microfinance in india

TRANSCRIPT

Presented By:- D.B.Bharghav Reddy (1st sem PGDM)

Micro Finance is the supply of loans, savings, and other basic financial

service to the poor .

- CGAP

To most, micro finance means providing very poor families with very small

loans (micro credit) to help them engage in productive activities or grow their

tiny businesses.

- Financial Gateway

Microfinance refers to small-scale financial services including both credits

and deposits provided to people who farm or fish or herd; operate small or

microenterprises where goods are produced, recycled, repaired, or traded;

provide services; work for wages or commissions; gain income from renting

out small amounts of land, vehicles, draft animals, or machinery and tools; in

both rural and urban areas.

“Microfinance is an economic development tool whose

objective is to assist the poor to work their way out of

poverty. It covers a range of services which include, in

addition to the provision of credit, many other services

such as savings, insurance, money transfers,

counseling, etc.”

– Reserve Bank of

India

In simple words, Microfinance serves as a tool for

providing financial services to the low-income

population., which do not have access to the

mainstream financial services.

Beneficiaries are from low income group.

Loans are of small amount.

Short duration loans .

Loans are offered without collateral.

High frequency of payment.

Loans are generally taken for income

generation purposes.

Prefer women costumers over men.

Traditionally , Macro-financial institutes like banks have been

reluctant to provide financial services to clients with little or

no cash income, because of various reasons –

1. ‘Break Even Point‘ in providing loans.

2. Few assets to be secured as collateral.

3. Lack of loan and other financial services from banks and

other institutes forces them to rely heavily on relatives or local

money lenders at the time of need .

Usually interest rate of moneylenders are very high.

According to a 1995 World Bank estimate, in most

developing countries the formal financial system reaches

only the top 25% of the economically active population -

the bottom 75% have no access to financial services

apart from moneylenders .

Micro-Credit movement started in 1970’s countries like

Bangladesh ( Grameen Bank led by Muhammad Yunus)

, Pakistan , Vietnam etc.

2005 is Declared as International year of Microcredit by

The Economic and Social Council of the United Nations.

In Bangladesh microfinance has successfully enabled

extremely impoverished people to engage in self-

employment projects that allow them to generate an

income and, in many cases, begin to build wealth and

exit poverty.

1974 – Establishment of Self-Employed Women’s Association

(SEWA) in Gujarat.

Sep 26, 1975 – Rural bank Ordinance was passed.

Oct 02, 1975 – Prathama bank (first RRB) came into existence.

1976 – Ordinance was replaced by Regional Rural Bank Act.

July 12, 1982 – NABARD was established on the recommendations

of Shivaraman Committee, by an act of Parliament to implement the

National Bank for Agriculture and Rural Development Act 1981.

Apr 02, 1990 – SIDBI was established through Small Industries

Development Bank of India Act 1989.

1992 – NABARD launched SHGs-Bank Linkage program.

1999 – SIDBI created Microcredit (SFMC) to create a national

network of strong, viable and sustainable Microfinance

Institutions from the informal and formal financial sector to

provide microfinance services to the poor, especially women’’.

2006 – NABARD launched the ‘Micro-Enterprise Development

Programme’ (MEDP) for skill development.

It provides a long-term increase in income and

consumption of poor families.

Access to credit helps the poor to smooth cash flows

and avoid periods where access to food, clothing,

shelter, or education is lost.

Credit make it easier to manage shocks like sickness of

a wage earner, theft, or natural disasters.

It provides support to Micro Enterprises . Thus booster

support to Entrepreneurship among the jobless people .

Plays an important role in Women Empowerment ,

particularly in Developing countries like India

Associations , Ex : Self Help Groups, SHGs (India)

Bank Guarantees , Ex : Latin America Bridge Fund

Community Banking , Ex: Grameen Bank (Ban.)

Cooperatives , Ex: Co-operative Bank (England)

Credit Unions

Non-Governmental Organizations , Ex: KIVA ,US

For-profit Banks , Ex: Khushali Bank (Pakistan)

Rotating Savings and Credit Associations

(ROSCAs)

Microfinance institutions in India are registered as one of the following five

entities:

1. Non Government Organizations engaged in microfinance (NGO-MFIs), comprised

of Societies and Trusts .

