seminar for senior bank supervisors from emerging...

TRANSCRIPT

Seminar for Senior Bank Supervisors from Emerging Economies

WHAT’S GOING ON IN BASEL?

Antonio PancorboFinancial Supervision and Regulation Division (MCM Department)

October 30, 2017

THE VIEWS EXPRESSED ARE THOSE OF THE PRESENTER ONLY. THEY DO NOT NECESSARILY REPRESENT THOSE OF THE IMF. PLEASE CHECK AGAINST DELIVERY.

The Basel Process

• A set of minimum standards

– Countries can go beyond that

• Based on consensus among members

– Standards not necessarily technical first best

• For internationally active banks

– Countries need to adapt to local markets and circumstances

• A common language on supervision

– All countries should comply with the conceptual framework

• Binding to Basel Committee members

– Other countries can go differently in its actual implementation

3

Basel Committee: created in 1975 by the G10 at the BISMembership expanded in 2009 and again in 2014

45 members from 28 jurisdictions--Argentina, Australia, Belgium, Brazil, Canada, China, European Union, France, Germany, Hong Kong SAR, India, Indonesia, Italy, Japan, Korea, Luxembourg, Mexico, the Netherlands, Russia, Saudi Arabia, Singapore, South Africa, Spain, Sweden, Switzerland, Turkey, United Kingdom, and the United States Plus 9 observers—Chile, Malaysia, United Arab Emirates: plus, BIS, the Committee’s Basel Consultative Group, European Banking Authority, European Commission, and the IMF

4

5

Organizational Structure

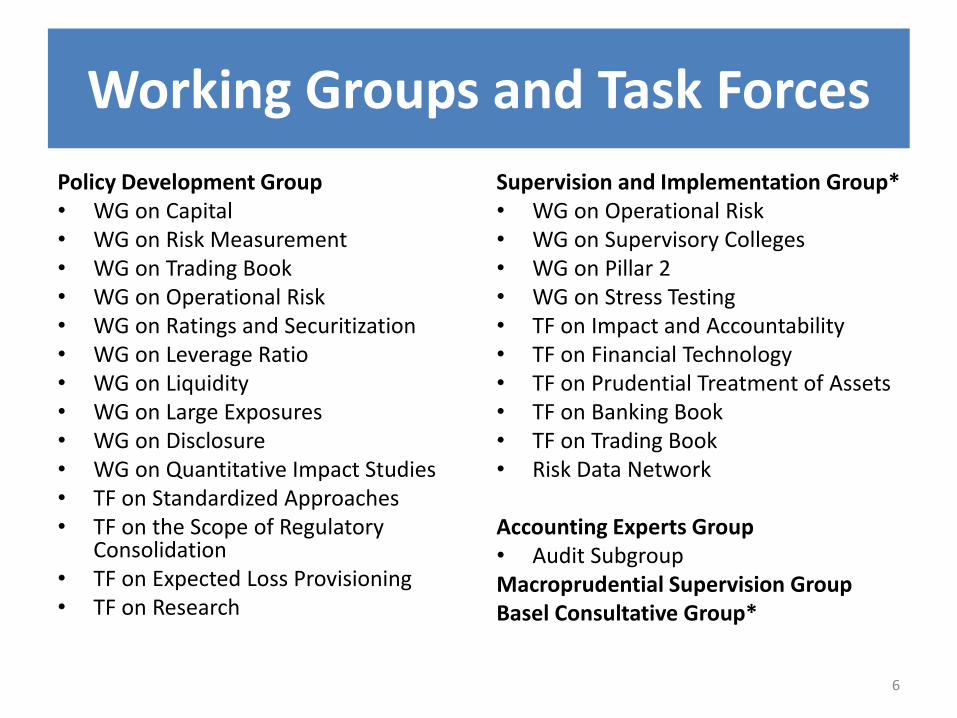

Working Groups and Task Forces

Policy Development Group• WG on Capital • WG on Risk Measurement• WG on Trading Book • WG on Operational Risk• WG on Ratings and Securitization • WG on Leverage Ratio • WG on Liquidity• WG on Large Exposures • WG on Disclosure • WG on Quantitative Impact Studies• TF on Standardized Approaches• TF on the Scope of Regulatory

Consolidation• TF on Expected Loss Provisioning • TF on Research

Supervision and Implementation Group*• WG on Operational Risk • WG on Supervisory Colleges• WG on Pillar 2• WG on Stress Testing• TF on Impact and Accountability• TF on Financial Technology• TF on Prudential Treatment of Assets• TF on Banking Book • TF on Trading Book • Risk Data Network

Accounting Experts Group• Audit SubgroupMacroprudential Supervision GroupBasel Consultative Group*

6

Basel Committee Outcomes

Standards

To be implemented by Committee members in their internationally active banks by the predefined timeframe.

