pakistan: issues and options in the energy sector · report no. 2953-pak pakistan: issues and...

TRANSCRIPT

Report No. 2953-PAK

Pakistan: Issues and Optionsin the Energy Sector

June 5, 1980

Energy Department

FOR OFFICIAL USE ONLY

Doent of the Wor fan

Thts doumen has a restrted dstrbtion and may be used by repontson In the performame of heir ofci duties Its contents rnay nototherWe be dsdosed wiout World Bank auhorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

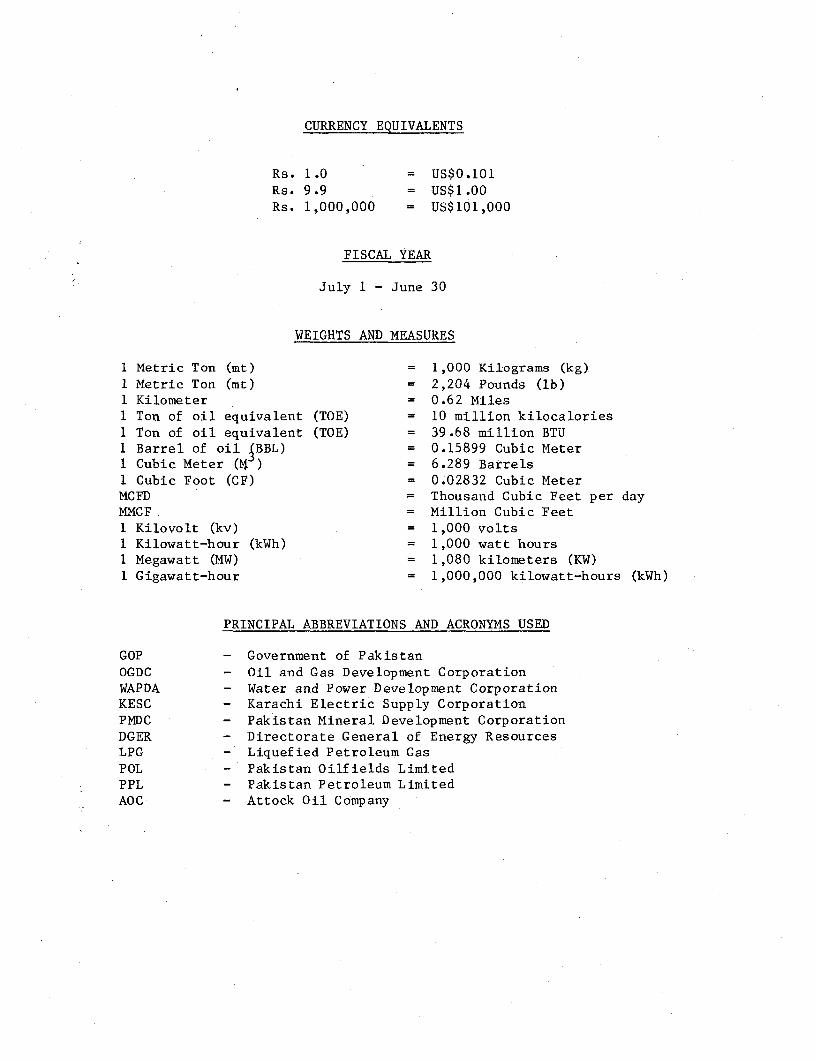

CURRENCY EQUIVALENTS

Rs. 1.0 = US$0.101Rs. 9.9 = US$1.00

Rs. 1,000,000 = US$101,000

FISCAL YEAR

July 1 - June 30

WEIGHTS AND MEASURES

1 Metric Ton (mt) = 1,000 Kilograms (kg)1 Metric Ton (mt) = 2,204 Pounds (lb)1 Kilometer = 0.62 Miles1 Ton of oil equivalent (TOE) = 10 million kilocalories1 Ton of oil equivalent (TOE) = 39.68 million BTU1 Barrel of oil NBBL) = 0.15899 Cubic Meter1 Cubic Meter (1 ) = 6.289 Barrels1 Cubic Foot (CF) = 0.02832 Cubic MeterMCFD = Thousand Cubic Feet per dayMMCF = Million Cubic Feet1 Kilovolt (kv) = 1,000 volts1 Kilowatt-hour (kWh) = 1,000 watt hours1 Megawatt (MW) = 1,080 kilometers (KW)1 Gigawatt-hour = 1,000,000 kilowatt-hours (kWh)

PRINCIPAL ABBREVIATIONS AND ACRONYMS USED

GOP - Government of PakistanOGDC - Oil and Gas Development CorporationWAPDA - Water and Power Development CorporationKESC - Karachi Electric Supply CorporationPNDC - Pakistan Mineral Development CorporationDGER - Directorate General of Energy ResourcesLPG - Liquefied Petroleum GasPOL - Pakistan Oilfields LimitedPPL - Pakistan Petroleum LimitedAOC - Attock Oil Company

PAKISTAN FOR OFFICIAL USE ONLY

ENERGY SECTOR MEMORANDUM

Table of ContentsPige No.

1. SUMMARY AND MAJOR ISSUES ... I.................. 1

Overview * ******* **........... *..................................... 1

Commercial Energy .................. . ....................... 1

Non-Commercial Energy ........ .......................... 5Sector Investment Requirements ............................ 5

Sector Issues ........ .................................... . 6

- Institutional Framework ..... ........................ . 6- Energy Pricing ...... 0....... ..................................... 6

- Other Issues ......................................... 9

2. THE EVOLUTION OF ENERGY DEMAND ............................ 10

Background ................................................... 10

Commercial Energy Consumption ............................. 11

- Consumption of Petroleum Products ... . ................. 13- Consumption of Natural Gas ....... .. .................. 15

- Consumption of Coal ................ .. ................ 15

- Consumption of Electricity ........... . .............. 16

Non-Commercial Energy ..................................... 17

- Firewood ....................................................... 17

- Bagasses .............................................. 18

- Dung Cakes ....... ............... ..................... 18

3. COMMERCIAL ENERGY SUPPLY .................................. 19

Background .... ........................................... .... 19

The Supply of Petroleum Products ........... .. ............. 19

- Crude Oil ............................................ 19

- Refined Products ..................................... 21

The Supply of Natural Gas ................................. 23The Supply of Coal ........................................ 24The Supply of Nuclear Fuels ............................... 25The Supply of Electricity ................................. 26

- Hydro Electricity .................................... 26

- Thermal Electricity . .......... .. ..................... 27- Transmission and Distribution ........................ 28

This report was prepared by Mr. Masood Ahmed, Energy Department. It incor-porates the findings of a series of missions to Pakistan made by staff of

the Energy Department and the South Asia Region during 1979 and 1980. Unlessotherwise stated, the statistics used in this report are based on data fromthe Government of Pakistan's Energy Data Book (1977) and Energy Year Book(1979).L This document has a restricted distribution and may be used by recipients only in the performance

of their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

-2-

Table of Contents (Continued) Page No.

4. ENERGY PRICING, TAXES AND SUBSIDIES ....................... 29

Background ................................................ 29Petroleum Products .................. 29

- Producer Prices ...................................... 29- Ex-refinery Prices ................................... 30- Consumer Prices ...................................... 30- Fiscal Contribution of the Sector .................... 31

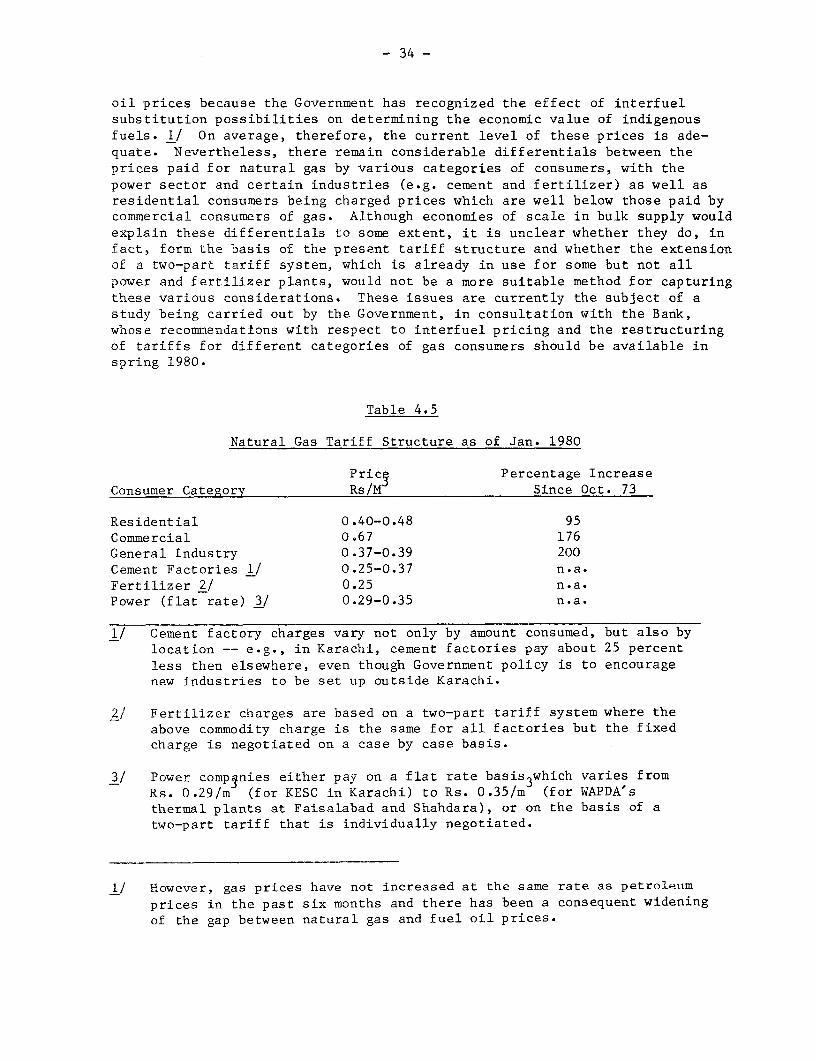

Natural Gas ............................................... 33

- Produder Prices ...................................... 33- Consumer Prices ...................................... 33- Taxes ................................................ 35- Liquid Petroleum Gas ................................. 35

The Power Sector .......................................... 35Coal ...................................................... 38Firewood .................................................. 38

5. ENERGY SECTOR ORGANIZATION AND INSTITUTIONS .... ........... 40

Background ................................................ 40The Hydrocarbons Sector ................................... 40

- Ministry of Petroleum and Natural Resources .... ...... 40- The Oil and Gas Development Corporation .... .......... 41- The Pakistan Mineral Development Corporation .... ..... 41- Other Organizations .................................. 42

The Power Sector ......................................... 42

- Water and Power Development Authority .... ............ 43- Karachi Electric Supply Corporation .................. 43- Others ............................................... 43

The Directorate of Energy Resources (DGER) .... ............ 43Energy Planning ........................................... 44

6. FUTURE DEMAND FOR ENERGY .................................. 45

Overview .................................................. 45The Demand for Petroleum .................................. 45The Demand for Natural Gas ................................ 47The Demand for Coal ....................................... 47Electricity Demand ........................................ 48Firewood .................................................. 49Energy Conservation and Demand Management ................. 49

- 3-

Table of Contents (Continued) Page No.

