nism update feb-apr 2013

Post on 20-Oct-2014

2.249 views

DESCRIPTION

TRANSCRIPT

Volume 4 / Issue 22

February-April 2013

2nd Annual Convocation

The 2nd Annual Convocation was held on April 29, 2013, to felicitate the successful students of the School for Securities Education, NISM. These candidates were from the Batch of 2011-12 of two programmes: the One-Year Full-time Post Graduate Programme in Securities Markets (PGPSM) and the One-Year Part-time Certificate in Financial Engineering & Risk Management (CFERM). A brief of this is given inside.

School for Regulatory Studies & Supervision of NISM conducted two programmes - “Securities Market Regulations - Anti Money Laundering Perspective” and “Financial Market Regulations” during Feb-Mar 2013. Forty two officers from SEBI and Enforcement Directorate and 115 officers from Indian Revenue Service attended the programmes, respectively. A brief of this is given inside.

After successful launch of the NISM-Series-V-B: Mutual Fund Foundation Certification Examination and NISM-Series-III-A: Securities Intermediaries Compliance (Non-Fund) Certification Examination during January, 2013, NISM has launched four new certification examinations during the period Feb-Apr, 2013. Details of these are given inside.

NISM has carried out a study on 'Trends in the Performance of the Corporate Sector'. A brief of this study is given in this issue.

As always, suggestions for improvements of the publication are welcome.

With best wishes

Shri Sandip GhoseDirector, NISM

Foreword

01

The 2nd Annual Convocation to felicitate the successful students of the School for Securities Education (SSE) was held on April 29, 2013. These candidates were from the Batch of 2011-12 of two programmes: One-Year Full-time Post Graduate Programme in Securities Markets (PGPSM) and the One-Year Part-time Certificate in Financial Engineering & Risk Management (CFERM). The event saw 180 attendees including students, their family, alumni, officers from key institutions, corporates, faculty and staff of NISM. It was covered by Bloomberg.

Shri Uday Kotak, Executive Vice Chairman and Managing Director-Kotak Mahindra Bank Ltd. was the Chief Guest. In his convocation address, he stressed on the dangers of over-leverage, the need for simplicity as opposed to over-engineering, humility and following one's dharma. He also appreciated NISM's passion for education in the field of securities markets.

Shri P K Nagpal, Executive Director-SEBI and immediate-past Director of NISM, was the Presiding Officer on the occasion. Both Shri Kotak as well as Shri Nagpal are also Members of the Board of Governors of NISM. Accompanying them on the dais, on the occasion, were Shri Sandip Ghose, Director-NISM and Shri G P Garg, Registrar-NISM.

Shri Ghose provided an activity report of NISM during the year gone by. He also made a mention about the strength of SSE in terms of faculty capabilities in curriculum and research. Shri Nagpal, advised the budding professionals to enjoy their work in order to bring in the required passion. While emphasizing the importance of regulation in financial markets, he praised NISM's unique educational process and encouraged inculcation of managerial skills among students. He distributed the certificates to the successful students of PGPSM and CFERM. Shri Garg proposed the vote of thanks and the ceremony concluded with the singing of the National Anthem

2ndAnnualConvocation

02

Redress of investor grievances through SEBI Compliances Redress System (SCORES)

Corporate Bonds and Government Securities as collateral

Product Labeling in Mutual Funds

▪

▪

▪

▪

(CIR/OIAE/1/2013 dated 17-04-2013)

Pursuant to the provisions of Section 15C SEBI Act, 1992, all listed companies are hereby called upon to redress the grievances of investors and inform them within 30 days of the complaints. The details of investor grievances relating to the respective companies can be accessed through the respective SCORES user ID and password of each company.

Failure by companies to file Action Taken Reports under SCORES within 30days of date of receipt of the grievance may also attract the provisions of Section 15A(a) of the SEBI Act, 1992.

The Hon'ble Finance Minister, in his announcement in the Union Budget for the year 2013 -14, has proposed, inter-alia, to permit FIIs to use their investment in corporate bonds and Government securities as collateral to meet their margin requirements towards their transactions on the recognized Stock Exchanges in India.

Reserve Bank of India vide RBI/2012-13/439 A.P. (DIR Series) Circular No. 90 dated March 14, 2013 has permitted FIIs to use, in addition to already permitted collaterals, their investments in corporate bonds as collateral in the cash segment and government securities and corporate bonds as collaterals in the F&O segment.

