md & analytical manager investor communications - americas ... · 1860: henry varnum poor’s...

TRANSCRIPT

S&P

Glo

bal R

atin

gs:

Insu

ranc

e R

atin

gs H

isto

ry, M

etho

dolo

gy

and

Pro

cess

NA

IC/C

IPR

Web

inar

O

ctob

er 1

4, 2

016

Kev

in A

hern

MD

& A

naly

tical

Man

ager

In

sura

nce

Rat

ings

Ger

ard

Pain

ter

Sr. D

irect

orIn

vest

or C

omm

unic

atio

ns -

Am

eric

as

Copy

right

© 20

16 b

y S&P

Glo

bal.

All r

ight

s res

erve

d.

Age

nda

2

•S&

P’s

Rat

ings

His

tory

in th

e In

sura

nce

Indu

stry

•G

loba

l Ins

uran

ce R

atin

gs C

over

age

•R

atin

gs P

roce

ss•

S&P

Fina

ncia

l Str

engt

h R

atin

gs S

cale

•In

sura

nce

Rat

ings

Fra

mew

ork

•R

atin

gs D

istr

ibut

ion

•A

ppen

dix

•C

apita

l Ana

lysi

s

•R

atin

gs P

erfo

rman

ce•

Ass

essm

ent o

f Ent

erpr

ise

Ris

k M

anag

emen

t

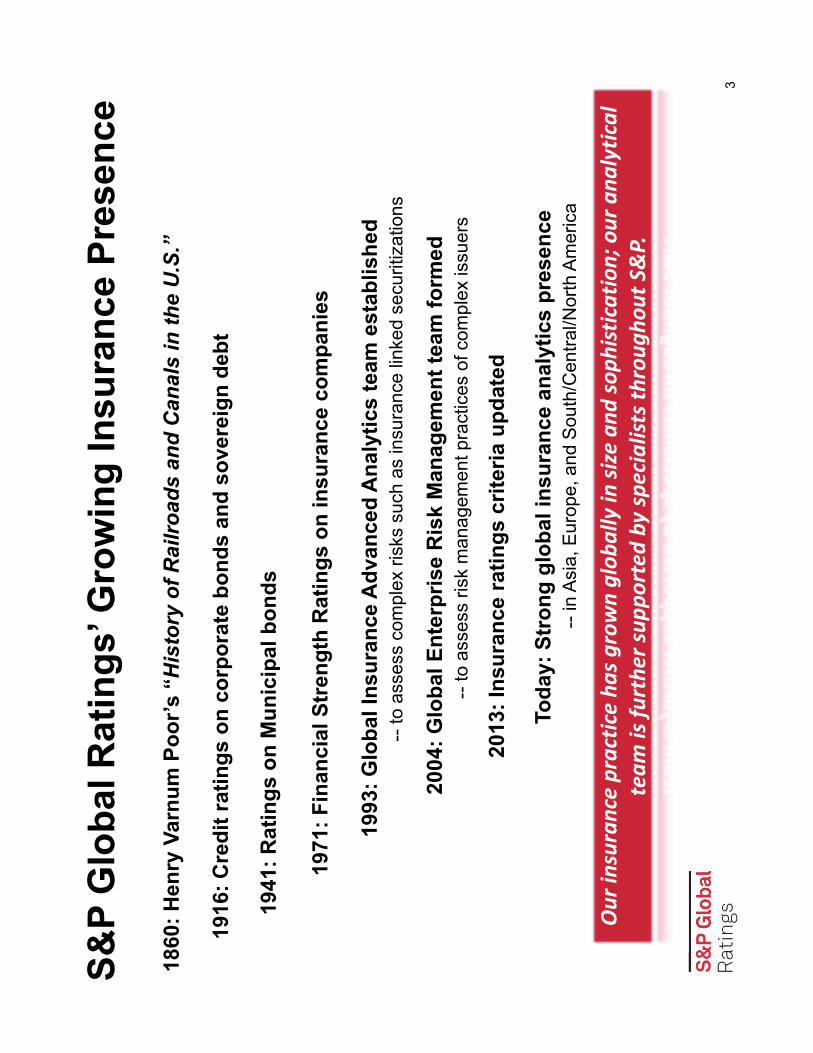

S&P

Glo

bal R

atin

gs’ G

row

ing

Insu

ranc

e Pr

esen

ce

3

1993

: Glo

bal I

nsur

ance

Adv

ance

d A

naly

tics

team

est

ablis

hed

--to

ass

ess

com

plex

risk

s su

ch a

s in

sura

nce

linke

d se

curit

izat

ions

2004

: Glo

bal E

nter

pris

e R

isk

Man

agem

ent t

eam

form

ed

--to

ass

ess

risk

man

agem

ent p

ract

ices

of c

ompl

ex is

suer

s

1971

: Fin

anci

al S

tren

gth

Rat

ings

on

insu

ranc

e co

mpa

nies

2013

: Ins

uran

ce ra

tings

crit

eria

upd

ated

1860

: Hen

ry V

arnu

m P

oor’s

“H

isto

ry o

f Rai

lroad

s an

d C

anal

s in

the

U.S

.”

Toda

y: S

tron

g gl

obal

insu

ranc

e an

alyt

ics

pres

ence

--

in A

sia,

Eur

ope,

and

Sou

th/C

entra

l/Nor

th A

mer

ica

Our

insu

ranc

e pr

actic

e ha

s gro

wn

glob

ally

in si

ze a

nd so

phist

icat

ion;

our

ana

lytic

al

team

is fu

rthe

r sup

port

ed b

y sp

ecia

lists

thro

ugho

ut S

&P.

