libor manip

TRANSCRIPT

Electronic copy available at: http://ssrn.com/abstract=1201389

1

LIBOR Manipulation?

Rosa M Abrantes-Metz *

Principal LECG LLC

675 Third Avenue, 26th Floor New York, NY 10017

Michael Kraten

Assistant Professor of Accounting Sawyer Business School

Suffolk University 40 Court Street

Boston, MA 02108

Albert D Metz Vice President and Senior Credit Officer

Moody’s Investors Service 7 World Trade Center at 250 Greenwich Street

New York, NY 10007

Gim S Seow Associate Professor of Accounting

School of Business University of Connecticut

2100 Hillside Road Storrs, CT 06269

Preliminary Comments are Welcome

August 4, 2008

* Contact author. E-mail: [email protected]. Telephone: (212) 506-3981. The authors gratefully acknowledge the suggestions of Mukesh Bajaj, John Cochrane, John Connor, Guy Erb, George Judge, Cathy Niden, Sofia Villas-Boas, and the assistance of Marissa Rich, Shelly Yang, and especially Susan Press. The views expressed in this study belong solely to the authors and should not be attributed to the organizations with whom they are affiliated or their clients.

Electronic copy available at: http://ssrn.com/abstract=1201389

2

ABSTRACT On May 29, 2008, the Wall Street Journal (the Journal) printed an article that alleged that several global banks were reporting unjustifiably low borrowing costs for the calculation of the daily Libor benchmark. Specifically, the writers alleged that the banks were reporting costs that were significantly lower than the rates that were justified by bank-specific cost trend movements in the default insurance market. Although the Journal acknowledged that its “analysis doesn't prove that banks are lying or manipulating Libor,” it conjectured that these banks may “have been low-balling their borrowing rates to avoid looking desperate for cash.” In this paper, we extend the Journal’s study and perform the following analyses: (a) a comparison of Libor with other rates of short-term borrowing costs, (b) an evaluation of the individual bank quotes that were submitted to the British Banker's Association (BBA), and (c) a comparison of these individual quotes to individual CDS spreads and market cap data. We do so during the following three periods: 1/1/07 through 8/8/07 (Period 1), 8/9/07 through 4/16/08 (Period 2), and 4/17/08 through 5/30/08 (Period 3). We select these periods because three major news items were announced in the public press on August 9, 2007: (a) there was a “coordinated intervention” by the European Central Bank, the Federal Reserve Bank, and the Bank of Japan; (b) AIG warned that defaults were spreading beyond the subprime sector, and (c) BNP Paribas suspended three funds that held mortgage backed securities. Furthermore, on April 17, 2008, the Wall Street Journal first published the news that the BBA intended to investigate the composition of these rates. Individual Libor quotes are analyzed from January 2007 through May 2008, while the level of the Libor itself is studied from 1990 using Bloomberg data sources. After verifying that the patterns are essentially the same for the one month and three month Libor rates, we generally restrict our attention to the one month Libor. We also study data on other market indicators, both at aggregate levels and for the individual Libor banks. A few missing days are filled by linear interpolation. Our primary findings are that, while there are some apparent anomalies within the individual quotes, the evidence found is inconsistent with an effective manipulation of the level of the Libor. However, some questionable patterns exist with respect to the banks' daily Libor quotes, especially for the period ending on August 8, 2007, for which the intraday variance for banks quotes is not statistically different from zero. Key words: LIBOR, LIBOR quotes, manipulations, conspiracies, collusion, CDS spreads, market cap.

JEL classification: C10, C22, G14, G24, K20.

3

I. INTRODUCTION On May 29, 2008, the Wall Street Journal (the Journal) printed an article that alleged that several global banks were reporting unjustifiably low borrowing costs for the calculation of the daily Libor benchmark (Mollenkamp and Whitehouse, 2008). Specifically, the writers alleged that the banks were reporting costs that were significantly lower than the rates that were justified by bank-specific cost trend movements in the default insurance market. Although the Journal acknowledged that its “analysis doesn't prove that banks are lying or manipulating Libor,” it conjectured that these banks may “have been low-balling their borrowing rates to avoid looking desperate for cash.” The British Banker's Association (BBA)'s website claims that “BBA Libor is the primary benchmark for short term interest rates globally. It is used as the basis for settlement of interest rate contracts on many of the world’s major futures and options exchanges (including LIFFE, Deutsche Term Börse, Euronext, SIMEX and TIFFE) as well as most Over the Counter (OTC) and lending transactions.” Thus, for transactions that utilize Libor as a benchmark for establishing borrowing costs, a slight understatement of the rate may generate sizable wealth transfers from lenders to borrowers. Subsequent to the publication of the Wall Street Journal article, other major financial publications voiced similar concerns. On June 2, 2008, for instance, The Financial Times agreed that “... the rate of borrowing in Libor has lagged behind other market-based measures of unsecured funding used by the vast majority of financial institutions. This has aroused suspicions that the small group of banks which supply the BBA with Libor quotes have understated true borrowing rates so as not to fan fears (that) they have funding problems.” (Mackenzie and Tett, 2008). The motivation of this study is to extend the Journal's analysis by employing a wider array of comparative statistical techniques and methodologies to gain a more thorough understanding of the issues underlying such speculations. While statistical methods alone do not prove that manipulation has occurred in a particular market, some questionable patterns do exist with respect to the banks' daily Libor quotes. Our analyses of these apparent anomalies within the individual quotes suggest that the evidence is inconsistent with an effective manipulation of Libor. Nevertheless, the analyses presented in this study demonstrate that distinct non-random patterns of reported borrowing costs did exist during distinct periods of time, patterns that go beyond the findings that were originally reported by the Journal. In particular, for the period ending on August 8, 2009, the intraday variance of individual quotes is not statistically different from zero, and the banks deciding group for the Libor includes almost the entirety of the sixteen banks for a period of over seven months.

4

II. THE POSSIBILITY OF COLLUSION AND MANIPULATION In 1984, the BBA sought to standardize rate terms on interest rate swaps between London based banks. Two years later, in 1986, the BBA introduced Libor to standardize rate terms on a wider variety of securities, including syndicated loans, futures contracts, and forward rate agreements. Today, Libor's primary function is to provide a point of reference for unsecured loans between London based banks. It is also used as a point of reference for a wide variety of securities contracts transacted across the globe. Libor rates are quoted daily on ten major currencies: Australian dollar, British pound, Canadian dollar, European euro, Danish krone, Japanese yen, New Zealand dollar, Swedish krona, Swiss franc, and US dollar. In this study, we focus on the US dollar Libor. The BBA selects only 16 banks to provide daily rate quotes for the calculation of Libor. The BBA website states that this “reference panel of banks ... reflects the balance of the market by country and by type of institution. Individual banks are selected within this guiding principle on the basis of reputation, scale of market activity, and perceived expertise in the currency concerned.” It is noteworthy that these factors do not include any consideration of net borrowing or lending positions. Because the "middle 8" quotes are converted into Libor through a simple arithmetic mean calculation, as few as 5 (of 16) banks, acting in concert, can conceivably affect the published Libor. What may motivate banks to artificially inflate or deflate rates? From a fiscal perspective, banks that are "net borrowers" would benefit from lower rates. Conversely, banks that are "net lenders" would benefit from higher rates. Although an analysis of the protocols employed to select Libor's 16 banks is beyond the scope of this study, the nature of the composition of this group might generate an opportunity for collusion if the majority of these banks tend to be “net borrowers” or “net lenders.”1 Collusion may generate non-fiscal benefits as well. The Journal has suggested that banks may use the Libor submission process to manage their perceived reputation and risk. In other words, they may use the Libor calculation process to signal to the market that their operating costs are lower (i.e. that they are more fiscally healthy) than they are in reality. Because Libor submissions are released to the general public, banks may also be able to utilize the process to signal to each other in much the same way as airlines use their online ticket reservation systems to communicate their pricing intentions.2 In addition, banks that operate in multiple global markets may be motivated to use Libor as a "hedge" (or, at a minimum, as an alternative financing resource) against rate fluctuations elsewhere. For instance, an American bank with operations in London might benefit by keeping Libor rates artifically low as compared to the Federal Funds Rate. 1 See Mackenzie (2008) and Mollenkamp and Norman (2008) for recent critiques of the Libor methodology. 2 See Konrad and Sandoval (2002) for a critique of systems such as American Airline's Sabre, Delta's Worldspan,

and United's Apollo.

5

This study presents an analysis that addresses the possibility of Libor manipulation and collusion by the 16 banks. Manipulation, though, can manifest in many forms. Henceforth, in this study, the term “manipulation” refers to potential anticompetitive behavior by the 16 banks when acting on their own, i.e., without any explicit coordination activities. On the other hand, the term “collusion” refers to behavior by the banks when acting as a group in a coordinated manner. This paper is organized as follows. Section II presents a literature review of bank reputation, credit ratings, and cost of capital studies, as well as the empirical methods that are utilized to detect conspiracies and manipulations of different types. Section III discusses our methodology and findings, and Section IV concludes with a discussion of implications and avenues for future research.

II. LITERATURE REVIEW

A. BANK REPUTATION, CREDIT RATINGS, AND THE COST OF CAPITAL The banking literature is vast. Our goal in this brief review is to highlight the linkages between bank reputation, credit ratings, and the cost of capital. Bank Reputation in Securities Underwriting Market

There is an extensive stream of literature on the reputational role of investment banks and auditors in establishing corporate securities' underwriting fees and quality. Reputation is defined as a complex phenomenon that requires careful management.

Using a sample of initial bank notes offered by new banks during the American Free

Banking Era (1838-1860), Gorton (1996) documented larger discounts for the debt of new banks as compared to banks that have credit histories (but that are otherwise identical). Furthermore, this excess discount declined over time as lenders observe defaults. This declining interest rate corresponds to the formation of reputation, a valuable asset that provides an incentive for banks not to choose risky projects. Prior to the establishment of reputation, new banks that issue debt are monitored more intensely.

To assess the importance of commercial bank reputation, Johnson (1997) examined the effect of bank characteristics on changes in client firm value during bank loan announcements. He found that valuation effects are positively related to bank deposit size and capital ratios, and are inversely related to loan loss provision ratios. The results imply that high-quality firms that need to raise external capital are motivated to develop relationships with large high-quality banks in order to avoid pooling with other bank loan customers or issuers of public securities in spite of deposit insurance.

Johnson’s findings are consistent with empirical findings for quality differentiation across

6

audit firms and investment bankers. In Livingston and Miller (2000), for instance, bond underwriters with stronger reputations charged significantly lower underwriting fees and provided higher offering prices (i.e. lower offering yields). Hubbard, Kuttner and Palia (2002) used a matched sample of individual loans, borrowers, and banks to investigate the effect of banks' financial health on the cost of loans after controlling for borrower risk and information costs. They found that low-capital banks tend to charge higher loan rates than well-capitalized banks. This effect is primarily associated with firms for which information costs are likely to be important. They also found that, when borrowing from weak banks, firms tend to hold more cash.

One implication of this stream of research is that banks' underwriting decisions reflect reputational concerns and are thus informative of issue quality. A second implication is that economic rents are earned on reputation, and thus such rents provide continued incentives for underwriters to maintain their reputation. Bank Reputation and Cost of Capital

A bank’s reputation plays a major role in affecting its cost of capital. Reputational benefits accrue through effective credit policies that (a) screen out high-risk loans, (b) provide for rigorous monitoring of loan portfolios, and (c) ensure prudent choices of capital adequacy ratios. An early study by Ederington, Yawitz and Roberts (1987) reported that corporate bond yields are significantly correlated with: (a) their credit ratings and (b) a set of financial accounting variables on leverage and coverage ratios. These results suggest that market participants base their evaluations of the creditworthiness of issues on more than bond credit ratings, and that the ratings provides incremental information to the market beyond what is contained in the set of accounting variables. Fridson and Garman (1998) noted that, for a sample of high-yield debt issues, 56% of the variance in risk premiums can be explained by ratings, terms, secondary-market spreads, and other quantifiable factors. They also found that the effectiveness of underwriters in presenting issuers to investors appears to materially affect pricing. Employing a sample of new corporate bond issues from 1990 to 2000, Crabtree and Maher (2005) showed that the degree of predictability of a firm's earnings is positively associated with its bond rating, and is negatively associated with its offering yield. Also, Gabbi and Sironi (2005) analyzed the spreads of Eurobonds issued by major G-10 companies from 1991to 2001. They demonstrated that: (a) bond ratings appear to be the most important determinant of yield spreads, and that investors' reliance on the judgment of rating agencies increases over time; (b) primary market efficiency and expected secondary market liquidity are not relevant explanatory factors of the cross-sectional variability of spreads; and (c) rating agencies adopt 'through the cycle' evaluation criteria of default risk.

Yi and Mullineaux (2006) examined whether credit ratings on syndicated loans convey information to capital markets. Although initial loan ratings and upgrades are not informative,

7

they find that downgrades are indeed informative. They also found that borrower default characteristics explain cross-sectional variations in loan ratings, but that these ratings are only partially predictable. Furthermore, they demonstrated that ratings are related to loan rates, given the effect of other influences (i.e. default risk, information asymmetry, and agency problems) on yields. This suggests that ratings provide valuable information that is not reflected in financial reporting data. Ratings may, in fact, capture idiosyncratic information about recovery rates (as each of the agencies claims) or information about default prospects that is not otherwise available to the market. Additional evidence is provided by Narayanan, Rangan and Rangan (2007) about how commercial banks enhance their reputation by extending their bond underwriting activities to syndicated loans and private placements (i.e. private debt). In the absence of bond market reputation, a strong private debt market reputation enables commercial banks to win underwriting mandates from loan clients. Further, it allows them to commit to investors in a credible manner against the opportunistic use of lending information. This provides superior certification benefits in the form of higher issue prices relative to competing investment bank underwriters. Because this pricing benefit is not offset by higher underwriting fees, borrowers benefit from lower total issuance costs.

B. EMPIRICAL METHODS TO DETECT CONSPIRACIES AND MANIPULATIONS

Empirical methods have been developed and applied to screen for “markers” that are associated with the existence of conspiracies and manipulations in various industries. Of course, such markers periodically occur in the absence of anticompetitive behavior. Likewise, collusions and/or manipulations periodically occur in the absence of such markers. Nevertheless, although screening activities cannot provide conclusive evidence of the existence (or absence) of anti-competitive market behavior, they can be utilized to signal that pattern(s) of observed data are inconsistent with patterns that are normally expected to occur under conditions of market competition. Price-Fixing Conspiracies Harrington (2006) asserted that certain “collusive markers” are more likely to occur when price fixing conspiracies exist than under a competitive setting. A price-fixing conspiracy is defined as an agreement between cartel members on one or more terms (most commonly, but not always, the price term) that is (are) fixed for a common product. More often than not, cartel members also agree on market share rates, as well as on punishment mechanisms for members who deviate from these terms of agreement. Collusion in bidding activities has also been observed from time to time. In this study, such techniques are applied to screen for collusion in the establishment of Libor. The collusive markers for price that are typically utilized are: (a) higher than expected average prices, (b) reduced price variations across customers, (c) declines in imports on substitutes, (d) prices that are strongly positively correlated across firms, (e) a high degree of

8

uniformity across firms in product price and other dimensions, (f) low price variances, and (g) abrupt changes in price that cannot be explained by demand and/or cost movements. In addition, the collusive markers for quantity that are typically utilized are: (a) market shares that remain highly stable over extended periods of time, and (b) market shares between firms that are negatively correlated over time. Though any of these collusive markers can be used as a screening method, they vary in terms of ease of implementation. Nevertheless, they all compare data patterns in an industry or market against a benchmark data set, one that has been developed within the same industry or market during a different period of time, or one that has been developed in a comparable (but different) industry or market during the same period of time. Abrantes-Metz, Froeb, Geweke and Taylor (2006), for instance, analyzed price movements around the collapse of a bid-rigging conspiracy in the frozen perch industry. They found that the average price decreased by 16% and the volatility of this price as measured by its standard deviation increased by over 200%. They also found that these changes in price could not be explained by changes in cost, and that these price patterns followed those of cost patterns more closely under competitive conditions than under collusive conditions. Harrington (2008) provides a comprehensive survey of the academic literature regarding cartel detection methods. Abrantes-Metz and Froeb (2008) describe recent efforts by competition authorities worldwide in the development of screening devices. At the present time, though, none of these empirical methods is capable of distinguishing conditions of explicit collusion from conditions of tacit collusion. Additionally, even when these (and the following) methods detect abnormal behavior in the data, the findings should not necessarily be interpreted as a proof of wrongdoing. Alternative explanations must be studied as well. Market Manipulations Though the term “manipulation” commonly encompasses a wide variety of situations, it has traditionally been applied to the commodities markets. Various definitions of the term have been used in different situations. Nevertheless, many of these definitions share common features such as “causation” and “price artificiality” (Russo, 1983). Manipulations are, in general, quite different from traditional price-fixing cartels in at least two respects: (a) they typically involve fewer members within the group than a cartel, often just a single firm or individual, and (b) they are not necessarily focused on maintaining a fixed price level. Instead, their goals might involve increasing price movements. Screening processes for manipulations are very similar to those for conspiracies, but they are relatively more difficult to develop and implement because of the variety of forms that are utilized by manipulators. There are several common approaches to detect manipulation markers. They include searches for distortions in prices that cannot be explained by seasonality, a common explanation for price changes in commodities markets. A very common “red flag” for manipulation in commodities futures markets is backwardation, i.e., a condition where a futures price is lower

9

than a spot price, an inversion from the typical contango relationship. While episodes of backwardation can occur in the absence of manipulation (e.g. when supply is unexpectedly unable to meet demand despite the presence of competitive market conditions), such episodes generally do not last for a long time. Recently, Abrantes-Metz and Addanki (2007) developed a new method to screen for manipulations in commodities markets. They hypothesized that manipulation induces noise in the market and distorts market expectations about future prices. By using the futures price as the market expectation for the future spot price, and by applying their model to a well-known episode of manipulation that occurred in the silver market in 1979 and 1980, they found that manipulation induced more volatile market forecasting errors regarding future prices. Manipulation in the stock market, as in the commodities markets, can assume various forms. For instance, insiders may take actions that influence stock prices through accounting and earnings manipulation, by withholding critical information that is expected to influence stock prices prior to the granting of options, and by disseminating misleading information and/or rumors while backdating stock options. Aggarwal and Wu (2003), Heron and Lie (2006) and Goldberg and Read (2007) present such screens.

