luke bowen – executive director. sessional committee on environment and sustainable development...

Post on 20-Dec-2015

216 views

TRANSCRIPT

Luke Bowen – Executive Director

Sessional Com

mittee on

Environment and Sustainable

Developm

ent

Northern Territory C

attlemen’s Association

October 16, 2009

Background – NTCABackground – NT IndustryAddress committee Terms of Reference

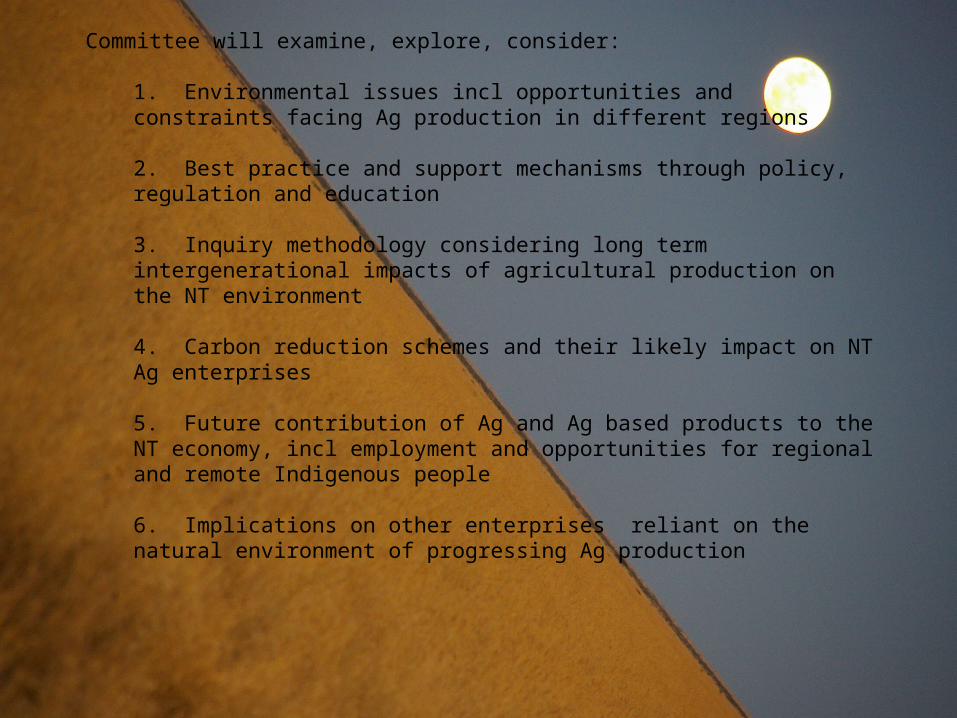

Committee will examine, explore, consider:

1. Environmental issues incl opportunities and constraints facing Ag production in different regions

2. Best practice and support mechanisms through policy, regulation and education

3. Inquiry methodology considering long term intergenerational impacts of agricultural production on the NT environment

4. Carbon reduction schemes and their likely impact on NT Ag enterprises

5. Future contribution of Ag and Ag based products to the NT economy, incl employment and opportunities for regional and remote Indigenous people

6. Implications on other enterprises reliant on the natural environment of progressing Ag production

The Cattle Industry & NTCA

NT QUALITY BEEF

95% of producers

48% of the NT

The Northern Territory - A reliable supplier of Quality Livestock

The Northern Territory - A reliable supplier of Quality Livestock

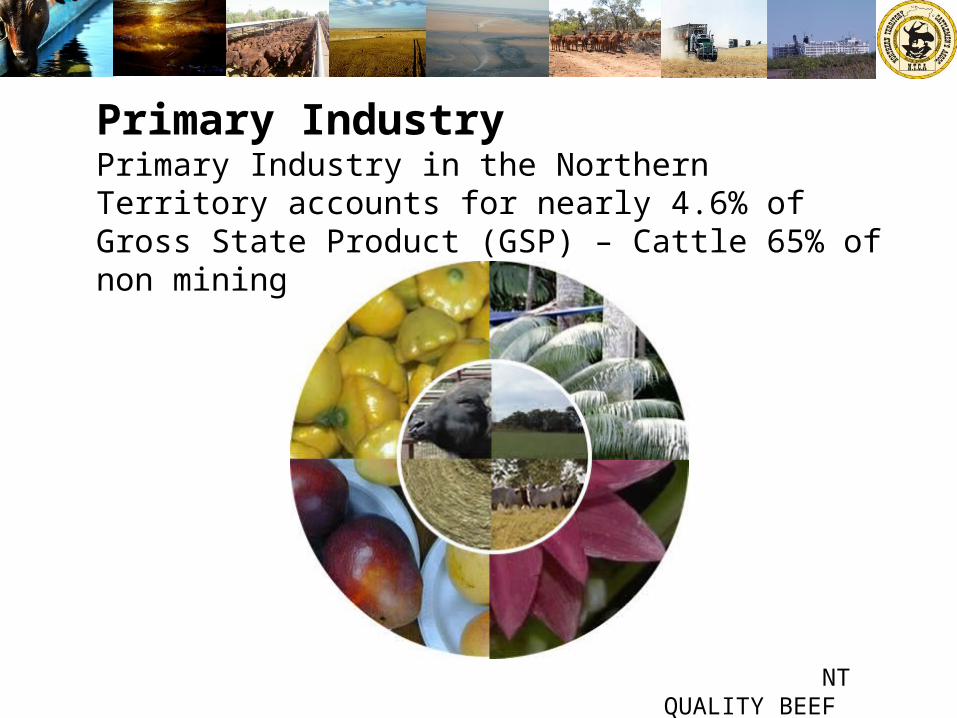

Primary IndustryPrimary Industry in the Northern Territory accounts for nearly 4.6% of Gross State Product (GSP) – Cattle 65% of non mining sector

NT QUALITY BEEF

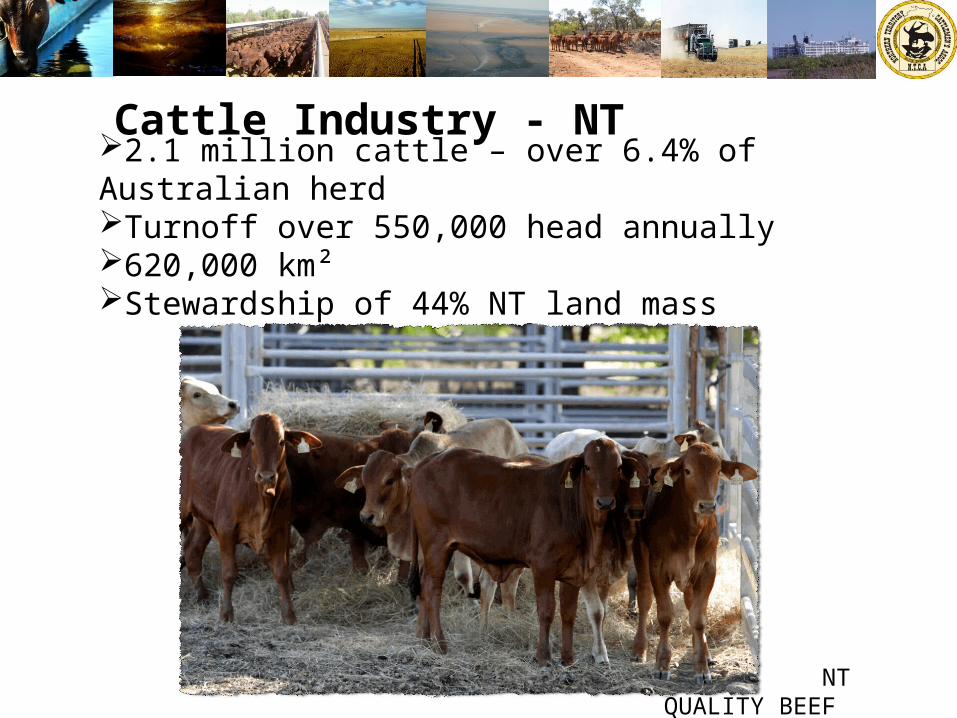

Cattle Industry - NT2.1 million cattle – over 6.4% of Australian herdTurnoff over 550,000 head annually620,000 km²Stewardship of 44% NT land mass

