minimum energy efficiency standards (mees). minimum energy efficiency standards (mees) the...

TRANSCRIPT

1

Minimum Energy Efficiency Standards (MEES)

The implications for

rent reviews, lease renewals and valuation

2

Contents

1.0 Introduction and acknowledgements ------------------------------------------------------------------------------ p2

2.0 MEES and the hypothetical effects on rents ---------------------------------------------------------------------- p8

3.0 Summary of the Regulations ------------------------------------------------------------------------------------------ p11

4.0 Valuation considerations ---------------------------------------------------------------------------------------------- p18

5.0 Introduction to the case study --------------------------------------------------------------------------------------- p23

6.0 The case study ----------------------------------------------------------------------------------------------------------- p27

7.0 Case study analysis ---------------------------------------------------------------------------------------------------- p32

8.0 Conclusions --------------------------------------------------------------------------------------------------------------p36

9.0 Addendum -------------------------------------------------------------------------------------------------------------- p42

10.0 About the authors ------------------------------------------------------------------------------------------------p43

3

4

ACKNOWLEDGEMENTS arbnco ltd would like to thank Dr Paul McNamara, Ian Feltham and Sue Elwood for their extensive comments on earlier drafts of this paper. Dr Paul McNamara Paul is a former Director and Head of Research at PRUPIM (now M&G Real Estate) and is now a consultant through his company Linden Parkside. He was Chairman of the Investment Property Forum 2005-2006, becoming a Life Member in 2007. He is also an Honorary Fellow, past President and past Chairman of the Society of Property Researchers; a Visiting Professor at Oxford Brookes University; a former non-executive director of IPD Holdings Ltd; and a past chair of property working groups at the IIIGCC and UNEP FI. He was awarded an OBE for services to the property industry in 2003, a lifetime achievement award from IPE magazine in 2008, and an Honorary Doctorate from Kingston University for services to responsible property investment in 2014. Ian Feltham Ian is a Fellow of the Royal Institution of Chartered Surveyors (RICS) and a qualified arbitrator. He is a director at surveyors HNG. Before joining HNG in 2007, Ian was a Senior Director with CBRE. He has specialized for over 25 years in the Landlord and Tenant sector, mainly dealing with offices in the South East of England and Central London. Sue Ellwood Sue is a Chartered Surveyor and an associate at HNG. Throughout her career, Sue has specialized in a wide range of rent reviews, lease renewals and valuations of commercial properties, predominantly offices located in London and the south east of England. DISCLAIMER: Neither arbnco Ltd or the authors of this paper provide any guarantee that these findings will be realised.

5

Section 1: the scope and focus

of this report

6

Purpose and scope of this report The purpose of this paper is to review the implications of the Energy Efficiency (Private Rented Property) (England and Wales) Regulations 2015, better known as the Minimum Energy Efficiency Standards (MEES) for commercial property values. It is intended to stimulate debate by providing an informed opinion of the possible effect of the regulations, particularly with effect to:

1. Rent reviews 2. Statutory lease renewals

A summary of the regulations is contained within this paper. However, for reasons of brevity we cannot provide an exhaustive review, and those seeking further details should refer to the regulations made on 26th March 2015, and the Government response to its consultation on regarding these regulations published on 22nd July 20141. For similar reasons, while some of the text over the following pages has been taken verbatim from the Government’s response and/or the regulations, much has had

to be summarised. Throughout this document, we offer commentary or analysis over how the regulations could be interpreted. Following an executive summary, the paper summarises the regulations, looks at the potential valuation considerations, and then explores these through an in-depth case study which outlines the potential effect of the regulations on rental and capital values, both now and in the future. During the drafting of this paper, the Government announced that no further funding will be made available to the Green Deal Finance Company. The Green Deal finance mechanism had been an integral part of the Energy Act 2011, which is the primary legislation for the MEES regulations. However, as Green Deal finance has never been available for non-domestic property, this recent announcement does not alter the findings of this paper.

1 https://www.gov.uk/government/consultations/private-rented-sector-energy-efficiency-regulations-domestic

7

Executive Summary

This paper considers the implications of the Energy Efficiency (Private Rented Property) (England and Wales) Regulations 20152, better known as the Minimum Energy Efficiency Standards (MEES) on rent reviews and statutory lease renewals, and the knock-on effects of this on commercial property values. As of 1st April 2018, a non-domestic property cannot be let unless it complies with the regulations. These place a requirement on landlords to ensure their properties comply with MEES, where the minimum standard will be set at an E rating (Energy Performance Certificate). If a property fails to meet this minimum standard, an assessment must be undertaken to identify relevant energy efficiency improvements. These improvements must then be implemented before the property can

2 http://www.legislation.gov.uk/ukdsi/2015/9780111128350/contents

be let, even if the EPC rating does not improve. Clearly, in many cases, there will be a financial cost to compliance, and this should be understood and considered in the context of rental valuations at rent review and lease renewal. MEES was introduced by the Energy Act 2011 and has been well sign-posted. As such, the property industry has had time to debate its effects, and the current expectation is that the incoming regulations could potentially suppress rental levels at rent review and lease renewal. If rental growth is suppressed, then, all other things being equal, growth in capital values will likewise be suppressed. Further, if evidence emerges that MEES affects rental values, and the property in question is thought to be at risk form this at a future rent review/lease renewal, then the yield could be

adjusted for an investment sale in expectation of a reduced rental growth rate following a future leasing event. This could also potentially suppress capital values further. This expectation of rental suppression could manifest itself through both the complexities and nuances of rent review and lease renewal negotiations, or through transactional evidence becoming available, showing buildings that are compliant with MEES achieving higher rents or sale prices than those that are not. Such hypotheses are not new. Where this paper differs is that, for the first time, arbitrators and solicitors have been engaged to identify and quantify this risk, using a realistic case study of a building and lease. The aim of this paper is therefore to determine whether the risks to value are real and, if so, to what extent.

