redefining the foundry model panel discussion at itac …itac.ca/uploads/pdf/norm_armour.pdf ·...

TRANSCRIPT

Redefining the Foundry Model Panel Discussion at ITAC - GSANorm ArmourVice President and General Manager, Fab 8

Overview

The endless march of technologyIncreasing complexity and cost in manufacturing

An industry in transitionThe shift from regional to global

Creating a sustainable modelCollaboration essential to innovation

The next evolution in the industryFrom contract manufacturing to collaborative manufacturing

April 29, 2010 2GLOBALFOUNDRIES CONFIDENTIAL

2009 Market Volume (No. of end-consumer devices)

130nm180nm+ 90nm 65nm 45nm 32nmProcess linewidth Media Phone

1B

500M

250M

100M

SmartPhone

Voice Only Phone

Personal & portable stereos

MP3 Players

Video game –Handheld & console

Digital Still Cameras

Discrete GPU

IGP Chipset

MPUSet-Top Boxes

Source: Bridge & GLOBALFOUNDRIES analysis, iSuppli Mobile Handset Tracker; iSuppli Consumer Platforms Market Tracker , Mercury Reports GPU, Gartner Reports GPU

April 29, 2010 3GLOBALFOUNDRIES CONFIDENTIAL

CPUs and GPUs still drive transitions, but wireless devices are not far behind

Leading-Edge Technology Adoption

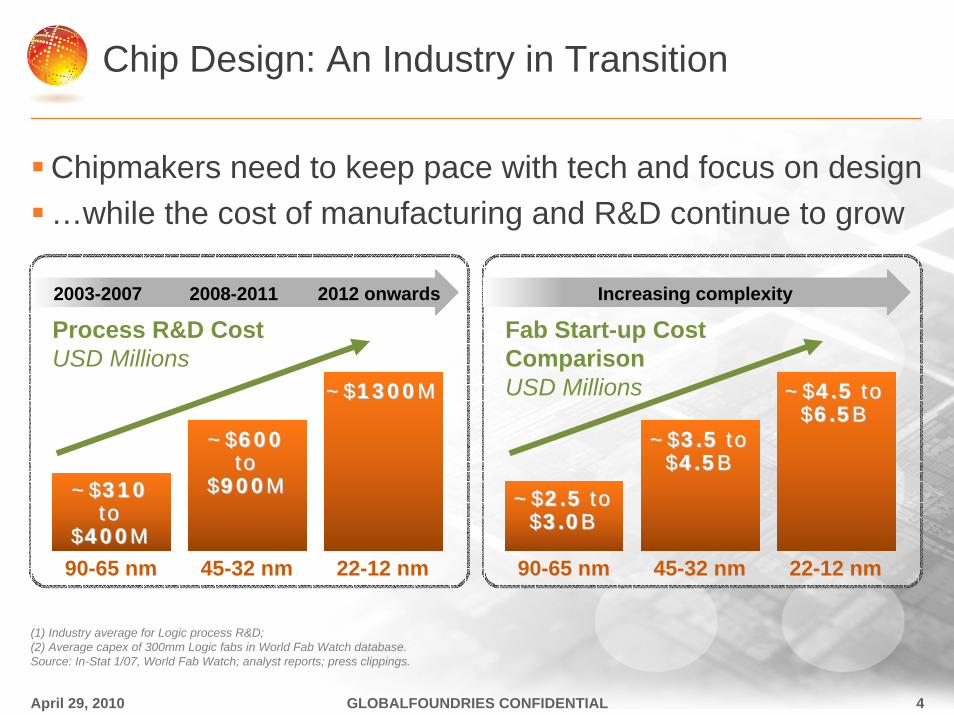

Chip Design: An Industry in Transition

Chipmakers need to keep pace with tech and focus on design…while the cost of manufacturing and R&D continue to grow

(1) Industry average for Logic process R&D; (2) Average capex of 300mm Logic fabs in World Fab Watch database. Source: In-Stat 1/07, World Fab Watch; analyst reports; press clippings.