2. Cooperatives registered under the conventional state-level cooperative acts, the

national level multi-state Cooperative Legislation Act (MSCA 2002), or under the

new state-level Mutually Aided Cooperative acts (MACS Act).

3.Section 25 Companies (not-for-profit).

4. For-profit Non-Banking Financial Companies (NBFCs)

5. NBFC-MFIs

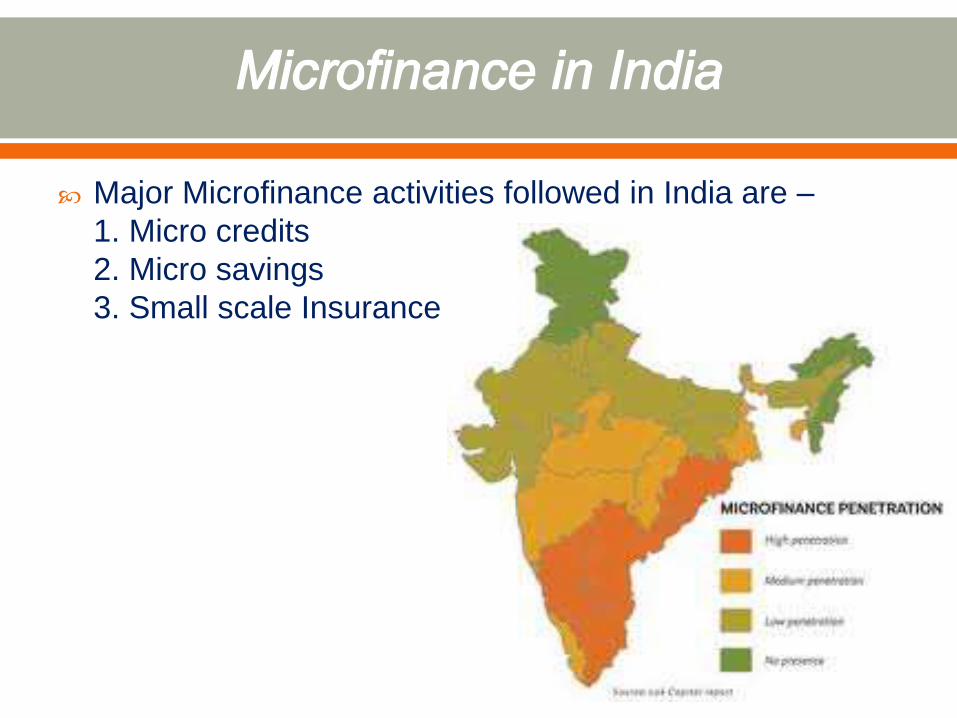

Major Microfinance activities followed in India are –

1. Micro credits

2. Micro savings

3. Small scale Insurance

What are NGOs?

