lloyd s register: marine lloyd's register lng bunkering...

TRANSCRIPT

Lloyd’s Register: Marine

Lloyd's Register LNG Bunkering Infrastructure Study

Apostolos Poulovassilis Regional Marine Manager Lloyd’s Register EMEA 31st October 2012

Lloyd’s Register: Marine

Forecast of LNG-fuelled deep sea shipping

• Identify strategic ports and locations worldwide for possible LNG bunkering infrastructure facilities, and gather the opinions of bunkering ports on their likely provision of LNG bunkering facilities in future.

• Assess likely scale of demand for LNG-fuelled new construction and LNG as a fuel for deep sea shipping up to 2025

Lloyd’s Register: Marine

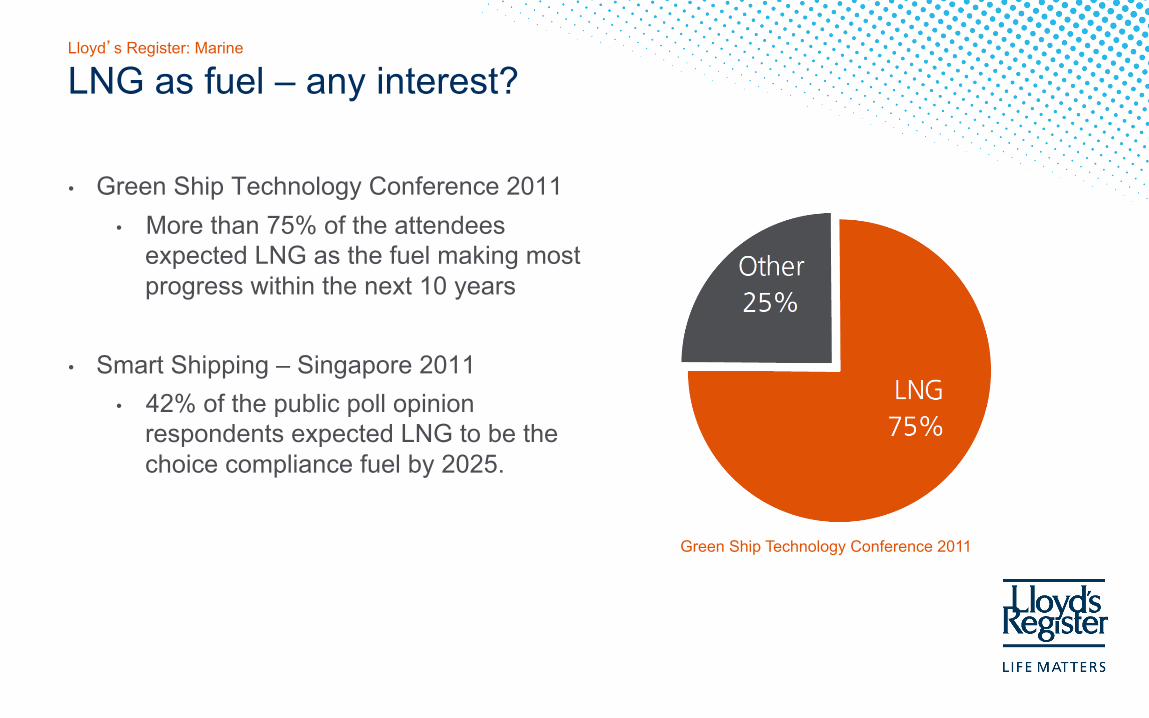

LNG as fuel – any interest?

• Green Ship Technology Conference 2011 • More than 75% of the attendees

expected LNG as the fuel making most progress within the next 10 years

• Smart Shipping – Singapore 2011 • 42% of the public poll opinion

respondents expected LNG to be the choice compliance fuel by 2025.