April 29, 2010 4GLOBALFOUNDRIES CONFIDENTIAL

2003-2007 2008-2011 2012 onwards

Process R&D CostUSD Millions

90-65 nm 45-32 nm 22-12 nm

~$~$310310toto

$$400400MM

~$~$600600toto

$$900900MM

~$~$13001300MM

Increasing complexity

Fab Start-up CostComparisonUSD Millions

90-65 nm 45-32 nm 22-12 nm

~$~$2.5 2.5 toto$$3.03.0BB

~$~$3.5 3.5 toto$$4.54.5BB

~$~$4.5 4.5 toto$$6.56.5BB

The First Truly Global Foundry

East Fishkill, NY

Austin, TX

HeadquartersSi Valley, CA

London, UK

Yokohama,Japan

Shanghai,China

Hsinchu,Taiwan

Munich, Germany

Global Manufacturing and Support Footprint

Manufacturing CentersSaratoga, New York Dresden, Germany SingaporeSales and Support Offices

Dresden, Germany

Singapore

Saratoga, NY

The New GLOBALFOUNDRIES

Headquartered in Silicon ValleyApproximately 10,000 employeesSpanning three continents across 12 locations300mm Fabs in Singapore, Germany, New York200mm Fabs in Singapore

One of the World’s Largest Foundries2009 revenue of ~$2.5B US 150 Customers including many of the world’s largest IC companies

The New Leader in Foundry Technology and Service

Substantial Time-to-volume advantage for advanced technologiesDriving the Global Standard for new technologiesFull foundry offering from mainstream to leading edge with Value-Added SolutionsCommitted to Best-in-Class customer service

Germany

Singapore

New York

State-of-the-Art 300mm Fabs

Global foundry capacity expansion minimizes geographic risk

Fab 1 in Germany Fab 7 in Singapore Fab 8 in New York

• 45nm and below • 130nm to 40nm • 28nm and below

• 300mm wafers• 60,000 wafers/month

• 300mm wafers• 50,000 wafers/month

• 300mm wafers• 42,000 wafers/month

• Production Now • Production Now •Groundbreaking July 2009• Production ramping 2012

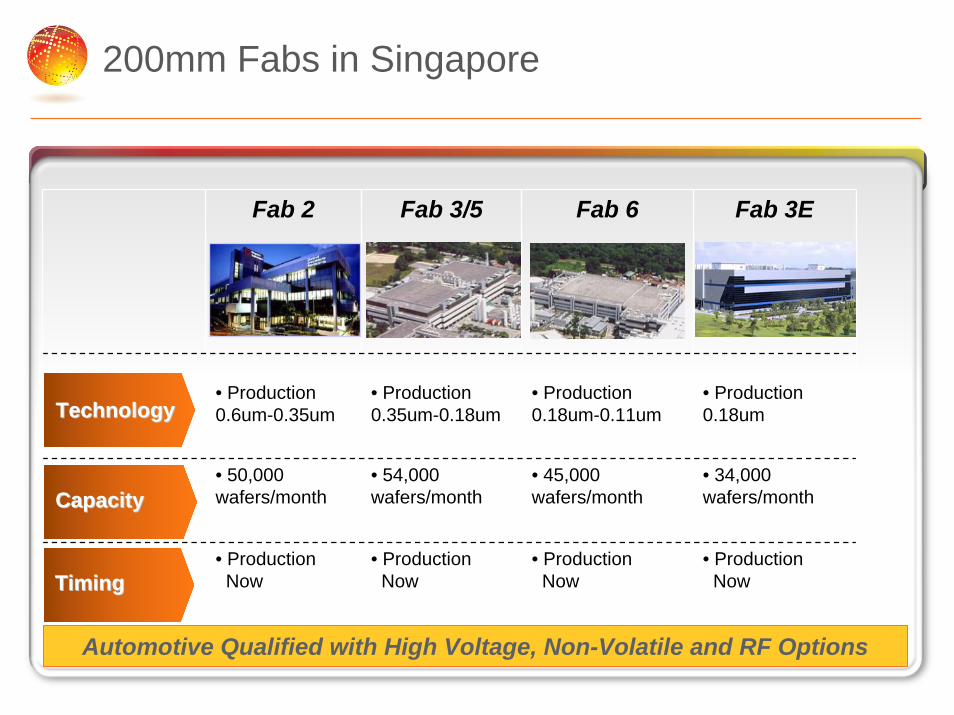

200mm Fabs in Singapore

Fab 2 Fab 3/5 Fab 6 Fab 3E

• Production 0.6um-0.35um

• Production 0.35um-0.18um

• Production 0.18um-0.11um

• Production 0.18um

• 50,000 wafers/month

• 54,000 wafers/month

• 45,000 wafers/month

• 34,000 wafers/month

• Production Now

• Production Now

• Production Now

• Production Now

TechnologyTechnology

CapacityCapacity

Timing Timing

Automotive Qualified with High Voltage, Non-Volatile and RF Options

Shared objectivesEarly-stage leading-edge R&DProduction-ready process technologies