>NGOs are voluntary social work organization who renders

help to government and society for improvement of quality of

life people

>Help in the formation of SHGs

>To reduce the smaller transaction NGOs help banks

>Over the last quarter century, a few organizations, outside the

purview of the public sector, have succeeded in effective

poverty alleviation through micro-credit

>Main objective is to draw attention about microfinance by

conduction meetings in rural areas

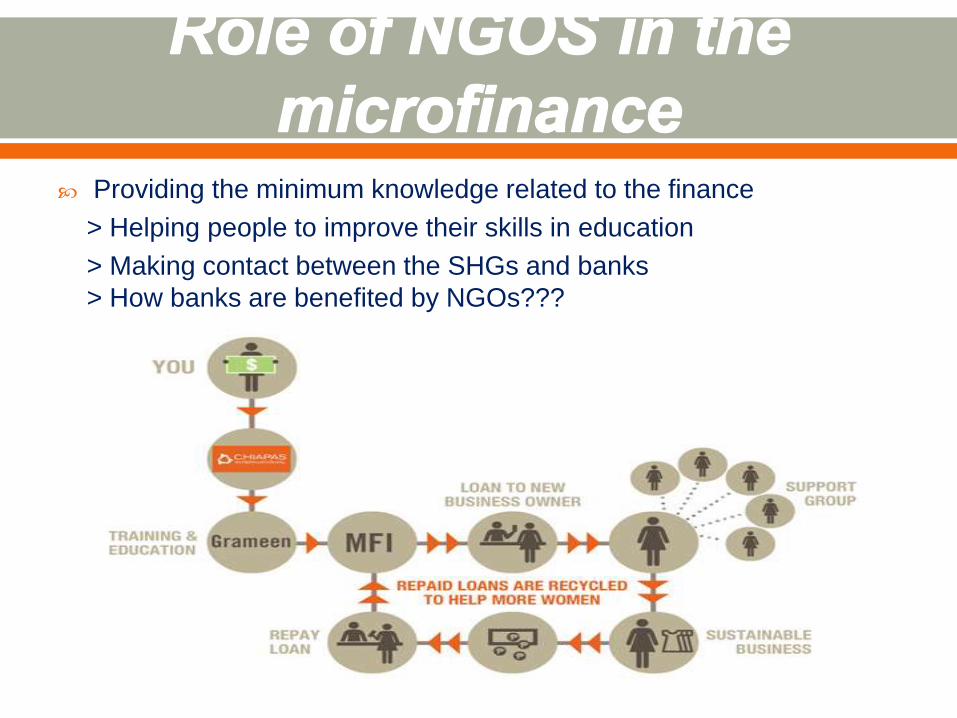

Providing the minimum knowledge related to the finance

> Helping people to improve their skills in education

> Making contact between the SHGs and banks

> How banks are benefited by NGOs???

Government interested in SHGs

> Rashtriya Mahila Kosh , Indira Mahila Yojana,

Swarnajayanti Gram Swarojgar Yojana (SGSY) launched in 1999

> Swarnjayanti Gram Swarojgar Yojana (SGSY) has emerged as a

main

anti-poverty programme

Providing refinance to lending institutions in rural

areas

Bringing about or promoting institutional

development .

Evaluating, monitoring and inspecting the client

banks

Acts as a coordinator in the operations of rural credit

institutions.

Vision:

Empowerment of rural poor by improving their access to the formal

credit system through various MF innovations in a cost effective

and sustainable manner .

Mission:

Promoting sustainable and equitable agriculture and rural development

through effective credit support, related services, institution building

and other innovative initiatives.

SHGs is a small group of rural poor, who have voluntarily come forward to form a group for improvement of the social and economic status of the members.

Homogeneous group of about 15 to 20.

Every member to save small amounts regularly.

Every member learns prioritization and financial discipline.

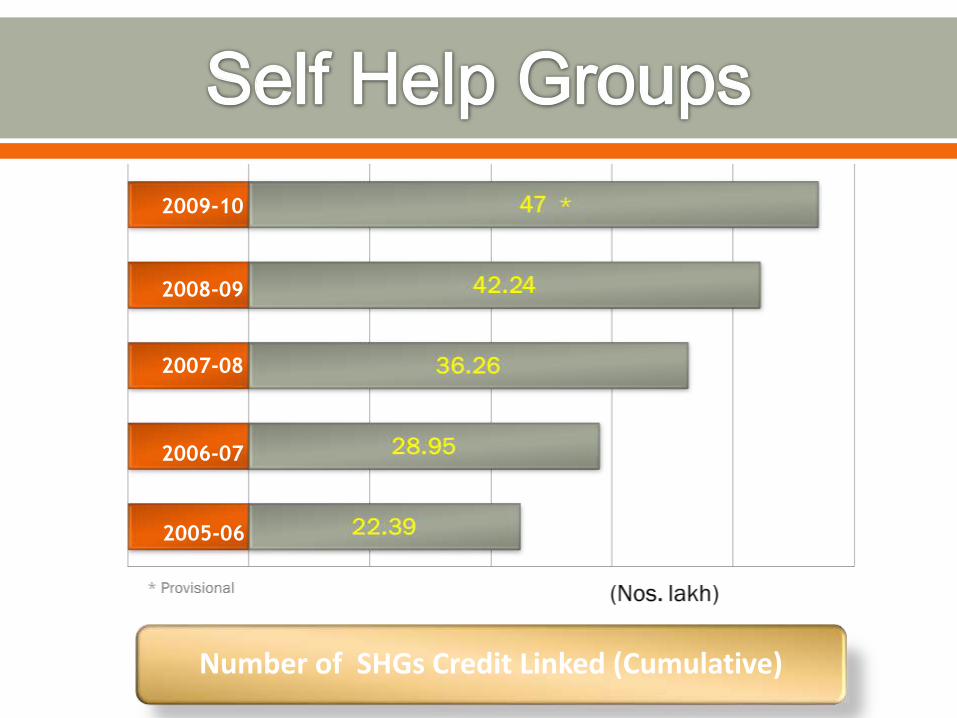

Number of SHGs Credit Linked (Cumulative)