In light of the above, henceforth FIIs are permitted to offer the following collaterals - government securities, corporate bonds, cash and foreign sovereign securities with AAA ratings, for their transactions in both cash and F&O segments.

(CIR/IMD/DF/5/2013 dated 18-03-2013)

In order to address the issue of mis-selling, and to provide investors an easy understanding of the kind of product/ scheme they are investing in and its suitability to them, SEBI has decided that all the mutual funds shall 'Label' their schemes on the parameters as mentioned under:

Nature of scheme such as to create wealth or provide regular income in an indicative time horizon (short/ medium/long term).A brief about the investment objective (in a single line sentence) followed by kind of product in which investor is investing (Equity/Debt).Level of risk, depicted by colour code boxes as under:

• Blue - principal at low risk.• Yellow - principal at medium risk.•Brown - principal at high risk.The colour codes shall also be described in text beside the colour code box.

A disclaimer that investors should consult their financial advisers if they are not clear about the suitability of the product.

(CIR/MRD/DRMNP/9/2013 dated 20-03-2013)

INITIATED BY SEBI

Regulatory Changes

03

In consultation with Stock Exchanges and the associations of stock brokers, SEBI has decided:

The Stock Exchange or the Clearing Corporation, as the case may be, shall, in consultation with SEBI, formulate a policy for annual inspection of their members in various segments and follow up action thereon. The policy shall also cover various kinds of risks posed to the investors and market at large on account of the activities/business conduct of their members.

The Stock Exchange or the Clearing Corporation, as the case may be, shall conduct inspection of their members in various segments in terms of the above policy and in case of members who hold multiple memberships of the exchanges, the Stock Exchanges shall establish an information sharing mechanism with one another on the important outcome of inspection in order to improve the effectiveness of supervision.

(CIR/IMD/DF/04/2013 dated 15-02-2013)

SEBI has decided to designate GDS of Banks as gold related instrument. Investment in GDS of Banks by Gold ETFs of mutual funds is subject to following conditions:

The total investment in GDS will not exceed 20% of total asset under management of such schemes. Before investing in GDS of banks, mutual funds shall put in place a written policy with regard to investment in GDS with due approval from the Board of the Asset Management Company and the Trustees. The policy should have provision to make it necessary for the mutual funds to obtain prior approval of their trustees for each investment proposal in GDS of any Bank. The policy shall be reviewed by mutual funds, at least once a year.Gold certificates issued by Banks in respect of investments made by Gold ETFs in GDS shall be held by the mutual funds only in dematerialized form.

(CIR/MRD/DP/05/2013 dated 08-02-2013)

SEBI has decided to permit stock exchanges to introduce Liquidity Enhancement Schemes (LES) to enhance liquidity of illiquid securities in their Equity Cash Market.

LES may be introduced in any of the following securities: • Securities having a mean impact cost greater than or equal to 2% for an order size of ̀ 1 lakh, where mean impact cost

of the security on the stock exchange is calculated over the past 60 trading days. • Securities introduced for trading in the “permitted to trade” category.

LES may be continued till such time as the security achieves mean impact cost of less than 2% for an order size of ` 1 lakh on the stock exchange during the last 60 trading days.

Discontinuation of LES shall be done after advance notice of 15 days.

(CIR/IMD/FIIC/3/2013 dated 08-02-2013)

The Reserve Bank of India vide circular RBI/2012-13/391, dated January 24, 2013, had enhanced the limit for investment by FIIs in the Government Debt Long Term category by US$ 5 billion to US$ 15 billion and the Corporate non-infrastructure debt category by US$ 5 billion.

▪

▪

Gold Exchange Traded Fund Scheme (Gold ETFs) investment in Gold Deposit Scheme (GDS) in Banks

▪▪

▪

Liquidity Enhancement Schemes for Illiquid Securities in Equity Cash Market

Increase in FII debt limit for Government and Corporate Debt category

04

Core Investment Companies (CICs) - Guidelines on Investment in Insurance

Foreign investment in India by SEBI registered FIIs in Government Securities and Corporate

Standardization and Enhancement of Security Features in Cheque Forms/Migrating to CTS 2010 standards

▪

▪

(RBI/2012-2013/466 dated 01-04-2013)

RBI has decided to permit CICs to set up a joint venture company for undertaking insurance business with risk participation, subject to safeguards. In view of the unique business model of CICs, RBI has issued a separate set of guidelines for their entry into insurance business.