Finally, Benford’s law has also been used to detect data tampering in taxes, in financial ratios, and in survey data. Newcomb (1881) and Benford (1938) developed a mathematical law that is based on the empirical observation that, in many naturally occurring numerical data sets, the leading significant digits are not uniformly distributed but instead follow a logarithmic weak monotonic distribution. Applications of this stream of research include Judge and Schechter (2006) and Nigrini (2005).

III. METHODOLOGY AND FINDINGS The methodology applied in this paper is consistent with those that are typically used to investigate potential anticompetitive behavior by market participants. We look into structural breaks in the series of interest rates and compare them against “reliable” benchmarks that are not suspected of manipulation. Using these benchmarks, we compute “but for” series which we then compare against the actual series, testing for (any) material manipulation(s). In addition, we review the level of similarity of individual quotes (when compared to each other) on a daily basis, as measured by the intraday variance of the quotes. We then search for possible explanations for any observed patterns by comparing them against patterns of other relevant benchmarks.

Individual Libor quotes are analyzed from January 2007 through May 2008, while the level of the Libor itself is studied from 1990 using Bloomberg data sources. After verifying that the patterns are essentially the same for the one month and three month Libor rates, we generally restrict our attention to the one month Libor. We also study data on other market indicators, both

10

at aggregate levels and for the individual Libor banks. A few missing days are filled by linear interpolation. Our primary findings are that, while there are some apparent anomalies within the individual quotes, the evidence found is inconsistent with an effective manipulation of the level of the Libor. However, some questionable patterns exist with respect to the banks' daily Libor quotes. This section contains the following analyses: (a) a comparison of Libor with other rates of short-term borrowing costs, (b) an evaluation of the individual bank quotes, and (c) a comparison of these individual quotes to individual CDS spreads.