NT QUALITY BEEF

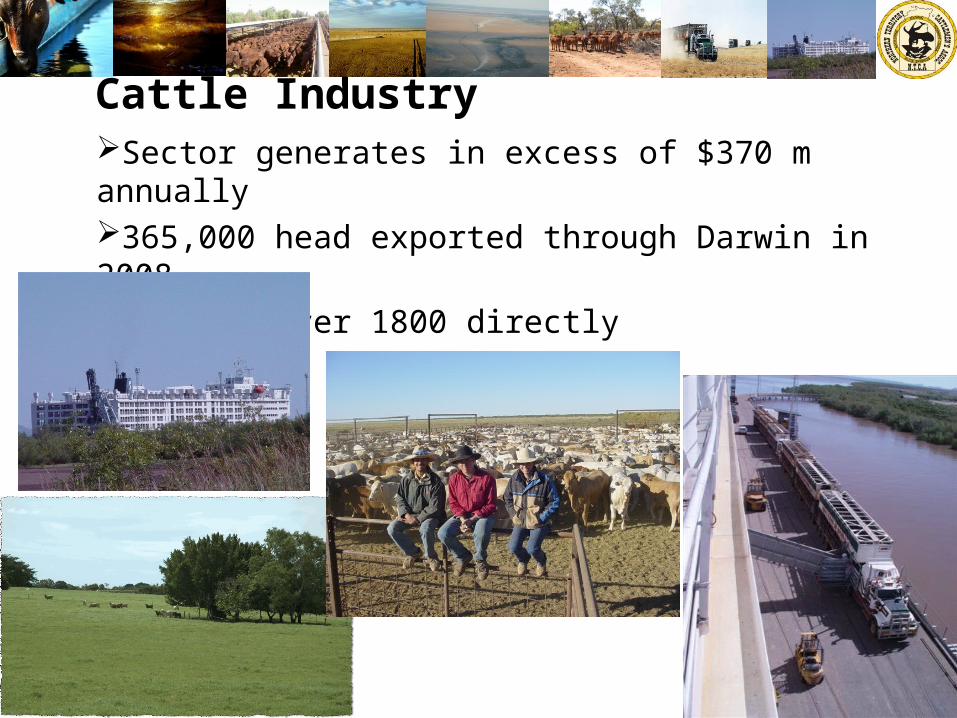

Cattle IndustrySector generates in excess of $370 m annually365,000 head exported through Darwin in 2008Employs over 1800 directly

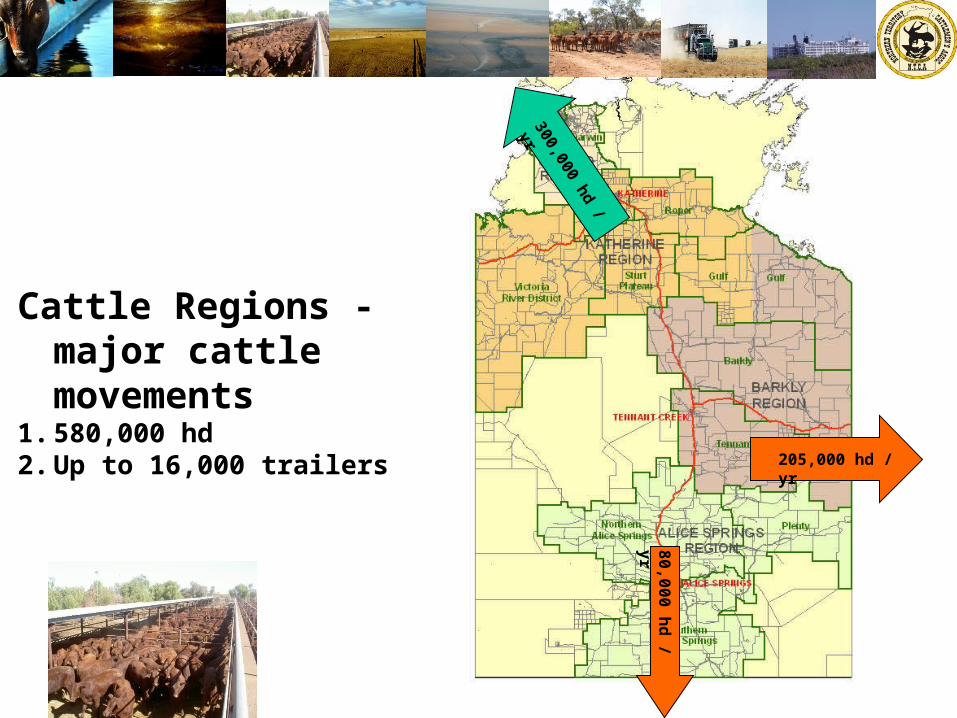

Cattle Regions - major cattle movements

1. 580,000 hd2. Up to 16,000 trailers

300,000 hd / yr

80

,00

0 h

d / y

r

205,000 hd / yr

Cattle Export

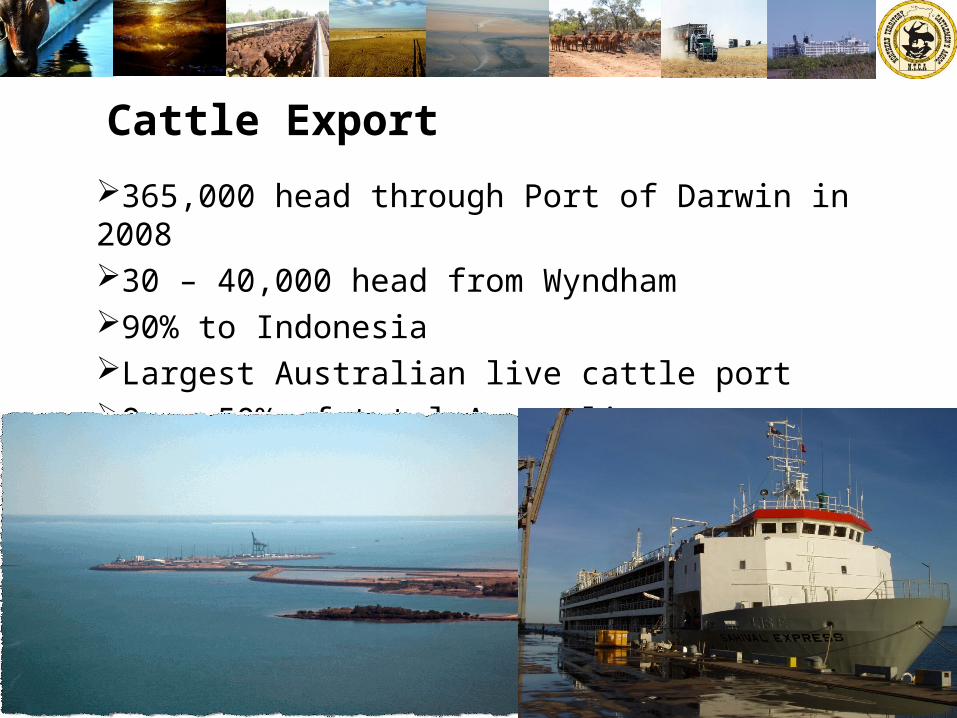

365,000 head through Port of Darwin in 200830 – 40,000 head from Wyndham 90% to IndonesiaLargest Australian live cattle portOver 50% of total Australian exports

Indonesia (90% of market) Population 260m Burgeoning middle class with increasing appetite for beef Similar trend through the region Market to double in next 6 - 10 years

NT QUALITY BEEF

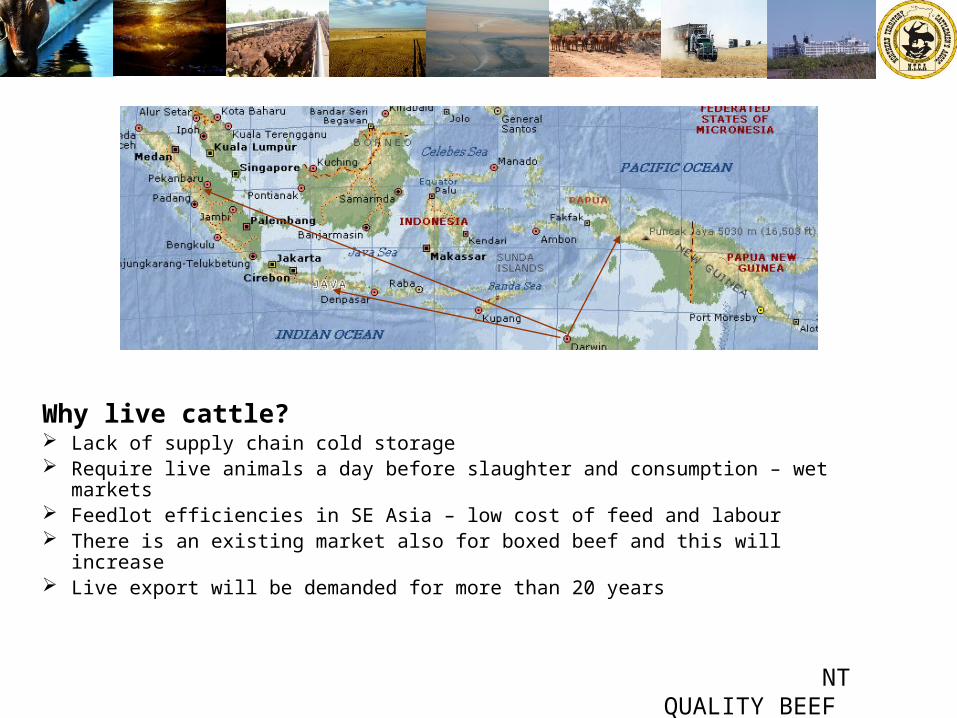

Why live cattle? Lack of supply chain cold storage Require live animals a day before slaughter and consumption – wet markets Feedlot efficiencies in SE Asia – low cost of feed and labour There is an existing market also for boxed beef and this will increase Live export will be demanded for more than 20 years