1916

: Cre

dit r

atin

gs o

n co

rpor

ate

bond

s an

d so

vere

ign

debt

1941

: Rat

ings

on

Mun

icip

al b

onds

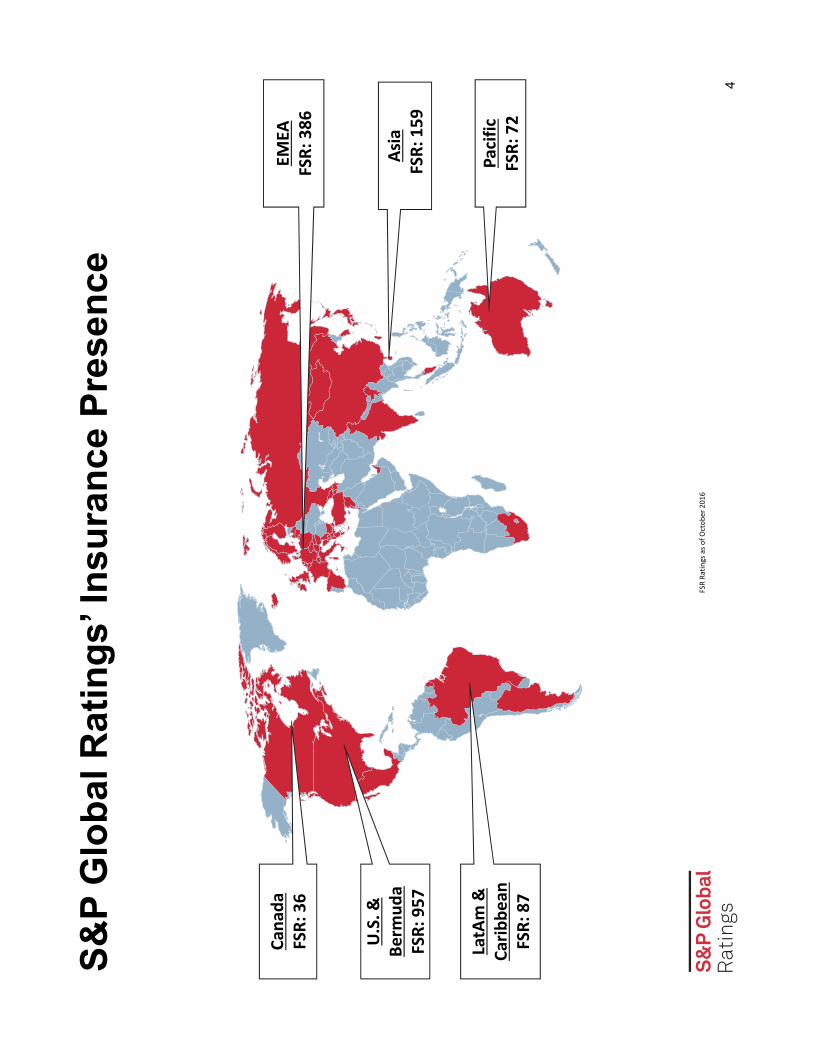

S&P

Glo

bal R

atin

gs’ I

nsur

ance

Pre

senc

e

4

U.S

. &

Berm

uda

FSR:

957

LatA

m &

Ca

ribbe

anFS

R: 8

7

Paci

ficFS

R: 7

2

Asia

FSR:

159

Cana

daFS

R: 3

6EM

EAFS

R: 3

86

FSR

Ratin

gs a

s of O

ctob

er 2

016

Our

Rat

ing

Proc

ess

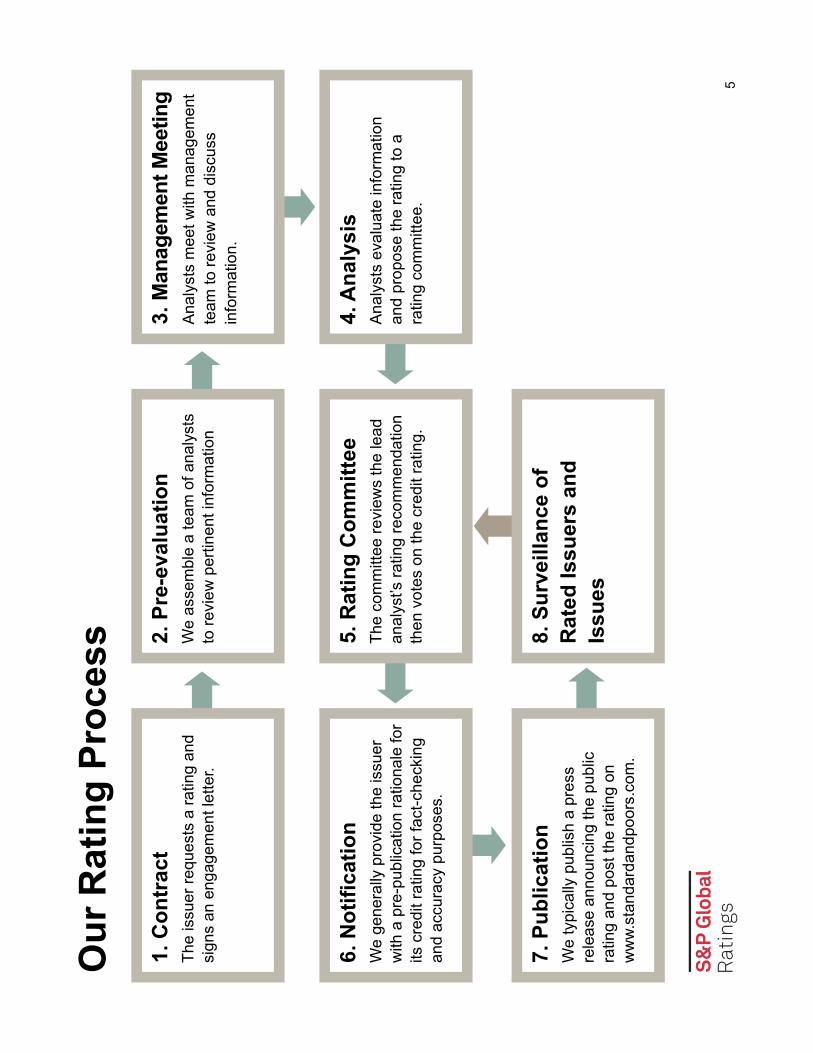

5

1. C

ontr

act

The

issu

er re

ques

ts a

ratin

g an

d si

gns

an e

ngag

emen

t let

ter.

2. P

re-e

valu

atio

nW

e as

sem

ble

a te

am o

f ana

lyst

s to

revi

ew p

ertin

ent i

nfor

mat

ion.

3. M

anag

emen

t Mee

ting

Ana

lyst

s m

eet w

ith m

anag

emen

t te

am to

revi

ew a

nd d

iscu

ss

info

rmat

ion.

6. N

otifi

catio

nW

e ge

nera

lly p

rovi

de th

e is

suer

w

ith a

pre

-pub

licat

ion

ratio

nale

for

its c

redi

t rat

ing

for f

act-c

heck

ing

and

accu

racy

pur

pose

s .

5. R

atin

g C

omm

ittee

The

com

mitt

ee re

view

sth

e le

ad

anal

yst’s

ratin

g re

com

men

datio

n th

en v

otes

on

the

cred

it ra

ting.

4. A

naly

sis

Ana

lyst

s ev

alua

te in

form

atio

n an

d pr

opos

e th

e ra

ting

to a

ra

ting

com

mitt

ee.

7. P

ublic

atio

nW

e ty

pica

lly p

ublis

h a

pres

s re

leas

e an

noun

cing

the

publ

ic

ratin

g an

d po

st th

e ra

ting

on

ww

w.st

anda

rdan

dpoo

rs.c

om.