Shared investmentsAdvanced manufacturing resourcesDiverse teams collaborating

Face-to-face and virtual

Shared returnsAccelerated access to advanced technologiesExperience from early, high-volume production to refine processes

Rich partner/IP eco-system to support leading-edge adoption

A Model for Shared Innovation

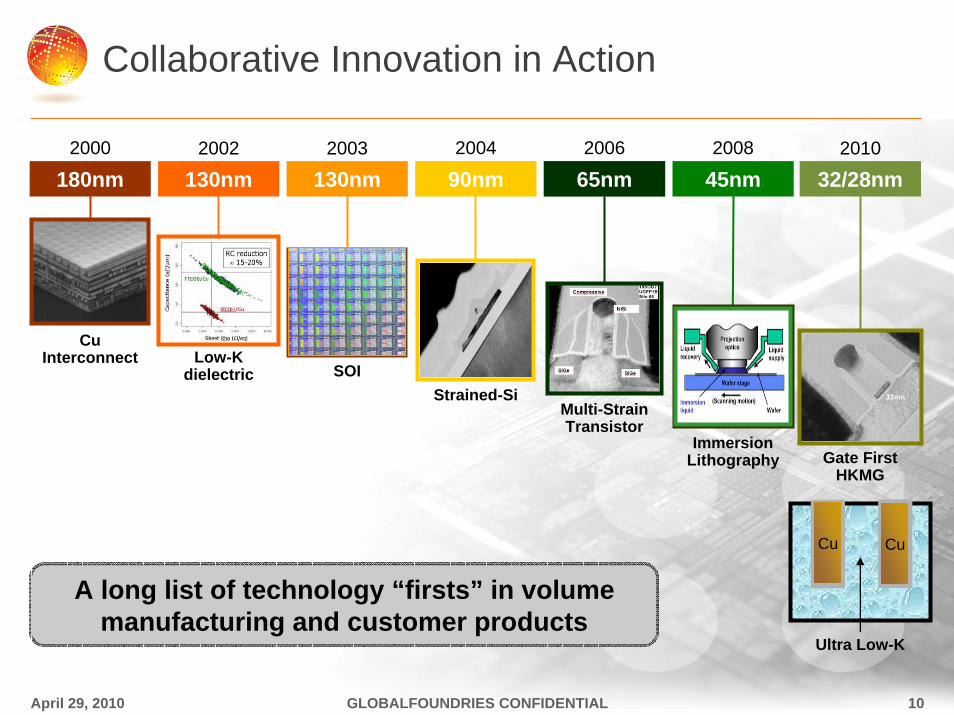

130nm2003

SOI

45nm2008

ImmersionLithography

180nm2000

CuInterconnect

90nm2004

Strained-Si

130nm2002

Low-Kdielectric

65nm2006

Multi-StrainTransistor

65nm 32/28nm

Gate First HKMG

2010

CuCu

Ultra Low-K

Collaborative Innovation in Action

April 29, 2010 10GLOBALFOUNDRIES CONFIDENTIAL

A long list of technology “firsts” in volumemanufacturing and customer products

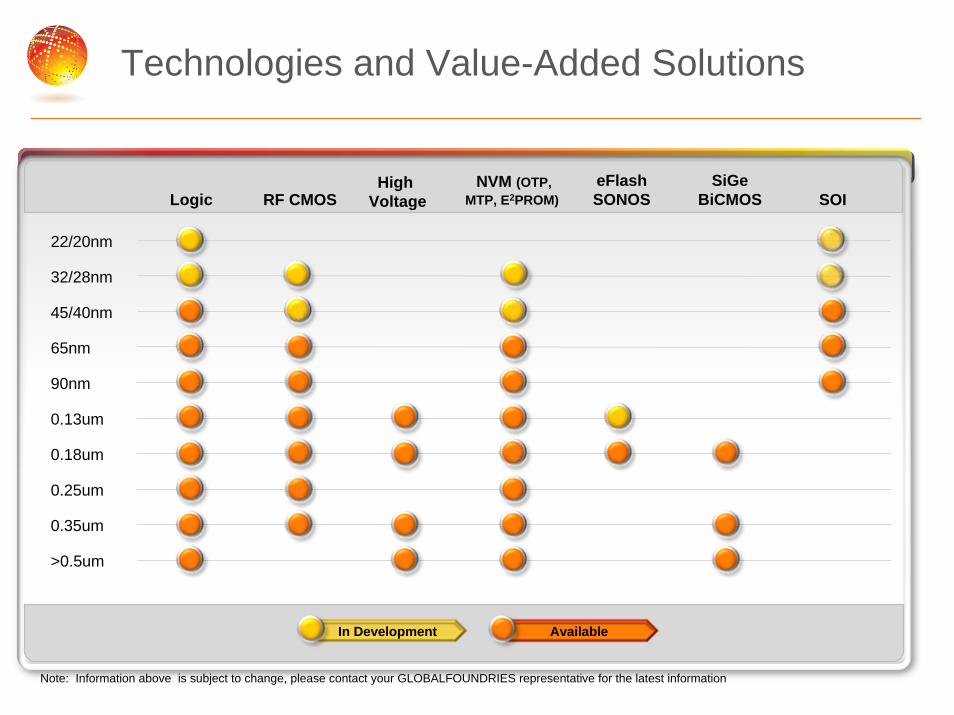

Technologies and Value-Added Solutions

Note: Information above is subject to change, please contact your GLOBALFOUNDRIES representative for the latest information

RF CMOSNVM (OTP,

MTP, E2PROM)eFlashSONOS SOI

22/20nm

32/28nm

45/40nm

65nm

90nm

0.13um

0.18um

0.25um

0.35um

>0.5um

SiGeBiCMOSLogic

High Voltage

In Development Available

Enabling Time-to-Market Leadership

As complexity of chip design increases, manufacturing partnerships become ever more critical

Closely collaborative foundry relationships are essential to enabling smooth and rapid time to market

GLOBALFOUNDRIES’ time-to-volume is unmatched in the foundry industry

– 45nm ramp far ahead of rest of foundry industry

– High-volume, complex x86 CPU drives yield learning for other customers