7. FUTURE ENERGY SUPPLY ...................................... 52

Overview .................................................. 52

Petroleum Supply ....... ............... .................... 53

- Crude Oil ............................................ 53- Refined Products ..................................... 53

Natural Gas Supply ........................................ 54The Supply of Electricity ................................. 54

- Generation Capacity .................................. 54- Transmission and Distribution ........................ 55

Renewable Energy Sources .................................. 56

- Biogas ............................................... 56- Micro-hydro ....... ............. .. .................... 57- Solar Energy ....... ............ .. .................... 57- Other Sources ...... ............. .. ................... 57

The Medium Term Perspective ............................... 58

8. ENERGY SECTOR INVESTMENT REQUIREMENT ...................... 59

The Power Sector .......................................... 59The Oil and Gas Sector .................................... 60

9. POTENTIAL BANK INVOLVEMENT ................................ 63

Previous Bank Group Involvement ........................... 63

Proposed Strategy ....... .................... .............. 64

-4-

ANNEXES

ANNEX I - Commercial Energy Balance FY79

ANNEX II - Glossary of Conversion Units

ANNEX III - Petroleum Sector Legislation and Policy

ANNEX IV - Statistical Tables

Table 4.1 - Oil Reserves as on June 30, 1979Table 4.2 - Production of Crude Oil in Pakistan 1948-79Table 4.3 - Output Mix of Domestic Oil Refineries 1979Table 4.4 - Sectoral Distribution of Petroleum Consumption -

FY65, FY68, FY72-79Table 4.5 - Petroleum Product - Sector Consumption Matrix FY79Table 4.6 - Natural Gas Reserves as on June 30, 1979Table 4.7 - Production of Gas in Pakistan 1955-79Table 4.8 - Sectoral Distribution of Natural Gas Consuwption -

FY65, FY68, FY72-79Table 4.9 - Coal Reserves as on December 31, 1979Table 4.10 - Coal Production in Pakistan 1974-79Table 4.11 - Sectoral Distribution of Coal Consumption 1965-79Table 4.12 - Dam Sites and their Hydro Electric PotentialTable 4.13 - Firm Installed Capacity of Electricity 1948-79Table 4.14 - Installed Electricity Capacity by Plant as on

June 30, 1979Table 4.15 - Electricity Generation By Source, 1948-79Table 4.16 - Sectoral Distribution of Electricity Consumption 1959-79Table 4.17 - Sectoral Distribution of Commercial Energy Consumption

FY65Table 4.18 - Sectoral Distribution of Commercial Energy Consumption

FY72Table 4.19 - Sectoral Distribution of Commercial Energy Consumption

FY79

MAPS

IBRD 13158R2: Pakistan - The Petroleum SectorIBRD 11215R2: Pakistan - Main Power Stations and Principal

Transmission Lines

SUMMARY AND MAJOR ISSUES

Overview

1.01 In 1979, primary commercial energy consumption in Pakistan wasestimated at 11.3 million TOE, implying a per capita consumption levelequivalent to roughly one-tenth the world average and one-half the averagefor all developing countries. Non-commercial energy sources, mainly woodand animal or vegetable wastes, supplied an estimated additional 7.5 to8.5 million TOE, and, although their share in total energy supply has beendeclining over time, firewood remains the largest single source of energyin the country. Within the commercial energy sector, despite progressivesubstitution of petroleum products by natural gas and hydroelectric power,the main indigenous fuels, the share of petroleum in energy supply was still38 percent in 1979. And the absolute consumption of petroleum products hascontinued to grow at a fairly rapid annual rate of 5.0%. As 90 percent ofpetroleum supply is met from imports, the impact of the post-1973 increases ininternational oil prices has been particularly severe on Pakistan's balance ofpayments. The net import bill for oil and oil products has increased from $50million in FY73 to $540 million in FY79 which is equivalent to 45 percent ofthe FY79 current account deficit and a third of the value of all merchandiseexports in that year.

1.02 Further scope for substitution of oil by gas and other indigenousenergy sources is limited, as over half of total oil consumption is in thetransport sector where alternative sources cannot generally be used economi-cally. However, domestic production of oil is expected to more than doubleby 1985 and the prospects for discovering additional recoverable reserves aregood. Consequently, during the next five years, approximately half of theincrease in total petroleum consumption, projected to grow at an averageannual rate of 6 percent, can be expected to be met from increased domesticproduction. In the longer term, a reduction in the import bill, and even aperiod of self-sufficiency in petroleum supply by 1990, are possible outcomesof the recently increased level of exploration activity in the country.

1.03 Realization of this optimistic scenario will, however, require aseries of government actions aimed at strengthening the sector's existinginstitutional framework and at developing the country's energy planningcapability in order to be able to assess the huge and difficult investmentdecisions on hydro-power, nuclear energy, natural gas, coal and oil develop-ment as well as to implement an appropriate longer term energy pricing policy.Substantial foreign assistance will also be required for financing plannedinvestments in the energy sector.

Commercial Energy

1.04 Pakistan's domestic energy resources are characterized by sizablereserves of natural gas, substantial hydro potential, but only limited knownreserves of crude oil, coal, and uranium or other mineral ores which might beused as nuclear fuels. Consequently, even prior to 1973, the main thrust of

- 2 -

government policy had been to increase the share of natural gas and hydropower in meeting the country's energy requirements. Since 1973, this policyhas been pursued with renewed emphasis and the net result has been a progres-sive reduction in the share of total energy supplied by oil and coal and aconcomitant increase in the share of natural gas and hydroelectricity. Inspite of these efforts, oil and oil products remain the largest single commer-cial energy source in the country, accounting for 38 percent of total supplyin 1979, followed closely by natural gas (36%) and hydroelectricity (21%).

1.05 Other than increasing the supply of alternative fuels, the Govern-ment has also reacted to the post-1973 increases in international oil pricesby increasing domestic energy prices and by promoting domestic explorationfor oil. Consumer prices for petroleum products have been raised on severaloccasions since 1973, but this has only been partially successful in curbingdemand, because the-Government has sought to protect certain economic sectorsand lower income groups from the full impact of higher prices and has con-sequently, until very recently, continued to subsidize the consumptionof diesel (used mainly for transport) and kerosene (used for cooking andlighting by low income groups) which together account for nearly 60% oftotal petroleum consumption. This situation has been somewhat altered bythe sharp increase in petroleum product prices announced in December 1979,but relative prices for both refined petroleum products and for other fuelscontinue to exhibit a variety of distortions and their early rectificationis a major issue in the future development of the energy sector.

1.06 As a result of these pricing distortions, and because total energyconsumption in the transport and residential sectors has been growing atrates well above the national average of 7.25% per year since 1972, theconsumption of petroleum products in these sectors has also grown at ratesabove the national average of 5.0% -- in the transport sector at over 10%per year, and in the residential sector at just under 9% a year. Indeed, ithas only been possible to restrain the overall rate of growth of petroleumconsumption to the above figure because of progressive substitution awayfrom oil and largely to gas in the industrial sector and for electricitygeneration where oil consumption has declined in absolute terms at annualrates of 4% and 24%, respectively. However, further possibilities for sub-stitution in these sectors are limited, and their net impact is likely to besmall because their combined share in total petroleum consumption is alreadyless than 6%.

1.07 Recognizing that oil and oil products will continue to play animportant role in supplying the country's energy requirements for the mediumterm and that the historic policy of almost exclusive dependence on importsto meet petroleum supply will become both increasingly expensive and subjectto interruptions of supply due to external conditions, the Government hasincluded as a major element in its energy policy the promotion of domesticoil exploration and production. In 1976, legislation governing privateexploration activity was amended to provide clear-cut incentives for foreigninvestment; the lack of such incentives was a major cause of the inadequateand sporadic nature of domestic oil exploration in the 1960s. The Governmentalso began the process of strengthening the state-owned Oil and Gas Development

- 3 -

Corporation (OGDC) to enable it to act as an effective partner in jointventures with foreign companies and to implement a much expanded public sectorexploration program. The results of these initiatives have been encouraging,both in terms of the increased level of private investment in oil explorationand in the form of higher domestic crude oil production which has increased by50 percent since 1975. These developments form the basis of the overall opti-mism about Pakistan's energy situation and prospects that is one of the majorconclusions of this report. However, the full realization of the potential ofPakistan's indigenous petroleum resources continues to depend critically onimprovements in the organizational and decision making structure of the publicand semi-private petroleum sector organizations. Adequate resources and theirefficient allocation, a clearer definition of the respective roles envisagedfor the public and private sector in the national exploration program, and thedevelopment of an integrated and rationalized downstream refinery strategy areall issues which need to be urgently addressed.