8. S

urve

illan

ce o

f R

ated

Issu

ers

and

Issu

es

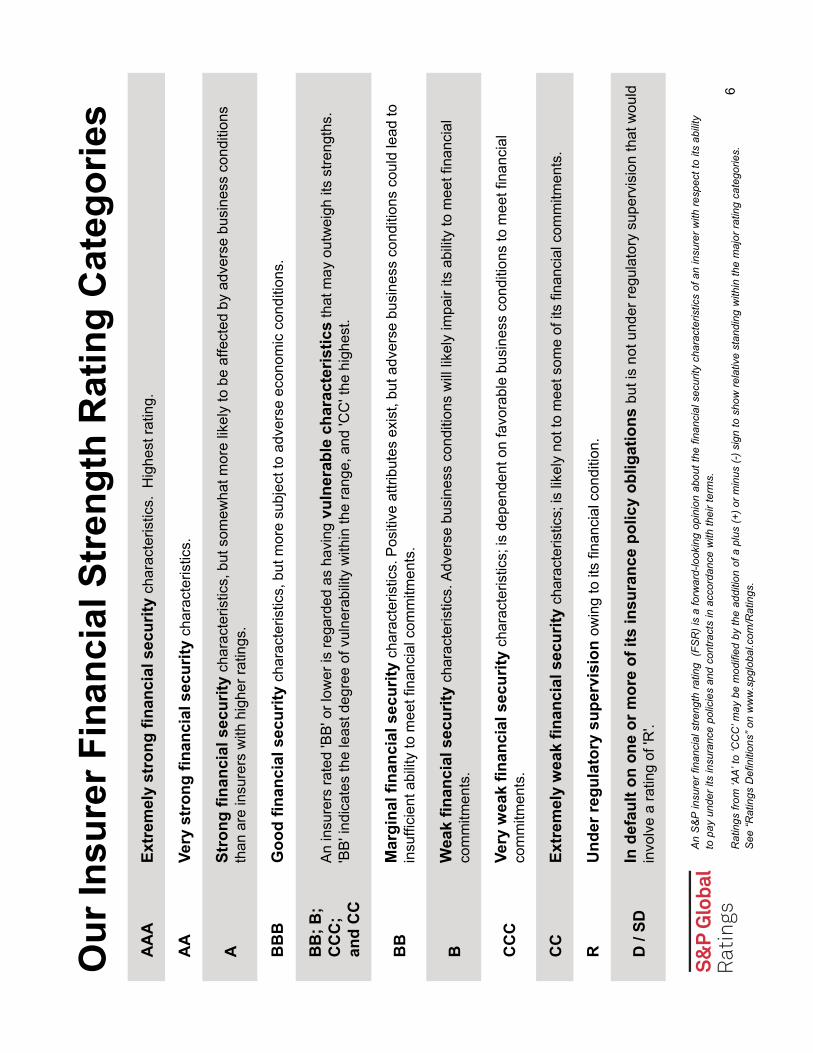

AA

AEx

trem

ely

stro

ng fi

nanc

ial s

ecur

itych

arac

teris

tics.

Hig

hest

ratin

g.

AA

Very

str

ong

finan

cial

sec

urity

char

acte

ristic

s.

ASt

rong

fina

ncia

l sec

urity

char

acte

ristic

s, b

ut s

omew

hat m

ore

likel

y to

be

affe

cted

by

adve

rse

busi

ness

con

ditio

ns

than

are

insu

rers

with

hig

her r

atin

gs.

BB

BG

ood

finan

cial

secu

rity

char

acte

ristic

s,bu

t mor

e su

bjec

t to

adve

rse

econ

omic

con

ditio

ns.

BB

; B;

CC

C;

and

CC

An

insu

rers

rate

d 'B

B' o

r low

er is

rega

rded

as

havi

ng v

ulne

rabl

e ch

arac

teris

tics

that

may

out

wei

gh it

s st

reng

ths.

'B

B' i

ndic

ates

the

leas

t deg

ree

of v

ulne

rabi

lity

with

in th

e ra

nge,

and

'CC

' the

hig

hest

.

BB

Mar

gina

l fin

anci

al s

ecur

ity c

hara

cter

istic

s. P

ositi

ve a

ttrib

utes

exi

st, b

ut a

dver

se b

usin

ess

cond

ition

s co

uld

lead

to

insu

ffici

ent a

bilit

y to

mee

t fin

anci

al c

omm

itmen

ts.

BW

eak

finan

cial

sec

urity

cha

ract

eris

tics.

Adv

erse

bus

ines

s co

nditi

ons

will

like

ly im

pair

its a

bilit

y to

mee

t fin

anci

al

com

mitm

ents

.

CC

CVe

ry w

eak

finan

cial

sec

urity

cha

ract

eris

tics;

is d

epen

dent

on

favo

rabl

e bu

sine

ss c

ondi

tions

to m

eet f

inan

cial

co

mm

itmen

ts.

CC

Extr

emel

y w

eak

finan

cial

sec

urity

cha

ract

eris

tics;

is li

kely

not

to m

eet s

ome

of it

s fin

anci

al c

omm

itmen

ts.

RU

nder

regu

lato

ry s

uper

visi

on o

win

g to

its

finan

cial

con

ditio

n.

D /

SDIn

def

ault

on o

ne o

r mor

e of

its

insu

ranc

e po

licy

oblig

atio

nsbu

t is

not u

nder

regu

lato

ry s

uper

visi

on th

at w

ould

in

volv

e a

ratin

g of

'R'.

An

S&

P in

sure

r fin

anci

al s

treng

th ra

ting

(FS

R) i

s a

forw

ard-

look

ing

opin

ion

abou

t the

fina

ncia

l sec

urity

cha

ract

eris

tics

of a

n in

sure

r with

resp

ect t

o its

abi

lity

to p

ay u

nder

its

insu

ranc

e po

licie

s an

d co

ntra

cts

in a

ccor

danc

e w

ith th

eir t

erm

s.

Rat

ings

from

‘AA

’ to

‘CC

C’ m

ay b

e m

odifi

ed b

y th

e ad

ditio

n of

a p

lus

(+) o

r min

us (-

) sig

n to

sho

w re

lativ

e st

andi

ng w

ithin

the

maj

or ra

ting

cate

gorie

s.

See

“Rat

ings

Def

initi

ons”

on

ww

w.s

pglo

bal.c

om/R

atin

gs.