– Initial 32nm HKMG production running now in Fab 1

GLOBALFOUNDRIES CONFIDENTIALApril 29, 2010

45/40nm Production Ramp300mm Wafers Shipped per Quarter (1000’s)

40nm - Other Leading

Foundries*

45nm

12

*Market data compiled by International Business Strategies

Continued Innovation Demands a New Approach

Design and manufacturing must work in unisonBringing a highly integrated model to foundry

Extension of customer operationsEarly customer-foundry engagementClose collaboration, joint technology development

Enable faster time to marketSmooth ramps to mature yieldsSpeed, accuracy, and agility

Requires committed investmentTechnology, capacity, capabilitiesEnable global scale and service

Design, technology and manufacturing tightly coupled for success of customer solutions

April 29, 2010 13GLOBALFOUNDRIES CONFIDENTIAL

Fab 8, Moduel 1

Fab 8: March 2010

Fab 8: March 2010

Fab8 m1 (Ph1)(210k sqft)

Fab8 m1(Ph2)(90k sqft)

Campus222.45 acres

Fab8

mod

ule2

Fab8 module3

Module 1 currently under construction. There is room on the campus to build Modules 2 & 3, but thosephases are not yet planned.

Fab 8: possible campus build out design

Thank You!

GLOBALFOUNDRIES, the GLOBALFOUNDRIES logo and combinations thereof are trademarks of GLOBALFOUNDRIES Inc. in the United States and/or other jurisdictions. Other names used in this presentation are for identification purposes only and may be trademarks of their respective owners.

©2010 GLOBALFOUNDRIES Inc. All rights reserved.

