slovak startups report 2016 - part of v4 startup survey (1)

TRANSCRIPT

sapie

SLOVAK STARTUPS REPORT 20162

SLOVAK STARTUPS REPORT 2016 3

CHAPTER 3

CHAPTER 6

CHAPTER 1

CHAPTER 4

CHAPTER 2

CHAPTER 5

Introduction 04

Financing 22

Innovation,challengesandopportunities 36

ExecutiveSummary

Metodhology,contribition,abouttheauthor,organizationandpartners

Startupmetrics 08

Employment 30

Recommendations 40

Business 16

Export 34

Table of contents

INTRODUCTION

4 SLOVAK STARTUPS REPORT 2016

Slovakiaisasmallcountryfullofgreat

ideas.The startup ecosystem is fairly young as the first steps of getting to know each other and starting to collaborating were taken in 2009.Allofftheactivitiescamefromthecom-munityandentrepreneurs.Nowtheecosystemisslowlymaturing.Therearemoreplayersinvolved,andthegovernmentisrealizingthepotentialofinnovation,andtheaddedvalueofthesebusinessesfortheeconomy.

Startupfoundersunderstandthatthelifeofanentrepreneurisexcitingandchallengingatthesametime.AseveralSlovakstartupshaveturnedintosuccessfulcompanieswithglobalreach.PixelFederation,Sygicandotherwithaglobalreachsuchcompaniesnowfallintothecategoryofscale-upsasdefinedbySherryCou-tuintheScale-upReport1.Thesearethestarseveryoneislookingat.

Petra Dzurovčinová, Executive Manager at the Slovak Alliance for the Innovative Economy

Introduction

1Definitionofscale-up:Scale-upsareenterpriseswithaverageannualizedgrowthinemployees(orinturno-ver)greaterthan20percentayearoverathree-yearperiod,andwith10ormoreemployeesatthebeginningoftheobservationperiod.TheScale-upReportonUKEconomicGrowth–http://scaleupreport.org/

INTRODUCTION

5SLOVAK STARTUPS REPORT 2016

Aeromobil,oneofourmostfamousstartups,managedtobringtogetherahighlyprofes-sionalandskilledteam,auniqueproductandaninternationalaudience.Theyarealsoagreatexampleofastartupthatbreaksthestereotypeandwasfoundedbydrivenandexperiencedprofessionals.Thereisanincreasingnumberofpeoplewhodecidetostarttheirownbusi-nessaftergatheringsomeexperienceworkinginacompany.Theirprimarygoalisnotthespot-lightandmediaattention,buttocreateinnova-tiveproductsthatareuniqueandwell-receivedacrosstheworld.

We can see that there is no lack of ideas in Slovakia and the V4 region.Whatweneedisgoodpolicy,astablelegislativeenvironment,skilledprofessionalsandresourcessothatwecancreateaworld-classSlovakia.

INTRODUCTION

6 SLOVAK STARTUPS REPORT 2016

Executive summary

1 Slovak startups are young.60% ofthemhaveincorporatedinthelastthreeyears(2014–2016)

2 78%ofSlovakstartupslookto globalmarkets.The majority of them want to, or already export to the US (43%) or EU countries (65%). Only30%ofthemarelookingatmarketsinAsia

3 There is an increasing number of female founders.30%offoundersarewomen.Womenarealsorepresentedasemployees(41%)

4 83%ofSlovakstartupfounders areaged20–39

5 Mostofthestartups(39%)areintheValidation/ Pre-seed stage:theyhaveabetaversionortestedprototypewhichtheyarefine-tuningthroughincubationandaccelerationprogramsinthe Efficiency/ Seed-stage: product putonmarket,earlyrevenuefromsales,trademodelestablished

6 Amongthebiggestinternalchallengesforthemareinvestment and human resources. Externally,thebiggestissuesareconcerningexport and entering new markets, tax systems and legislative framework

INTRODUCTION

7SLOVAK STARTUPS REPORT 2016

7 Theyareeitherfinancingtheirven-turesthroughtheirown capital (87%), busi-ness angel (30%) or through a VC fund (local and abroad) 24%

8 Over50%ofthemaredevelopinganewproductorserviceinthetopthreethefieldsofweb services (26%), SaaS (26%) and mobile software services (23%)

9 Theyarealsoplanningtogrow in the number of employees in the next 6 months, 47%ofthemwanttohire1–3employeesand33%alreadydidinthepast3months

10 45%ofthemare planning to open a branch abroad

11 68%ofthemareregistered as a businessinthewesternpartofSlovakia, withBratislavarepresenting75%

12 70%ofcompaniesarelimited liability companiesregisteredinSlovakia (s.r.o.)oritsequivalentabroad

8

CHAPTER 1 STARTUP METRICS

SLOVAK STARTUPS REPORT 2016

Who are they

Slovak startups are young and highly educated. 83%areaged20–39years.67%ofthemhavetertiaryeducation,with21%currentlystudyingatuniversity.Theirlevelsandfieldsvarythough,withthemostpopularfieldsbeingtechnical–mainlycomputersciences(appliedinformaticsorprogrammingcourses)andbusiness–rep-resentedbymarketingandmanagement.Theyhavechosenartanddesigninsmallernumbers.

Startup metrics

5% <20 45% 20–29 38% 30–39

19% Secondary 66% Tertiary

6% 40–49 6% >50

21% University 13% PhD.

Age The highest level of education attained by founder(s)

Thelargestpartoftheresponsescamefromthoseagedbetween20and29years.Thisgrouprepresented45%ofallsurveyresponses.Thesecondmostpopulatedgroupwasbetween30and39yearsold,with38%.Only6%ofre-spondentsthatwerebetween40and50yearsoldrespectively.Only4%wereyoungerthan20yearsold.

Thenumberoffemalefoundersisincreasing.30%ofstartupshavewomenasfoundersorco-founders.Amongstartupemployees,womenmakeup40%ofthebase.

9

STARTUP METRICS CHAPTER 1

SLOVAK STARTUPS REPORT 2016

Location

ThemajorityofSlovakstartupschooseSlovakiaastheircountryofregistration(89%).WesternSlovakiaisthemostpopularplaceforregistra-tion–68%residehere.Furthermore,themajor-ityofthosewhostatedtheiroriginalmunicipal-ityinthewesternpartofSlovakiaarelocatedinitscapital–Bratislava.

Afewstartupsarealsoregisteredinthesouth-ernpartofwesternSlovakia,inNovéZámkyandŠamorín.OthercitiesintheWesternpartincludePiešťanyandNitra.

ThecentralandeasternpartofSlovakiaareequallyrepresentedinthesurvey,withhubsinŽilinaandBanskáBystricainthecenterandKošiceintheeast.

10%CentralSlovakia

10%EasternSlovakia

68%WesternSlovakia

75%Bratislava

10

CHAPTER 1 STARTUP METRICS

SLOVAK STARTUPS REPORT 2016

Do you have or intend to have a branch abroad?