Our

Insu

rer F

inan

cial

Str

engt

h R

atin

g C

ateg

orie

s

6

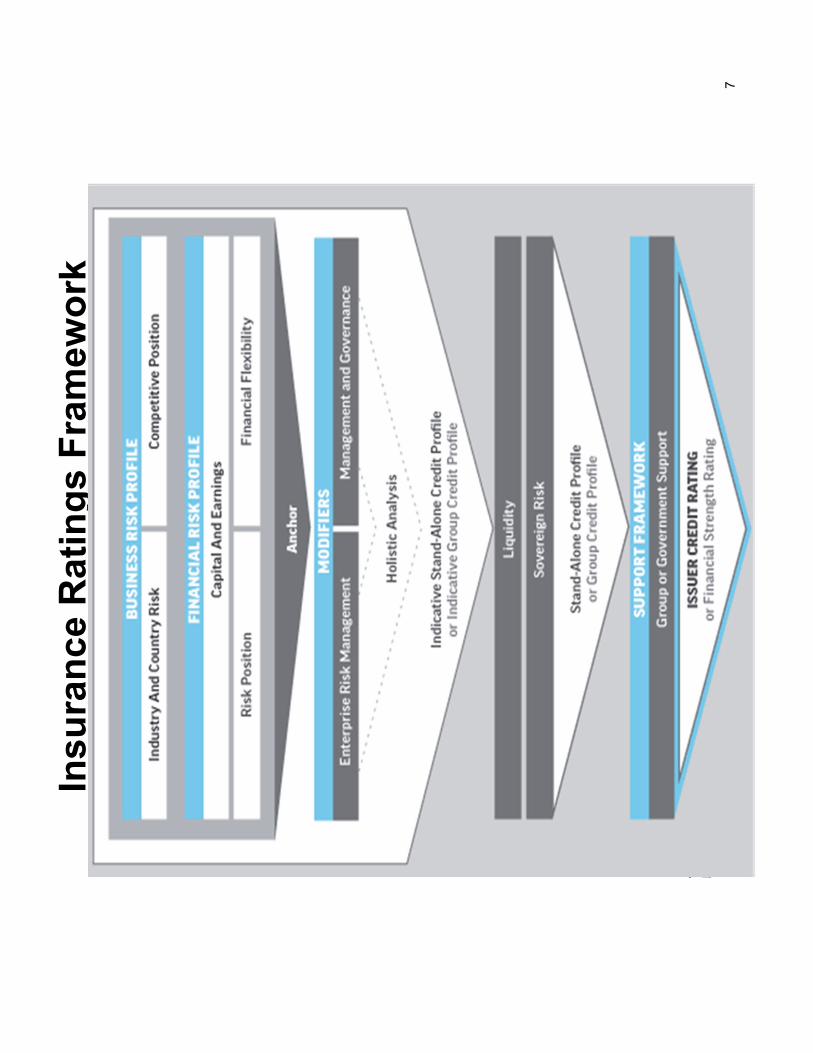

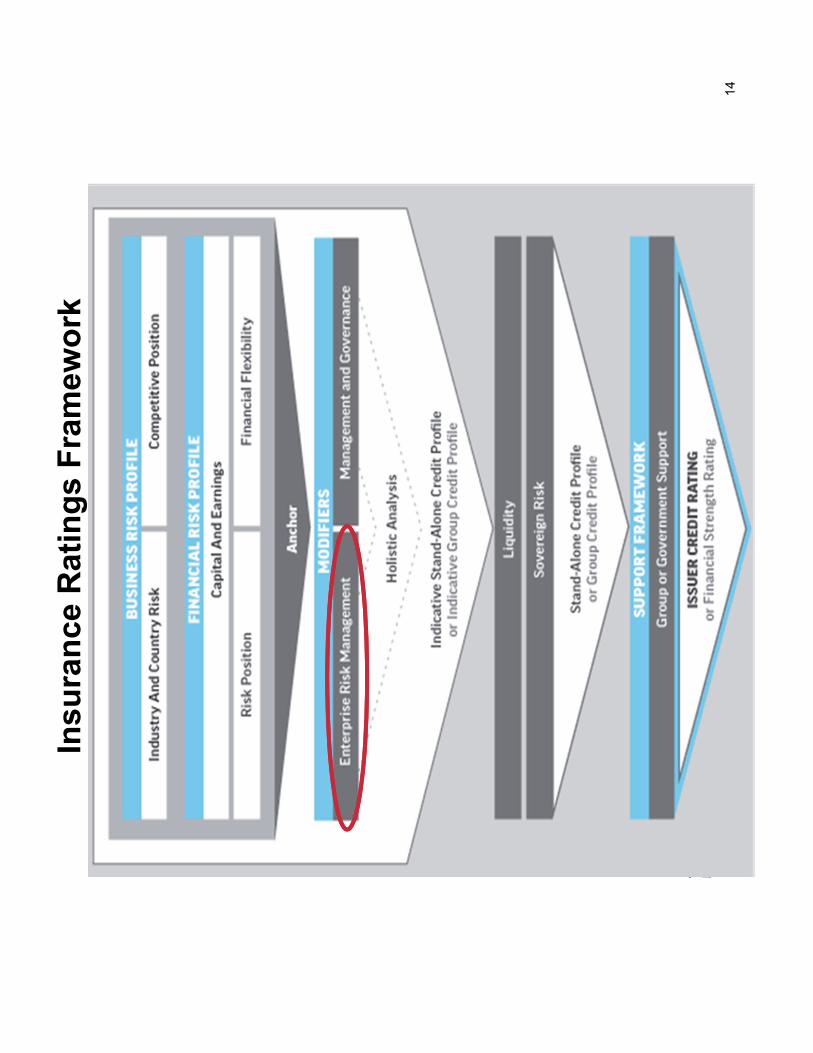

Insu

ranc

e R

atin

gs F

ram

ewor

k

7

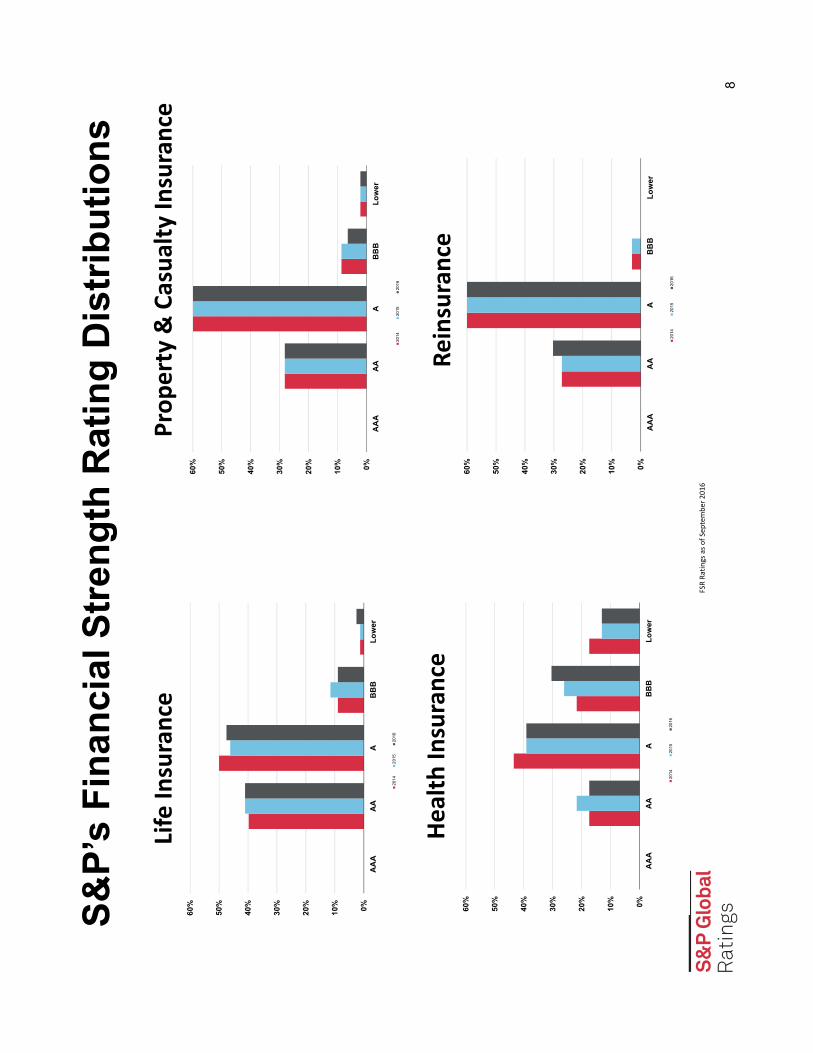

S&P’