NT QUALITY BEEF

The Northern Territory - A reliable supplier of Quality Livestock

Projected Growth – 15 years

2 m head 3.5 m head

+30%

+30%

+100%

+15%

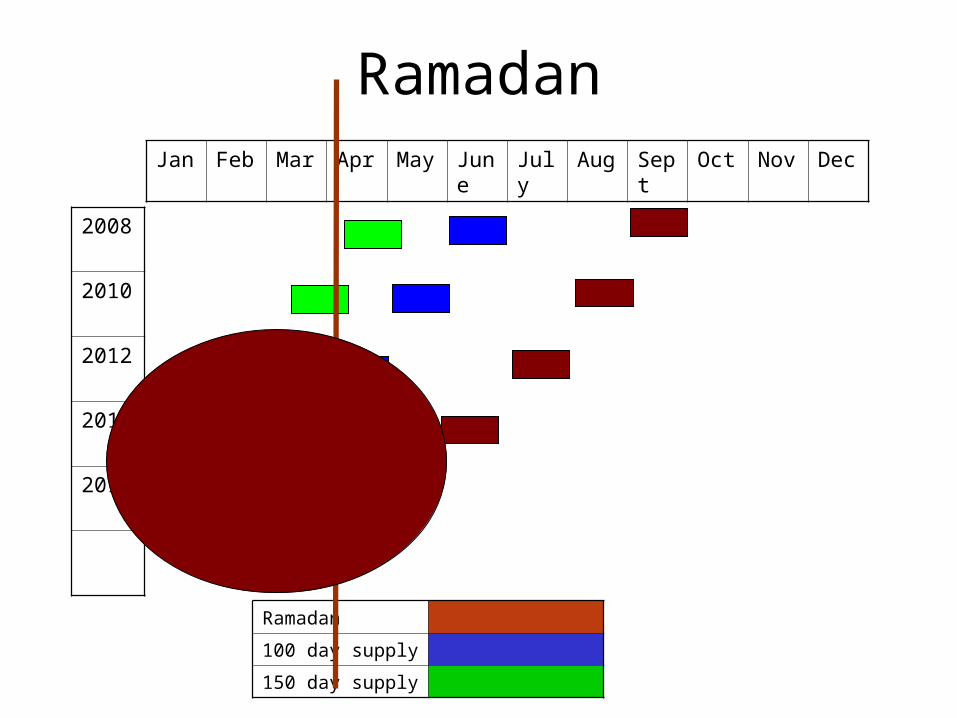

Ramadan

2008

2010

2012

2014

2017

Jan Feb Mar Apr May June July Aug Sept Oct Nov Dec

Ramadan

100 day supply

150 day supply

Increasingly complex environment

A future Business management

Layers of government

Climate variability

Human resource management

Marketing

Running families and lives

Government regulation

Technology

Environmental regulation

Resource management

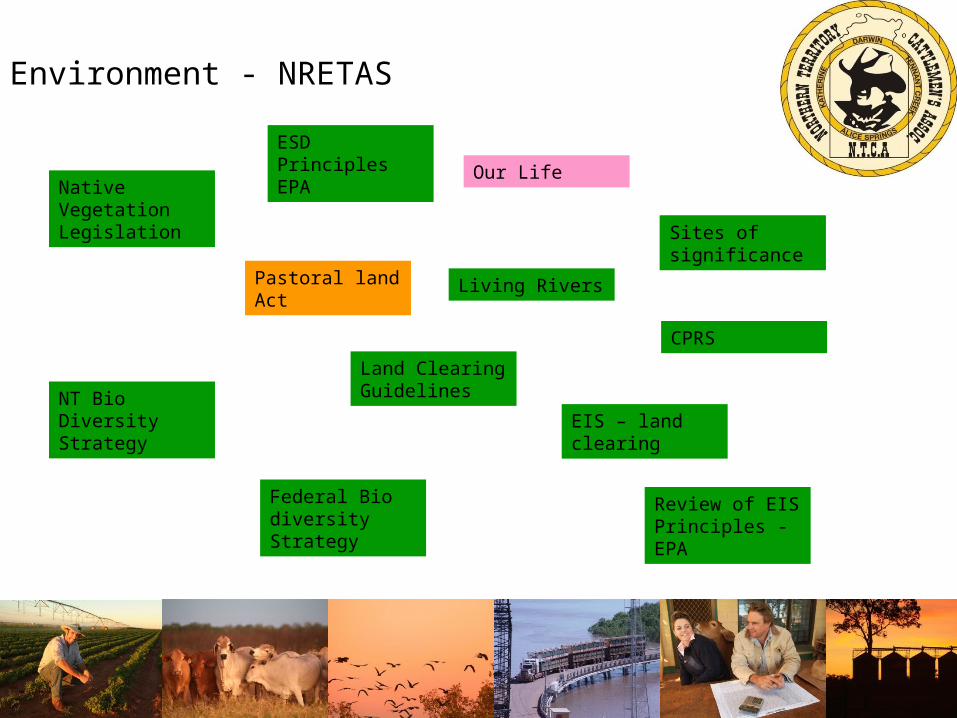

Environment - NRETAS

Pastoral land Act

Living Rivers

Review of EIS Principles - EPA

EIS – land clearing

Native Vegetation Legislation

NT Bio Diversity Strategy

Federal Bio diversity Strategy

Sites of significance

Land Clearing Guidelines

Sites of significance

Our Life

ESD Principles EPA

CPRS

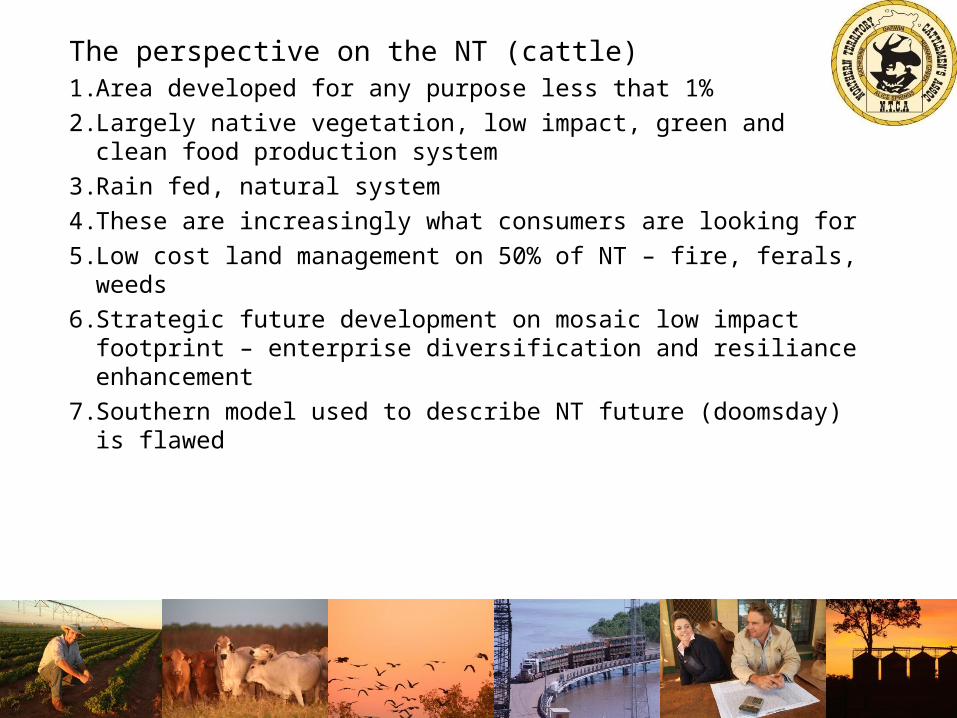

The perspective on the NT (cattle)1. Area developed for any purpose less that 1%

2. Largely native vegetation, low impact, green and clean food production system

3. Rain fed, natural system

4. These are increasingly what consumers are looking for

5. Low cost land management on 50% of NT – fire, ferals, weeds

6. Strategic future development on mosaic low impact footprint – enterprise diversification and resiliance enhancement

7. Southern model used to describe NT future (doomsday) is flawed

TOR IEnvironmental issues incl opportunities and constraints facing Ag production in different regions

