senegal stabilization, partial adjustment and stagnation...senegal stabilization, partial adjustment...

TRANSCRIPT

-7~ ~ ~ ~ ~ E-

Report No. 11506-SE

SenegalStabilization, Partial Adjustmentand StagnationSeptember 24, 1993

Office of the Chief EconomistAfrica Region

FOR OFFICIAL USE ONLY

M4ICROGRAPHICS

Reprt o:11506 SEType: ECO

Docunmet of hWoi'Bk

* y- * ' *-> q .A ' ' ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~I, a

Thsdomerimthas a restrcted ditribution and miay b used by irecipiensnyArt thep' nanco- f 'beiro ofc'aa°dutiesv '-C-, Itscotr "bwis ,$jsctos~d w'i bou '' ftnt Way Bn irttv w ,o

I,a~ aoth.'. . .a .f,''' . '''t ' '. ''

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

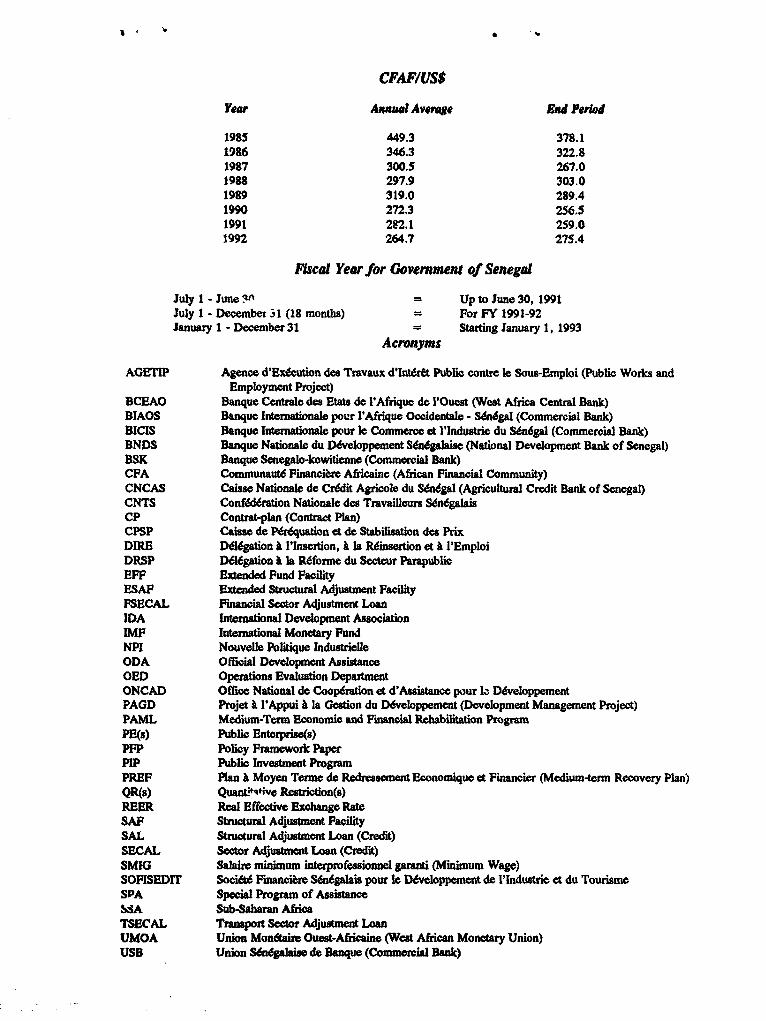

CFAF/US$

Year AW Averge Had Period

1985 449.3 378.11986 346.3 322.81987 300.5 267.01988 297.9 303.01989 319.0 289.41990 272.3 256.51991 282.1 259.01992 264.7 275.4

FYscal Year for Government of Senegal

July 1 - June 3n = Up to June 30, 1991July 1 - December 31 (18 months) = For FY 1991-92lanuay 1 - December31 = Statting January 1, 1993

Acronyms

AGETlP Agence d'Bxdcution des Travaux d'Inte Public contre to Sous-Emploi (Public Works andEmployment Project)

BCEAO Banque Centre des Etats de l'Afriquc de l'Ouest (West Africa Central Bank)BIAOS Banque Intenationale pour l'Afiique Occidentale - Senegal (Commercial Bank)BICIS Banque Internationale pour le Commerce et l'lndustrie du S6negal (Commercial Bank)BNDS Banque Nationale du Ddvelppenent Sdndgalaise (National Development Bank of Senegal)BSK Banque Senogalo-kowitienne (Commercial Bank)CPA Communaut6 Fmnanciere Africaine (African Financial Community)CNCAS Caiss Nationale de Credit Agricole du Senegal (Agricultural Credit Bank of Senegal)CNTS Confederation Nationale des Travailleurs SdndgalaisCP Contrat-plan (Contrc Plan)CPSP Caise de P uation et de Stabilisation des PrixDIRE DEgation I l'Insertion, a la Rdinsertion et I l'EmploiDRSP DElegation I la R6forme du Secteur ParapublicEFF Extended Fund FacilityESAP Exended Stucurl Adjustment FacilityPSECAL Financial Sector Adjustment LoanIDA Inernational Development AssociationIMF Itmenational Monetary FundNPW Nouvelle Politque IndustrielleODA Official Development AssistanceOED Operations Evaluation DepartmentONCAD Office National de Coopradon et d'Asistance pour Lb DeveloppementPAGD Projet I l'Appui I la Gestion du Ddveloppement (Development Management Project)PAML Medium-Term Econonic and Financial Rehabiliation ProgrmPE(s) Public Enterprisc(s)PPP Policy Fmework PaperPIP Public Investment ProgamPREP Plan Moyen Terme de Redrasemnent Economique et Financier (Medium-tenrm Recovery Plan)QR(s) Quant:tqtive Restriction(s)REER Real Effective Exchange RateSAP Structural Adjustment FacilitySAL Structural Adjustment Loan (Credit)SECAL Sector Adjustent Loan (Credit)SMIG Salaire minimum inatprofessionel gsaanti (Minimum Wage)SOFISEDIT Soci&6 Fmanciere Sdn6galais pour Ic D&vcoppement de lIndustri et du TourismeSPA Special Prgram of AssistanceSSA Sub-Sahan AfricaTSECAL Transport Sector Adjustment LoanUMOA Union Mondtaire Ouest-Africaine (West African Monetary Union)USB Union Sndgalaise de Banque (Commercial Bank)

FOR OMCIAL UE ONLY

kThia ro,iozt ka prpmd bY. MusOpha'Rouls (APRCE, wAih e

Thisreport revie wus eegl' atustet unot psna4r0UoDasc sinc 1980 fua, thifonis fear Sene

dOaUlt*htO4its irst adse progIram. The report da&ahaiyon sevea on the vnous st*Jep8 of h

adj uusoimats. 4.vdo~ents Senegal's paziulryrelatcingt implement.ingm poucyaein,m haszbeens m hised Seneg, alid oes,m wiell Iind moetryandosan irTe Mde, pricing and Aetrade,anfinanci5a 5b setrplces, bteln poody in driprov ted cutry's copetiiveness. Thedeltisrvesw1policy pursued by Senega ha wnot poduced Seve the moes results tageted in

sthe 4yenme' mediumterm s flnanch progsramadPliy Fh ~~ramhewo ~rk Papers Ihed aetlay policyha le~d to severe fsc.ab Pl compression epandcts in pbipnigi

hsreporit areview Snaequaegadm'nstradutiven cpreforhanc sinerl 1980te the yearectSenegalolaunchdits fstradjustmicesant program.ible re portifcuseas oen thrsed varoussteps ofthteiienladjusmet process harodsig tot iplemuen theepceercation adomcrenmicnd setoerea

bez men rixeld. asenearslt,eprshv o performed well oeayadcei, poesicin andux trade, andcomancie agector plcieapiprs, but porlyat inmrvingmethes coutry'st competitienesshe fThedefbliationar plcyhpursed by fasenegagle handos not provdceden the modsts resu lts tageed_

defdlationary policy has led toseverefiscalmpression and cutse i cs ingw

~~, ':.:,, Y

Theintdcuernaadutmnprcs has no produced thsrbto n a e expcte depreci ations ony n the pofregal

of their offcial duties. Its contents may not otherwise be disclosed without World Bank authorization.

Table of Contents

Executive Summary

I Background and Overview 1

U Dedgn and Impetaon of the Adjustnent Progam 7

A. Macoeconomic Policy and Management 7B. Pricing and Trade Policies 16C. Institutional and Other Policies 25D. Summary 41

m Macroeconomic Outcomes of the Adjustment Program 47

A. Macroeconomic Stabilizaon 48B. The Compedtiveness of te Economy 53C. The Supply Response 56D. Summary S8

IV Seetoral Outcomes of the Adjustment Program 59

A. Agricultura Sector 59B. Industra Sector 62C. Public Enterprises Sector 67D. Social Sectors and Income Distribution 68E. Summary 71

V LAmons Learned and Reo dations 73

BIbliographIy 81

Boxes

1 Lessons Leaned and Recommendations Xl2.1 Framework for MoUtay Policy in UMOA Countaies 122.2 Government Ownersip: Two Differt Approches

to the Revision of the Labor Code 242.3 Senegal vil Sevie Volutary Dqep Program:

A Policy Failure After A Good Start 40

.* 54

-* ~ ~ ~ ', I^ .. i. -. * i

-. -||f vi...i *1 .- 9-. ;s,f ,7

t44ff ~ ~ ~ -4 * f4-. Ilk~~~~~' v

.

