microfinance in india

TRANSCRIPT

Microfinance in India

IntroductionMicrofinance is a general term to describe financial services to low-income individuals or to those who do not have access to typical banking services. Microfinance is also the idea that low-income individuals are capable of lifting themselves out of poverty if given access to financial services.

It is an activity that includes the provision of financial services such as credit, savings, and insurance to low income individuals

DefinitionAcc to Robinson: Microfinance refers to small scale financial services for both credits and deposits- that are provided to people who farm or fish or herd; operate small or micro enterprise where goods are produced, recycled, repaired, or traded; provide services; work for wages or commissions; gain income from renting out small amounts of land, vehicles, draft animals, or machinery and tools; and to other individuals and local groups in developing countries in both rural and urban areas.

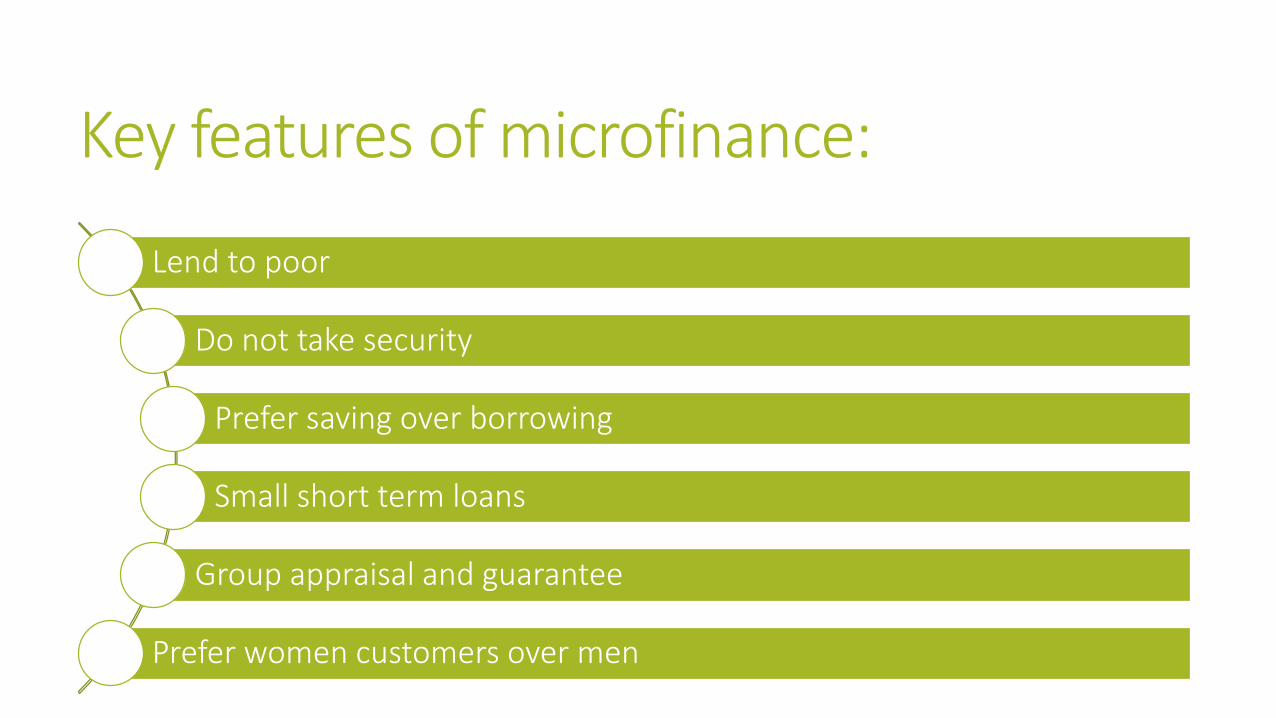

Key features of microfinance:

Lend to poor

Do not take security

Prefer saving over borrowing

Small short term loans

Group appraisal and guarantee

Prefer women customers over men

Need of Microfinance in India India is said to be the home of one third of the world’s poor; official estimates range from 26 to 50 percent of the more than one billion population

About 87 percent of the poorest households do not have access to credit

The demand for micro credit has been estimated at up to $30 billion; the supply is less than $2.2 billion combined by all involved in the sector

About two thirds of India’s more than 1billion people live in rural areas

For more than 21 percent of them, poverty is a chronic condition. Three out of four of India’s poor live in rural areas of the country

Continue…..