Guidelines

Supplement Committee standards by providing additional guidance for the purpose of members’ implementation.

Good Practices papers

Describe actual practices to promote common understanding and identify areas for improvement among members.

Implementation and others papers

Moving forward

To issue Basel international standards that are simpler, allow for comparability, and provide for proportionality in application.

7

Cumulative Number of Finalized Publications by the Basel Committee

Basel Committee documents

STANDARDSJun 2017--Simplified alternative to the standardized approach to market risk capital requirements - consultative documentMar 2017--Regulatory treatment of accounting provisions -interim approach and transitional arrangementsMar 2017--Pillar 3 disclosure requirements - consolidated and enhanced frameworkOct 2016--TLAC holdings standardJul 2016--Revisions to the securitization frameworkApr 2016--Interest rate risk in the banking bookApr 2016--Revisions to the Basel III leverage ratio framework -consultative documentMar 2016--Standardised Measurement Approach for operational risk - consultative documentOct 2014--Basel III: the net stable funding ratioApr 2014--Supervisory framework for measuring and controlling large exposuresApr 2014--Capital requirements for bank exposures to central counterpartiesJan 2014--Liquidity coverage ratio disclosure standardsJan 2014--Basel III leverage ratio framework and disclosure requirementsJan 2013-- Basel III: The Liquidity Coverage Ratio and liquidity risk monitoring toolsOct 2012--A framework for dealing with domestic systemically important banksSep 2012--Principles for the supervision of financial conglomeratesSep 2012--Core principles for effective banking supervisionDec 2010--Basel III: A global regulatory framework for more resilient banks and banking systems - revised version June 2011Jun 2009--Core Principles for Effective Deposit Insurance Systems 8

GUIDELINESOct 2017--Identification and management of step-in riskJul 2017--Criteria for identifying simple, transparent and comparable short-term securitisations - consultative documentJun 2017--Sound management of risks related to money laundering and financing of terrorism: revisions to correspondent banking annexApr 2017-- Prudential treatment of problem assets - definitions of non-performing exposures and forbearanceSep 2016--Guidance on the application of the Core Principles for Effective Banking Supervision to the regulation and supervision of institutions relevant to financial inclusionDec 2015--Guidance on credit risk and accounting for expected credit lossesJul 2015--Guidelines for identifying and dealing with weak banksJul 2015--Corporate governance principles for banksJun 2014--Principles for effective supervisory collegesMar 2014--External audits of banksJan 2014--Sound management of risks related to money laundering and financing of terrorismJan 2013--Principles for effective risk data aggregation and risk reportingJun 2012--The internal audit function in banks Jun 2012--Composition of capital disclosure requirements - Rules textDec 2010--Guidance for national authorities operating the countercyclical capital bufferAug 2010--Microfinance activities and the Core Principles for Effective Banking Supervision - final documentMar 2010--Report and recommendations of the Cross-border Bank Resolution GroupSep 2008--Principles for Sound Liquidity Risk Management and Supervision

9

The Basel Committee Flagship

Basel I Basel II Basel III

Basel Accord 1988, first international agreement

Focused on sufficiency of capital vis-à-vis credit risk

Fixed risk weights

Amended in 1996 to include a parallel capital requirement for market risk

Published in 2004

Introduced 3 Pillars

Menu of more risk-sensitive approaches

Sup review process

Disclosure

Broader coverage of risks

Credit risk

Market Risk

Operational Risk

Published in 2010

Implementation 2013-2019

Capital: better definition of capital, enhanced risk coverage, new and higher ratios

Leverage Ratio

Mitigate pro-cyclicality

Capital Conservation and Counter-Cyclical Buffers

Two new Liquidity Standards

Focus on Global Systemically Important Institutions

G-SIB surcharge

Enhanced disclosure

Securitization, off-balance sheet vehicles, components of capital

Proportionality of policy implementation

• The complexity of Basel III raised the issue of “proportionality”– ie -- how best to tailor regulatory requirements to non-internationally active banks, especially

smaller and less complex ones.

• National approaches to proportionality differ considerably.• Key features

– the criteria used to identify the banks to which a proportional framework is applied– the scope of the regulatory adjustments for smaller or less complex banks to reduce the

operational burden for banks

• Proportionality should acknowledge other relevant policy objectives, such as – the implications for financial stability – the implications for the domestic competitive environment– Proportionality should entail rules which are simpler but not necessarily less stringent

See “FSI Insights on policy implementation No 1: Proportionality in banking regulation: a cross-country comparison” August 2017 www.bis.org/fsi/publ/insights1.pdf

10

Capital “per books” may not be enough

• Capital based on information verified by supervisors*– Verification of accounts and regulatory compliance– Confidence in risks being analysed and measured properly

• Bad loans are hidden among the good ones (bearing hidden losses)– Offsite analysis, external audit, banks’ reporting, mathematical

models, stress tests, RWA evaluation may not prove enough.