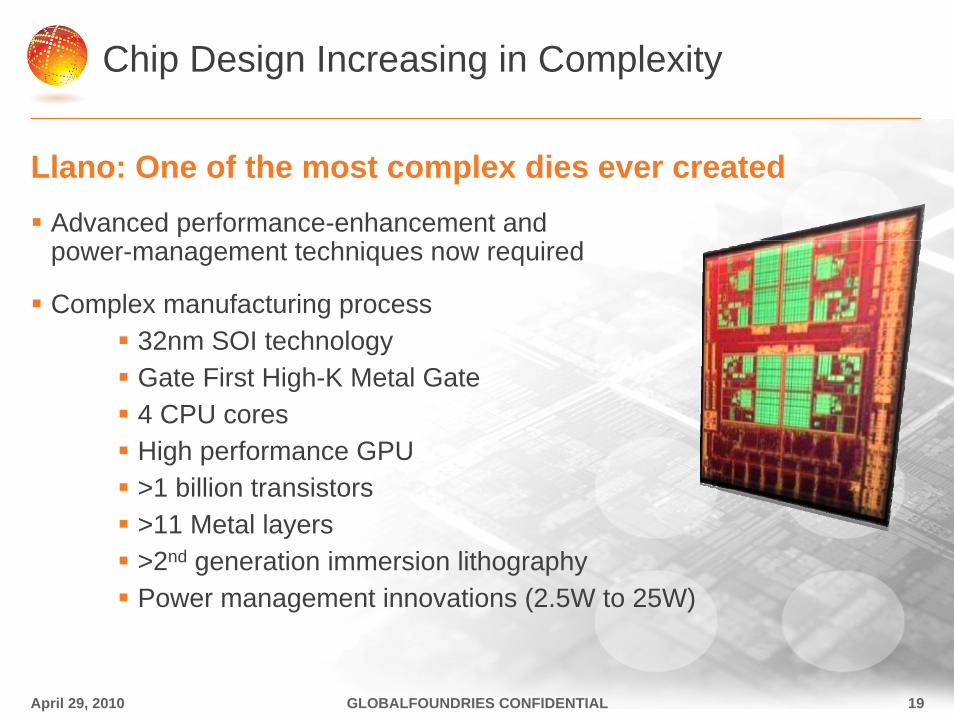

Chip Design Increasing in Complexity

Llano: One of the most complex dies ever createdAdvanced performance-enhancement and power-management techniques now required

Complex manufacturing process32nm SOI technologyGate First High-K Metal Gate4 CPU coresHigh performance GPU >1 billion transistors>11 Metal layers>2nd generation immersion lithographyPower management innovations (2.5W to 25W)

April 29, 2010 19GLOBALFOUNDRIES CONFIDENTIAL

Continuous Innovation Required

Innovation in thinkingPerformance-per-watt, battery life, parallel computing, virtualization, visual computing, small form factor

Innovation in designMultiple cores, CPU/GPU integration, embedded memory, power management, system-level architecture

Innovation in manufacturing and technologyNew materials, transistor structures, 3D stacking, immersion/EUV lithography, ultra-low k dielectrics, High-k Metal Gate

April 29, 2010 20GLOBALFOUNDRIES CONFIDENTIAL

Despite technical challenges, biggest hurdle to continued innovation is economics

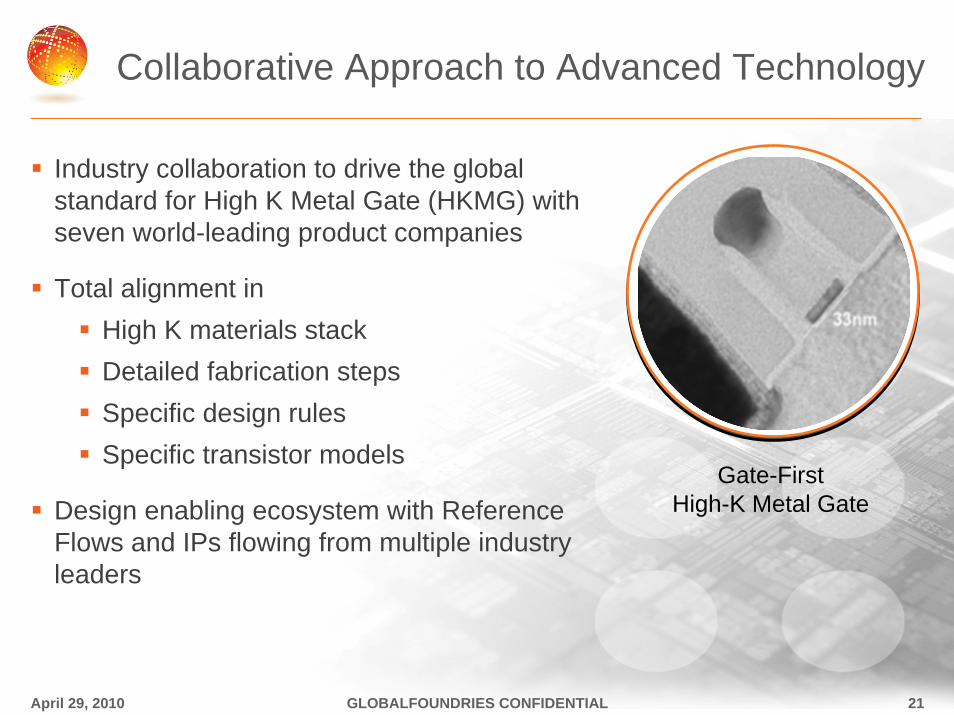

Collaborative Approach to Advanced Technology

Industry collaboration to drive the global standard for High K Metal Gate (HKMG) with seven world-leading product companies