s Fi

nanc

ial S

tren

gth

Rat

ing

Dis

trib

utio

ns

8

0%10%

20%

30%

40%

50%

60%

AA

AA

AA

BB

BLo

wer

2014

2015

2016

Prop

erty

& C

asua

lty In

sura

nce

0%10%

20%

30%

40%

50%

60%

AA

AA

AA

BB

BLo

wer

2014

2015

2016

Life

Insu

ranc

e

0%10%

20%

30%

40%

50%

60%

AA

AA

AA

BB

BLo

wer

2014

2015

2016

Rein

sura

nce

0%10%

20%

30%

40%

50%

60%

AA

AA

AA

BB

BLo

wer

2014

2015

2016

Heal

th In

sura

nce

FSR

Ratin

gs a

s of S

epte

mbe

r 201

6

App

endi

x

9

Insu

ranc

e R

atin

gs F

ram

ewor

k

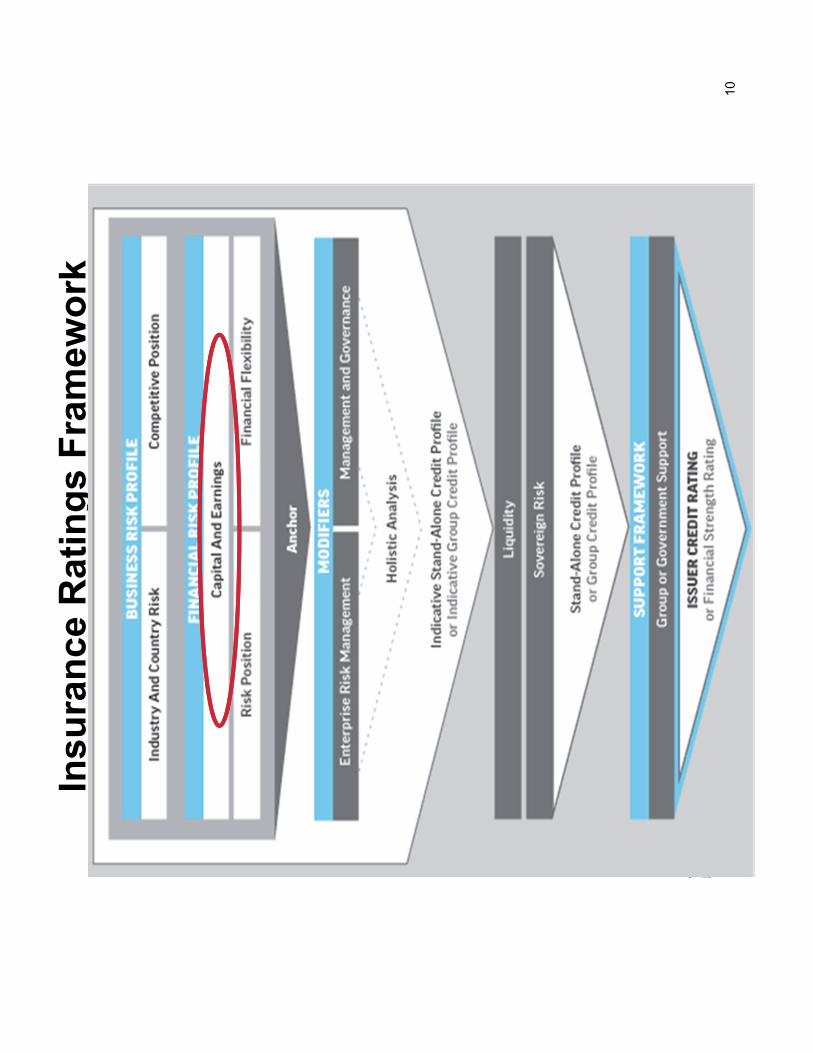

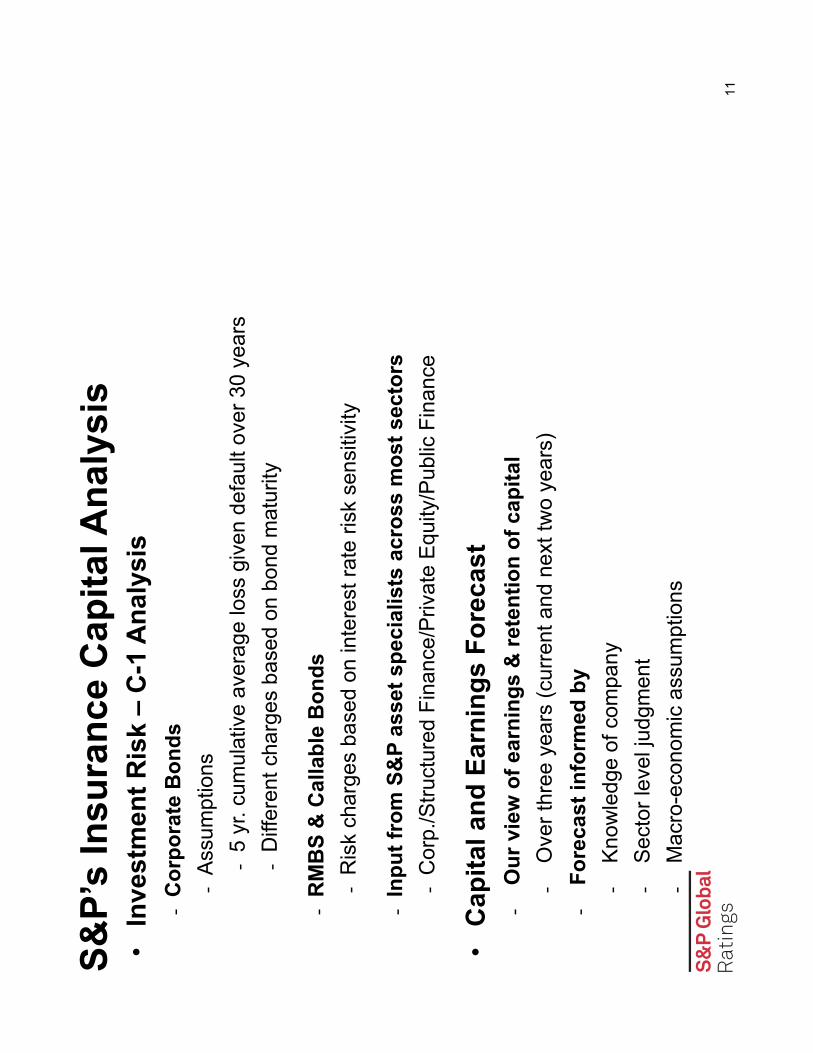

10

•In

vest

men

t Ris

k –

C-1

Ana

lysi

s-

Cor

pora

te B

onds

-A

ssum

ptio

ns-

5 yr

. cum

ulat

ive

aver

age

loss

giv

en d

efau

lt ov

er 3

0 ye

ars

-D

iffer

ent c

harg

es b

ased

on

bond

mat

urity

-R

MB

S &

Cal

labl

e B

onds

-R

isk

char

ges

base

d on

inte

rest

rate

risk

sen

sitiv

ity

-In

put f

rom

S&

P as

set s

peci

alis

ts a

cros

s m

ost s

ecto

rs-

Cor

p./S

truct

ured

Fin

ance

/Priv

ate

Equ

ity/P

ublic

Fin

ance

•C

apita

l and

Ear

ning