Green Ship Technology Conference 2011

Lloyd’s Register: Marine

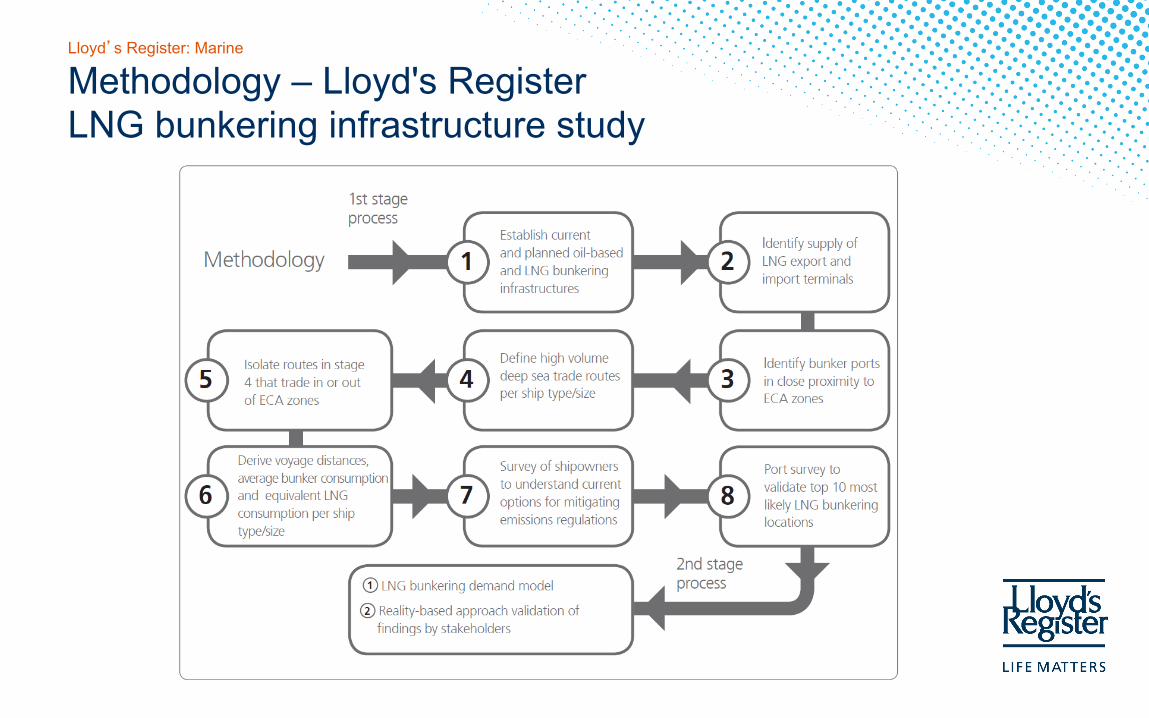

Methodology – Lloyd's Register LNG bunkering infrastructure study

Lloyd’s Register: Marine

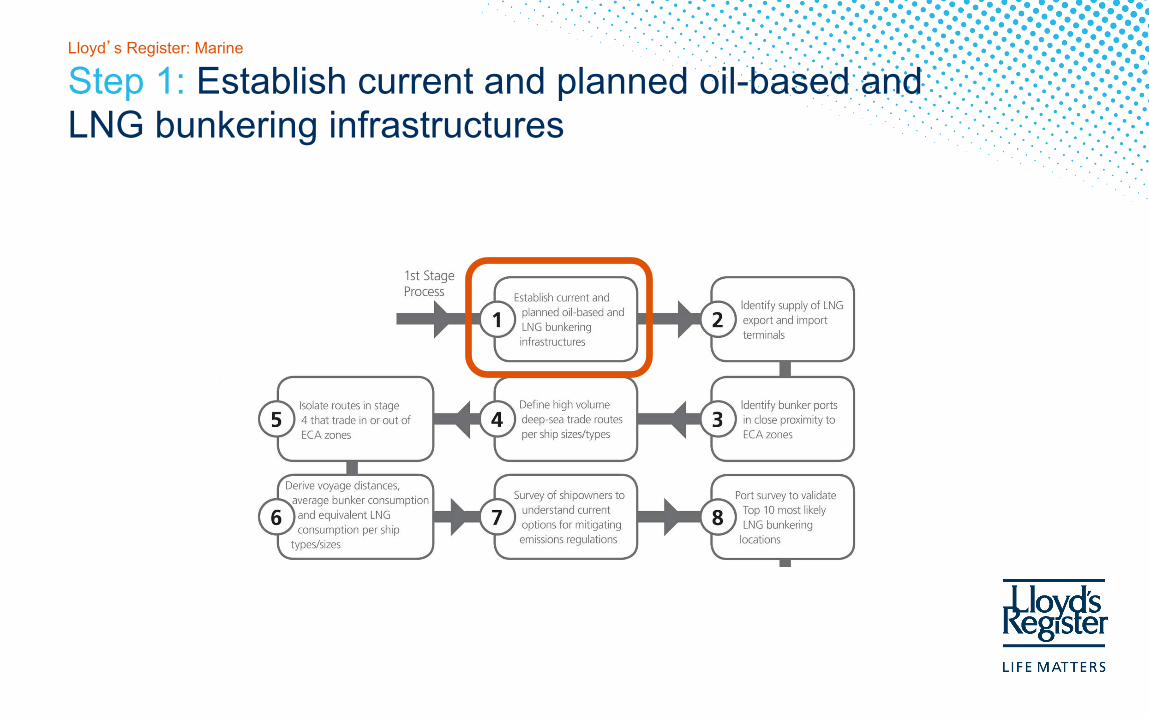

Step 1: Establish current and planned oil-based and LNG bunkering infrastructures

Lloyd’s Register: Marine

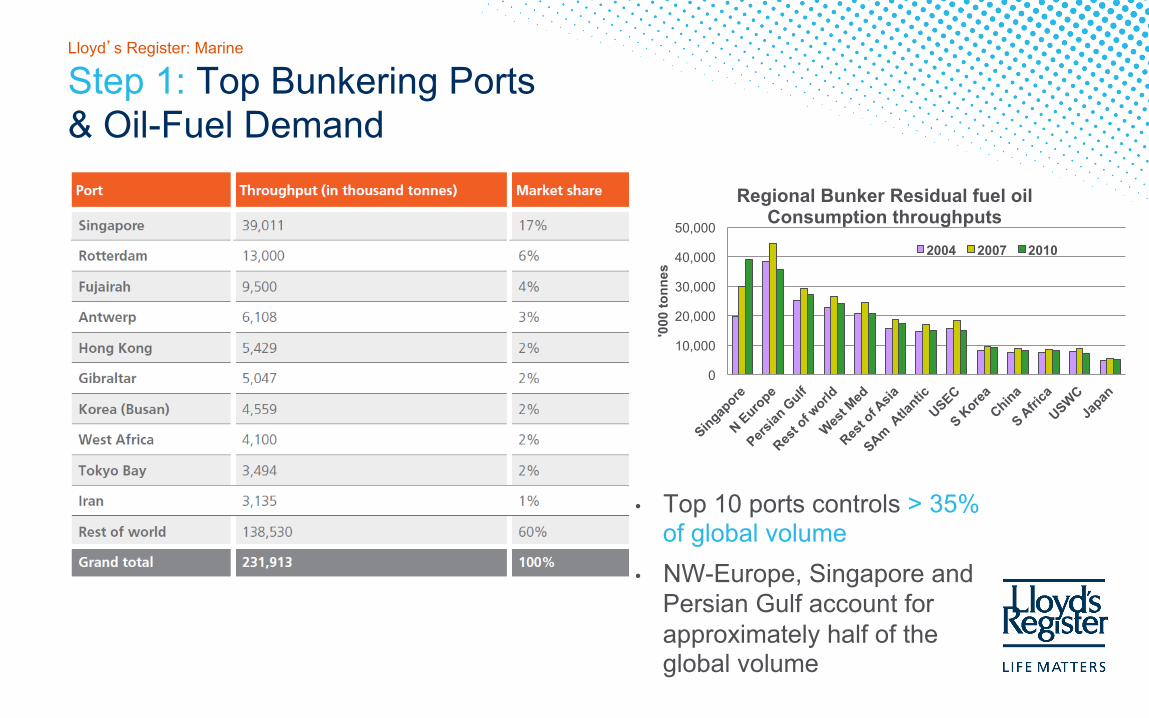

Step 1: Top Bunkering Ports & Oil-Fuel Demand

0

10,000

20,000

30,000

40,000

50,000

'000

tonn

es

Regional Bunker Residual fuel oil Consumption throughputs

2004 2007 2010

• Top 10 ports controls > 35% of global volume

• NW-Europe, Singapore and Persian Gulf account for approximately half of the global volume