Looking outside Slovak borders

19%ofstartupshaveasubsidiaryabroadand45%plantohaveoneinthefuture.Ofthesubsetofthosehavinganestablishedbranchabroad,onethirdislocatedinUSAandtwothirdsarelocatedintheEU,withtheCzechRepublicasthemostpopulardestination.

27%No

44%Plan

19%Yes

CHAPTER1 STARTUPMETRICS

SLOVAKSTARTUPSREPORT201610

11

STARTUP METRICS CHAPTER 1

SLOVAK STARTUPS REPORT 2016

Legal form of your company Planned legal form

Legal forms

Inregardstothelegalformoftheirenterprise,thedatashowsthatthemostpreferedformisalimitedliabilitycompany(LLC)oranothercountry-specificversionofaprivatelimitedcompany–SROinSlovakRepublicorIVSinDenmark.Thislegalformdominatedtheresultswithaproportionalrepresentationof70%followedby17%ofrespondentsusingtheformajoint-stockcompany,and3%ofrespondentsbeingself-employed.

17% Joint-stockcompany 70% Limitedliabilitycompany 10% Other 3% Self-employed

87% LimitedLiability 13% Joint-stockcompany

Someoftherespondentshaven’tfoundedtheircompanyyet.Mostoftheserespondents(87%)areconsideringalimitedliabilitycompanyoverajoint-stockcompany.

12

CHAPTER 1 STARTUP METRICS

SLOVAK STARTUPS REPORT 2016

Slovak startups are young companies

60%ofthemhaveincorporatedinthelastthreeyears(2014–2016).Themajorityofstartups(37%)werefoundedin2015.Ontheotherhand20%ofprojectshavebeenaroundsince2011andlonger.

Thosewhohaven’tcreatedalegalentityareworkingontheirprojectsince2015(33%) orformorethan3years(58%).

39%ofstartupsarenowattheValidation or Pre-seed stagewithabetaversionortestedprototypethatisbeingfine-tunedthroughincubationandaccelerationprograms.Thesecondlargestgroup(30%)istheEfficiency or Seed Stagewithaproductorserviceputonthemarket,earlyrevenuefromsales,andabusi-nessmodelestablished.

6% 2016 37% 2015 17% 2014

3% 2017 6% 2016 33% 2015

10% 2013 10% 2012 20% 2011&older

30% 2014 27% 2013&older

Year of registrat ion Date when your project was launched

13

STARTUP METRICS CHAPTER 1

SLOVAK STARTUPS REPORT 2016

36% Yes 64% No

Have you been previously involved in a startup?

Other startup experience

36%ofrespondentshavebeeninvolvedinan-otherstartupinthepast,whichshowsthatthecultureofentrepreneurshipisimprovingandserialentrepreneursareontherise.Somemighthavefailedorsuccessfullyexitedtheirpreviousventures,andtheyhavedecidedtotryagain.

14

CHAPTER 1 STARTUP METRICS

SLOVAK STARTUPS REPORT 2016

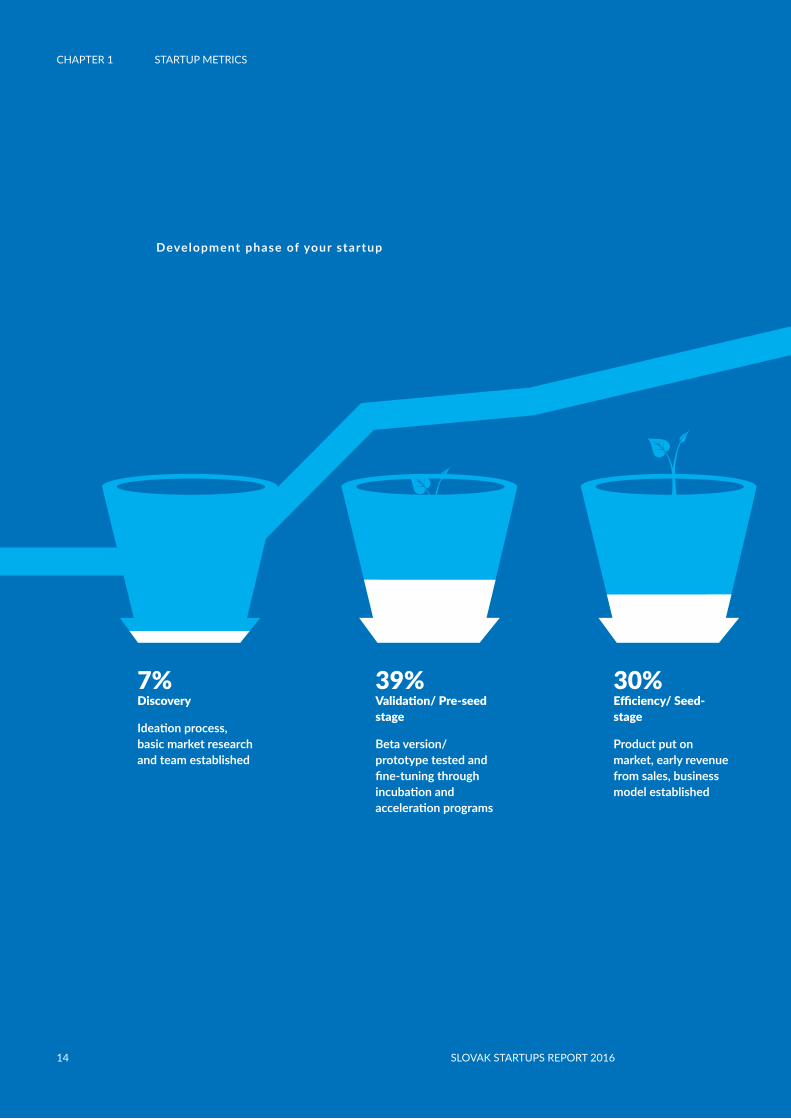

Development phase of your startup

7%Discovery

Ideation process, basic market research and team established

39%Validation/ Pre-seed stage

Beta version/prototype tested and fine-tuning through incubation and acceleration programs

30%Efficiency/ Seed-stage

Product put on market, early revenue from sales, business model established

CHAPTER1 STARTUPMETRICS

14 SLOVAKSTARTUPSREPORT2016

15

STARTUP METRICS CHAPTER 1

SLOVAK STARTUPS REPORT 2016

11%Scale/ Series A

Increasing revenues and market share, growth strategies developed

11%Establishing/ Series B

Established user base and business model

2%Maturing/ Series C

Expanding and acquisitions

STARTUPMETRICS CHAPTER1

15SLOVAKSTARTUPSREPORT2016

16

CHAPTER 2 BUSINESS

SLOVAK STARTUPS REPORT 2016

Business

TheSlovakstartupecosystemwascreat-edbottom-up,basedontheenthusiasmofin-dividualyoungentrepreneurs.One of the most important elements was help and mentoring from successful and experienced entrepreneurs, while many co-working spaces have been sup-ported by successful businesses and corporate partners.Amongtheimportantcornerstonesformingthestartupcommunitywasthe StartupAwards.SKcompetition,whichplayedtheroleofconnectingtheentireecosystem.Thegovernmenthasrealizedonlyrelativelylatethattheneedtosupportthedigitaleconomyiscrucialforthefutureandsuccessofournation.