Camels, horses, donkeys, dogs, fire,

Central Australia•Climate variability•Low production costs•High productivity•Organic low input•Low pest footprint•Diversification and market advantage – ie hort

•Labour availability•Demographic trends and Indigenous development

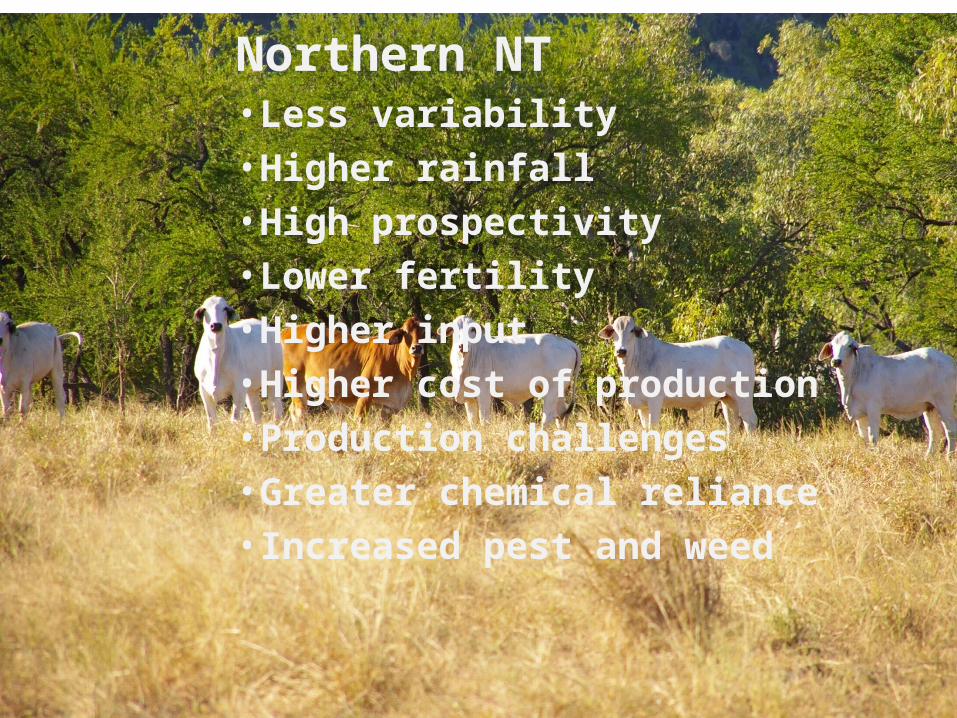

Northern NT•Less variability•Higher rainfall•High prospectivity•Lower fertility•Higher input•Higher cost of production•Production challenges•Greater chemical reliance•Increased pest and weed

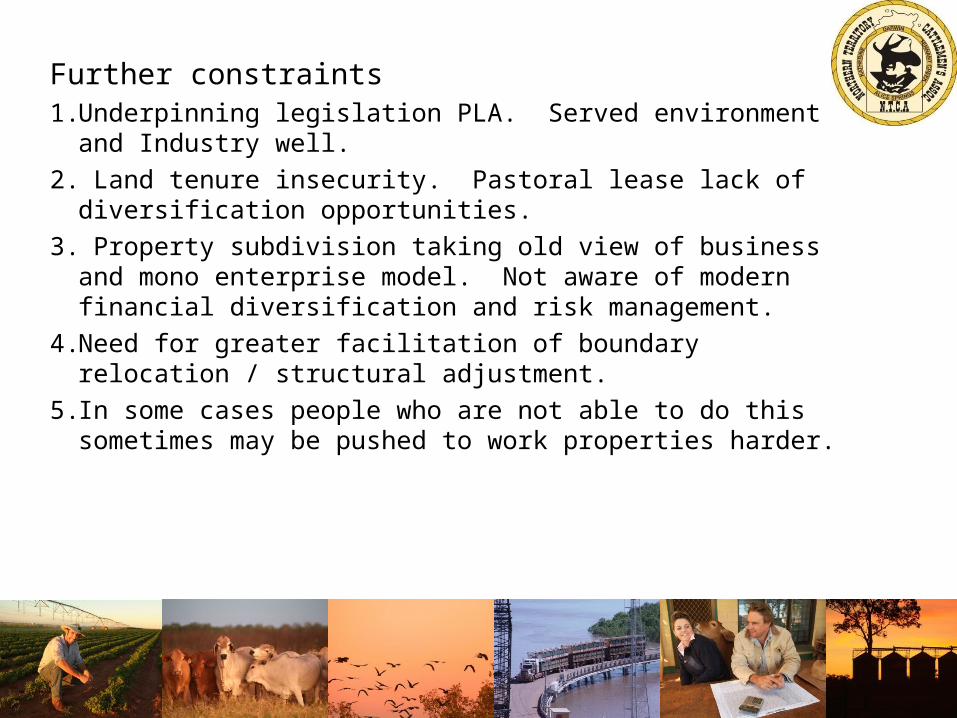

Further constraints1. Underpinning legislation PLA. Served environment and

Industry well.

2. Land tenure insecurity. Pastoral lease lack of diversification opportunities.

3. Property subdivision taking old view of business and mono enterprise model. Not aware of modern financial diversification and risk management.

4. Need for greater facilitation of boundary relocation / structural adjustment.

5. In some cases people who are not able to do this sometimes may be pushed to work properties harder.

What’s on the horizon??

Diversification / enterprise mix

Intensification of land use / production

Greater resource planning and scoping by government Infrastructure requirements

Regulation / development

Greater harmonisation across departments / industry

Holistic approach – health, education, infrastructure, economic development and Indigenous disadvantage

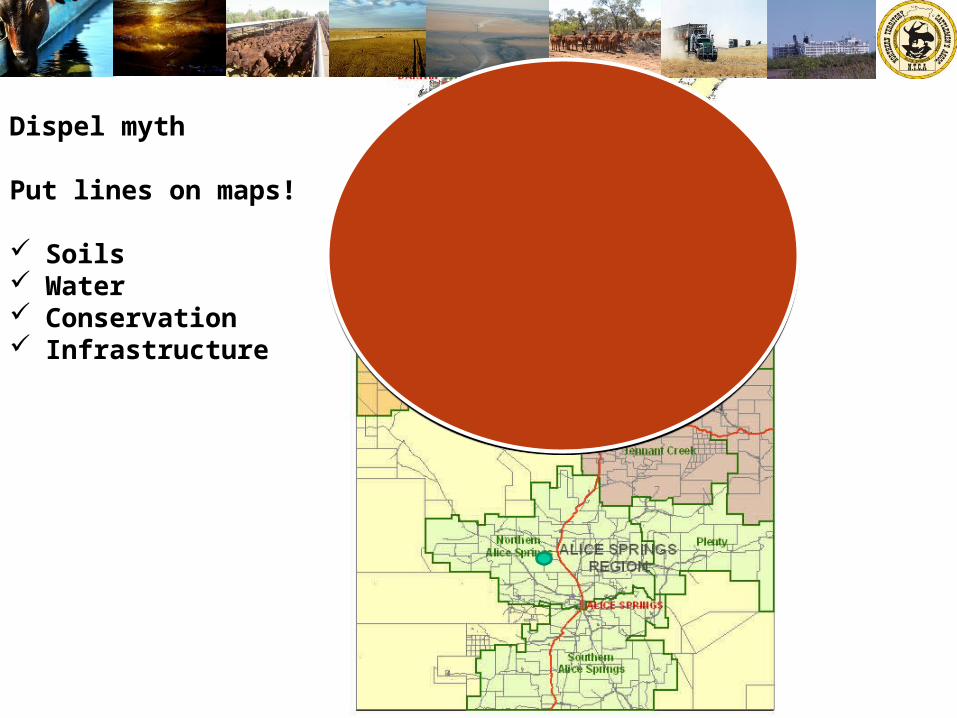

Scope prospective areas?

Put lines on maps!

Soils Water Conservation Infrastructure

Dispel myth

Put lines on maps!

