renault group q3 2015 jérôme stoll dominique thormann

TRANSCRIPT

RENAULT GROUP

Q1 2016THIERRY KOSKAS

DOMINIQUE THORMANN

2

INVESTOR RELATIONS

RENAULT Q1 2016 PRESENTATION APRIL 21, 2016 PROPERTY OF GROUPE RENAULT

Information contained within this document may contain forward looking statements.

Although the Company considers that such information and statements are based on

reasonable assumptions taken on the date of this report, due to their nature, they can be

risky and uncertain (as described in the Renault documentation registered within the French

financial markets regulation authorities) and can lead to a difference between the exact

figures and those given or deduced from said information and statements.

Renault does not undertake to provide updates or revisions, should any new statements and

information be available, should any new specific events occur or for any other reason.

Renault makes no representation, declaration or warranty as regards the accuracy,

sufficiency, adequacy, effectiveness and genuineness of any statements and information

contained in this report.

Further information on Renault can be found on Renault’s web site (www.group.renault.com),

in the section Finance / Regulated Information.

DISCLAIMER

3

INVESTOR RELATIONS

RENAULT Q1 2016 PRESENTATION APRIL 21, 2016 PROPERTY OF GROUPE RENAULT

01Q1 2016 COMMERCIAL RESULTS UPDATETHIERRY KOSKASEVP, SALES & MAKETING

02Q1 2016 REVENUES & OUTLOOKDOMINIQUE THORMANNEVP & CFO

03 QUESTIONS & ANSWERS

AGENDA

4

INVESTOR RELATIONS

RENAULT Q1 2016 PRESENTATION APRIL 21, 2016 PROPERTY OF GROUPE RENAULT

STRONG EUROPEAN MARKET

MIXED SITUATION IN EMERGING MARKETS

SUCCESS OF OUR NEW PRODUCTS

STRONG FOREX HEADWIND

FY GUIDANCE CONFIRMED

KEY TAKE-AWAYS FROM Q1 RESULTS

5

INVESTOR RELATIONS

RENAULT Q1 2016 PRESENTATION APRIL 21, 2016 PROPERTY OF GROUPE RENAULT

Q1 2016 COMMERCIAL RESULTS UPDATETHIERRY KOSKASEVP, SALES & MARKETING

01

6

INVESTOR RELATIONS

RENAULT Q1 2016 PRESENTATION APRIL 21, 2016 PROPERTY OF GROUPE RENAULT

* PC+LCV including USA & Canada

TIV EVOLUTION Q1 2016 VS Q1 2015

RUSSIA -16.9%

TURKEY -2.7%

ALGERIA -54.4%

MOROCCO +17.5%

INDIA +3.3%

BRAZIL -28.3%

ARGENTINA +1.6%

COLOMBIA -16.3%

WORLD*

TIV +1.5%

EURASIA

TIV -12.4%

AFRICA-ME-INDIA

TIV -7.8%

AMERICAS

TIV -11.5%

ASIA-PACIFIC

TIV +2.8%

EUROPE

TIV +8.2%

FRANCE +8.4%

GERMANY +4.8%

UK +4.5%

SPAIN +7.1%

ITALY +21.1%

CHINA +5.9%

SOUTH KOREA +5.2%

7

INVESTOR RELATIONS

RENAULT Q1 2016 PRESENTATION APRIL 21, 2016 PROPERTY OF GROUPE RENAULT

646

399

69 70 8028

692

434

6795

7225

Q1'15 Q1'16 Q1'15 Q1'16 Q1'15 Q1'16 Q1'15 Q1'16 Q1'15 Q1'16 Q1'15 Q1'16

GLOBAL

+7.3%

EUROPE

+8.9%

AMERICAS

-11.1%

ASIA-PACIFIC

-11.5%

AFRICA-ME-INDIA

+36.1%

EURASIA

-2.0%

INTERNATIONAL +4.7%

K units

(PC+LCV)

+1.5% TIV +8.2% -12.4% -7.8% -11.5% +2.8%

GROUP

WORLD MARKET SHARE: 3.1% (+0.2 pts)

RENAULT GROUP UNIT REGISTRATIONS Q1 2016 VS Q1 2015

8

INVESTOR RELATIONS

RENAULT Q1 2016 PRESENTATION APRIL 21, 2016 PROPERTY OF GROUPE RENAULT

FRANCE01

ITALY02

03

INDIA

UK04

BELGIUM+LUX

05

06

07

08

09

BRAZIL

26.5 %

4.7 %

9.2 %

4.4 %

GERMANY

3.6 %

6.9 %

RUSSIA 7.3 %

11.7 %

TURKEY 17.5 %

Market share

(PC+LCV)

+0.1 pts

-1.5 pts

+0.2 pts

+0.1 pts

vs.