The critical question for the future is if these public activities can be tied to already existing initiatives by the private sector. Onlycoopera-tionbetweentheprivateandpublicsectorscanbringsynergiesandnotdistorttheecosystem.Thereisnootherchoiceforthefutureoftheinnovationeconomy.

Peter Kolesár, CEO at Neulogy

17

BUSINESS CHAPTER 2

SLOVAK STARTUPS REPORT 2016

Character of products

77%ofstartupsprovidetheircustomerswithproducts,66%withservices,and28%withtechnology.Formostoftherespondentsthecasewasacombinationofthese.

77% Product 66% Service 28% Technology

What does your startup offer? (mult iple answers)

18

CHAPTER 2 BUSINESS

SLOVAK STARTUPS REPORT 2016

Industry

Ourrespondentscoveredawiderangeofdigitalandinnovationindustries.Themostrepresent-edinourstudywereSaaS,thewebservicesandmobilesoftwareservicesindustry.

26%

SaaS

13%

MarketingTechnologies

2%

Marketplace

2%

ProgrammingDevelopmentTools

11%

E-Commerce

4%

Analytics/ResearchTools/BusinessIntelligence

13%

CloudTechnologies

4%

Big Data

26%

Webservices

6%

Internet ofThings

23%

MobileSoftwareServices

4%

Electronics/Robotics

Theyarefollowedbytheeducationsector,Cloudservices,e-commerceandsoftwarehouseservices.Ourrespondentsoftencombinemultiplesectorsintheiroffering.

Which industry do you operate in?

19

BUSINESS CHAPTER 2

SLOVAK STARTUPS REPORT 2016

6%

VirtualReality/AugmentedReality

9%

Telecommuni-cations

11%

Software house

6%

Content/SocialServices

15%

Education

21%

Other

6%

Gaming/Entertainment

2%

Transport/Logistics

2%

Lighting

9%

Finances

6%

LifeScience/Healthcare

2%

BusinessServices

2%

MicroandNa-noelectronics

4%

HRservices

6%

AdvancedManufacturingTechnologies

2%

Telemedicine

6%

Energy

4%

Design

...

20

CHAPTER 2 BUSINESS

SLOVAK STARTUPS REPORT 2016

SlovakstartupsservebothB2CandB2Bmarkets.Individualconsumersareatargetgroupfor60%ofstartups.SMEsaretargetsforthemajorityofstartups,with38%ofmicrobusinesses,53%ofsmallbusinesses,55%ofmediumbusinessesand49%oflargeenterpris-es.Only26%ofcompaniesprovidesolutionsforpublicinstitutions.

Target customers

69%

38%

53% 55%49%

26%

Individuals Micro enterprises(upto10employees)

Smallenterprises(10–50employees)

Mediumenterprises(51–250employees)

Largeenterprises(morethan250employees)

Publicinstitutions(e.g.schools,hospitals,

governmentalagencies)

20 SLOVAKSTARTUPSREPORT2016

21

BUSINESS CHAPTER 2

SLOVAK STARTUPS REPORT 2016

Withregardstothenoveltyoftherespectiveproducts,51%ofstartupprojectsofferanewlydevelopedproductofservice,13%provideanupgradeto,orinnovationofaproductbeingal-readyavailableonthemarket,26%eitheradaptanavailableproductordirectlyimitateit,and11%areuncertainoftheanswer.

51%

13%

26%

11%

Newproduct or service

Weupgradeaproduct or service

Weimitateandadjusta product orservice

Hardtosay

Character of your product or service

21SLOVAKSTARTUPSREPORT2016

22

CHAPTER 3 FINANCING

SLOVAK STARTUPS REPORT 2016

Financing

Slovakia'sshortcomingsasastartupandinnovationhubstemprimarilyfromunderlying,systemicissueswhichneedcoordinatedactionforboththemid-andlong-termpublicandpri-vateactors.Whileinthelastfiveyearswehaveseenactivityandgrowthfavouringstartupsonbasicallyallfronts–universities,publicagen-cies,privateincubators,investmentsandmediaattention–thiswasmorearesultofpent-upenergybeingreleasedprimarilyduetothefirstangel,acceleratorandVCinvestments

andfirstcommunitymobilizingevents andinitiatives.

From the point of view an investors, there are only three problems – people, people, people. First,becauseoftherelativelyclosedimmigra-tionpolicy,Slovakfounderstendtobelimitedininternationalexperienceandmuch-neededlanguageskills.Second,thelong-neglectededucationsystem,particularlyatthetertiarylevel,doesnotproduceenoughbusinessand

Michaela Jacová, Investment Manager at Neulogy Ventures, co-founder of Startup Awards.SK

23

FINANCING CHAPTER 3

SLOVAK STARTUPS REPORT 2016

technicaltalent,muchlessfounderswithskillssetinboththeseareas.Importantly,muchofthistalentmovesoutofthecountry,whereitisnurturedandmotivated.Reversingthisbraindrainisatoppriorityissuefortheprivatesec-tor,particularlyduetothelackofhome-grownexcellenceinthechronicallyunderfundedR&Dbase.Third,duetohistoricalandculturalreasonsincombinationwiththeabove,Slovakialacksaprominent,engagedandabundantclassofmid-careertoretiredserialentrepreneurs

withwealthofbothcapitalandinternationalbusinessexperiencethatwouldbereadilyavail-abletofirst-timefoundersinbothmentorshipandinvestmentroles.Unless we take action to address this talent problem, the growth of Slovakia's innovation ecosystem will be sub-op-timal for the years to come.