8

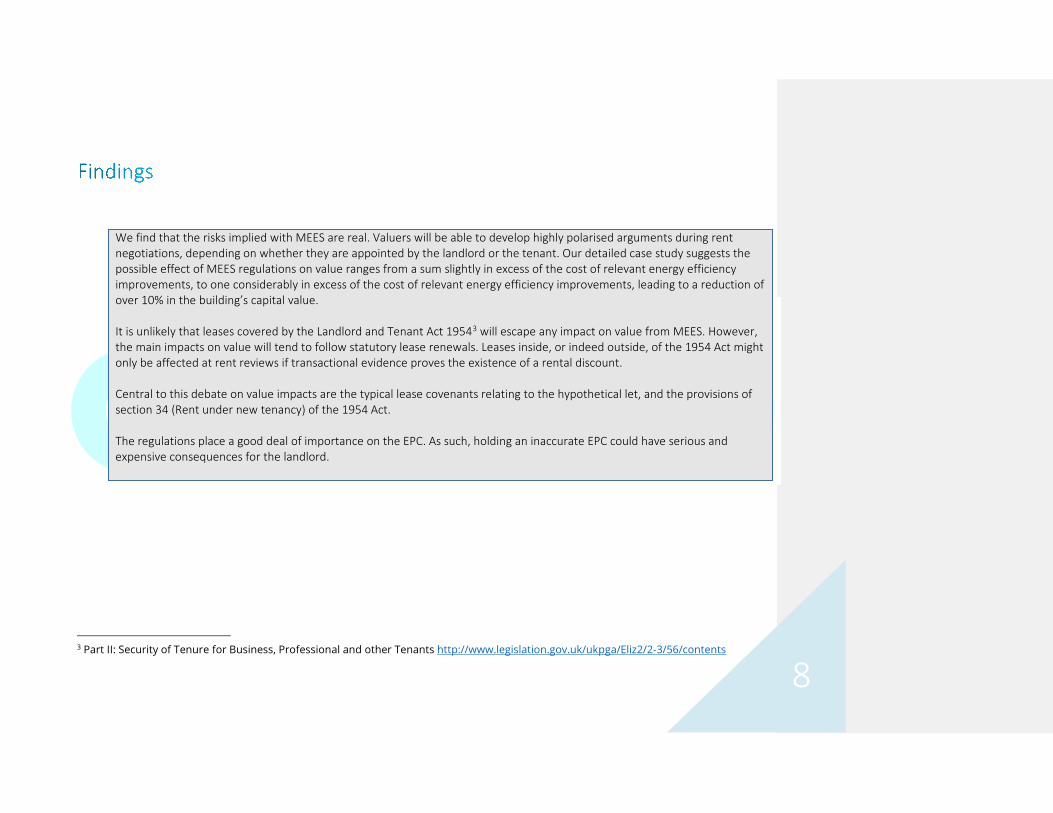

We find that the risks implied with MEES are real. Valuers will be able to develop highly polarised arguments during rent negotiations, depending on whether they are appointed by the landlord or the tenant. Our detailed case study suggests the possible effect of MEES regulations on value ranges from a sum slightly in excess of the cost of relevant energy efficiency improvements, to one considerably in excess of the cost of relevant energy efficiency improvements, leading to a reduction of over 10% in the building’s capital value. It is unlikely that leases covered by the Landlord and Tenant Act 19543 will escape any impact on value from MEES. However, the main impacts on value will tend to follow statutory lease renewals. Leases inside, or indeed outside, of the 1954 Act might only be affected at rent reviews if transactional evidence proves the existence of a rental discount. Central to this debate on value impacts are the typical lease covenants relating to the hypothetical let, and the provisions of section 34 (Rent under new tenancy) of the 1954 Act. The regulations place a good deal of importance on the EPC. As such, holding an inaccurate EPC could have serious and expensive consequences for the landlord.

3 Part II: Security of Tenure for Business, Professional and other Tenants http://www.legislation.gov.uk/ukpga/Eliz2/2-3/56/contents

9

Section 2: MEES and

hypothetical effects on

rents

10

Section 2: MEES, the hypothetical let, and effects on net rents

Rent reviews are typically undertaken using the assumption of a hypothetical letting. This sets out the assumptions upon which rental valuations are based, and includes a number of factors that affect valuation. These include the length of the lease to be valued, whether a rent-free period needs to be accounted for, and whether a tenant’s improvements should be disregarded. As previously noted, MEES is an obligation to the landlord. However, where the tenant is responsible for fitting-out – and it is the fit-out that facilitates compliance with MEES – there is a risk that the result of disregarding a tenant’s improvement work means that this hypothetical property cannot be let. In such cases, the cost of the relevant energy efficiency improvements will need to be calculated and amortised over a period of time in order to arrive at a reduced ‘net’ rent. This disregard is generally only possible where the fit-out has had the landlord’s formal consent. Whether or not such disregards become generally accepted could depend on existing case law, and the extent to which any precedents can be extended to include MEES. The assumption of “fit and available for immediate occupation and use” is a typical provision in most leases. As such, this raises the issue of whether this would also include the possession of the required rating of EPC. Case law that could be applied to compliance with MEES include Orchid Lodge v Extel (1991) and Pontsarn v Kansallis Osake Pankki Bank (1992) – both of which established the legal precedent of what is meant by ‘fit for immediate occupation and use”. Where a property is subject to a statutory lease renewal pursuant to the 1954 Act, section 34 of that Act applies. Unlike a rent review, under section 34 there is no assumption of compliance with covenants, or that the premises are fit and available for immediate use and occupation. As such, if the legal precedents from the aforementioned cases are extended to include MEES, this is unlikely to assist landlords at renewal.

11

Section 3: Summary of

the regulations

12

Summary of the Regulations Landlords and tenants are being forced to reassess the energy performance of buildings because legislation has, for the first time, created a mechanism for monetising energy efficiency. The implications of this need to be analysed and factored into anticipatory portfolio and asset management. As of 1st April 2018, a non-domestic property cannot be let unless it complies with the regulations. These place a requirement upon landlords to ensure that their properties comply with Minimum Energy Efficiency Standards (MEES). The standards are set at an E-rating on an Energy Performance Certificate (EPC). If a property fails to meet the minimum standard, an assessment must be undertaken to identify relevant energy efficiency improvements which must then be carried out, even if the EPC rating does not improve. Only then may a property with an EPC rating lower than E be let. A relevant energy efficiency improvement is defined by the following:

(a) it must be listed in: (i) the Schedule to the Green Deal (Qualifying Energy Improvements) Order 2012; or (ii) Table 6 of the Building Regulations Approved Document Part L2B(a); and

(b) Has been identified as a recommended improvement for that property in a Green Deal report, an EPC Recommendation Report, or a report prepared by a surveyor on the RICS register of valuers.

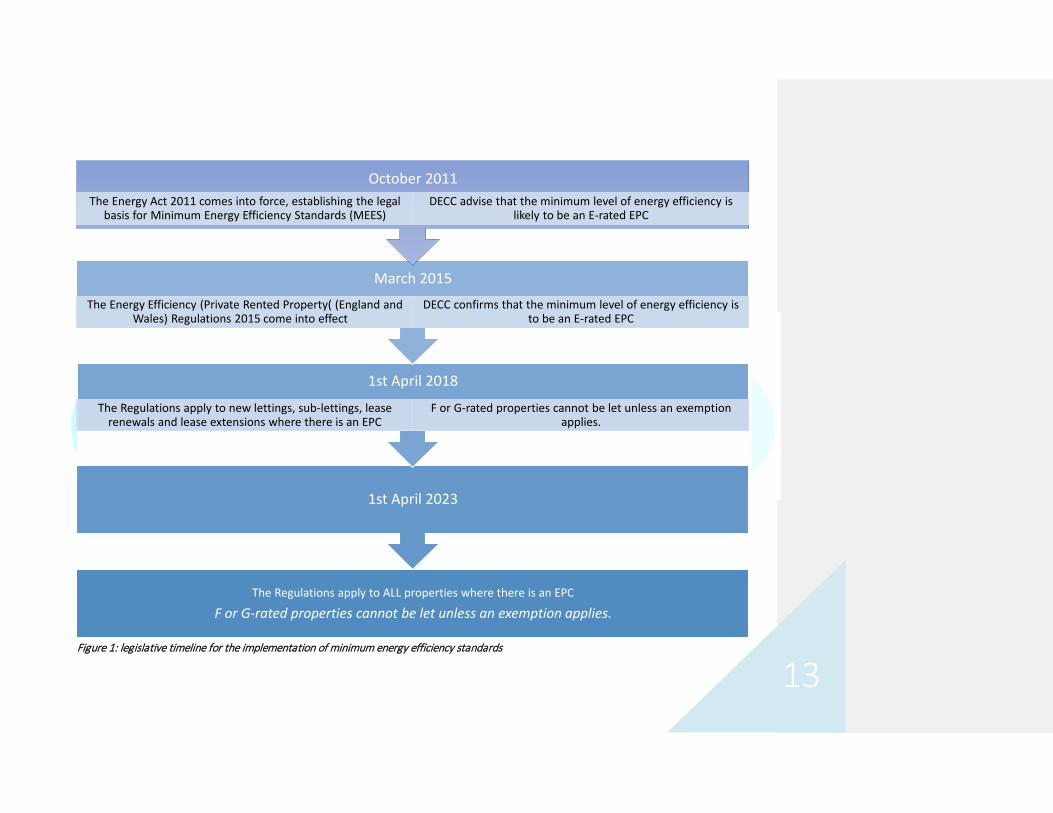

These regulations apply to new lettings, including sub-lettings, and to lease renewals and lease extensions where the property has an EPC. From 1st April 2023, MEES will apply to all non-domestic property where there is an EPC (unless an exemption applies).