Total alignment in High K materials stackDetailed fabrication steps Specific design rulesSpecific transistor models

Design enabling ecosystem with Reference Flows and IPs flowing from multiple industry leaders

Gate-First High-K Metal Gate

April 29, 2010 21GLOBALFOUNDRIES CONFIDENTIAL

The World’s First Truly Global Foundry

Fab 8Future leading-edge

300mm manufacturingSaratoga County, NY

Fab 1Leading-edge 300mm manufacturing campus

Dresden, Germany

Fab 2, 3, 3e, 5, 6Mainstream 200mm manufacturing

campusWoodlands, SingaporeTampines, Singapore

Fab 7Mainstream 300mm

manufacturing campusWoodlands, Singapore

Global Manufacturing Operations

Fab 8

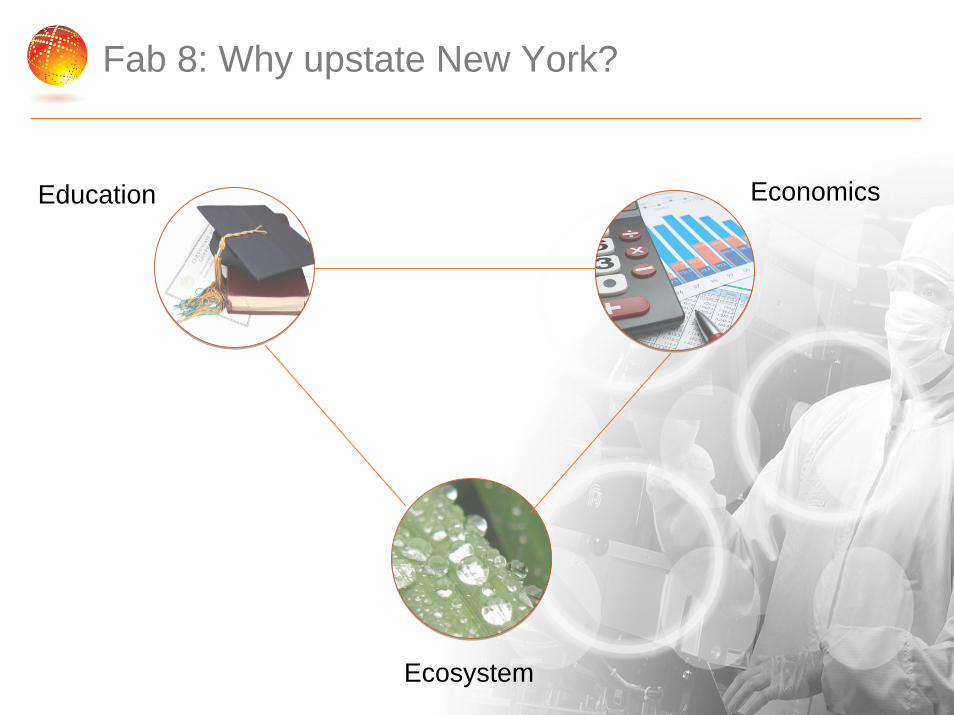

Fab 8: Why upstate New York?