46k _ ,, t 49

14

.~ .-. ..- *s- 35

h. s; . .,& .+ .Q. : w. / ~~~~~~~~~~~1 .9:>.~~~~~k'

23

es. ~ . -.. -. ;- .1..9

* . . )-.s 27

...' ....-. ,...,37

48- . . i . . .j . . ; -s i , . ws 61

6465

'4" , *~44; 4; 6*. , As. J

87

.5, . ~ . s . 8889

90

91-. 5, 5-, .5 ~~~~~94.5 .' ,X,, tr . 4.<t 2 , So 9s

~ 4 4 445 45.'A *j~' 4 r fb\f1

f5 - '-' .> .'. .4.. 9

Executive Summay

Introdudon

1. This study evaluates Senegal's adjustment performance since 1980, theyear Sene_ launched its first adjustment program. In the early years of the decade(1982-85) little structurl adjustment took place and this is referred to as the stabilizationor pre-adjustment period. The second half of the decade witnessed some structuralchanges in the economy, and is refaered to as the period of partal adjustment. Theevz!uation covers the government's reorm program in its entrety, and is not limited toBank-supported lending operations. The report focuses on the variou steps of theadjustment pkocess- from deign to implementation-and on macoeconomic and sectoradjustment impacts. The methodology used to evaluate the impact of adjustment oneconomic performance is the "before and af" approach.

The Financia Crisis and Govermm's Response

2. Senegal is a small, semi-arid Sahelian nation with a population of 7.6milion. It is predominan aly ral with limited naual resource endowments. At thecurrent exchange rate, the 1991 income per capita of US$720 places Senegal at thebottom of the lower-middle-income economies. At independence in 1960, Senegalinheited a relatively well-developed physical and socal infrastructure due to theprominent role Dalar played in the large French West Afrcan colony as a whole.Senegal has enjoyed a high profile in Afican affairs because of its lively democraticsystem and its highly vocal press. This has helped Senegal mobilize substantial exralresources over the years. Seneal has had a long traditon of African socialismnresultg in widespread govenment participation in the real economy and regulatorycontrols of the private sector.

3. In the first two decdes following indepedence (1960-80), Senegal'seconomic perform0c was poor, even by Sub-Saharan Afrca standards. Senegaleerienced the lowest GDP growth rate of any African state not affected by war or civilstrife. GDP grew on average by 2.1% in real tem per anum, compared to apopulation growth rate of 2.8%. In 1981, all key economic indicators reflected seriousfinancal and strucr imbalances: the fiscal deficit stood at 12.5% of GDP (or around10% if interet payments were excluded), the curent account deficit reached 25.7% ofGDP (or about 22%, if interest payments due were excluded), the inflaion Ste soaredto 12%, the tem of trade index dropped by 12% from its 1975 level, savings werenegative, and total consmption exceeded GDP. Te total stock of debt represented overtwo-thirds of GDP and the debt service represented nearly one-fifth of total eWorts.

ii

4. The need for structul economic changes in Senegal can be traced to theearly years of independence when Senegal lost its lae Fnch West Afrcan makeLKey economic indicators pointed to macrenomic imbalances in as early as 1966, whengroundnut exports suddenly lost their preferential French market and had to compete inthe world market. The ovesized public sector was also characterstic of the Seneeseeconomy at that time. Government was slow to mcognize the need for strucural changes.During the short-lived commodity boom in tfie second half of the 1970s, the governmentresponded by borrowing heavily on commercial terms, extpecing a return to morefavorable terms of trade.

5. In the late 1970s, the government began to recognize the shortcomings ofits ambitious public sector development plans and nationaliaton policies, and inDecember 1979 it announced its medium-tenn recovery plan for 198084. This programsought to staibilize the internal and etal financial situation, raise public savings,increse investment in dte productive sctors, libealize trade, and reduce the state rlein the economy. This first attempt at stabilizing the financial sitation and creating thebasis for growth did not, however, yield atisfcory results because the reforms wereonly partally carried out. Renewed efforts were launched in 1984 with the onizationof the first Consultative Group (CG) meeting for Senegal, and with the financial supportof the donors of the second phase of the adjustment program for 1985-92. Thegovernment's reform effort has been supported since 1980 by six Bank adjustment andsector operations, and by a seies of IB arrangements, including a three-year ExtendedStructural Adjustment Facility (ESAF). A total of five Policy Framework Papers (PFPs)were approved by the Bank and the IMF Boards between 1986 and 1991.

6. Senegal has been a recipint country of the Specal Program of Assistance(SPA) since its establishment in 1988. The adjustnt program in Senegal has beengenerously supported by the donor community, either directly or as co-finciers ofBakMP opeaons. In 1991, Senegal per capita ODA reached US$84 (or 12% ofGDP per capita), over twice the average for SSA. Between 1981 and 1991, budgetarysupo to Senegal accounted for nearly two-thirds of tetal net disbursement of officialdevelopment asitn (ODA) which, in turn, accounted for 4.3% of the total amountreceived by Sub-Sabaran Africa.

Design and equendng of the Rfonm Program

7. The intenal adjusment strategy that Senegal adopted relied on policiesot tan devaluation to restore growth, and internal and external lance. Thesepolicies conisted of deflary monetary and fiscal policies (demand managementpolicies), second-best trade policies (high tariffs and export subsdies), and s lreforms. The laUtter reforms are deigned to lbealize market and prices, reduce the sizeof the public sector and rationaize its activities, and encourage private sector investmentand development. Reospectively, the internal adjustment policy proved to be more andmore difficult and complicated to imp t. This shows clearly the importance of theexchange rate as one of the major adjustment tools. It is not certain that the Senegaleseeconomy could get out of its long recession without a more flexible exchange rate policy.

iii

Und the internladjutme strategy, if competiivenesst i achieved, it will be &chievedin the fina phe of the adjustment process rater than at the beginning when adepreiation of the red exchange ate is part of the adjustment progrm.

8. Chronologically, the reform pwgam focussed on economic stabiliaton(I.e. reducing the Intnal and extal imbalances and lowering the inflaon rate);agricultul marketng l n; inprovement of public sector management,incuding pubic enterprise and civil service; wage and labor market deegulation;popultion growth, bang ctor uc g; and tasport sector alion. Thesequencing and coheence between these varous components of the reform program havebeen closely montored through the PFP process. Apart from the exchange rate issue,the adjustment program desg would have been comprehensive had the human resourcessector, particduy edu , been fuly addrssed.

9. Notwittanding that the design of the adjustment program componentshas improvd over time as Senegal gined more experience in adjustment, the sequencingOf the rerms has had some setious flaws. The decision to liberae extenal tradebefore esabishing an efective t administratin, eliminatig labor rigidities, andreducing the cost of production, refiects insufEfcient cn given to the sequencingof rforms. Similarly, the decision to proceed with the civil servce departr programbefore establishig a robust datase on wages and civil sermats, and a monitoringsstem, also refects a defciency the sewquencing of reforms. Banking sector reform,although well implemented, should have been carried out earlier had the seventy of thecris been kom. Finally, the pv on of public enterprises ought to have beeninitiated once a good regulatory and incentives framework was in place to encourageprvate so develt.

Gvowwtn Cbmmlte

10. Govenment's comitent to the reform program seems to depend ondtee lky elemets: the degree to which a conseu exist among the various interstgroups, the stength of instion in charge of formlatig and coordating the reformproam, and the nate of the refms thmselves-the more poically and sociallydifficut, the more reluctant government is to fully implementing them. Over timre, thegovernment has teded to more widely consult interest pardes on policy measures andto debate tese mea publicly. A case in point is the revision of the labor codewhi involved exnsive discusons between the government, labor unions andemployer ion, and, more recently, the discussion of the higher education sector.Nowithnding this efot, the involvement of the private sectuor in the design of thereform proam has been far from satsactoy.

11. Th momentum of the goverment's c to the refbrm programseems to have been lost folowing the 1988 elecdon when the technocrats' influence waswealkned as a resut of poliical pressre. During 1986-88, a com team of technocrtswere instumental in the implment of refom. Senegal was leas successful in its

iv

refrm implementain where vested interest was strong and leaderip was weak Thiswas the case in the agicultual pricing reform program, in the libealization of tie labormarket, and in refomaing higher education. The lack of Weement between thegovernment and the key donors, including the Bank, on the agricultural SECAL, whichhas been under prepaation for over three year., is a good example relectig the pointdiscussed above. To deal with the govemment's weak commitment to the adjustmentpirt-nften, government implemented the reforms in form rather an in

substance-recent adjustment opertions supported by the Bank put heavy e.. phasis onup-front conditionality.

Implementaton of the Rform Program

12. Overall, Senegal's performare in implementing its adjustment programhas been mixed. This evaluation is carrico out by major policy categories and by majorseucors of the economy. Senegal performed well in monetay and credit policy, pricingand trade policy, and financial sectr policy-the latter being an area where Senegal wasone of the first countries in the CFA zone to undertake such a far reaching reform. Twocaveats are in order here. First, the government began in recent years reversing itsimport potecdon policy, and second, govemment was not aggresve in recovring thebking sector bad debts owig to its hesitancy to pursue t arge debtors. Theunfinished financial reform agenda is mainly in monetary policy where there is a needto shift to a market-based system of money and credit management.