s Fo

reca

st-

Our

vie

w o

f ear

ning

s &

rete

ntio

n of

cap

ital

-O

ver t

hree

yea

rs (c

urre

nt a

nd n

ext t

wo

year

s)-

Fore

cast

info

rmed

by

-K

now

ledg

e of

com

pany

-S

ecto

r lev

el ju

dgm

ent

-M

acro

-eco

nom

ic a

ssum

ptio

ns

S&P’

s In

sura

nce

Cap

ital A

naly

sis

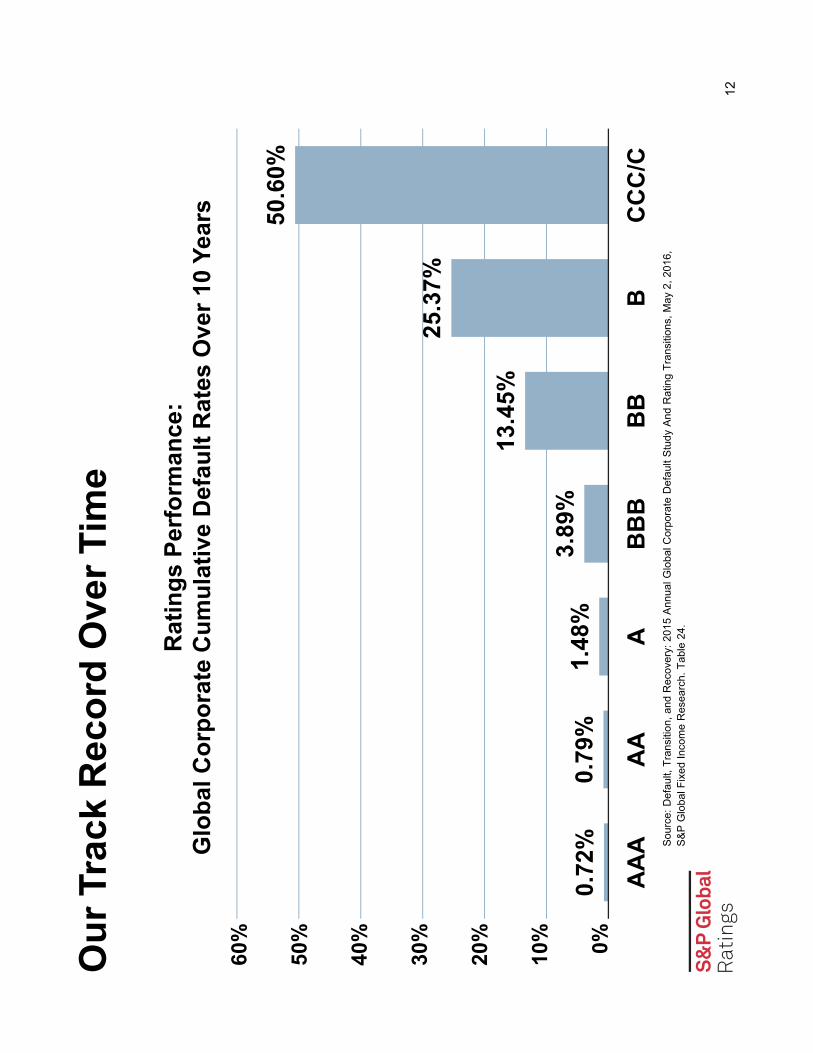

11

0.72

%0.

79%

1.48

%3.

89%

13.4

5%

25.3

7%

50.6

0%

AA

AA

AA

BB

BB

BB

CC

C/C

Rat

ings

Per

form

ance

: G

loba

l Cor

pora

te C

umul

ativ

e D

efau

lt R

ates

Ove

r 10

Year

s60

%

50%

40%

30%

20%

10% 0%

Sou

rce:

Def

ault,

Tra

nsiti

on, a

nd R

ecov

ery:

201

5 A

nnua

l Glo

bal C

orpo

rate

Def

ault

Stu

dy A

nd R

atin

g Tr

ansi

tions

, May

2, 2

016,

S

&P

Glo

bal F

ixed

Inco

me

Res

earc

h. T

able

24.

Our

Tra

ck R

ecor

d O

ver T

ime

12

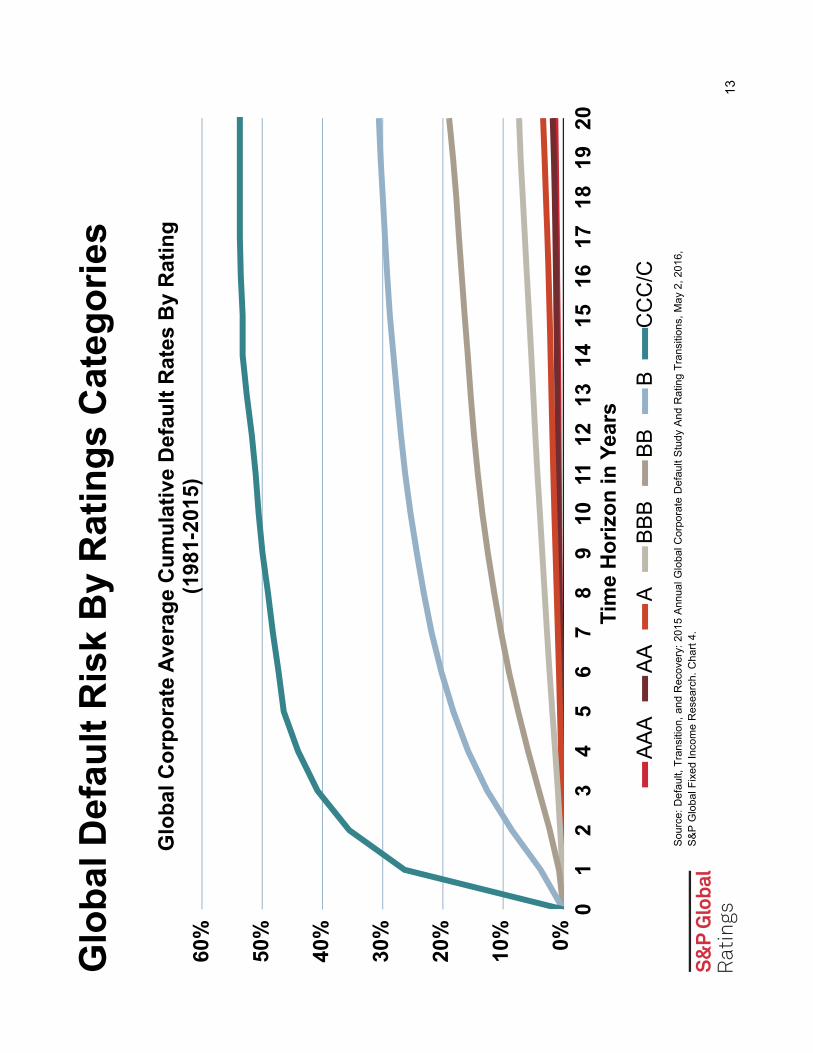

Glo

bal D

efau

lt R

isk

By

Rat

ings

Cat

egor

ies

01

23

45

67

89

1011

1213

1415

1617

1819

20Ti

me

Hor

izon

in Y

ears

Glo

bal C

orpo

rate

Ave

rage

Cum

ulat

ive

Def

ault

Rat

es B

y R

atin

g (1

981-

2015

)