Education Economics

Ecosystem

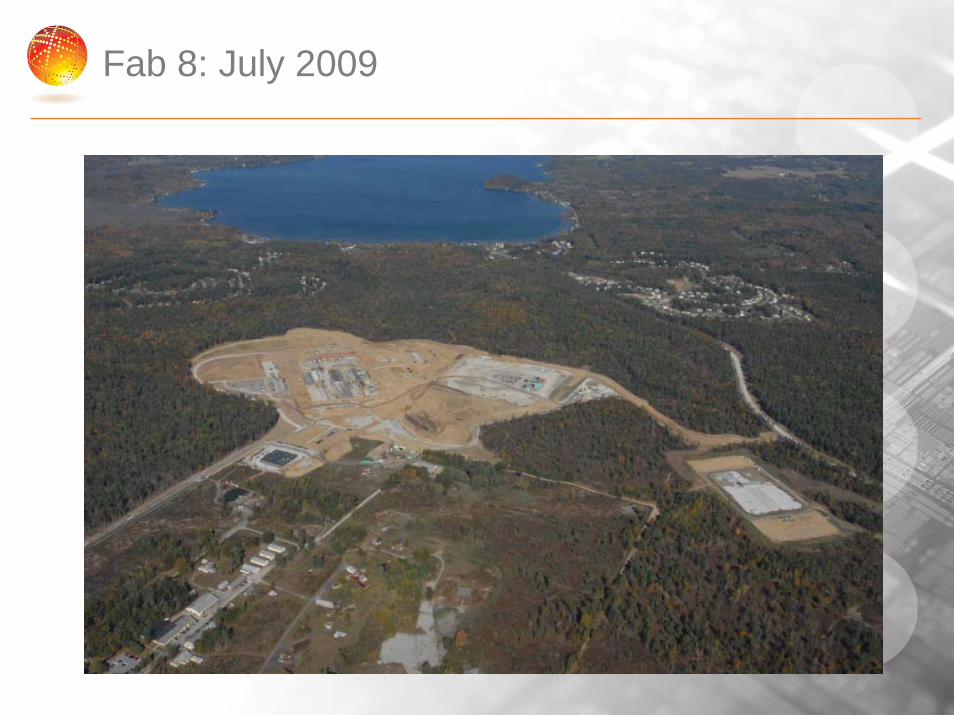

Fab 8: July 2009

Fab 8: December 2009

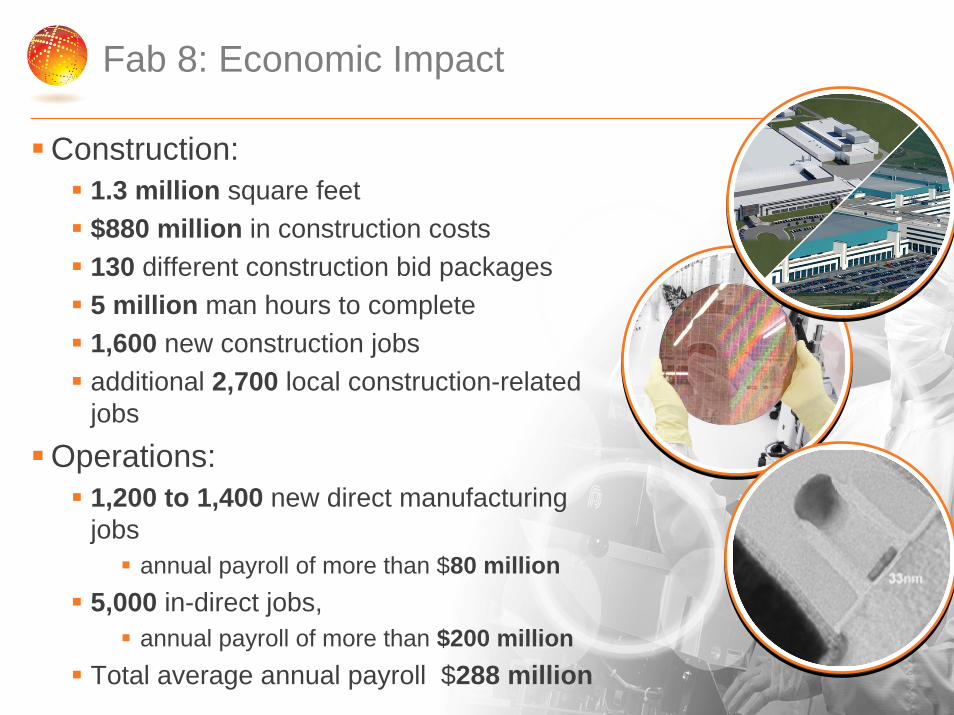

Fab 8: Economic Impact

Construction:1.3 million square feet$880 million in construction costs130 different construction bid packages5 million man hours to complete1,600 new construction jobsadditional 2,700 local construction-related jobs

Operations:1,200 to 1,400 new direct manufacturing jobs

annual payroll of more than $80 million 5,000 in-direct jobs,

annual payroll of more than $200 millionTotal average annual payroll $288 million