13. Senegal's performance has been exceptionally poor in improving thecountry's competitiveness in the world market. The real exchange rate has appreciatedby at least 20% in foreign currency terms during the partal adjustment period, i.e. since1985. The labor market has been only marginally lelized libealization of hiringpraces, and part relauation of the constraints on the use of temporary employmentcontracts). A new draft labor code, which diminates the rigidities in the labor market,has been prepared by government in close consultation with labor unions and theemployers' association but has yet to be enacted into law. As a result of the peristenceof the rigidities in the labor market, labor costs remain a serious impediment toinvestment, growth and competitiveness.

14. On the fiscal front, the government achieved its main objective ofdiminating the budget deficit by 1990, but the situaon reversed soon thereafter. During1986-90, the government imlemented a wide range of tax reforms designed to simplifythe tax struc (namely by introducing a global personal income tax and a single taxon corpoate income), modenized the tax astation system, and mobiLized resourcesby widening the scope of the value-added tax. The government also introducedxeniture control measures, pardcularly in the area of public investment. Govemment

tended, however, to focus on short-term financial considerations, such as reliance onwindfall revenue from petroleum and nce imports and the intoducton of numerous, ad-hoc tax measures ather than on structural issues. Revenue mobiization and resourcealocation were done at the expense of ompetitives and long-term growth, a reflectionof the aeceive preoccupation with the short-term. In expendires, government reduced

v

investment (below appropriate levels for replacement) and asocatins to O&M, butproted wages and salaries, thus jeopadizing future growth and employment. In sum,the required fundamental restucturing has not been achieved. The key fiscal reformsleft to be implemented are ngening the t administration, particulaly customs,reducing dependence on rvenues from petoleum, redg the wage bill, controllingtansfe to PEs, and raising investment and O&M.

15. A review of the implementation of the sector reforns also reveals a mixedperformance. The implemenion of the agricture reform program has bees limiitedto the liberalizadon of domestic tade, price decontrols on most comma :s, andelimination of input subsidies. On the other hand, rice import controls remain a majorissue and producer prices for cash crops, namely groundnuts and cotton, continue to haveno direct relation to world prices. Liberaization of the domestic market for mostcommodities has been a necessary, although insufficient conditions to turn agriculturaproduction around. The appreiation of the ral exchange rate and the unfavorable termsof trade for groundut oil and cotton, remain major obstacles to agriculturaldevelomet. A comprehensive reform program addressing the competitiveness of thegrundnuts, cotton, and rice sectors is urgently needed.

16. The implemention of the industrial reform program has been verylimted. What was supposed tohave been a comprehensive and well-sequenced programtuned out to be only y implemented. The policies effectively implemented werethe liblizaion of domestic and international tade, and the decontrol oA most domesticpices. In recent yes, however, government started reversing its trade policy primarilyfor fiscal reasons, but also to protect industry and to compensate for the appreciation ofthe real exchange rate. Crocial reforms such as labor deregulation, improvement in thelegal and dmive environment, reduction in the cost of energy, and export subsidyschemes were not only partly implemeted, but were implemented late in theadjusment process. Among the measures implemented to improve the regulatoryenvironment were the revision of the investment code and the smplification ofinvestmn procedures. The industri program, conceived as a comprehensive reformprogrm, was finally reduced to price and trade liberaliztion.

17. The implemenion of the PE sector reforms has been uneven.Goverment lqidated 21 PEs and privafized, totaly or parily, 26 others, togetherrepreenting 42% of the total number of PBs. These PEs represet only 19% and 11%,repectively in tems of assets and gov ent equity. Divestiture, which is nearlycomplete in the financial sector, is far from being so in the non-financial PEs. Theprogress made in the divestitre program is very recent-th-uart of the PEsprivatized and liquidated, which ransled into about 80% of their assets and govemmentequity have been achieved sice 1989. A total of ten PEs (out of 27 planned) have beenrestructured. And, a total of 24 (out of 44 planned) contact plans and letters ofmission' have been signed between government and selected PEs. The use of contractplas bas imprved transparency and accoulit of the two contracting parties-nota small achievement-but has encountered major problem in its financial implications.On the financial front, the government implemented the refoms in "lette but not in

vi

spirit.* Te govement rduced direct subsdes to PEs but the benefit of this reformwas deftd when the PBs crtousy sought financing through commercial overdraftsand gSermment guantees This loophole was corectd in 1990 by prohibiting tis typeof fLa_ing; this in tutn was defeatod by te PEs through the accumuladon of arear.Ihe settement of these arre between government and PEs has ben carried out twicein a comprehsive manner and the problem seeu to be slightly less acute now becauseof the introducdon of concurret preventive measures.

18. In the human resources sector (education and health), only a limitednumber of reforms have been implemented. The unfinished reform agenda includes artwu',tion in the imbalances between primary education and higher education, andbetween basic health care and a curtve hedth system. Reforn programs for highereducation and health are currently under active considration by the government.

19. Figure 1 presents the major reforms undertaken during the period 1980-91and those not yet undertaken. Pending reforns needed to inprove the competitivenessand allocation of resources include the depreciation of the nrd exchange rate, theadoptton of indiect instruments of monetary control, the eliminaton of rigidities in thelabor market, the impwvement in the legd and adminive fiamework, and the controlof the wage bill. A com ve reorm program addressing the groundnuts, cotton,and rice subsectors is urgendy needed. Finally, major reforms are also needed todevelop the human capital in Senegal.

Mocroeconomlc Oucms f the A4jw men

20. At best, Sened has acheved mixed macoeconomic results during theadjustment period. It esentiaUy achieved financil stabiization with stagnation of theeconomy-per capita income has registered only a slight increase. Furhermore, evenwhere positive results were achieved, they do not compare favorably with the expecedmodest results of adjustment, as envaged in five consecutive PFPs. Ihe key factorsexpaining this mixed pefmance are the poor refor mplementaion, real exchangerate appreyation, and external shocks (weather conditions and terms of trade).Nonethles, Snegal is now better off than it was in 1981, but it is still faced witipoliy disttons which seriously undemine the country's longer term prospects.

21. By 1990, Senegal eliminated its fiscad deficit (the primay deficit hasalready been eliminated as early as 1980, and cut its exten imbalance by two-tirds

vii

Flue Is Jliaam.tiMoa Satus ofMor PeRy Rfodbnmsfa Se&pi, 1960.9

80 62 84 *6 8 90 91 1

Fiscal PolicyRationalize tax system XXXXXXXX XXX XXXX Iloprove tax administration XXXx 2Introduce cost recovery 3Control wage bill xIxOXXoXooXX I///I 2loprove pubtic investment programing XX XxI:1x::2111XXui[ 4Reduce PE subsidy 2lmprove debt nanagement XX I 1

Monetary and Financial PoliciesAdopt flexible int. rate & credit policy XXXX IEstablish bank supervison body XXXX 1Restructure the banking sector XX XXI7x JXXXXXXX 1Develop capital market 3Shift to indirect instru. of monetary control 3

Reat Exchange Rate PolicyAdopt deflationary policy 3

Domestic Prices and Trade LiberalizationDecontrol prices XX XXXX XX XlajLiberalize input & cereals output marketing XX XXXXXXXXXXX ib1Reduce fnput subsidy XX XIIIIIIIIXX 1 IEliminate monopolies (special aoreeents) 3Reduce cost of production XXXX 2

Labor Market LiberalizationDeregulate aog setting system 3Deregulate labor market XX XX 2

External Trade LfberalifationEliminate non-tariff restrictions XXXXXXXX /1/U//Il IC/Reduc tariff categories and levels XXXXXXXX I/I/lW 1c/loprove export incentives xx XXXX XXXXI//I 2

PEs Reform ProgramRestructure key enterprises --------- Ilarplement divestiture program XX XX XXXXXXXX 4Rationalize supervision system XXXX XXXX 1Use performance contracts 2

Enablfng Environment ReformSimplify legal & adcin. procedures 3Improve investment incentives XXXX XXXX 1iReform civil service XXXXXX 2

Other reformPopuattfon control XX 2Reform education sector 3Reform health sector 3Reform rice, cotton, & groundnut sectors 3Adopt social safety net measures XXXX xxXX 2

XXC Policy UVISUMaNIGOs. n MIUA261 III Pocy R . I _ .

2 Not oflSc"ny bnplnsttd.Pdos on 14 how eman coonolled. 3- NGt bmpinted.

bl.ice muts mannar oonulebd. 4- Coadnum.Kof Giadual policy revmnld

Souxc: SA Ta S.

yin

(current account deficit dropped to nearly 8% of GDP). This was achieved throughdemand conmprsson in private consumption,o investmetl, and expenditure on priorityarea. The, intuation rat dropped to leas than 3%, onec-fourth of what it was during thecrisis period. This stabifliztion, particularly in the fiscal area, renains fiagile, andunless additiona strucutua reforms in civil service and tax collections are introduced, itwill not be Nsusaned and may lead to a deterioration in long-team growth of the economyand in the competitveness of Senega. As a result of the lack of significant stucuralreform on the fiscal side, Senegl continues to rely on large petroleum revenues (to thetune of 22% of tax revenue) and large external resources to finace its budgetary deficit.Improemenat in the current accunt was largely due to a sharp decline in prices since1986 for the country's m4jor import items-petroleum products and rice-and to importcompression associated with low investment (at around 13% of GDP) and growth.Export performance has been. erratic with an overal downward trend.