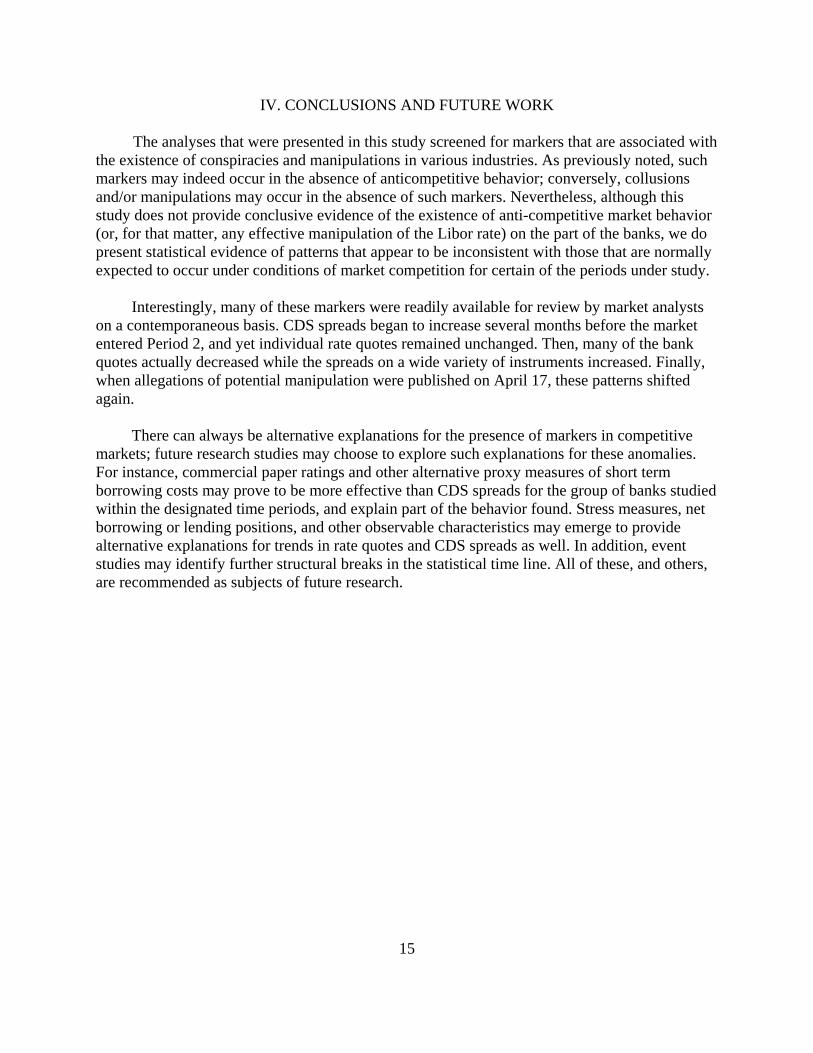

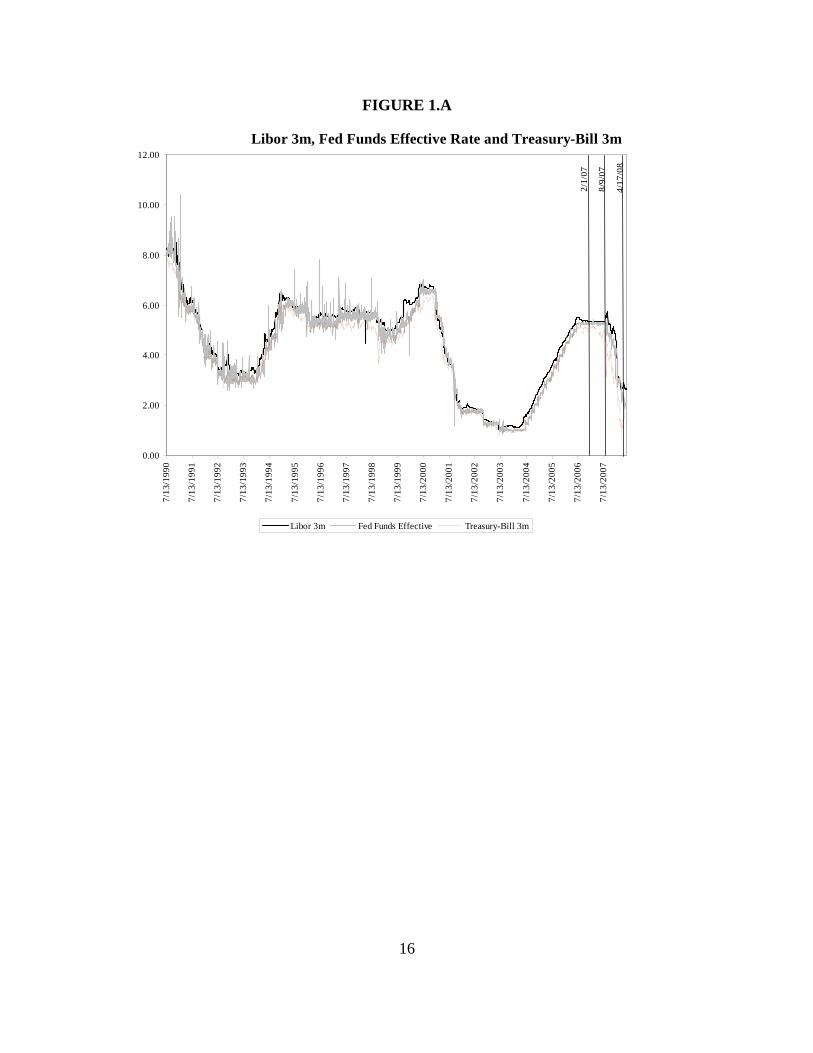

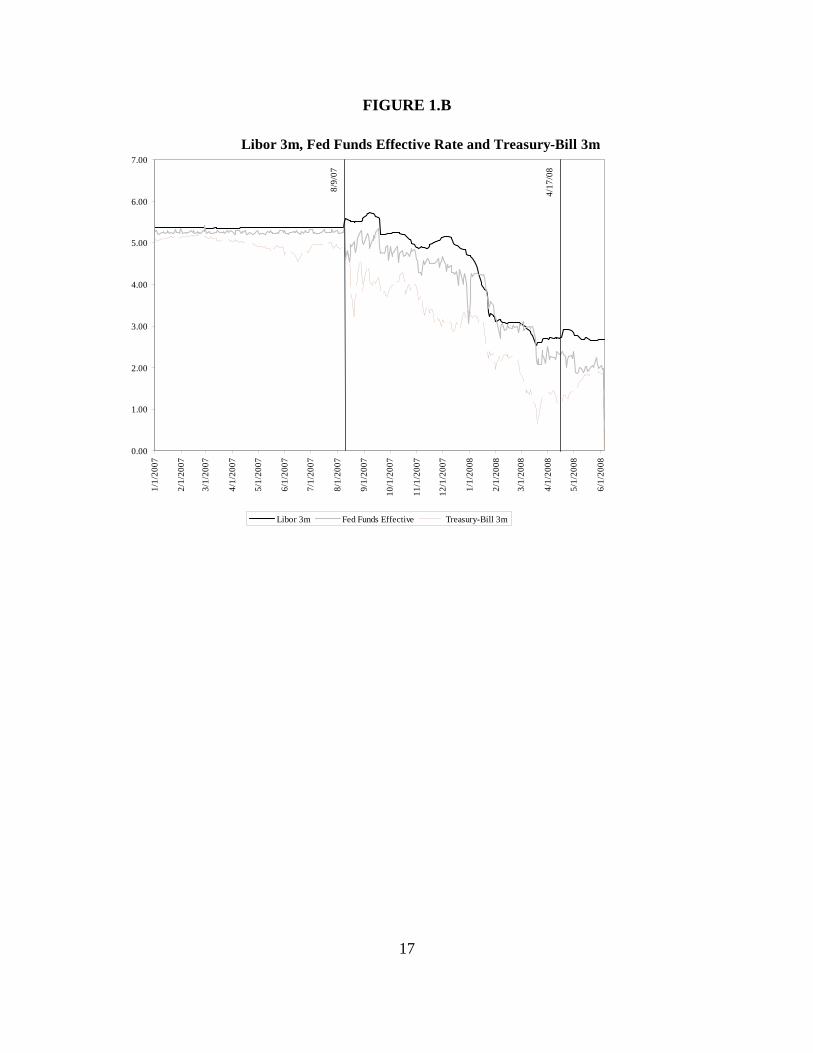

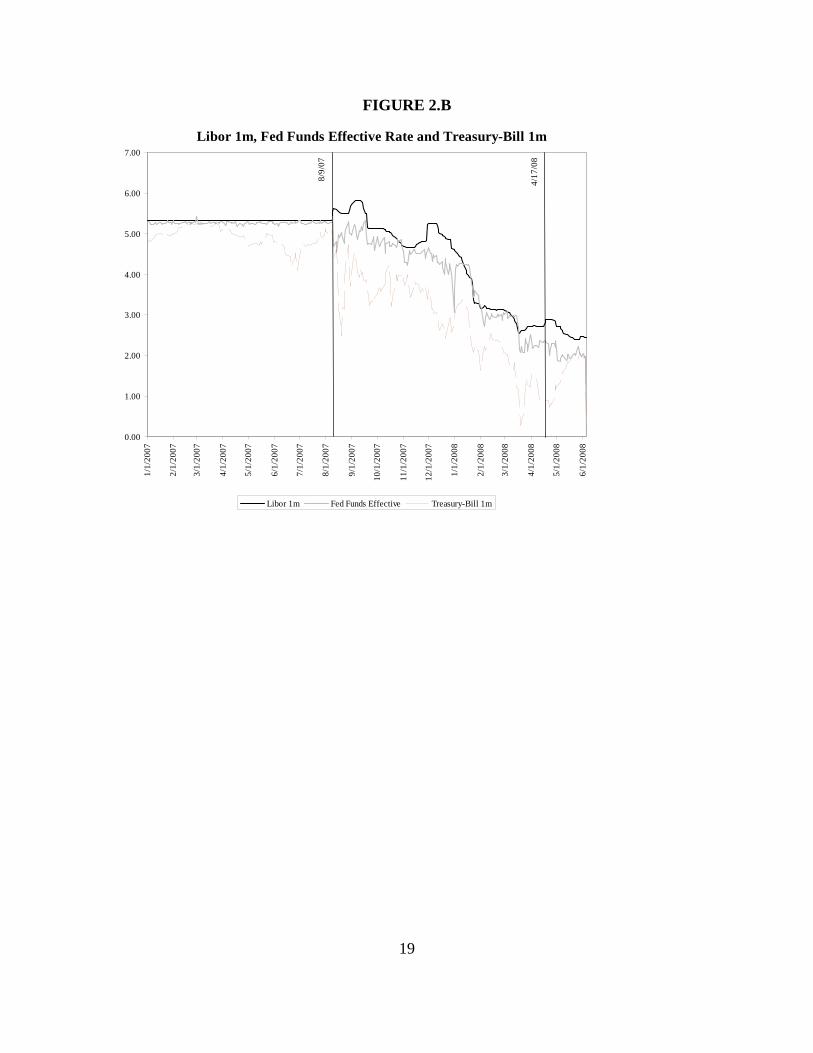

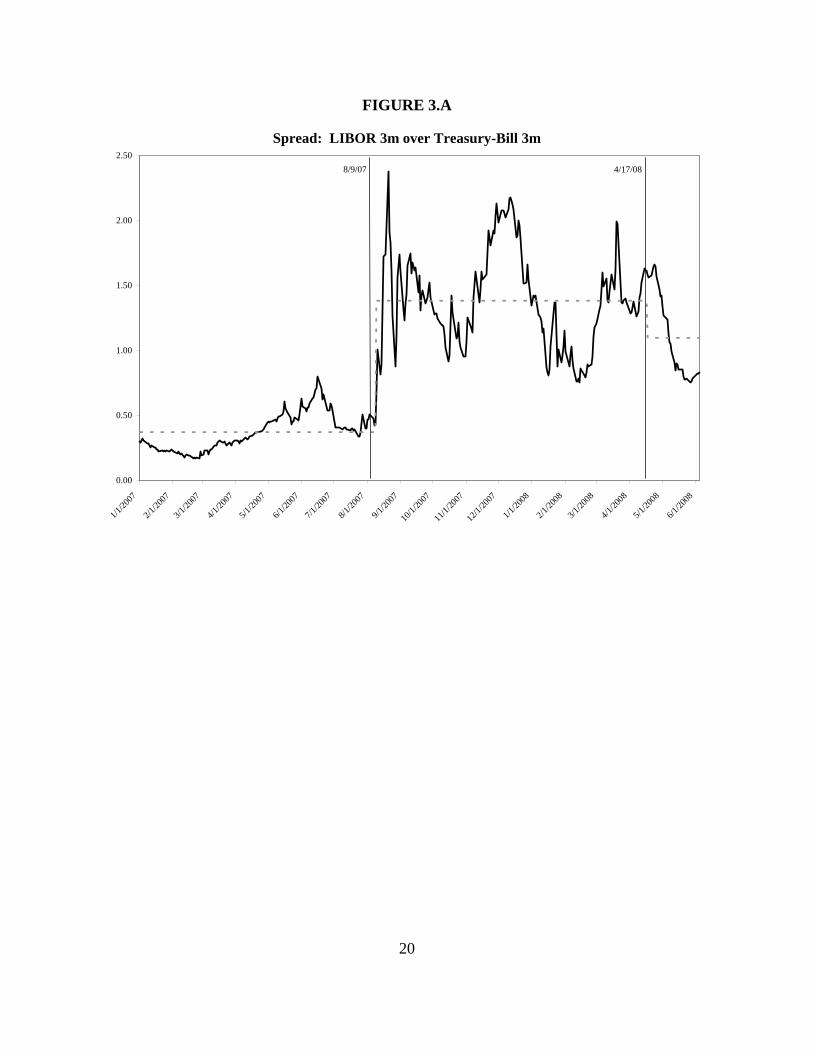

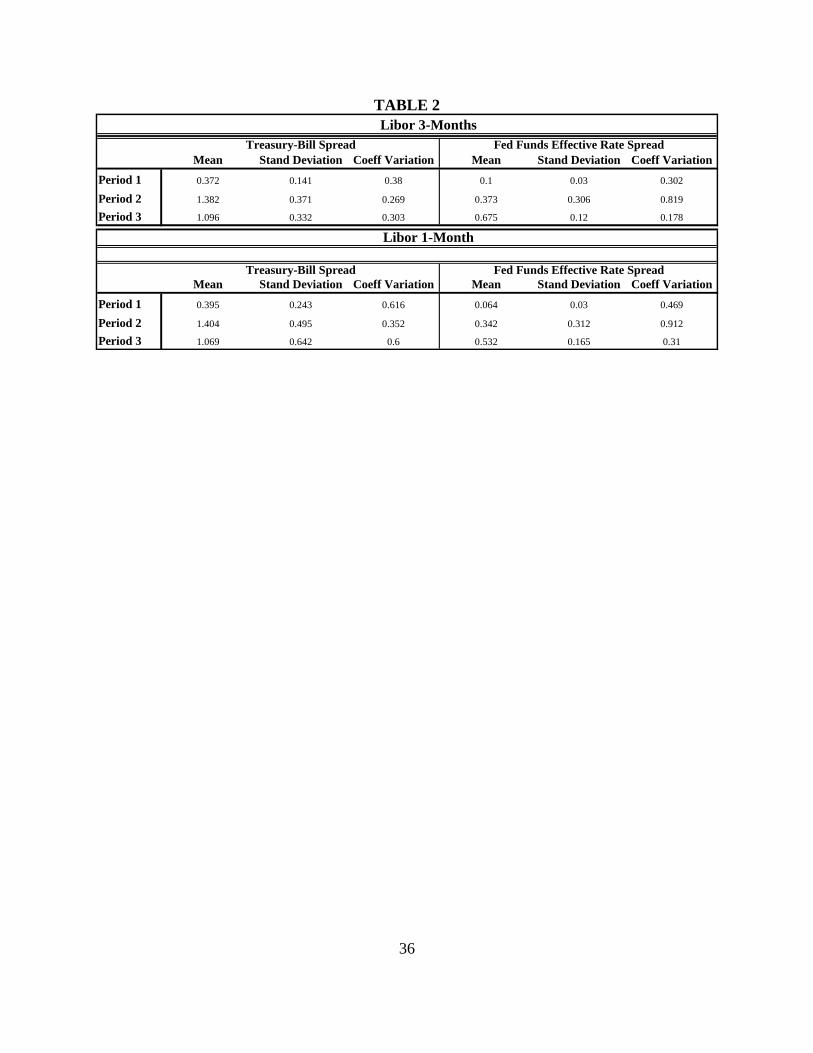

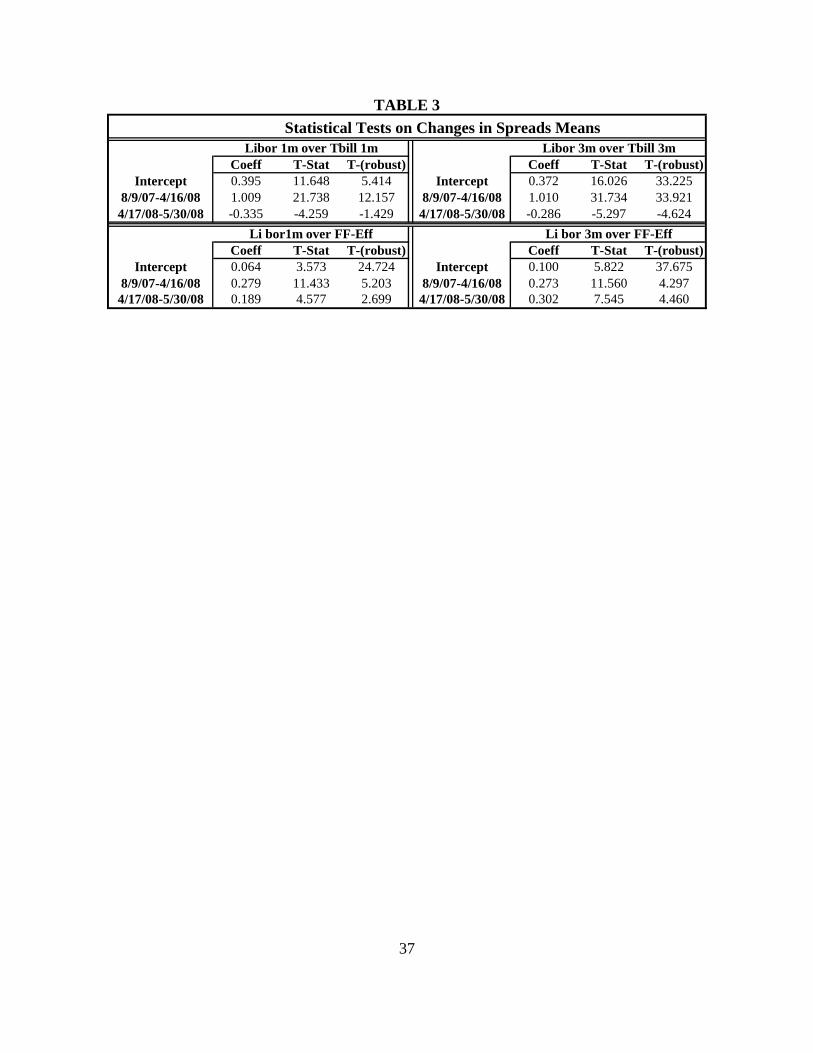

A. LIBOR AND BENCHMARKS We begin by comparing the 3 month Libor against the 3 month Treasury and the Federal Funds Effective rate.3 Figure 1.A covers the entire period of 1990 through 2008, while Figure 1.B focuses on the period from January 2007. Figures 2.A and 2.B are analogous presentations of the 1 month Libor. It is clear from these exhibits that the Libor closely follows the other rate indicators for both maturities. We continue this analysis but focus directly on the spreads of Libor over other rates, and we restrict our attention to the recent period beginning January 2007. Figure 3.A shows the spread of 3 month Libor over 3 month Treasury, separately identifying the mean spread within the subperiods 1/1/07 through 8/8/07 (Period 1), 8/9/07 through 4/16/08 (Period 2), and 4/17/08 on (Period 3). An increase in the spread beginning August 9, 2007 is evident and statistically significant. Figure 3.B is a similar presentation of the spread over the Fed Funds Effective Rate, and again we see a significant widening of this spread beginning August 9. Figures 4.A and 4.B are similar presentations of the 1 month Libor spreads; the same pattern of significantly wider spreads is apparent.

Three major news items were announced in the public press on August 9, 2007: (a) there was a “coordinated intervention” by the European Central Bank, the Federal Reserve Bank, and the Bank of Japan; (b) AIG warned that defaults were spreading beyond the subprime sector, and (c) BNP Paribas suspended three funds that held mortgage backed securities. This same day, there was a widening of spreads in terms of both average (i.e. mean) level and variance. In short, it would appear there is a “structural break” on August 9. Furthermore, we consider a second “structural break” on April 17, 2008, the day when the Journal first published the news that the BBA intended to investigate the accuracy of these rates. Table 1 restates these time period definitions.4 While it is true that spreads significantly widened beginning August 9, 2007, we should not necessarily conclude that these spreads were unusual and/or suspicious in nature. If, as the Journal alleges, the level of the Libor was manipulated downwards since January 2008 (i.e. 3 The effective rate is the weighted average of rates of actual exchange between banks. 4 Future researchers may wish to search for other structural breaks, less significant than these two breaks, during

the period of analysis. Any such additional breaks, though, fall outside of the scope of this study.

11

during period 2), the spreads of Libor over one or more of these other benchmark rates would have been significantly or unusually low. To test for this effect, we must form an estimate of what the Libor would have been “but for” this alleged manipulation. The Federal Funds Effective (FFE) rate is the interest rate at which banks (and other depository institutions) lend balances through the Federal Reserve Bank to other depository institutions. Because this rate is usually applied to overnight loans, it represents a short term rate of borrowing between banks, making it a suitable benchmark for our study.

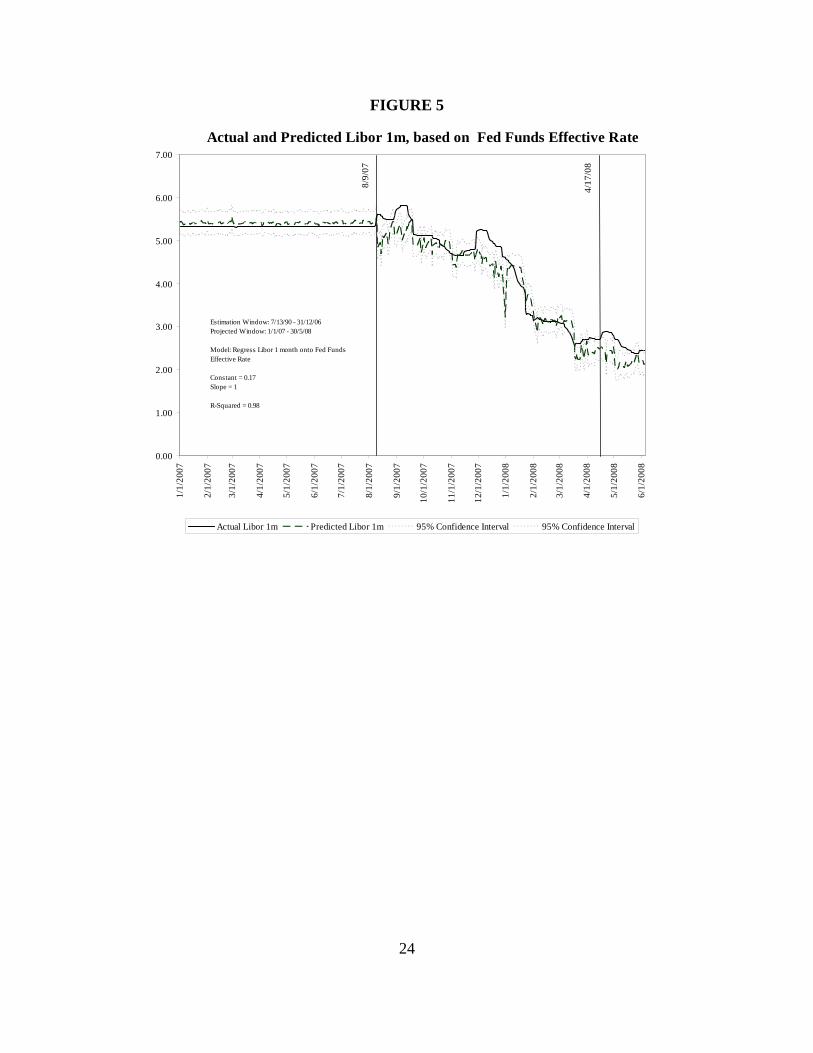

We first project the 1 month Libor on the FFE rate from 1990 through 2006. We then use this estimated relationship to predict what the 1 month Libor should have been, given the FFE rate for Periods 1, 2 and 3 as previously defined; our results are presented in Figure 5.

Clearly, the relationship between this Libor and the FFE is very strong during the

estimation period, a period covering two major cycles in the economy; thus, this rate should represent an effective “but-for” estimate of the Libor during the test period. However, the actual Libor rate is not statistically different from its predicted values in either Period 1, 2 or 3. In other words, the empirical evidence is not consistent with the supposition that the level of Libor has been effectively manipulated downwards. Similar results were found when studying the 3 month Libor rate series.