2005-06

2006-07

2007-08

2008-09

2009-10

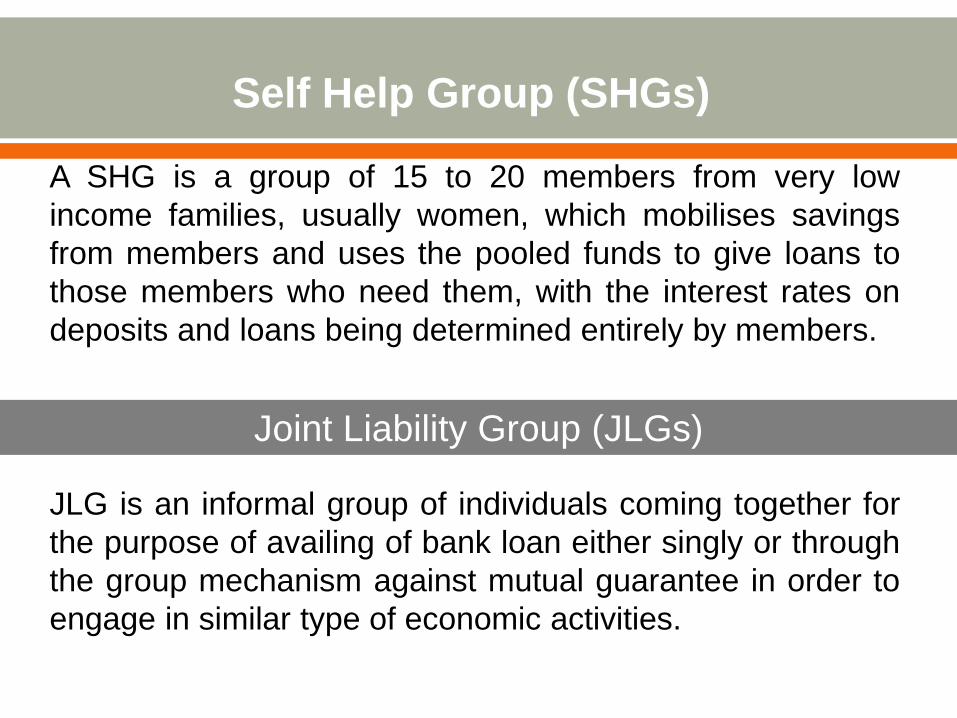

Self Help Group (SHGs)

A SHG is a group of 15 to 20 members from very low

income families, usually women, which mobilises savings

from members and uses the pooled funds to give loans to

those members who need them, with the interest rates on

deposits and loans being determined entirely by members.

Joint Liability Group (JLGs)

JLG is an informal group of individuals coming together for

the purpose of availing of bank loan either singly or through

the group mechanism against mutual guarantee in order to

engage in similar type of economic activities.