22. Competitiveness of the Senegalese economy has not improved during thepartia adjustment period. The real exchange rate has significantly appreciated and thecost of production has remained high. Furthermore, the frequent changes in tarff andtaxaton policies and the distortions entailed, together with the poor implementation ofexport subsidies, have smnt the wrong signals to an already weakeed and uncompetitiveindustria sector. The Gambias rapid trade liberaliztion, combined with its uniquegeographic location vis-k-vis Senegal, has further exposed the Senegalese mranufacturingseCtor to stiff competition.

23. The averap annual economic growth rate was 3.2 % during the period ofparia stuctural adjustmet (1986-91) compared to 2. 1% in the first half of the decadein relation to population growth rat of 2.9% to 3.2%. This stagntion in per capitaincome shoud be cautiously interpreted given the poor data qualit of national accounts,particularly for the period under paria adjousmet. In spite of its relatively small shaeof GDP?, agricltur, whose promnewas largely determined by weather conditions,continued to have a major impact on overall growth thrugh the multiplier effect on therest of the economy. While there has been some improvement in public investment

progammng,there has been litte diversification in the structure of the economy.Furdthemor, the level of investmnent has dropped to below the minimum level forpreserving existigifratutt assets in Senegal let alone for accelerating growth.

Sectr Outcwome f the Adjusvnent

24. During the partial adjustment period 1986-91, agiutrlproduction(including forestry, livestock and fishery) registered a modest inraeof 2.9% perannum. The increase in production was largely due to favorable weathe conditions inspite of a drop in cultivated land. While there is indication that interna terms of trademay have shifted slightly in favor of agriculture and away from industry, this shift shouldbe interpreted with caution as it is not statstically robust. Production of food cropsincreased faster than cash crops, lagely as a result of an expanson of subsistance

agriultre,interal tradelbrliain and producer price differentials in favor of foodcrops. Because of both good harvests and favorable domestic cereal prices, cereal

ix

imports (rice and wheat) drop dgnificantly during the partal adjustment period. Ona per capita basis, cerel consumption declined by 1.7% annually durin the partialadjustment period. This decline does not however imply a drop in food consumption asSenegal has likely incased fish and vegetable consumption. Indicators of productionincentives and efficiency show st among the ceals, diough millet and maize have aconsideably higher comparative advantage than rice, they have barely adequateprotection to sustain production for local consumption because of RER overvaluation.Far too many resources have been devoted to irrigated rice production, a sector whichhas yet to be sigmficantly reformed. Of the cash crops, cotton had a higher comprativeadvantage than groundnuts but received barely enough protection to maintain production.The prospects of the agrcultunl sctor remain dependent on the real exchange raepolicy, the terms of trade for cash crops, and thie climate conditions.

25. Regarding the manufacng sector, production increased in real termsfaster during the parial adjustment period than during pre-adjustment, owing to a vibrantinformal sector. There has been a supply shift from formal to informal sectors as aresult of trade liberali combined with the lack of progress on the real exchange ratedepreciation, energy cost reduction, and labor and wage libealization. Rigidities in amore liberalized policy environment have led to serious difficulties for large-scale firmsthat had previously benefitted from protection against imports and local competition. Thefew large industries that did well were mining, chemical, and energy-industies thatgenerally were not diretly affected by the reforms. The partial reform progam led tosome of the manufacuring sector. It resulted in both the establishment ofa few new firms-mainly small-scale exporft-rented agro-industries,-and the closing ofnon-performing ones. Small-scale enterprises are more dynamic than medium- or large-scale enterpises. SSEs may have compensated for the decline of large firms in spite ofthe weak demand growth in Senegal since 1986. A substantial share of small firms havemanaged to increase investment, output and profits. Manufactuing firms thatsuccessflly expanded after 1986 were relatively more flexible in changing the output-mix, purchaing new equipment, and adopting an export-oriented strategy. Overall, themanufacturng sector has been party restructured with medium- and large-scaleindustries still operating under ptcion. Partly because of the reversal of tradeliberalization policies, and pardy because of dynamic small-scale enteis, Senegal hasnot experenced a major de-industraization as defined by the rapid shrinking of itsindustrial base-though there has been a shift from the formal to the informal sectr.This shift, however, does not provide a satsfctory bwse for Senegal's long-term growthand employment.

26. The public enterprise sector is now smaller (see para 17) and most liklymore efficient than before the adjustment program. There is some evidence ofimprovement in internal mgement of some PEs as a result of their increased financialautonomy (as in the case of sociWts nationales") and the curtaiment of the role of thesupersoy agencies. For some key enterprises, such as the power company, the portauthority, and the railway authority, there seems to be some improvement in theirfinancial and management performance. However, to provide a definite answer to thequestio of efficiency, more detailed information on individual enterpises is needed.

x

27. Despite sagnant and decning real per capita public extpenditures oneducatlou and health duing the 1980s, pimary education and basic healtfi statw hasslightly improved and regional differences have nanowed. In education, the governmenttrained teacher salarie, allowing more teaches to be hired. Teachers in

administrative postons were re-deloyed and major innovations were introduced inprimary education such as mixed-grd classes and double shifts which allowed moreefficient use of classroms and teachers. In health care a reallocation of resources infavor of pdmary health care, increased private and donor financing, and the increasedeffectiveness of peventive health services contributed to the overall improvement. Itshould be noted, however, that thse achievements in social indicators ae not only poorin comparison with counties at Senegal's level of income but, more importantly,represent short-term gains which camot be sustained given the current pattern and levelof resource allocations to the social sectors.

28. Has Senegal succeeded in reducing poverty and in protecting the mostvulnerable groups of the socety during the reom process in the 1980s? This is adifficult question to answer in the absence of hard data. However, it can be argued thatpoverty may have worsened in Senegal during the 1980s as a result of economicstagnation which, in turn, is a reflecton of the of the intenal adjustment stategy thatSenegal chose to follow. Had Senegal fully implemented its adjustment program,including a substantial RER depreciaton, poverty would most likely have bee reduced.This study has also found that the cost of stabilizaion and partial adjustent has notfillen di onately more on the poor than on other social groups. T.here has beenslight ipvement in the rural-urban terms of trade in favor of the runl sector. Thisis due more to the drop in utban incomes than to increases in nual incomes. Public wageeamers had declining real income over the 1980s, with incomes of the unsilled labordeclining less rapidly than those for skilled labor. Thus there has been a move towardsa less skewed wage income distribution.

29. The impact of adjustment on employment is hard to assess given the scarcity ofdata It is etmated that about 8% of tota employment in the modern sector would havebeen lost since 1986, largely in the modern manu sector and the civil service.Most job losses in manu ing were due to the liquidation of a few companies whichwere bound to be closed with or without adjustment reforms. There is evidence that theloss of employment in the modern sctor was offset by job creation in the informalsector. The social safety net progams have contributed marginally to an increase inemployment.

Lessons Lrned and Recmmendaons

30. IBMTrATMoF INTERNAL ADltSDm . The deflationary policy pursuedby Senegal has not produced even the modest results tageted in the government'smedium-term financial program and PFPs. In retospect, the deflationary policy has ledto severe fiscal ession and cuts in public spending in priodity areas; inadequateadminitative capacity has sevey limited the effectiveness of second-best tradepolicies; and no credible income policy has been pursued. Consequently, the internal

id

adjustment process has not produced the expected depeiatn in e real exchange rateand, as a result, eWorts have not performed well, domesfic industry could not competeagainst cheap imports, and private invesment has at best stgnated. Senegal still needsto achieve a rapid, substantial, and sustained depciation in the real exchange rte.

31. The financial stabilizadon achieved so far is fragile and does not providethe basis for long-term financial equilibria and sustined growth. It has inceasinglyrelied on higher taxation at the exense of competitiveness and has led to a reduction ininvestments, in operations and maintenance expendiu, in expenditure on humanresource development (mainly primary education and health care), and in the provisionof adequate public services-all crucial elements for longer-term growth anddevelopment. The small increase, if any, in per capita income and slightly favorablesocial indicators are essentially modest, short-term achievements which are far frombeing satiscory for a meangful development of Senegal

32. PUBLC SBTR MANAGBNT. This has improved somewhat, butmisallocation of public resources remains a problem. Wages and salaries continue to bedispoportonate with respect to expenditumes on maintenance and operations andinvesment, and unless the size of the civil service wage bill is reduced drastically, thefiscal situation as well as the productivity of the civil service sector will deterioraterpidly.

33. While inter-sector allocations appear satisfactory, intra-sector allocationsrmain a problem in agriculture, education and health. Expenditu on irrigation weremade at the expense of extension and research services, those on higher educaton weremade at the expense of primary education, and those on a health curative system weremade at the expense of preventive health care. Inluding the agricultural sector, wherea proposed goverment sector reform program has been under discussion with the Bankand major donors for the last treeyears, the adjustment process has yet to deal with thesocial sectors -n a more comprehensive manner. Given the scarcity of resources inSenegal, alternative ways for the govemment to deliver social services have to be found.