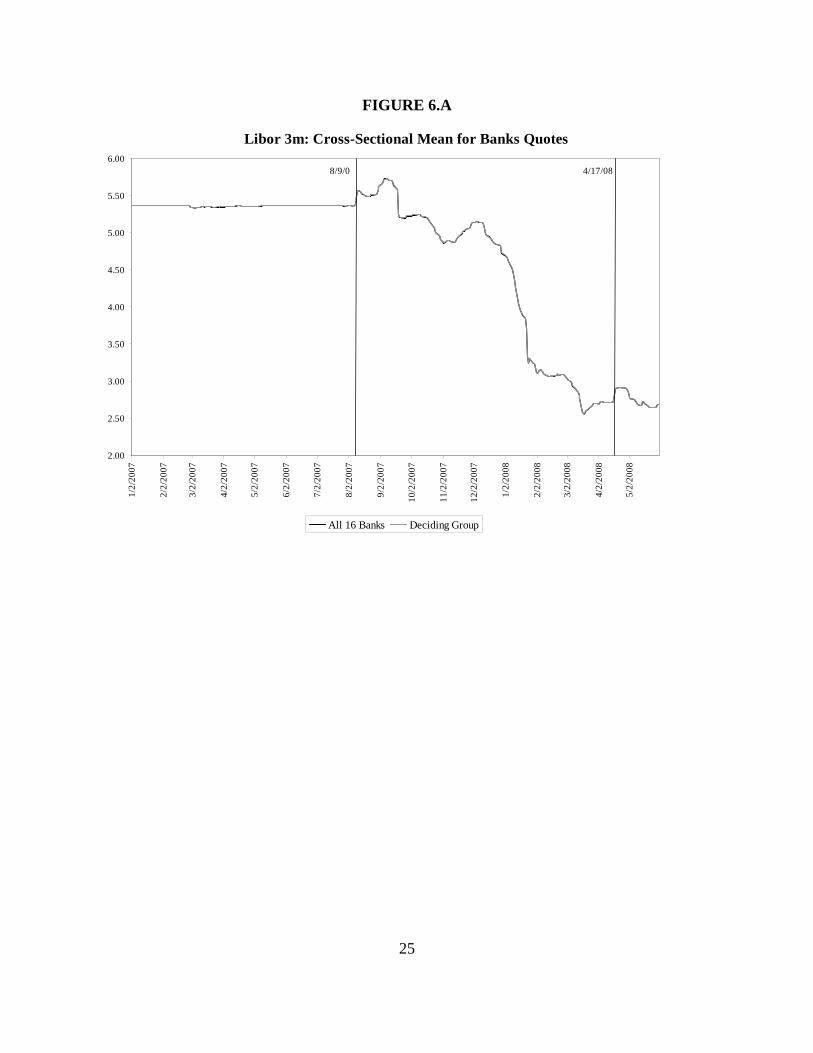

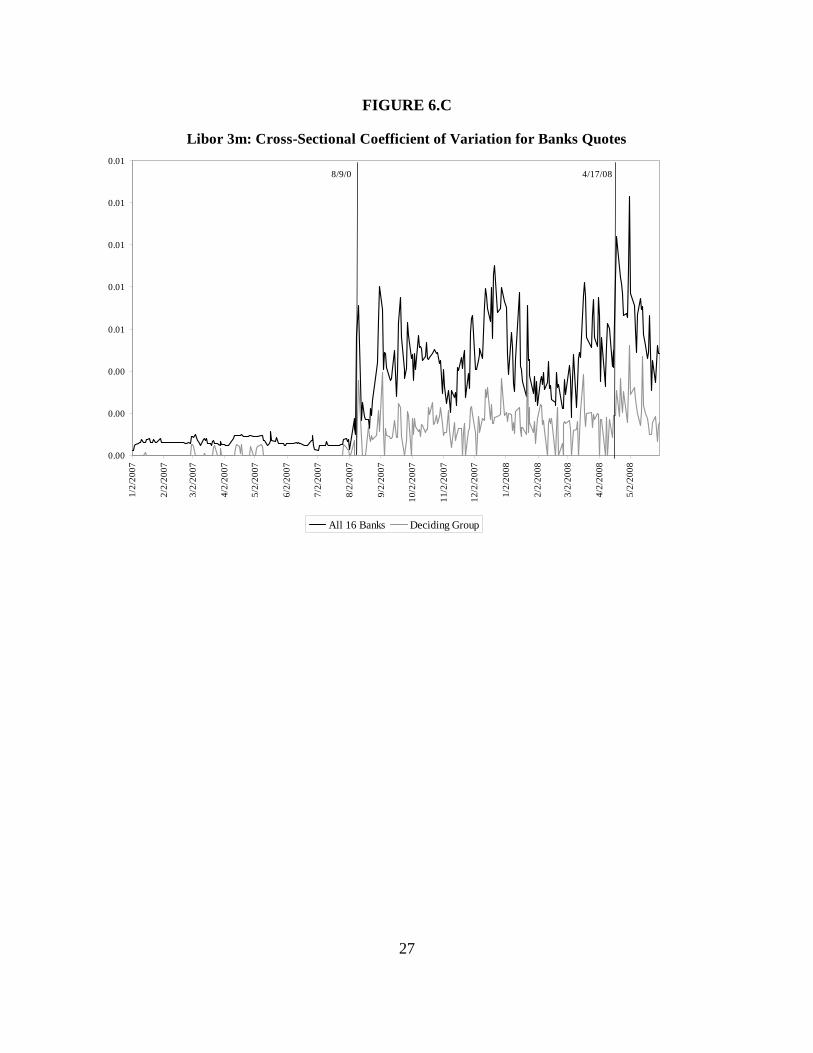

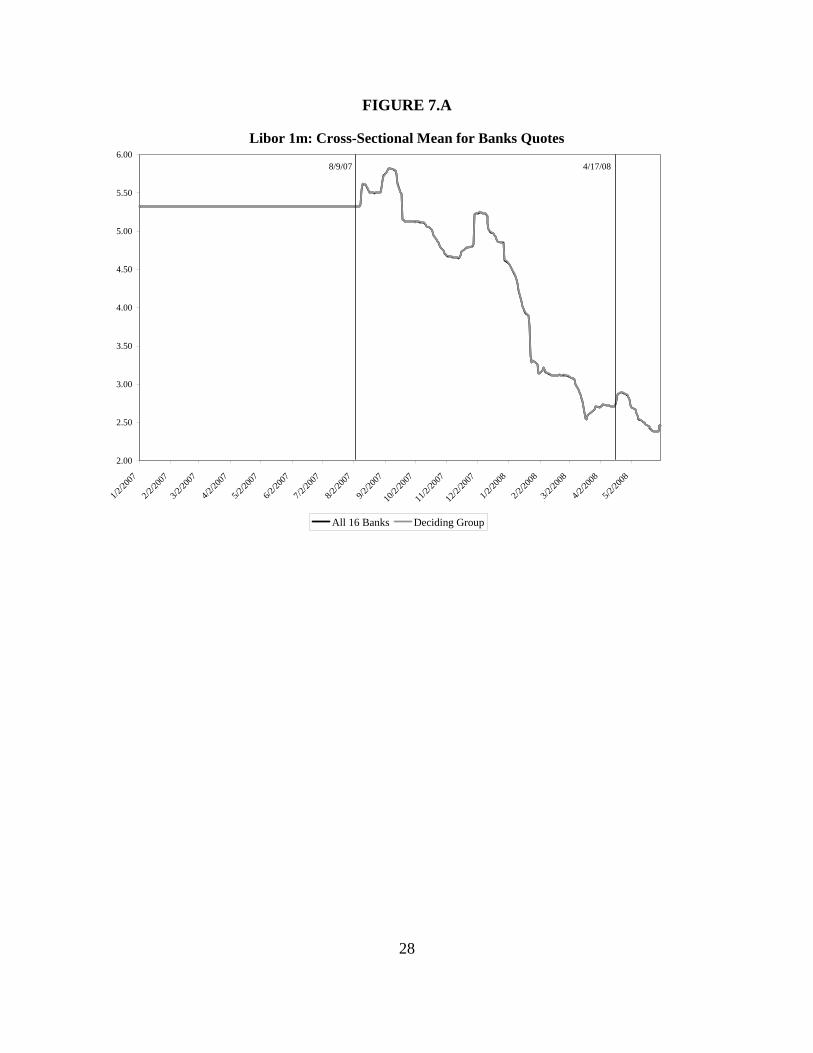

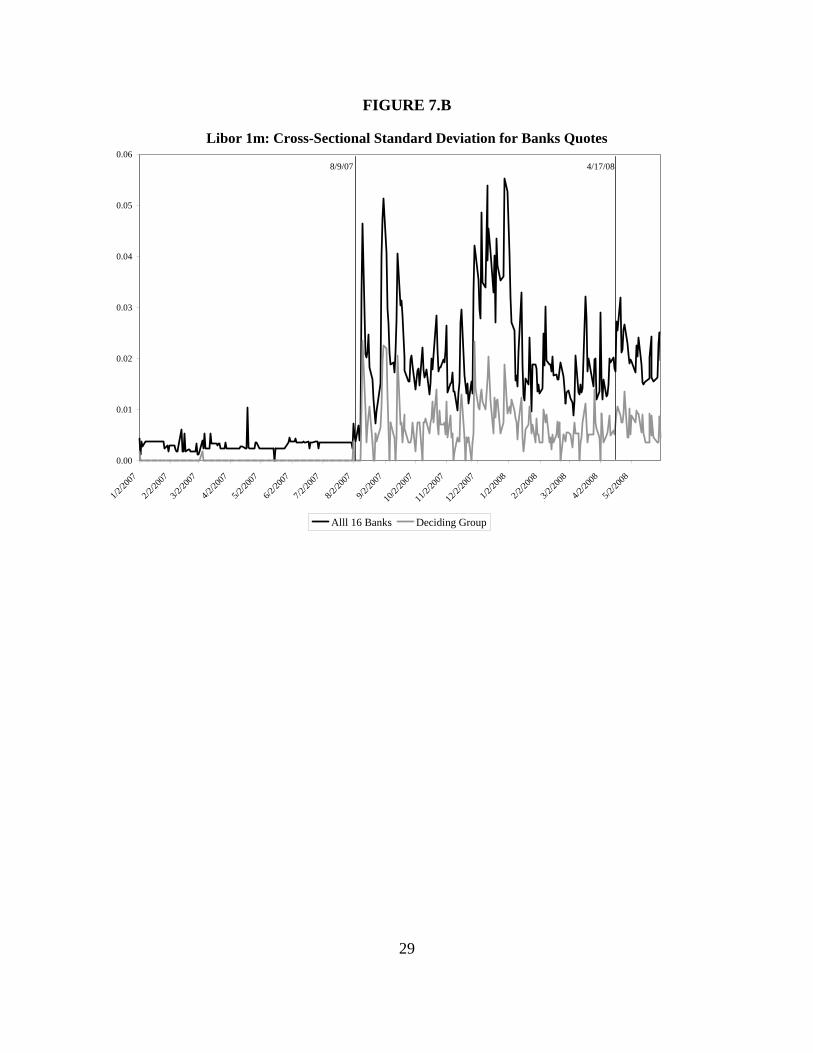

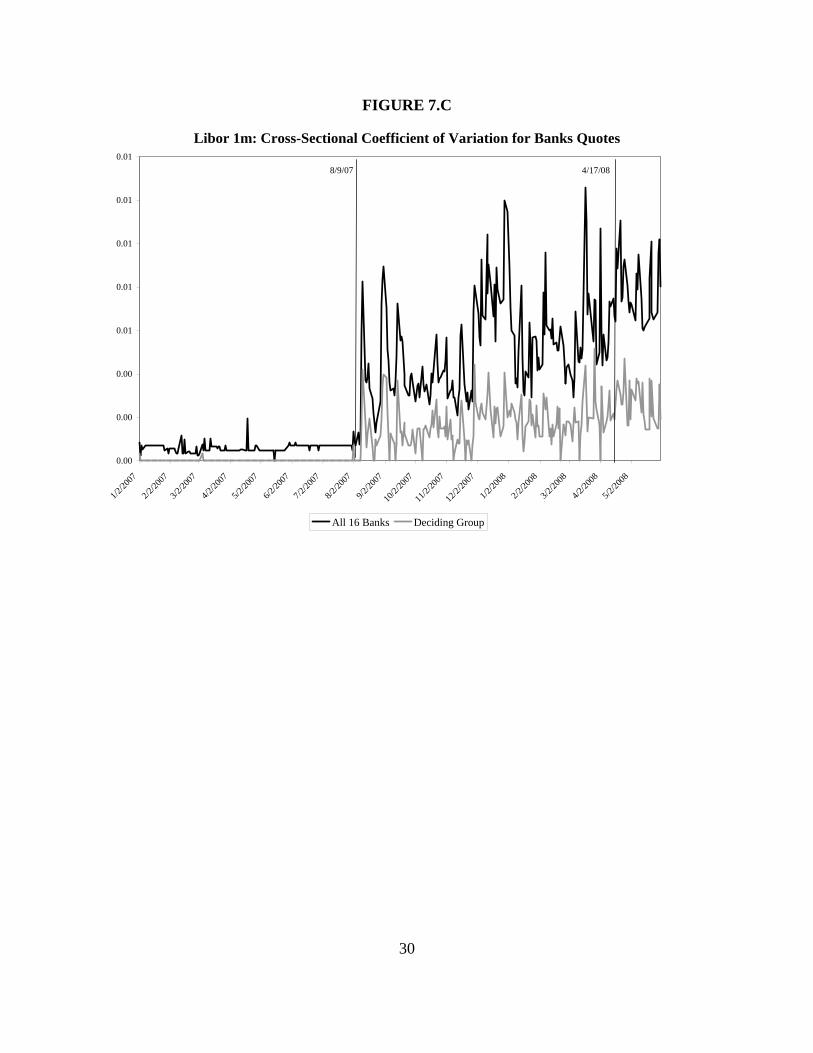

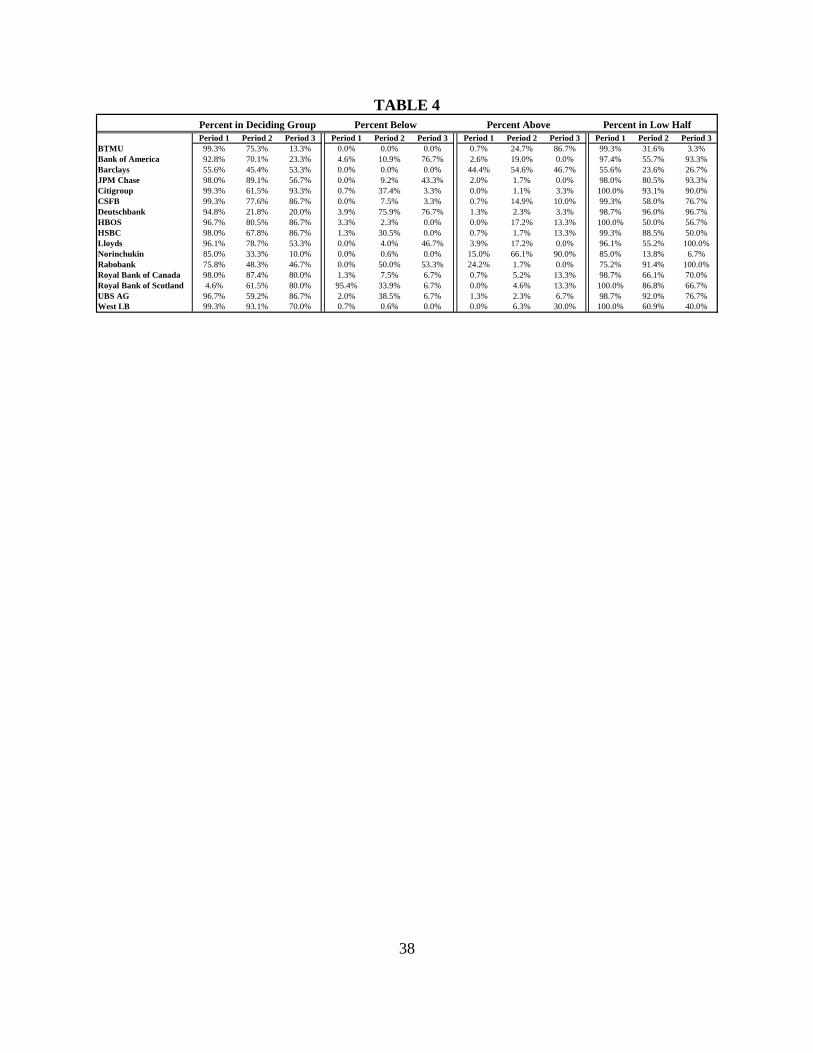

B. INDIVIDUAL BANK QUOTES According to the Journal (Mollenkamp and Whitehouse, 2008), the 16 banks may “have been low-balling their borrowing rates to avoid looking desperate for cash.” However, the Journal did not present an analysis of the type we conducted above (i.e. an examination of the level of the Libor against a suitable “but-for” predictor), but instead examined patterns among the individual bank quotes. In particular, the Journal noted that the intraday variances for the bank quotes was unusually small as compared to the intraday means since January 2008, and suggested that this is evidence of a pattern of manipulation. They also investigated the credit default swap (CDS) market and developed estimates of the banks' individual Libor quotes, given a “but for” condition that rates were not manipulated. In this section, we extend the Journal’s analysis of individual quotes by reviewing 2007 data, by investigating CDS spreads for each bank, and by studying other potentially relevant indicators. Figures 6.A, 6.B and 6.C show the cross-sectional means, the standard deviations, and the coefficients of variation of the individual 3 month Libor quotes, distinguishing the entire set of 16 banks from the “deciding group” of 8 which determines the actual Libor. Figures 7.A, 7.B and 7.C are analogous for the 1 month Libor. Once again, a structural break that begins on August 9, 2007 is evident. The intraday mean of the Libor (both 3 month and 1 month) is generally constant throughout Period 1. During Period 2, it briefly increases and then trends downward through the remainder of the period. Likewise, the intraday variance for these quotes significantly increases during Period 2. A similar pattern emerges for the intraday coefficients of variation as well.

12

It appears that the individual quotes were very compressed in Period 1 relative to the later

periods. In other words, if the data produced during Period 2 is believed to be evidence of manipulation, then Period 1 would appear to contain far greater manipulation as far back as January 2, 2007 and until August 8, 2007. Although it is not clear why the banks might have manipulated their quotes for such an extended period, the very low variability in the intraday quotes during Period 1 also appear anomalous. Nevertheless, we did not find any evidence that the level of the Libor significantly differed from what it “should have been,” given the FFE rate. The Libor is established as the simple average of the intermediate set of 8 quotes submitted by the 16 participating banks. In other words, the BBA ranks the quotes from 1st to 16th and then calculates the Libor as the average of the 5th through 12th quotes. It should be noted that, if several banks submit identical quotes, more than 8 banks may produce quotes that are tied for 5th place or 12th place; i.e. more than 8 banks on any given day may join the deciding group. Table 4 reports summary statistics on rates of inclusion in the deciding group by period. We report (a) how often each bank joined the deciding group, (b) how often each submitted a quote higher than the deciding set, (c) how often each submitted a lower quote, and (d) how often each submitted a quote that was less than or equal to the median quote on each day. During Period 1, a somewhat stunning result emerges: a vast majority of the banks join the deciding group more than 95% of the time, due to the significant number of identical quotes that were submitted; this resulted in the very low intraday variance mentioned above. In particular, BTMU, JPMChase, Citigroup, HSBC, West LB, Royal Bank of Canada and CSFB are in the deciding group on virtually each day. This nearly perfect participation rate is followed closely by a second group: HBOS, Lloyds, and UBS AG. This group is distantly followed by a single bank, Barclays, which participates about 50% of the time. The Royal Bank of Scotland participates least often, at a rate of approximately 5%. It would thus appear that the composition of the deciding group is relatively constant during Period 1, a period with many instances when more than 8 banks participate because of identical quote submissions. These patterns change significantly during Period 2. The composition of the deciding group becomes less stable. Although JPMChase and West LB continue to experience relatively high participation rates, they are significantly reduced from their rates in Period 1. Conversely, the participation rate of the Royal Bank of Scotland soars to approximately 60%, while the rate of Deutschbank plummets to approximately 21%.

These patterns change, once again, during Period 3. The participation rate of JPMChase declines significantly, while the rates of Citigroup and the Royal Banks of Canada and Scotland increase.