Soils Water Conservation Infrastructure

TOR IIBest practice and support mechanisms through policy, regulation and education

Best practice1. Over 25% of producers are engaged in some form of practice

improvement and benchmarking establishing baseline data Endeavouring to link production and environmental health measures

2. Major driver for change and increased resiliance Adaptability to change, enviro, market, production, economic etc Off property risk investment and diversification

3. These need to be supported and extended to expand take-up and drive wider change – federal / state / industry partnerships

4. Increased R&D and extension investment (11 times return on $, RRDC Report)

Best practice cont1. Selected industry data shows some properties / businesses

have spent in excess of $50,000 over past 7 years to support benchmarking and property improvement

2. Require promotion to increase uptake

3. Seed investment by government to kick off (Southern Beef Producers Group / Sturt Plateau)

Gill Family – Douglas Daly

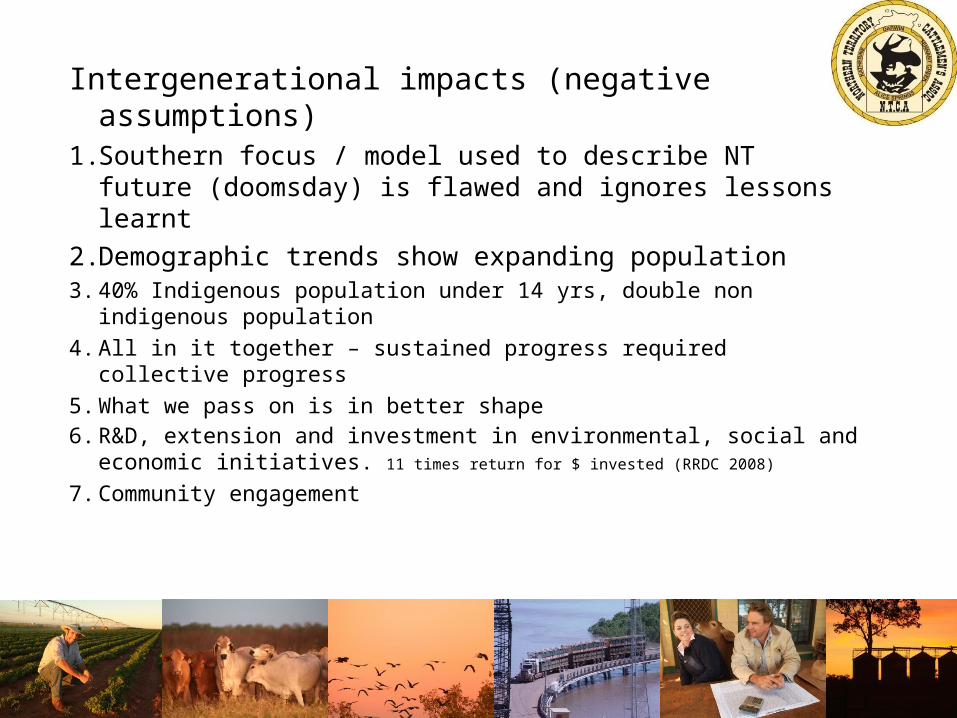

TOR III.Inquiry methodology considering long term intergenerational impacts of agricultural production on the NT environment

Ooratippra NT

Mt Riddock Past Cop (Cadzow)

Intergenerational impacts (negative assumptions)1. Southern focus / model used to describe NT future

(doomsday) is flawed and ignores lessons learnt2. Demographic trends show expanding population 3. 40% Indigenous population under 14 yrs, double non

indigenous population4. All in it together – sustained progress required collective

progress5. What we pass on is in better shape6. R&D, extension and investment in environmental, social

and economic initiatives. 11 times return for $ invested (RRDC 2008)

7. Community engagement

Impacts

Failure to look holistically at development of our industries and communities will be at the peril of future generations