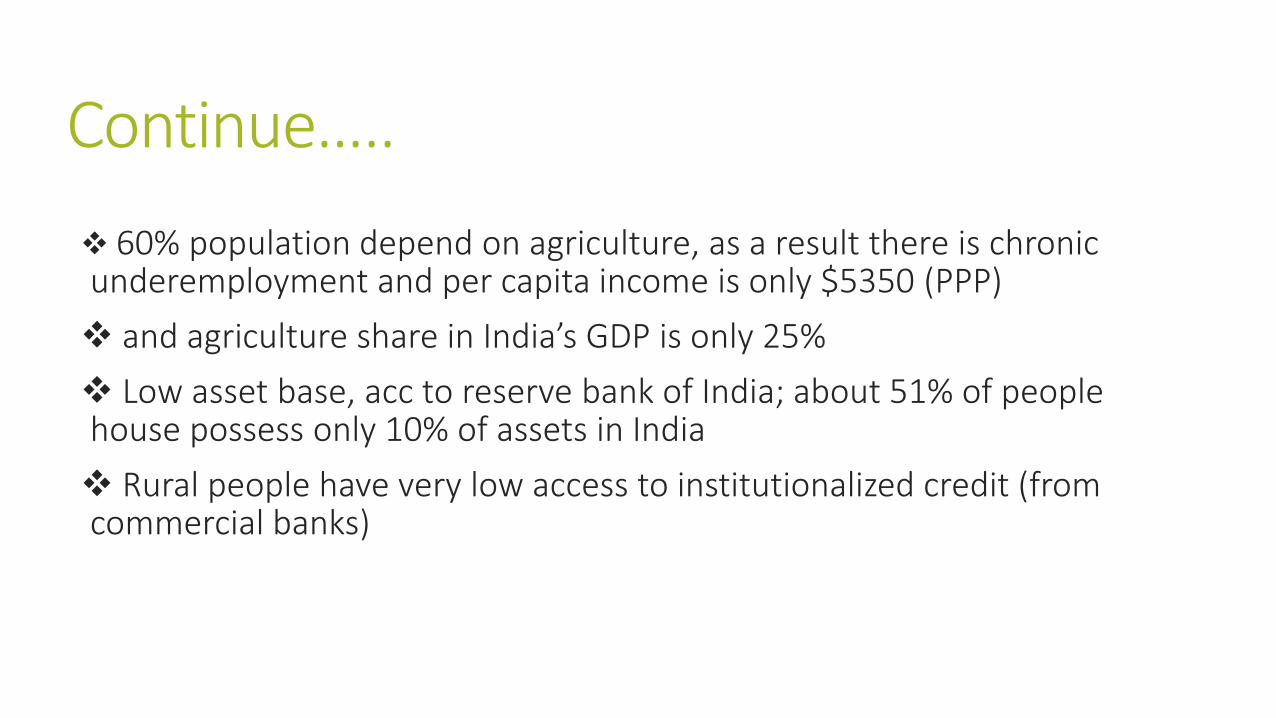

60% population depend on agriculture, as a result there is chronic underemployment and per capita income is only $5350 (PPP)

and agriculture share in India’s GDP is only 25%

Low asset base, acc to reserve bank of India; about 51% of people house possess only 10% of assets in India

Rural people have very low access to institutionalized credit (from commercial banks)

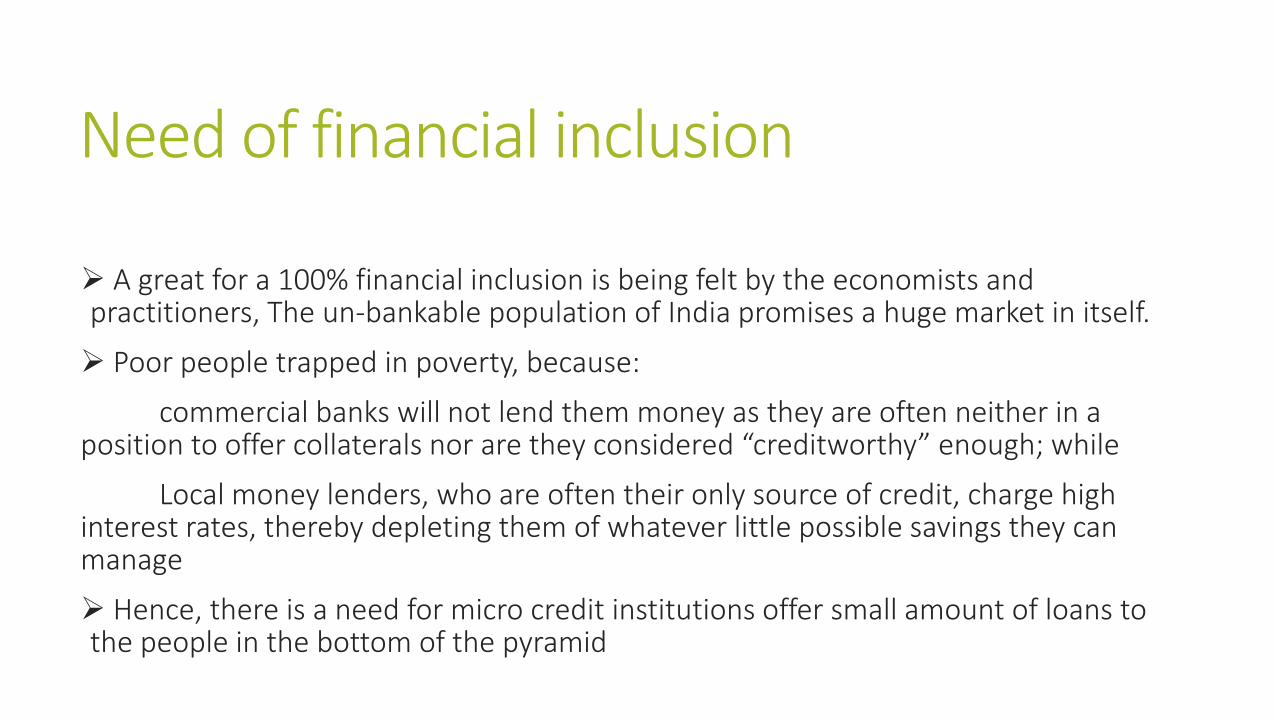

Need of financial inclusion

A great for a 100% financial inclusion is being felt by the economists and practitioners, The un-bankable population of India promises a huge market in itself.