Lloyd’s Register: Marine

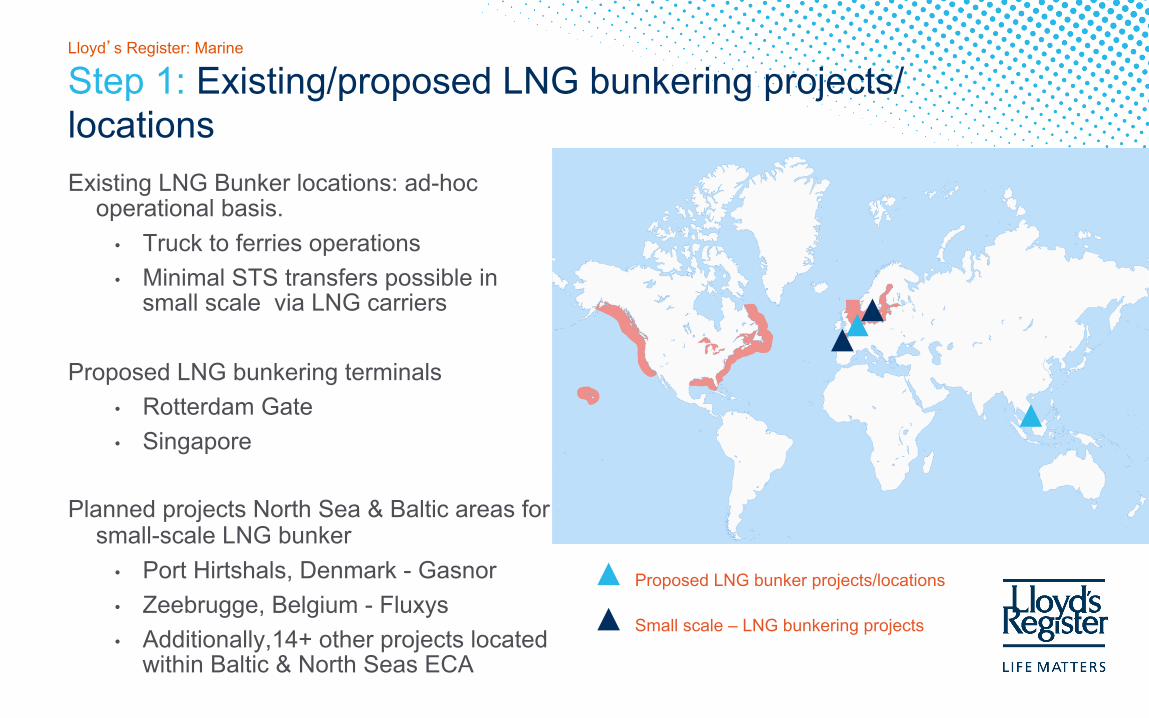

Step 1: Existing/proposed LNG bunkering projects/locations Existing LNG Bunker locations: ad-hoc

operational basis. • Truck to ferries operations • Minimal STS transfers possible in

small scale via LNG carriers

Proposed LNG bunkering terminals • Rotterdam Gate • Singapore

Planned projects North Sea & Baltic areas for small-scale LNG bunker

• Port Hirtshals, Denmark - Gasnor • Zeebrugge, Belgium - Fluxys • Additionally,14+ other projects located

within Baltic & North Seas ECA

Proposed LNG bunker projects/locations

Small scale – LNG bunkering projects

Lloyd’s Register: Marine

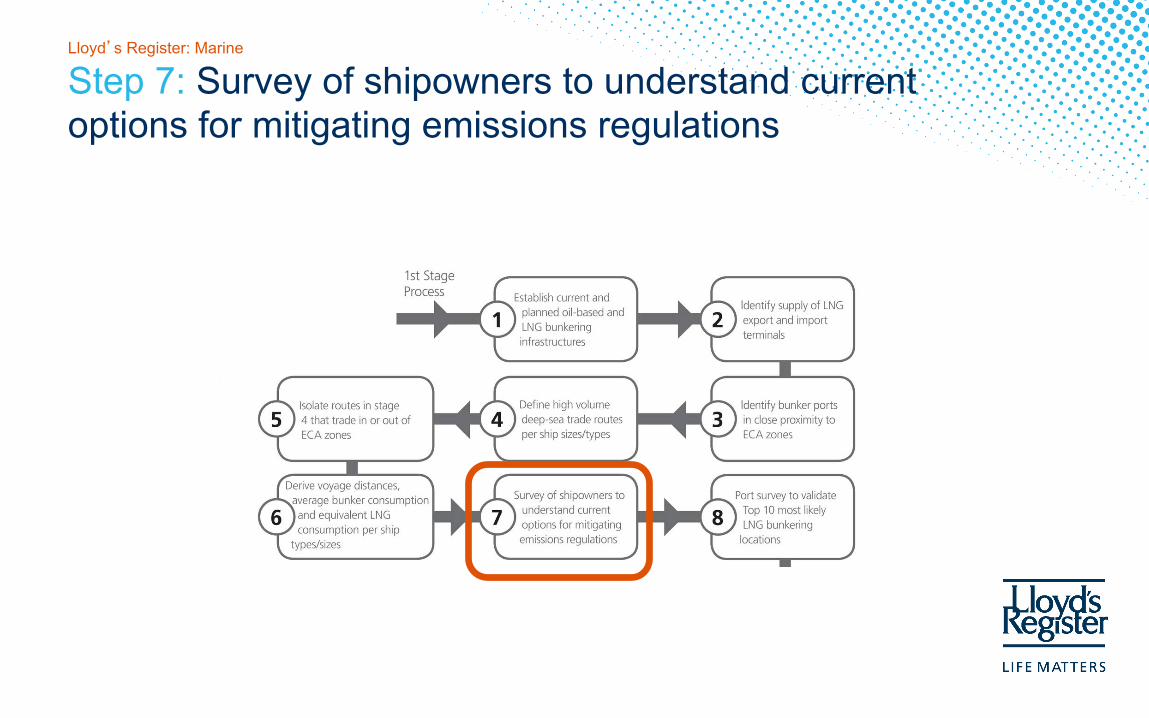

Step 7: Survey of shipowners to understand current options for mitigating emissions regulations