Q1 2015

SPAIN 10.4 %

+0.3 pts

+0.1 pts

+1,5 pts36% 42%48%

55% 52%48%

Q1 2010 Q1 2011 Q1 2012 Q1 2013 Q1 2014 Q1 2015 Q1 2016

31% 37% 49% 44% 38%45%

+0.1 pts

+2,3 pts

-0,6 pts

37%

INTERNATIONALEUROPE

69% 63% 51% 56% 62%55% 63%

REGIONAL SALES BREAKDOWN

EUROPE KEEPS PUSHING SALES MOMENTUM

10

TOP 10 MARKETS BY VOLUME

9

INVESTOR RELATIONS

RENAULT Q1 2016 PRESENTATION APRIL 21, 2016 PROPERTY OF GROUPE RENAULT

EUROPE REGIONGROUP PC+LCV : BREAKDOWN OF REGISTRATIONS

399434

Q1 2015 TIV PERF Q1 2016

-1

TIV

& MARKET MIX

PERFORMANCE+36

GROUP ORDER BOOK PC + LCV

Q1’15Q1’16

K units

(PC+LCV)

GROUP MARKET SHARE PC+LCV

Europe 9.8%

+0.1 pts

France 26.5%

+0.1 pts

10

INVESTOR RELATIONS

RENAULT Q1 2016 PRESENTATION APRIL 21, 2016 PROPERTY OF GROUPE RENAULT

69 67

Q1 2015 TIV PERF Q1 2016

EURASIA REGION

RENAULT KADJAR

-4

GROUP PC+LCV : BREAKDOWN OF REGISTRATIONS

+3

GROUP MARKET SHARE PC+LCV

Eurasia 11.9%

+1.3 pts

Turkey 17.5%

+1.5 pts

PERFORMANCETIV

& MARKET MIX

+3-5Q1’15 Q1’16

K units

(PC+LCV)

11

INVESTOR RELATIONS

RENAULT Q1 2016 PRESENTATION APRIL 21, 2016 PROPERTY OF GROUPE RENAULT

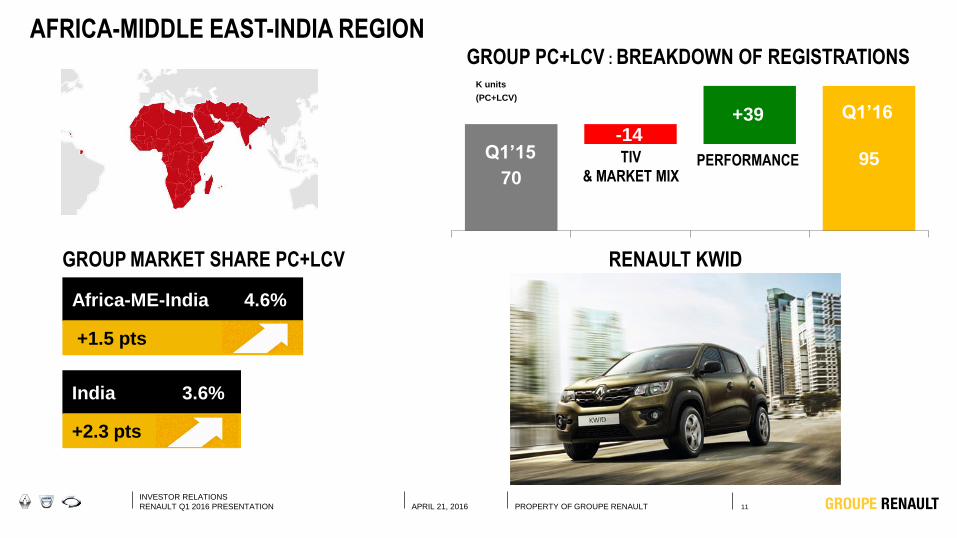

AFRICA-MIDDLE EAST-INDIA REGION

GROUP MARKET SHARE PC+LCV

Africa-ME-India 4.6%

+1.5 pts

India 3.6%

+2.3 pts

GROUP PC+LCV : BREAKDOWN OF REGISTRATIONS

7095

Q1 2015 TIV PERF Q1 2016

+39-14

Q1’15

Q1’16

PERFORMANCETIV

& MARKET MIX

RENAULT KWID

K units

(PC+LCV)