While the eligibility criteria, in general, are similar to that for other NBFCs, no ceiling is being stipulated for CICs in their investment in an insurance joint venture. Further it is clarified that CICs cannot undertake insurance agency business.

CICs exempted from registration with RBI do not require prior approval provided they fulfill all the necessary conditions of exemption as provided under/ in CC No.206 dated January 05, 2011. Their investment in insurance joint venture would be guided by IRDA norms.

(RBI/2012-2013/465 dated 01-04-2013)

RBI has decided to merge the existing debt limits for investments by FIIs and long term investors in Government securities and non-convertible debentures (NCDs) / bonds issued by an Indian company, into two broad categories as under:

▪ Government Debt limit: Government securities of USD 25 billion by merging the existing sub-limits under Government securities [(a)USD 10 billion for investment by FIIs in Government securities including Treasury Bills and (b) USD 15 billion for investment In Government dated securities by FIIs and long term investors]; and

▪ Corporate Debt Limit: Corporate debt of USD 51 billion by merging the existing sub-limits of corporate debt [(a) USD 1 billion for Qualified Foreign Investors (QFIs), (b) USD 25 billon for investment by FIIs and long term investors in non-infrastructure sector and (c) USD 25 billion for investment by FIIs/QFIs/long term investors in infrastructure sector].

(RBI/2012-2013/44 dated 18-03-2013)

On a review of the progress made by banks so far in migration to CTS-2010 standard cheques and in consultation with a few banks and Indian Banks Association, RBI has decided to put in place the following arrangements for clearing of residual non-CTS-2010 standard cheques beyond the cutoff date of March 31, 2013.

All cheques issued by banks (including DDs / POs issued by banks) with effect from the date of this circular shall necessarily conform to CTS-2010 standard.

Banks shall not charge their savings bank account customers for issuance of CTS-2010 standard cheques when they are issued for the first time. However, banks may continue to follow their existing policy regarding cheque book issuance for additional issuance of cheques, in adherence to their accepted Fair Practices Code.

INITIATED BY RBI

05

Permission of Insurers to invest in Category I Alternative Investment

▪

▪

▪

▪

▪

(IRDA/F&I/INV/CIR/054/03/2013 dated 18-03-2013

In light of SEBI Alternative Investment Fund Regulations, 2012, IRDA permits Insurers to invest in Alternative Investment Funds subject to the following:

The investments in Category I Alternative Investment Funds are permitted under the Head “Other Investments”. Further, such Investments should be restricted to Infrastructure Funds and SME Funds as defined in the Alternative Fund Regulations.

Insurers should ensure that such Category I Funds should not invest in securities of companies incorporated outside India as Insurers are prohibited for investment of funds outside India vide sec. 27C of the Insurance Act, 1938.

The sponsor of such Alternative Investment Fund should not be in the promoter group of the Insurer.

The Fund shall not be managed by an Investment Manager who is either directly or indirectly controlled or managed by the Insurer or its promoters.

The Investments in Alternative Investment Funds should be clubbed with the investments in Venture Funds and reported to the Authority in the quarterly Investment returns under the category code 'OVNF'.

INITIATED BY IRDA

▪

▪

All residual non-CTS-2010 cheques with customers will continue to be valid and accepted in all clearing houses [including the Cheque Truncation System (CTS) centers] for another four months up to July 31, 2013, subject to a review in June 2013.

Cheque issuing banks shall make all efforts to withdraw the non-CTS-2010 Standard cheques in circulation before the extended timeline of July 31, 2013 by creating awareness among customers through SMS alerts, letters, display boards in branches/ATMs, log-on message in internet banking, notification on the web-site etc.

Circular on replacing the existing facility of 'Phased Withdrawal' with 'Deferred Withdrawal’(PFRDAI2013/6/PDEX/5 dated 11-03-2013)

PFRDA has decided to replace the “Phased Withdrawal” option currently available with a “Deferred withdrawal” option whereby the subscriber can time the lump sum withdrawal allowed under NPS at the time of exit, with immediate effect.

Under the Deferred withdrawal facility, the subscribers at the time of exit from National Pension System (NPS) can exercise an option to defer the withdrawal of eligible lump sum withdrawal and stay invested in the NPS. However, it may be noted that no fresh contributions are accepted and also no partial withdrawals are allowed during such a period of deferment. The subscriber can withdraw the deferred lump sum amount at any time before attaining the age of 70 years by giving a withdrawal application or notice. If no such notice is given, the accumulated pension wealth would be automatically monetized and credited to his bank account upon attaining the age of 70 years.