1.08 Pakistan's total commercial energy requirement is projected togrow at just over 8% per year from 480 trillion BTU in FY79 to 780 trillionBTU in FY85. This estimate is based on an anticipated GDP growth rate ofabout 5.5% over this period and on an historic energy/GDP elasticity valueof 1.45 1/. The consumption of different fuels will grow at different ratesaround this average. The bulk of additional energy demand will continue tobe met from increases in the supply of natural gas and hydroelectricity andconsumption of these two energy resources is forecast to grow at approximately10% and 12% per annum, respectively. Coal and nuclear power are expected toplay a marginal role as sources of energy over the next five years althoughtheir contribution to national energy supply could increase substantially inthe latter half of this decade; and though the consumption of LiquefiedPetroleum Gas (LPG) is expected to increase rapidly, its contribution willcontinue to be small in relation to total energy supply. 2/ The consumptionof oil and oil products is expected to increase at about 6% per year over thisperiod, a rate which is below the projected rate of growth of overall energyconsumption but somewhat higher than the rate at which the consumption ofpetroleum products has been rising to date. This is a reflection of thechanged sectoral consumption pattern of petroleum products and the limitedpotential for further substitution away from oil in the short term. Thisimplies that by 1985 Pakistan will require about 6 million tons of oil and oilproducts, and to meet this demand increased amounts of crude oil will have tobe imported unless indigenous crude oil in known fields is brought intoproduction and recent discoveries are evaluated and developed rapidly.

1.09 Increasing domestic production of crude oil from its present levelof 10,500 barrels/day (0.5 million tons/year) will depend, in the short term,primarily on increased production from three known fields, Tut, Adhi andMeyal, which currently account for 85% of all domestic oil production. Onthe basis of present production levels and the estimated pace of development

1/ Between FY72 and FY79 a GDP growth rate of 5.0% was accompanied by anannual growth in total primary commercial energy consumption of 7.25%.

2/ For a discussion of the medium term options facing Pakistan in thedevelopment of its energy sector strategy, see also paras. 7.22-24.

-4 -

drilling activity, the annual production of indigenous crude oil from dis-covered fields is conservatively projected to increase to about 1.6 milliontons in 1985, which would be sufficient to meet over half the projectedincrease in petroleum demands over this period and would reduce Pakistan'snet oil import bill in that year by an estimated $225 million in 1980 prices.

1.10 Further reductions in the oil import requirement could result fromproduction at one other field at Dhodak which has yet to be fully appraisedbut where results to date have been promising. However, Pakistan's continuingdependency on imported crude oil will be critically determined by the successof current exploration activity being undertaken by foreign explorationcompanies and the OGDC. Estimates of the extent of Pakistan's oil reservesvary widely, partly due to the slow pace of exploration activity over the pasttwenty years, with Government estimates being a high 184 million barrels (25million tons). 1/ However, the success rate so far for oil and gas explorationactivity has been good. Given the expected increase in exploration activityand a modest degree of success, substantial inroads can be expected to be madeinto the country's oil import bill in the late 1980s.

1.11 The supply of other primary energy sources is also projected toincrease. Natural gas production has been increasing rapidly and with thecommissioning of additional processing and transmission facilities is expectedto continue to do so. Total proven remaining 'recoverable' reserves areestimated at 15.9 trillion cubic feet (286 million TOE) which would meetforeseeable internal demand until the end of this century. This figure wouldincrease by the extent of the reserves proven at Dhodak and Pirkoh which arestill being subjected to detailed geological examination.

1.12 Pakistan's hydro potential is estimated at about 20,000 MW but itsdevelopment is hampered by geographic problems of distance from load centres,difficult terrain and by seasonal variation and silting in the major rivers.With the full development of the Tarbela, Mangla and Warsak projects by 1985,installed hydro capacity will increase from the current level of 1,567 MW to3,300 MW, leaving considerable room for further expansion as demand grows.The Government is also working on developing an indigenous hydro technologybased on simple design and low costs that could make numerous micro-hydrosites in the 100-200 KW range economic and affordable.

1.13 Although the contribution of coal to national energy supply hashistorically been declining and only small increases in the supply of coalare projected for the immediate future, the potential for exploiting thisindigenous resource is large. Pakistan's coal reserves have *not been ade-quately delineated and the proven reserves figure (100 million tons) isexpected to amount for only a small fraction (about 10-15%) of the remainingrecoverable reserves. In spite of their largely poor quality these reserveshave the potential for use in electric power generation and further work isurgently required to develop an integrated national strategy for theirexploitation.

1/ This excludes an estimated additional 200 million barrels at Dhodak,

which have yet to be proven.

-5-

Non-Commercial Energy

1.14 Non-commercial energy sources have traditionally supplied more thanhalf of the country's total energy requirements and currently account foran estimated 40 percent of them. However, data on their consumption by fueltype or sector of use are inevitably sparse. In 1974/75 national con-sumption of non-commercial fuels was estimated at 7.4 million TOE, of whichfirewood (54%), dungcakes (16%) and bagasses (17%) were the major sources.In the case of firewood, nearly all of the total consumption of 11 milliontons was met through the unregulated use of trees and shrubs outside theofficially classified forestry areas. The damaging effects of this large-scale deforestation have not been documented but they urgently need furtherstudy and attention. Non-commercial fuel consumption is primarily forresidential use (80%), with bagasses being the only fuel consumed principallyfor industrial energy in sugar processing. Non-commercial fuels will continueto meet a large part of the energy needs of rural households in the future,although their consumption is expected to continue growing at a slower pacethan commercial energy consumption. The government has recently been analyz-ing and experimenting with the more productive utilization of existing fuels,such as animal dung for biogas generation, and with the potential for non-conventional energy sources, including the development of geothermal, solarand wind energy. A hundred demonstration biogas plants are being set upthroughout the country and the technical and economic feasibility of usingwind and solar energy for cooking and pumping water in rural areas is beingtested. Although many of these developments are as yet at an exploratorystage and unlikely to have a significant impact on the overall energy picturein the near future, the potential savings from more efficient utilization offirewood for residential use are large and the prospects for biogas generatingplants are promising.

Sector Investment Requirements

1.15 The development of indigenous energy resources will require large-scale investment in this sector and the government has recognized this byallocating Rs 33.5 billion (US$ 3.4 billion) for investments in the energysector during the Fifth Plan Period (FY79-83). This is equivalent to 22% ofall public investment during this period, a proportion which is substantiallyhigher than in previous years and well above the average for developingcountries as a whole (15%). The bulk of this planned investment (87%) will befor the development of the power sector, but Rs 5.6 billion (US$570 million)would be spent on developing oil and gas, with about Rs 4 billion earmarkedfor investment in exploration and development by the Oil and Gas DevelopmentCorporation. Private sector investment in the exploration and development ofdomestic oil and gas resources is expected to total about $150 million overthe Plan Period, which is markedly higher than in the past but still repre-sents a modest effort in relation to the costs associated with what wouldconstitute an adequate programme for the development of indigenous hydrocarbonenergy resources.

-6-

Sector Issues

1.16 Considerable progress has been made since 1973 in improving andstrengthening the institutional framework of the energy sector, in raisingenergy prices to reflect real opportunity costs, in developing and promotingdomestic oil exploration and production and in analyzing and experimentingwith the more efficient utilization of traditional energy sources (such asbiogas from animal manure) and the application of new ones such as solar ormicro-hydro energy. Nevertheless, if the optimistic energy outlook envisagedin this report is to be realized, the Government will have to take steps todevelop a national energy planning capability, rectify a series of anomalies(particularly with regard to relative energy pricing) and further strengtheninstitutions in the hydrocarbon sector as well as in the power sector and thefield of renewable energy development. Some of these issues are summarizedbelow. 1/

Institutional Framework

1.17 In the oil and gas sector, some institutional strengthening hasalready taken place and OGDC is now being developed as a commercially-orientedinstitution (5.04, 8.06) with overall guidance and support being provided bythe Ministry of Petroleum and Natural Resources (5.03). Nevertheless, thereis a need to ensure that this momentum is not dissipated through shortagesof either trained personnel or adequate funding. Competent technical staffrequired for exploration and drilling, for whom a buoyant market exists in theGulf States, have been difficult to find and to keep and it is important thattheir remuneration package reflects market conditions of supply and demand.It is also important that OGDC continue to adopt modern management techniquesand consider the functional separation of its operational activities from theother responsibilities it has to discharge in its capacity as a national oilcompany (5.04). The Government should also consider the clearer definitionof the respective roles envisaged for the public, semi-private and privatesectors in the petroleum exploration and development field.

1.18 The development of coal resources will also depend criticallyon institutional strengthening and the formulation of an integrated nationalcoal policy. The Pakistan Mineral Development Corporation is well run andhas qualified and experienced technical staff, but its influence is limitedto the small share of coal produced by the public sector (20%). A mechanismwill have to be developed for providing technical assistance and extensionservices in modern mining techniques to the numerous small private mineoperators which supply the bulk of the country's coal requirements, if thefull potential of the country's coal resources is to be realized.

1.19 In the power sector, a rationalization of the existing institutionalframework is required to enable the sector to cope with the demands that willbe made upon it in the 1980's. After 1982, the country will have an inte-grated national power network which should be planned for as a whole (7.12);

1/ For a more detailed discussion of these issues, see paragraph referredto in parentheses.

-7-

yet WAPDA and KESC,the main power generating authorities, continue to plan fortheir own systems largely independently of each other (6.19). Furthermore,the methodology used for demand forecasting and the short time horizon overwhich these forecasts are made, precludes them being used as a basis forplanning the scope and timing of power capacity expansion plans (6.19). Thereis an urgent need to strengthen the planning function in the power sector andto decide on where a national power planning unit should be located.

1.20 A number of government and autonomous bodies have been involved withthe development of renewable energy resources (7.17-20) which is perhaps asit should have been in the initial stages of analysis and experimentation.However, there now exists a need for the Government to take stock of thework that has been done in this field, to identify the most promising avenuesfor further analysis and to allocate funds for the development of renewableresources in accordance with these priorities (7.22).