• Social development

• Health

• Education

• Infrastructure

TOR IV

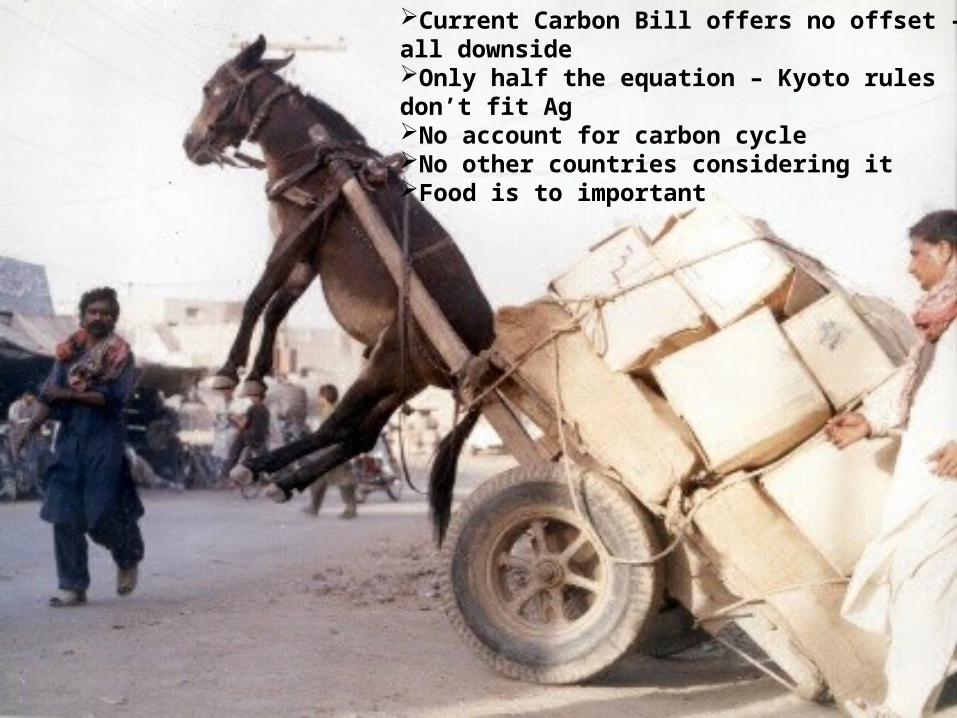

Carbon reduction schemes and their likely impact on NT Ag enterprises

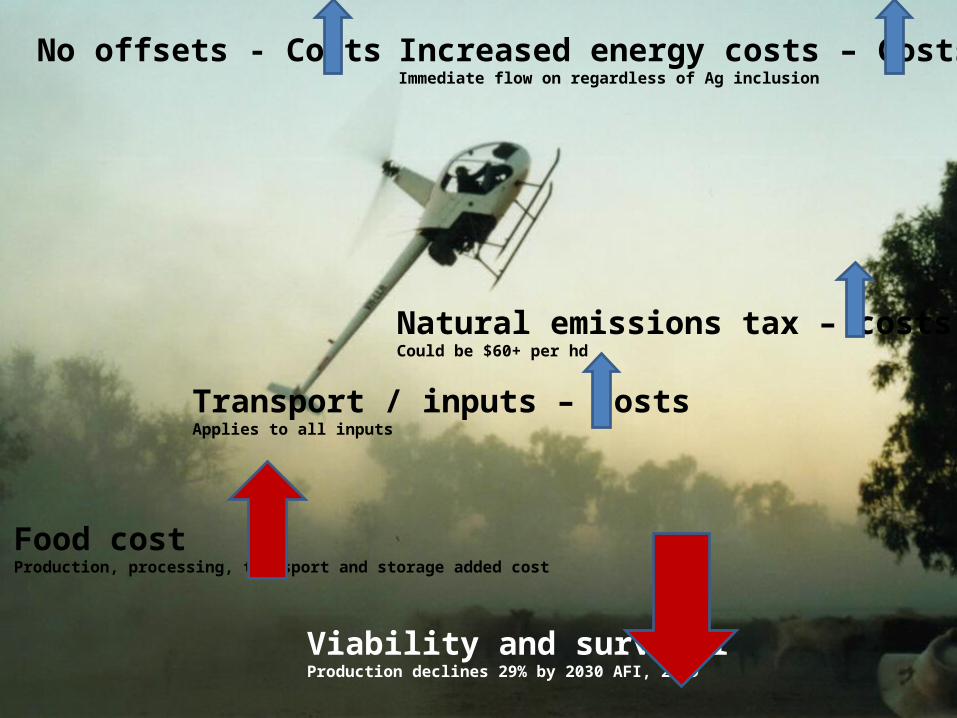

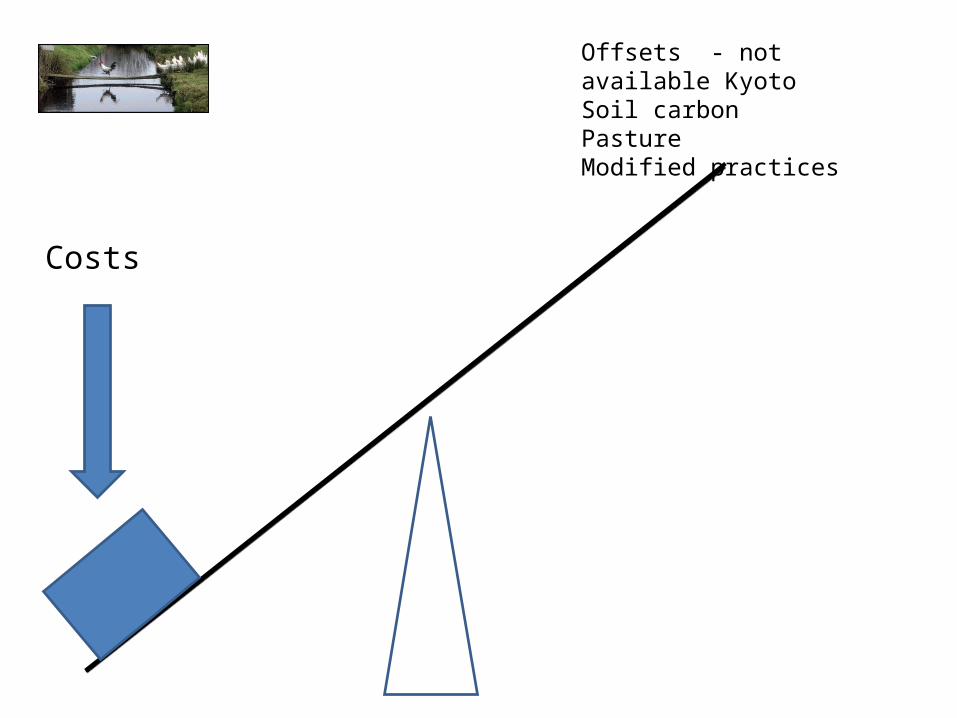

Current Carbon Bill offers no offset – all downsideOnly half the equation – Kyoto rules don’t fit AgNo account for carbon cycleNo other countries considering itFood is to important

No offsets - Costs Increased energy costs – CostsImmediate flow on regardless of Ag inclusion

Natural emissions tax – costsCould be $60+ per hd

Transport / inputs – costsApplies to all inputs

Food costProduction, processing, transport and storage added cost

Viability and survivalProduction declines 29% by 2030 AFI, 2009

Offsets - not available KyotoSoil carbonPastureModified practices

Costs

1.5% of world emissions, Ag 16% and includes burning and other non related emissions

Don’t go alone to make a statement and shoot our food production sector in the process!

International competition and a level playing field!

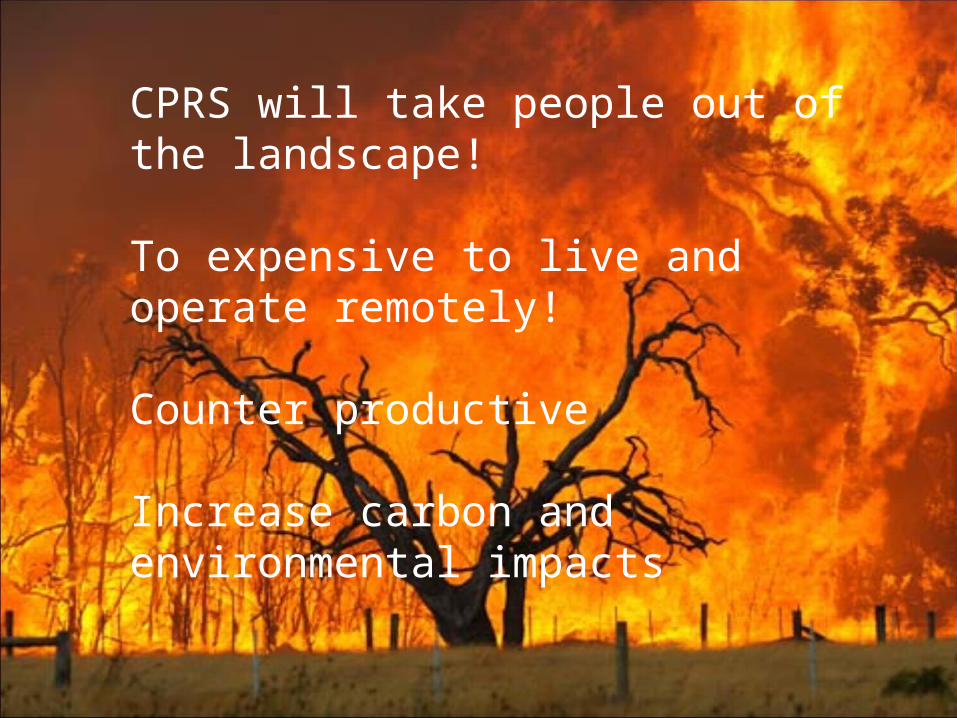

CPRS will take people out of the landscape!

To expensive to live and operate remotely!

Counter productive

Increase carbon and environmental impacts

Ooratippra NT

Mt Riddock Past Cop (Cadzow)

TOR V

Future contribution of Ag and Ag based products to the NT economy, incl employment and opportunities for regional and remote Indigenous people

Employment and engagement1. Current industry (cattle) employment 1800 pa direct

2. Percentage seasonal

3. Periodic shortages with consistent demand for experienced people – no shortage of entry level (McLoads Daughters phenomenon)

4. Capital has replaced labour and driven large reductions in past 30 years

5. Technology and cost of production will continue to drive labour reduction

6. Some upside with new livestock handling and management practice

Employment and engagement cont1. Industry engagement in Indigenous employment programs –

2 full time NTCA staff (indigenous employment programs, Alice Springs / Katherine)

2. 75 Indigenous people working under structured programs, 2009

3. Historic relationships and local arrangements still employing over 200 people across the NT

4. Indigenous advantage over out of town labour

5. Challenges overcoming: Health, literacy, numeracy, social and cultural issues Work and reliability Cross cultural and workplace acceptability and understanding

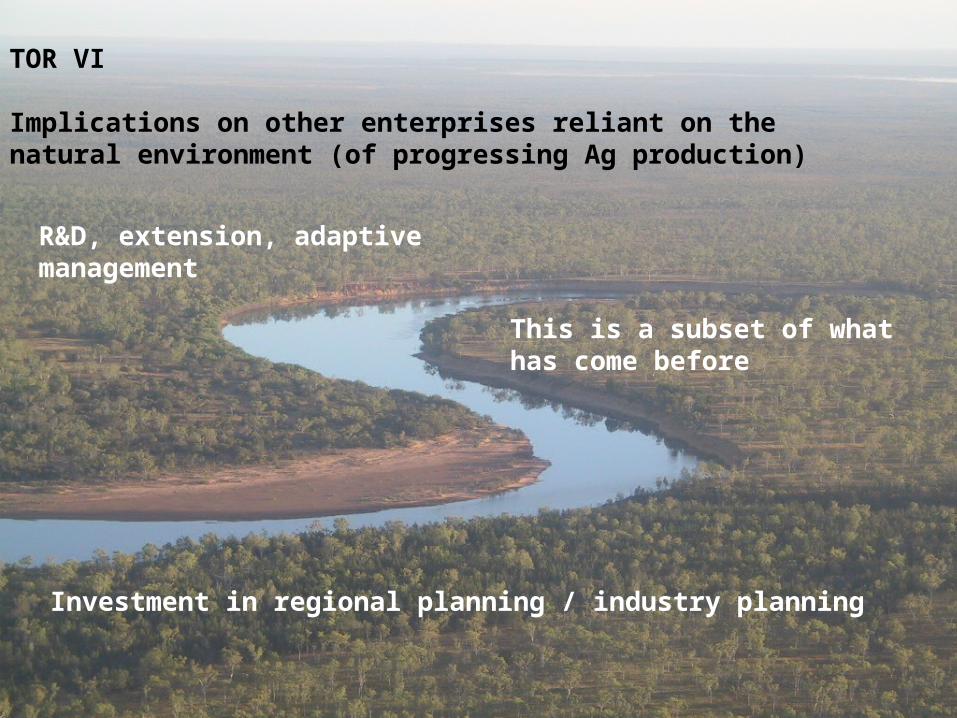

TOR VI

Implications on other enterprises reliant on the natural environment (of progressing Ag production)