INITIATED BY PFRDA

06

Activities at Nism

SEBI Financial Education Resource Persons Programme

SCHOOL FOR INVESTOR EDUCATION AND FINANCIAL LITERACY (SIEFL)

No. of Resource Personsempanelled and trained

DatesVenue

Patna

Ahmedabad

Lucknow

Bhubaneshwar

Chandigarh

Guwahati

42

68

51

53

48

46

Dec 26-30, 2012

Jan 13-16, 2013

Jan 28-31, 2013

Feb 9-13, 2013

Feb 23-27, 2013

March 17-20, 2013

Ahmedabad 13-16th Jan 2013

NISM organised new empanelment of SEBI Financial Education Resource Persons at Patna, Ahmedabad, Lucknow, Bhubaneshwar,Chandigarh and Guwahati from December 2012 to March 2013. A total of 308 new Resource Persons were empanelled and trained at these centres as detailed below.

Shri Gyan Bhushan, Chief Gen Manager, SEBI distributing certificates to one of the newly empanelled Resource Persons.

Financial Literacy Programs in Schools

From December 2012 to March 2013, Teachers’ Training Programs were conducted in 18 locations covering 893 teachers of schools in Kerala, Karnataka, Tamilnadu, Andhra Pradesh, Mumbai, and Navi Mumbai. They were trained in basic financial literacy concepts viz. financial planning, banking, stock market, insurance and so on. This in turn would be passed on to the students in their respective schools.

07

SCHOOL FOR REGULATORY STUDIES & SUPERVISION

Securities Market Regulations - Anti Money Laundering Perspective

The School for Regulatory Studies & Supervision organised a program on “Securities Market Regulations – Anti Money Laundering Perspective” in February, 2013 that was attended by 42 officers from SEBI and Enforcement Directorate. It was inaugurated by Shri Sunil Sawhney, Special Director, Enforcement Directoratein a function attended by Shri P K Nagpal, then Director, NISM, Shri Samir Bajaj, Joint Director, Enforcement Directorate and Shri K Sukumaran, Dean, SIEFL & SRSS, NISM. Some of the important topics covered in the program were, Regulatory Environment in Securities Market, Regulations under FEMA as relevant to securities market, Foreign Investments by FIIs/QFIs, AML and KYC Issues, etc. The programme came to an end with valedictory session attended by Shri G P Garg, Registrar, NISM.

Participants of the programme SECURITIES MARKET REGULATIONS - ANTI MONEY LAUNDERING PERSPECTIVE

Financial Market Regulations

The program on “Financial Market Regulations” was organised by NISM for the Indian Revenue Service (IRS) Officers on the request from National Academy of Direct Taxes (NADT), Nagpur. The program, a workshop cum exposure visit, was attended by 115 officers from IRS between March 18-22, 2013 at Navi Mumbai. The program started with a session on 'Securities Markets' followed by sessions on 'Regulatory Environment in Securities Market', 'Role of Intermediaries in Securities Markets', 'Regulatory Environment in Banking Market', 'Risk Management in Securities Market', 'Banking Operations – An Overview', and many more. The participants visited SEBI, RBI, BSE, NSE and NSDL wherein they got an exposure to the functioning of each organisation.

08

SCHOOL FOR CERTIFICATION OF INTERMEDIARIES (SCI)

Examination Update

NISM Certification Examinations are available through all NISM, NSE, MCX-SX and BSE Test Centers. For further

details please visit www.nism.ac.in.

1. Launch of NISM-Series-XI: Equity Sales Certification Examination

NISM has launched the NISM-Series-XI: Equity Sales Certification Examination on March 7, 2013. This

examination seeks to create a common minimum knowledge benchmark for all persons involved in equity sales

in order to enable a better understanding of equity markets, better quality investor service, operational process

efficiency and risk controls.

2. Launch of NISM-Series-XII: Securities Markets Foundation Certification ExaminationNISM has launched the NISM-Series-XII: Securities Markets Foundation Certification Examination on March 21, 2013. This examination aims to impart basic knowledge about the Indian Securities Markets and different rules and regulations governing the securities markets. This examination is a voluntary examination for entry level professionals, who wish to make a career in the securities markets.