1.21 Finally the absence of a well defined energy planning organizationthat could coordinate the investment, pricing and conservation policies ofthe different energy subsectors has posed a serious problem in the past(5.15). The Government has recently taken steps to rectify this by appointinga high level inter-ministerial committee, chaired by the Minister of Finance,to develop and recommend policies for energy development and utilization.However, it will require continued Government attention and support to ensurethat the secretariat for this committee is adequately staffed and funded toenable the effective build-up of a national energy planning capability (5.16).

Energy Pricing

1.22 In spite of recent Government action to increase domestic energyprices and rationalize their structure, there remains a need to develop along-term pricing policy which, within the Government's broader objectives,provides adequate incentives to developing existing hydrocarbon resources inan optimal manner, reflects more precisely the economic costs of bringingenergy products to the consumer, and establishes interfuel price relationshipsmore closely on the basis of the opportunity cost of competing fuels.

1.23 In particular, in the oil and gas sector the following pricingissues deserve consideration:

(i) The wellhead price of natural gas is too low to provide anyincentives for new exploration. Gas exploration outside theOGDC has now come to a standstill and although proven reservesare high, this issue may require examination in the near futureif additional reserves are to be developed (4.12).

(ii) Ex-refinery prices of petroleum products have historically beentoo low to provide revenues adequate to cover operating costsof the country's two principal refineries, and the presentsystem, whereby the Government reimburses the refineries'operating shortfall, does not encourage improved operatingefficiency. Although the recent increase in ex-refinery prices

-8 -

has rectified this problem it is important to ensure that

future increases in refinery costs are translated rapidlyinto the structure of ex-refinery prices (4.05).

(iii) Consumer prices for some petroleum products (such askerosene) and for natural gas in some consuming sectors(such as for households and cement production) have beenkept at or below import parity opportunity costs whileother products (such as gasoline) have been traditionallypriced at much higher levels. The prevalence of crosssubsidies has aggravated imbalances in the demand for lightand middle distillates in the petroleum sector which haveto be met by the import/export of refined products whichis costly in terms of storage, transport and handling(4.06).

(iv) Finally, the pricing of Liquified Petroleum Gas (LPG),which is a potential substitute for kerosene, gasolineand diesel, requires close attention. At present, LPG ispriced at a higher level than either of these products,but given the expected increases in LPG supply, projectedto grow to 250,000 tons by 1985, consideration should begiven to encouraging its substitution for diesel, gasolineand kerosene which already have to be imported in refinedform to meet high and rapidly increasing domestic consump-tion levels (4.15). This could be done by lowering LPGprices while raising the price of its substitutes.

1.24 In the power sector, the current tariff structure is complex anddistorted. Energy and minimum charges are generally not directly related tothe costs of supplying electricity to consumers. In particular, capacity orKW charges are well below long-run marginal costs and low voltage consumersare charged significantly below the cost of supply (4.16). The Governmenthas recognized the extent and seriousness of these distortions and has commis-sioned a study in collaboration with the Bank, to prepare a revised tariffstructure for the power sector. This study has now been completed and itrecommends a series of changes to the existing power tariff which would bothraise average costs and restructure individual tariffs to correspond moreclosely to the marginal costs of supply to different consumer categories(4.17).

1.25 A number of other issues also exist with regard to power sectorpricing. Capacity charges in industry would still be well below supply costsand should be raised in subsequent tariff revisions (4.17), and the questionof the treatment of losses in tariff calculations (4.18), the economic valueof natural gas used in thermal electricity generation (4.19), the questionof uniform national tariffs and the implications for cross subsidization ofdifferent consumer groups and regions (4.20) and the present policy withregard to connection charges (4.21) need to be examined further.

-9-

Other Issues

1.26 A related issue in the power sector is the high and increasingpercentage of system losses (including losses through the theft of power)which now amount to a third of total electricity generation. The governmenthas now embarked on a large program of extension and reinforcement for itssecondary transmission network, which should help reduce these losses to about25% of total generation in FY85, but this will require continued governmentattention.

1.27 In the case of refined petroleum product consumption, the long termimplications of the continued divergence between, the structure of demand andthe output mix of domestic refineries, which has been caused in part by theGovernment's historical demand management and relative pricing policies, needsto be critically assessed; in particular, with regard to the strategy to beadopted for the expansion of domestic refinery capacity (3.08, 4.07, 7.07).

1.28 Finally, the Government should now take steps to capture the momentumgenerated by its effective media campaign for energy conservation and toensure that the efficiency of energy utilization, particularly in the indus-trial and residential sectors, is improved to reflect higher energy costs.The commercial energy/ GDP coefficient for the period 1973-79 is still high(1.45) and reductions in its value would have important benefits in terms ofrelaxing the tight balance of payments situation that will be the majorconstraint to Pakistan's economic development in the 1980's (6.16-20). 1/

1/ See Pakistan Economic Development and Prospects, (1980, Bank report).

- 10 -

THE EVOLUTION OF ENERGY DEMAND

Background

2.01 In 1948, the first year after Pakistan's independence, per capitaenergy consumption in the country was estimated at 0.1 TOE, of which only 30percent was met from commercial energy sources, mainly coal and oil. By 1979this picture had altered dramatically. Energy consumption per capita hadincreased to 0.25 TOE and the share of commercial energy sources doubled to60 percent of this total. Commercial energy consumption had therefore risenat a much more rapid rate, more than quadrupling in per capita terms from 0.03TOE to 0.14 TOE and registering an eleven fold increase in absolute termsfrom 0.95 million TOE to 11.3 million TOE over the same period. In spite ofthis rapid growth, commercial energy consumption in Pakistan is still low byinternational standards, with per capita consumption levels in 1977 beingestimated at approximately one-tenth the world average and one-half theaverage for all developing countries.

2.02 Notwithstanding the marked reduction in the share of total energysupplied by non-commercial fuels, firewood remained, in 1979, the single mostimportant energy source contributing over half of non-commercial energy supplyand about 23% of total energy supply; just ahead of the contribution of themost important commercial energy source -- petroleum (22%); and the mainindigenous commercial fuel, natural gas (21%). The remaining 34% was suppliedby hydroenergy (12%) and coal (3%) in the commercial sector, and bagasses(7%), animal manure (7%) and a variety of other non-commercial fuels based onvegetable residues.

2.03 The major energy consuming sectors in 1979 were residential demandfor cooking and lighting (44%), followed by industry (34%) and transport(12%). However, this overall consumption pattern subsumes two very differentpictures of energy consumption once commercial and non-commercial energysources are separated. The household sector derives three-quarters of itsenergy from non-commercial fuels and is in turn responsible for over 80% ofall non commercial energy consumption, but accounts for less than 20% of theconsumption of commercial energy sources. On the other hand, the industrialsector gets over three quarters of its energy from commercial energy sourcesand is responsible for about 45% of their consumption, but of less than 20% ofthe consumption of non-commercial fuels. The other major sectors only consumecommercial fuels and consequently their shares in commercial energy consump-tion far exceed the proportion of total energy which they consume.

2.04 The existence of these differences, the fact that the data on non-commercial energy supply and consumption in Pakistan are both more sparse andless reliable, and the fact that the difficulties of aggregating energyconsumption from different sources without making allowances for differencesin the end use efficiency of consumption for different fuels in differentsectors, are compounded when non-commercial energy sources, such as bagassesand dung cakes, are included with commercial hydrocarbons, suggests that anexamination of the disaggregated demand pattern for commercial and non-commercial energy sources separately may prove more instructive.

- 11 -

Commercial Energy Consumption

2.05 The growth in commercial energy consumption in Pakistan can be attri-buted to three major factors. First, the diversification of the Pakistanieconomy from being almost entirely agrarian to one where nearly two-thirdsof GDP and 45% of total employment is generated outside the agriculturalsector in more energy intensive activities. Second, within the agriculturalsector, although the overall intensity of commercial energy consumptionremained low -- this sector was responsible for the production of two-thirdsof national output but only 10 percent of national commercial energy con-sumption in 1979 - increases in output over the past two decades have beenclosely associated with energy intensive mechanization and artificial irriga-tion. The incremental commercial energy consumption/output growth ratio inthis sector has averaged 2.3 over the period FY65-79 - well above thecorresponding value for any other sector. 1/ Finally, the increasing urban-ization of the economy, with the share of urban population increasing from18% in 1951 to 27% in 1977, has resulted in reduced access to traditional,non commercial sources of energy and caused a more rapid rate of growth ofcommercial energy consumption than would have been implied by rising realincomes alone.

2.06 Increases in the overall level of commercial energy demand havebeen accompanied by changes in the sectoral composition of that demand.The household sector has steadily increased its share in total commercialenergy consumption because of the factors listed above; but the growthof consumption in the other sectors has been more varied. Between 1965and 1972, the shares of industry and agriculture in total commercial energyconsumption increased, largely because output in these sectors was growingat rapid rates. Since FY72, however, economic growth in Pakistan has beenslowed down by political and industrial unrest which adversely affectedindustrial output, investment and productivity, and by droughts, floodingand other problems which have reduced agricultural output growth. Onemanifestation of these troubles has been slower growth in commercial energyconsumption in these sectors, and a consequent decline of their shares inthe total.

1/ The corresponding values for the industrial and transport sectors are1.3 and 1.6, respectively. However, these estimates should be treated asindicative of broad orders of magnitude only because of the broad natureof sectoral classification and the consequent variety of activitieswithin each sector, and because of the progressive reallocation of energyconsumption over time from "other or unallocated" to the consumingsectors as data collection and analysis improved, which may have affectedthe estimated rate of growth of energy consumption in different sectorsdisproportionately. Nevertheless, the Revised Action Program for Agri-culture and Water Resources Development carried out by WAPDA, withUNDP and Bank assistance, brings out the high capital intensity ofPakistan's agricultural development and strategy. More emphasis offimproved agriculture practices, including water management, would makePakistan's agricultural development somewhat less energy intensive.

- 12 -

Table 2.1

Percentage Distribution of Commercial Energy Consumption

Average Annual Growth RateSector FY65 FY72 FY79 1965-72 1972-79

Industrial and Commercial 43 47 44 8.5 5.3Agricultural 8 11 9 11.5 5.0Transport 17 17 21 6.3 10.4Residential 10 11 18 7.6 14.7Govt./Other 22 14 8 -0.5 -0.1

TOTAL 100 100 100 6.6 7.25

Notes: (1) Percentage share of each sector includes both direct consump-tion of primary energy and prorated share of energy consumedthrough electricity generation.