12

INVESTOR RELATIONS

RENAULT Q1 2016 PRESENTATION APRIL 21, 2016 PROPERTY OF GROUPE RENAULT

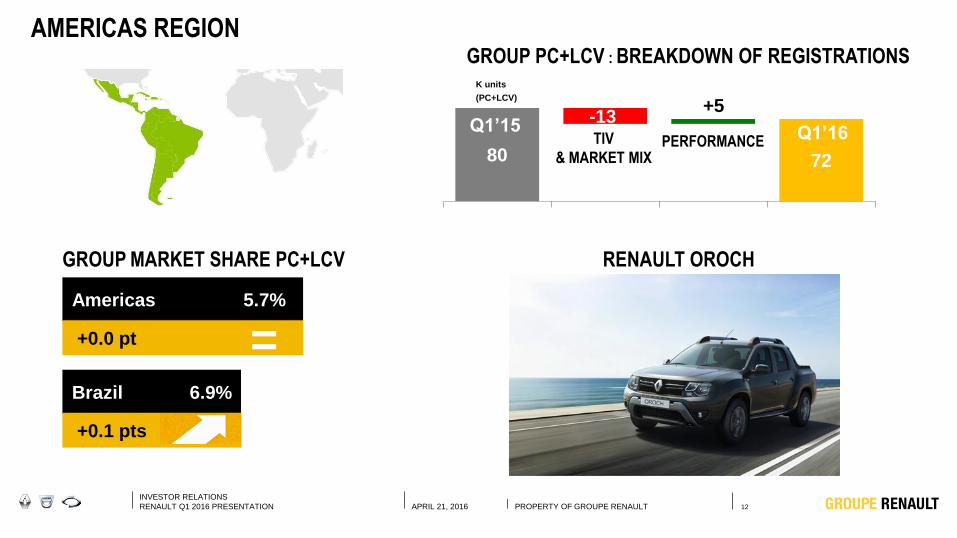

AMERICAS REGION

GROUP MARKET SHARE PC+LCV

Americas 5.7%

+0.0 pt

Brazil 6.9%

+0.1 pts

RENAULT OROCH

-17

GROUP PC+LCV : BREAKDOWN OF REGISTRATIONS

=

80 72

Q1 2015 TIV PERF Q1 2016

+5

PERFORMANCETIV

& MARKET MIX

-13Q1’15 Q1’16

K units

(PC+LCV)

13

INVESTOR RELATIONS

RENAULT Q1 2016 PRESENTATION APRIL 21, 2016 PROPERTY OF GROUPE RENAULT

ASIA-PACIFIC REGION

GROUP MARKET SHARE PC+LCV

Asia-Pacific 0.3%

South Korea 4.0%

-0.3 pts

0.0 pt

RENAULT SAMSUNG SM6

=

3027

Q3’14Q3’15

-5+2

GROUP PC+LCV : BREAKDOWN OF REGISTRATIONS*

28 25

Q1 2015 TIV PERF Q1 2016

TIV

& MARKET MIX PERFORMANCE

+1

-4Q1’15Q1’16

* Restatement on 2015 & 2016 Chinese sales: reported on retail sales basis versus wholesales previously

K units

(PC+LCV)