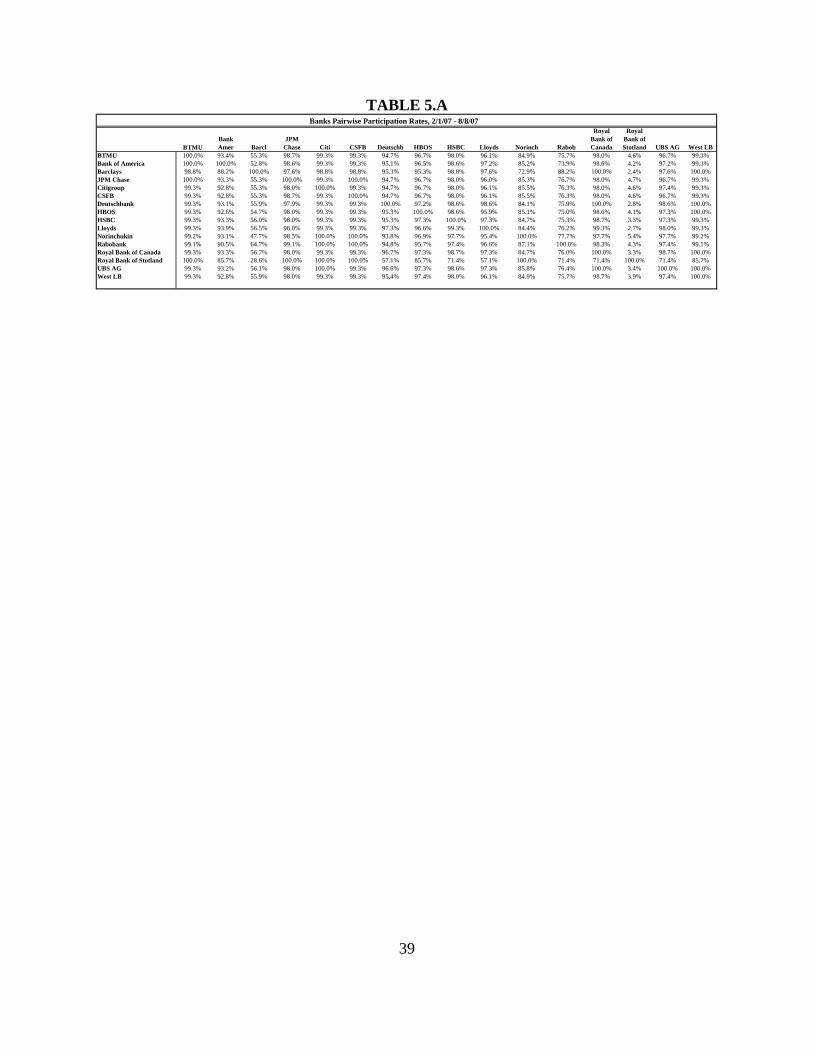

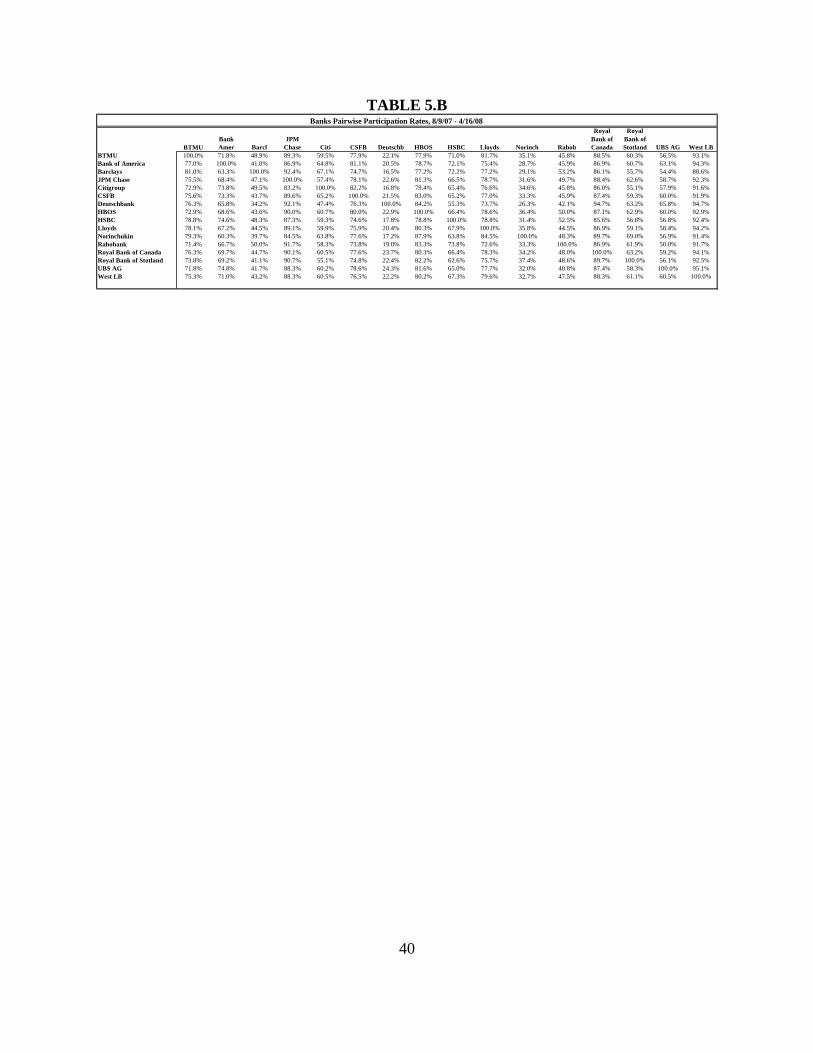

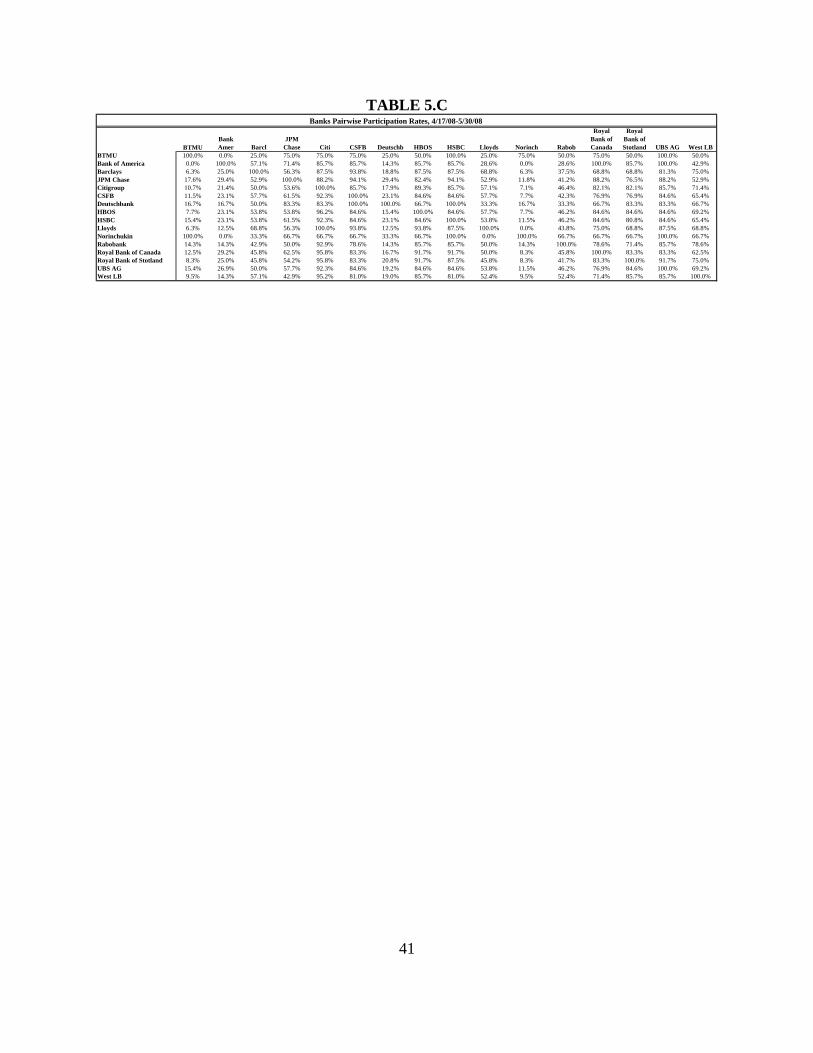

To test the stability of the deciding group in each Period, we now explore the joint (pairwise) inclusion of banks. In other words, for any given reference bank, we ask the question, “when this bank joins the deciding group, how often do each of the other banks join the group?”

13

The results are presented in Tables 5.A through 5.B. For example, when we report 93.4% in row “BTMU” and column “Bank America,” we

indicate that, when BTMU is in the deciding group, Bank of America joins the group 93.4% of the time. Note that this matrix is not symmetric; for instance, by reviewing the row “Bank of America” and column “BTMU,” we can note that each time Bank of America joined the group, BTMU did so as well. From these tables, we can identify groups of banks that tend to cluster together in each of the three periods in order to form the deciding group.

As expected, we see many joint inclusion rates in excess of 90% during Period 1, including several that exceed 99%. These rates fall significantly in Period 2, when we fail to see a single pairwise inclusion rate of 100%. Period 3, though, is more mixed; the average pairwise inclusion rate is evidently reduced in comparison to Period 1, but is greater in comparison to Period 2. It should be noted, though, that Period 3 contains significantly fewer days than Periods 1 or 2.