3. Launch of NISM-Series-IX: Merchant Banking Certification ExaminationNISM has launched the NISM-Series-IX: Merchant Banking Certification Examination on March 21, 2013. The examination seeks to create a common minimum knowledge benchmark for employees working with SEBI registered Merchant Bankers and performing various SEBI regulated functions such as those relating to IPO, FPO, Open Offer, Buy-Back, Delisting etc.

4. Launch of NISM-Series-V-C: Mutual Fund Distributors (Level 2) Certification ExaminationNISM has launched the NISM-Series-V-C: Mutual Fund Distributors (Level 2) Certification Examination on April 16, 2013. This is a voluntary higher level examination, for those candidates who wish to assess themselves against higher standards of overall expertise related to mutual funds sales, distribution and advisory functions.

5. SEBI's Notification for NISM Certification ExaminationsSEBI has notified the following certification examinations of NISM under regulation 3 of SEBI (CAPSM) Regulations, 2007:

(a) NISM-Series-VIII: Equity Derivatives Certification Examination [vide notification LAD-NRO/GN/2012-13/30/5474

dated January 11, 2013]

(b) NISM-Series-III-A: Securities Intermediaries Compliance (Non-Fund) Certification Examination [vide notification

LAD-NRO/GN/202-13/33/1103 dated March 11, 2013]

09

Consolidated Status Report ( Period: As on April 28, 2013)

NISM Certification Examination

SrNo.

NISM EXAMINATIONTotal Candidates

EnrolledTotal Candidates

Appeared

Mutual Fund Distributors (Launched on 01/06/2010)

RTA - Mutual Fund(Launched on 03/08/2009)

Currency Derivatives

(Launched on 15/05/2009)

Currency Derivatives - Gujarati

(Launched on 01/11/2012)

Securities Intermediaries Compliance(Non-Fund)(Launched on 28/01/2013)

Interest Rate Derivatives(Launched on 17/05/2010)

Mutual Fund Distributors - Gujarati(Launched on 01/06/2010)

Mutual Fund Distributors - Hindi(Launched on 01/06/2010)

Currency Derivatives - Hindi

(Launched on 01/11/2012)

RTA - Corporate

(Launched on 03/08/2009)

Mutual Fund Foundation(Launched on 14/01/2013)

Depositories Operations(Launched on 21/02/2011)

Securities Operations and Risk Management(Launched on 22/11/2010)

Equity Derivatives(Launched on 08/10/2012)

Merchant Banking(Launched on 21/03/2013)

Equity Sales Certification Examination(Launched on 07/03/2013)

Securities Markets Foundation(Launched on 21/03/2013)

01

02

03

04

05

06

07

08

09

10

11

13

14

15

16

17

18

PassPercentage

PassPercentage

Mutual Fund Distributors (Level 2)(Launched on 16/04/2013)