Poor people trapped in poverty, because:

commercial banks will not lend them money as they are often neither in a position to offer collaterals nor are they considered “creditworthy” enough; while

Local money lenders, who are often their only source of credit, charge high interest rates, thereby depleting them of whatever little possible savings they can manage

Hence, there is a need for micro credit institutions offer small amount of loans to the people in the bottom of the pyramid

Continue…. There is a tremendous demand from 100mn poor and vulnerable households in India

0

20

40

60

80

100

120

Finance (Accessed by poor households) Finance(Needed by poor households)

Demand in US $

20x growthpotential

UnmetDemand

Who Requires Microfinance?In India, generally microfinance is sought by:

• Small and marginal farmers;

• rural artisans

• and economically weaker sections

• women constitute a vast majority of users of microcredit and savings facilitates

10%90%

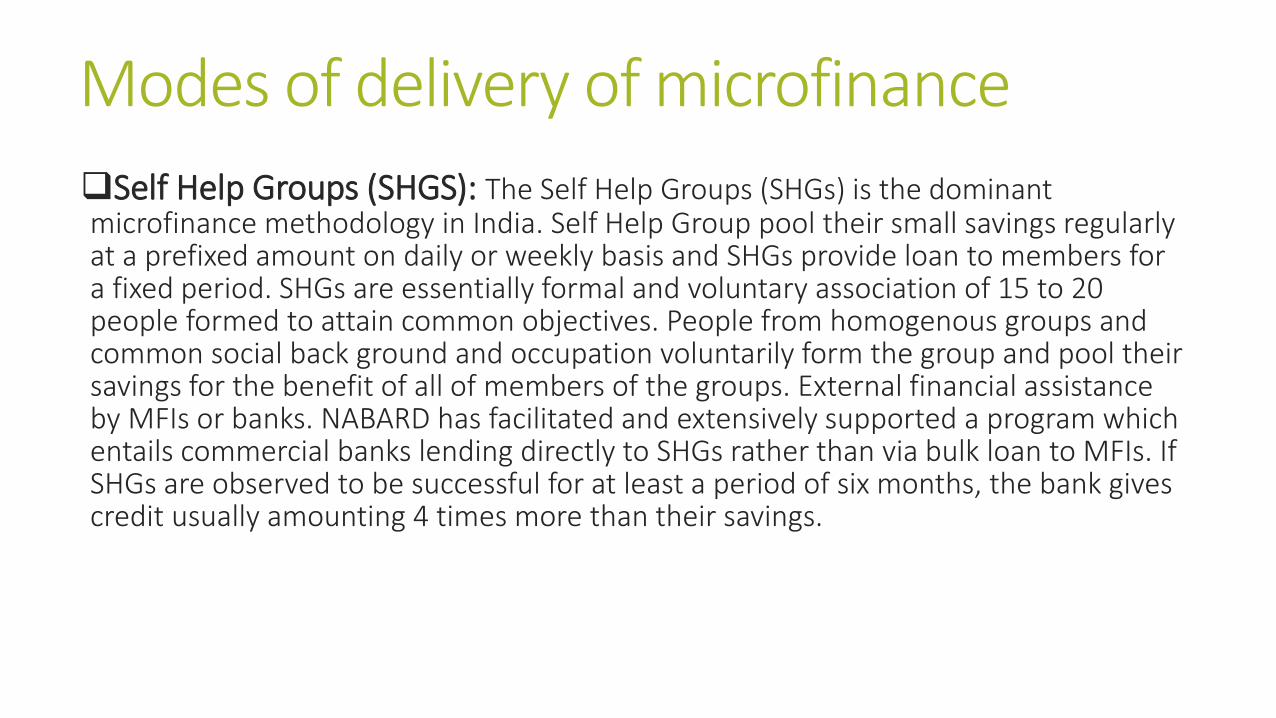

Modes of delivery of microfinance

Self Help Groups (SHGS): The Self Help Groups (SHGs) is the dominant microfinance methodology in India. Self Help Group pool their small savings regularly at a prefixed amount on daily or weekly basis and SHGs provide loan to members for a fixed period. SHGs are essentially formal and voluntary association of 15 to 20 people formed to attain common objectives. People from homogenous groups and common social back ground and occupation voluntarily form the group and pool their savings for the benefit of all of members of the groups. External financial assistance by MFIs or banks. NABARD has facilitated and extensively supported a program which entails commercial banks lending directly to SHGs rather than via bulk loan to MFIs. If SHGs are observed to be successful for at least a period of six months, the bank gives credit usually amounting 4 times more than their savings.

Continue….Individual Banking Programmes (IBPS):

There is provision by Microfinance institutions for lending to individual clients though they may sometimes be organized into joint liability groups, credit and saving cooperatives. This model is increasingly popular through cooperatives. In cooperatives, all borrowers are members of organization directly or indirectly by being member of cooperative society. Credit worthiness and loan securing are a function of cooperative membership in which member’s savings and peer pressure are assumed to be key factors.

Grameen Model: Grameen Model was pioneered by DR Mohammed Yunus of Grameen Bank of Bangladesh. It is perhaps the most well-known and widely practiced model in the world. In Grameen Model the groups are formed voluntarily consisting of five borrowers each. The lending is made first to two, then to the next two and then to the fifth. These groups of five meet together weekly, with seven other groups, so that bank staff meets with forty clients at a time. While the loans are made to the individuals, all in the group are held responsible for loan repayment. According to the rules, if one member ever defaults, all in the group are denied subsequent loans.