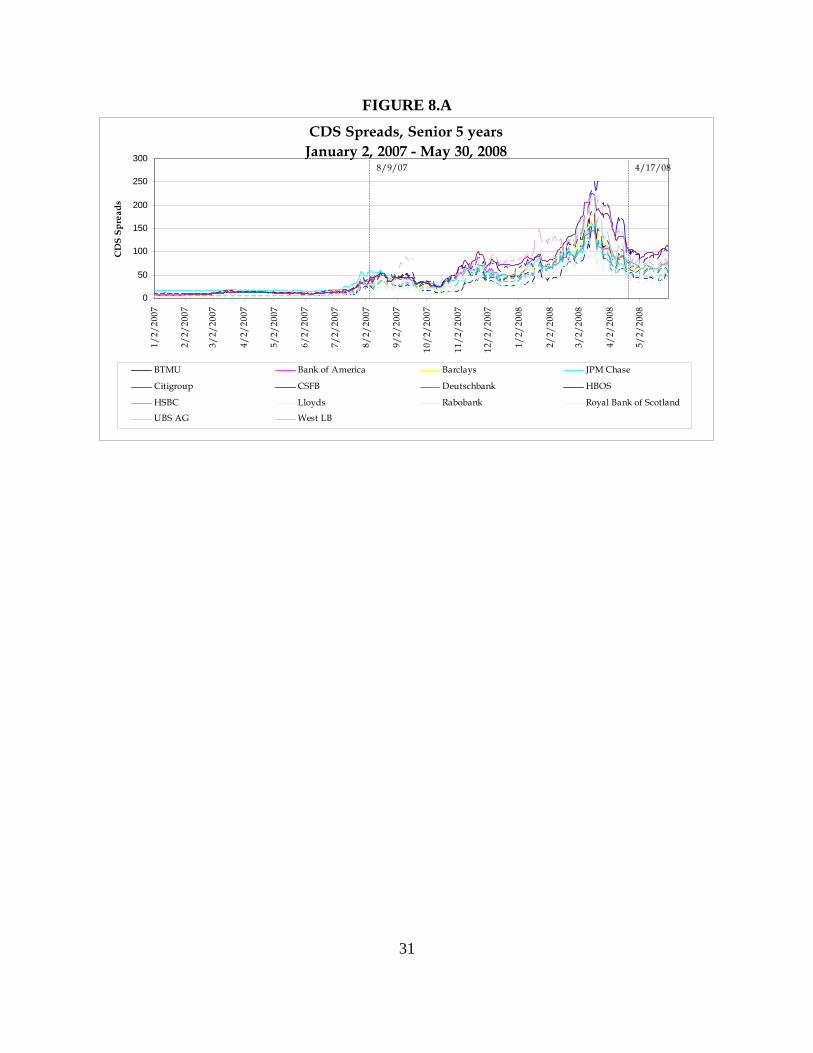

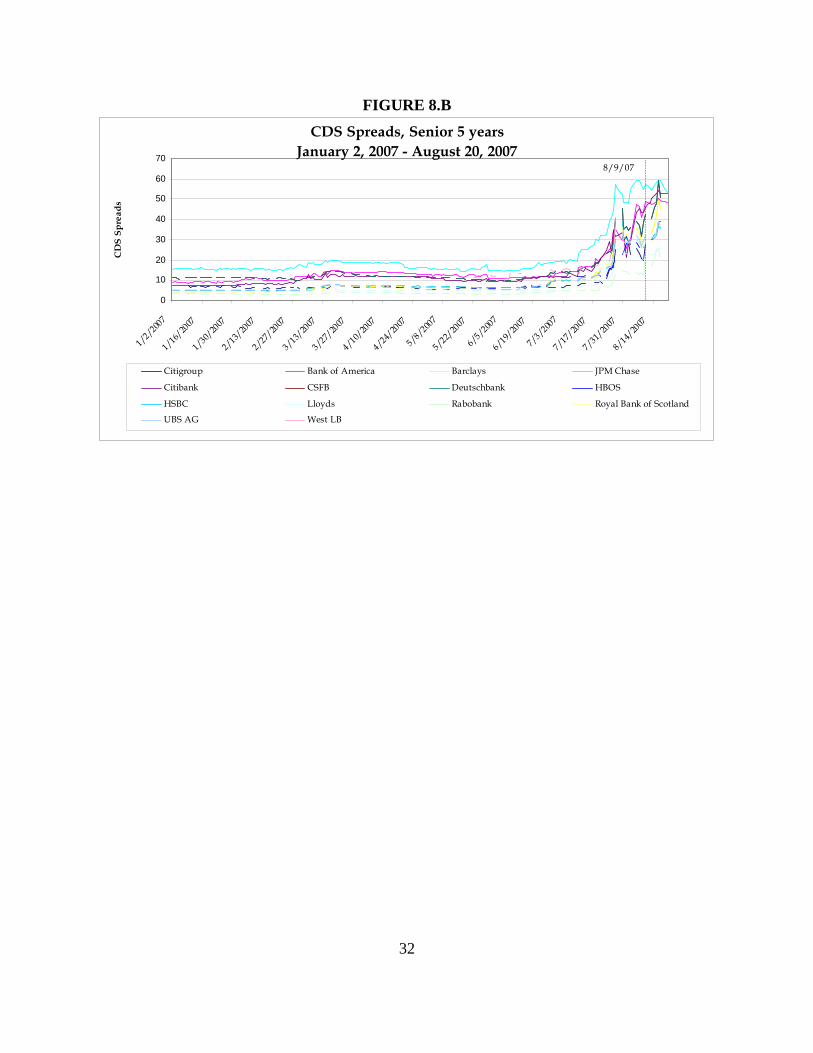

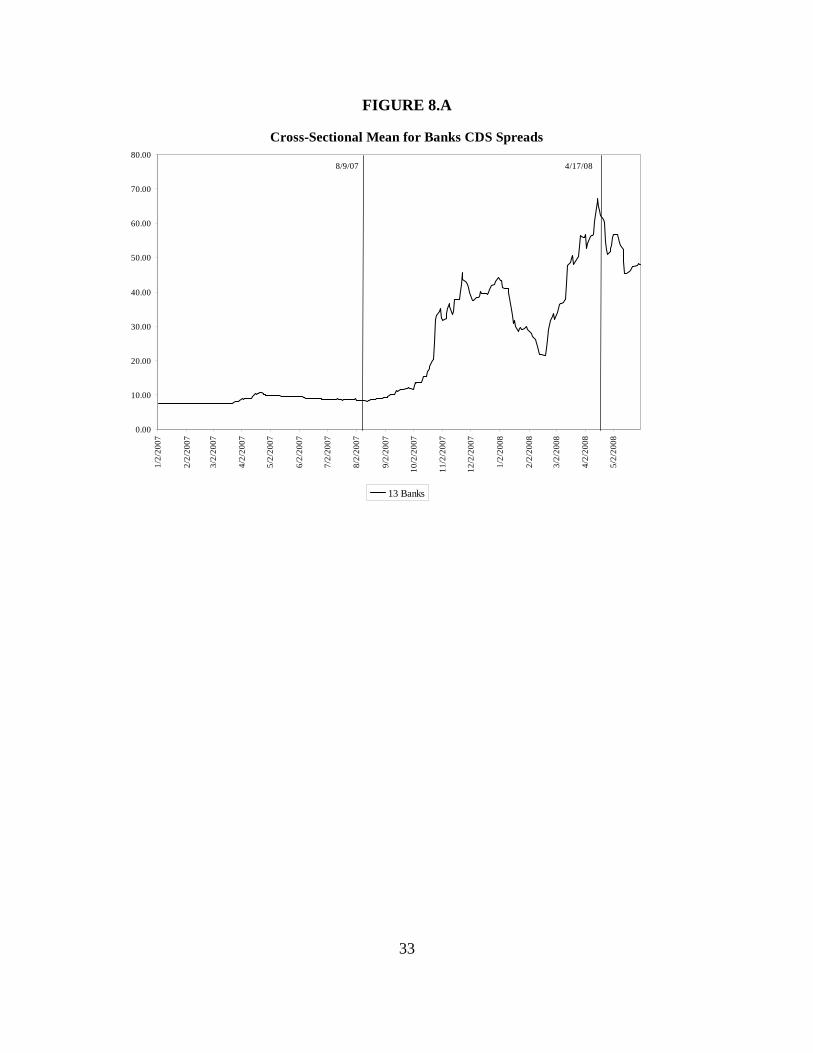

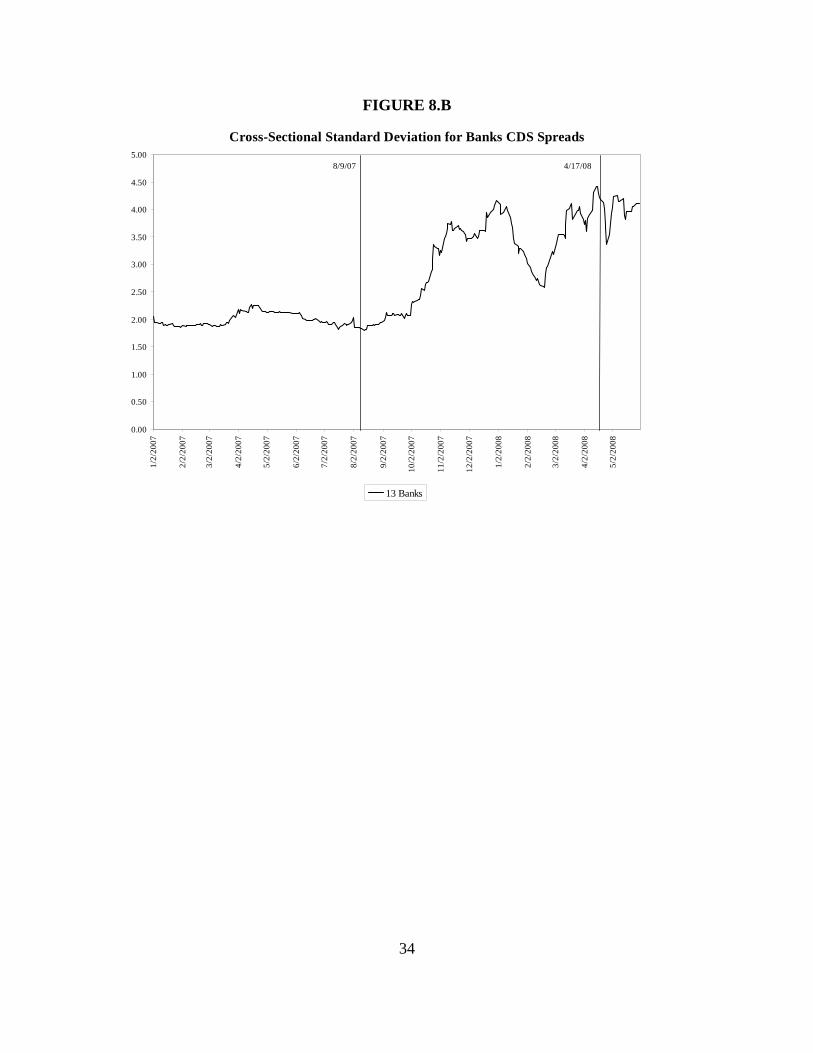

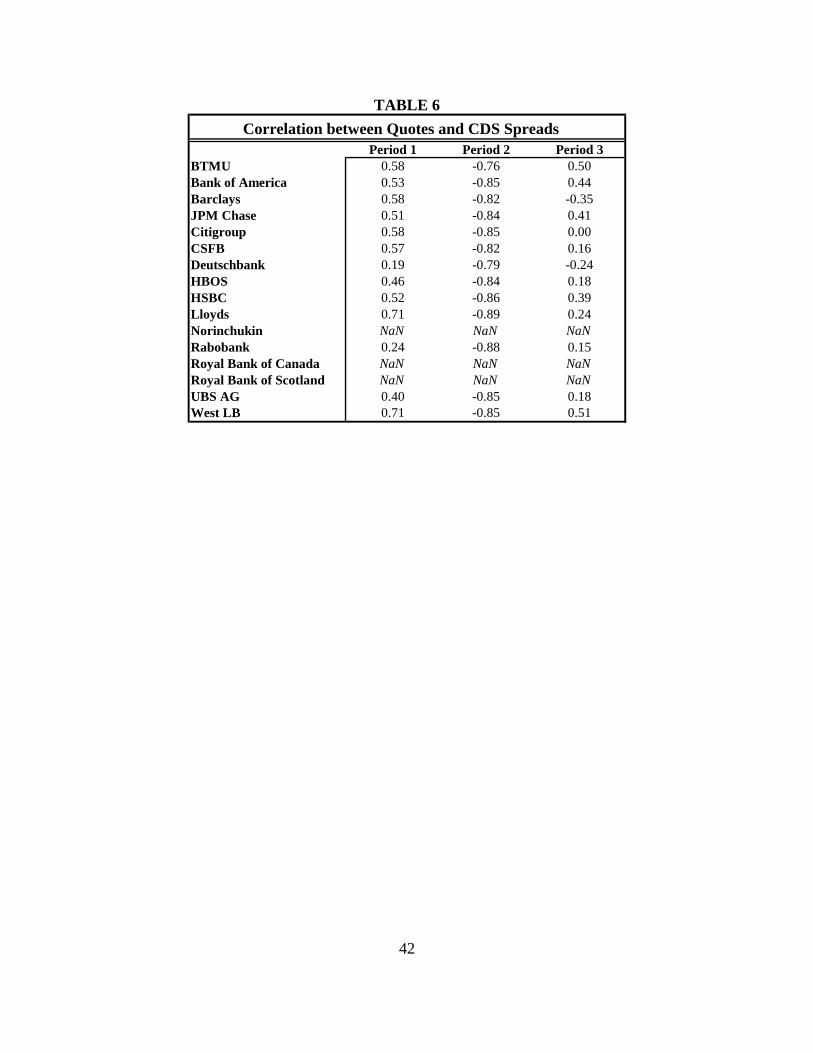

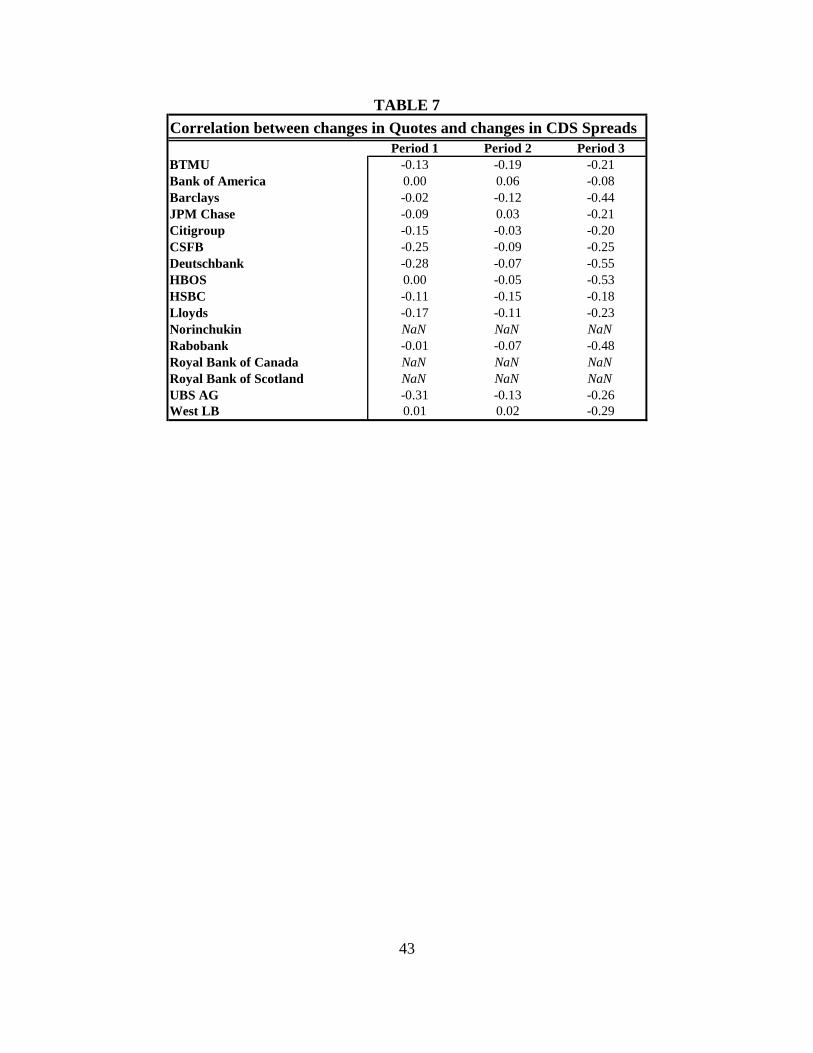

C. CONSISTENCY OF BANK QUOTES AND CDS SPREADS In this section of our analysis, we investigate the Journal's presumption that CDS spreads serve as effective benchmarks for assessing the reasonableness of Libor quote data. According to the Journal, the borrowing costs of banks are presumed to be a function of their perceived conditions of solvency and financial strength. The prices of CDS contracts are also presumed to be a function of financial strength and, according to the Journal, thus serve as a useful indicator of the cost of borrowing. Of course, there are many reasons why significant discrepancies may exist between CDS spreads and short-term borrowing costs. For instance, the time horizons of interest may be different, i.e. a creditor may believe that a bank is fully able to meet its obligations over the next 30 days and thus may lend to it at a low rate during that time, but (s)he may doubt its ability to meet its obligations over the next five years. The two parties may also possess different sensitivities to market risk, and thus may command different (and differently evolving) risk premia. In addition, if the CDS market is segmented, there may be additional (and evolving) liquidity premia associated with a CDS contract. These (and many other) observations notwithstanding, it is evident ceteris paribus that a “more risky” bank should have higher borrowing costs and CDS spreads than a “less risky” bank, though any specific results should be interpreted with these caveats in mind. Figure 8.A plots the CDS spreads from January 2007 onwards; Figure 8.B plots the same data only through August 2007 to illustrate Period 1 in more detail. Apparently, consistent with the trend of the Libor quotes, the spreads were much more compressed in Period 1 than in later periods. Furthermore, Figure 9.B presents the cross-sectional standard deviations. They are significantly greater in Periods 2 and 3 than in Period 1, a similar pattern to those found in the banks' intraday quotes. It should be noted, though, that the standard deviations of CDS spreads began to increase prior to August 9, 2007.

14

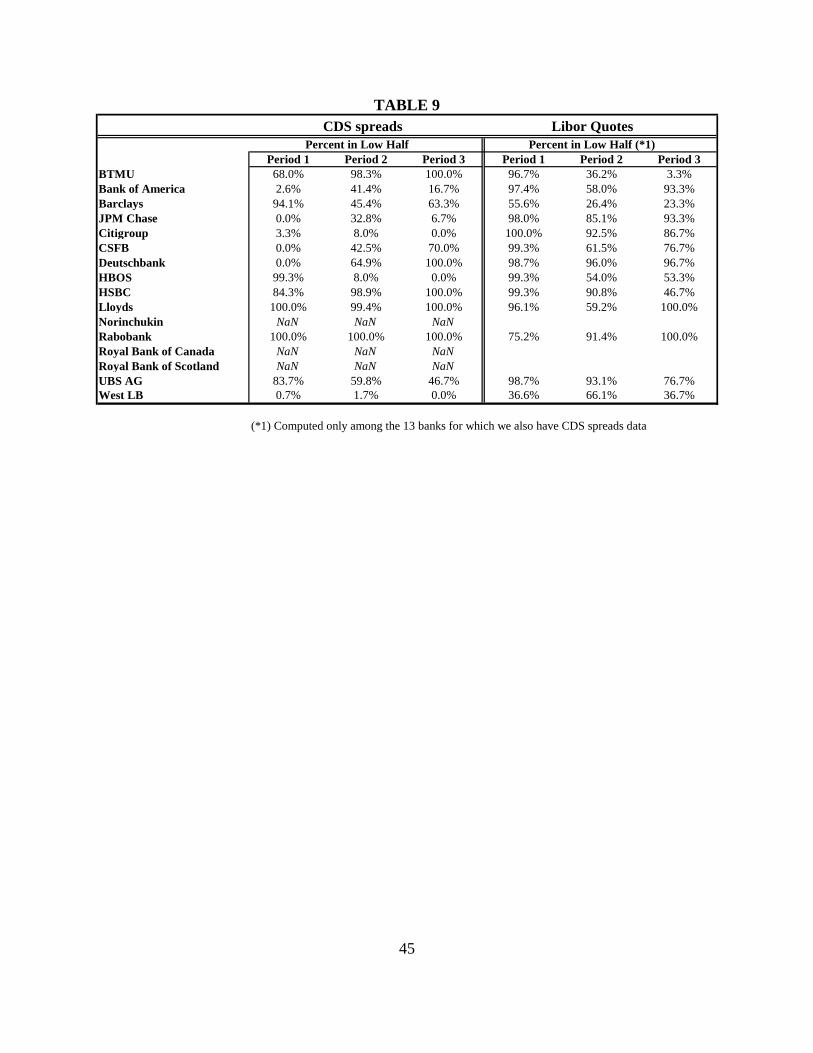

We also compare the ordinal content of the CDS spread data with the individual Libor

quotes. Specifically, we compare for each period (a) the percentage of time each bank’s CDS spread is less than or equal to the median spread, with (b) the percentage of time each bank's Libor quote is less than or equal to the median rate. Our results are presented in Table 9.

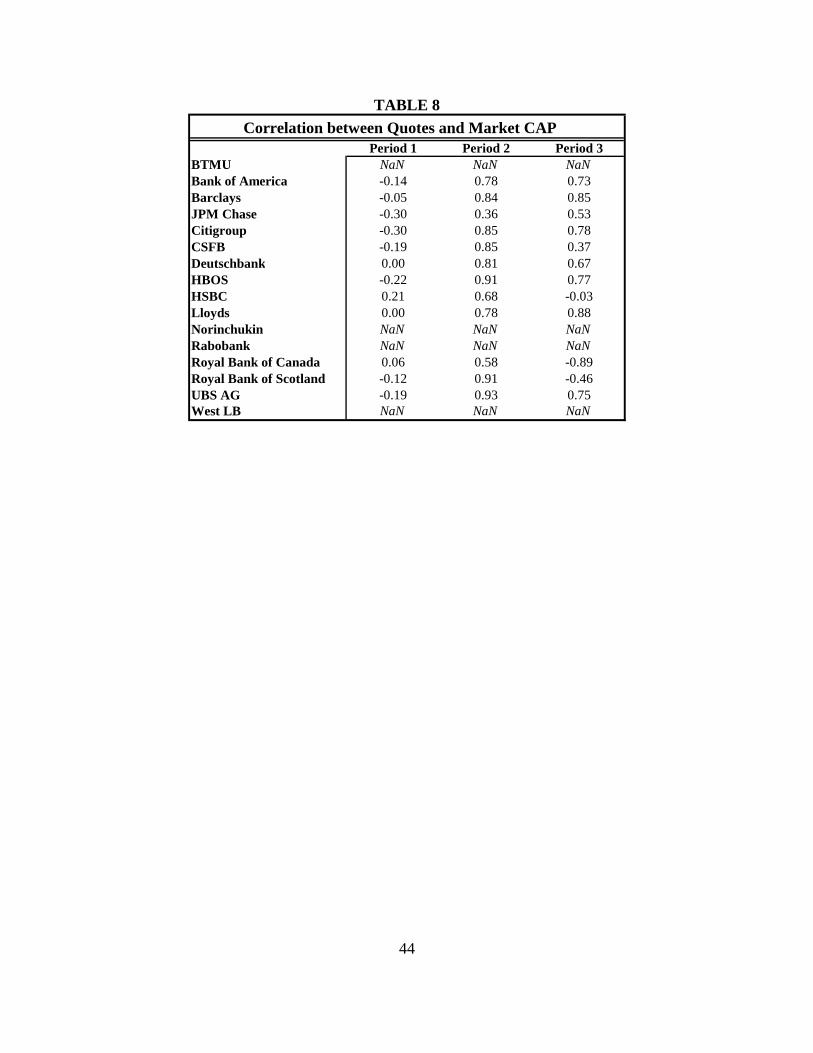

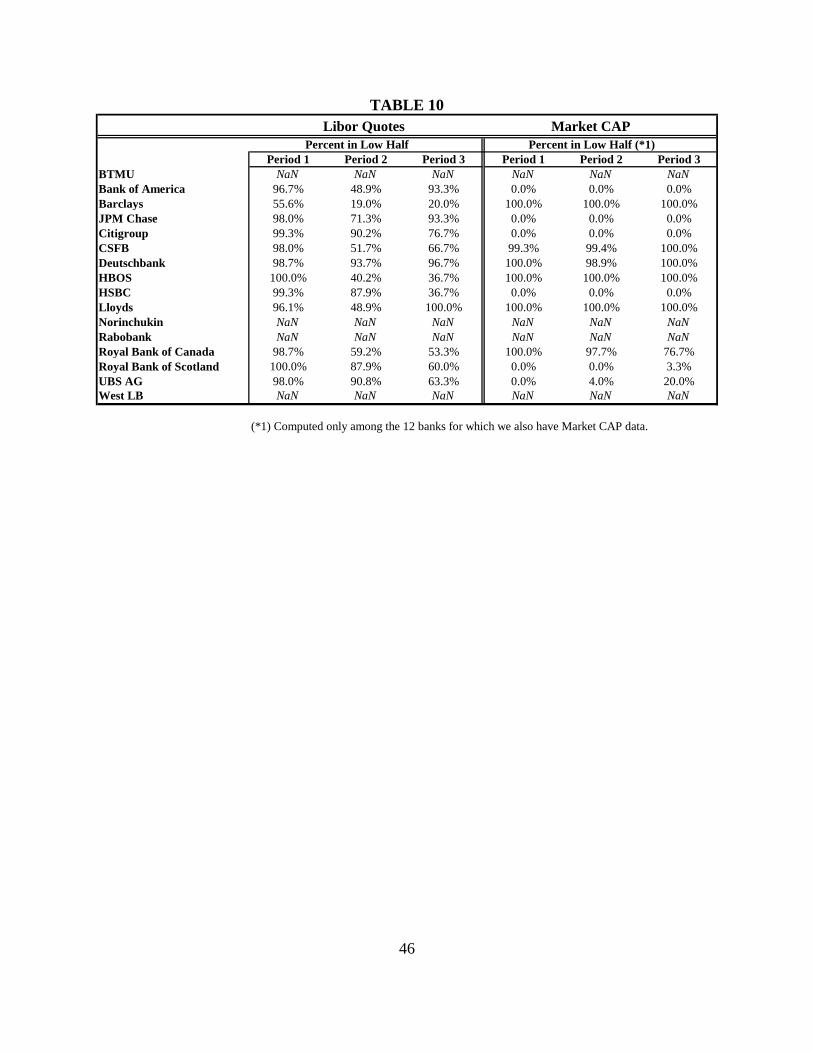

We are interested in “outliers,” defined as banks that consistently offered “low” Libor quotes while featuring “high” CDS spreads. During Period 1, JPMChase, CSFB, and Deutschbank meet this criterion; their Libor quotes were essentially always less than or equal to the median but their CDS spreads were never less than or equal the median. Bank of America is quite similar, with “low” Libor quotes 97% of the time but “low” CDS spreads only 2.6% of the time. Citigroup’s quotes were low 100% of the time, but its CDS spreads were low only 3.3% of the time.5 In sum, this cross-sectional analysis reveals that banks with low rate quotes do not necessarily enjoy low CDS spreads during Period 1. Similar examples continue during Period 2. For instance, the rate quotes of Citigroup and HBOS were low 93% and 54% of the time, respectively, but their CDS spreads were only low 8% of the time. The rate quotes of West LB were low 66.1% of the time, but its CDS spreads were only low 1.7% of the time. And the rate quotes of JPM Chase were low 85.1% of the time, but its CDS spreads were only low 32.8% of the time.6 Once again, similar examples continue during Period 3. These results suggest that either (a) CDS spreads are not effective ordinal indicators of borrowing costs, or (b) this sample of banks is unusual and atypical in some manner that is not easily identified. Although this issue falls beyond the scope of our analysis, it should be noted that many of the “outlier” banks are relatively large as defined by their market caps. In other words, as shown in Table 10, very large banks appear to have borrowing costs that are low in relation to their CDS spreads. For example, for Period 1, the low borrowing costs of JPMorgan and Citigroup provide a potential explanation for the disparities found when comparing their CDS spreads with their quotes. Why is this true? One explanation is that larger banks may be able to obtain “volume discounts” and thus may be able to borrow at lower rates than smaller banks. Other explanations, of course, are possible as well, and deserve additional study in future research work.

5 An exploratory analysis for West LB produced results that were consistent with (albeit less significant than) the

results that were generated by these other banks. The quotes produced by West LB were low 36.6% of the time, but its CDS spreads were only low 0.7% of the time.

6 Interestingly, BTMU served as an outlier on the “high side.” Its quotes were high 36.2% of the time, but its CDS spreads were low 98% of the time.

15

IV. CONCLUSIONS AND FUTURE WORK The analyses that were presented in this study screened for markers that are associated with the existence of conspiracies and manipulations in various industries. As previously noted, such markers may indeed occur in the absence of anticompetitive behavior; conversely, collusions and/or manipulations may occur in the absence of such markers. Nevertheless, although this study does not provide conclusive evidence of the existence of anti-competitive market behavior (or, for that matter, any effective manipulation of the Libor rate) on the part of the banks, we do present statistical evidence of patterns that appear to be inconsistent with those that are normally expected to occur under conditions of market competition for certain of the periods under study.

Interestingly, many of these markers were readily available for review by market analysts

on a contemporaneous basis. CDS spreads began to increase several months before the market entered Period 2, and yet individual rate quotes remained unchanged. Then, many of the bank quotes actually decreased while the spreads on a wide variety of instruments increased. Finally, when allegations of potential manipulation were published on April 17, these patterns shifted again.

There can always be alternative explanations for the presence of markers in competitive

markets; future research studies may choose to explore such explanations for these anomalies. For instance, commercial paper ratings and other alternative proxy measures of short term borrowing costs may prove to be more effective than CDS spreads for the group of banks studied within the designated time periods, and explain part of the behavior found. Stress measures, net borrowing or lending positions, and other observable characteristics may emerge to provide alternative explanations for trends in rate quotes and CDS spreads as well. In addition, event studies may identify further structural breaks in the statistical time line. All of these, and others, are recommended as subjects of future research.