14

INVESTOR RELATIONS

RENAULT Q1 2016 PRESENTATION APRIL 21, 2016 PROPERTY OF GROUPE RENAULT

NEW MODELS ON THE RIGHT TRACK

* RV : Residual Value

KADJAR

Registrations Q1: 35,358

KWID

Registrations Q1: 23,288

NEW ESPACE

Registrations Q1: 7,735

RV* France: +18 pts vs

Espace IV

NEW MEGANE

Registrations Q1: 13,587

RV France: +9.3 pts vs

Mégane III

TALISMAN

Registrations Q1: 5,007

RV France: +13.5 pts vs

Laguna

DUSTER OROCH

Registrations Q1: 3,191

15

INVESTOR RELATIONS

RENAULT Q1 2016 PRESENTATION APRIL 21, 2016 PROPERTY OF GROUPE RENAULT

Q1 2016 REVENUES & OUTLOOKDOMINIQUE THORMANNEVP & CFO

02

16

INVESTOR RELATIONS

RENAULT Q1 2016 PRESENTATION APRIL 21, 2016 PROPERTY OF GROUPE RENAULT

RENAULT GROUP REVENUES BY DIVISION IN Q1 2016

In million euros Q1 2016 Change (%)Q1 2015

Automotive

Sales Financing

TOTAL

9,942

547

10,489

+12.6%

-2.1%

+11.7%

8,829

559

9,388

17

INVESTOR RELATIONS

RENAULT Q1 2016 PRESENTATION APRIL 21, 2016 PROPERTY OF GROUPE RENAULT

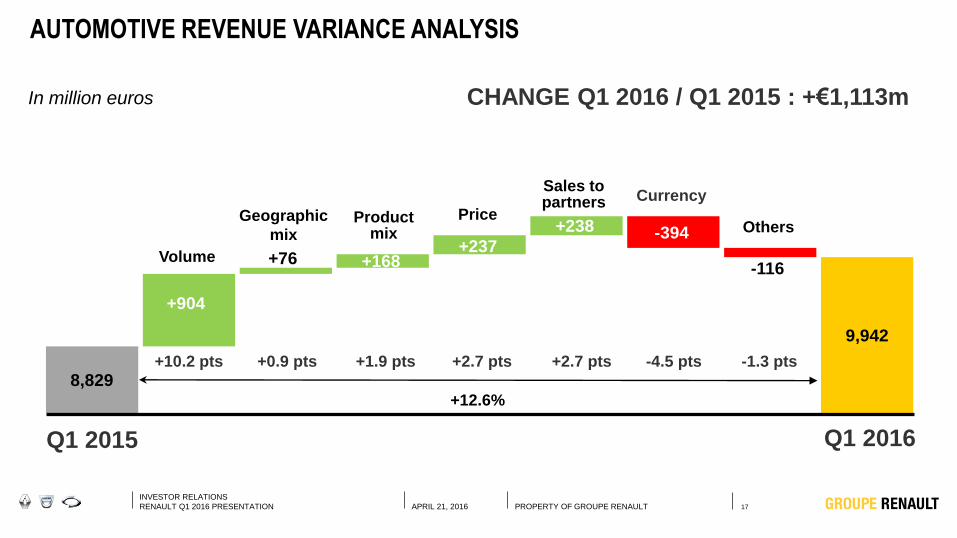

8,829

9,942

-394

+904

+76 +168+237

+238

-116

AUTOMOTIVE REVENUE VARIANCE ANALYSIS

Currency

Volume

Geographic

mixProduct

mix

Price

Sales to partners

Others

+12.6%

-4.5 pts+10.2 pts +0.9 pts +1.9 pts +2.7 pts +2.7 pts -1.3 pts

In million euros CHANGE Q1 2016 / Q1 2015 : +€1,113m

Q1 2015 Q1 2016

18

INVESTOR RELATIONS

RENAULT Q1 2016 PRESENTATION APRIL 21, 2016 PROPERTY OF GROUPE RENAULT

488527

495 493

459

515 511 503465

575

100

255

158

254

106

264

178

260

141

298

388

272

337

240

353

251

333

243

324

277

DEC'13 MAR'14 JUN'14 SEP'14 DEC'14 MAR'15 JUN'15 SEP'15 DEC'15 MAR'16

NEW VEHICLE DISTRIBUTION STOCK (IN K UNITS)

GROUP

INDEPENDENTDEALERS

TOTAL

Number of days of sales

(previous period)757663 62 74 57 74 64 53 76

19

INVESTOR RELATIONS

RENAULT Q1 2016 PRESENTATION APRIL 21, 2016 PROPERTY OF GROUPE RENAULT

RCI BANQUE PERFORMANCE

Q1 2016 Change (%)Q1 2015

Revenues (in € m)

Average Performing Assets*(in € bn)

New contracts (in thousand units)

New financings(in € bn)

559

27.6

320

3.7

* Restated to include operating leases since the beginning of 2016, representing :

€ 0.3 bn in Q1 2015 and € 0.5 bn in Q1 2016

547

31.1

353

4.1

-2.1%

+12.8%

+10.2%

+11.3%

20

INVESTOR RELATIONS

RENAULT Q1 2016 PRESENTATION APRIL 21, 2016 PROPERTY OF GROUPE RENAULT

OUTLOOK 2016

In 2016, the global market is expected to grow 2% compared to 2015. The

European market is now expected to increase by at least 5% (vs +2%

previously).

Outside Europe, the Brazilian and Russian markets are expected to decline

further, by 15% to 20% (vs -6% previously) and 12% respectively. On the

contrary, China (+4% to +5%) and India (+8%) should pursue their positive

momentum.

THE GROUP* IS AIMING TO:

Increase group revenues (at constant exchange rates)

Improve group operating margin

Generate a positive Automotive operational free cash flow

* at constant scope of consolidation

21

INVESTOR RELATIONS

RENAULT Q1 2016 PRESENTATION APRIL 21, 2016 PROPERTY OF GROUPE RENAULT

QUESTIONS & ANSWERS03

22

INVESTOR RELATIONS

RENAULT Q1 2016 PRESENTATION APRIL 21, 2016 PROPERTY OF GROUPE RENAULT