12

42%

25%

8%

71%

60%

85%

18%

42%

17%

16%

91%

53%

77%

56%

100%

88%

100%

0%

Total

120112

5819

54104

8

27

2218

53

657

654

961

94

27886

14904

7258

8

11

11

2

244787

120116

5413

49858

8

26

2019

34

471

549

794

66

25433

14015

6775

3

8

4

0

225592

50282

3261

2

2

1442

29

84

91

127

60

13452

10768

3827

3

7

4

20762

0

104203

10

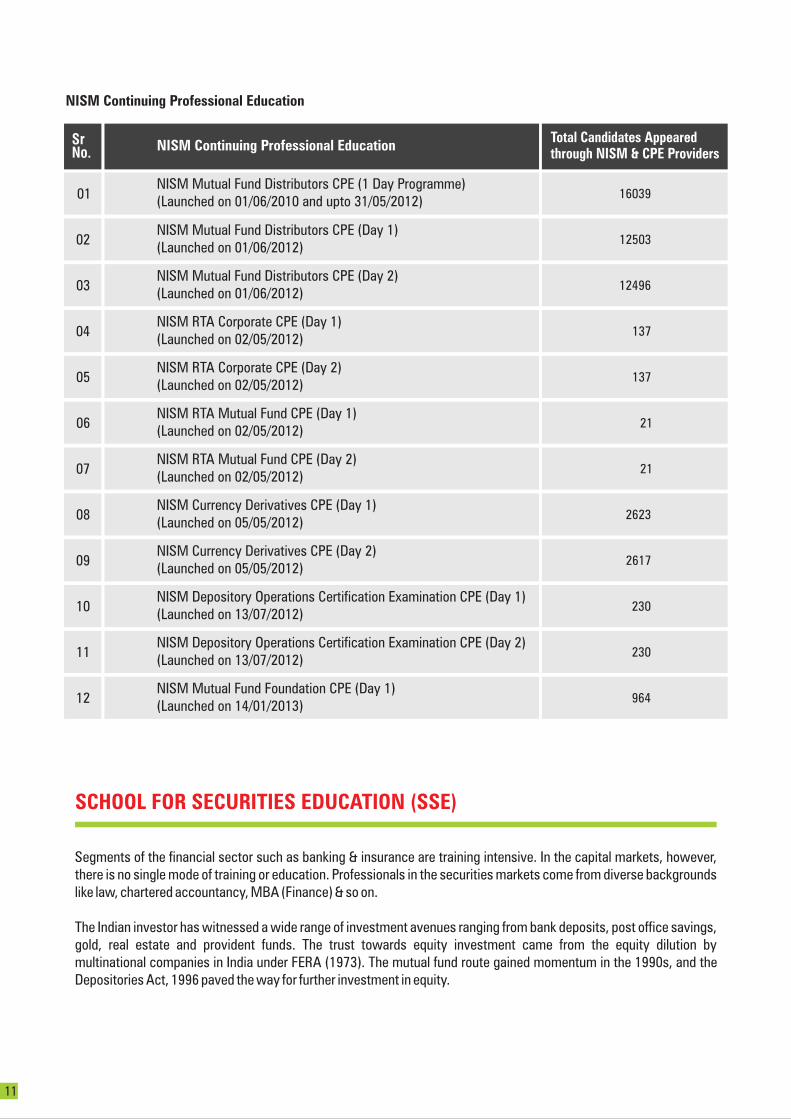

SCHOOL FOR SECURITIES EDUCATION (SSE)

Segments of the financial sector such as banking & insurance are training intensive. In the capital markets, however, there is no single mode of training or education. Professionals in the securities markets come from diverse backgrounds like law, chartered accountancy, MBA (Finance) & so on.

The Indian investor has witnessed a wide range of investment avenues ranging from bank deposits, post office savings, gold, real estate and provident funds. The trust towards equity investment came from the equity dilution by multinational companies in India under FERA (1973). The mutual fund route gained momentum in the 1990s, and the Depositories Act, 1996 paved the way for further investment in equity.

NISM Continuing Professional Education

SrNo. NISM Continuing Professional Education

01

02

03

04

05

06

07

08

09

Total Candidates Appearedthrough NISM & CPE Providers

NISM Mutual Fund Distributors CPE (1 Day Programme)(Launched on 01/06/2010 and upto 31/05/2012)

NISM Mutual Fund Distributors CPE (Day 1)(Launched on 01/06/2012)

NISM Mutual Fund Distributors CPE (Day 2)(Launched on 01/06/2012)

NISM RTA Corporate CPE (Day 1)(Launched on 02/05/2012)

NISM RTA Corporate CPE (Day 2)(Launched on 02/05/2012)

NISM Currency Derivatives CPE (Day 1)(Launched on 05/05/2012)

NISM Currency Derivatives CPE (Day 2)(Launched on 05/05/2012)

NISM RTA Mutual Fund CPE (Day 1)(Launched on 02/05/2012)

NISM RTA Mutual Fund CPE (Day 2)(Launched on 02/05/2012)

10

11

12

NISM Depository Operations Certification Examination CPE (Day 1)(Launched on 13/07/2012)

NISM Depository Operations Certification Examination CPE (Day 2)(Launched on 13/07/2012)

NISM Mutual Fund Foundation CPE (Day 1)(Launched on 14/01/2013)

16039

12503

12496

137

137

2623

2617

21

21

230

230

964

11

Trends in the Performance of the Corporate Sector

Quarterly Corporate Results are one of the indicators of economic activity in the country. A study on Quarterly Earnings of 100 companies (Nifty 50 companies and Nifty Junior 50 companies) is carried out with a view to obtain broad trends in the performance of companies and various sectors for Quarter October-December 2012 as compared to October-December 2011. As on February 15, 2013, all the 99 companies reported earnings except Mphasis Limited, which follows a different year/quarter ending.