Lloyd’s Register: Marine

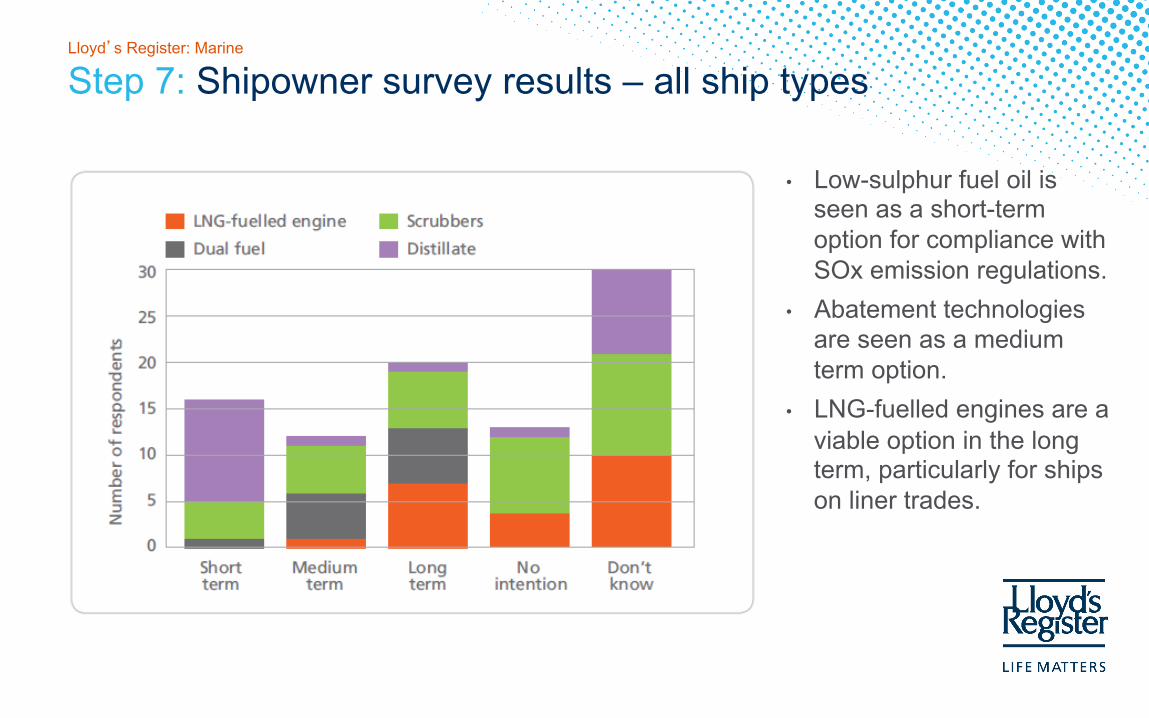

Step 7: Shipowner survey results – all ship types

• Low-sulphur fuel oil is seen as a short-term option for compliance with SOx emission regulations.

• Abatement technologies are seen as a medium term option.

• LNG-fuelled engines are a viable option in the long term, particularly for ships on liner trades.

Lloyd’s Register: Marine

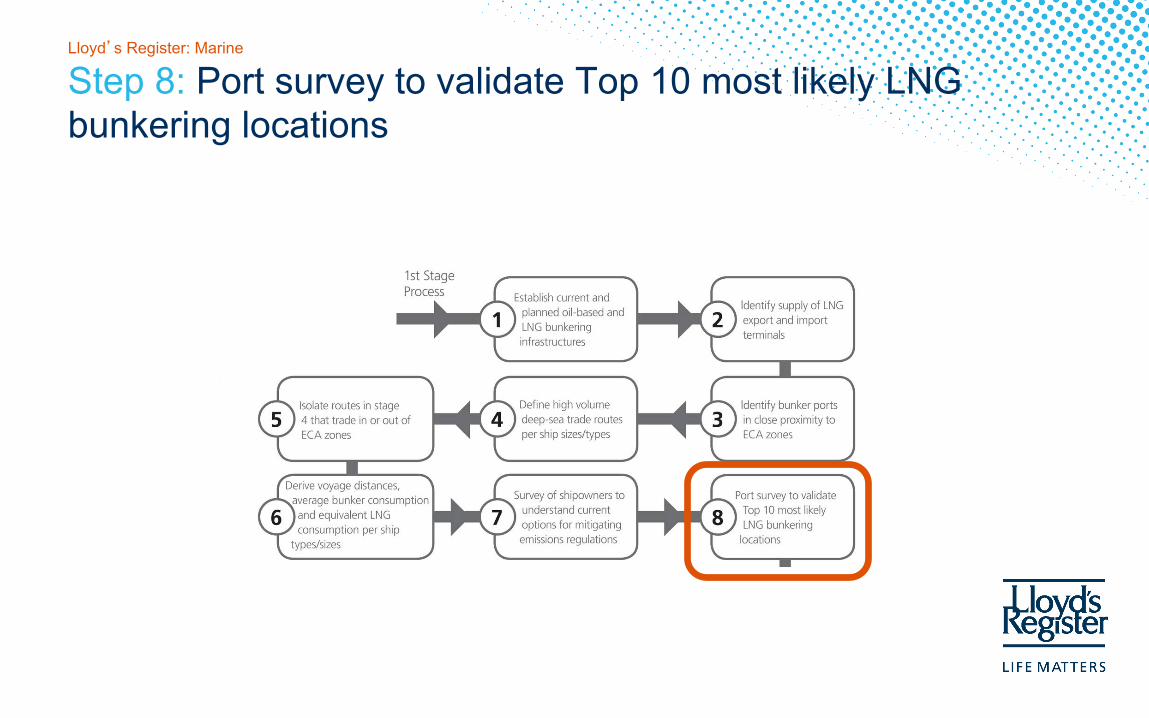

Step 8: Port survey to validate Top 10 most likely LNG bunkering locations

Lloyd’s Register: Marine

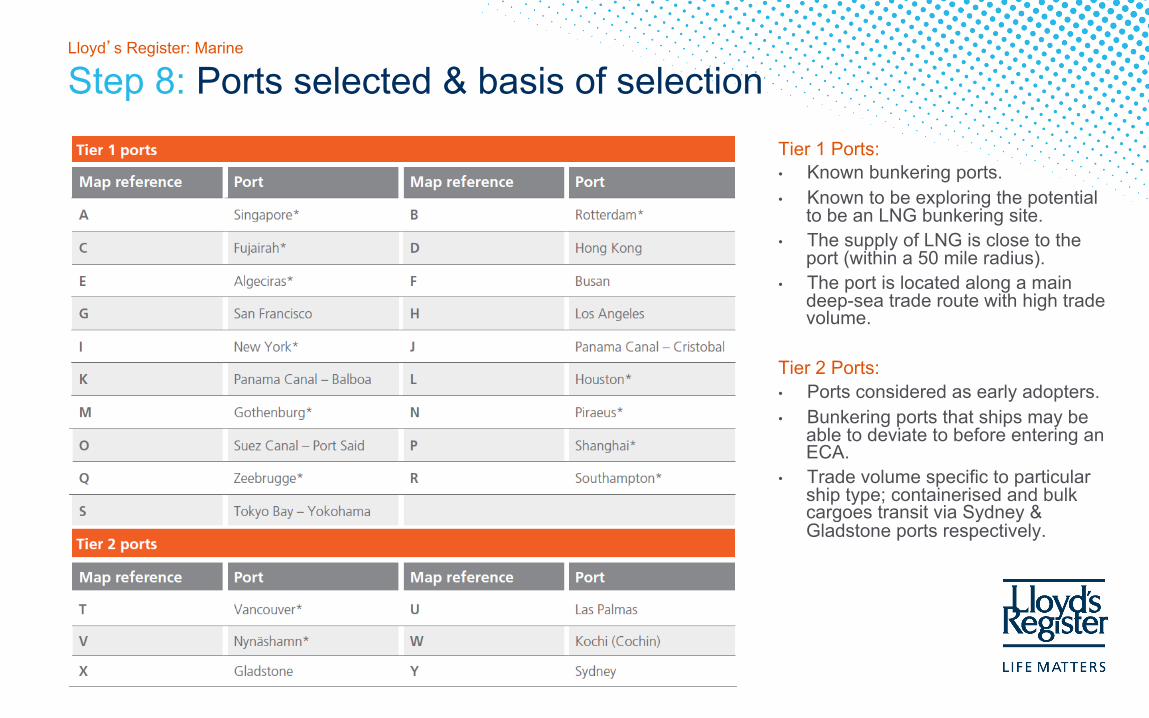

Step 8: Ports selected & basis of selection Tier 1 Ports: • Known bunkering ports. • Known to be exploring the potential

to be an LNG bunkering site. • The supply of LNG is close to the

port (within a 50 mile radius). • The port is located along a main

deep-sea trade route with high trade volume.