Investment in regional planning / industry planning

This is a subset of what has come before

R&D, extension, adaptive management

Thank you

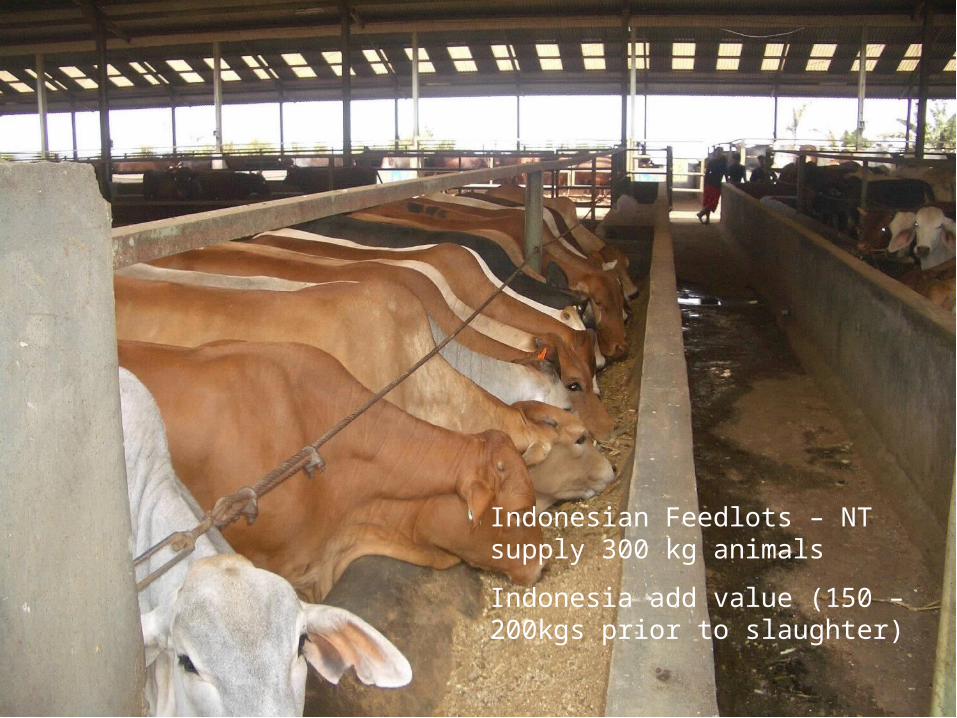

Indonesian Feedlots – NT supply 300 kg animals

Indonesia add value (150 – 200kgs prior to slaughter)