Continue….

Mixed Model: Some MFIs started with the Grameen model but converted to the SHG model at a later stage. However they did not completely do away with Grameen type lending and smaller groups. They are a mix of SHG and Grameen model. The main difference between these programs is rather marginal. Grameen programmes have traditionally not given much importance to savings as a source of funds whereas SHGs place considerable emphasis on the source of funds. The SHG programs have compulsory deposit schemes in which the members themselves determine the amount. The SHGs model is widely used in India.

Among all methodologies, Self Help Groups (SHGs) model is more popular in India.

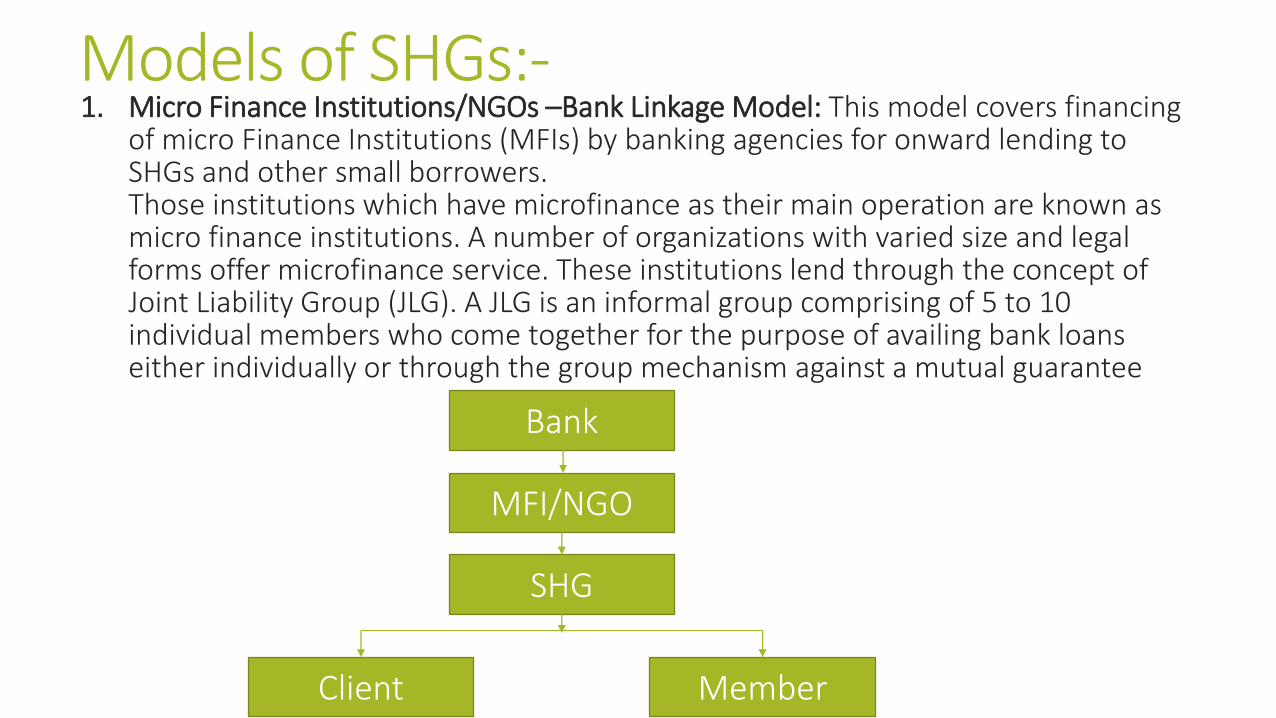

Models of SHGs:-1. Micro Finance Institutions/NGOs –Bank Linkage Model: This model covers financing

of micro Finance Institutions (MFIs) by banking agencies for onward lending to SHGs and other small borrowers. Those institutions which have microfinance as their main operation are known as micro finance institutions. A number of organizations with varied size and legal forms offer microfinance service. These institutions lend through the concept of Joint Liability Group (JLG). A JLG is an informal group comprising of 5 to 10 individual members who come together for the purpose of availing bank loans either individually or through the group mechanism against a mutual guarantee