Tier 2 Ports: • Ports considered as early adopters. • Bunkering ports that ships may be

able to deviate to before entering an ECA.

• Trade volume specific to particular ship type; containerised and bulk cargoes transit via Sydney & Gladstone ports respectively.

Lloyd’s Register: Marine

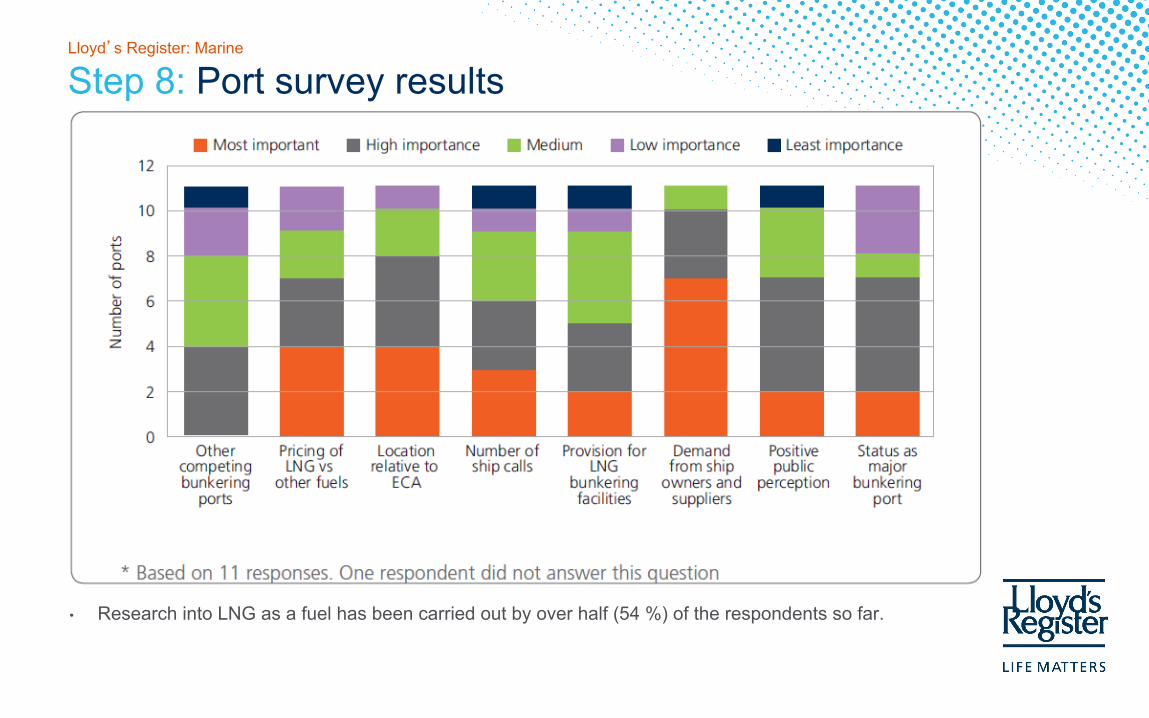

Step 8: Port survey results

• Research into LNG as a fuel has been carried out by over half (54 %) of the respondents so far.

Lloyd’s Register: Marine

2nd Stage Process

Lloyd’s Register: Marine

LNG bunkering demand model

Lloyd’s Register: Marine

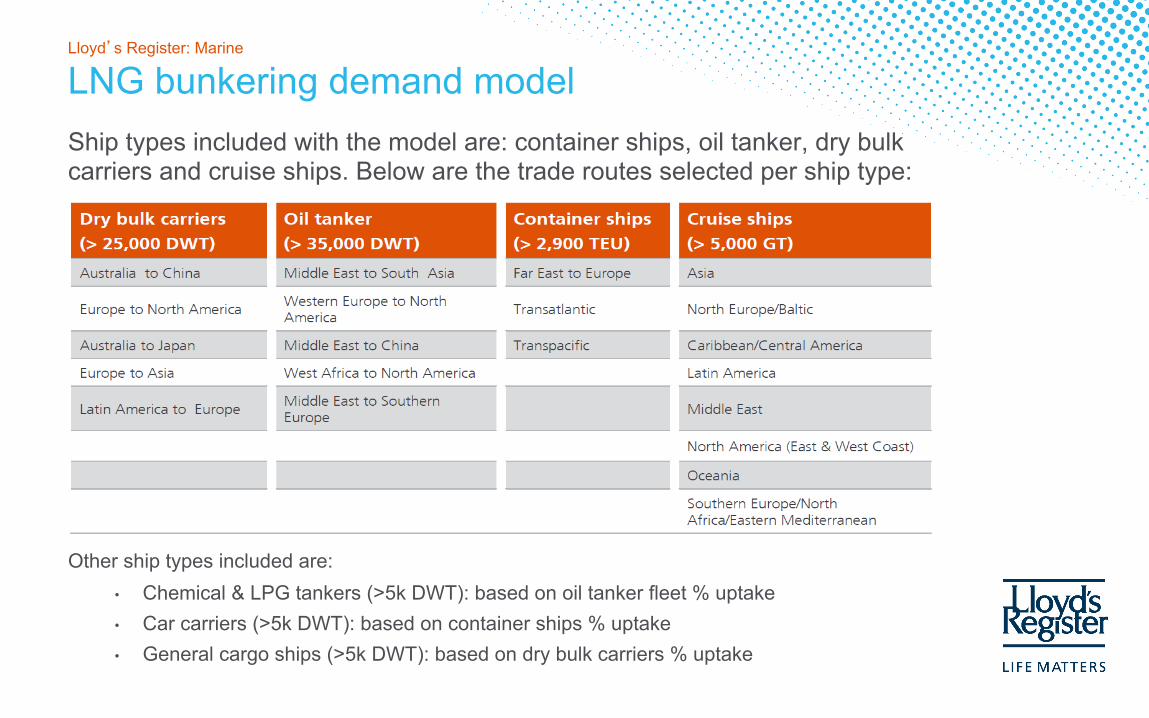

LNG bunkering demand model Ship types included with the model are: container ships, oil tanker, dry bulk carriers and cruise ships. Below are the trade routes selected per ship type: Other ship types included are:

• Chemical & LPG tankers (>5k DWT): based on oil tanker fleet % uptake • Car carriers (>5k DWT): based on container ships % uptake • General cargo ships (>5k DWT): based on dry bulk carriers % uptake

Lloyd’s Register: Marine

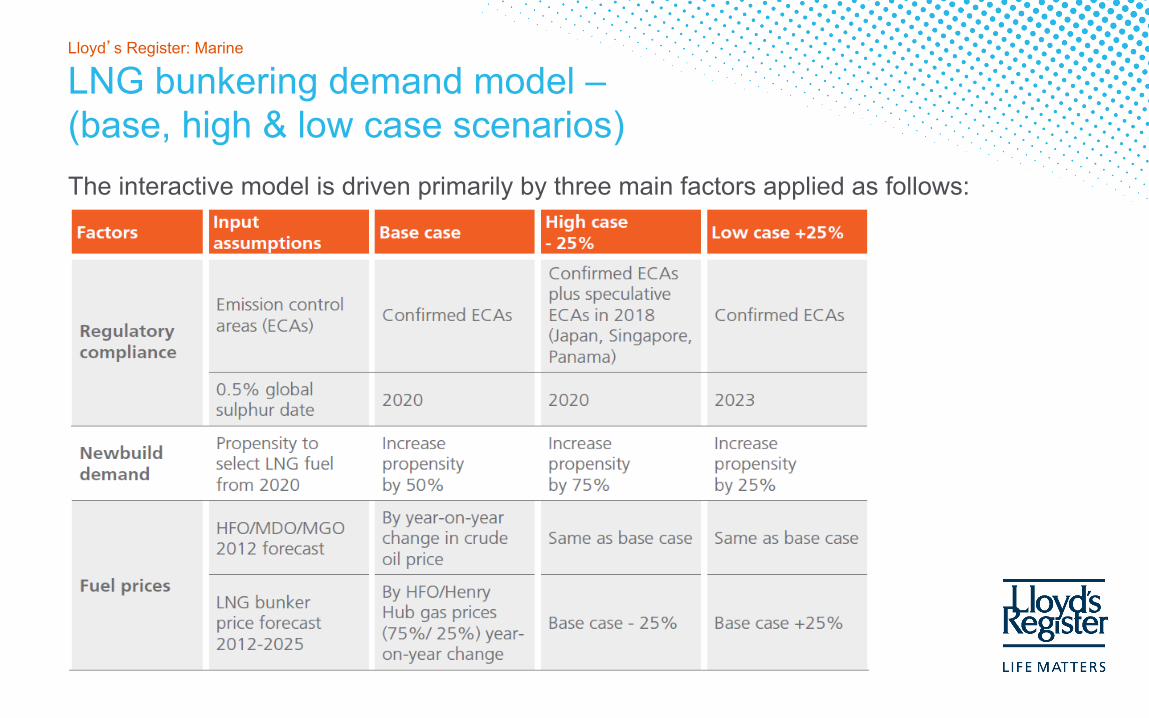

LNG bunkering demand model – (base, high & low case scenarios) The interactive model is driven primarily by three main factors applied as follows:

Lloyd’s Register: Marine

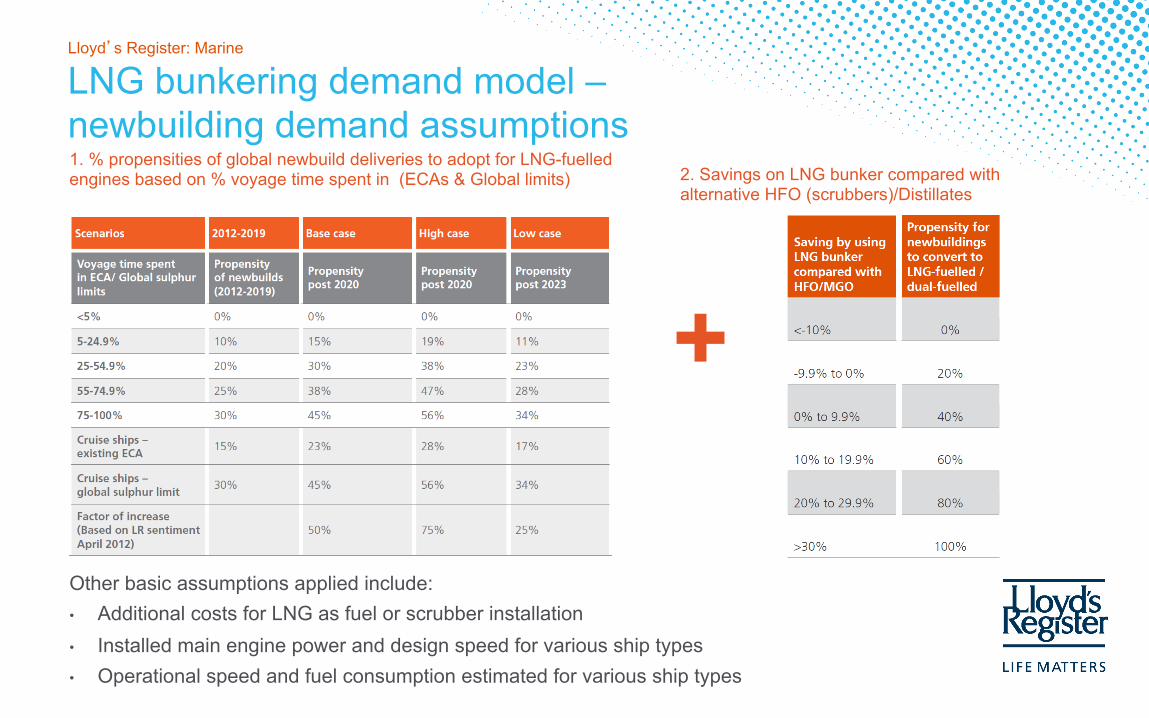

LNG bunkering demand model – newbuilding demand assumptions

Other basic assumptions applied include: • Additional costs for LNG as fuel or scrubber installation • Installed main engine power and design speed for various ship types • Operational speed and fuel consumption estimated for various ship types