13

Figure 1: legislative timeline for the implementation of minimum energy efficiency standards

The Regulations apply to ALL properties where there is an EPC

F or G-rated properties cannot be let unless an exemption applies.

1st April 2023

1st April 2018

The Regulations apply to new lettings, sub-lettings, lease renewals and lease extensions where there is an EPC

F or G-rated properties cannot be let unless an exemption applies.

March 2015

The Energy Efficiency (Private Rented Property( (England and Wales) Regulations 2015 come into effect

DECC confirms that the minimum level of energy efficiency is to be an E-rated EPC

October 2011The Energy Act 2011 comes into force, establishing the legal

basis for Minimum Energy Efficiency Standards (MEES)DECC advise that the minimum level of energy efficiency is

likely to be an E-rated EPC

14

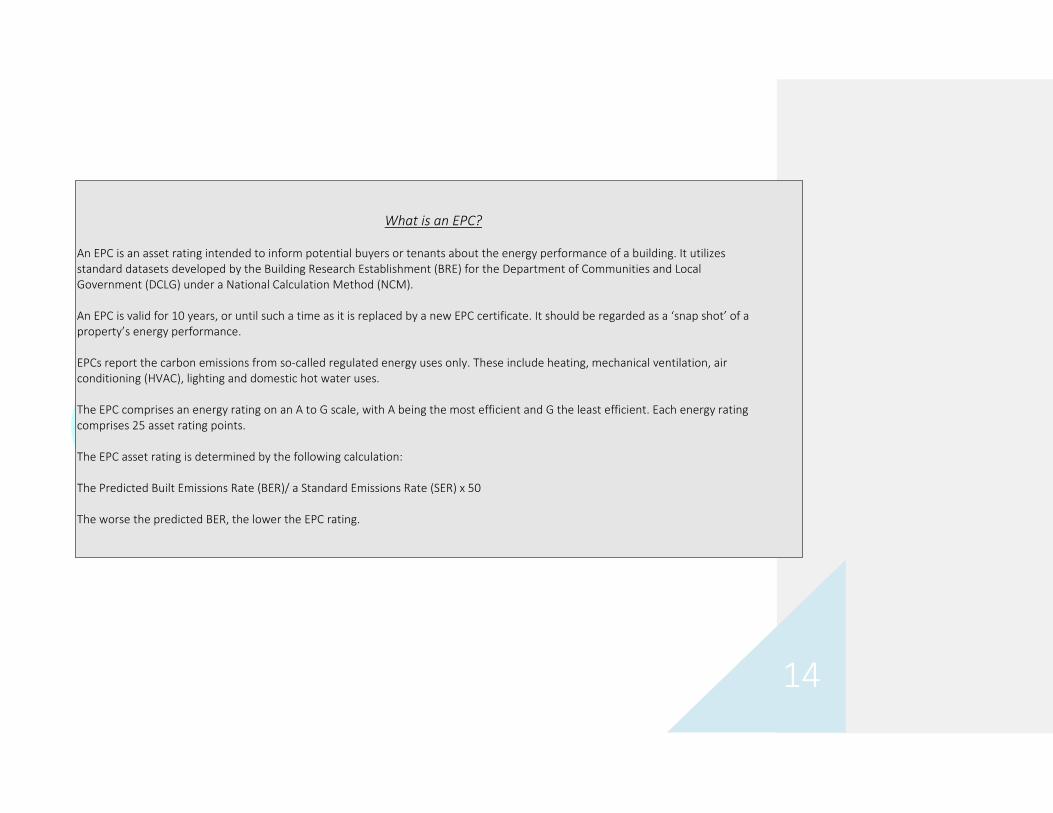

What is an EPC? An EPC is an asset rating intended to inform potential buyers or tenants about the energy performance of a building. It utilizes standard datasets developed by the Building Research Establishment (BRE) for the Department of Communities and Local Government (DCLG) under a National Calculation Method (NCM). An EPC is valid for 10 years, or until such a time as it is replaced by a new EPC certificate. It should be regarded as a ‘snap shot’ of a property’s energy performance. EPCs report the carbon emissions from so-called regulated energy uses only. These include heating, mechanical ventilation, air conditioning (HVAC), lighting and domestic hot water uses. The EPC comprises an energy rating on an A to G scale, with A being the most efficient and G the least efficient. Each energy rating comprises 25 asset rating points. The EPC asset rating is determined by the following calculation: The Predicted Built Emissions Rate (BER)/ a Standard Emissions Rate (SER) x 50 The worse the predicted BER, the lower the EPC rating.

15

3.1 The regulations and the 1954 Act Under the 1954 Act, a tenant is entitled to a new lease on similar terms to the expired lease. The new lease might not therefore address MEES if it has been drafted ahead of 1st April 2018, and is on similar terms and covenants to the expired lease. This would leave the issue of MEES unresolved and therefore subject to valuation risk. As a result, the effect of applying the new regulations to lease renewals and extensions (where the property has an EPC) is that any property with a lease inside of the 1954 Act and an EPC could now be affected by MEES – albeit any valuation impact may not be fully realised until after April 2018. This also applies to leases expiring ahead of 2018, since a tenant can currently obtain a new lease which extends beyond 2018.

3.2 Scope of the Regulations MEES regulations apply to any property let on a tenancy granted for more than six months and less than 99 years. Very short term and long-term leases are thereby excluded. As a general ‘rule of thumb’ the regulations apply to all commercial property where there is a requirement for an EPC under the Energy Performance of Buildings Directive (EPBD). Only the following types of property are excluded:

a. Buildings used as places of worship and for religious activities b. Temporary buildings with a planned time of use of less than two years or less; industrial sites, workshops and residential

agricultural buildings with low energy demand; and residential agricultural buildings which are in use by a sector covered by a national sectoral agreement on energy performance

c. Stand-alone buildings with a total useful floor area of less than 50m2 d. Buildings and monuments officially protected as part of a designated environment, or because of their special architectural or

historic merit (in so far as compliance with certain energy efficiency requirements would unacceptably alter their character or appearance)

We should note that the Department for Communities and Local Government (DCLG) is responsible for making sure buildings in England meet the standards required by the EU’s EPBD, and has interpreted exclusion (d) above as meaning any building listed by English Heritage (or its Welsh equivalent) will be exempt from the requirement to have an EPC. However, buildings that are simply part of a designated environment, such as conservation areas, that are not listed, must have an EPC.

Commented [LH1]: This only covers England & Wales. Devolved to Scotland and Northern Ireland

16

The Department for Business, Energy and Industrial Strategy (BEIS) – formerly the Department for Energy and Climate Change (DECC) - is responsible for the implementation of MEES, and has stated that all non-domestic property types are within the scope of the regulations, with the exception of those specifically excluded from the EPC regulations (as above). Therefore, domestic and non-domestic listed buildings are likely to be exempt from MEES.

3.3 Exemptions To ensure the regulations are equitable, a number of exemptions will apply. These include if:

• The property is not within the scope if it does not require an EPC under the EU EPBD • The measures are not cost-effective, either within a seven-year payback or under the Green Deal’s so-called Golden Rule • Despite reasonable efforts, the landlord cannot obtain the necessary consent to install the required energy efficiency

improvements. This includes consent from tenants, lenders and superior landlords. Only the consents that a landlord is legally bound to seek and obtain before the work can be undertaken is within the scope. This includes planning consent.

• A relevant, suitably qualified expert provides written evidence that the measure will reduce a property’s value by 5% or more, or that wall insulation required to improve energy efficiency will damage the property.

Exemptions apply for a period of five years. If it was a tenant who caused the exemption by refusing the consent, this exemption expires either after five years or once that tenant vacates – whichever happens sooner.