(2) Hydro and nuclear energy converted at 12,000 BTU/kWh toapproximate heat rate of thermal generation.

(3) Excludes use of gas as feedstock in fertilizer production.

(4) In view of the high proportion of "other" or unallocatedconsumption in the figures for the earlier years and thepossible reallocation of consumption to other sectors withimproved data collection, the sectoral growth rates forenergy consumption in the sixties should be treated asindicative of orders of magnitude only.

2.07 In spite of these problems, total commercial energy consumptionhas continued to grow at a higher rate (7.25%) in the seven years since1972 than it had done in the preceding seven years. This is partlybecause the last two years, FY78-79, have seen a revival of industrialand agricultural activity which has offset, to some extent, the somewhatlackluster performance of earlier years, and partly because incomes in theresidential sector and output in the transport sector have continued togrow rapidly and resulted in rapid growth in energy consumption in thesesectors.

2.08 One of the implications of these changes in the intersectoralpattern of commercial energy consumption, has been that commercial energy/GDPelasticity for the economy as a whole has remained at a relatively high levelin the seventies in spite of the manifold increases in world energy prices. 1/

1/ This is partly the result of the Government's domestic pricing policywhich has entailed domestic energy prices being raised only gradually tointernational levels and whose impact on curbing energy demand in thisperiod has, therefore, been limited (See Chapter 4 below).

- 13 -

Between FY72 and FY79 an annual average GDP growth rate of about 5.0% has beenassociated with a 7.25% growth rate for commercial energy consumption whichresults in an uncompensated energy output elasticity estimate of 1.45 for thisperiod, a figure which is marginally higher than the corresponding value forthe previous seven years (1.36). Although this figure is not unreasonablyhigh for a country at Pakistan's stage of economic development, the fact thatno reduction in the value has been made to reflect the changed world energysituation suggests that improvements in energy utilization efficiency andmeasures to conserve energy could play an important role in the Government'sdemand management policies in the eighties. 1/

2.09 Changes in the intersectoral energy consumption pattern have alsohad an important effect on the demand pattern for different commercial fuels.The transport sector relies almost exclusively on petroleum products forenergy, whereas industry relies mainly on natural gas (48%) and electricity

(34%). Agricultural energy consumption derives primarily from electricity(75%) but also from oil (25%); and the household sector relies on electricity(46%), oil (37%) and gas (15%). As a result of these differences, the patternof demand for the four major fuels -- petroleum, natural gas, coal andelectricity -- has evolved along different lines.

Consumption of Petroleum Products

2.10 Between FY65 and FY79 the total consumption of petroleum products inPakistan increased from 2.1 to 3.9 million metric tons per annum. As thefollowing figures show, this overall increase was accompanied by a substantialreallocation of petroleum consumption across sectors.

Table 2.2

Sectoral Distribution of Petroleum Consumption in Pakistan(percent)

TotalAgri- Other/ Consumption

Year Domestic Industry culture Transport Power Govt. (000 Tons)FY65 11.6 13.7 6.5 35.9 1.2 31.5 2106.7FY72 13.7 9.6 10.3 40.1 3.6 22.7 2782.5FY79 17.4 5.2 6.0 57.4 0.4 13.6 3890.7

Annual Average Growth Rate: (%)

FY65-72 7.0 -1.0 11.2 6.1 21.0 -0.7 4.1FY72-79 8.7 -3.9 -2.9 10.4 -23.7 -2.7 5.0-------------------------------------------------------------------- __-------__------

1/ In Thailand, for example, the value of the commercial energy/GDP coeffi-cient has been successfully reduced from 2.06 in the period 1968-73,to 1.08 for the five year period thereafter.

- 14 -

2.11 The main trends to note here are the absolute decline in industrialoil consumption even prior to the 1973 oil crisis; the continued increasein petroleum consumption in the transport and residential sectors wherehigher oil prices in the seventies have not stopped oil consumption fromincreasing proportionately more than in the previous decade; and, the reversalof earlier trends in the agricultural and power sectors where consumptionlevels have been sharply reduced in the seventies. An important featureof the current sectoral consumption pattern is that the transport sector --where interfuel substitution possibilities are more limited -- accounts forover half of total consumption, and household demand -- largely kerosene forcooking and lighting purposes -- for another 18 percent. Oil consumptionin industry, agriculture and for power generation is already small and thepotential savings from curbing demand in these sectors are limited. Thisfactor has an important bearing on the appropriate demand management policiesthat the Government can adopt, and it also affects the structure and growthof demand for the various petroleum products.

Table 2.3

Demand for Petroleum Products

Percentage Share and Historic Growth Rates

Share of FY79 Average Annual Growth RateProduct Consumption FY65-72 FY72-79

Aviation fuels 8.6 9.3 8.5Gasoline - regular 10.1 ] 4.6 5.8

- premium 2.9 T 11.6Diesel - light 6.3 ] -2.6

high speed 40.6 8.5 9.7Kerosene 17.8 5.9 7.4Fuel Oil 13.7 -.0.5 -4.5

TOTAL 100.0 4.1 5.0

2.12 Kerosene and high speed diesel, two products which together accountfor 60 percent of all petroleum consumption, have also been experiencing veryrapid rates of demand growth, which is partly a result of the price subsidi-zation of these products. Whereas some justifications for such a policyexist, insofar as kerosene is used mostly for cooking and heating by rural andpoorer urban households which do not have access to natural gas or electricity,and diesel is the predominant fuel for public transport, the continuationof these marked diversities in product demand growth has major implicationsfor the operation of domestic refining capacity, especially if the demandfor fuel oil continues to decline in the future. 1/

1/ See also paras. 3.08, 4.07, 7.06.

- 15 -

Consumption of Natural Gas

2.13 The consumption of natural gas, the main indigenous fuel inPakistan, has increased rapidly from a low initial figure of 9 MMCFD in1955 to 510 MMCFD in FY79. Natural gas is used principally for thermalelectricity generation and as an industrial fuel, but a fifth of total gasconsumption is as feedstock for the fertilizer industry. The evolution ofthe current sectoral pattern and associated historical growth rates arepresented below.

Table 2.4

Sectoral Distribution of Gas Consumption in Pakistan

Sector Percentage Consumption Annual Average Growth Ratein FY79 FY65-72 FY72-79

Residential 6.50 27.5 27.0Commercial 3.25 18.3 17.0Industry 48.23 13.2 7.8Power 29.19 8.3 1.3All Energy (87.18) 10.8 7.4Fertilizer Feedstock 12.82 38.5 8.6

Total Consumption 186.15 12.4 7.6(billion cu. feet)

2.14 Continued rapid growth in gas consumption by the residential andcommercial sectors has significantly increased their share but they stillaccount for less than 10 percent of total consumption. The use of gas asfeedstock in the fertilizer industry has also increased at an above-averagerate and has resulted in total gas consumption rising at a higher rate thanits use as a source of energy.

Consumption of Coal

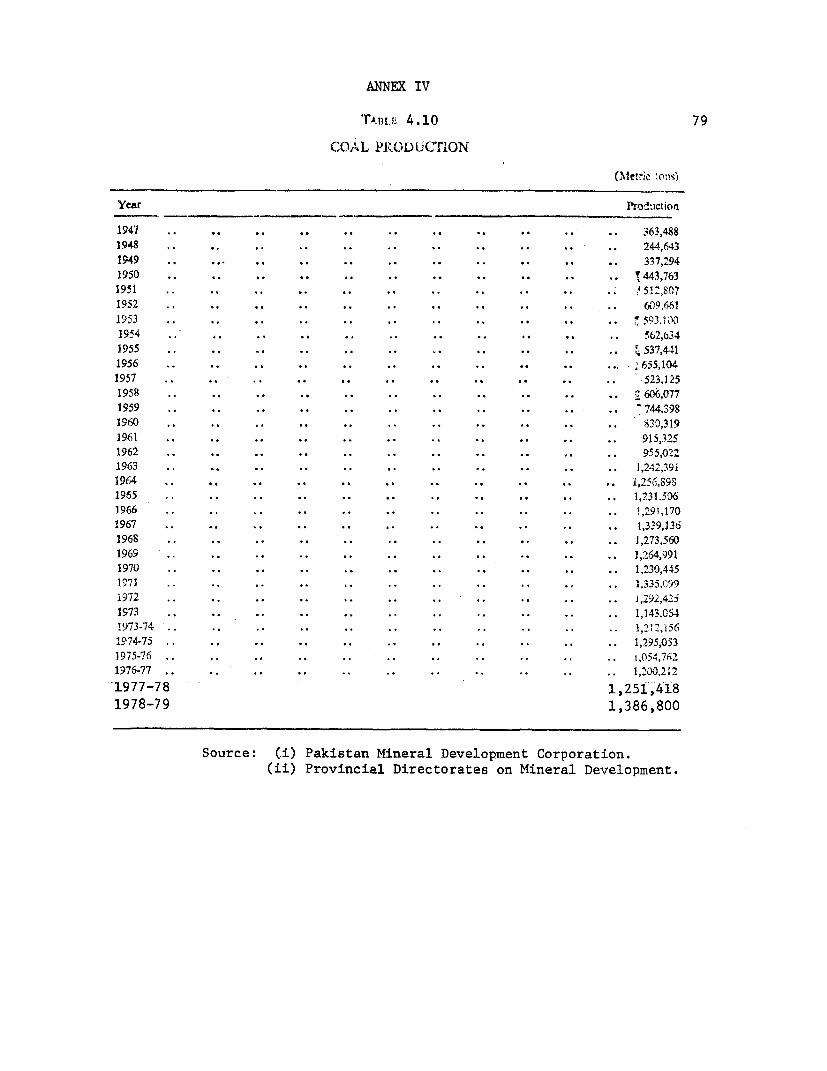

2.15 Recorded coal consumption in Pakistan has remained roughly constantat about 1.3 million tons since 1965 and consequently its importance as anational energy source has declined considerably. 1/ Prior to the availabilityof gas and the use of diesel powered locomotives, the major users of coal werethermal electricity generation plants, the railway, and the fertilizer, cementand brickmaking industries. Currently, its use is restricted largely to thebrickmaking industry in areas where natural gas is not available, with smallamounts being used for power generation and by households for cooking andheating. The sectoral consumption pattern for coal is presented below.