Fab 8: concrete foundation

Fab 8: vertical concrete walls

Fab 8: vertical concrete walls

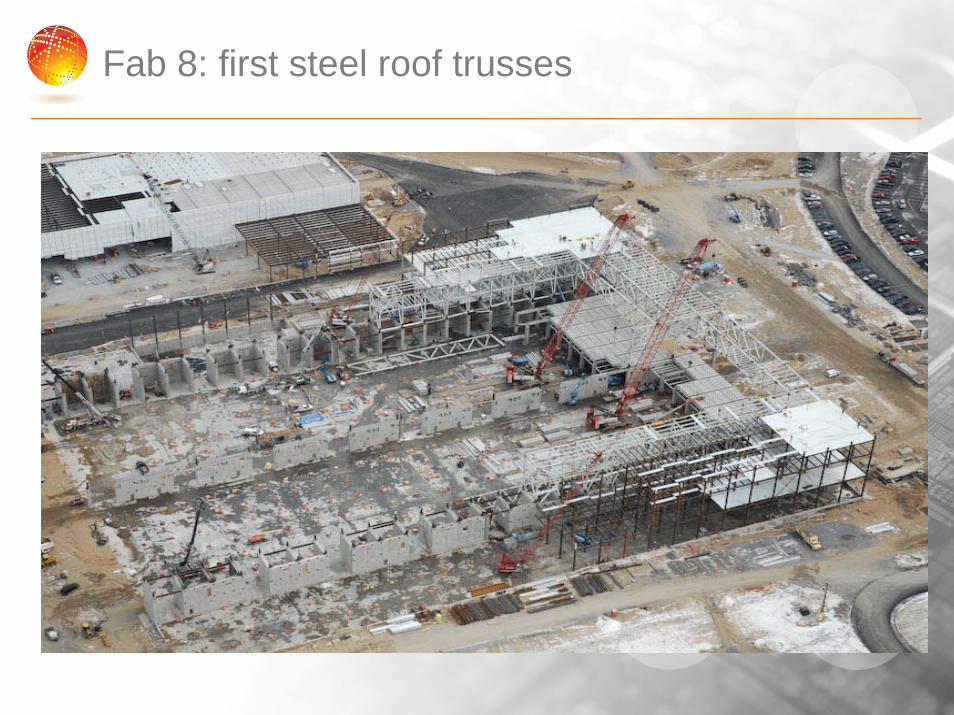

Fab 8: first steel roof trusses

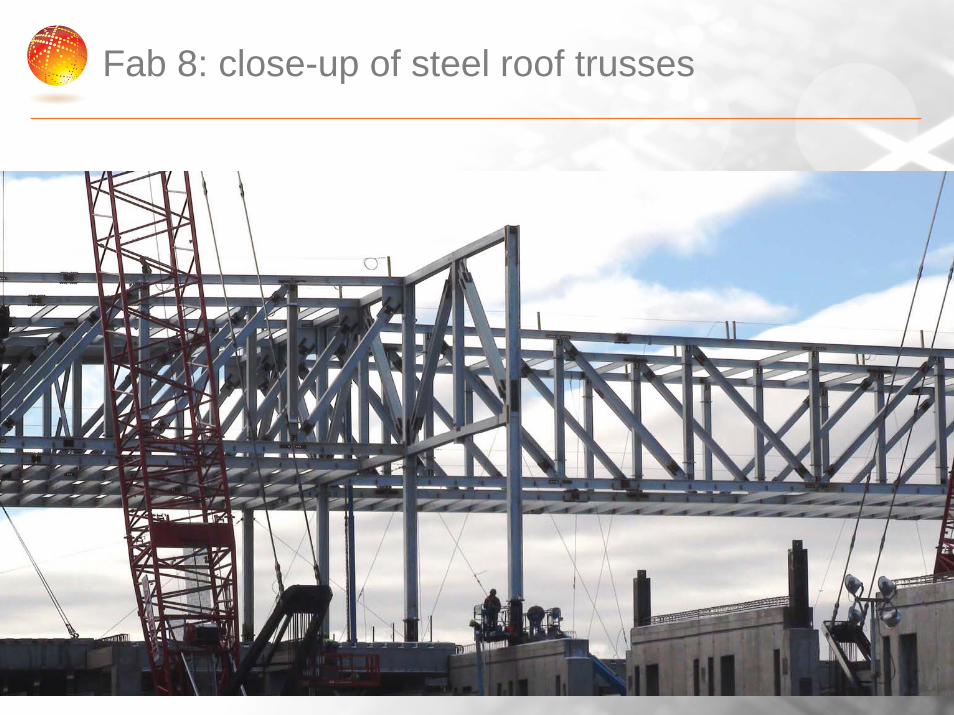

Fab 8: close-up of steel roof trusses

Fab 8: Waffle Table

Fab 8: March 2010

Fab 8: Rendering of Phase 1

Fab 8: potential Phase2 expansion completion - 300k ft-2 (27.9k m-2)

Phase1Phase2

Fab 8: February 2010

Fab 8