1. % propensities of global newbuild deliveries to adopt for LNG-fuelled engines based on % voyage time spent in (ECAs & Global limits) 2. Savings on LNG bunker compared with

alternative HFO (scrubbers)/Distillates

+

Lloyd’s Register: Marine

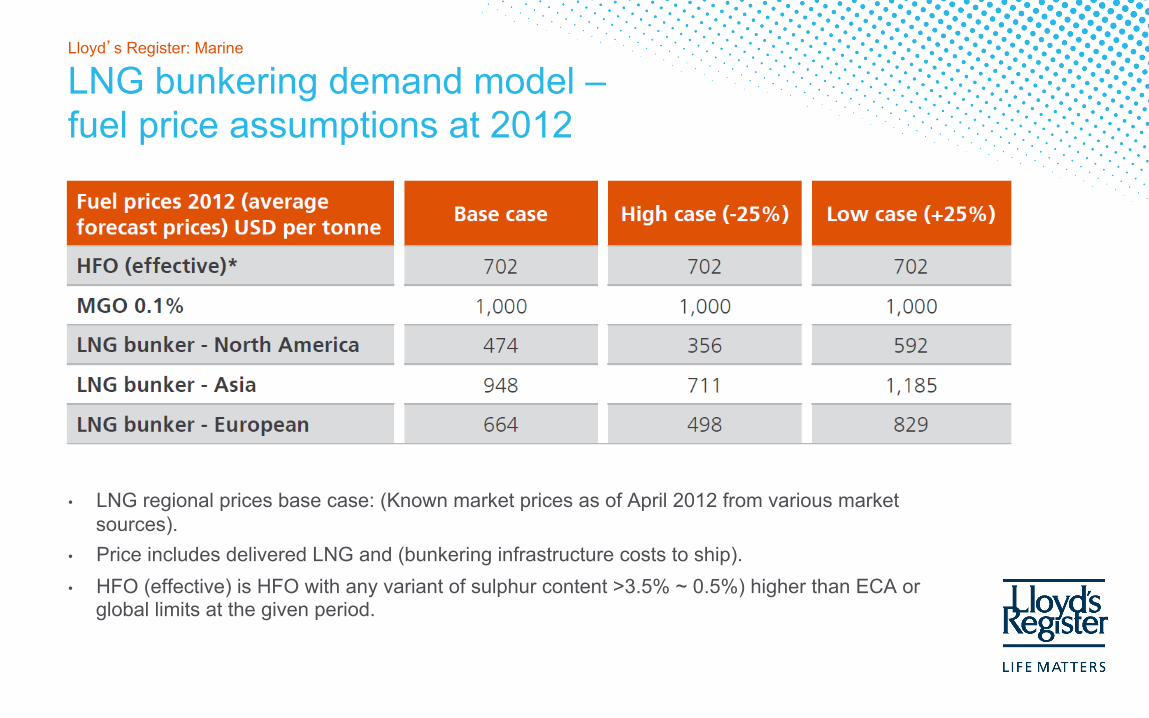

LNG bunkering demand model – fuel price assumptions at 2012

• LNG regional prices base case: (Known market prices as of April 2012 from various market sources).

• Price includes delivered LNG and (bunkering infrastructure costs to ship). • HFO (effective) is HFO with any variant of sulphur content >3.5% ~ 0.5%) higher than ECA or

global limits at the given period.