24

CHAPTER 3 FINANCING

SLOVAK STARTUPS REPORT 2016

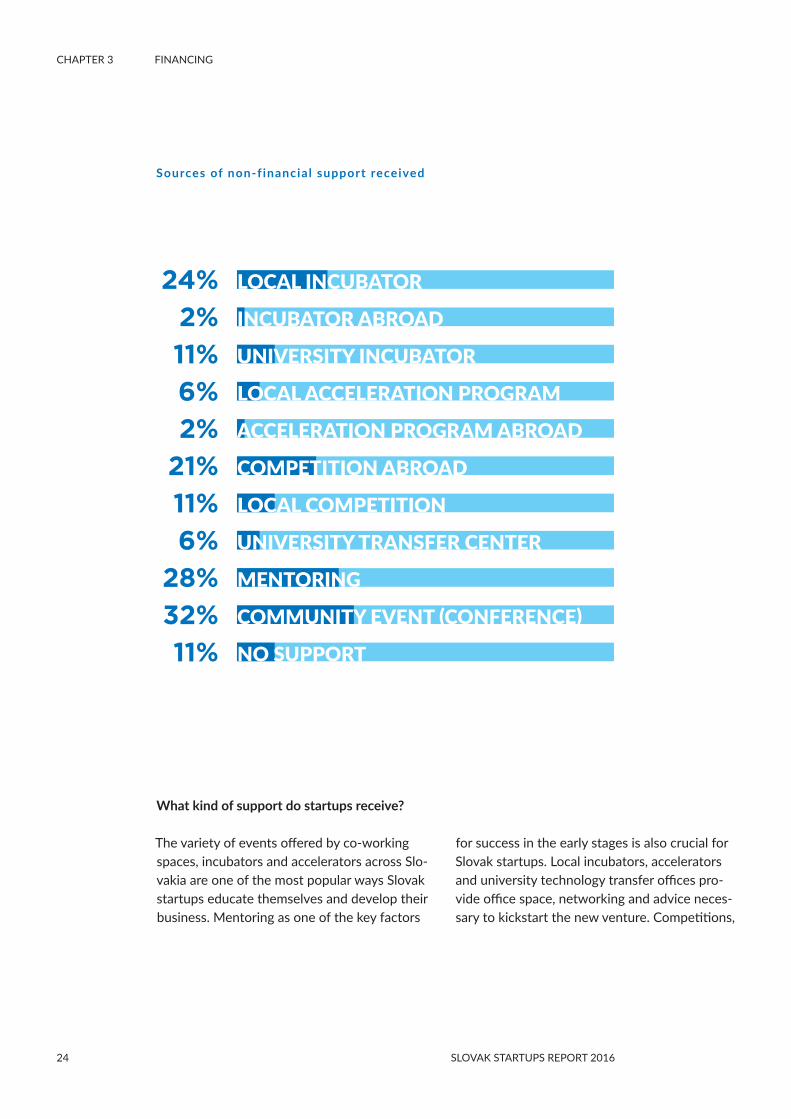

What kind of support do startups receive?

Thevarietyofeventsofferedbyco-workingspaces,incubatorsandacceleratorsacrossSlo-vakiaareoneofthemostpopularwaysSlovakstartupseducatethemselvesanddeveloptheirbusiness.Mentoringasoneofthekeyfactors

Sources of non-f inancial support received

24%2%11%6% 2%

21%11% 6%

28% 32%11%

forsuccessintheearlystagesisalsocrucialforSlovakstartups.Localincubators,acceleratorsanduniversitytechnologytransferofficespro-videofficespace,networkingandadviceneces-sarytokickstartthenewventure.Competitions,

LOCAL INCUBATOR

INCUBATOR ABROAD

UNIVERSITY INCUBATOR

LOCAL ACCELERATION PROGRAM

ACCELERATION PROGRAM ABROAD

COMPETITION ABROAD

LOCAL COMPETITION

UNIVERSITY TRANSFER CENTER

MENTORING

COMMUNITY EVENT (CONFERENCE)

NO SUPPORT

25

FINANCING CHAPTER 3

SLOVAK STARTUPS REPORT 2016

If you have used the services of a business incubator or accelerator, what was your motivation? (mult iple answers)

15%Information about funds

47%Mentoring and business advice

32%Networking with potential sponsors

13%Office space

eithernationalorinternational,areagreatwaytoraiseawareness,promoteideasandeventuallyaimtogaincustomersandinvestors.11%ofstartupscouldbeconsidered“lonewolves”thatneverre-ceivedorrequiredanyhelpwiththeirventure.

FINANCING CHAPTER3

25SLOVAKSTARTUPSREPORT2016

26

CHAPTER 3 FINANCING

SLOVAK STARTUPS REPORT 2016

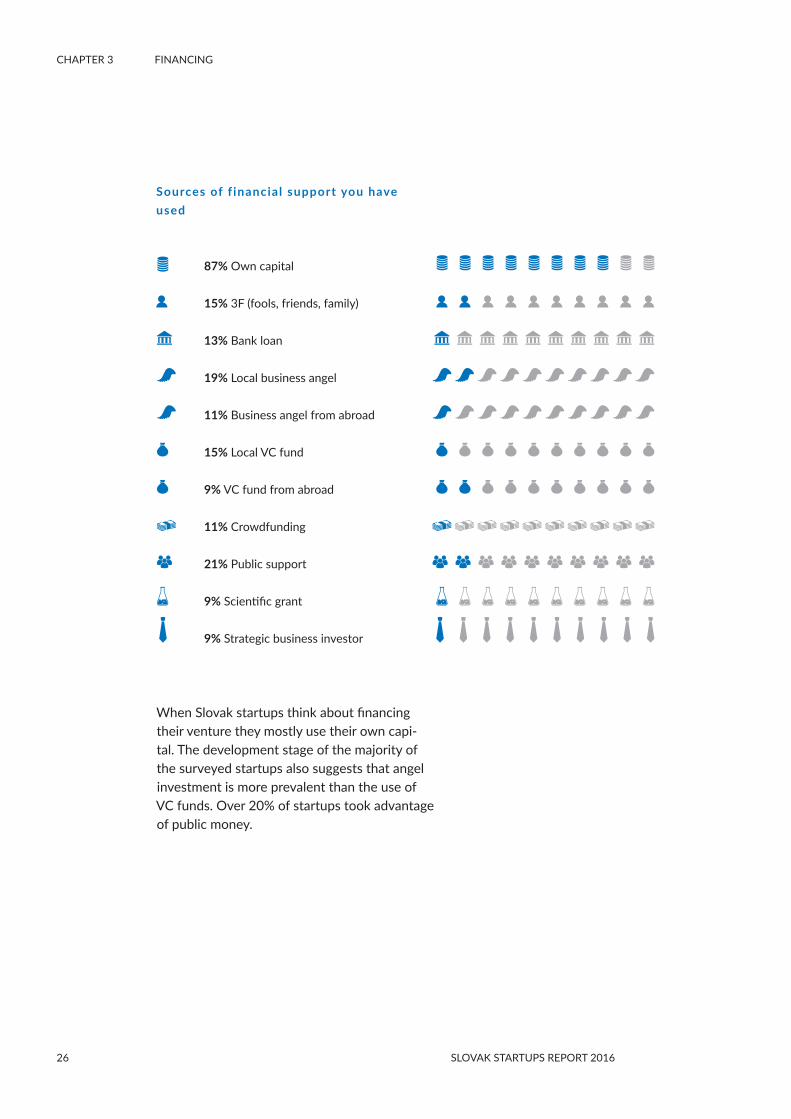

WhenSlovakstartupsthinkaboutfinancingtheirventuretheymostlyusetheirowncapi-tal.ThedevelopmentstageofthemajorityofthesurveyedstartupsalsosuggeststhatangelinvestmentismoreprevalentthantheuseofVCfunds.Over20%ofstartupstookadvantageofpublicmoney.