34. More vigorous state enteprise sector-shrinking is imperative. The recentprogress in privatizing public enterprises in Senegal, which can be attributed to a changein govemment stategy towards being prAgmatic while avoiding the syndrome of 'softbudget,' (e.g. subsidies) should continue vigorously. It is recommended that keycompanies, including the gromdnut processing company and the utlity companies, benext in the privatization pmcess.

35. ADDICION TO BUDwETARY AssisTANCE. Senegal has become addictedto budgetary external assistance which accounts for the posponement of hard economicand social changes such as the doinsizing of the ciil service, the adoption of a newlabor code, and the restructuring of the agricultural rice sector. The lack of realsancdons by donors, including the Bank and the Fund, has been a major factor inSenegal's slow progress in adjustment. Further adjustment support for Senegal should

xii

be selective and conditional on the implementaton of up-front key policy meures.Over ime, extenal asie hould shift back to investment.

36. THE ENARLNG ENVIRONMENT FOR THE PRIVATE SBCTOR. Whilemacroeconomic stabilization and relaitve price reforms are necessary, a healthy busnessenvironment is essential to a quick recovery of private investment and growth. Theenabling environment is determined by the following elements: the degree of certaintyabout government policies, the quality of the legal and regulatory framework, the stateof physical infrastructure, and the efficiency of labor and financial markets. Whileprogress has been made in all four years, only in the financial sector has it been fullysadsfactory. In the case of trade policy and civil service reform, policies were reversedin recent years. The deficiency of the labor market, the civil sevice and the regulatoryenvironment (namely the judiciary system) are the most important areas needing rapidreform.

37. GovE,NmT ComrMENT. For any reform progran to be successfullyimplemented, it must be accompanied by consensus-building efforts among the variousinteres groups. This has not always been the case in Senegal. The government's resolveto take actions agreed under the program has weakened over the years, as the adjustmentprogram became increasingly biting and decision-makers became reluctant to oppose theinterest groups (rligious groups, civil service, labor unions) who stood to lose most fromthe reforms.

38. THE ADJUsTmeNr PRocES Am SEQUENCiNG. This process has provento be more complex than stabilization. The packaging and sequencing of the reformmeasures are as crtical as the policy content of the adjustment program itself. As sutedin paragraph 9, the sequencing of the reforms has been seriously flawed in the areas ofreal exchange rate policy, labor markets, the privatization of PEs, the wage billreduction, and the civil service reform. These flaws could be largely corected if the realexchange rate depreciates, and if the regulatory environment and the institutional capacityimprove.

39. In desiging the adjustment program, it is imperative to take into accountthe longer-term objectve of poverty alleviation and the temporary social costs ofadjustment. In Senegal, this was done on a trial and error basis rather than as part ofthe overall macroeconomic framework. This deficiency was due to lack of infornationabout the people expected to suffer the most from the reforms-a shortcoming which willbe overcotme with fte results of the ongoing household surveys.

40. A summary of the major lessons learned and recommendations is presentedin Box 1.

�.

4 4 #�.III 115 II�3. U: Eli Irus

4. 'A if � �k �hI'��i 41%U#11

Ii:N.K.

....

I tli.. �

,.,� run III bti' ULIMfti�R

Sn sea - *4 ,,.~Afle

W 4I4swamaw tS, .4A *a Wu.

vw- msdv .a ia. __" - i_ &flg@ a at p i be Iq-+ _* ;~ A *ka* r' %ar * aafthmci tW bsd*wvmc

so.~~W~l *V'4wai* 4w 60" t 44AFI bM U

it ,tafl4t "S SWU't f* WY *S AX kms as cvss nd 4 e

* .:; 4 ft.n.t rffl-M a dm o a4^d umuue.a J * c e *4i * X -1a (a apclhn wi.aa

W$*'Sijt%}z ̂W *£ * St" f .4A4 L#;lS ..:

J~~ }~ ,P >, *$ W ,, g¢' + tFl Has w4 oft caccmi

4-" obtiM # Jw ti l 'w .*a I b4 ci t mot O 4a XaSk

'B; f *.f ?r'.t' *C0 Xn ?*44 Isat* 'w ib XW b*i tva

:$*4 ? raqpi 4 %4g kiv.;ftfA* 4 sw * subsS ah kiti. ito,~~i h4t4 twk4 r gW4c at t' @0UIfl '*J a 'to-~

c 4 ; iar+* *1. A'~.s I4*LThe bw a pvvba viabt4l. A .JX.*.X y,4', *0 ibs>8s P pvaiawc xm

,-a r .X W'+*4sit *4wWIkt$tat *0 4t4A In gunaz

<+'>'** *i' bf &..wf ti"'*. ij #r4 tea*.bns Stil bt R X

Background and Overvew

Introducton

1.1 This study evaluates Senegal's adjusument perfonrance since 1980, theyear Senegal launched its first adjustnent progrm. The evaluation covers thegovenment's reform program in its entirety, and is not limited to Bank-supportedlending opeaions. In reality, given the Bank's long association with structuraladjustament in Senegal, ar- the IMF's long association with stabilization, an evaluationof the government's reform program is almost synonymous to an evaluation of WorldBank/MP adjustment lending operations. The report focuses on the vaious steps of theadjustment process-from design to implementtion (Chapter 2), and on themacroeconomic and sector adjustment impacts (Chapters 3 and 4). Lessons learned fromthe Senegalese adjustnent experience are discussed in Chapter 5. This study is one ofseveral country case studies being prepared by the Africa Region in parallel to theAfrican Adjustment Study currently under preparation by the Policy ResearchDepartment (PRD).

1.2 This report draws on the findings of several recent studis on economicdevelopments in Senegal, particularly those related to the adjustment exience (seeBibliography). Three studies are worth ngling out: *The World Bank and Senegal,1960-87' (1989d); 'Senegal Maeno mic Update Report (1993a); and wenegalPublic Expenditre Review' (1991b).

1.3 The present chapter gives a brief background on the perormance of theSenegalese economy during the period 1960-80. It highlights the oriin of the financialimbalances that led to a serious cisis in the late 1970s, and consequently to the adoptionby the government of the adjustment program for the decade of the 1980s. The 1980sconisted of two distinct sub-periods. The first half of the decade (1980-85) was a periodwhen litle structral adjustment took place, and, for that reason, is referred to as thestabilization or pre-adjustment period. The second half of the decade witnessed someefforts towards the reform of the economy, and is referred to as the period of partidaladjustment (or adjustment for short).

1.4 The methodology used to evaluate the impact of adjustment on economicperformance (n Chapters 3 and 4) is the 'before and after approach. The main flawof this approach is that it relies on the assumption that other things are being held equalwhich is highly implausible. To complement this approach, it is suggested that futurework focus on othr methodologies which have been followed in the literate. The'control group' approach allows, in principle, to overcome the inability of the 'beforeand after apprach to distinguish the dfect of adjustment per se and the effect of otherfactors. It compares the performance in adjusting counties with performance in arefrence group of non-adjusting counties to esimate what would have happened in theadjusting counmtes had adjustment not taken place. The control group approach would

2

be the most appropriate approach for this kdnd of analysis, but the lack of reliable dmeseries data precludes any attempt to quantify the impact of the reforms.

lhe Emic Sening

1.5 Senegal is a small, semi-arid Sahelian nation with a population of 7.6million, predorinny rmal, and with limited natural resource endowments. Themainstays of the traditional economy remain millet cultivation and nomadic cattle ramsingfor domestic consumption, and groundnut cultivation for exports. The modern sectorincludes fisig, phosphates, chemical industres, and tourism, and is concentrated inDakar and on the coastal belt. At the current exchange rate, the 1991 income per capitaof US$720 places Senegal almost at the bottom of the lower-middle-income ecnomies.

1.6 At independence in 1960, Senegal inherited a relatively well-developedphysical and social infrastucture due to the prominent role Dakar played as the capitalof the large French West Afrcan colony. Senegal has enjoyed a high profile in Africanaffairs and has been, until recently, the only Sahelian country with a lively democraticsystem, including a vocal press. This has helped Senegal mobilie substantial externalresources over the years. Seegal has had a long tradition of 'African socialism'resulting in widespread direct government intervention in the economy, and regulatorycontrols. Cultural values still play an important role in social, economic and politicalspheres.

1.7 During the first two decades following independence (1960-80), Senegal'seonomic performance was on the whole poor, even by Sub-Saharan Africa standards(Table 1.1.) GDP grew on average by 2.1% per amum compared to a populationgrowth of 2.8%. Senegal experienced the lowest GDP growth rate of any African statenot affected by war or civil strife. This period can be divided into four distinct sub-periods. Until 1966 when Senegal lost the preferental tment accorded to itsagicdultal exports to the EEC, the economic management was relatively sound and theeonomy grew at about 3.5% p.a., surpasing the population growth rate. Between 1967and 1974 when the world oil price quadrupled, GDP grew by only 1.3% p.a., andgroundnut producton fell by almost half. During this period, Senegal actively pursueda n lion policy and an industrial import-substitution policy. During the thirdperiod, 1974 to 1978, the average GDP growth rate was roughly the same as population,largely explained by favorable weather conditions and a very favorable terms of trade,reldting from higher world prices for phosphate and groundnuts.