AA

AA

AA

BB

BB

BB

CC

C/C

60%

50%

40%

30%

20%

10% 0%

Sou

rce:

Def

ault,

Tra

nsiti

on, a

nd R

ecov

ery:

201

5 A

nnua

l Glo

bal C

orpo

rate

Def

ault

Stu

dy A

nd R

atin

g Tr

ansi

tions

, May

2, 2

016,

S

&P

Glo

bal F

ixed

Inco

me

Res

earc

h. C

hart

4.

13

Insu

ranc

e R

atin

gs F

ram

ewor

k

14

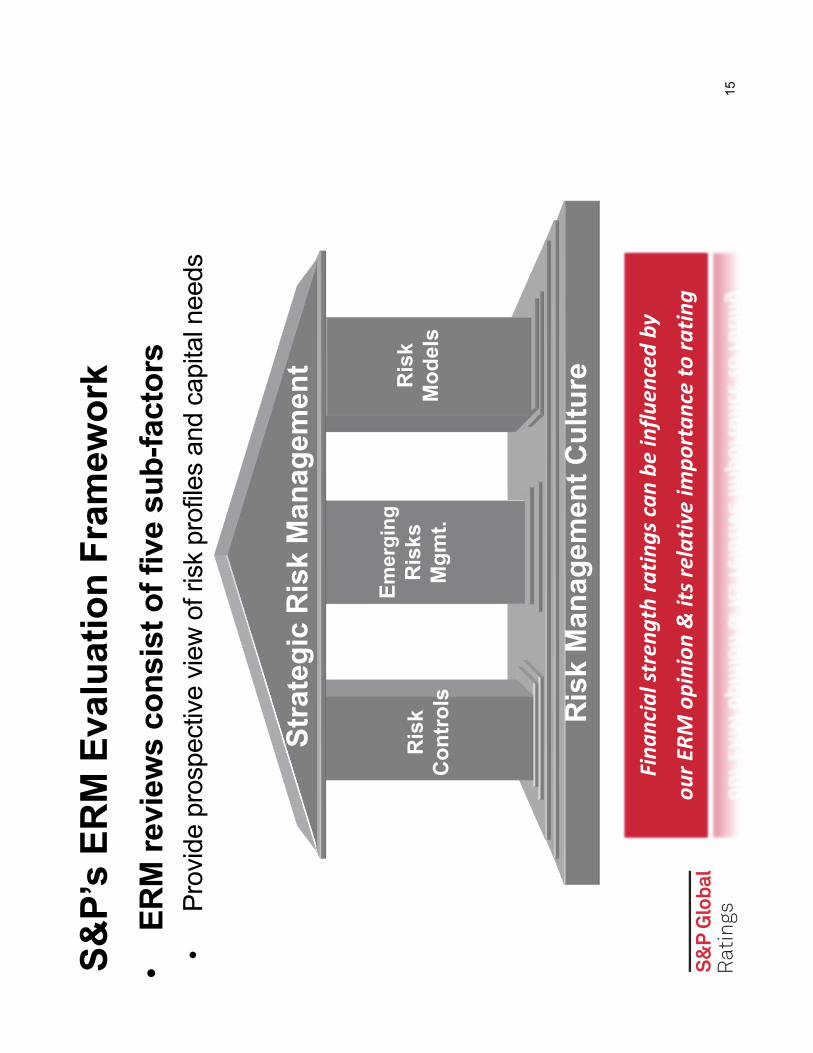

•ER

M re

view

s co

nsis

t of f

ive

sub-

fact

ors

•Pr

ovid

e pr

ospe

ctiv

e vi

ew o

f ris

k pr

ofile

s an

d ca

pita

l nee

ds

S&P’

s ER

M E

valu

atio

n Fr

amew

ork

Ris

k M

anag

emen

t Cul

ture

Ris

k

Con

trol

s

Emer

ging

Ris

ks

Mgm

t. R

isk

Mod

els

Stra

tegi

c R

isk

Man

agem

ent

15

Fina

ncia

l str

engt

h ra

tings

can

be in

fluen

ced

byou

r ERM

opi

nion

& it

s rel

ativ

e im

port

ance

to ra

ting

For m

ore

info

rmat

ion

on S

&P

Glo

bal R

atin

gs,

go to

ww

w.U

nder

stan

ding

Rat

ings

.com

16

Copy

right

© 20

16 b

y Stan

dard

& P

oor’s

Fina

ncial

Ser

vices

LLC

. All r

ights

rese

rved.

No co

ntent

(inclu

ding

ratin

gs, c

redit

-relat

ed a

nalys

es a

nd d

ata, v

aluati

ons,

mode

l, soft

ware

or ot

her a

pplic

ation

or o

utput

there

from)

or a

ny pa

rt the

reof

(Con

tent)

may b

e mod

ified,

reve

rse

engin

eere

d, re

prod

uced

or d

istrib

uted

in an

y for

m by

any m

eans

, or s

tored

in a

datab

ase

or re

trieva

l sys

tem, w

ithou

t the p

rior w

ritten

perm

ission

of S

tanda

rd &

Poo

r’s F

inanc

ial S

ervic

es L

LC or

its

affili

ates (

colle

ctive

ly, S

&P).