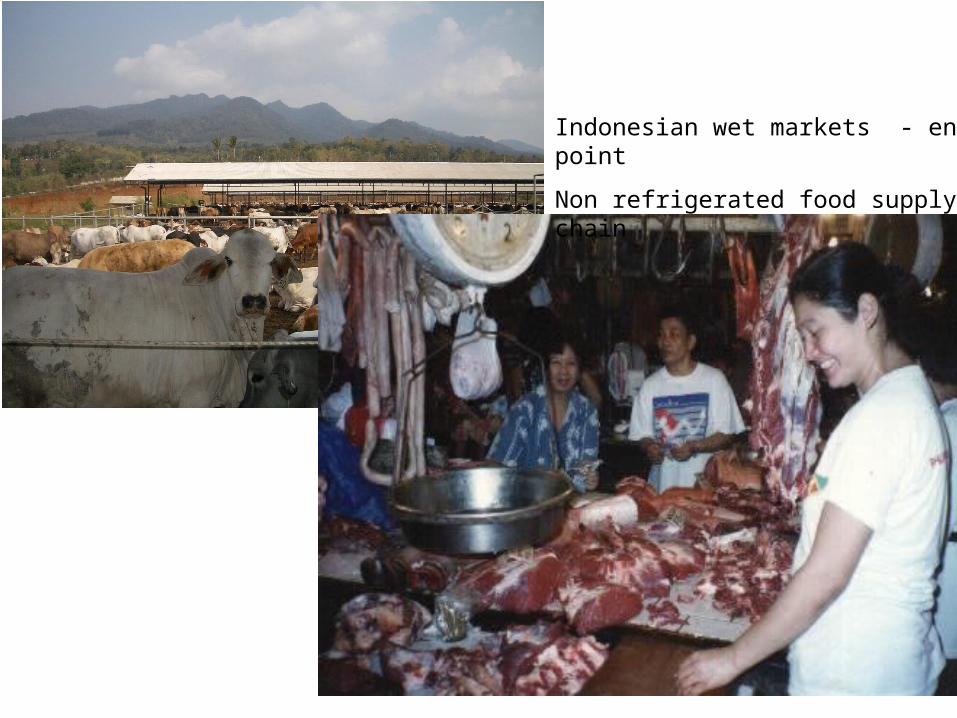

Indonesian wet markets - end point

Non refrigerated food supply chain

Barkly Producer - AACo

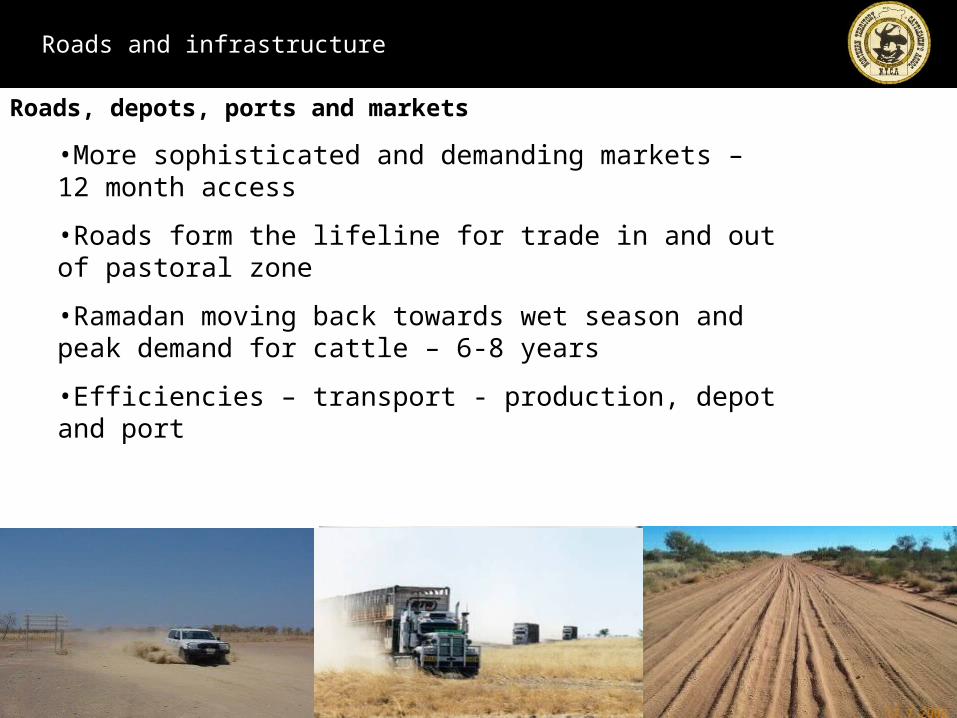

DEPARTMENT OFPRIMARY INDUSTRY, FISHERIES AND MINESOur roads and infrastructure

Roads

• Statistics

• The Total NT Road Network is 41,521 km

• Total sealed 31%

•Of this 1% is sealed and curbed 190 km

•Total unsealed 69% or over 28,600 km

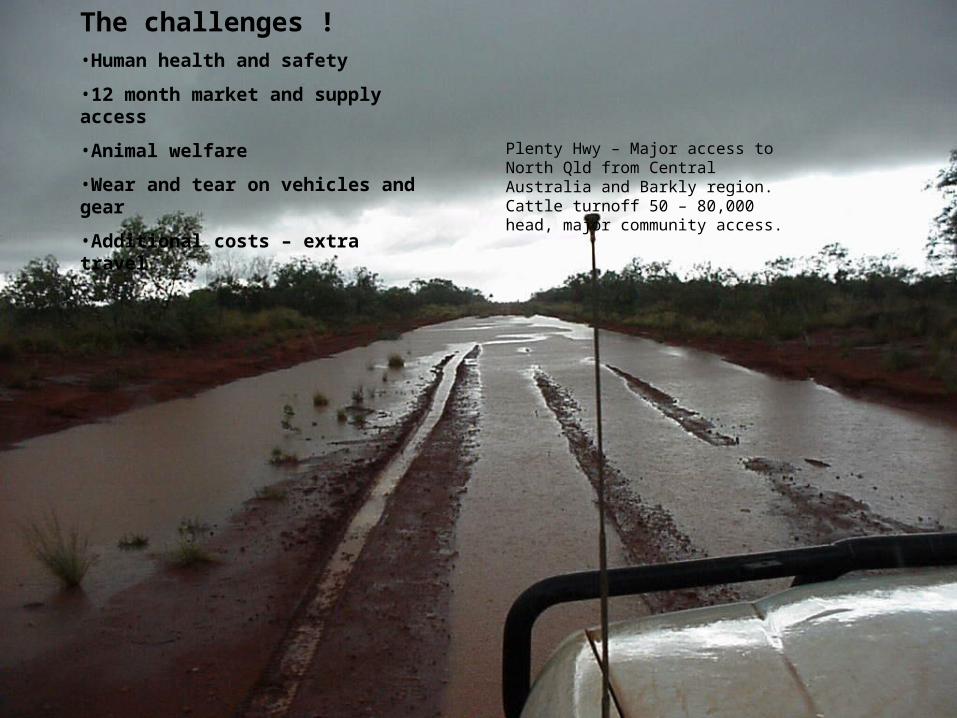

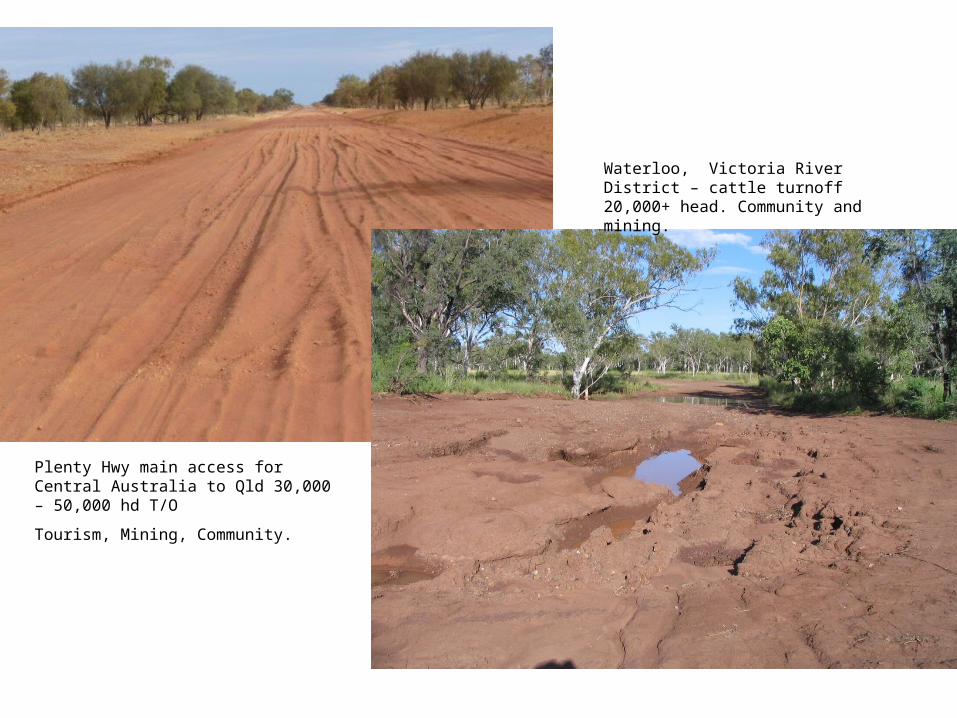

Plenty Hwy – Major access to North Qld from Central Australia and Barkly region. Cattle turnoff 50 – 80,000 head, major community access.

The challenges !•Human health and safety

•12 month market and supply access

•Animal welfare

•Wear and tear on vehicles and gear

•Additional costs – extra travel

Plenty Hwy

Oenpelli Rd, east East Alligator Crossing.– only access to Northern Arnhem Land. Closed 4 months of the year. Cattle turnoff 8,000 head, major community access, mining, tourism, huge prospective area.

Numery Rd, Central Australia – Beef, mining, community.

Tanami Rd – major mining, community and tourism and link to WA Kimberley.

Plenty Hwy main access for Central Australia to Qld 30,000 – 50,000 hd T/O

Tourism, Mining, Community.

Waterloo, Victoria River District – cattle turnoff 20,000+ head. Community and mining.

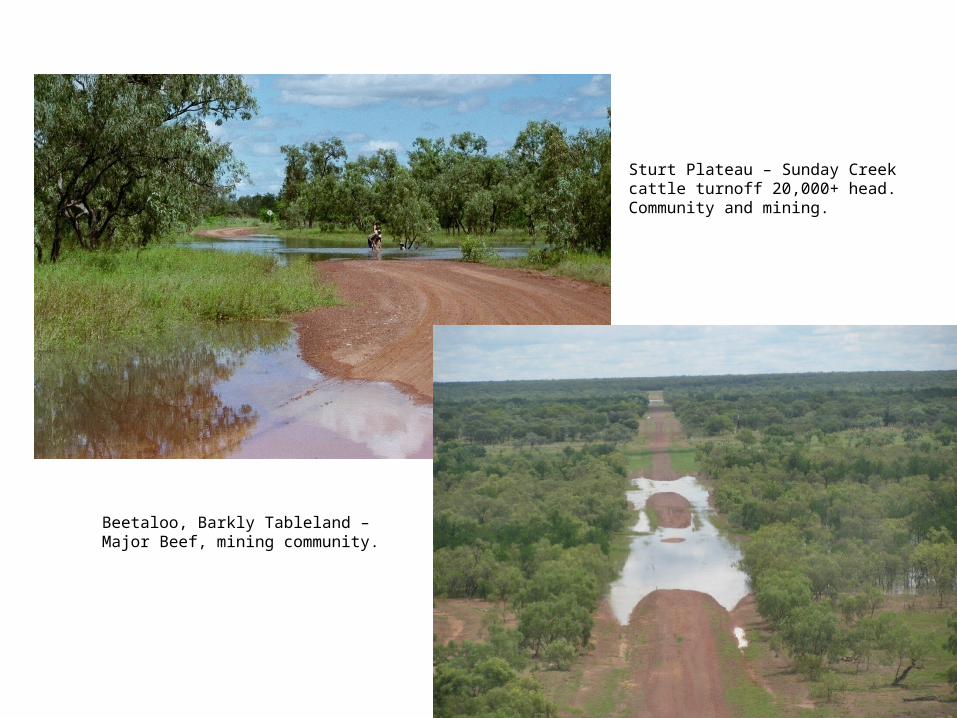

Sturt Plateau – Sunday Creek cattle turnoff 20,000+ head. Community and mining.

Beetaloo, Barkly Tableland – Major Beef, mining community.

Roads and infrastructure

Roads, depots, ports and markets

•More sophisticated and demanding markets – 12 month access

•Roads form the lifeline for trade in and out of pastoral zone

•Ramadan moving back towards wet season and peak demand for cattle – 6-8 years

•Efficiencies – transport - production, depot and port

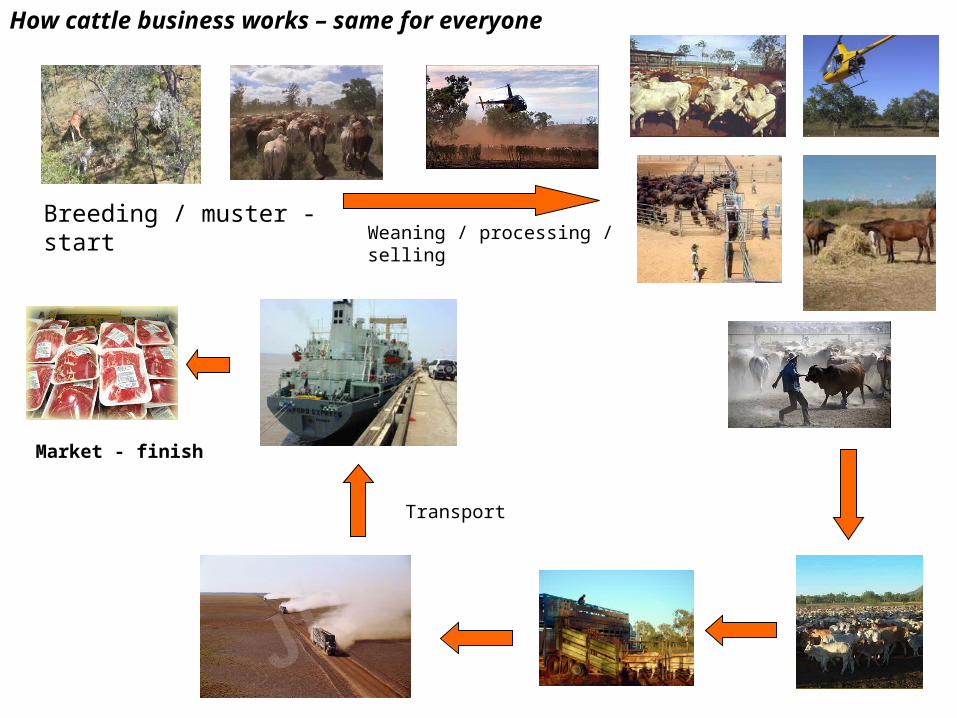

Breeding / muster - startWeaning / processing / selling

Transport

Market - finish

How cattle business works – same for everyone