• Non-performing loans do not performeven if this affects dividends and bonuses – Performance should be based on borrowers’ repayment capacity

• Unrealistic capital figures is bank mangers’ primary responsibility– And eventually bank supervisors’ too

• Good to focus strongly on capital buffers– As long as this supports preventive measures:

verification, compliance, and risk assessment

11

How could the Basel process better serve EMEs?

12

Time for a Break!

13

BASELWORK IN PROGRESS

14

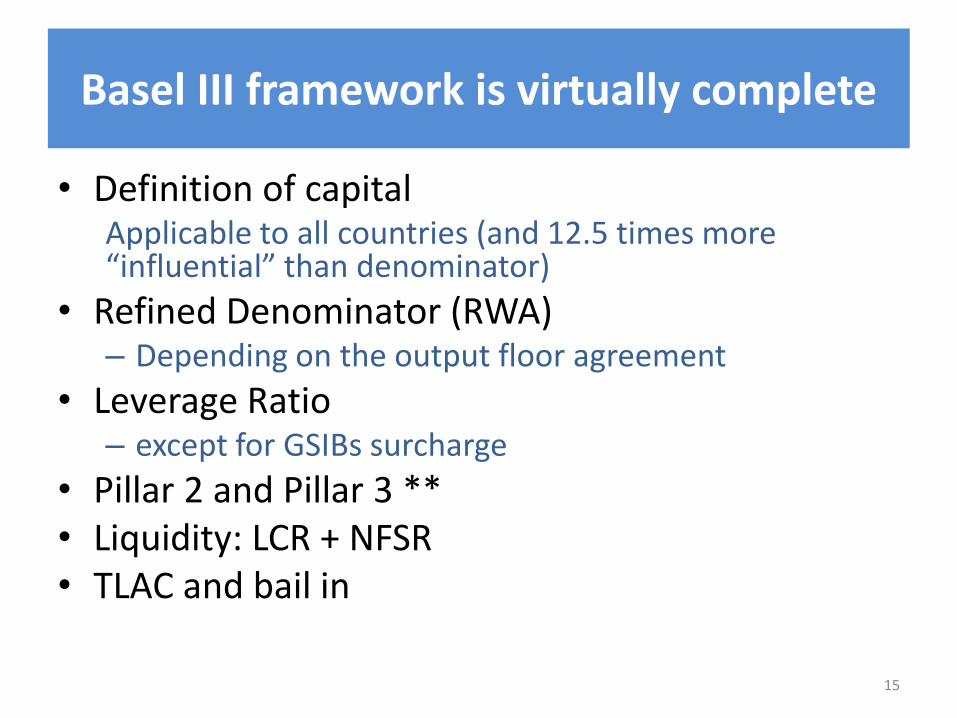

Basel III framework is virtually complete

• Definition of capitalApplicable to all countries (and 12.5 times more “influential” than denominator)

• Refined Denominator (RWA)– Depending on the output floor agreement

• Leverage Ratio– except for GSIBs surcharge

• Pillar 2 and Pillar 3 **• Liquidity: LCR + NFSR• TLAC and bail in

15

FIRB

AIRB

Internal Models

Cred. Standardized

IMM

BIA

TSA / ASAAMA

Finalizing Basel III

• More risk-sensitive

standardized approaches

(SA)