Bank

MFI/NGO

SHG

Client Member

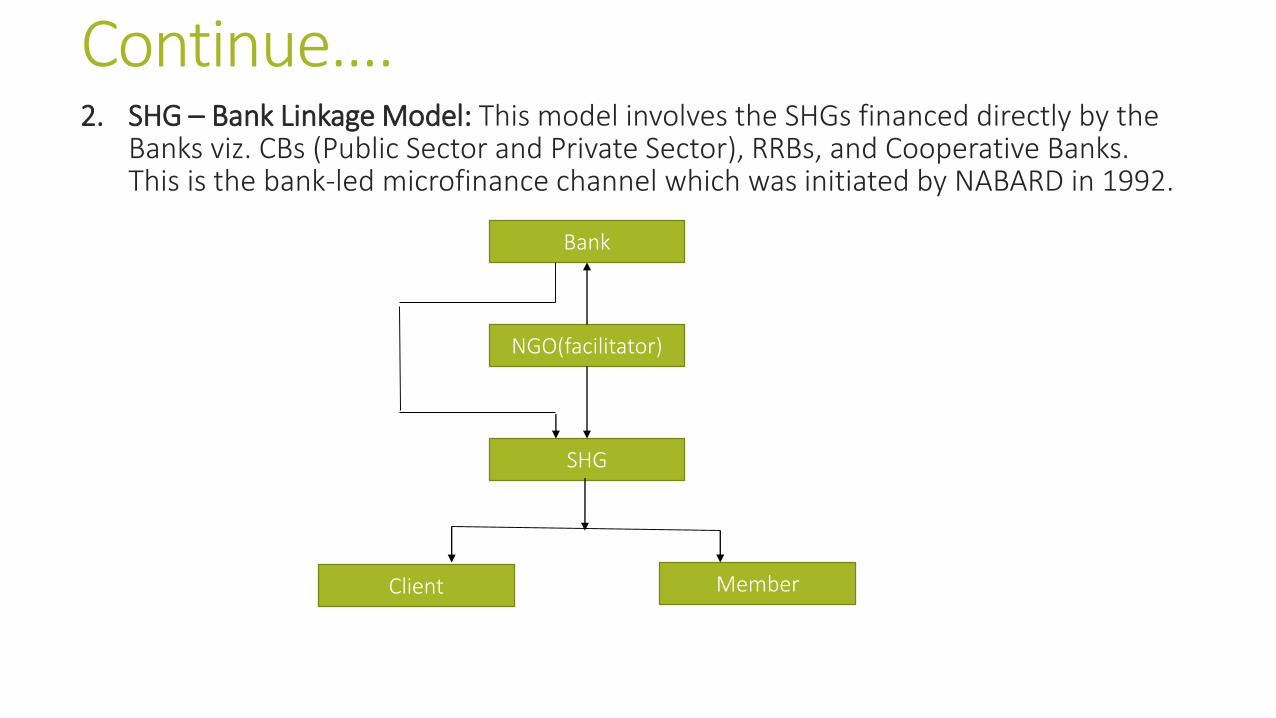

Continue….2. SHG – Bank Linkage Model: This model involves the SHGs financed directly by the

Banks viz. CBs (Public Sector and Private Sector), RRBs, and Cooperative Banks. This is the bank-led microfinance channel which was initiated by NABARD in 1992.

Bank

NGO(facilitator)

SHG

MemberClient

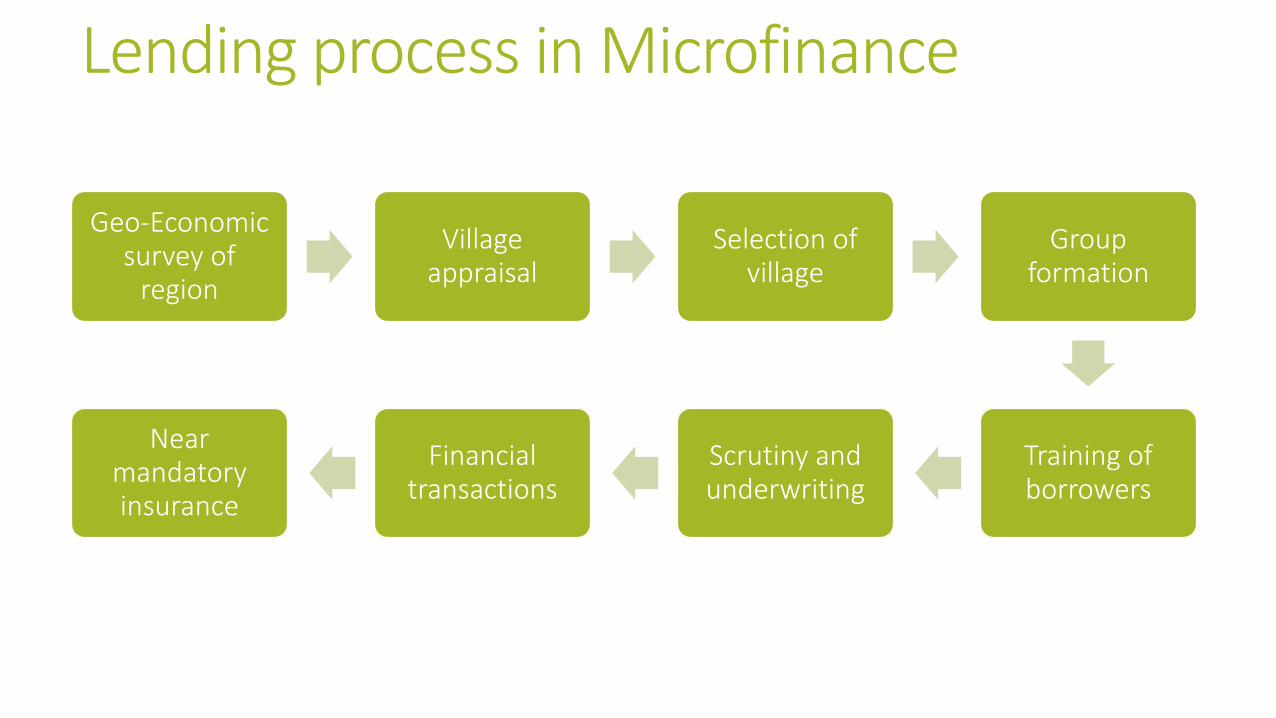

Lending process in Microfinance

Geo-Economic survey of

region

Village appraisal

Selection of village

Group formation

Training of borrowers

Scrutiny and underwriting

Financial transactions

Near mandatory insurance

Present Status of Microfinance in India

1) Overall Progress under SHGs-Bank Linkage:

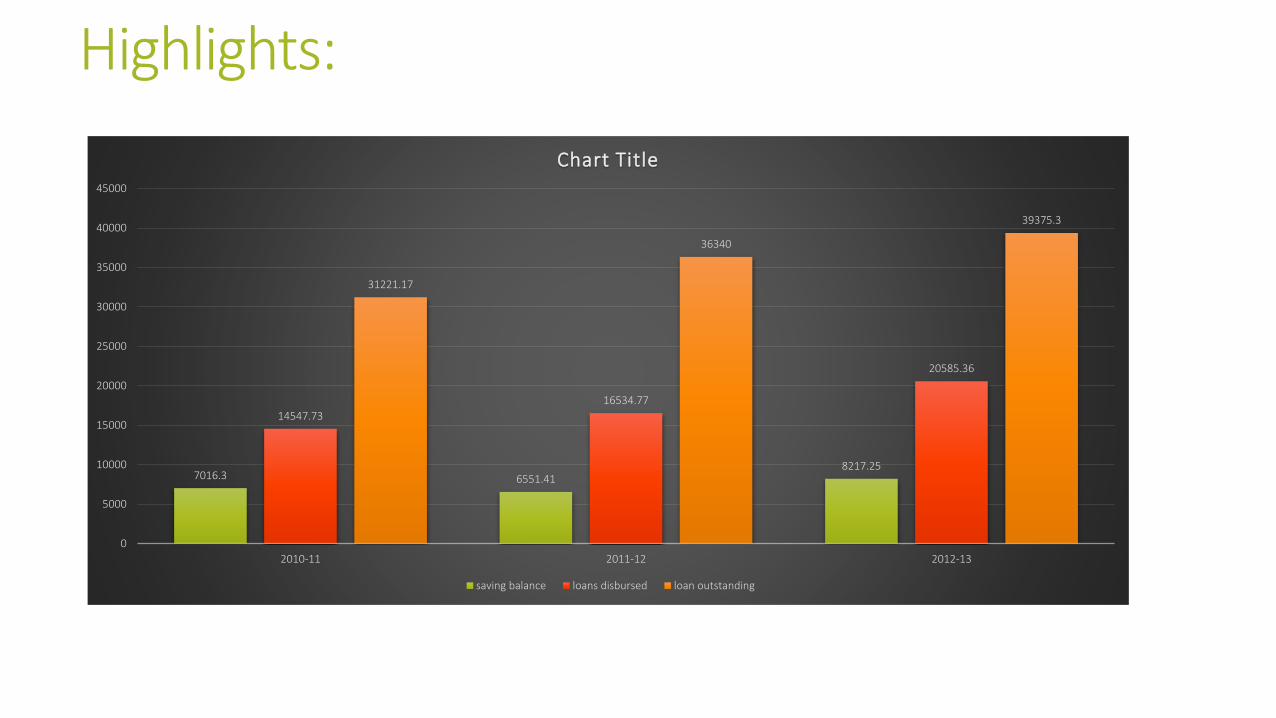

Under the SHG-Bank linkage programme, the coverage of rural households having access to regular savings through SHGs linked to banks came down by around 8% during the year to 95 million as on 31 March 2013. A similar decline of number of SHGs savings linked to Banks was also observed with only 73.18 lakh SHGs linked to Banks as against 79.60 lakh a year back. Number of SHGs having outstanding credit with banks, however, showed a marginal increase of 2% to 44.5 lakh as against 43.5 lakh the previous year. The average loan outstanding of SHGs with banks is `88,500 against `83,500 a year back.

Highlights:

