© 2014 Deloitte The Netherlands

Tax transformationAlignment with business maturity

The role (and potential need for improvement) of the Tax Function varies with the maturity level of the

organisation.

Growthrate

Time

Phase 1 - Introduction Phase 2 - Growth Phase 3 - Maturity

Operational risk management Avoid failures, e.g. fraudMeet Business Control Framework

requirements

Meet Business Control Framework

requirements

Tax planning Utilisation of tax facilities Avoid business disruptionActively manage tax portfolio through

planning

Tax compliance / filing Compliance oriented Process oriented IT oriented

Tax reporting Report ETR Manage ETR Plan ETR

Risk No risk register Periodic risk register Continuous monitoring

1

2

3

© 2014 Deloitte The Netherlands

Tax transformation (cont’d)Alignment with business maturity

Driving Value through

Analytics

Concentration of

processes

Valu

e

Standardisation of

processes

1

2

3

Automation of

processes

Time

4

Approach

© 2014 Deloitte The Netherlands

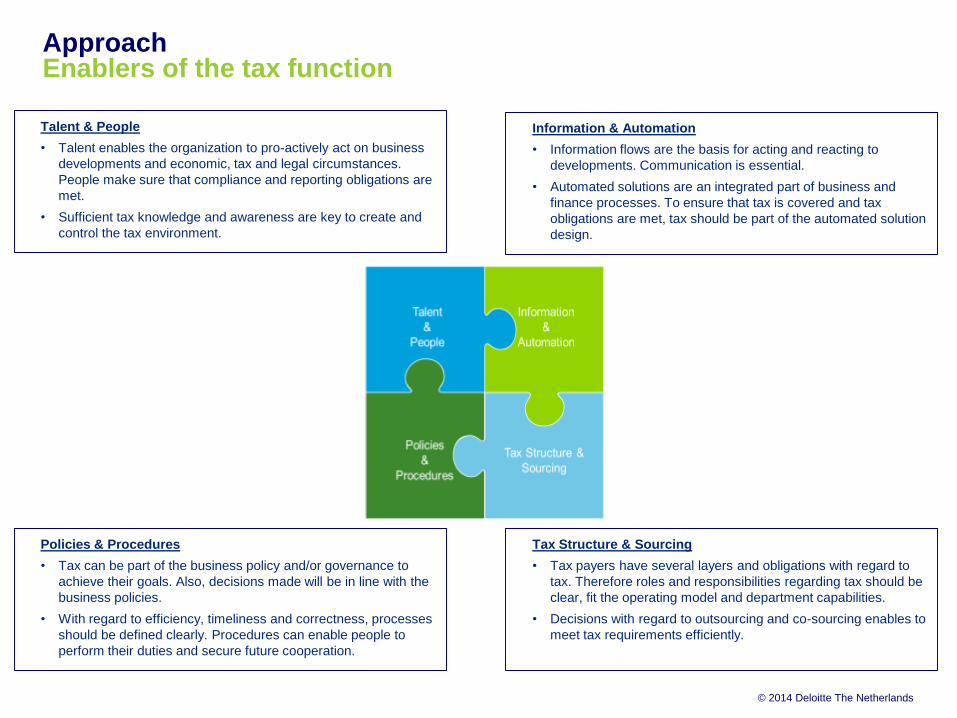

ApproachEnablers of the tax function

Talent & People

• Talent enables the organization to pro-actively act on business

developments and economic, tax and legal circumstances.

People make sure that compliance and reporting obligations are

met.

• Sufficient tax knowledge and awareness are key to create and

control the tax environment.

Information & Automation

• Information flows are the basis for acting and reacting to

developments. Communication is essential.

• Automated solutions are an integrated part of business and

finance processes. To ensure that tax is covered and tax

obligations are met, tax should be part of the automated solution

design.

Policies & Procedures

• Tax can be part of the business policy and/or governance to

achieve their goals. Also, decisions made will be in line with the

business policies.

• With regard to efficiency, timeliness and correctness, processes

should be defined clearly. Procedures can enable people to

perform their duties and secure future cooperation.

Tax Structure & Sourcing

• Tax payers have several layers and obligations with regard to

tax. Therefore roles and responsibilities regarding tax should be

clear, fit the operating model and department capabilities.