17

3.4 Enforcement and the PRS Exemptions Register Local Trading Standards authorities will determine the responsibility for enforcement of the MEES Regulations. Where a landlord considers an exemption applies, allowing them to let their property below an E rating, the landlord will need to log this on a centralised register (the Private Rented Sector [PRS] Exemptions Register). BEIS may use this information to assist local authorities in targeting their enforcement activity. The Government intends to establish an online PRS Exemptions Register which will be run by BEIS. If a landlord considers they are eligible for a prescribed exemption, they will be required to notify this exemption on the Register.

18

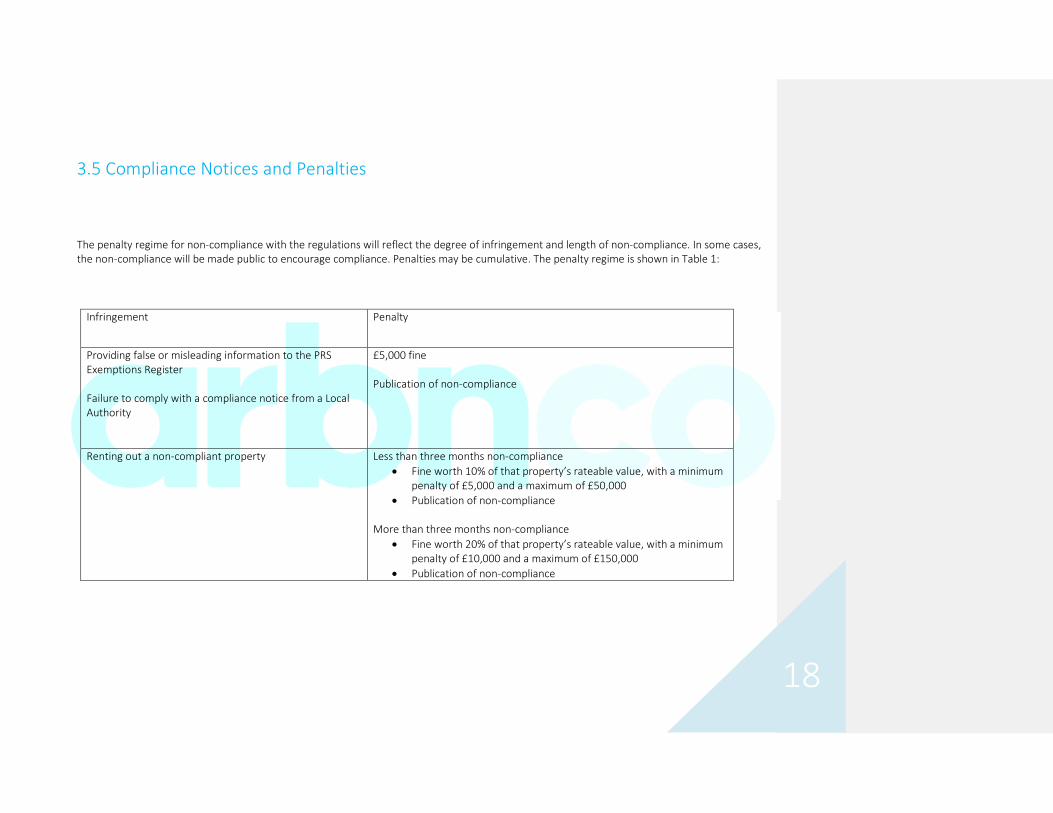

3.5 Compliance Notices and Penalties The penalty regime for non-compliance with the regulations will reflect the degree of infringement and length of non-compliance. In some cases, the non-compliance will be made public to encourage compliance. Penalties may be cumulative. The penalty regime is shown in Table 1:

Infringement Penalty

Providing false or misleading information to the PRS Exemptions Register Failure to comply with a compliance notice from a Local Authority

£5,000 fine Publication of non-compliance

Renting out a non-compliant property Less than three months non-compliance • Fine worth 10% of that property’s rateable value, with a minimum

penalty of £5,000 and a maximum of £50,000 • Publication of non-compliance

More than three months non-compliance

• Fine worth 20% of that property’s rateable value, with a minimum penalty of £10,000 and a maximum of £150,000

• Publication of non-compliance

19

Section 4: Valuation

considerations

20

The following section provides background information on MEES, and discusses some if the issues that will be of relevance to valuers and investment professionals such as asset and fund managers.

4.1 Minimum Efficiency Standards As noted previously, in order to let a property post-April 2018, it must have an EPC rating of E or higher. Otherwise, for assets with an F or G-rating, any relevant cost-effective energy efficiency improvements must be implemented, unless an exemption applies. There are two viability tests to determine whether an improvement is cost-effective. These are: The Golden Rule (Green Deal) This existed as a basis to access Green Deal finance, and stated that repayments for improvements, including any interest charges, must be the same or less than the expected energy bill savings in the first year. However, Green Deal finance was never available for non-domestic property, and in July 2015 the Government announced that no further funding will be made available to the Green Deal Finance Company. At the time of writing, it remains to be seen whether the regulations will be amended to reflect this development. Simple Payback Where Green Deal finance is not being accessed, then any measures listed in Table 6 of the Building Regulations Approved Document Part L2B which pass a simple payback period test of seven years or less must be retrofitted. The cost of installation includes the cost of purchasing and installing the item, as well as any related interest payments. Interest rates are calculated using the prevailing Bank of England base rate. It should be clear from the above that the regulations place a great deal of importance on the EPC. As such, holding an inaccurate EPC could have serious and expensive consequences for a landlord.

Commented [LH2]: Pasted figure in as a temporary measure, will need to alter it to fit in with new branding

21

4.2 The Department of Communities and Local Government’s4 EPC Conventions An EPC assessor will base his or her findings on whatever is observed on the day of the inspection. They estimate the building fabric U-values, and the U-values and g-values for glazing. They also calculate the efficacy of the building’s services. Where they cannot obtain the information required to make these assessments, assessors must refer to the DCLG’s EPC Conventions. These provide a comprehensive summary of the assumptions an EPC assessor must make where information is unknown or incomplete. These conventions are updated periodically and are not iterative; the latest conventions must always be adopted. Importantly, given the central role being played by EPCs in MEES, where information cannot be ascertained, then typically the assessor is expected to use “worst case default values”. For example, if the efficacy of a boiler cannot be determined, then the assessor is forced to revert to the default “worst case” value for that type of boiler. This will naturally negatively affect the EPC rating.

Again, if there are no building services (such as lighting), the assessor must also make assumptions. These assumptions will differ depending on:

• If the property is newly built and being offered to the market in ‘shell and core’ form for the first time; or

• If the property has previously been fitted-out In the former case, the assessor will refer to Building Regulations Part L2A Conservation of Fuel and Power in New Buildings (Other than Dwellings); in the latter, the assessor will refer to the latest version of the Conventions. Using another example, if a tenant occupier removes some or all of its lighting as a result of a terminal schedule of dilapidations, an assessor will be required in the absence of information to the contrary, as part of DCLG EPC conventions, to assume these will be replaced by the least efficient lamp type that can be housed in the installed light fitting. If no light fittings are observed, or the lamp type(s) cannot be ascertained, the default selection of “tungsten” lamps must be made. Again, this will negatively affect the EPC rating

. 4 EPCs are devolved to the Scottish Government and Northern Ireland Executive

22

4.3 The Importance of Fit-Out Under the current NCM it is not possible for a property to get a good EPC rating without having energy efficient building services. However, it is possible, in many cases, to get an E rating or better with efficient building services, but relatively poor building fabric. Tenant fit-out can therefore play an important part in complying with the regulations and the way in which a fit-out is treated in the context of the lease can, therefore, affect property valuation. It is important to note that NCM is dynamic and is revised each time there is an update to Building Regulations Part L2A. to date, these revisions have had a direct effect on the EPC rating, affecting the Standard Emissions Rate (SER) and making it harder to achieve the same rating. As such, the effect of this is that an E rated EPC prepared before April 2011 is likely to be an F or G rated EPC today, even if nothing in the building has changed. This means that over the course of a lease, a ‘virtuous cycle’ of improvements and planning could be required to maintain compliance with MEES.