1/ Official records may understate actual consumption because of unreplortedproduction of coal from some small private mines. Preliminary resultsof a survey recently carried out by the PMDC suggest that actual totalcoal consumption in the country may be the order of 1.8 million tonsper year. However, this does not alter significantly the share oftotal energy supplied from coal.

- 16 -

Table 2.5

Sectoral Distribution of Coal ConsumptionAnnual Average Growth

Precentage Share in: Rates 1965-79Sector 1965 1971 1978-9 %

Brick kilns 70.1 75.2 94.4 + 2.3Power 12.0 9.5 2.3 -10.5Domestic 2.5 2.2 2.4 - 0.3Other 1/ 15.4 13.1 1.0 -17.5

Total (000 tons) 1251.3 1417.6 1386.8 0.0

Consumption of Electricity

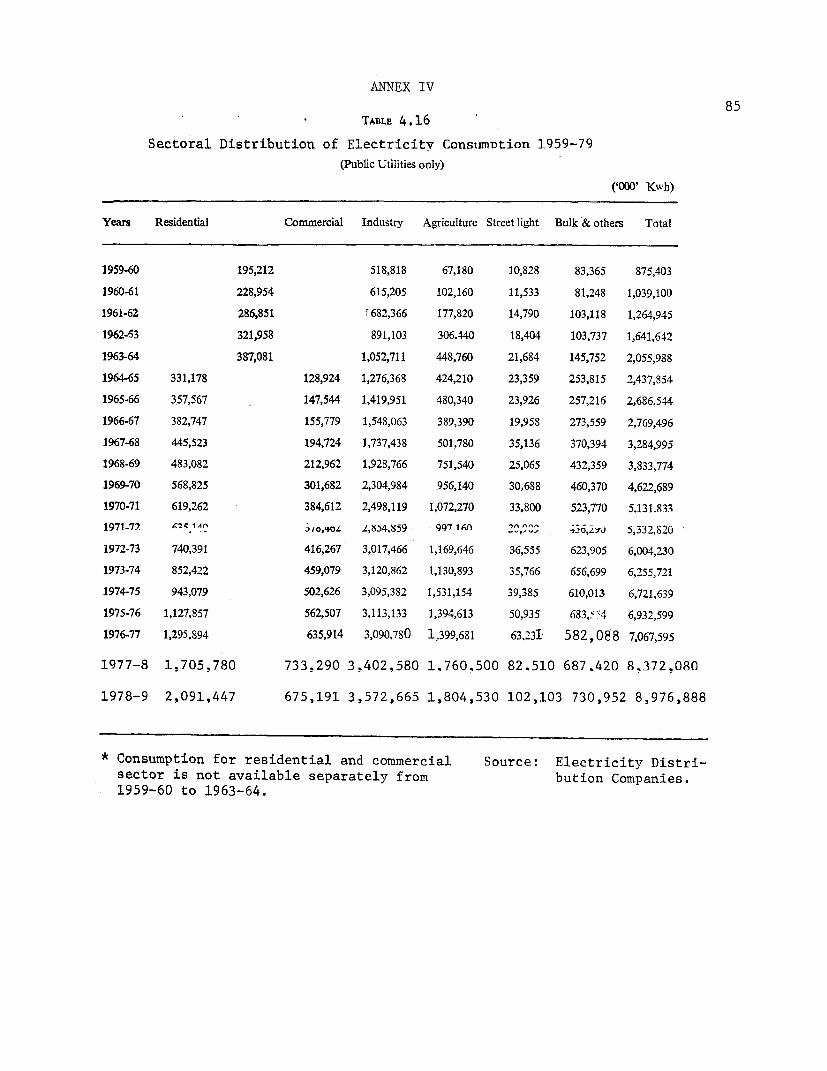

2.16 Electricity consumption has been increasing at about 10% a yearsince 1965 and is currently estimated at about 9 billion kWh. 2/ Industrialand agricultural electricity consumption accounts for 60% of the total buthousehold demand, which has been growing at one and a half times the averagerate, now accounts for a quarter of total consumption and this share isprojected to increase in the future. Sectoral consumption growth rates inthe seventies differ markedly from those of earlier years. The growth ratefor household electricity consumption has doubled, but for the industrialand agricultural sectors, which had been growing at above-average rates inthe sixties, consumption growth rates in this decade have fallen sharply toreflect their slower overall output growth.

Table 2.6

Sectoral Distribution of Electricity Consumption

Annual Average Growth RatePercentage Distribution (%)

Sector FY65 FY72 FY79 FY65-72 FY72-79

Residential 13.5 12.2 23.3 9.8 18.6Commercial 5.3 7.1 7.4 16.6 8.6Industrial 52.4 53.4 39.7 12.2 3.3Agriculture 17.4 18.6 20.1 13.0 8.8Street Lighting 1.0 0.6 1.4 4.1 18.6Bulk and others 10.4 8.1 8.1 8.0 7.6

Total Million kWh 2437.9 5332.8 8976.9 11.8 7.7

1/ Much of the consumption in the "other" category for the earlier years wasfor the railways which were coal-fueled in that period. More disaggregatedconsumption data for those years are not available.

2/ Based on number of units sold; excludes power theft estimated at about1.5 billion kWh.

- 17 -

Non-Commercial Energy

2.17 Although non-commercial energy sources have traditionally suppliedmore than half of the country's total energy requirements and currentlyaccount for an estimated 40% of them, data on their consumption by type offuel or sector of use are inevitably sparse. The most comprehensive bodyof data derives from a survey done in 1974-5 by the Energy Resources Cellof GOP which covered 18,300 households and 4,960 shops and workshops. Theresults of this survey showed that an estimated 7.43 million TOE of non-commercial fuels were used in the country during FY75. Over 80 percent ofthis consumption was for residential use, industrial consumption beinglimited to firewood (largely for tobacco curing) and bagasses (used as fuelin the sugar industry). About 17% of the total consumption of non-commercialfuels was in urban areas.

Table 2.8

Consumption of Non-Commercial Fuels 1974-75Percentage Consumed In Total Consumption BTU9 %

Fuel Residential Commercial Industrial (000 tons) xlO Share

Dung cakes 100 - - 5535 95800 15.5Firewood 96 3 1 10923 159808 54.2Charcoal 37 63 - 41 767 0.3Bagasses 5 - 95 2922 48596 16.5Cotton sticks 100 - - 1580 18808 6.4Sawdust 100 - - 146 3807 1.3Shrubs 100 - - 1579 16473 5.6Weeds 100 - - 61 845 0.3Tobacco sticks 100 - - 13 138 0.1

TOTAL 82 1.85 16.01 - 295042 100

Source: Energy Resources Cell, Government of Pakistan.

Firewood

2.18 Over half of all energy derived from non-commercial sources isfrom firewood, and this makes firewood the single most important indigenousenergy source in terms of both commercial and non-commercial energy. Onthe basis of data collected by the Goverment, the production of firewoodfrom registered plantations was 120,000 tons in FY75, only a minute fractionof total consumption which was estimated by the ERC survey to be about 11million tons in that year. The implications of this disparity are serious.Although recorded forest areas (8.8 million ha) represent about 10% of theland area of the country, most are range lands and unproductive scrub forests.The productive forests mainly comprise scattered mountain coniferous forestsin the north of the country, totalling some 1.8 million ha. Development oftimber production in these forests has been severely constrained by thedifficult topography, inaccessibility, the need to protect the watersheds,

- 18 -

and by the rights and concessions of local residents. The problem has beenfurther exacerbated by the historical deforestation that has resulted frompopulation pressures and the need for more farmland. The severe lopping andpremature felling of trees has caused widespread soil erosion resulting indecreased soil fertility and a greater amount of silt carried by the rivers,shortening the lifespan of expensive hydroelectric facilities.

Bagasses

2.19 Bagasses are the residue left after sugar cane is crushed for theproduction of sugar. Consequently, their production is directly related tothe production of sugar cane. 1/ In FY77, bagasses production was estimatedat 3.15 million tons but due to the adoption of a policy of intensified sugarcane cultivation since then, their production is expected to increase rapidly.

Dung Cakes

2.20 The use of animal dung for cooking and heating has been animportant component of traditional energy supply in rural and poorer urbanareas. In rural areas only a small part of the available animal wastes isburnt for fuel as its use as manure has traditionally been more profitable.In this context the use of biogas plants, with which the Government iscurrently experimenting, may enable animal wastes to be used for bothmanure and fuel, thereby increasing the proportion of animal dung availablefor fuel use from the current level of 25% to one that is much closer tothe total supply estimated at 98 million tons in FY75. 2/

1/ Bagasse production estimated at being equal to 12.75% of crushedsugar cane availability.

2! For a discussion of the Government's biogas project, see belowparas 7.15-16.

- 19 -

COMMERCIAL ENERGY SUPPLY

Background

3.01 Pakistan's domestic energy resources are relatively unusual inbeing characterized by sizeable reserves of natural gas, substantial hydropotential but only limited known reserves of crude oil, coal, and uranium orother mineral ores which might be used as nuclear fuels. Consequently, evenprior to 1973, the main thrust of government policy had been to increase theshare of natural gas and hydro power in meeting the country's energy require-ments. Since 1973, this policy has been pursued with renewed emphasis, andwith the modification that the government has also taken measures to step upthe level of domestic exploration for oil in an attempt to reduce its depend-ance on imported energy sources. This is particularly important in view ofthe fact that in spite of a progressive reduction in the share of totalcommercial energy that is supplied by oil, oil and oil products still remainthe largest single source of commercial energy supply in Pakistan -- account-ing for 38 percent of the total supply in FY79.