• Decisions with regard to outsourcing and co-sourcing enables to

meet tax requirements efficiently.

© 2014 Deloitte The Netherlands

ApproachExample roadmap

Standardization

Topic2014 2015 2016

Ambition

2020

E2E Manage Taxes

Process

• Cycle time filing & reporting

• Accurate compliance & reporting

• Process excellence

• Sustainable monitoring and tax

control

• Integration and standardization of

enabling landscape and system

architecture

Maintain tax master

data • Clear guidelines for TP policy

implementation into master data

Maintain tax policies

& procedures

• Implement standardized processes

• Clearly defined roles &

responsibilities and back-up

structure

• Shared, standardized information,

documentation, resources and

policy & procedures

Perform knowledge

management

• Sufficient, shared and sustainable

tax knowledge and awareness

throughout the global organization

Perform tax

planning/strategy

• Optimization of sustainable tax

planning and global tax cash

optimization

Perform tax risk

management• Standardized tax risk management

process facilitated by automation

Monitor tax

compliance• Insight in global tax compliance

status

Manage tax

provisions• Standardized and optimized UTP

recognition and determination

Perform tax reporting• Automated (improved) tax reporting

template for efficient consolidation

and tax reporting positions

Prepare returns

(indirect) • Automated tax determination

Identification Roll-outPilot Value realization

Phase

T05 Design PIL

T05 Implement PIL

T02 VAT Analytics T04 Data analytics (improvement initiatives)

T01 TA Analytics T04 Data analytics

T03 T&C Analytics T04 Data analytics

T06 Tax Dashboard

T07 TP

RACI

T10 RACI

T11 Central Repository

T12 GSA

T13 Esc

T14

T15 Tax Learning

T16 Scenario Planning

T17 Tax Opt Study

T18 Tax Risk Control

Monitoring

DDT

T21 UTP

T22 Tax Pack

T23 Automate AP

T24 VAT add on

T08 Process

T09

P&P

Aris

T19

T20

© 2014 Deloitte The Netherlands

ApproachExample roadmap (cont’d)

Roll-out

1. Remaining countries / entities / tax processes

2. Current state analysis

3. Fit-gap analysis

4. Implementation of Tax processes, RACI, Control Measures, P&P, Tax Dashboard

and Central Repository

Roll-out (based on project charters) remaining standardization projects

Prioritize & Project

Charter

RACI / Control

Measures

Tax Central

Repository / Tax

DashboardTax processes

The level 4, 5 and 6 To-Be

standardized process

design and documentation

for tax has been delivered

Validation workshops

Tax strategy workshop

Prioritize standardization

topics

Develop project charter for

all key defined projects

with the objective to

schedule budget and

resources

Design To-Be

standardized RACI’s and

Control Measures for all

tax processes on level 5

and 6

Assumption that level 4

design has been

performed by xxx.

Draft To-Be Tax Policies &

Procedures

Tax Policies & Procedures

will be based on existing

materials

Functional design req.

repository for shared,

standardized processes,

information, resources and

policy & procedures

Functional design req.

dashboard to create clear

overview of tax kpi’s

Q1/2/3/4/2014 Q4 2014

De

sig

n

Review/Analysis Pilot ImplementationTax processes, RACI, Control Measures and Policies &

Procedures

Q1/2 2015 Q1/2 2015

Pilot implementation:

1. Selection of countries / entities / tax processes

2. Current state analysis

3. Fit-gap analysis

4. Implementation of Tax processes, RACI, Control Measures and P&P

Pilot implementation review consisting of:

1. Evaluate of pilot implementation (1) start-up and design, (2) Implementation

and (3) Handover, Operations and User Perspective

2. Lessons learned per key issue, lessons and action (to be) taken

3. Transition to Roll-outPilo

t Im

ple

men

tati

on

Remaining standardization topicsTax processes, RACI, Control Measures, Policies &

Procedures, Central Repository and Tax Dashboard

Q2/3 2015 2015 / 2016

Ro

ll-o

ut

Policies &

Procedures

Q1 2015

© 2014 Deloitte The Netherlands

Questions and answers

© 2014 Deloitte The Netherlands