1.8 During the fourth period, 1978 to 1981, Senegal experienced two majordroughts together with a substantial fall in groundnut world prices and, corespondingly,a GDP growth rate of 0.8% p.a By the end of this period, aU key economic indicatorsreflected serious financial and st rl imbalances. The fiscal deficit and the currentaccount deficit reached 12.5 % and 25.8% of GDP, respectively. Savings were negadveand total consumption exceeded GDP. The inflation rate soared to 12% and the tennsof tade dropped by 12% between 1975 and 1982. The total stock of debt represented967.4% of GDP and the schedled debt seri represented 18.5% of total ports of GNFS.

3

TWs 1: MUMMAo k&AW 196041

RSWGM"& Rat. (%) shaawefGDlP(

196i70 19M70 19I75-80 1060 1970 198

GDM 2.5 23 1.8 100.0 100.0 100.0GDP par capIta 0.2 .OS -1.0 - - -Prdmay Secmort 3.0 0.9 1.0 24.3 24.1 17.8Export GNY4 0.1 6.0 -0.7 39.6 27.4 32.1Up" of GNPS 0.2 7.4 1.4 40.6 32.0 51.4ODI 1.4 4.4 0.6 15.6 IS.7 12.60Ds 2.1 5.2 -2.8 14.6 11.1 -6.5GovanCOnto 0.8 S.3 5.8 17.3 14.9 20.4PMAW Corpti o 3.0 2.6 2.7 68.1 74.0 863

tnflatlonte (GDP deflor) ... 7.4 9.1 ...REER (198S-100) ... 5.6 -3.2 ...Fbcal defict bl ... ... ... ... -0.6 -12.SCurmnaocouJt dieict e/ ... ... ... ... 410.4 -25.8Debt vice scheduled ... ... ... ... IA 7.4

ai Inluding aqlcul, Uveac fatry ad fierqbI On a c - bais A and ecluding ra8c/xludn officiltanfr-Ekiber not railal or not aplicble

Soue: World D data Sfl ad aff e_mes.

1.9 The need for strucural economic c in Senegal can be traced to the earlyyears of independence when Senegal lost its large French West African market, andended up with oversized industies and public sector. The key economic indicapointed to macroeconomic imbalances as early as 1966, when groundnut epot suddenlylost their guaranteed French market and had to compete in the world marlkts.Government was slow to recognie the need for strucual changes. To make materworse, the government responded to the short-lived commodity boom in the early yearsof the second half of the 1970s by borowing heavily from foreign commci banks inexpectaton of a return to more favorable terms of trade. The 1987 Country EconomicMemorandum observes that wadjustment became unavoidable at the end of the 1970s,when a combination of poor financial and investment policies, woened terms of tradeand successive droughts plunged an aleady weakned economy into a severe crisis.0

The Goverwn a's Response to die Financi Cisis

1.10 In the late 1970s, the govemment began to recognize the sotcomings of itsambitious public sector development plans and na lion policies and in December1979, it announced its medium-term program for economic and financial adjustment,

4

known by its French acronym PREP (Plan a moyen terme de redressement economiqueet financier), covering the perod 1980-84. This program was designed in closecollaboration with the Bank and the Fund and sought to stabilize the financial situation,raise public savings, increase investment in the productive sectors, liberalize trade, andreduce the state role in the economy. This first attempt at stabilizing the financialsituation and creating the basis for growth did not, however, yield satisfactory resultsbecause of lack of implementation of agreed adjustment measures. The IMP three-yearExtended Fund Facility (EEF) arrangement, which was approved in August 1980, wasshifted to a simple one-year stand-by a year later, which in turn was canceled in 1983.Something similar happened to the Bank's first structual adjustment loan-it wasapproved in 1980, but its second tranche was cancelled in 1983.

1.11 Renewed efforts were launched in 1984 with the same broad policy objectives inmind. The first meeting of a Consultative Group (CO) for Senegal was organized by theBank in December 1984, after which Senegal prepared a medium-term adjustmentprogram for the period 1985-92 which was endorsed by the donors. This was followedby a second CG organized in 1987. The government's adjustment effort has beensupported since 1980 by four Bank SALs (1980, 1986, 1987, and 1990) and twoSECALs (financial sector in 1989, and transport sector in 1991), and by a series of IMParrangements (EFF in 1980, followed by five standbys, a two-year SAP and a three-yearESAF). Senegal, along with Kenya and Turkey were the first countries to receive anadjustment credit or loan from the Bank. A total of five Policy Framework Papers(PFPs) were approved by the Bank and IS Boards between 1986-91. Senegal has beena recipient country of the Special Program of Assistance since its establishment in 1988.The adjustment program in Senegal has been generously supported by the donorcommunity, either directly or as co-financiers of Bank opeaions. Between 1981 and1991, adjustment support to Senegal accounted for nearly two-thirds of total netdisbursement of official development assistance (ODA) which, in tun, represented 4.3%of the total amount received by Sub-Saharan Africa. This contrasts well with the smallweight of Senegal in SSA as measured by the shares of its population (1.5%) and grossnational product (GNP) (0.3%). In 1991, net aid flows per capita to Senegal amountedto US$84 or 12% of GDP per capita.

Senegal Database

1.12 The analysis of Senegal's economic performance is complicated by significantweaknesses in the country's databas. The recent Macroeconomic Update Report (1993a)points out that official s.tastics are paricularly weak. Senegal's national incomeaccounts sistics continue to experience long delays in publication. Some evidence forthe poor data quality are presenied here. There are unexplained discrepancies betweenthe performance of agriculture and industry as measured by crop output or productionindices and the national accounts figures. The composition of sectoral output raisesserious concern. The tertiry sector in Senegal accounts for over 60% of GDP, a figuremore likey to be found in industal economies than in developing countries, particularlyat Senegal's level of development, which ranges from 35% to 50%. As much as 40%

5

of total GDP b on exralions of data obtained from old baseline surveys.Finally, agie's cotribution to nominal GDP seems to be overestated due to thepactie of valuing local coare gains at official prices while official purchases accoutfor less tha 10% of total output Senegal's balas.ce of payments data, parcularly dataon mradi exports, as show major siortcomings. Consequenty, th figumunderlying the analysis in this report awe peliminary esmat and may be subject tosgnifict alteations. This challenges the accuracy of Senegal's actal economicpeomance, which may in fact be much lower than the official figures.

2

Design and Implementaion of the Adjustment Program

2.1 This chapter 1' deals with te desin and implementation of policy reforms inSenegal during the 1980s. The intnal adjusment stgy that Senegal adopted rliedon policies othe ta exchange rate adjustment to restore growth and internal andexternal balance. These policies consed of dexlationr monetary and fisc poliies(demnad management policies), second-best trade policies igh tariffs and exortsubsidies), and structual refonns. The latter reforms ae designed to liberalize marketsand prices, reduca the size of te public sector and rationalize its activities, andencourage private sector investment and development. Retrospectively, the interaladju*ement policy proved to be more and more difficult and complicated to implement.This shows clearly the importance of the exchange rate as one of the major adjustmenttools. It is not certain that the Senegales economy could get out of its long recessionwthout a more fleible exchange rate poLicy. Under the intemal adjustment strategy,If competitivene is achieved, it will be achieved in the final phase of the adjustmentprocess rather than at the beginning when a depreciation of the real exchange rate is partof the adjustment program.

2.2 This chapter is organized in four sections. Section one covers fiscal, monetaryand exchange rate policies; secton two covers pridng and trade polices as well as laborand wage policy; and section three covers key sectors in the economy (financial, publicentepises and social sectors) as well as the institutional and legal frameworl Finally,sectn four provides a summary assesment of the adequacy of the reform program inSenegal in terms of ooverage and sequncing, and the progress made in implementation.

A. Macroeconomic Policy and Management

Fisca Poliy and M

hntr"oduct ki

2.3 As in most countries undergoing adjustment programs, fiscal policy was used inSenegal as a primary insument for reducing aggrgate demand and conecting majordisequilbria in the economy. The frmework for fiscal policy in Senegal is, however,affected by several facts which not only complicate the design of the refonn program

jI A longer version of this chaptr make up the enir report wrien by tbio author wi& coauthor Brian Ngoentitled Mesig and of Adjusmeat Pograms in SenegaL.

8

but also render the assessment of the peface more intricate. Some of these factorsare spedfic to Senel; others are reated to the nles that rguate fiscal and monetarypoUces within the West Afican Monetary Union (mown by its French aconym UMOA)of which Senegal Ii a member.

2.4 Becs. Senpl belongs to UMOA-which among other tins regulatesthe money suply by a4ustng crits-Senegal has relied on fiscal policy for its

I4ustmmt effort. While the French Tresury's "operations accounte provide UMOAcountries the 8une of fincing balce of payments shortfa, safeguard featuridopted by the Banque Cetae des Ea de l'Afrdque de l'Ouest (BCEAO) (the regionalcental bank) to prvent monetary expansion impose a statutory act wherby themaximum level of BCEAO advances to the Senegalese Govemment may not exceed 20%of the previous year's ordinary budgetary receipts. While there are several sources ofleakge to this overdraft rule, the rule does impose a limit on the financing ofgovment deficits from the central bank. Thus, while Senegal's membership in UMOAmay help limit th reat dof inflaton, the system is prone to liquidity ctises.