Sources of f inancial support you have used

87%Owncapital

15%3F(fools,friends,family)

13%Bankloan

19%Localbusinessangel

11%Businessangelfromabroad

15%LocalVCfund

9%VCfundfromabroad

11%Crowdfunding

21%Publicsupport

9%Scientificgrant

9%Strategicbusinessinvestor

27

FINANCING CHAPTER 3

SLOVAK STARTUPS REPORT 2016

Plansforthefuturefollowasimilartrend.Themajorityofstartupswanttostayindependent.Sincetheinvestmentsinlaterstagesaremoresubstantial,startupsarelookingatsecuringdealswithVCfirmsabroadorsecuringastrate-gicbusinessinvestor.

How do you plan to f inance further growth in the fol lowing s ix months?

72%Owncapital

9%3F(fools,friends,family)

13%Bankloan

11%Localbusinessangel

9%Businessangelfromabroad

15%LocalVCfund

30%VCfundfromabroad

6%Crowdfunding

15%Publicsupport

2%Scientificgrant

19%Strategicbusinessinvestor

28

CHAPTER 3 FINANCING

SLOVAK STARTUPS REPORT 2016

Public Grants and Support

Startupsrealizethebenefitsofreceivingpublicgrantsorsupportthatmighthelpthemdeveloptheirbusiness.Themainreasonstoapplyforpublicsupportisfortheabilitytoacquirecus-tomersandtodoeffectivemarketingandenternewmarkets,theinabilitytoaccesscommercialbankingproductsandtohelpwithproductde-velopment,andtoinvestintoinnovativetech-nologies,andtousethefundstocreateanewserviceorproductwithhighcapitalintensity.

Itfurthercanbeusedtoemployprofessionalstodeploytheseproducts.Thesefundsarealsointerestingtosocialenterprisesthatareaimingatcreatingaviablebusinessmodel,buttheirprimarygoalistoservesociety.

44%ofstartupsdecidednottoapproachpublicinstitutionsforsupportduetothebureaucraticproceduresinvolvedwithapplyingforthissup-portorthattheyseenoneedforthesefunds.

Are you interested in receiving publ ic grant and support?

56% YES44% NO

29

FINANCING CHAPTER 3

SLOVAK STARTUPS REPORT 2016

56% YES

Generating revenues

MorethanhalfofSlovakstartupsarealreadygeneratingrevenues.Somecompanies(19%)startedgeneratingstable,expectedandsuffi-cientrevenueafteracoupleofmonthsinthefirstyearoftheiroperation.

After what t ime did your company start to bring in stable, expected and suff ic ient revenue?

19%inbetweenthefirstandsecondyearofexistenceand11%ofstartupsaftertwoyears,atthetimeofthesurvey.6%ofourrespond-entsstartedgeneratingrevenuesimmediate-ly.45%ofthecompaniesarenotgeneratingrevenuesyet.

6%Immediately

11%Aftertwoyears

19%Aftercoupleofmonths,inthefirstyear

19%Betweenthefirstandsecondyear

45%Wearenotgeneratingrevenuesyet

30

CHAPTER 4 EMPLOYMENT

SLOVAK STARTUPS REPORT 2016

Data about the labour market data is key for finding the right employees

In2016,Slovakiahasreachedthelowestunem-ploymentrateinsevenyearsandnowhasthehighestnumberofjoboffersavailable.

Thelabourmarkethaschangedinthepreviousmonthsanditshowssignsofoverheating.Ontheonehandtherearethehighestnumberofoffers,whileontheothertheunemploymentrateisfallingandthereareasmallernumberofavailablecandidates.The ratio between job offers and available candidates is leaning towards more offers and this will be worsening in the future.Thistrendisfavorabletocandi-dateslookingforanewposition,sincetheycanchoosefrommorepossibilitiesanditismucheasiertonegotiateanoffer.

Forcompanieslookingfornewemployeesthissituationgetsmorecomplicated.Sincetheunemploymentratehasdecreasedtherearefewercandidates.Theremeansmorecompeti-tionamongemployers,whichisthemostvisibleamonghighly-skilledprofessions.Newoppor-tunitiesariseforprofessionalswhoarealreadyemployed,butmightbelookingforabetterdeal.

In the high value-added fields there is fierce competition for the best talent.

InQ12016Profesiaregisteredayearlyincreaseinjoboffersof43%inservicesand30%inindustry.

Employment

InMarch2016wereached two magical milestones.ThenumberofoffersonProfesiareached20000andtheunemploymentratedroppedtounder10%.

Ivana Molnárová, Executive Director at Profesia.sk

31

EMPOLOYMENT CHAPTER 4

SLOVAK STARTUPS REPORT 2016

5 facts about the current labour market

1 There is more work and fewer people. Thereareveryfewavailablecandidatesandthosewhoareinterestedalreadyworkforsomeoneelse.Companiestodayneedtofindsuitablecandidateswithaninterestingandtailoredoffer.

2 Recruitment needs to happen where the crowd is. Tofindtherightcandidatecompaniesneedtobecreativeandtargetedonline.

3 Candidates know they have more options.Thebesttalentisreceivingoffersregularlysotheirselectioncriteriaaregettingmorecomplex.BasedonGraftonRecruitmentSlovenskoin2015,candidatesrefused23%ofjoboffer.

4 The best talent requires a work/life bal-ance.Thebestemployeesvaluetheirfreetime,health,andrelationships.

5 Create a HR strategyforrealpeople.

32

CHAPTER 4 EMPLOYMENT

SLOVAK STARTUPS REPORT 2016

Who works for Slovak startups?

LookingatSlovakstartupsthereisanincreas-ingmixofmaleandfemalefounderswiththenumberofwomenfoundersreaching30%.Thedatashowsthatstartupsusuallyhavemorethanonefounder.

Number of people in your company or project

Amongemployeesthegendersplitwas60to40formen,whichbuststhemythofthestartupandtechnologyworldbeingsolelyaman’sworld.

70% Male/Founders

30% Female/Founders

60% Male/

Employees

40%Female/Employees

56% Male/Unpaidworkforce(interns,advisors)

44% Female/Unpaidworkforce(interns,advisors)

CHAPTER4 EMPLOYMENT

32 SLOVAKSTARTUPSREPORT2016

33

EMPOLOYMENT CHAPTER 4

SLOVAK STARTUPS REPORT 2016

Reflectingtheneedtogrowandscaletheirbusiness,startupsarelookingathiringmoretal-entfortheiroperationsinthenextsixmonths.47%haveaconservativeestimateofhiring1–3newemployeesand17%arelookingat4–10newhires.Inthelastsixmonths,mostcompa-nieseitherdidn’tneedmorestafforhired1–3newpeople.

Startups are looking at hir ing more talent for their operations in the next s ix months

Increase in the last 6 months

48% 0 33% 1–3 12% 4–10 2% 11–20 5% 20andmore

Plan for the next six months

25% 0 47% 1–3 17% 4–10 6% 11–20 5% 20andmore

EMPOLOYMENT CHAPTER4

33SLOVAKSTARTUPSREPORT2016

34

CHAPTER 5 EXPORT

SLOVAK STARTUPS REPORT 2016

ExportYour primary market

79%Global

21%National

65%Europe

43%US

CHAPTER 5 EXPORT

TheUSandEUmarketsarelocationsofinterestformostofthestartups,theCzechRepublicbe-ingoneofthefirstdestinationsforexpansion.Almosteveryentityisoperatingorexportingtomorethanonelocation.SeveralstartupsarelookingatAsianandAfricanmarkets.