23

4.4 Multi-let buildings A landlord of a multi-let building with a common centralised HVAC system can choose to comply with the EPBD in two ways. They can:

• Prepare an EPC on a demise-by-demise basis, together with an EPC for the common parts; or

• Prepare a single EPC for the entire property which can then be used for multiple tenancies

Multi-let buildings without a common centralised HVAC system must have EPCs prepared on a demise-by-demise basis.

4.5 Market adjustment to MEES There will be landlords that cannot afford to pay for relevant energy efficiency improvements and cannot or do not want to access finance. In such cases, landlords might market a property with an F or G rated EPC and agree, as part of the letting, that the tenant will contribute or undertake the necessary work to improve the EPC rating to an acceptable level and/or secure an exemption. If and how such an arrangement can be formulated without breaching MEES will need to be determined by solicitors. As a result of such practices, market evidence may develop, demonstrating a value differential between those properties with an EPC of at least an E, those where an exemption applies, and those that are not compliant with MEES.

24

Section 5: case study

25

A case study of the valuation implications of MEES

5.1 Introduction to the case study In order to explore the potential effect of the MEES regulations on rental and capital valuations, we have prepared the following case study. Clearly, the effect of MEES on valuation is not yet known, and will ultimately be determined by market forces, case law, and government legislation. However, while it may not be possible to provide a precise assessment of the valuation impact, our case study considers the potential effects of MEES on rent and capital values by examining the impact of the various related arguments valuers might raise at rent reviews or lease renewals. As we shall see, these arguments are polarized and their potential effects on values could range from negligible to the profound. This introduces uncertainty into the valuation process and, as such, increases property risk. Albeit simplified and adapted, the details of the following case study are based on an actual building and different leases. It represents a common scenario, namely where the landlord of a multi-let procures EPCs on a demise-by-demise basis when a property is marketed. Although the case study is an office building, many of the findings are directly transferable to retail, industrial, and other forms of property.

26

5.2 The case The year is 2018. Three of four existing tenancies are all due a rent review, and the fourth a lease renewal. All leases are inside Part II of the 1954 Act. All occupiers are professionally represented. The landlord procured an EPC for each demise at the point of letting, with all lettings completed in May 2013. In all cases the landlord partially refurbished the building, but did not replace the original lighting system and controls. This resulted in an EPC rating of G for each demise. Each tenant went on to install a lighting system as part of its fit-out. All tenants fitted out with LED lights and modern controls. While tenants 1 and 2 obtained the landlord’s consent for works and completed a license for alterations, tenants 3 and 4 discussed the proposals with the landlord but did not obtain formal written consent as required by the leases. In all cases the cost of the work was £65 per m2 (£6 per foot). Th simple payback is less than three years. So, the seven-year simple payback rule under MEES is met comfortably. Following the fit-out, tenants 2 and 3 commissioned a revised EPC rating and, as a result of the new lighting and upgraded controls, the rating on their demises improved to an E.

27

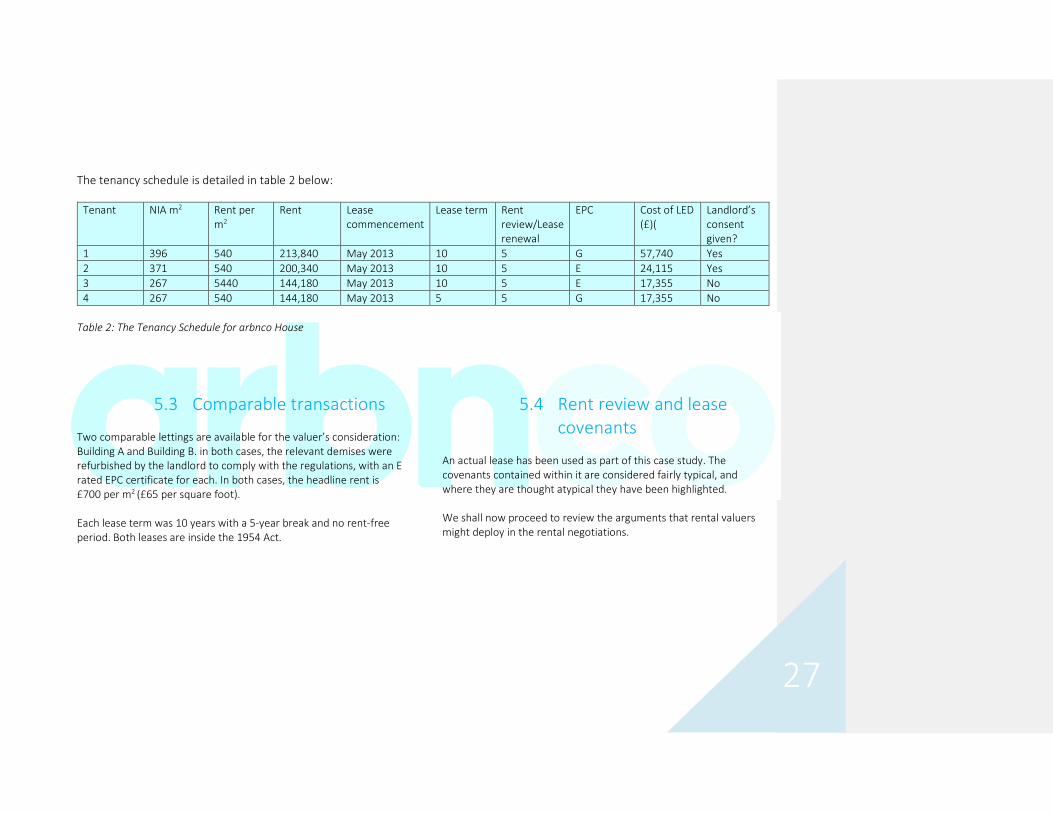

The tenancy schedule is detailed in table 2 below:

Tenant NIA m2 Rent per m2

Rent Lease commencement

Lease term Rent review/Lease renewal

EPC Cost of LED (£)(

Landlord’s consent given?

1 396 540 213,840 May 2013 10 5 G 57,740 Yes 2 371 540 200,340 May 2013 10 5 E 24,115 Yes 3 267 5440 144,180 May 2013 10 5 E 17,355 No 4 267 540 144,180 May 2013 5 5 G 17,355 No

Table 2: The Tenancy Schedule for arbnco House

5.3 Comparable transactions Two comparable lettings are available for the valuer’s consideration: Building A and Building B. in both cases, the relevant demises were refurbished by the landlord to comply with the regulations, with an E rated EPC certificate for each. In both cases, the headline rent is £700 per m2 (£65 per square foot). Each lease term was 10 years with a 5-year break and no rent-free period. Both leases are inside the 1954 Act.

5.4 Rent review and lease covenants

An actual lease has been used as part of this case study. The covenants contained within it are considered fairly typical, and where they are thought atypical they have been highlighted. We shall now proceed to review the arguments that rental valuers might deploy in the rental negotiations.

28

Section 6: case study analysis

29

6.1 Potential arguments by tenants

• Tenants 1,2 & 3 all have rent reviews at the same date, and the tenants’ advisors argued that since the lighting was a tenant’s improvement these works should be disregarded, meaning the letting could not go ahead as at the review date of May 2018. This was because the EPC rating without the replacement lighting was below an E-rated EPC, and the offices would not therefore satisfy the minimum standard.

• Given this, the tenants could well argue that, to comply with the MEES regulations, the landlord would have to undertake the required works at his or own cost. This would lead to a period of disruption to the tenant and, as such, they would require a rent-free period to cover the time over which the works were carried out.

• The tenants would also attempt to negotiate a rental reduction to reflect the fact that they would not be able to occupy the offices from the start of the lease. They would have to make alternative arrangements and, as a result, the tenant could lose business and/or incur costs, which require compensation by way of a rent reduction.