• Constraints in the use of

internal models

• Output floors as backstop

relative to the SA; o Final design and calibration

pending: current suggestions

in the range of 70-75%

• Agreement difficult to reach

Pillar I

Charges

Credit

Risk

Market

Risk

Operational

Risk

Market Standardized

Internal

ModelsStandardized

9

Basel III Phase-in arrangements

17See Basel III Monitoring Report, February 2017, www.bis.org/bcbs/publ/d397.pdf

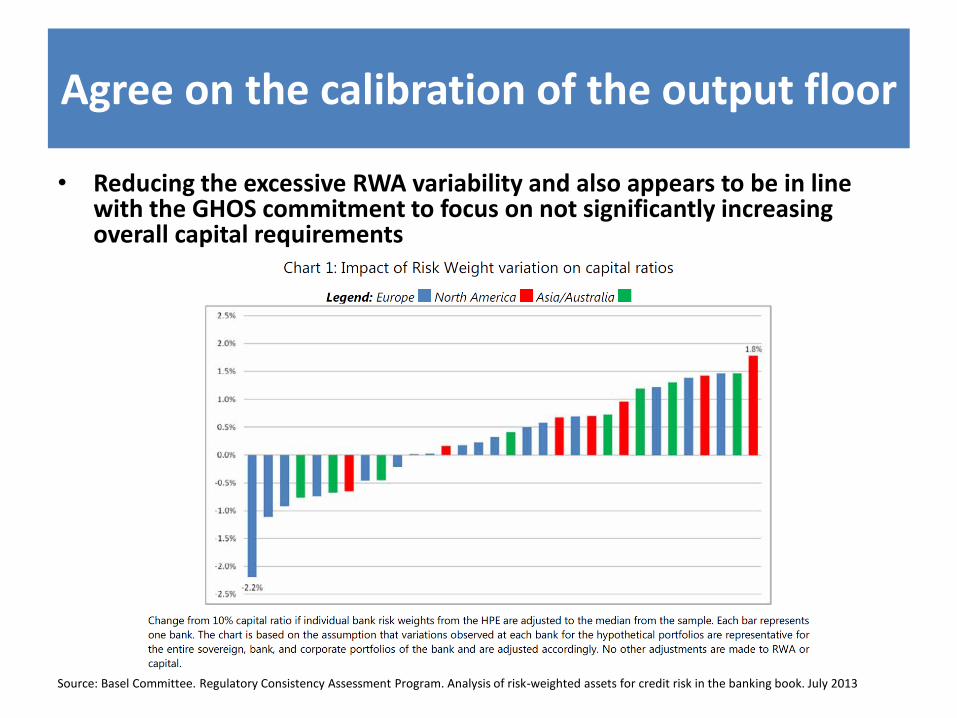

Agree on the calibration of the output floor

• Reducing the excessive RWA variability and also appears to be in line with the GHOS commitment to focus on not significantly increasing overall capital requirements

Source: Basel Committee. Regulatory Consistency Assessment Program. Analysis of risk-weighted assets for credit risk in the banking book. July 2013

Banks constrained by different capital metrics (percentage)

19

100% Capital requirements

Standardized Models

Floor: 70 -75%

Additional capital

Basel Committee moving forward

STANDARDSJun 2017--Simplified alternative to the standardized approach to market risk capital requirements ------ consultative documentMar 2017--Regulatory treatment of accounting provisions - interim approach and transitional arrangementsMar 2017--Pillar 3 disclosure requirements - consolidated and enhanced frameworkOct 2016--TLAC holdings standardJul 2016--Revisions to the securitization frameworkApr 2016--Interest rate risk in the banking bookApr 2016--Revisions to the Basel III leverage ratio framework - ---------------------------------------------------------consultative documentMar 2016--Standardised Measurement Approach for operational risk -------------------------------------------- consultative documentOct 2014--Basel III: the net stable funding ratioApr 2014--Supervisory framework for measuring and controlling large exposuresApr 2014--Capital requirements for bank exposures to central counterpartiesJan 2014--Liquidity coverage ratio disclosure standardsJan 2014--Basel III leverage ratio framework and disclosure requirementsJan 2013-- Basel III: The Liquidity Coverage Ratio and liquidity risk monitoring toolsOct 2012--A framework for dealing with domestic systemically important banksSep 2012--Principles for the supervision of financial conglomeratesSep 2012--Core principles for effective banking supervisionDec 2010--Basel III: A global regulatory framework for more resilient banks and banking systems - revised version June 2011Jun 2009--Core Principles for Effective Deposit Insurance Systems

20

GUIDELINESOct 2017--Identification and management of step-in riskJul 2017--Criteria for identifying simple, transparent and comparable short-term securitisations - consultative documentJun 2017--Sound management of risks related to money laundering and financing of terrorism: revisions to correspondent banking annexApr 2017-- Prudential treatment of problem assets - definitions of non-performing exposures and forbearanceSep 2016--Guidance on the application of the Core Principles for Effective Banking Supervision to the regulation and supervision of institutions relevant to financial inclusionDec 2015--Guidance on credit risk and accounting for expected credit lossesJul 2015--Guidelines for identifying and dealing with weak banksJul 2015--Corporate governance principles for banksJun 2014--Principles for effective supervisory collegesMar 2014--External audits of banksJan 2014--Sound management of risks related to money laundering and financing of terrorismJan 2013--Principles for effective risk data aggregation and risk reportingJun 2012--The internal audit function in banks Jun 2012--Composition of capital disclosure requirements - Rules textDec 2010--Guidance for national authorities operating the countercyclical capital bufferAug 2010--Microfinance activities and the Core Principles for Effective Banking Supervision - final documentMar 2010--Report and recommendations of the Cross-border Bank Resolution GroupSep 2008--Principles for Sound Liquidity Risk Management and Supervision

What are the Committee’s main concerns?

• Impact of individual standards

– Including Basel III

• Consistent Implementation by all members

• Effective and forward-looking supervision

• Timely corrective actions

• Bank resolution at the lowest fiscal cost

21

What are the implementation challenges faced by your organization?

22