Across All 99 companies, PAT (Profit after Tax) has grown 24% over the corresponding Quarter in the previous year. This is achieved with the help of 10% growth in Sales, 9% growth in Operating Profit and 14% growth in Other Income. These 99 companies are classified into 13 sectors. Out of 13 sectors, 9 sectors have reported an increase in PAT, significant observations are Pharma (257%), Engery (45%) and FMCG (20%). Out of 13 sectors, 4 sectors have reported a decline in PAT, i.e. Realty (-92%), PSE (-18%), Auto (-13%) and Metal (-8%).

Nifty P/E ratio increased to 18.68 from 16.85 a year back, in-spite of increase in PAT by 24%. This could imply that Nifty companies attracted more investments on a perception of improved earnings prospects. As against the Nifty P/E of 18.68 , the P/E of Pharma was the highest (44.74) and the P/E of PSU Banks was the lowest (8.07).

Research at NISM

Over the last three decades, the securities markets have been institutionalized through several structures. The School for Securities Education has a team of dedicated academicians that impart knowledge based on in-depth research and constant interaction with industry and policy-makers at the highest level. This experience is interwoven with skills and experiential learning. The curriculum is carefully designed and delivered by academicians, policy-makers and practitioners based on global benchmarks.

The following are the three programmes conducted by SSE:

For full details, please visit www.nism.ac.in

Post Graduate Programme in

Securities Markets (PGPSM)One-year full time programme or fresh graduates or experienced graduates.

Certificate in Financial

Engineering and Risk

Management (CFERM)

One-year part time programme for working executives. Format A is held on

Saturday evenings and Sundays. Format B is held in 10-day modules

four times in a year.

Certificate in Securities

Law (CSL)A six-month programme for working executives across 26 Saturdays

12

Taxation and Securities Markets

Prof. Sunder Ram Korivi, Dean - SSE and SSIR, NISM

The Tobin Tax (a type of tax proposed by Nobel Laureate James Tobin) has increasingly become a tool being applied by

policy-makers. It is based on the principle of 'polluter pays'. Those who contribute to pollution (volatility, in this case)

ought to pay for it. In the financial markets, speculators and traders have a higher churn rate than, say, a life-insurance

company, pension fund or a Warren Buffet-like investor. Hence, a transaction tax would hurt speculators and traders

more. Furthermore, since retail investors generally do not trade in derivatives, a transaction tax on derivatives falls on

institutional and rich investors. For this reason, a transaction tax is also termed as a Robin Hood tax - taxing the rich to

finance the poor. In recent times, Brazil, an export-oriented economy, introduced an anti-volatility transaction tax

aimed to keep FII flows at bay and prevent an undue strengthening of its currency.

In the 1980s and thereafter, countries made serious attempts to enhance trade relations. There are over 2000 Double Tax Avoidance Treaties (DTAT) of a bilateral nature (India has entered into 85 treaties). There are agreements between countries such as Developed-Developed, Developed-Developing and Developing-Developing. Tax arbitrage becomes rich with opportunity where the tax differences are the highest. This raises the popularity to tax havens, where the rates of taxation are zero to low. Following the rise of terrorism and its financing in the 2000s, the Financial Action Task Force (FATF) was initiated. FATF was mandated to eradicate the scourge of terror financing and brought several tax havens to question. Government action has now shifted to the unfair use of tax havens for purely economic offences. The several bilateral Tax Information Exchange Agreements (TIEA) that prevail are to be viewed in such light.

Gita Gopinath of Harvard has been advising the French government on fiscal measures to improve their finances. Being a member of the Euro-zone, France (like other members of the Euro-zone) suffers from currency and interest-rate rigidities. The only way to gain financial strength is to raise new taxes. This provides the backdrop against which France and ten other countries in the Euro-zone have raised a Financial Transaction Tax.

Tax havens are likely to come under increasing focus, especially owing to the moderation in the effective tax rates from 32% to 24% over the past decade in non tax haven countries. Under such a situation, tax havens play spoil-sport to the tax-mobilization efforts of other nations. Thus, Robin Hood-style taxes seek to mobilize funds from the haves for the benefit of the have-nots.

The low tolerance to tax havens views them in fresh light: the doctrine of 'tax minimization' questions the doctrine of 'tax avoidance' on ethical-technical grounds. Investments are international, but taxes are domestic, leaving loopholes in the hands of clever lawyers from British Virgin Islands to Samoa. This view has increasingly dominated OECD thinking, G20 thinking, and the thinking among tax authorities in India. It is now contextually clearer as to why the Transaction Taxes, a super-rich tax (albeit as a surcharge), GAAR and the aggressive posturing of the Indian tax authorities.