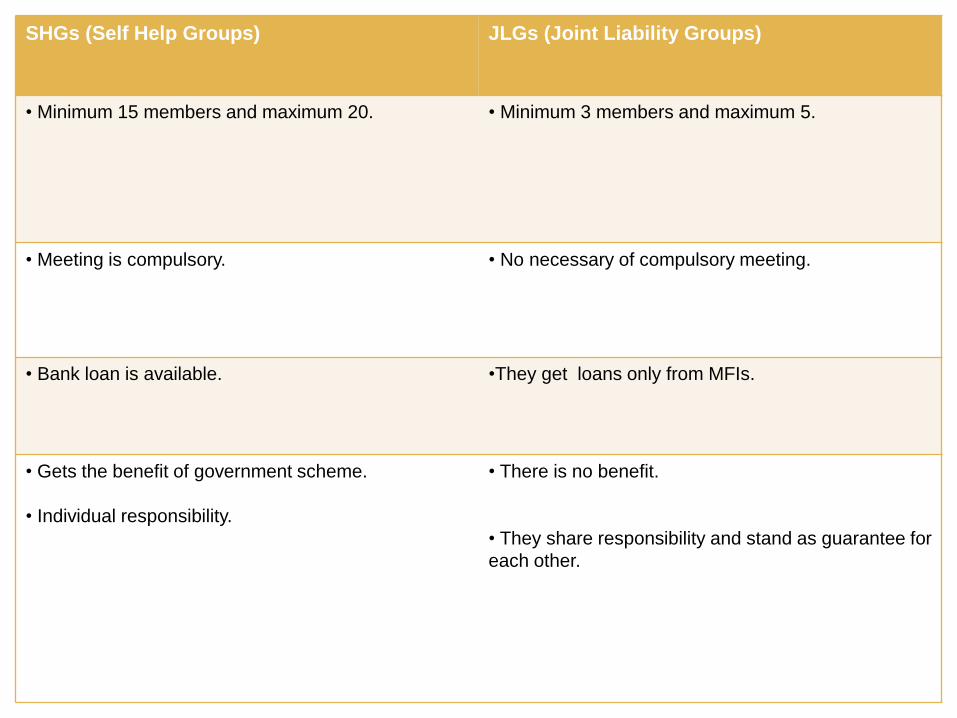

SHGs (Self Help Groups) JLGs (Joint Liability Groups)

• Minimum 15 members and maximum 20. • Minimum 3 members and maximum 5.

• Meeting is compulsory. • No necessary of compulsory meeting.

• Bank loan is available. •They get loans only from MFIs.

• Gets the benefit of government scheme.

• Individual responsibility.

• There is no benefit.

• They share responsibility and stand as guarantee for

each other.

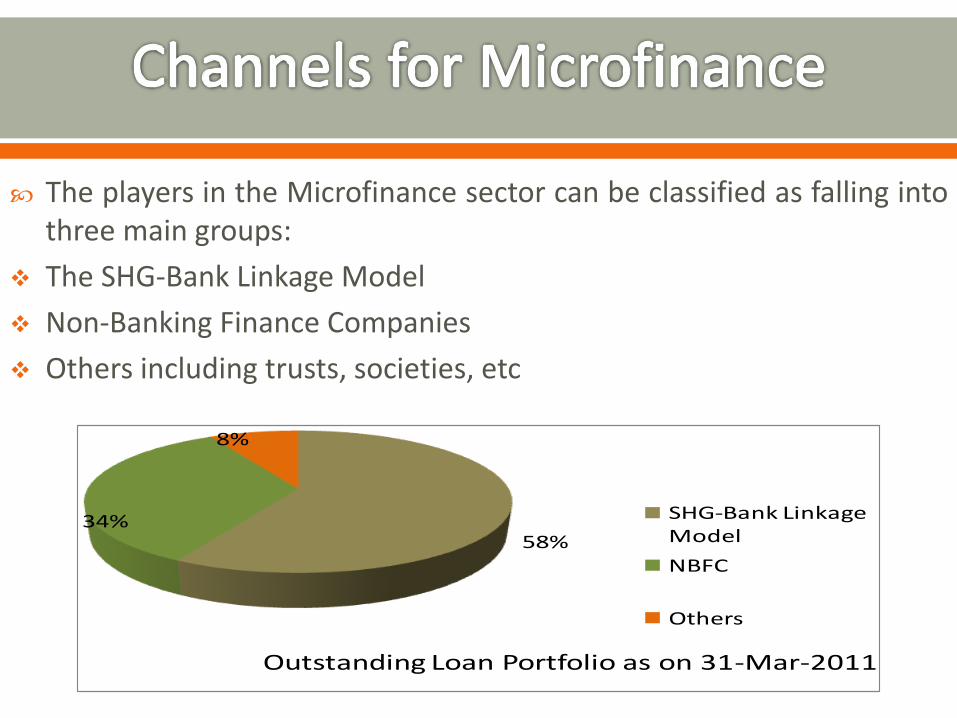

The players in the Microfinance sector can be classified as falling intothree main groups:

The SHG-Bank Linkage Model

Non-Banking Finance Companies

Others including trusts, societies, etc

58%34%

8%

Outstanding Loan Portfolio as on 31-Mar-2011

SHG-Bank Linkage Model

NBFC

Others

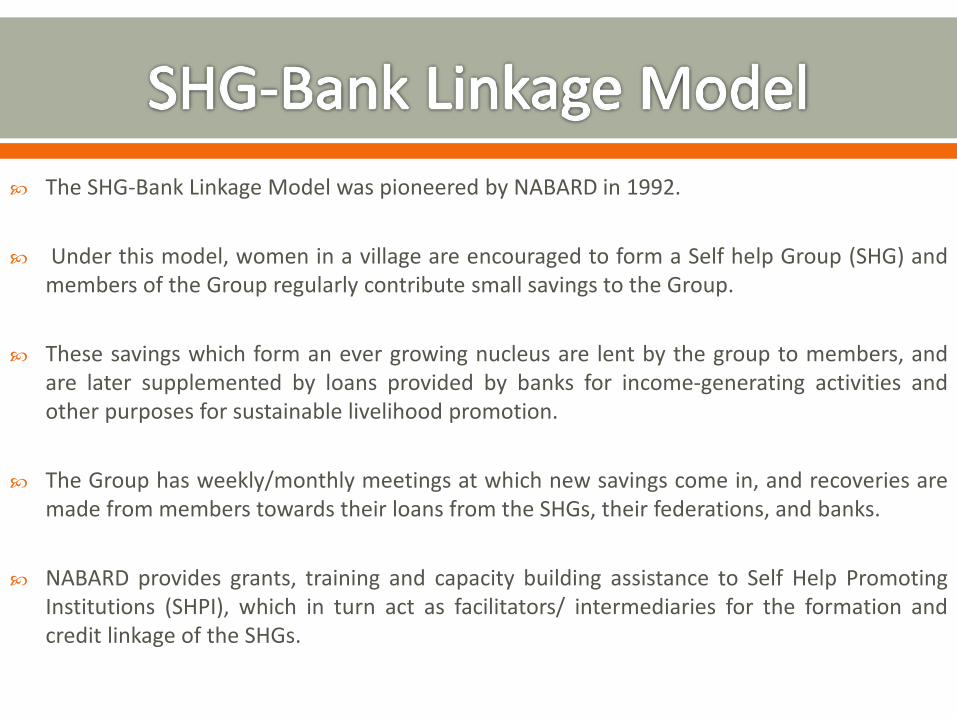

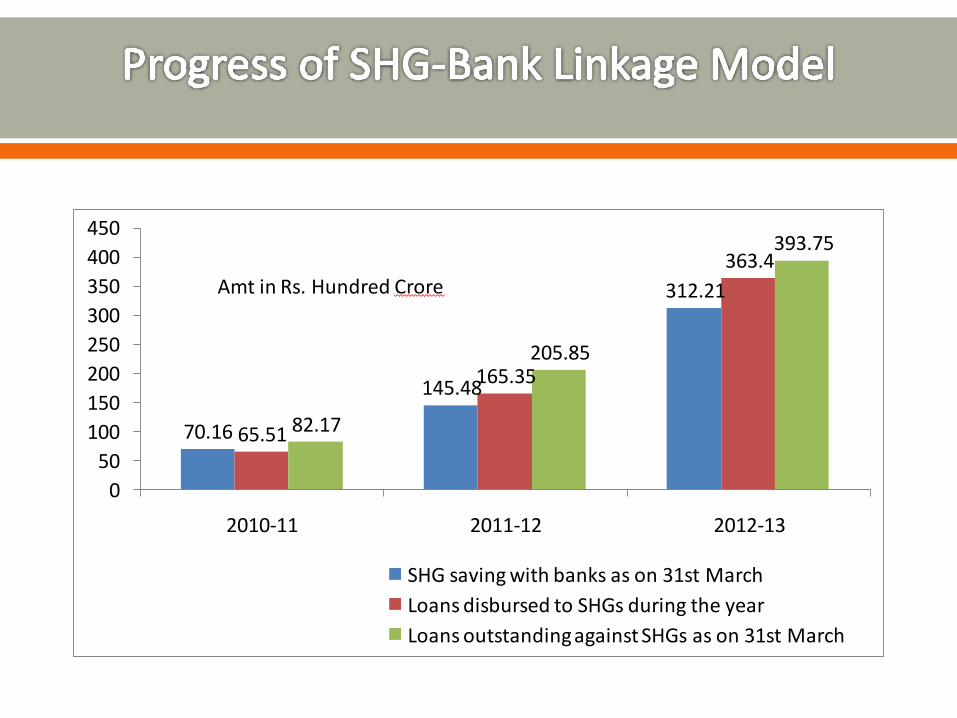

The SHG-Bank Linkage Model was pioneered by NABARD in 1992.

Under this model, women in a village are encouraged to form a Self help Group (SHG) andmembers of the Group regularly contribute small savings to the Group.

These savings which form an ever growing nucleus are lent by the group to members, andare later supplemented by loans provided by banks for income-generating activities andother purposes for sustainable livelihood promotion.

The Group has weekly/monthly meetings at which new savings come in, and recoveries aremade from members towards their loans from the SHGs, their federations, and banks.

NABARD provides grants, training and capacity building assistance to Self Help PromotingInstitutions (SHPI), which in turn act as facilitators/ intermediaries for the formation andcredit linkage of the SHGs.

70.16

145.48

312.21

65.51

165.35

363.4

82.17

205.85

393.75

0

50

100

150

200

250

300

350

400

450

2010-11 2011-12 2012-13

SHG saving with banks as on 31st March

Loans disbursed to SHGs during the year

Loans outstanding against SHGs as on 31st March

Amt in Rs. Hundred Crore

Under the NBFC model, NBFCs encourage villagers to form Joint Liability Groups (JLG) and give loans to the individual members of the JLG.

The individual loans are jointly and severally guaranteed by the other members of the Group.

Many of the NBFCs operating this model started off as non-profit entities providing micro-credit and other services to the poor.

However, as they found themselves unable to raise adequate resources for a rapid growth of the activity, they converted themselves into for-profit NBFCs.

Others entered the field directly as for-profit NBFCs seeing this as a viable business proposition.