The C

onten

t sha

ll not

be us

ed fo

r any

unlaw

ful o

r una

uthor

ized

purp

oses

. S&P

and

any t

hird-

party

pro

vider

s, as

well

as th

eir d

irecto

rs, o

fficer

s, sh

areh

older

s, em

ploye

es o

r age

nts (c

ollec

tively

S&P

Par

ties)

do no

t gua

rante

e the

accu

racy

, com

pleten

ess,

timeli

ness

or av

ailab

ility o

f theC

onten

t. S&P

Par

ties a

re no

t res

pons

ible

for an

y erro

rs or

om

ission

s (ne

glige

nt or

othe

rwise

), re

gard

less o

f the c

ause

, for t

he re

sults

obtai

ned

from

the us

e of th

e Con

tent, o

r for

thes

ecur

ity or

main

tenan

ce o

f any

data

input

by th

e use

r. Th

e Con

tent is

pr

ovide

d on

an “a

s is”

basis

. S&P

PAR

TIES

DIS

CLAI

M AN

Y AN

D AL

L EX

PRES

S OR

IMPL

IED

WAR

RANT

IES,

INCL

UDIN

G, B

UT N

OT LI

MITE

D TO

, ANY

WAR

RANT

IES

OF

MERC

HANT

ABILI

TY O

R FI

TNES

S FO

R A

PART

ICUL

AR P

URPO

SE O

R US

E, F

REED

OM F

ROM

BUGS

, SOF

TWAR

E ER

RORS

OR

DEFE

CTS,

THA

T TH

E CO

NTEN

T’SFU

NCTI

ONIN

G W

ILL

BE U

NINT

ERRU

PTED

OR

THAT

THE

CON

TENT

WILL

OPE

RATE

WIT

H AN

Y SO

FTW

ARE

OR H

ARDW

ARE

CONF

IGUR

ATIO

N. In

no ev

ent s

hall S

&P P

artie

s be

liable

to an

y par

ty for

any

direc

t, ind

irect,

incid

ental

, exe

mplar

y, co

mpen

sator

y, pu

nitive

, spe

cial o

r con

sequ

entia

l dam

ages

, cos

ts, ex

pens

es, le

gal fe

es, o

r loss

es (in

cludin

g, wi

thout

limita

tion,

lost in

come

or lo

st pr

ofits

and

oppo

rtunit

y cos

ts or

loss

es ca

used

by n

eglig

ence

) in c

onne

ction

with

any u

se of

the C

onten

t eve

n if a

dvise

d of

the po

ssibi

lity of

such

dama

ges.

Cred

it-rela

ted a

nd ot

her a

nalys

es, in

cludin

g ra

tings

, and

state

ments

in th

e Con

tent a

re st

ateme

nts of

opini

on a

s of th

e date

they

are e

xpre

ssed

and

not s

tatem

ents

of fac

t. S&P

’s op

inion

s, an

alyse

s and

ratin

g ac

know

ledgm

ent d

ecisi

ons (

desc

ribed

belo

w) a

re n

ot re

comm

enda

tions

to pu

rchas

e, ho

ld, o

r sell

any s

ecur

itieso

r to m

ake a

ny in

vestm

ent d

ecisi

ons,

and d

o not

addr

ess t

he

suita

bility

of an

y sec

urity

. S&P

ass

umes

no ob

ligati

on to

upda

te the

Con

tent fo

llowi

ng p

ublic

ation

in an

y for

m or

form

at. T

heCo

ntent

shou

ld no

t be r

elied

on a

nd is

not a

subs

titute

for th

e skil

l, jud

gmen

t and

exp

erien

ce o

f the u

ser,

its m

anag

emen

t, em

ploye

es, a

dviso

rs an

d/or c

lients

whe

n ma

king

inves

tmen

t and

othe

r bus

iness

decis

ions.

S&P

does

not a

ct as

a fid

uciar

y or a

n inv

estm

ent a

dviso

r exc

ept w

here

regis

tered

as s

uch.

Whil

e S&P

has

obtai

ned

infor

matio

n fro

m so

urce

s it b

eliev

es to

be re

liable

, S&P

doe

s not

perfo

rm a

n aud

it and

unde

rtake

s no d

uty of

due

dilige

nce

or in

depe

nden

t ver

ificati

on o

f any

infor

matio

n it r

eceiv

es.

To th

e exte

nt tha

t reg

ulator

y auth

oritie

s allo

w a r

ating

age

ncy t

o ack

nowl

edge

in on

e jur

isdict

ion a

ratin

g iss

ued i

n ano

therj

urisd

iction

for c

ertai

n re

gulat

ory p

urpo

ses,

S&P

rese

rves t

he rig

ht to

assig

n, wi

thdra

w or

susp

end

such

ackn

owled

geme

nt at

any t

ime a

nd in

its so

le dis

cretio

n. S&

P Pa

rties d

isclai

m an

y duty

wha

tsoev

er a

rising

out

of the

assig

nmen

t, wi

thdra

wal o

r sus

pens

ion o

f an

ackn

owled

gmen

t as w

ell as

any l

iabilit

y for

any d

amag

e all

eged

to ha

ve b

een

suffe

red

on ac

coun

t the

reof.

S&P

keep

s cer

tain

activ

ities o

f its b

usine

ss u

nits s

epar

ate fr

om ea

ch o

ther in

orde

r to p

rese

rve th

e ind

epen

denc

e an

d ob

jectiv

ity of

their

resp

ectiv

e ac

tivitie

s. As

a re

sult,

certa

in bu

sines

s unit

s of

S&P

may h

ave i

nform

ation

that

is no

t ava

ilable

to ot

her S

&P b

usine

ss u

nits.

S&P

has e

stabli

shed

poli

cies a

nd p

roce

dure

s to m

aintai

n the

confi

denti

ality

of ce

rtain

non-

publi

c info

rmati

on re

ceive

d in

conn

ectio

n wi

th ea

ch a

nalyt

ical p

roce

ss.

S&P

may r

eceiv

e co

mpen

satio

n for

its ra

tings

and

certa

in an

alyse

s, no

rmall

y fro

m iss

uers

or un

derw

riters

of se

curiti

es o

r fro

m ob

ligor

s. S&

P re

serve

s the

right

to dis

semi

nate

its op

inion

s and

an

alyse

s. S&

P's p

ublic

ratin

gs a

nd a

nalys

es a

re m

ade

avail

able

on its

Web

sites

, www

.stan

dard

andp

oors.

com

(free

of ch

arge

), an

d ww

w.ra

tings

direc

t.com

and

www

.glob

alcre

ditpo

rtal.c

om

(subs

cripti

on),

and m

ay be

distr

ibuted

thro

ugh

other

mea

ns, in

cludin

g via

S&P

pub

licati

ons a

nd th

ird-p

arty

redis

tributo

rs. A

dditio

nal in

forma

tion

abou

t our

ratin

gs fe

es is

avail

able

at ww

w.sta

ndar

dand

poor

s.com

/usra

tings

fees.

Austr

alia

Stan

dard

& P

oor's

(Aus

tralia

) Pty.

Ltd.

holds

Aus

tralia

n fin

ancia

l ser

vices

licen

se nu

mber

337

565

unde

r the

Cor

pora

tions

Act

2001

. Stan

dard

& P

oor’s

cred

it rati

ngs a

nd re

lated

rese

arch

are

not

inten

ded

for an

d mus

t not

be di

stribu

ted to

any p

erso

n in

Austr

alia

other

than

a wh

olesa

le cli

ent (

as de

fined

in C

hapte

r 7 of

the C

orpo

ratio

ns A

ct).

STAN

DARD

& P

OOR’

S, S

&P a

nd R

ATIN

GSDI

RECT

are

regis

tered

trad

emar

ks o

f Stan

dard

& P

oor’s

Fina

ncial

Ser

vices

LLC.

17