Intermsofexportourcompaniesaremostlyintheextremes.Theyareeitherhighlyexport-ori-entedoralmostnotexportingatall.Goingglob-alfromdayoneisastrategyfor79%ofstartups.

Just21%considerSlovakiaastheirprimarymarket.

IntheEU,companiesareexportingtothefollowingcountries:CzechRepublic,Austria,Hungary,Germany,France,Cyprus,Poland,Switzerland,Bulgaria,UnitedKingdom, andSweden.

34 SLOVAKSTARTUPSREPORT2016

35

EXPORT CHAPTER 5

SLOVAK STARTUPS REPORT 2016

What is the percentage of export in your sales?

40% 0–25% 3% 25–50% 11% 50–75% 46% 75–100%

Scale of operation: global vs. local markets

46%ofstartupsfullyrelyontheexportoftheirproductsorservices,another41%generatessalesonthedomesticmarket.

EXPORT CHAPTER 5

35SLOVAKSTARTUPSREPORT2016

36

CHAPTER 6 INNOVATION, CHALLENGES AND OPPORTUNITIES

SLOVAK STARTUPS REPORT 2016

Innovation, challenges

Cooperation with universities and research centres

BusinessanduniversitycooperationisstillinitsinfancyinSlovakia.Just3%ofcompanieswerecreatedasauniversityspin-off.Spin-offsdemonstratetheabilityofinnovativeideastobeturnedintoviablebusinesseswiththerealimpactofresearchonoursociety.

97% No 3% Yes

0% University(productdevelopmentcollaboration) 30% University(informalconsultations) 2% Commercialreserachcenter(collaboration) 11% Commercialreserachcenter(consultations)

Are you a research/university spin-off? Do you cooperate, a lso informal ly, with universit ies and/or research centres?

Startupspreferinformalconsultationswithuniversitiesandcommercialresearchcentersinsteadofnearlynon-existentcollaborationonproductdevelopment.ThesenumbersshowanopportunitytoimprovetheconnectionbetweenresearchinstitutionsandtofosterinnovationwithinSlovakia.

37

INNOVATION, CHALLENGES AND OPPORTUNITIES CHAPTER 6

SLOVAK STARTUPS REPORT 2016

How do you create your product?

Product development

Programmingismainlyperformedasanin-houseactivity.70%ofrespondentschosethisanswerandtherestoutsourcethedevelopmentoftheirproducteithernationally(17%ofthewholedataset),orabroad(6%ofthewholedataset).Asimilarsituationarisesinthemanu-facturingofaphysicalproduct,where30%ofrespondentstendtomanufacturetheirproductin-houseandanother30%outsourcethebe-fore-mentionedactivitiesnationallyandabroad.Materialsusedforthismanufacturingprocessareobtainedin-housein15%ofthecaseswhileothersoutsourceiteithernationally(17%)orfromabroad(17%).Nearly20%ofrespondentsdonotdevelopormanufacturetheirproducts.

In-house

70% Programming30% Manufacturing15% Materials9% Wedonotprogramandmanufacture

Outsourced nationally

17% Programming15% Manufacturing17% Materials4% Wedonotprogramandmanufacture

Outsourced abroad

6% Programming4% Manufacturing17% Materials4% Wedonotprogramandmanufacture

Legal protection

72%ofstartupsinthesurveydonothaveorneedanyformofintellectualpropertyprotec-tion,beitintheformoftrademarksorpatentregistrations.Theremaining23%haveregis-teredatrademarkorpatentvalideitherglobally(2%ofthosewhoansweredyes)intheEurope-anUnion(9%ofthosewhoansweredyes)orinSlovakia(27%ofthosewhoansweredyes).

Have you registered any trademarksor patents?

72% No 23% Yes

and opportunities

38

CHAPTER 6 INNOVATION, CHALLENGES AND OPPORTUNITIES

SLOVAK STARTUPS REPORT 2016

External – Finance, Marketing, Legal

Thelargestobstacleperceivedbystartupsistheabilitytoenteranewmarket.Theyhavereportedissuessuchaslackoffinancingtoenterthemarket,thedifficultiesofstartingmassproduction,andkeepingthepaceofinno-vationandcompetition.Culturalandlanguageappropriatebrandingandmarketingarecrucialareforcustomeracquisition,aswellasunder-standinglegalnuancesthatwilldecreasetheirlegaluncertainty;however,complexlegislativesystemsinotherEUmarketsaresometimestoobiganissueforasmallventure.Connectionstotherightbusinesspartners,suppliersanddis-tributorsbycreatinganetworkandreferencesfromcustomersareessentialtothesuccessfulproductionanddistributionoftheirproduct orservice.

What are your biggest chal lenges external ly? (mult iple answers)

Complexlegislationandtaxlicensingforstart-upsisreportedasthesecondbiggestobstacle.SomecompaniesareconsideringmovingtheiroperationstotheUS.ComplicatedlegislationsuchastheLabourCodecausesissueswhilehiringanewemployeeorprofessionalsfromthird-worldcountries.Dataprotectionandprotectingintellectualpropertyrightswerealsoreported.CompaniesstatedthatmissingeGovermentservicescostcompaniestimeandresourcesthatcouldbeallocatedtorunningtheirbusiness.Theyalsoperceivealackofsupportfromthegovernmentwhilestartingandrunningabusiness.Theenforceabilityoflegislationandofcontractualobligationswereamongthementionedchallenges.

32% Administrativeburden 47% Taxes

34% Complicatedlegislation 49% Export&entering

aforeignmarket

39

INNOVATION, CHALLENGES AND OPPORTUNITIES CHAPTER 6

SLOVAK STARTUPS REPORT 2016

Internal – Human Resources and Investment

Thebiggestinternalchallengesincludeinvest-ment,humanresourcesandnetworking.MostSlovakstartupsareusingtheirowncapitaltostarttheirbusiness.Astheygrowbiggertheyneedmoreresourcestooperate.Investmentisconsiderablewhenstartupsreachtheseedandscalingphases,andthesolutionmightbebetteraccesstoventurecapital.

Humanresourcesareoneofthehighestcostsforanewventure.TheirrecruitmentandretentioninhighlyskilledprofessionsseemstobemoreandmorechallengingbasedonthedataprovidedbythelargestjobportalProfesia.

What are your biggest chal lenges internal ly? (mult iple answers)

Startupscanusetheirbrandandmoderncompanyculturetoattractthebesttalentonthemarket.Connectionstotherightbusinesspartners,suppliersanddistributorsarecrucialtothesuccessfulproductionanddistributionofproductsorservices.