7016.3 6551.418217.25

14547.73

16534.77

20585.36

31221.17

36340

39375.3

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

2010-11 2011-12 2012-13

Chart Title

saving balance loans disbursed loan outstanding

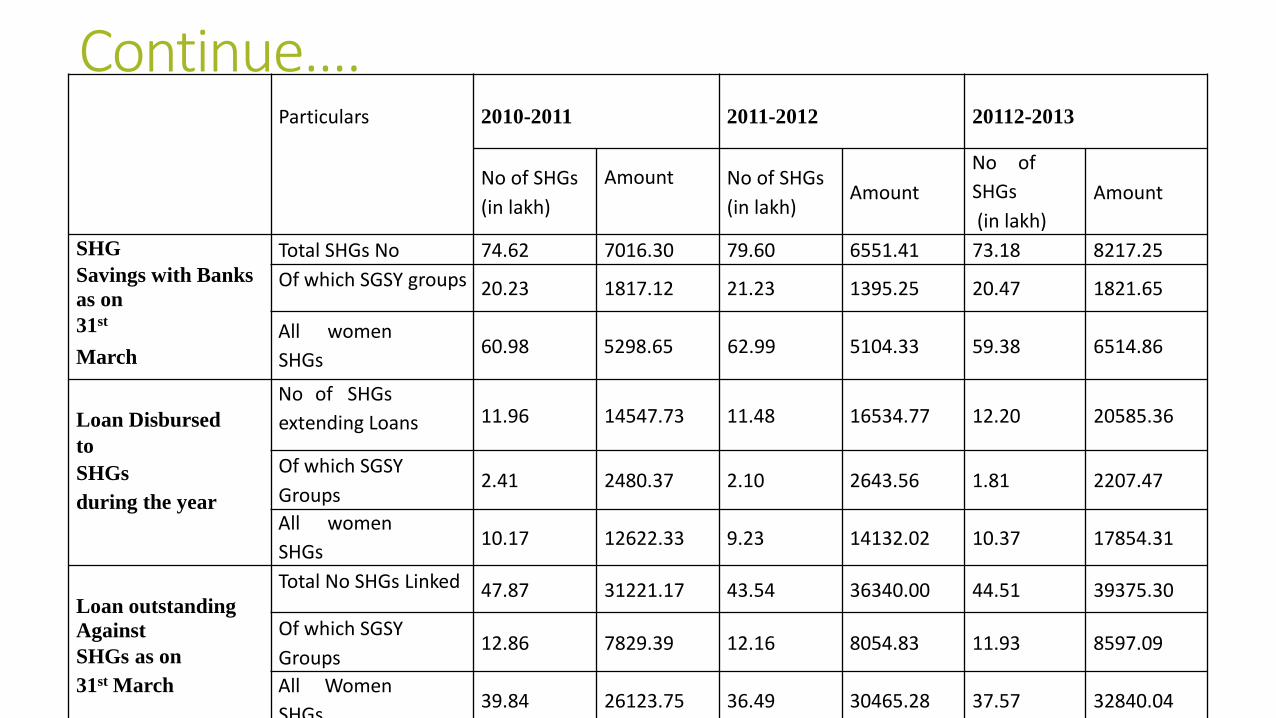

Continue….Particulars 2010-2011 2011-2012 20112-2013

No of SHGs

(in lakh)

Amount No of SHGs

(in lakh)Amount

No of

SHGs

(in lakh)

Amount

SHG

Savings with Banks

as on

31st

March

Total SHGs No 74.62 7016.30 79.60 6551.41 73.18 8217.25

Of which SGSY groups 20.23 1817.12 21.23 1395.25 20.47 1821.65

All women

SHGs 60.98 5298.65 62.99 5104.33 59.38 6514.86

Loan Disbursed

to

SHGs

during the year

No of SHGs

extending Loans 11.96 14547.73 11.48 16534.77 12.20 20585.36

Of which SGSY

Groups 2.41 2480.37 2.10 2643.56 1.81 2207.47

All women

SHGs 10.17 12622.33 9.23 14132.02 10.37 17854.31

Loan outstanding

Against

SHGs as on

31st March

Total No SHGs Linked 47.87 31221.17 43.54 36340.00 44.51 39375.30

Of which SGSY

Groups 12.86 7829.39 12.16 8054.83 11.93 8597.09

All Women

SHGs 39.84 26123.75 36.49 30465.28 37.57 32840.04

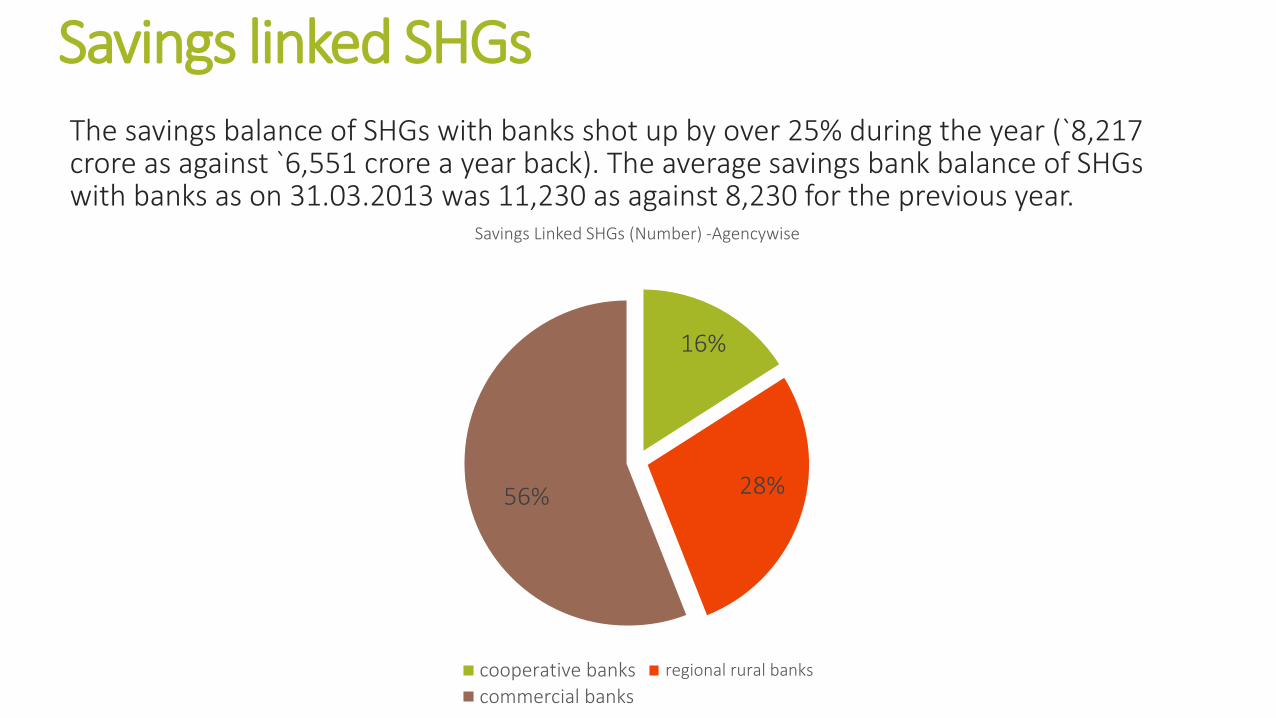

Savings linked SHGsThe savings balance of SHGs with banks shot up by over 25% during the year (`8,217 crore as against `6,551 crore a year back). The average savings bank balance of SHGs with banks as on 31.03.2013 was 11,230 as against 8,230 for the previous year.