Table 3.1

Commercial Energy Supply by Source

Annual Average GrowthPercentage of Total Supply Rates (%)

Source FY65 FY72 FY79 FY65-72 FY72-79

Petroleum Products 49 42 38 4.2 5.8Natural Gas 1/ 26 35 36 11.2 7.6Coal 16 8 5.5 -3.5 0.1Hydroelectricity 9 15 21 15.2 12.2LPG 0 2/ 0.3 n.a. 36.0Nuclear 0 0.4 0.2 n.a. 0.0TOTAL 100 100 100 6.6 7.3

1/ Excludes non-energy use of gas as feedstock for fertilizer.

2/ Less than 0.1%.

The Supply of Petroleum Products

3.02 Crude Oil. Historically the supply of crude oil in Pakistan hasbeen characterized by an almost exclusive reliance on imports. In FY79,domestic crude production at 0.51 million tons accounted for about 12 percentof the total crude requirements of domestic refineries. Even this level hadbeen reached after a sharp reversal of earlier trends which had resulted indomestic crude production steadily falling from 460,000 tons in 1965 to325,000 tons in FY75.

- 20 -

3.03 The low level of crude oil production is attributable mainly to theinadequacy of domestic exploration activity in the thirty year period priorto 1977, which was itself a function of the relatively low level of inter-national oil prices prior to 1973 and the lack of adequate incentives for oiland gas exploration provided by the Government. In the 30 years from 1947 to1977 only 160 exploration and development wells were drilled in Pakistan byforeign oil companies, and a further 20 by the state owned Oil and Gas Devel-opment Corporation (OGDC). Furthermore, the pace of exploration activity hasbeen uneven. Exploration activity by foreign companies reached a peak in1958 (following discoveries of large gas reserves at Sui) but fell sharplyagain from 1960 onwards. During the 1960s most of the exploratory drillingwas carried out by OGDC, but with only limited success in detecting increasedreserves of crude oil.

3.04 However, the changed economics of oil exploration since 1973 meanthat increased domestic oil exploration in Pakistan has become more impor-tant and more viable. The country's geological structure, though complex andvaried, is in many respects similar to that of Iran and Iraq where substantialoil pools have been discovered, and 80 percent of its total land area of310,000 square miles is characterized by sedimentary basins which have thepotential for generating and accumulating hydrocarbons. Further substantia-tion is provided by the relatively high success rate enjoyed by whateverexploration activity there has been in Pakistan. One in six wildcat wellsdrilled in the country has had significant hydrocarbon shows, compared toa world average of one in ten. Estimates of total oil reserves vary widelyand are not well determined. The Government has estimated remaining recover-able reserves to be in the order of 184 million barrels (25 million tons), butthe proving up of estimated reserves at Dhodak would increase this figure to384 million barrels (52 million tons). 1/ Although these reserves are smallby international standards, they would still satisfy Pakistan's own consump-tion requirements for well over a decade.

3.05 The government has recognized the need to stimulate privateexploration activity in the petroleum sector as a vital component of itsstrategy for increased domestic oil production and, to this end, in 1976it amended the legislation governing the petroleum sector to provide theclear cut incentives which had hitherto been lacking. 2/ This amendmentdefined the tax and oil pricing basis on which production sharing agreementscould be negotiated, and provided for further incentives by limiting themaximum share of government in gross profits to 55 percent, allowing conces-sionary import duties on exploration equipment and assuring the repatriationof annual net profits. 3/ Maximum emphasis has, therefore, been laid on

1/ See Annex 4, Table 1 for field-specific reserve estimates.

2/ 1976 Amendment of Pakistan Petroleum (Production) Rules, 1949 andForeign Private Investment (Promotion and Protection) Act 1976.

3/ A detailed description of petroleum legislation is attached asAnnex III.

- 21 -

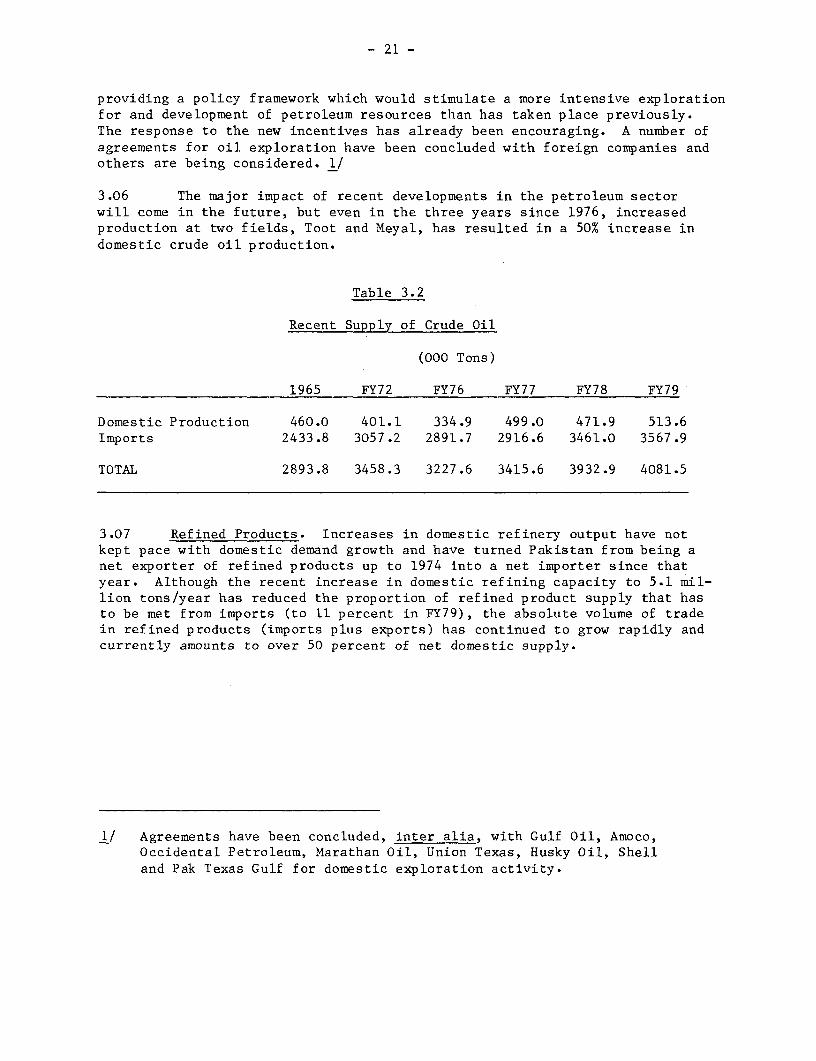

providing a policy framework which would stimulate a more intensive explorationfor and development of petroleum resources than has taken place previously.The response to the new incentives has already been encouraging. A number ofagreements for oil exploration have been concluded with foreign companies andothers are being considered. 1/

3.06 The major impact of recent developments in the petroleum sectorwill come in the future, but even in the three years since 1976, increasedproduction at two fields, Toot and Meyal, has resulted in a 50% increase indomestic crude oil production.

Table 3.2

Recent Supply of Crude Oil

(000 Tons)

1965 FY72 FY76 FY77 FY78 FY79

Domestic Production 460.0 401.1 334.9 499.0 471.9 513.6Imports 2433.8 3057.2 2891.7 2916.6 3461.0 3567.9

TOTAL 2893.8 3458.3 3227.6 3415.6 3932.9 4081.5

3.07 Refined Products. Increases in domestic refinery output have notkept pace with domestic demand growth and have turned Pakistan from being anet exporter of refined products up to 1974 into a net importer since thatyear. Although the recent increase in domestic refining capacity to 5.1 mil-lion tons/year has reduced the proportion of refined product supply that hasto be met from imports (to 11 percent in FY79), the absolute volume of tradein refined products (imports plus exports) has continued to grow rapidly andcurrently amounts to over 50 percent of net domestic supply.

I/ Agreements have been concluded, inter alia, with Gulf Oil, Amoco,Occidental Petroleum, Marathan Oil, Union Texas, Husky Oil, Shelland Pak Texas Gulf for domestic exploration activity.

- 22 -

Table 3.3

Recent Supply of Refined Petroleum Products

(000 Tons)

1965 FY72 FY76 FY77 FY78 FY79

(i) Domestic Production 2793.1 3170.8 2957.9 2889.8 3731.8 3782.6

(ii) Imports 123.1 418.7 896.1 1058.5 1091.0 1403.9

(iii) Exports 639.6 726.1 454.3 519.9 1023.8 928.8

(iv) Domestic Supply 2276.6 2863.4 3399.7 3428.4 3799.0 4257.7

(v) Ratio of Domestic Prod.to Domestic Supply 1.23 1.11 0.87 0.84 0.98 0.89

(vi) Ratio of Absolute Trade(ii+iii) to Domestic Supply 0.34 0.40 0.40 0.46 0.56 0.55

3.08 Some trade in refined products is inevitable and even profitablefor most countries, but in Pakistan's case it also reflects fundamentalimbalances between the mix of domestic refinery output and the structure ofproduct demand. The demand for kerosene and diesel has been growing at rateswell above the average, while furnace oil consumption has declined in absoluteterms (para. 2.10 above). Consequently, the share of these products in thestructure of domestic demand has incressingly diverged from the relativelyunaltered mix of domestic refinery output. As a result, large quantitiesof diesel and kerosene are currently imported and substantial surpluses offurnace oil and naphtha are exported. With production increasing from thePotwar oil fields, the surplus of fuel oil and naphtha is projected toincrease and the location of the Attock Oil Refinery, which uses domesticcrude, at Rawalpindi, means that arrangements will have to be made to trans-port these products to Karachi for eventual export. The high prices at whichPakistan has been able to export naphtha and furnace oil on the spot marketin recent years has to some extent offset the equally high prices it has hadto pay for importing refined products. Nevertheless, the net refined productimport bill is high (US$155 in FY79) and rising (up from US$92 million inFY78). An assessment of the refinery mix problem, and the implicationsfor future refinery investment, is urgently required as part of a nationalenergy planning effort.