Amongotherinternalchallengesarethevalida-tionofthebusinessmodel,networkingthe righttiming.

51% HR 57% Investment 12% Skills

27% Network 12% Other

RECOMMENDATIONS

40 SLOVAK STARTUPS REPORT 2016

Recommendations

1 Flexible forms of incorporation. TheSlo-vakgovernmenthasintroducedanewformofjoint-stockcompanythatwillcomeintoeffecton1January2017.Thisnewformofjoint-stockcompanywillalloweasierinvestorrelationsandmodernmanagementofahighgrowthcompa-ny.Policymakersshouldalsoconsidersupport-ingsocialentrepreneurship,whichconnectssocialcauseswithviablebusinessmodelswithadefinitionandsuitablelegalform.

2 Nurture early stage startups.TheMinis-tryofEconomyanditsdedicatedagencieshaveplansandfundsallocatedtostartupsinthediscovery,pre-seedandseedstages.Theirgoalistocreatementoringprograms,internationalinternshipsandeventshelpingentrepreneurswithissuesregardingtheirbusinesses.Men-toringandlocaleventsaresuitableforunder-standinghowtobuildabusinessmodel,financeyourgrowth,acquirecustomersandmanagetalent.Forstartupswithabetaversionortestedprototype,internshipsinentrepreneurialhubsacrosstheworldarevaluable.Thereareotherformsofsupportthatareplannedfromthestructuralfunds.Publicauthoritiesshouldbeawarethatgovernmentsupportforstartupscanbeadouble-edgedsword.Ontheonehand,morefinancialresourcesintheecosystemcan

stimulatetheprivatesectortoinvestmorehu-manandfinancialresourcesinyounginnovativecompanies.Ontheotherhand,ifnotdesignedwell,tobetransparentandsimpleandincollab-orationwiththeprivatesector,thegovernmentsupportschemescaneasilydistorttheprivatemarketinitiatives,especiallysincetheSlovakecosystemisstillrelativelyfragile.

3 Create the Slovak 300. Usetheex-ampleofIrelandtocreateanetworkofIrishprofessionalsworkingandlivingabroadwhofeelaconnectiontotheirhomelandandwanttohelpfellowIrishmen.Thisnetworkhelpsindividualsorcompanieswithintroductionstopotentialbusinesspartnersintheirspecificfieldsandcitiestheyresidein.TheyalsowanttoattractinvestmentinIreland,whichinthecaseofasuccessfulrealization,bringsthemafindersfeefromtheIrishgovernment.Slova-kia,similarlytoIreland,hasalotofexpatriateslivingabroadwhoareverysuccessfulintheirfields.Awell-thoughtoutprogramwillcertainlyactivatethemandbringsimilareffectsastheIrishprogram.

RECOMMENDATIONS

41SLOVAK STARTUPS REPORT 2016

4 Scaleup. SupportthescalingofSlo-vakstartupsiswheretherealvalueiscreated.Thesecompaniescreatejobsforhighly-skilledprofessionals,generateturnovergrowthandexpandtonewmarkets.69%ofstartupsareinthepre-seedandseedstageandwillneedtools,supportandmechanismstoeffectivelyscaletheiroperations.Theirneedsaredifferentfromdiscoveryandpre-seedstagesandtheyneedtoberecognizedbypublicandprivateplayers.Amongthekeysupportmechanismsare:• Learningandmentoringprogramsfor

leadershipdevelopmentformanagersinscale-ups.

• Representationoninternationaltrademis-sionsandclosecooperationwiththeeco-nomicdepartmentsoftheSlovakembassiesabroad.

• Investmentininnovationshouldberead-ilyavailableandthegovernmentshouldconsidertaxbenefitstoencourageresearchandinnovation.

• Explorewayshowtoincreasetheinvolve-mentofscale-upsinpublicprocurementbymakingitmoretransparentandbydecreas-ingitsadministrativeburden.

• A‘startupandscale-upvisa’shouldbemadeavailabletoinnovativecompaniessotheycanrecruitstafffromthirdworldcountriesthatarenotavailableinthelocalmarket(professionalsinITorotherspecificfields)withintwoweeksofapplying.Theseforeignworkershelpexpandthedistributionoflocalscale-upcompanies’existingproductstoforeignmarketsandhelplocalscale-upsintroducenewproductsandservices.

5 Support diversity.Adiverseworkforcecreatesbenefitsforcompaniesaswellasthesociety.Employingtheyoungergenerationde-creasesyouthunemploymentandtapsintotheircreativepotential.Encouragingwomenaddsdifferentskillsandcreativepotential.Howevervariousgroupshavedifferentneedsthatneedtobecateredforthroughcompanycultureaswellaslegislativeflexibility–forexamplethelabourcode.

6 Transparent and simple use of public support for startups and scale-ups.Amongthekeybarriersofapplyingforpublicsupportistheamountofbureaucracyconnectedtothewholeprocess.Startupsalsoreportedthepotentialfearofcorruption.Atransparentandsimpleprocesswithcleargoalsandselectioncriteriawouldreducefearandallowtheinnovativesectortoflourish.

7 Deregulation and self regulation. Inthefieldofcustomeranddataprotectionallowcompaniesandthemarkettoregulatethemselvesandsupporttheinitiativestocreatecodesofconductsuchastheonefordataprivacy.