16%

28%56%

Savings Linked SHGs (Number) ‐Agencywise

cooperative banks regional rural banks

commercial banks

Continue….2) Progress under MFI-Bank Linkage Programme: Fresh loans issued to MFIs by Banks showed a 50% increase

2010-11 2011-2012 2012-2013

No

of

MFIs

Amount

No

of

MFIs Amount

No

of

MFIs Amount

Loans Disbursed by

Banks To MFIs 471 8448.96 465 5205.29 426 7839.51

Loans outstanding

against MFIs as on 31st

March

2315 13730.62 1960 11450.35 2042 14425.84

Fresh loans as

% age to Loans

outstanding

61.5 45.5 54.3

Continue….Agency wise data:

Financing

Agency

Period

Loans disbursed to MFIs

during the year (crore)

Loan outstanding against MFIs

as on 31 March (crore)

No. of MFIs Amount No. of MFIs Amount

All Commercial

Banks

2011-12 336 4950.98 1684 9810.98

2012-13 368 7422.66 1769 12467.72

Regional Rural

Banks

2011-12 113 13.28 128 37.51

2012-13 14 4.58 153 70.66

Cooperative

Banks

2011-12 4 1.61 19 4.75

2012-13 3 4 18 6.83

SIDBI 2011-12 12 239.42 129 1597.11

2012-13 41 408.27 102 1880.63

Total by all

agencies

2011-12 465 5205.29 1960 11450.35

2012-13 426 7839.51 2042 14425.84

Impact of Microfinance

Impact on poverty: The study found that after joining the microfinance programme the income of the programme participants has increased by 2.5 times. The average individual income of the participants is Rs. 1,725 per month in post-SHG as compared to Rs. 718 per month in pre-SHG situation.

Impact on Employment: The study shows that microfinance programme has helped participants to increase their level of employment. Before joining the microfinance programme, 49 per cent of the total participants were employed and 51 per cent were unemployed. But after joining the microfinance programme the participants received loans and utilized these loans to start economic activities. As a result, 80 per cent of the participants were employed in post-SHG situation.

The study conducted under the supervision of Punjabi university on 21-Oct-2011 conclude the following impacts of micro finance in Punjab.

Continued…

Impact on Women Empowerment: Women empowerment is a process which gives power or authority to challenge submissive social condition or status of the women

The unique feature of microfinance programme is that it focuses on women for development. the microfinance programme increases the economic prospects of the participants which help them to have an access and control over the household economic resources such as ownership of house, ownership of land, and possession of gold and jewelry. In this way, the role of women is changed altogether; they become financially independent; and are involved in every financial decision of their families.

In the study it is found that 21 per cent of the participants govern the household financial decisions as compared to 11 per cent of the nonparticipants.

It has been observed that 46 and 79 per cent of the participants are more confident to visit a city and nearest town as compared to 14 and 69 per cent of nonparticipants respectively.

Key Issues in Micro financingLow Outreach: In India, MFI outreach is very low. It is only 8% as compared to 65% in Bangladesh.

Loan Default: Loan default is an issue that creates a problem in growth and expansion of the organization because around 73% loan default is identified in MFIs

Low Education Level: The level of education of the clients is low. So it creates a problem in the growth and expansion of the organization because its percentage is around 70% in MFIs

Language Barrier: Language barrier makes communication with the clients (verbal and written) is an issue that creates a problem in growth and expansion of the organization because around 54% language barrier has been identified in MFIs

Late Payments: Late payments are an issue that creates a problem in growth and expansion of the organization because late payments are around 70% in MFIs

Debt Management: Clients are uneducated about debt management 70% of the clients in MFIs are unaware of the fact that how to manage their debt. Because of the lack of education and understanding on the part of the clients.

High Interest Rate: MFIs are charging very high interest rates, which the poor find difficult to pay.

Negligence of Urban Poor: It has been noted that MFIs pay more attention to rural areas and largely neglect the urban poor.

Barriers and Challenges for MFIs

Financial illiteracy

Inability to generate sufficient funds

Dropouts and Migration of group members

Cluster formation – fight to grab established market

Multiple Lending and Over-Indebtedness

High Transaction Cost

Loan Collection Method

Fraud

Suggestions and Recommendations

1. Proper Regulation

2. Field Supervision

3. Encourage rural penetration

4. Complete range of Products

5. Transparency of Interest rates

6. Technology to reduce Operating Cost

7. Alternative sources of Fund:

By getting converted to for-profit company i.e. NBFC

Portfolio Buyout

Securitization of Loans

conclusionMicrofinance has a long way despite doubts expressed and criticism launched about its viability, impact, and poverty fighting capacity. The task of building a poverty-free world is yet to be finished. There are still over 1.2 billion people living in extreme poverty on this planet. They are not living in one country or region but spread all over the world. The last decade has witnessed an impressive growth of microfinance; lack of funding is still considered a major obstacle in the way of its growth. However, it is encouraging that the situation is changing. People with some special skills have to be given priority in lending microcredit. These clients should also be provided with post loan technical and professional aid for success of their microenterprises. If government and MFIs act together then microcredit can play a great role in poverty alleviation.