- 23 -

Table 3.4

Structure of Petroleum Product Supply FY79

Domestic DomesticOutput Percentage Supply Percentage Net Imports

Product 000 Tons Share 000 Tons Share 000 Tons

Aviation Fuels 520.1 (13.8) 337.8 (7.9) -182.3Motor Spirits 479.9 (12.7) 516.4 (12.1) 36.5Kerosene 154.2 (4.1) 689.7 (16.2) 535.5Diesel 1074.5 (28.4) 1867.4 (43.9) 792.9Furnace Oil 1212.3 (32.1) 592.5 (13.9) -619.8LPG 34.3 (0.9) 34.3 (0.8) --

Naphtha 119.2 (3.2) 31.4 (7.4) - 87.8Other Non-Fuel 188.1 (5.0) 188.1 (4.4) --

TOTAL 3782.6 (100) 4257.6 (100) 475.0

The Supply of Natural Gas

3.09 Natural gas was first discovered in the mid-fifties and for morethan two decades has been an important component of Pakistan's primaryenergy resources. The principal producing field is that of Sui in BaluchistanProvince, which began production in 1958 and which is currently responsiblefor over 90% of Pakistan's annual gas production of 200 billion cubic feet(5.0 million TOE). Remaining recoverable reserves from the Sui reservoirare estimated at 6.83 trillion cubic feet (172 million TOE). The nextlargest field, Mari, is being utilized for the production of nitrogenousfertilizer. The remaining gas fields are much smaller and account for lessthan 8% of total production. Taking these other fields into account, theremaining recoverable reserves are estimated at 15.9 trillion cubic feet (286million TOE); this figure will rise by the extent of the reserves proven atDhodak and Pirkoh which are still being evaluated, and should meet forsee-able internal demand until at least the end of this century. 1/ Since FY72the production of associated gas, from the fields at Meyal and Dhulian, hasincreased at a slightly higher rate than overall gas supply and becauseof its higher calorific value its share in terms of energy supply has risenmarginally faster.

1/ See Annex 4, Table 6 for field-specific estimates of natural gasreserves.

- 24 -

Table 3.5

Natural Gas Supply FY65-79(billion cubic feet)

Share of Associatedin Total (%)

Non-Associated Associated Total Volume BTUs

FY65 50.94 4.38 55.32 8 9FY72 114.37 10.42 124.79 8 10FY79 200.13 20.26 220.39 9 11

Annual Average Growth Rate

FY72-79 8.4 10 8.5 - -

The Supply of Coal

3.10 Recorded coal production in Pakistan has remained roughly constantat about 1.3 million tons and there has been a consequent decline in itsimportance as an energy source. This has been due to a variety of historicaland institutional reasons. Prior to the 1973 increase in international oilprices, most developing countries had only limited incentives to develop theirindigenous coal resources. In Pakistan's case this situation was furtherexacerbated by the discovery and development of large reserves of natural gasand by the poor quality and limited nature of proven coal reserves; variouslyestimated at between 100-170 million tons. Nearly all of these reserves areof poor quality lignite or sub-bituminous coal with limited coking potential,a low heating value (average 8,500 BTU/lb) and a high sulfur and ash content.Much of this coal is subject to spontaneous combustion when stacked anddeteriorates when exposed to the atmosphere, further restricting its wide-spread use as fuel. The development of the coal mining industry has also beenhampered by its fragmented institutional structure. About 80% of the currentproduction of coal is from small, private mines which employ rudimentarymining techniques and have historically suffered from shortages of reinvestedcapital and qualified technical personnel.

3.11 The Government recognises these problems and is also aware of theincreased attractiveness of developing indigenous coal reserves that hasresulted from the changed international energy situation. In spite of theirpoor quality, these reserves have the potential for exploitation and use in,inter alia, mine-mouth power generation plants, and the Government has commis-sioned a feasibility study for such a plant at Lakhra, where the largestknown reserves are found. Preliminary results of this study, which is beingcarried out with Japanese assistance, confirm the economic and financialviability of establishing a 250MW plant which could, if additional indicatedreserves are proven, be expanded to an ultimate capacity of 100OMW to meetthe power requirements of the lower Sind area. The Government is also workingon a plan to produce 0.1 million t.p.a. of medium coking coal from the Sharighcolleries in Baluchistan for use in the Karachi Steel Mill Complex.

- 25 -

3.12 These developments are welcome steps in the full utilization ofindigenous coal reserves, but an integrated development strategy for coalstill needs to be formulated. In particular, further work needs to be urgentlydone on delineating the extent and potential of Pakistan's coal reserves,estimates of which vary widely. The Geological Survey of Pakistan has recentlyestimated the country's total coal resources at 508 million tons (proven - 102m.t.; indicated - 217 m.t.; possible 189 m.t.), but these do not includeadditional possible reserves of 370 million tons in operating coal fieldswhich have not been subjected to any detailed geological investigation. 1/Studies should also be made to determine whether, with the utilization ofmodern mining techniques, some of the better and deeper situated reserves ofcoal could be economically utilized for local residential use, which wouldhave the additional benefit of alleviating some of the ill effects of uncheckedfirewood consumption.

Table 3.6

Coal Production and Imports

Production Imports Total Supply(000 tons)

FY65 1243 37.3 1280.3FY72 1214 32.2 1246.2FY79 1387 - 1387.0

The Supply of Nuclear Fuels

3.13 In 1976, the uranium resources of Pakistan at a cut-off grade of0.1% U 0 were calculated to be 150,000 tonnes of mineralized material contain-ing 18? Ponnes of uranium. The presence of uranium in the Neogene Siwaliksandstones of Dera Ghazi Khan has been known for several years but severalanomalies have also been located in the Potwar area near Islamabad. The mainagency responsible for the development of indigenous uranium resources is thePakistan Atomic Energy Commission, whose other responsibilities also includeplanning for the overall development of nuclear powered electricity generationin the country. So far, Pakistan's experience with nuclear electricitygeneration has been limited to a small 137MW heavy water reactor that has beenin operation at Karachi since 1971. This plant has contributed more than2,700 GWh to the KESC grid, but due to difficulties in obtaining adequate fuelsupplies its output has dropped from a peak of 610 GWh in FY76 to 106 GWh inFY79.

1/ See Annex 4, Table 9 for a field specific estimate of coal reserves.

- 26 -

The Supply of Electricity

3.14 Rapid increases in generating capacity and an increased relianceon hydro power have been the major characteristics of electricity supply inPakistan over the past two decades. In 1965, total generating capacity wasjust under 900 MW of which only 30 percent was based on hydro energy. Since

then, total capacity has nearly quadrupled to 3,353 MW and a much fasterincrease in hydro-based capacity to 1567 MW has raised its share in the totalto 47 percent. Because of higher plant utilization--60 percent as opposed to52 percent for thermal plants--the share of hydro energy in terms of units of

electricity generated has risen even higher to 58 percent of the FY79 total

figure of 14,174 GWh.

Table 3.7

Electricity Generation By Source

Hydro Thermal Nuclear Total

FY65 GWh 1362 1814 -- 3176% 42.9 57.1 -- 100

FY72 GWh 3679 3789 104 7572X 48.6 50.0 1.4 100

FY79 GWh 8252 5836 106 14174% 58.2 41.1 0.7 100

Annual averagegrowth rates

FY65-72 15.3 11.1 -- 13.2

FY72-79 12.2 6.4 0.2 9.4

Hydroelectricity

3.15 Efforts to harness the large hydroelectric potential of the Indus

and Jhelum rivers, which provide for almost all of the country's total pres-ently estimated economically feasible hydro potential of 20,000 MW, had beenan important element of national energy policy well before 1973, and thisstrategy has been given an added impetus by increases in the price of alter-native hydrocarbon fuels for thermal electricity generation. However, thelong gestation period required for the development of hydroelectric schemesimplies that any increases in the share of hydroelectricity in meeting thecountry's electricity requirement that has occurred in the past five years,is more the result of large investments made in this sector in the 1960's

- 27 -

than a response to post 1973 higher oil prices. To this extent, Pakistanwas fortunate in being able to reap in the 1970's, when hydro-generationhad become relatively more attractive, the benefits of earlier investmentsin developing the country's hydroelectric potential. 1/

3.16 The bulk of the existing hydro capacity is located at two sites--Tarbela (which accounts for 45 percent of the total) and Mangla (38 percent). 2/The remainder is shared by ten much smaller sites, all of which are alsolocated in the hilly northern part of the country. This geographical concen-tration of existing and potential hydroenergy sites away from the southernpart of the country which is the major market for electric power consumption,poses one of the problems with regard to the full utilization of Pakistan'shydroenergy resources. The long distances over which electricity must betransmitted from the place of generation to the place of consumption togetherwith inadequate distribution facilities, have resulted in high transmissionlosses and raised costs, and made even more important the concomittant develop-ment of an adequate high voltage transmission and distribution network. Twofurther considerations also need to be mentioned. The first of these relatesto the significant seasonal variation in the flow of the relevant rivers whichresults in large differences between installed and firm capacity for thegeneration stations. 3/ The second factor, about which little is known atpresent, is the relatively high siltation rates which may limit the life ofexisting and planned reservoirs; there are some estimates that the Tarbelareservoir will lose 90% of its capacity over the next fifty years and the oneat Mangla 30% over the same period. In spite of these limitations, hydroelec-tricity has developed as a major source of commercial energy. It continuesto provide one of the most promising avenues for the further development ofindigenous energy resources at both existing and new sites. 4/

Thermal Electricity

3.17 Thermal electricity is generated at 22 power stations in the centraland southern regions of the country, with a total capacity of 1649 MW. Theseplants vary in size from 1.5 MW to 265 MW, with the three largest stations--the natural gas power stations at Multan and Faisalabad, and the thermal powerstation at Guddu--accounting for 694 MW or 42% of the total. Since the early1960's, the main fuel for thermal electricity generation has been indigenousnatural gas, but prior to 1973 the system's reliance on oil had been increasing.Since then, the Government has acted to reduce the share of petroleum as a

1/ See Annex 4, Table 11 for a site-specific list of hydroelectricpotential.