2.S The stcu of the public sctor in Senegal further complicates theman_gement of public finances. In addition to the consolidated central governmentoperains, the Treasuy maintains divers specia and corespodent accounts. Untilchanges intoduced in July 1991, these accounts were not int into the budget andwe not subjected to normal budgetauy procedures. Thus, the lack of effective controlon these accounts could cause large yearly variations in the Treasury's liabilities vis-i-visthese accounts. The design and management of fiscal policy was also more complexbecause of the close assocation of key fiscal measures with the industrial policy,parcularly those related tf tariff reforms and production costs.

2.6 Some of the policy conflicts reflect the constant prccpation with theshort-tum and, to some extent, a conflict of objecdt among donors, particularlybtwen t DIP, wbih gave p to issues of stabiliztion and thus theoverwheing cono about rvue mobilizmon at tbe exense of growth promotion,and W od k which put geater empha on longer-term issues such as reducingtbe costg k inpu and th corpt tax e. Also large inflows of official assistancefom m l agen and bilate donors (Prance in partcular) made it possible forSenegal to postpone "hard-budget" choices (see paras 3.10 and 3.11).

Desgn of the Rgfbnn Prgram

2.7 The reform of fiscal policy in Senegal covers a broad range of objectives,the most im ant of which is to inWoe govemmm nces. Senegal began thedecade of the 1980s with in ovUrall budget deft (on a payment order basis andeluing grat) of 12.5% of GDP (dmary defict of about 10% of GDP) and a totalpublic aedture of about 32% of GDP. The civil ce wage bill, by far the largestepedtre item. accounted for 40% of total ependi. A key fiscal objective wasto nance the buoyany of the tax ytem to increase revenue. Following the

of an ItP fiscal mission which visited Senegal in May 1985, the

9

government adopted a fiscal reform program aimed at modernizing the tax system,creating a more effective and less distord tax regime, and widening the tax basn.

2.8 The government also pursued a restricted expenditure policy. Itrecognized the need for a two-pronged approach-to control the wage bill and to limittransfers to the Public Ent:prise (PE) sector. Measures were takm to contain the wagebifl either within a ceiling or as a share of total expenditures, and to reduce the numberof civil servants. These measures (such as the avoidance of general salary mereases andthe limitation of advancements and promotions of civil servants) were mostly ad-hoc innature and not until 1990 did the government adopt a coherent civil service progam (seepam 2.85). Another important component of the fiscal reform was to improve thefinancil performane of public enterprises so as to reduce the budgetary burden of thatsector and to increase the sector's efficiency (see para 2.69). With a few exceptions(road maintenance and primary school teachers recruitment under SAL IV), no specificmeasures to protect key social sectors, to provide adequate exenditures on opetionsand mainteance, and to protect a core public investment program were built into thereform program.

2.9 Another important objective of the fiscal reform progam was to improvete pubikc inwesment program (PIP) by adopting a thre-year urollingw PIP. This wasdone in 1986 and has since ben updated on a yearly basis. The objectives of the PEPreform package were to: make investment projects consistent with the macoeconomicfamework and sectorial priorities; improve project prepation and appraisal; monitorsystemadcally the physical and financial aspects of project implementation; incorporatethe investment budget into the government's overall budget (keeng recurrent cost andindbtedness implications in mind); and strengthen technical ministries' capcity toidentify, prepare, and monitor their respective projects.

2.10 The third fiscal objective was to improve the extenal debt managementsystem. A computeaized debt management system was established with IDA-financedtchnical assistance to provide data on outstanJing debt, arrears, and scheduled debtevice and to issue computerized payment orders. To improve the strre of its

exnal debt, the government also implemented several measures to discontinuecommercial borowing, curtail public guarantee to private borrowers, and stop thetansfer of proceeds from debt relief negotiated by the government to the final borrowers.

implmeadon of the Rform Program

2.11 The implementation of the fiscal reforms varied across policy areas. Since1986, the government has initiated wide-ranging tax reforns. A general tax code wasintroduced in early 1987 aimed at changing specific dties to an ad-valorem basis, andwidening the scope of the value-added tax (VAI) to trzde and constrution sectors. TheVAT was genelized to sevices and the transport sector in 1991 and VAT rates worerevised to simplify and reduce the rate structure. Refrms of foreign trade taxatioi,included simplifying the tariff struct-c annd the lifting of QRs (see pam 2.29). InSeptember 1989, the govemment instituted a withholding tax on professonal and

10

propety income, a glob tax on personal income-replacing a variety of sctedular taxes,and, in Januay 1990, it placed a single tax of 35% on corporate income. Another effortto widen the tax base consisted of corapledng the fiscal cadastre for the Dakr region;follow-up meases to institute the tAx have, however, suffered much delay. Finally,efforts were continuing to be made to raise tax revenue fiom the informal sector.

2.12 In parallel to reforms aimed at modenizing the tax system, sevel othermeasures were introduced to mobilize additional revenue. , The design andimplementaton of this plethora of new measures was particularly taxing to the- limitedadministrave capacity and the government tended to focus efforts on short-termconsideions rather tan on structural issues. The new measures also resulted inadditionaldistortions to an already ratier elaborate tax system. The predominance ofshort-term revenue considerations over longer-term growth promotion measures haveprevented a meaningful reduction in the energy cost and the sustainability of the customtariff harmoniztion and reduction.

2.13 The implementadon of measures aimed at reducing the size of the civilsevice and controlling the wage bill encountered serious slippages (see pam 2.86) andas a resdt the wage bill st represented the lion share of government revenues andrecurnt expenditures. The lack of significant progress in the control of transfers (directand indirect subsidies) to the PEs reflects the complex situafon in this sector and the lackOf commitment of those in chwge of the reform to undertake politically sensitivedecons to reduce the amount of transfers from the budget to this sector (see pam2.74).

2.14 Management of the PIP has improved, particularly in eliminating conflictsbetween capital investment and sector strategies. Prtects are also generally betterprepared. Institutional capacity buiding must continue to be strengthened or elseprogress achieved so far will be iheatened. To do this, the cpacity of technicalmisties to identify and prepare projects in their respective sectors must be strengthenedand coordination between services in charge of the PIP and Treasury staff enhanced sothat recurrent cost and debt implications of the PIP are clearly reflected in the budget.Without this coordination, there is a high risk of insufficient allocation of operatons andmaintenance for new projects and, consequently, poor project economic rates of retun.

21 /iorwt maae introduced in the lat three Yas include: Oi a S percent ine in coms duty tax(Au 1989); (0) the Intrduction of minimum assosed tan imports (September 1989) and their extnionto a much largr group of commodite (July 1990); ( an increase in a number of stamp duties (by between50 and 100 percent) and an nreaed excise tax on cigaettes, alcoholic beverages, tobacco products, softdrinks, coffee, and tea (August 1990); (v) an inoduction of an ad-valoem toms fee of 3 percen (August199I) (v) a reduction of deferrd customs payments (1990.91); (vi) an Ireaso in personal income tax ratesby S pret (Ocber 1990) wAich was later rescinded becae of strng polica resitnco; (vii) an incrsein raes and covee of stamp t and fees (August 1990); (viii) the inrduction of a tax on sugar (March1991); ( tho tion of a transaction fee of S pe¶cent on sales of used motor vehicles and of 2 percent fornw vebicles Mach 1991).

11

2.15 As discussed in Chapter 3, the financi position of the governmentimproved duing the 1980s, though not without serious problems left to be resolved.Poor tax adminion was magnified by the need to design and implement numerousnew taxes within a short time perod. Equally important, the decision to proceed withthe liberzaion of the economy before the establishment of an effective taxadministration and before subiliaion results were conolidated reflect insufficientconsiderion given to the sequencing of the reform program. Oter reform measureshave seen their impt drastically reduced because of poor implementation. For instance,efforts to combat under-invoicing through computeized customs declaration have so faryielded few significant results because concrete efforts to improve the funcioning of thevalue assessment section, without which under-invoicing remains mostly undetected, havenot been rigorously undertakn. Recent experience with the Societe general. desurveilance offer some hope for improving customs receipts. Deficiencies in revenuemobilization and in controlling the wage bill affected the other expenditue items whichfiurther undermined the success of fiscal adjustment.

Monetay Policy

Design of Monetary Policy

2.16 Within the institutional framework described in Box 2.1, Senegal'smonetary policy aims at three objectives: to manage overall demand to correct extnalimbalances; to gain a competitive advantage by keeping the level of inflation below thatof major trading partners; and to strengthen the management of liquidity and reinforcebank supervision. While the first two objectives mentioned above were achieved mainlythrough restrictive credit policies, a more comprehensive set of measures was undertakenin the banldng sector including the introduction of market-detemined interest rates.

2.17 In September 1989, Senegal adopted, with other members of the UMOA,a comprehensive reform of monetary policy instruments designed to replace theadministive controls over money and credit with an indirect and market-orientedsystem of monetary instruments. In particular.