16

FIGURE 1.A

Libor 3m, Fed Funds Effective Rate and Treasury-Bill 3m

0.00

2.00

4.00

6.00

8.00

10.00

12.007/

13/1

990

7/13

/199

1

7/13

/199

2

7/13

/199

3

7/13

/199

4

7/13

/199

5

7/13

/199

6

7/13

/199

7

7/13

/199

8

7/13

/199

9

7/13

/200

0

7/13

/200

1

7/13

/200

2

7/13

/200

3

7/13

/200

4

7/13

/200

5

7/13

/200

6

7/13

/200

7

Libor 3m Fed Funds Effective Treasury-Bill 3m

8/9/

07

4/17

/08

2/1/

07

17

FIGURE 1.B

Libor 3m, Fed Funds Effective Rate and Treasury-Bill 3m

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.001/

1/20

07

2/1/

2007

3/1/

2007

4/1/

2007

5/1/

2007

6/1/

2007

7/1/

2007

8/1/

2007

9/1/

2007

10/1

/200

7

11/1

/200

7

12/1

/200

7

1/1/

2008

2/1/

2008

3/1/

2008

4/1/

2008

5/1/

2008

6/1/

2008

Libor 3m Fed Funds Effective Treasury-Bill 3m

8/9/

07

4/17

/08

18

FIGURE 2.A

Libor 1m, Fed Funds Effective Rate and Treasury-Bill 1m

0.00

2.00

4.00

6.00

8.00

10.00

12.00

7/13

/199

0

7/13

/199

1

7/13

/199

2

7/13

/199

3

7/13

/199

4

7/13

/199

5

7/13

/199

6

7/13

/199

7

7/13

/199

8

7/13

/199

9

7/13

/200

0

7/13

/200

1

7/13

/200

2

7/13

/200

3

7/13

/200

4

7/13

/200

5

7/13

/200

6

7/13

/200

7

Libor 1m Fed Funds Effective Treasury-Bill 1m

8/9/

07

4/17

/08

2/1/

07

19

FIGURE 2.B

Libor 1m, Fed Funds Effective Rate and Treasury-Bill 1m

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.001/

1/20

07

2/1/

2007

3/1/

2007

4/1/

2007

5/1/

2007

6/1/

2007

7/1/

2007

8/1/

2007

9/1/

2007

10/1

/200

7

11/1

/200

7

12/1

/200

7

1/1/

2008

2/1/

2008

3/1/

2008

4/1/

2008

5/1/

2008

6/1/

2008

Libor 1m Fed Funds Effective Treasury-Bill 1m

8/9/

07

4/17

/08

20

FIGURE 3.A

Spread: LIBOR 3m over Treasury-Bill 3m

0.00

0.50

1.00

1.50

2.00

2.50

1/1/20

07

2/1/20

07

3/1/20

07

4/1/20

07

5/1/20

07

6/1/20

07

7/1/20

07

8/1/20

07

9/1/20

07

10/1/

2007

11/1/

2007

12/1/

2007

1/1/20

08

2/1/20

08

3/1/20

08

4/1/20

08

5/1/20

08

6/1/20

08

8/9/07 4/17/08

21

FIGURE 3.B

Spread: LIBOR 3m over Fed Funds Effective Rate

-0.50

0.00

0.50

1.00

1.50

2.00

1/1/

2007

2/1/

2007

3/1/

2007

4/1/

2007

5/1/

2007

6/1/

2007

7/1/

2007

8/1/

2007

9/1/

2007

10/1

/200

7

11/1

/200

7

12/1

/200

7

1/1/

2008

2/1/

2008

3/1/

2008

4/1/

2008

5/1/

2008

6/1/

2008

8/9/07 4/17/08

22

FIGURE 4.A

Spread: LIBOR 1m over Treasury-Bill 1m

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

1/1/20

07

2/1/20

07

3/1/20

07

4/1/20

07

5/1/20

07

6/1/20

07

7/1/20

07

8/1/20

07

9/1/20

07

10/1/

2007

11/1/

2007

12/1/

2007

1/1/20

08

2/1/20

08

3/1/20

08

4/1/20

08

5/1/20

08

6/1/20

08

8/9/07 4/17/08

23

FIGURE 4.B

Spread: LIBOR 1m over Fed Funds Effective Rate

-0.50

0.00

0.50

1.00

1.50

2.00

1/1/

2007

2/1/

2007

3/1/

2007

4/1/

2007

5/1/

2007

6/1/

2007

7/1/

2007

8/1/

2007

9/1/

2007

10/1

/200

7

11/1

/200

7

12/1

/200

7

1/1/

2008

2/1/

2008

3/1/

2008

4/1/

2008

5/1/

2008

6/1/

2008

8/9/07 4/17/08

24

FIGURE 5

Actual and Predicted Libor 1m, based on Fed Funds Effective Rate

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

1/1/

2007

2/1/

2007

3/1/

2007

4/1/

2007

5/1/

2007

6/1/

2007

7/1/

2007

8/1/

2007

9/1/

2007

10/1

/200

7

11/1

/200

7

12/1

/200

7

1/1/

2008

2/1/

2008

3/1/

2008

4/1/

2008

5/1/

2008

6/1/

2008

Actual Libor 1m Predicted Libor 1m 95% Confidence Interval 95% Confidence Interval

8/9/

07

4/17

/08

Estimation Window: 7/13/90 - 31/12/06 Projected Window: 1/1/07 - 30/5/08

Model: Regress Libor 1 month onto Fed Funds Effective Rate

Constant = 0.17Slope = 1

R-Squared = 0.98

25

FIGURE 6.A

Libor 3m: Cross-Sectional Mean for Banks Quotes

2.00

2.50

3.00

3.50

4.00

4.50

5.00

5.50

6.00

1/2/

2007

2/2/

2007

3/2/

2007

4/2/

2007

5/2/

2007

6/2/

2007

7/2/

2007

8/2/

2007

9/2/

2007

10/2

/200

7

11/2

/200

7

12/2

/200

7

1/2/

2008

2/2/

2008

3/2/

2008

4/2/

2008

5/2/

2008

All 16 Banks Deciding Group

8/9/0 4/17/08

26

FIGURE 6.B

Libor 3m: Cross-Sectional Standard Deviation for Banks Quotes

0.00

0.01

0.01

0.02

0.02

0.03

0.03

0.04

0.04

0.05

0.05

1/2/

2007

2/2/

2007

3/2/

2007

4/2/

2007

5/2/

2007

6/2/

2007

7/2/

2007

8/2/

2007

9/2/

2007

10/2

/200

7

11/2

/200

7

12/2

/200

7

1/2/

2008

2/2/

2008

3/2/

2008

4/2/

2008

5/2/

2008

Alll 16 Banks Deciding Group

8/9/0 4/17/08

27

FIGURE 6.C

Libor 3m: Cross-Sectional Coefficient of Variation for Banks Quotes

0.00

0.00

0.00

0.01

0.01

0.01

0.01

0.01

1/2/

2007

2/2/

2007

3/2/

2007

4/2/

2007

5/2/

2007

6/2/

2007

7/2/

2007

8/2/

2007

9/2/

2007

10/2

/200

7

11/2

/200

7

12/2

/200

7

1/2/

2008

2/2/

2008

3/2/

2008

4/2/

2008

5/2/

2008

All 16 Banks Deciding Group

8/9/0 4/17/08

28

FIGURE 7.A

Libor 1m: Cross-Sectional Mean for Banks Quotes

2.00

2.50

3.00

3.50

4.00

4.50

5.00

5.50

6.00

1/2/20

07

2/2/20

07

3/2/20

07

4/2/20

07

5/2/20

07

6/2/20

07

7/2/20

07

8/2/20

07

9/2/20

07

10/2/

2007

11/2/

2007

12/2/

2007

1/2/20

08

2/2/20

08

3/2/20

08

4/2/20

08

5/2/20

08

All 16 Banks Deciding Group

8/9/07 4/17/08

29

FIGURE 7.B

Libor 1m: Cross-Sectional Standard Deviation for Banks Quotes

0.00

0.01

0.02

0.03

0.04

0.05

0.06

1/2/20

07

2/2/20

07

3/2/20

07

4/2/20

07

5/2/20

07

6/2/20

07

7/2/20

07

8/2/20

07

9/2/20

07

10/2/

2007

11/2/

2007

12/2/

2007

1/2/20

08

2/2/20

08

3/2/20

08

4/2/20

08

5/2/20

08

Alll 16 Banks Deciding Group

8/9/07 4/17/08

30

FIGURE 7.C

Libor 1m: Cross-Sectional Coefficient of Variation for Banks Quotes

0.00

0.00

0.00

0.01

0.01

0.01

0.01

0.01

1/2/20

07

2/2/20

07

3/2/20

07

4/2/20

07

5/2/20

07

6/2/20

07

7/2/20

07

8/2/20

07

9/2/20

07

10/2/

2007

11/2/

2007

12/2/

2007

1/2/20

08

2/2/20

08

3/2/20

08

4/2/20

08

5/2/20

08

All 16 Banks Deciding Group

8/9/07 4/17/08

31

FIGURE 8.A

CDS Spreads, Senior 5 years January 2, 2007 - May 30, 2008

0

50

100

150

200

250

3001/

2/20

07

2/2/

2007

3/2/

2007

4/2/

2007

5/2/

2007

6/2/

2007

7/2/

2007

8/2/

2007

9/2/

2007

10/2

/200

7

11/2

/200

7

12/2

/200

7

1/2/

2008

2/2/

2008

3/2/

2008

4/2/

2008

5/2/

2008

CD

S Sp

read

s

BTMU Bank of America Barclays JPM Chase

Citigroup CSFB Deutschbank HBOS

HSBC Lloyds Rabobank Royal Bank of Scotland

UBS AG West LB

8/9/07 4/17/08

32

FIGURE 8.B

CDS Spreads, Senior 5 years January 2, 2007 - August 20, 2007

0

10

20

30

40

50

60

70

1/2/2007

1/16/20

07

1/30/20

07

2/13/20

07

2/27/20

07

3/13/20

07

3/27/20

07

4/10/20

07

4/24/20

07

5/8/2007

5/22/20

07

6/5/2007

6/19/20

07

7/3/2007

7/17/20

07

7/31/20

07

8/14/20

07

CD

S Sp

read

s

Citigroup Bank of America Barclays JPM Chase

Citibank CSFB Deutschbank HBOS

HSBC Lloyds Rabobank Royal Bank of Scotland

UBS AG West LB

8/9/07

33

FIGURE 8.A

Cross-Sectional Mean for Banks CDS Spreads

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.001/

2/20

07

2/2/

2007

3/2/

2007

4/2/

2007

5/2/

2007

6/2/

2007

7/2/

2007

8/2/

2007

9/2/

2007

10/2

/200

7

11/2

/200

7

12/2

/200

7

1/2/

2008

2/2/

2008

3/2/

2008

4/2/

2008

5/2/

2008

13 Banks

8/9/07 4/17/08

34

FIGURE 8.B

Cross-Sectional Standard Deviation for Banks CDS Spreads

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

5.001/

2/20

07

2/2/

2007

3/2/

2007

4/2/

2007

5/2/

2007

6/2/

2007

7/2/

2007

8/2/

2007

9/2/

2007

10/2

/200

7

11/2

/200

7

12/2

/200

7

1/2/

2008

2/2/

2008

3/2/

2008

4/2/

2008

5/2/

2008

13 Banks

8/9/07 4/17/08

35

TABLE 1 Time Periods

Period 1 January 2, 2007 - August 8, 2007Period 2 August 9, 2007 - April 16, 2008Period 3 April 17, 2008 - May 30, 2008

36

TABLE 2 Libor 3-Months

Treasury-Bill Spread Fed Funds Effective Rate SpreadMean Stand Deviation Coeff Variation Mean Stand Deviation Coeff Variation

Period 1 0.372 0.141 0.38 0.1 0.03 0.302

Period 2 1.382 0.371 0.269 0.373 0.306 0.819

Period 3 1.096 0.332 0.303 0.675 0.12 0.178

Libor 1-Month

Treasury-Bill Spread Fed Funds Effective Rate SpreadMean Stand Deviation Coeff Variation Mean Stand Deviation Coeff Variation

Period 1 0.395 0.243 0.616 0.064 0.03 0.469

Period 2 1.404 0.495 0.352 0.342 0.312 0.912

Period 3 1.069 0.642 0.6 0.532 0.165 0.31

37

TABLE 3 Statistical Tests on Changes in Spreads Means

Coeff T-Stat T-(robust) Coeff T-Stat T-(robust)Intercept 0.395 11.648 5.414 Intercept 0.372 16.026 33.225

8/9/07-4/16/08 1.009 21.738 12.157 8/9/07-4/16/08 1.010 31.734 33.9214/17/08-5/30/08 -0.335 -4.259 -1.429 4/17/08-5/30/08 -0.286 -5.297 -4.624

Coeff T-Stat T-(robust) Coeff T-Stat T-(robust)Intercept 0.064 3.573 24.724 Intercept 0.100 5.822 37.675

8/9/07-4/16/08 0.279 11.433 5.203 8/9/07-4/16/08 0.273 11.560 4.2974/17/08-5/30/08 0.189 4.577 2.699 4/17/08-5/30/08 0.302 7.545 4.460

Libor 1m over Tbill 1m

Li bor1m over FF-Eff

Libor 3m over Tbill 3m

Li bor 3m over FF-Eff

38

TABLE 4 Percent in Deciding Group Percent Below Percent Above Percent in Low Half

Period 1 Period 2 Period 3 Period 1 Period 2 Period 3 Period 1 Period 2 Period 3 Period 1 Period 2 Period 3BTMU 99.3% 75.3% 13.3% 0.0% 0.0% 0.0% 0.7% 24.7% 86.7% 99.3% 31.6% 3.3%Bank of America 92.8% 70.1% 23.3% 4.6% 10.9% 76.7% 2.6% 19.0% 0.0% 97.4% 55.7% 93.3%Barclays 55.6% 45.4% 53.3% 0.0% 0.0% 0.0% 44.4% 54.6% 46.7% 55.6% 23.6% 26.7%JPM Chase 98.0% 89.1% 56.7% 0.0% 9.2% 43.3% 2.0% 1.7% 0.0% 98.0% 80.5% 93.3%Citigroup 99.3% 61.5% 93.3% 0.7% 37.4% 3.3% 0.0% 1.1% 3.3% 100.0% 93.1% 90.0%CSFB 99.3% 77.6% 86.7% 0.0% 7.5% 3.3% 0.7% 14.9% 10.0% 99.3% 58.0% 76.7%Deutschbank 94.8% 21.8% 20.0% 3.9% 75.9% 76.7% 1.3% 2.3% 3.3% 98.7% 96.0% 96.7%HBOS 96.7% 80.5% 86.7% 3.3% 2.3% 0.0% 0.0% 17.2% 13.3% 100.0% 50.0% 56.7%HSBC 98.0% 67.8% 86.7% 1.3% 30.5% 0.0% 0.7% 1.7% 13.3% 99.3% 88.5% 50.0%Lloyds 96.1% 78.7% 53.3% 0.0% 4.0% 46.7% 3.9% 17.2% 0.0% 96.1% 55.2% 100.0%Norinchukin 85.0% 33.3% 10.0% 0.0% 0.6% 0.0% 15.0% 66.1% 90.0% 85.0% 13.8% 6.7%Rabobank 75.8% 48.3% 46.7% 0.0% 50.0% 53.3% 24.2% 1.7% 0.0% 75.2% 91.4% 100.0%Royal Bank of Canada 98.0% 87.4% 80.0% 1.3% 7.5% 6.7% 0.7% 5.2% 13.3% 98.7% 66.1% 70.0%Royal Bank of Scotland 4.6% 61.5% 80.0% 95.4% 33.9% 6.7% 0.0% 4.6% 13.3% 100.0% 86.8% 66.7%UBS AG 96.7% 59.2% 86.7% 2.0% 38.5% 6.7% 1.3% 2.3% 6.7% 98.7% 92.0% 76.7%West LB 99.3% 93.1% 70.0% 0.7% 0.6% 0.0% 0.0% 6.3% 30.0% 100.0% 60.9% 40.0%

39

TABLE 5.A Banks Pairwise Participation Rates, 2/1/07 - 8/8/07

BTMUBank Amer Barcl

JPM Chase Citi CSFB Deutschb HBOS HSBC Lloyds Norinch Rabob

Royal Bank of Canada

Royal Bank of Stotland UBS AG West LB

BTMU 100.0% 93.4% 55.3% 98.7% 99.3% 99.3% 94.7% 96.7% 98.0% 96.1% 84.9% 75.7% 98.0% 4.6% 96.7% 99.3%Bank of America 100.0% 100.0% 52.8% 98.6% 99.3% 99.3% 95.1% 96.5% 98.6% 97.2% 85.2% 73.9% 98.6% 4.2% 97.2% 99.3%Barclays 98.8% 88.2% 100.0% 97.6% 98.8% 98.8% 95.3% 95.3% 98.8% 97.6% 72.9% 88.2% 100.0% 2.4% 97.6% 100.0%JPM Chase 100.0% 93.3% 55.3% 100.0% 99.3% 100.0% 94.7% 96.7% 98.0% 96.0% 85.3% 76.7% 98.0% 4.7% 96.7% 99.3%Citigroup 99.3% 92.8% 55.3% 98.0% 100.0% 99.3% 94.7% 96.7% 98.0% 96.1% 85.5% 76.3% 98.0% 4.6% 97.4% 99.3%CSFB 99.3% 92.8% 55.3% 98.7% 99.3% 100.0% 94.7% 96.7% 98.0% 96.1% 85.5% 76.3% 98.0% 4.6% 96.7% 99.3%Deutschbank 99.3% 93.1% 55.9% 97.9% 99.3% 99.3% 100.0% 97.2% 98.6% 98.6% 84.1% 75.9% 100.0% 2.8% 98.6% 100.0%HBOS 99.3% 92.6% 54.7% 98.0% 99.3% 99.3% 95.3% 100.0% 98.6% 95.9% 85.1% 75.0% 98.6% 4.1% 97.3% 100.0%HSBC 99.3% 93.3% 56.0% 98.0% 99.3% 99.3% 95.3% 97.3% 100.0% 97.3% 84.7% 75.3% 98.7% 3.3% 97.3% 99.3%Lloyds 99.3% 93.9% 56.5% 98.0% 99.3% 99.3% 97.3% 96.6% 99.3% 100.0% 84.4% 76.2% 99.3% 2.7% 98.0% 99.3%Norinchukin 99.2% 93.1% 47.7% 98.5% 100.0% 100.0% 93.8% 96.9% 97.7% 95.4% 100.0% 77.7% 97.7% 5.4% 97.7% 99.2%Rabobank 99.1% 90.5% 64.7% 99.1% 100.0% 100.0% 94.8% 95.7% 97.4% 96.6% 87.1% 100.0% 98.3% 4.3% 97.4% 99.1%Royal Bank of Canada 99.3% 93.3% 56.7% 98.0% 99.3% 99.3% 96.7% 97.3% 98.7% 97.3% 84.7% 76.0% 100.0% 3.3% 98.7% 100.0%Royal Bank of Stotland 100.0% 85.7% 28.6% 100.0% 100.0% 100.0% 57.1% 85.7% 71.4% 57.1% 100.0% 71.4% 71.4% 100.0% 71.4% 85.7%UBS AG 99.3% 93.2% 56.1% 98.0% 100.0% 99.3% 96.6% 97.3% 98.6% 97.3% 85.8% 76.4% 100.0% 3.4% 100.0% 100.0%West LB 99.3% 92.8% 55.9% 98.0% 99.3% 99.3% 95.4% 97.4% 98.0% 96.1% 84.9% 75.7% 98.7% 3.9% 97.4% 100.0%