RECOMMENDATIONS

42 SLOVAK STARTUPS REPORT 2016

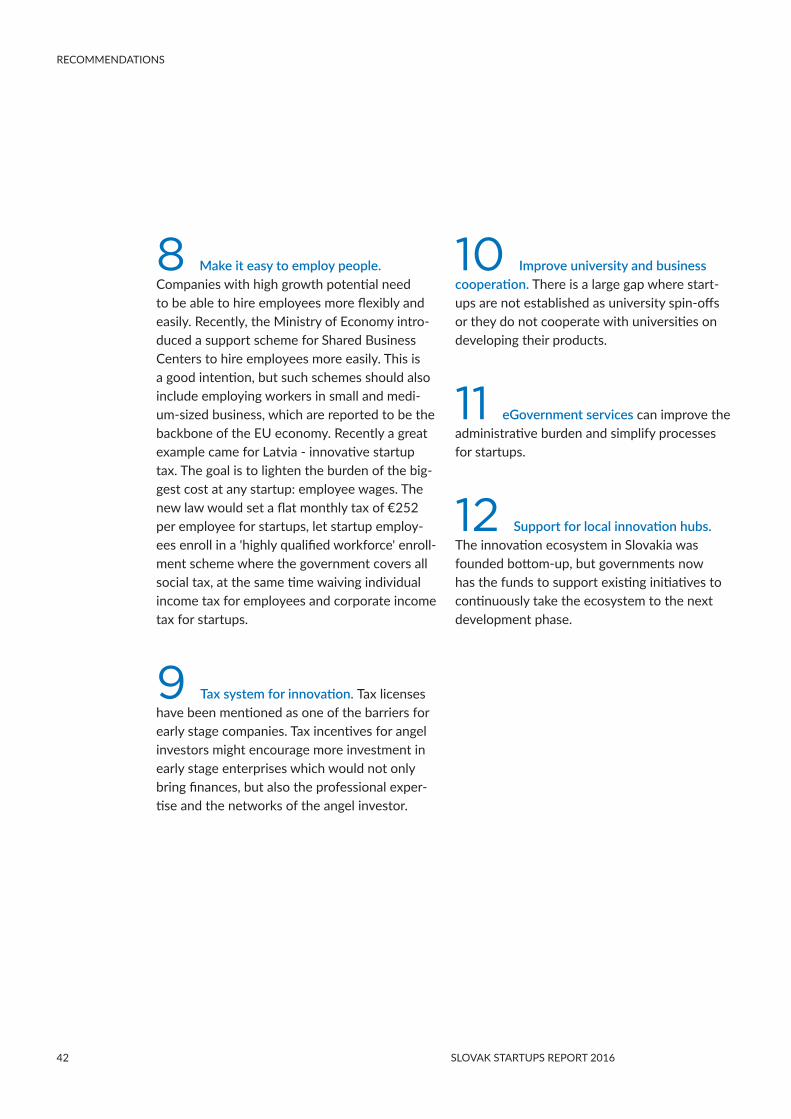

8 Make it easy to employ people. Companieswithhighgrowthpotentialneedtobeabletohireemployeesmoreflexiblyandeasily.Recently,theMinistryofEconomyintro-ducedasupportschemeforSharedBusinessCenterstohireemployeesmoreeasily.Thisisagoodintention,butsuchschemesshouldalsoincludeemployingworkersinsmallandmedi-um-sizedbusiness,whicharereportedtobethebackboneoftheEUeconomy.RecentlyagreatexamplecameforLatvia-innovativestartuptax.Thegoalistolightentheburdenofthebig-gestcostatanystartup:employeewages.Thenewlawwouldsetaflatmonthlytaxof€252peremployeeforstartups,letstartupemploy-eesenrollina'highlyqualifiedworkforce'enroll-mentschemewherethegovernmentcoversallsocialtax,atthesametimewaivingindividualincometaxforemployeesandcorporateincometaxforstartups.

9 Tax system for innovation. Taxlicenseshavebeenmentionedasoneofthebarriersforearlystagecompanies.Taxincentivesforangelinvestorsmightencouragemoreinvestmentinearlystageenterpriseswhichwouldnotonlybringfinances,butalsotheprofessionalexper-tiseandthenetworksoftheangelinvestor.

10 Improve university and business cooperation.Thereisalargegapwherestart-upsarenotestablishedasuniversityspin-offsortheydonotcooperatewithuniversitiesondevelopingtheirproducts.

11 eGovernment servicescanimprovetheadministrativeburdenandsimplifyprocessesforstartups.

12 Support for local innovation hubs. TheinnovationecosysteminSlovakiawasfoundedbottom-up,butgovernmentsnowhasthefundstosupportexistinginitiativestocontinuouslytaketheecosystemtothenextdevelopmentphase.

METHODOLOGY

43SLOVAK STARTUPS REPORT 2016

Methodology

TheSlovak Alliance for the Innovative Economy (SAPIE)partneredwithsimilarorganisationsintheVisegrad Grouptoconductasurveyofinnovativecompanies,startups,inallfourcountries(Poland,CzechrepublicandHungary).Throughourpartnersandmemberswehavedistributedthesurveyoverthetwomonthperiod.Ourgoalwastocollectresponsesfrominnovativetechnologycompaniesregis-teredinSlovakia.

Thesurveyquestionsweredevelopedincollaborationwithourpartners,closelycorrelatingwiththeCzechversionofthesurveyduetoadministrative,legisla-tiveandculturalsimilarities.Mostofthequestionsinthesurveywerevoluntarytoanswer.Survey was completed by 47 startup companies based in Slovakia. Toevaluatetheanswerswehaveusedknowstatisticalmethodswithmodernanalyticaltools.Inthereportwehavestatedwheretherewasapossibilitytousemultipleanswers.WithourexperienceandknowledgeoftheSlovakstartupscenewecanextrapolatetheresultstoreflectthecurrentstateoftheinnovationeco-systeminSlovakia.

ABOUT THE AUTHOR

44 SLOVAK STARTUPS REPORT 2016

About the Author

Petra DzurovčinováistheExecutiveManagerofSAPIEsinceitsinceptionin2014.TheorganizationwassetuptorepresenttheneedsofglobalandSlovakinnova-tivecompanies,improvethestateofITeducation,boostthestartupecosystemandhelpcompaniesscaleglobally.AmongourmembersaretechgiantsaswellasgloballysuccessfulSlovakcompaniesandrisingstars.SAPIEactsasanindustrybodyforover40companies,representingthembeforepolicymakers,andcreatesnationalandregionalpartnershipsandadvocatesforinnovation.InthepastPetraworkedasDigitalCommunicationsManageratTheRoyalInstitutionofAustralia,anorganizationpromotingscienceandtechnicaleducation.ShestudiedInterna-tionalBusinessinBratislavaandÉcoleSupérieuredeCommerceBretagneBrestandFuturestudiesatSKKUinSeoul,Korea.

CONTRIBUTION

45SLOVAK STARTUPS REPORT 2016

Contribution

Matej Greš

Matej'sareasofexpertisearegraphicdesignandstatisticalanaly-sis.InrecentyearshewashelpinginthisareaswithpreparationandrealisationofpoliticalcampaingsandBlack-boxtestinginfinancialsector.InSAPIE,Matejisinvolvedinpreparationofsur-veys,eventsorganizationandinnovationeconomyanalysis.

Branislav Dudáš

BranislavDudášstudiedinternationaltradeattheUniversityofEconomicsinBratislavaaswellaslawattheDanubiusUniversity.Hehasheldvariousadministrativeandexecutivepositionsinbusinessandnon-profitsector.ForfouryearshehasbeenanadvisortothesecretaryofstateattheMinistryoftransport,con-struction,andregionaldevelopmentofSlovakRepublic.Hecaresdeeplyaboutwords,language,andlearning.

ABOUT ORGANIZATION AND PARTNERS

46 SLOVAK STARTUPS REPORT 2016

TheSlovakAlliancefortheInnovativeEconomy(SAPIE)wassetuptorepresenttheneedsofglobalandlocalInternetandinnovativecompanies,improvethestateofITeducation,boostthestartupecosystemandhelpcompaniesscaletothegloballevel.Amongourmembersaretechgiantsaswellasgloballysuccess-fulSlovakcompaniesandrisingstars.SAPIEactsasanindustrybodyforover40companies,representingthembeforepolicymakers,createsnationalandregionalpartnershipsandadvocatesforinnovation.ThisprojectwassupportedbyStartupAwards.SK,Martinus.skandESET.

About the organization and partners

sapieSLOVENSKÁ ALIANCIA PRE INTERNETOVÚ EKONOMIKU

sapie