According to William Poole of Cato Institute, tax-deductibility of interest has led to the leverage boom and the bust of the financial system. It is time for tax authorities to have a close re-look at the deductibility of not only interest, but also other items such as royalty and fees for technical services, especially those routed through tax havens. As Andrew Sheng (formerly of the Hong Kong Monetary Authority) mentions, finance is a good servant but a bad master. Cyprus is an example of an outsized financial sector, in relation to its real sector.

Articles

13

On the whole, the world seems to have come around to the principle (known as the Ramsay Principle) that a device whose sole intention is to avoid tax, without commercial substance, is questionable, and must be pursued to bear its fair share to the exchequer. History tells us that players in the financial sector may lie low until public outrage subsides and make fresh attempts for a retention of the status quo.

Mr. Naresh Shabbani, Manager, F&A, NISMKautilya's Arthashastra, an ancient and revered Indian literature on statesmanship, detailed the four duties of the king towards his subjects viz Raksha (Protection), Vriddhi (Enhancement), Palana (Maintenance) and Yogakshema (Safeguard). In the context of corporates where the Board of Directors dons the role of king and the shareholders form the subjects, the duties are being reoriented to represent the objectives of corporate governance:1.Protection of shareholder's wealth from devaluation2.Enhancement of the shareholder's wealth by prudent investments3.Maintenance of the shareholder's wealth by optimum utilisation of resources4.Safeguard of the interests of the shareholders by acting as a trustee

Ccorporate governance also deals with rights of minority shareholders vis-à-vis majority shareholders as well as duties towards other stakeholders such as customers, employees, environment, regulators, creditors, suppliers and the society at large.

There is an ever growing realization among policy-makers in India about the importance of corporate governance in improving the investment climate and also in promoting development of vibrant and transparent capital markets. Scams and other frauds have adversely affected the confidence of common investors in a country where less than 3% of the population invest their savings into stock markets.

It has also dawned upon the corporate sector that sincere efforts have to be made to address concerns of all stakeholders in order to achieve sustainable development in a country where growing disparity between the haves and the have-nots threaten to disrupt the very ecosystem in which they operate. Additionally, there is increasing research pointing to a direct relation between the levels of corporate governance in a company to its stock performance.

Indian corporate sector presents a salient characteristic that may call for a unique corporate governance code in terms of dealing with the high concentration of ownership by family-owned groups or the government. However, the basic principles that any governance code addresses remains separation of governance from management, fairness, transparency, accountability, risk management, probity and sustainable growth over long-term.

The main regulators of corporate governance in India are the Ministry of Corporate Affairs (MCA) and the SEBI. Although the Companies Act, 1956 provided a basic framework for regulation of all companies, the MCA vide Companies Bill, 2012 has inserted detailed provisions to strengthen corporate governance in India. Additionally, the ministry has issued Corporate Governance Voluntary Guidelines, 2009 to encourage highest standards of corporate governance through voluntary adoption.

On the other hand, SEBI addresses corporate governance in all listed companies through clause 49 of the listing agreement that contains 1) mandatory provisions - those standards which are absolutely essential and do not require legislative amendments and 2) non mandatory provisions – those standards which are desirable but require changes in law.

However, implementation of rules and regulations in letter and in spirit is the need of the hour for India to shine as an epitome of corporate governance haven.

Corporate Governance in India: A round-up

14

Certificate in Securities Law (CSL):

Top-notch faculty comprising of practitioners, regulators, academicians

Innovative teaching methods including cases, field visits, exposure to policy-makers

Good infrastructure and specialized library

High-quality class mix

Convenient format: 26 Saturdays (10:00 am to 5:00 pm), delivered at Nariman Point, Mumbai

▪

▪

▪

▪

▪

▪

Contemporary curriculum, from the fusion between Law and Economics

Eligibility: Graduation. Background in Law or Finance will be preferable.

Selection Process: Interview and Essay

Become a specialist in securities market laws and make career in compliance, reporting, investment banking, securities

market operations, consulting, legal process analytics, etc.

Six-month part-time programme for working executives

NISM Bhavan, Plot No. 82, Sector 17, Vashi, Navi Mumbai - 400 703Phone: 022 66735100-05 | Fax: 022 66735110www.nism.ac.in

National Institute of Securities Markets (An Educational Initiative by SEBI)

Last date for application: June 26, 2013