(a) the preferential rediscout rate was abolished; the centralbank's refinancing rate was set above the money marketrates-at levels slighy gher tan those for the Frenchfranc-and bank were given more flexibility indetermining their rates on deposits and loans;

(b) conditions for acce to centr bank rinancing weretightened and crop credit will be refinanced by the centralbank only if it is within general refinancing limits andunder the overall credit ceiling of the commercial bank;

(c) rigorous controls were placed upon state guarAntees forborrowing of public and private enteprises. Government-

12

guaranteed non-performing loans will be Imputed to theoverall credit ceiling set for the government;

(d) the system of secoral credit allocatn was elimnted andprior autoization will be used only as qualitative creditcontrol instrument; and

(e) the BCEAO's bank inspection and supervision were sharplyreinforced with the creation of the union-wide banksupeMision body (Comssion banWcaire).

u gu l a8t 4E t&Nf N, Gu Na Ibj Dls.~ 19ZVO

S E !~~~~~~g . .... . .

~~~~~~~~~~~~~~~~~~~~~~~~~~~. .. g .. .. .

4qatoIV*EeN o$tD m4Sofb E>o~a

- !;~ 4as'~~aq

13

2.18 In a subsequent phase of reforms, the introducdon of reserve sis envisaged. Duing the transition period, the conduct of monetary and credit poicywill contnue to rely maily on intre te policy and overall credit ceilings.

Implemetadon Of dX RfornM Progr8m

2.19 The heavy involvement of the BCEAO, and the need to re-etablishconfidence in the banking sector, after the ailing banks were liquidated, led to a forefuland timely implementaton of monetary and credit policy reform. With minordiffeences, most of these reforms applied to all members of the union, thus givin moreimpotance to their implementation. The reforms have led to a sounder environmentwhere government interference in the proces of credit allocation is limited. Thegovernment's reliance on bowng from the bankng sector has been cured due tostricter controls on government's borwing tough sate-owned entepris.

2.20 The BCEAO's adherence to a restictive monetary policy in the Last fewyears has improved Senegal's extra accounts. a This policy has, however, severelycons*tained domestic credit to the rest of the economy. During 1986-91, crdit to thenon-government sector (excluding crop credit and the refinancing of ONCAD debt)increased on average by only 0.7% per year (in terms of money supply at the begininof the year); in real tms it declined substantially. The money supply (M2) has folbweda similar trend although the decline has been less severe. As a result of these trends, theratio of M2 to GDP which measures the degee of fnancial deepeniq has fallen from0.28 in 1984 to 0.23 in 1991 (see Table 2.1).

2.21 The BCEAO polic appeared, in the context of the fixed exage rate,appropriate to maintain a ssaiable external position, particularly given the lack ofsuccess in contrling the fiscal situation. it is questionable that this policy can bemaintained without an adverse impact on the growth of the economy. This issue will

at n view of its sianc in ft dermInato of money and credit policy, dveopment of Segl's otexterna poston warrants a brief descit at this Jure. h oxternal at positio boga to saIlie n1989 following wide flucuon expienced durt 1983488 ac cout of a mared Ih theexternl curmt acount betwe 1983 nd 1985, folowed by sinfat privat capil outhowi 1987 nd1988. As a result, Senel's egav position In t operations account rubed a peak of CPA? 97.2 blinin Jun 1986. The ddetioration of Senga's eral acounts tbrough 1985 smmed from high Im t, adirect refction of fte hig lvol of ovell demand. A stgficat improvement in th exteral acco bein 1986.

Mst of ths improvemet ca be atrbuted to the pursuit of strict mneary polcy. Tbefiscal situato,which improved significantly from 1982 through 1987, worsened during the peod 19870. As hw inTable 2.1, BCEAO's nt oims on the Govermen declned shaply 1 1987. Teso d.vel fnt reflet dheavailability of lager extl budgetary asistace In support of the country's strctua a4stment program.The was o evidence of efforts to reduce net leding to the govenment, irrepecv of th dstatu oyldefined in the BCEAO's ro and regulons which mits total advances to theo Goem t to 20 perc offical revesaus collwcted h tho previous year. This development was even mao nlo if oe ca0sa thoseries of measures desgned to curta government borrwig via the proviion of guammos for borrwing bypubli entep from the banin sector.

14

Tabb 21: Sumaof Monday Indicaor(Annal cho I % uept MGDP)

Cred to Mono NOnalr RualOYer GvRnem /g Ecoomy I (M2) Ig GD?P M4/ODP

1984 5.5 2.0 5.2 8.1 0.281985 7.5 8.6 4.5 13.4 0.261986 1.6 1.3 11.2 12.S 0.261987 -1.7 3.5 0.2 6.1 0.241988 2.3 9.6 0.5 7.3 0.231989 -7.2 1.3 10.3 0.1 0.251990 -5.2 8.6 -4.8 7.0 0.221991 0.6 -4.3 5.8 2.5 0.23

It Change in p_erntag of the money ulmf;y at the begining of the peiod.

Source: Senegal - Mwacmwonomic Update Report (SA Table 48), June 1993.

be discussed in more detail in the next secdon of tis rep. The policies have also beensuccessful in controlling fte rate of domestic inflation which has stabilized at below 3%in recet years. Better control of inflation has helped Senegal recover a cerin degreeof competitiveness.

2.22 One of the results of the monety and credit sector reform has been thelibealiztion of the interest stcte. By eliminating the preferntial discount rat-which formerly applhed to agriculture, the eot sector, small- and medium-sizedcompanies and residential constrction-and the libealiation of margins andcommissions, lending rates for prime borrowers curntly stand at 16% to 18% while theinflaton rate remains at less than 3%. Banks' lending continues to reflect the prefeenceof short-term trade-related activities at the expense of longer-term investment projects,thereby undermining the growth prspects of the economy. Between 1985 and 1991, theshare of short-term lending increased from 60% to 67% of cumulative bank lending,while loans to industial proects have fallen from 22% to less than 15%.

2.23 The conduct of monety and credit policy in Senegal has been desinedand implemented in a firm, timely and consstent manner. These measures have helpedin keeping infladon low, curtailing overall domestic demand, providing the basis for amore robust banking sector and restictng government intervention in the allocation ofcredit. They have not, however, succeeded in creating tie foundadons for sainablegrowth.

IS

-_ UME

.-ea.w of t 1A.%A, SecgaJ has enjoyed, since 1948, a convertible4 -' M t fa p *ith thec Frnc h frac (CFAF 50 per French franc).

4^ >.a.. > . 4.ULV s AZtu t smpkru and transferability of capital. The.. **. ,, +., ,> ; s- S rnA& biiils duwn t an implicit effort to depreciate the

1e4&49 fS~44 #w , 4U M*Aftf WOM-CU

-'t -^v4m t 9dn, Senegal has witnssd a swing in its terms.i .,;-cA -,... £ . r. d h..h infUitary rtes and low productivity gains.

*} 1t~' ii .+: *+t .2--iv ; < i mir by 4.5% per year compared to Senegal's." 'L .s ; *-- 2* t ->< , eclrwxI vsnce. This development, together with

z$48 J :> . ^$.&, t XfN..< utof nonCFA neighboring countries and the>', .A- .f. l, ' _' W¶, htc ,+i 46a, eicvcrely eroded Senegal's competitiveness

%"$V UA tflwt V."&~ Ra3 JIM - 100)

T;m oxf Rrim.e 8awe 'GDP)

-5.2-14.5

4 ;,.-19.3.4.4+ r: u -12.3

-12.3.4Ly .* % 9.5

-11.2

IA s 8 t .8 -5.6)ts 44 1 ls -5.0

V<i- I s S i X -5.2-4.7

£4 IA .4.9

.... . .... o. _ ... I - .zhat" defu. byiw -S *,-. . .. .,W..CAgo .,, 4*AW.g&4is iJO.& &s- r Sea s .w 20 awe imota nt Imdiztg

16

2.26 The movement in the real ecffeve exchange rate (EER), a commonlyused measure of compedtivenesss, h that, in the 1980s, while the competitivenessof other developing countries (SSA, Lati America, heavily-indebted middle-incomecounties) was improving, that of the CFA zone, including Senegal, was actallyworsening despite implementaton of intnal adjustment progams. Table 2.2 indicatesthat the REER has depreciated (in foreig currency tems) by 14% during 1980-84 andthen preciated by 20% during 1985-91. The appreciation of the REER during thesecond half of the 1980s is due to the appreciation of the French franc vis4-vis the U.S.dollar and the Naira. The real exchange rate vis-k-vis Ghana, Nigeria and China, againstwhich Senegal has to compete on export markets, have substandally arat,paicularly since 1985. v'

Real Exchange Rate and Balance of Payments

2.27 The reationship between the real exchange rate and the trade ba e, canbe observed in Table 2.2. In Sbenea, while the REER appreciaed by 20% between1985 and 1991, the trade baance had improved by 6 percentage points of GDP. Acloserlook atthe disaggpgated data provides an explanaonin ine withtheory. ITheimprovement in the btade balance was due to a drop in exports by nearly 5 percentagepoints of GDP in line with expectations, and a drop in official imports by 1 percentagepoints of GDP. The latter was a direct result of drastic cuts in public expenditreprograms, partcularly investment, and low growth.

B. Pricing wad Trade Policies

Internaional Trade Reform

Background