40

TABLE 5.B Banks Pairwise Participation Rates, 8/9/07 - 4/16/08

BTMUBank Amer Barcl

JPM Chase Citi CSFB Deutschb HBOS HSBC Lloyds Norinch Rabob

Royal Bank of Canada

Royal Bank of Stotland UBS AG West LB

BTMU 100.0% 71.8% 48.9% 89.3% 59.5% 77.9% 22.1% 77.9% 71.0% 81.7% 35.1% 45.8% 88.5% 60.3% 56.5% 93.1%Bank of America 77.0% 100.0% 41.0% 86.9% 64.8% 81.1% 20.5% 78.7% 72.1% 75.4% 28.7% 45.9% 86.9% 60.7% 63.1% 94.3%Barclays 81.0% 63.3% 100.0% 92.4% 67.1% 74.7% 16.5% 77.2% 72.2% 77.2% 29.1% 53.2% 86.1% 55.7% 54.4% 88.6%JPM Chase 75.5% 68.4% 47.1% 100.0% 57.4% 78.1% 22.6% 81.3% 66.5% 78.7% 31.6% 49.7% 88.4% 62.6% 58.7% 92.3%Citigroup 72.9% 73.8% 49.5% 83.2% 100.0% 82.2% 16.8% 79.4% 65.4% 76.6% 34.6% 45.8% 86.0% 55.1% 57.9% 91.6%CSFB 75.6% 73.3% 43.7% 89.6% 65.2% 100.0% 21.5% 83.0% 65.2% 77.0% 33.3% 45.9% 87.4% 59.3% 60.0% 91.9%Deutschbank 76.3% 65.8% 34.2% 92.1% 47.4% 76.3% 100.0% 84.2% 55.3% 73.7% 26.3% 42.1% 94.7% 63.2% 65.8% 94.7%HBOS 72.9% 68.6% 43.6% 90.0% 60.7% 80.0% 22.9% 100.0% 66.4% 78.6% 36.4% 50.0% 87.1% 62.9% 60.0% 92.9%HSBC 78.8% 74.6% 48.3% 87.3% 59.3% 74.6% 17.8% 78.8% 100.0% 78.8% 31.4% 52.5% 85.6% 56.8% 56.8% 92.4%Lloyds 78.1% 67.2% 44.5% 89.1% 59.9% 75.9% 20.4% 80.3% 67.9% 100.0% 35.8% 44.5% 86.9% 59.1% 58.4% 94.2%Norinchukin 79.3% 60.3% 39.7% 84.5% 63.8% 77.6% 17.2% 87.9% 63.8% 84.5% 100.0% 48.3% 89.7% 69.0% 56.9% 91.4%Rabobank 71.4% 66.7% 50.0% 91.7% 58.3% 73.8% 19.0% 83.3% 73.8% 72.6% 33.3% 100.0% 86.9% 61.9% 50.0% 91.7%Royal Bank of Canada 76.3% 69.7% 44.7% 90.1% 60.5% 77.6% 23.7% 80.3% 66.4% 78.3% 34.2% 48.0% 100.0% 63.2% 59.2% 94.1%Royal Bank of Stotland 73.8% 69.2% 41.1% 90.7% 55.1% 74.8% 22.4% 82.2% 62.6% 75.7% 37.4% 48.6% 89.7% 100.0% 56.1% 92.5%UBS AG 71.8% 74.8% 41.7% 88.3% 60.2% 78.6% 24.3% 81.6% 65.0% 77.7% 32.0% 40.8% 87.4% 58.3% 100.0% 95.1%West LB 75.3% 71.0% 43.2% 88.3% 60.5% 76.5% 22.2% 80.2% 67.3% 79.6% 32.7% 47.5% 88.3% 61.1% 60.5% 100.0%

41

TABLE 5.C Banks Pairwise Participation Rates, 4/17/08-5/30/08

BTMUBank Amer Barcl

JPM Chase Citi CSFB Deutschb HBOS HSBC Lloyds Norinch Rabob

Royal Bank of Canada

Royal Bank of Stotland UBS AG West LB

BTMU 100.0% 0.0% 25.0% 75.0% 75.0% 75.0% 25.0% 50.0% 100.0% 25.0% 75.0% 50.0% 75.0% 50.0% 100.0% 50.0%Bank of America 0.0% 100.0% 57.1% 71.4% 85.7% 85.7% 14.3% 85.7% 85.7% 28.6% 0.0% 28.6% 100.0% 85.7% 100.0% 42.9%Barclays 6.3% 25.0% 100.0% 56.3% 87.5% 93.8% 18.8% 87.5% 87.5% 68.8% 6.3% 37.5% 68.8% 68.8% 81.3% 75.0%JPM Chase 17.6% 29.4% 52.9% 100.0% 88.2% 94.1% 29.4% 82.4% 94.1% 52.9% 11.8% 41.2% 88.2% 76.5% 88.2% 52.9%Citigroup 10.7% 21.4% 50.0% 53.6% 100.0% 85.7% 17.9% 89.3% 85.7% 57.1% 7.1% 46.4% 82.1% 82.1% 85.7% 71.4%CSFB 11.5% 23.1% 57.7% 61.5% 92.3% 100.0% 23.1% 84.6% 84.6% 57.7% 7.7% 42.3% 76.9% 76.9% 84.6% 65.4%Deutschbank 16.7% 16.7% 50.0% 83.3% 83.3% 100.0% 100.0% 66.7% 100.0% 33.3% 16.7% 33.3% 66.7% 83.3% 83.3% 66.7%HBOS 7.7% 23.1% 53.8% 53.8% 96.2% 84.6% 15.4% 100.0% 84.6% 57.7% 7.7% 46.2% 84.6% 84.6% 84.6% 69.2%HSBC 15.4% 23.1% 53.8% 61.5% 92.3% 84.6% 23.1% 84.6% 100.0% 53.8% 11.5% 46.2% 84.6% 80.8% 84.6% 65.4%Lloyds 6.3% 12.5% 68.8% 56.3% 100.0% 93.8% 12.5% 93.8% 87.5% 100.0% 0.0% 43.8% 75.0% 68.8% 87.5% 68.8%Norinchukin 100.0% 0.0% 33.3% 66.7% 66.7% 66.7% 33.3% 66.7% 100.0% 0.0% 100.0% 66.7% 66.7% 66.7% 100.0% 66.7%Rabobank 14.3% 14.3% 42.9% 50.0% 92.9% 78.6% 14.3% 85.7% 85.7% 50.0% 14.3% 100.0% 78.6% 71.4% 85.7% 78.6%Royal Bank of Canada 12.5% 29.2% 45.8% 62.5% 95.8% 83.3% 16.7% 91.7% 91.7% 50.0% 8.3% 45.8% 100.0% 83.3% 83.3% 62.5%Royal Bank of Stotland 8.3% 25.0% 45.8% 54.2% 95.8% 83.3% 20.8% 91.7% 87.5% 45.8% 8.3% 41.7% 83.3% 100.0% 91.7% 75.0%UBS AG 15.4% 26.9% 50.0% 57.7% 92.3% 84.6% 19.2% 84.6% 84.6% 53.8% 11.5% 46.2% 76.9% 84.6% 100.0% 69.2%West LB 9.5% 14.3% 57.1% 42.9% 95.2% 81.0% 19.0% 85.7% 81.0% 52.4% 9.5% 52.4% 71.4% 85.7% 85.7% 100.0%

42

TABLE 6 Correlation between Quotes and CDS Spreads

Period 1 Period 2 Period 3BTMU 0.58 -0.76 0.50Bank of America 0.53 -0.85 0.44Barclays 0.58 -0.82 -0.35JPM Chase 0.51 -0.84 0.41Citigroup 0.58 -0.85 0.00CSFB 0.57 -0.82 0.16Deutschbank 0.19 -0.79 -0.24HBOS 0.46 -0.84 0.18HSBC 0.52 -0.86 0.39Lloyds 0.71 -0.89 0.24Norinchukin NaN NaN NaNRabobank 0.24 -0.88 0.15Royal Bank of Canada NaN NaN NaNRoyal Bank of Scotland NaN NaN NaNUBS AG 0.40 -0.85 0.18West LB 0.71 -0.85 0.51

43

TABLE 7 Correlation between changes in Quotes and changes in CDS Spreads

Period 1 Period 2 Period 3BTMU -0.13 -0.19 -0.21Bank of America 0.00 0.06 -0.08Barclays -0.02 -0.12 -0.44JPM Chase -0.09 0.03 -0.21Citigroup -0.15 -0.03 -0.20CSFB -0.25 -0.09 -0.25Deutschbank -0.28 -0.07 -0.55HBOS 0.00 -0.05 -0.53HSBC -0.11 -0.15 -0.18Lloyds -0.17 -0.11 -0.23Norinchukin NaN NaN NaNRabobank -0.01 -0.07 -0.48Royal Bank of Canada NaN NaN NaNRoyal Bank of Scotland NaN NaN NaNUBS AG -0.31 -0.13 -0.26West LB 0.01 0.02 -0.29

44

TABLE 8 Correlation between Quotes and Market CAP

Period 1 Period 2 Period 3BTMU NaN NaN NaNBank of America -0.14 0.78 0.73Barclays -0.05 0.84 0.85JPM Chase -0.30 0.36 0.53Citigroup -0.30 0.85 0.78CSFB -0.19 0.85 0.37Deutschbank 0.00 0.81 0.67HBOS -0.22 0.91 0.77HSBC 0.21 0.68 -0.03Lloyds 0.00 0.78 0.88Norinchukin NaN NaN NaNRabobank NaN NaN NaNRoyal Bank of Canada 0.06 0.58 -0.89Royal Bank of Scotland -0.12 0.91 -0.46UBS AG -0.19 0.93 0.75West LB NaN NaN NaN

45

TABLE 9 CDS spreads Libor Quotes Percent in Low Half Percent in Low Half (*1)

Period 1 Period 2 Period 3 Period 1 Period 2 Period 3BTMU 68.0% 98.3% 100.0% 96.7% 36.2% 3.3%Bank of America 2.6% 41.4% 16.7% 97.4% 58.0% 93.3%Barclays 94.1% 45.4% 63.3% 55.6% 26.4% 23.3%JPM Chase 0.0% 32.8% 6.7% 98.0% 85.1% 93.3%Citigroup 3.3% 8.0% 0.0% 100.0% 92.5% 86.7%CSFB 0.0% 42.5% 70.0% 99.3% 61.5% 76.7%Deutschbank 0.0% 64.9% 100.0% 98.7% 96.0% 96.7%HBOS 99.3% 8.0% 0.0% 99.3% 54.0% 53.3%HSBC 84.3% 98.9% 100.0% 99.3% 90.8% 46.7%Lloyds 100.0% 99.4% 100.0% 96.1% 59.2% 100.0%Norinchukin NaN NaN NaNRabobank 100.0% 100.0% 100.0% 75.2% 91.4% 100.0%Royal Bank of Canada NaN NaN NaNRoyal Bank of Scotland NaN NaN NaNUBS AG 83.7% 59.8% 46.7% 98.7% 93.1% 76.7%West LB 0.7% 1.7% 0.0% 36.6% 66.1% 36.7%

(*1) Computed only among the 13 banks for which we also have CDS spreads data

46

TABLE 10 Libor Quotes Market CAP Percent in Low Half Percent in Low Half (*1)

Period 1 Period 2 Period 3 Period 1 Period 2 Period 3BTMU NaN NaN NaN NaN NaN NaNBank of America 96.7% 48.9% 93.3% 0.0% 0.0% 0.0%Barclays 55.6% 19.0% 20.0% 100.0% 100.0% 100.0%JPM Chase 98.0% 71.3% 93.3% 0.0% 0.0% 0.0%Citigroup 99.3% 90.2% 76.7% 0.0% 0.0% 0.0%CSFB 98.0% 51.7% 66.7% 99.3% 99.4% 100.0%Deutschbank 98.7% 93.7% 96.7% 100.0% 98.9% 100.0%HBOS 100.0% 40.2% 36.7% 100.0% 100.0% 100.0%HSBC 99.3% 87.9% 36.7% 0.0% 0.0% 0.0%Lloyds 96.1% 48.9% 100.0% 100.0% 100.0% 100.0%Norinchukin NaN NaN NaN NaN NaN NaNRabobank NaN NaN NaN NaN NaN NaNRoyal Bank of Canada 98.7% 59.2% 53.3% 100.0% 97.7% 76.7%Royal Bank of Scotland 100.0% 87.9% 60.0% 0.0% 0.0% 3.3%UBS AG 98.0% 90.8% 63.3% 0.0% 4.0% 20.0%West LB NaN NaN NaN NaN NaN NaN

(*1) Computed only among the 12 banks for which we also have Market CAP data.

47

REFERENCES Abrantes-Metz, R. M., Froeb, L. M., Geweke, J. F. and Taylor, C. T. 2006. A variance screen for collusion. International Journal of Industrial Organization 24, 467-486. Abrantes-Metz, R. and S. Addanki, 2007. Is the Market being Fooled? An Error-Based Screen for Manipulation. Working paper, available at http://papers.ssrn.com/sol3/cf_dev/AbsByAuth.cfm?per_id=339863. Abrantes-Metz, R. and L. Froeb, 2008. Competition Authorities are Screening for Conspiracies: What are they Likely to Find?, The American Bar Association Section of Antitrust Law Economics Committee Newsletter, March 2008.

Aggarwal, R. and W. Guojun, 2003, “Stock Market Manipulation: Theory and Evidence,” AFA 2004 San Diego Meetings, http://papers.ssrn.com/sol3/papers.cfm?abstract_id=474582 Benford, F., 1938, ‘The law of anomalous numbers’, Proceedings of the American Philosophical Society 78(4), 551–572. British Banker's Association, June 7, 2008. BBA Libor – Frequently Asked Questions. Available at http://www.bba.org.uk/bba/jsp/polopoly.jsp?d=225&a=1416. Crabtree, A. D. and J. J. Maher, 2005, “Earnings Predictability, Bond Ratings, and Bond Yields,” Review of Quantitative Finance and Accounting, 25, 233-253. Ederington, L. H., J. B. Yawitz and B. E. Roberts, 1987, “The Information Content of Bond Ratings,” Journal of Financial Research, 10, 211-226. Fridson, M. S. and M. C. Garman, 1998, “Determinants of Spreads on New High-Yield Bonds,” Financial Analysts Journal, 54, 28-38. Gabbi, G. and A. Sironi, 2005, “Which Factors Affect Corporate Bonds Pricing? Empirical Evidence from Eurobonds Primary Market Spreads,” European Journal of Finance, 11, 59-74. Goldberg, R. and J. Read, 2007, “Just Lucky? A Statistical Test for Option Backdating”, Working Paper, available at http://papers.ssrn.com/sol3/papers.cfm?abstract_id=977518. Gorton, G., 1996, “Reputation Formation in Early Bank Note Markets,” Journal of Political Economy, 104, 346-397. Harrington, J., 2006, “Behavioral Screening and the Detection of Cartels,” European University Institute, Working Paper. Harrington, J, 2008, “Detecting Cartels," in Handbook in Antitrust Economics, Paolo Buccirossi,

48

editor, MIT Press. Heron, R. and E. Lie, 2006, “Does backdating explain the stock price pattern around executive stock option grants?”, Journal of Financial Economics, forthcoming. Hubbard, R.G., K. N. Kuttner and D. N. Palia, 2002, “Are There Bank Effects in Borrowers' Cost of Funds? Evidence from a Matched Sample of Borrowers and Banks,” Journal of Business, 75, 559-581. Johnson, S. A., 1997, “The Effect of Bank Reputation on the Value of Bank Loan Agreements,” Journal of Accounting, Auditing & Finance, 12, 83-100. Judge, G. and L. Schechter, 2006, “Detecting Problems in Survey Data using Benford’s Law”, Working paper, University of California at Berkeley. Konrad, R. and Sandoval, G. 2002. Orbitz rivals cry foul, claim monopoly in air travel. CNET News.com, April 11, 2002. http://news.cnet.com/2009-1017-879314.html. Livingston, M. and R. E. Miller, 2000, “Investment Bank Reputation and the Underwriting of Nonconvertible Debt,” Financial Management, 29, 21-34. Mackenzie, M. 2008. Libor bankers brush off calls to reform way key rate is calculated. Financial Times (May 31): Mackenzie, M. and Tett, G. 2008. Libor remarks fail to put unease to rest. Financial Times (June 2): 16. Mollenkamp, C. and Norman, L. 2008. British bankers group steps up review of widely used Libor. Wall Street Journal (April 17), C7. Mollenkamp, C. and Whitehouse, M. 2008. Study casts doubt on key rate; WSJ analysis suggests banks may have reported flawed interest data for Libor. Wall Street Journal (May 29), A1. Narayanan, R. P., K. P. Rangan and N. K. Rangan, 2007, “The Effect of Private-Debt Underwriting Reputation on Bank Public-Debt Underwriting,” Review of Financial Studies, 20, 597-618. Newcomb, S., 1881, ‘Note on the frequency of use of the different digits in natural numbers’, American Journal of Mathematics 4, 1, 39–40. Nigrini, J., 2005, “An Assessment of the Change in the Incidence of Earnings Management Around the Enron-Andersen Episode,” Review of Accounting and Finance, 4, 1, 92-110. Russo, T., 1983-93, Regulation of the Commodities Futures and Options Markets, Colorado

49

Springs: Shepard’s/MacGraw-Hill, 12-19. Yi, H.-C. and D. J. Mullineaux, 2006, “The Informational Role of Bank Loan Ratings,” Journal of Financial Research, 29, 481-501.