• Since the works were paid for by the tenants, and the rent review clause in each lease disregards any increase in rental value attributable to any tenants’ improvements with the landlord’s consent, the tenants

would also argue that, since the cost of the lighting amounted to approximately £65 per m2 (£6 per ft2), this cost should be amortised over the period of the remaining lease term of five years. On a straight-line basis, this would amount to a rate of £13 per m2 (£1.20 per ft2) which should be deducted from the rent, assuming an E rating.

• The evidence from comparable buildings with an E rated EPC suggests a rent of £700 per m2 (65 per ft2). As such, this amortised cost would reduce that rent to £687 per m2(£63.80 per ft2). This is before any deduction for the rent free and the disruption relating to the work. With a rent free of, say, three months (analysed over five years) and a 5% deduction for the disruption, the tenant’s advisors could argue for a rent based on approximately £619 per m2 (£57.50 per ft2)

• Naturally, the landlord’s advisor would not accept the tenant’s arguments and would refer to the wording of the rent review provisions in each of the leases. He or she would point out that the definition of ‘open market rent’ includes the following assumptions and disregards relevant to rent review negotiations.

o The premises are fit and available for immediate occupation

30

o The covenants contained within the lease on the part of the landlord and the tenant have been fully performed and observed

o Disregarding any increase in rental value of the demised premises attributable to the existence of any improvement carried out by the tenant with the consent of the landlord, otherwise than in pursuance of an obligation to the landlord

• In order for the premises to be assumed fit and available for immediate occupation, it must have a minimum EPC rating of E, or an exemption must apply. As such, the landlord would argue that this assumption requires the parties to assume that it has that rating or an exemption – otherwise it would not be fit and available for occupation. This means, in turn, that the tenant will not be rewarded with a discounted rent for making improvements.

• One of the landlord’s covenants contained within the lease is that they have complied with all statutory obligations. To satisfy the assumption that the landlord has complied with the covenants, it must be assumed that the relevant energy efficiency improvements have been carried out, and the premises have an E rating or an exemption – otherwise the landlord would be in breach of the regulations by attempting to let a property with a G rating. Again, this means that the tenant will not be rewarded with a discounted rent for making improvements. However, it should be noted that this clause is not present in all leases.

• It is one thing to assume that the premises have the minimum rating or an exemption to enable they hypothetical letting to take place. It is quite another to argue that the increase in rent as a result of the tenant’s improvements should not be disregarded if leasing conditions are satisfied, given that one of the conditions is that the landlord’s consent is required.

31

6.2. Potential arguments by landlords

• Tenants 1 and 2 have consent, whereas tenants 3 and 4 do not. In respect of the rent reviews, the landlord would argue that tenants 1,2 and 3 must be assumed to have the minimum EPC rating of E (or an exemption). That being the case, it need not concede any reduction in rent to reflect a rent-free period or disruption as argued for by the tenants, as no works should be assumed to be required.

• In the case of tenants 1 and 2, the landlord may be prepared to agree a rental reduction to reflect the amortised cost of the works. However, the benefit to the landlord would be longer than five years, and therefore, the period over which the costs should be amortised would be longer. Rather than agree to a reduction of £13 per m2 (£1.20 per ft2), the landlord may instead agree to, say, half that amount. As such, the rent would increase to, say, £693.50 per m2 (£64.40 per ft2) to reflect the costs of the improved lighting.

• Tenant 3 did not have the landlord’s consent to install

the lighting. The landlord would argue that since they did not comply with the condition requiring the landlord’s consent, the works should not be disregarded and the offices should be valued at the full rate having regard to the evidence at £700 per m2 (£65 per ft2)

• In contrast to the above examples, tenant 4 does not have a rent review, but has a lease expiry in August 2018, and the parties are negotiating a new lease. The reviewed rent will be determined under section 34 of the Landlord and Tenant Act 1954, and the following points apply:

o There is no assumption that the premises are fit for immediate occupation, nor that the parties have complied with the covenants in the lease.

o There is a disregard of any effect on rent of tenant’s improvements, other than in pursuance of an obligation to the landlord. As such, there is no requirement for the works to have had the landlord’s prior consent.

o The tenant could argue that, prior to the tenant’s works, the EPC rating was G and, therefore, the rent should be the same as agreed with other tenants in the comparable cases, namely £619 per m2 (£57.50 per ft2)

• The landlord would counter this by arguing that, even though there are no assumptions contained in Section 34 enabling the landlord to assume an E rating, the reality is that it would in fact achieve an E, as the works have been completed.

• Tenant 4 did not have the landlord’s consent for the works, but under section 34 consent is not required. As long as it was a tenant’s improvement, which is not

32

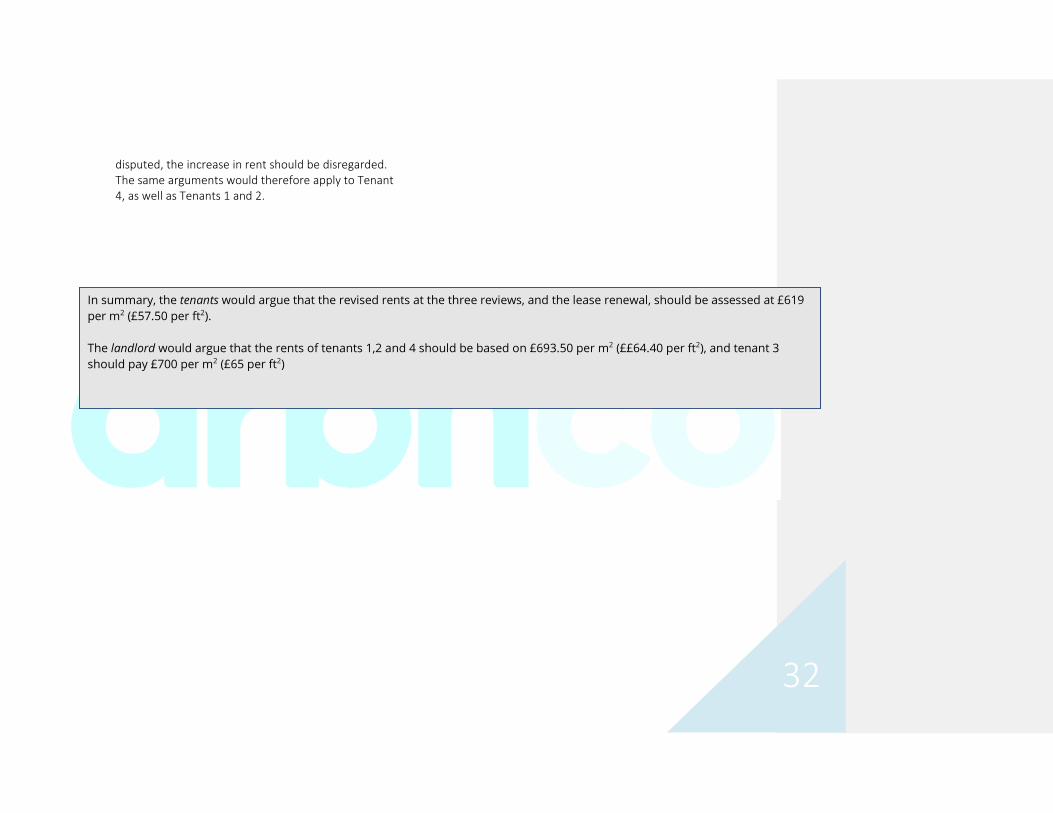

disputed, the increase in rent should be disregarded. The same arguments would therefore apply to Tenant 4, as well as Tenants 1 and 2.