Significant amounts of private equity funds have consequently been attracted to this sector.

Initiative taken by govt of A.P to enhance the profit of shg

members

Loans are at 2.5 % interest

Achieved great response from poor

Presently there are 1.15 lakh DWCRA groups and 2.19

lakh SHG groups in Andhra Pradesh with a membership

of 46 lakh women having a savings of Rs.300 crores.

It is the state that have only microfinance as tool

eliminate the poor.

In Orissa Mission shakti , a government driven

programme, formed in 2001 with a target to organize 2

lakhs WSHGs(women self help group) covering all

revenue villages of the State. The main aim is to provide

supports to different stakeholders working in the field of

women empowerment such as Banks, NGOs, MFIs and

other institutions.

There are around 35 MFIs registered in the state out of

which 8-10 are functional, with the recovery rate of these

institutions being around 95%..

Micro-Finance Institutions (MFIs) operating in Orissa

have advanced loans worth Rs 1500 crore in the past

three to four years, reaching out to more than two million

customers in the state

Annapurna Microfinance Pvt Ltd

BSS Microfinance Pvt Ltd

Cashpor Micro Credit

Disha Microfin Pvt Ltd

Equitas Microfinance Pvt Ltd

Fusion Microfinance Pvt Ltd

Grameen Financial Services Pvt Ltd

Janalakshmi Financial Services Pvt Ltd

SKS Microfinance Ltd

Sonata Finance Pvt Ltd

Suryoday Micro Finance Pvt Ltd

Ujjivan Financial Services Pvt Ltd

Estimated that in next five years, 65% of the poor people will have excess to MFIs.

Many Pvt. Banks and Foreign Banks would enter this business segment, because of very low NPAs.

Estimated that 5 % of the number of people below the poverty line

will get reduced in the next 5 years.(World Bank report)

In India micro-finance has succeeded with repayment rates upto

90% reported all across the country ( from the states like AP, Tamil

Nadu, Karnataka, Kerala ,West Bengal and Orissa etc. )

This tells us that micro finance has certainly has the capacity to

reduce poverty by a great margin

Any

Questions