Lloyd’s Register: Marine

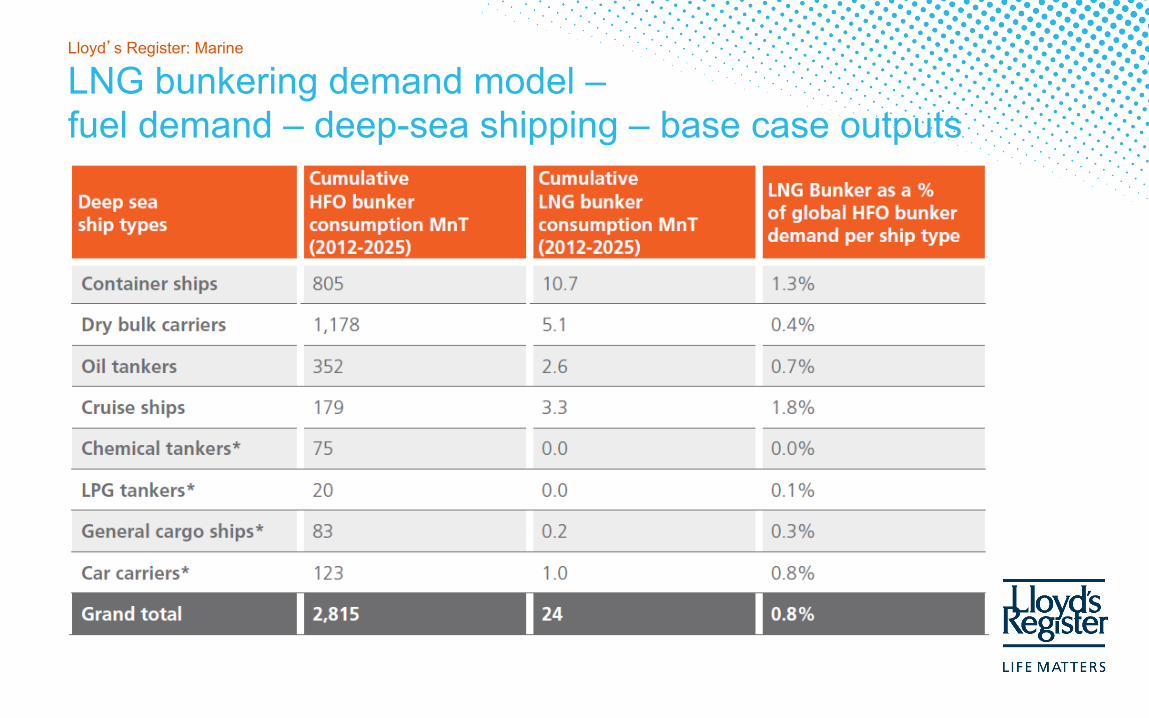

LNG bunkering demand model – fuel demand – deep-sea shipping – base case outputs

Lloyd’s Register: Marine

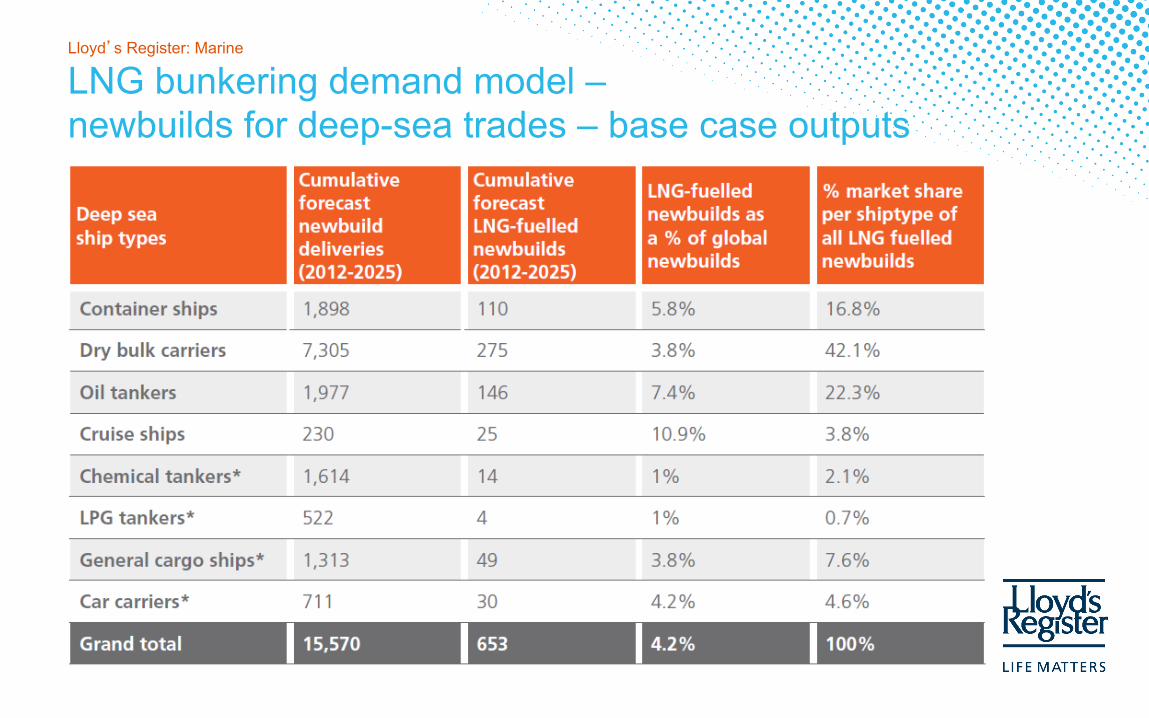

LNG bunkering demand model – newbuilds for deep-sea trades – base case outputs

Lloyd’s Register: Marine

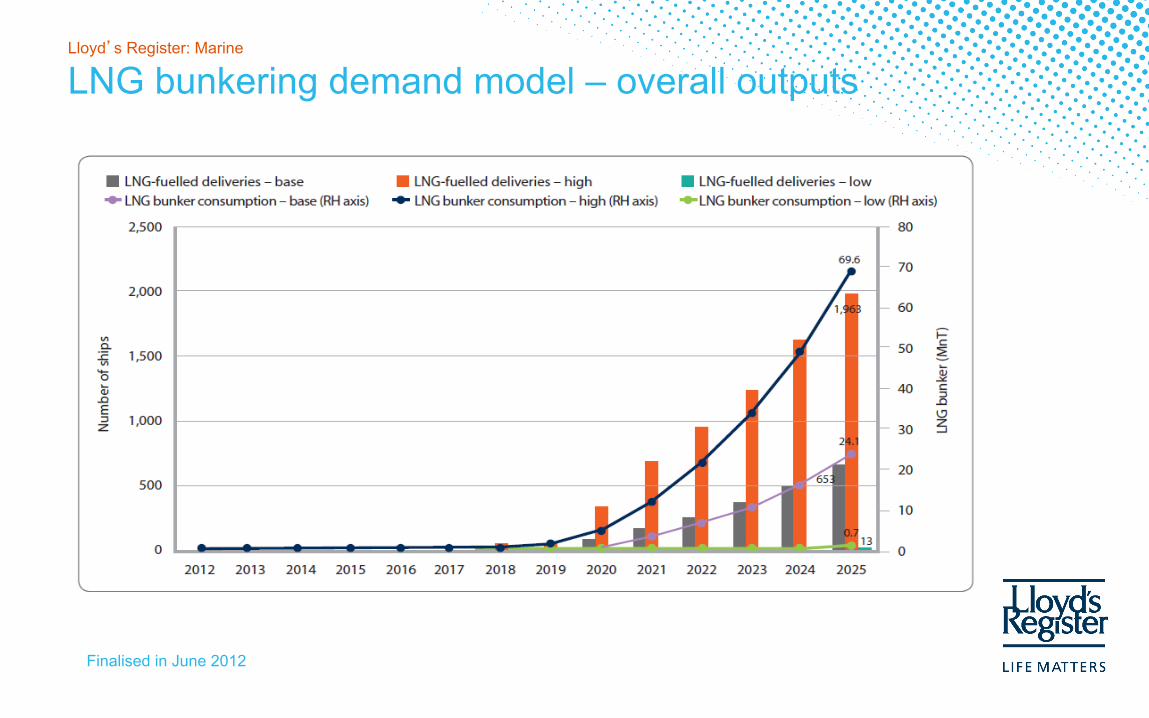

LNG bunkering demand model – overall outputs

Finalised in June 2012

Lloyd’s Register: Marine

Conclusion

• Existing oil bunkering hubs are well positioned to supply LNG bunker for ships, if demanded by owners.

• Dedicated global LNG bunkering facilities is still a challenge. • LNG bunkering in short-sea shipping regionally could facilitate

investments in deep-sea routes. • Solutions will be ship type and trade route specific. • LNG-fuelled engines are a viable options for deep sea trades in long-term

(10+ years) particularly on liner trades. • Likelihood of global LNG bunkering facilities being established will depend

on high demand for LNG-fuel on deep-sea trades, which will be driven by the price of LNG relative to current and future fuel alternatives.

Lloyd’s Register: Marine

Reality-based approach validation of findings by stakeholders

Lloyd’s Register: Marine

Reality-based approach validation of findings by stakeholders • Validation of set assumptions used within the model – done

• Reiteration of some values used within the model – done

• Following one of our stakeholder’s review, the model has now been adapted recently to focus on a specific region and quantify demand for LNG bunker fuel within the region – ongoing process

• Sensitivity testing and validation of the model will the done at intervals as the market evolve – ongoing process

Lloyd’s Register: Marine

Next Steps

1. Continual yearly updates of the model and press releases of periodic findings.

2. LNG bunkering demand model exploratory discussions with selected key market stakeholders, to seek and investigate appetite for further joint industry projects with potential consultative services. • Gas supplier; engine maker; shipyard; shipowner; port terminal

operator (ongoing process).

Lloyd’s Register: Marine

LNG-fuelled deep sea shipping –

the outlook for LNG bunker and LNG-fuelled newbuild demand up to

2025

Thank You!