In summary, the tenants would argue that the revised rents at the three reviews, and the lease renewal, should be assessed at £619 per m2 (£57.50 per ft2). The landlord would argue that the rents of tenants 1,2 and 4 should be based on £693.50 per m2 (££64.40 per ft2), and tenant 3 should pay £700 per m2 (£65 per ft2)

33

Section 7: Impacts on rental and

capital values

34

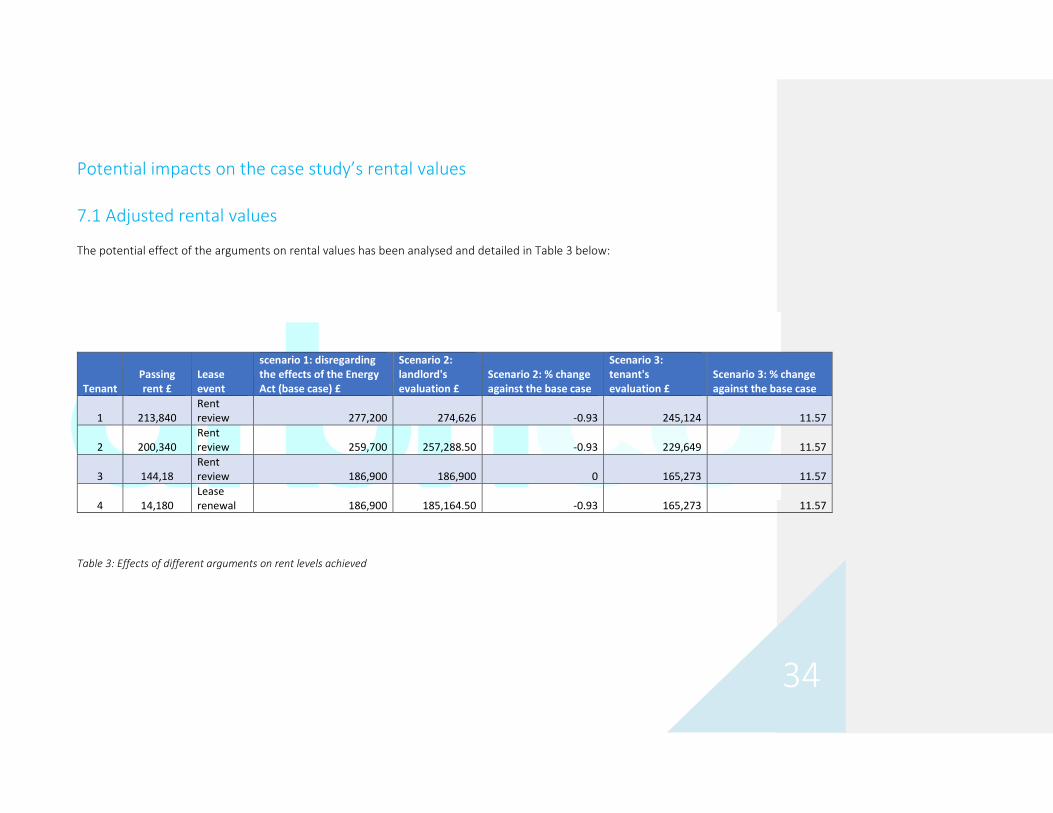

Potential impacts on the case study’s rental values 7.1 Adjusted rental values The potential effect of the arguments on rental values has been analysed and detailed in Table 3 below:

Tenant Passing rent £

Lease event

scenario 1: disregarding the effects of the Energy Act (base case) £

Scenario 2: landlord's evaluation £

Scenario 2: % change against the base case

Scenario 3: tenant's evaluation £

Scenario 3: % change against the base case

1 213,840 Rent review 277,200 274,626 -0.93 245,124 11.57

2 200,340 Rent review 259,700 257,288.50 -0.93 229,649 11.57

3 144,18 Rent review 186,900 186,900 0 165,273 11.57

4 14,180 Lease renewal 186,900 185,164.50 -0.93 165,273 11.57

Table 3: Effects of different arguments on rent levels achieved

35

7.2 Potential impact on the case study’s capital values An all-risks yield of 7% has been applied to three valuation scenarios: Scenario 1 considers the capital value of the case study on the assumption that the Energy Act 2011 and/or subsequent regulations are revoked, or have no impact on value. This is the base case valuation scenario:

(a) Scenario 1: the base case (disregarding the effects of the Energy Act)

Scenario 2 considers the capital value of the case study on the assumption that the valuation by the landlord’s surveyors are realised:

(b) Scenario 2: Capital value based on landlord’s rental valuation

Tenant Disregarding the effect of the

Energy Act Capitalisation at 7% Capital values Cost of LED 1 £274,626 14.29 £3,924,405.54 £25,740 2 £257,288.50 14.29 £3,676,653 £24,115 3 £186,900 14.29 £2,670,801 £17,355 4 £185,164 14.29 £2,646,000.71 £17,355

Capital value (total) £903,462 N/A £12,917,859.92 £84,565 Effect on value -£96,043.08

Tenant Disregarding the effects of the Energy Act Capitalisation at 7% (100/7) Capital values Cost of LED1 £277,200 14.29 £3,961,188 £25,7402 £259,700 14.29 £3,711,113 £24,1153 £186,900 14.29 £2,670,801 £17,3554 £186,900 14.29 £2,670,801 £17,355

Capital value (total) £910,700 N/A £13,013,903 £84,565

36

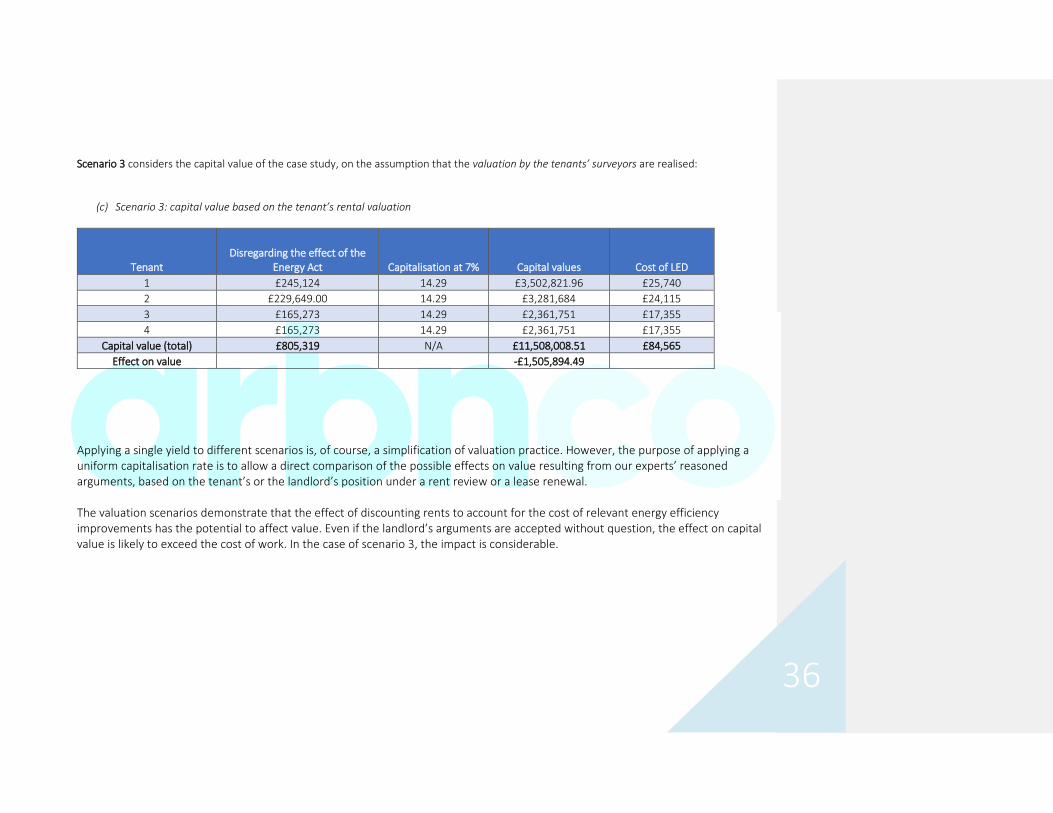

Scenario 3 considers the capital value of the case study, on the assumption that the valuation by the tenants’ surveyors are realised:

(c) Scenario 3: capital value based on the tenant’s rental valuation

Tenant Disregarding the effect of the

Energy Act Capitalisation at 7% Capital values Cost of LED 1 £245,124 14.29 £3,502,821.96 £25,740 2 £229,649.00 14.29 £3,281,684 £24,115 3 £165,273 14.29 £2,361,751 £17,355 4 £165,273 14.29 £2,361,751 £17,355

Capital value (total) £805,319 N/A £11,508,008.51 £84,565 Effect on value -£1,505,894.49

Applying a single yield to different scenarios is, of course, a simplification of valuation practice. However, the purpose of applying a uniform capitalisation rate is to allow a direct comparison of the possible effects on value resulting from our experts’ reasoned arguments, based on the tenant’s or the landlord’s position under a rent review or a lease renewal. The valuation scenarios demonstrate that the effect of discounting rents to account for the cost of relevant energy efficiency improvements has the potential to affect value. Even if the landlord’s arguments are accepted without question, the effect on capital value is likely to exceed the cost of work. In the case of scenario 3, the impact is considerable.

37

Section 8: Conclusions

38

Conclusions On the basis of the above study, we can conclude as follows with respect to the assumptions that rental valuers will make regarding: RENT REVIEWS LEASE RENEWALS RENTAL AND CAPITAL VALUATIONS

39

8.1 Rent reviews

• At any rent review at or beyond 1st April 2018, valuers must assume the necessity for an EPC. This is because the rent review hypothesis is predicated upon an open market letting with vacant possession and that, in turn, will require an EPC with a rating of E or higher, or an exemption.

• At any review date prior to 1st April 2018 where the hypothetical term runs beyond that date, there is no need to assume the necessity for a minimum EPC rating. However, the tenant may argue that a low EPC rating will impact adversely on their ability to sublet (and therefore press for a lower rent).

• If the rent review provisions allow for a valuation in whole or in part, then it may be open to the landlord to obtain an EPC for the entire building, or on a demise-by-demise basis. There may be substantially different specifications across different demises occupying the same building, and it is unclear how this may impact upon the whole.

• Where there is an assumption in the lease that premises are “fit and available for immediate occupation”, there is the potential for an argument that the premises must be legally fit for occupation and, therefore, hold the required EPC rating.

o There is case law on issues similar to MEES that could be extended to this scenario. These include: Orchid Lodge v Excel, where “fit for

occupation and use” in a Licence for Works meant that the tenant could not argue that the works were insufficient to make the premises fit for office use;

Pontsarn v Kansallis Osake Pankki Bank, where “vacant and fit for immediate occupation and use” meant that the premises were free form defects, and fit to be occupied.

• Where there is an assumption in the lease that the landlord’s covenants have been fully performed, this may give rise to an assumption that the works required to increase the EPC rating have been carried out. In such cases, it will depend on whether the landlord has

40

an obligation under the terms of the lease to comply with this statute.

• On the assumption that the landlord’s works need to be carried out after the hypothetical transaction has taken place, then these are the landlord’s works that could potentially result in a period of time when the tenant could not occupy. This would require a rent-free period and a reduction in the net rent to be granted.

• There may be implications for the specification of fit-out works. The EPC recommendations report specifies those works that must be carried out to improve the rating. It is possible that, once undertaken, the resulting rating ends up better than an E and therefore may command a higher rent (though there would also likely be a rent-free period – see above).

• Where there is a disregard of a tenant’s improvements, once those works are set aside it is quite conceivable that the resulting rating will no longer have a satisfactory EPC rating. However, as this is a

hypothetical building, it may be necessary to have the hypothetical EPC assessed. At arbitration, it may be necessary to have experts appear on behalf of both parties to examine what the EPC rating of the hypothetical building might have been.

• Most disregard clauses provide that works are only disregarded if they have been carried out with the landlord’s consent. If there is no consent, then the landlord may value. If the tenant has carried out works to improve the EPC rating, the landlord may take these into account under these circumstances.

• The cost of the works will be amortised over a period of time in order to arrive at a net rent (see above). There are a number of plausible periods over which amorisation could take place:

o Viability of the works is assessed over seven years;

o The EPC validity period of ten years; o The hypothetical term; o In perpetuity.

41

8.2 Lease Renewals Lease renewals are governed by section 34 of the 1954 Act, which is silent on many of the issues covered by a lease. In particular, it makes no assumption of compliance with covenants, or whether premises are fit and available for immediate use and occupation. Section 34 contains a general disregard of tenants’ improvements unless these have been undertaken as an obligation to the landlord. There is no assumption that works must have been carried out with consent. As a result, all non-obligatory tenants’ works are disregarded.

8.3 Rental and capital valuations Comparable evidence may arise in the future, proving that the implementation of MEES provisions does affect rental values. This will undoubtedly impact rent review and lease renewal negotiations and, therefore, capital values. It is feasible that rents at rent review or lease renewals will be discounted to reflect the cost of improvement works and/or to compensate occupiers for disruption. Therefore, even without direct comparable evidence to prove that MEES affects rents, one can identify immediately the risk of discounts being negotiated that will negatively impact capital values. Through the application of capitalisation rates, the effects of discounts are potentially amplified, meaning the impact on value can exceed the cost of work, potentially by considerable sums. Given that the cost of works may have a uniform impact on decreasing rents, capitalisation could affect lower-yielding prime buildings more than higher-yielding secondary buildings.

42

The accuracy of the EPC It is clear that an EPC rating has the potential to impact value and the scope for disputes and litigation, with experts for both landlords and tenants making representations on the accuracy of the EPC, is high. It is, therefore, essential that all parties procure the best quality EPCs they can, and retain access to the data that is behind the certificate. It should be clear form the above that cutting costs when procuring EPCs could well result in the resultant EPCs including worst-case scenario default inputs which lead, in turn, to a lower grading outturn and potentially major and deleterious impacts on rental and capital values.

43

Addendum: Section 63 requirements (Scotland only) The relevant energy efficiency legislation is the Assessment of Energy Performance of Non-domestic Buildings (Scotland) Regulations 2016. This is also known as Section 63, and came into effect in September 2016. The legal requirements cover non-domestic buildings over 1,000 m2, and their requirements for an EPC. This is triggered when the building is put up for sale or leased to a new tenant – and the building must achieve an E-rated EPC as a minimum. If the building does not achieve this rating, building owners must ensure a further assessment is carried out by a suitably-qualified person (known as a Section 63 advisor) who will produce an Action Plan, which includes targets for improving the energy performance and carbon performance of the building, and sets out the actions needed to achieve this. Once the action plan has been produced, the building owner may either:

• Make these improvements, or; • Defer making these improvements by reporting the annual operational energy ratings annually, via a Display Energy Certificate

(DEC). • All Action Plans and DECs must be lodged on the Scottish EPC Register, and must be made available to prospective owners or

tenants. • The Action Plan must be provided to the new owner/tenant.

44

About the authors Andrew Cooper is a Chartered Institution of Building Services Engineers (CIBSE) qualified EPC assessor to Level 5, and an MEI Chartered Energy Manager. He has over 20 years of property experience, and a background in general practice surveying. Andrew writes about sustainability for many market-leading professional journals, including the Estates Gazette and the CIBSE journal. Dr Megan Strachan is former Head of Development at arbnco Ltd. Megan comes from a background in building surveying, and recently completed a PhD examining the decision-support mechanisms surrounding the energy-led retrofit of non-domestic buildings. Copyright © arbnco Ltd 2017. All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means without the prior written consent of arbnco Ltd. Disclaimer: this publication is based on material that we believe to be accurate. Whilst every effort has been made to ensure its accuracy, we cannot offer any warranty that it contains no factual errors. We would like to be told of any such any errors in order to correct them.

45