islamic microfinance in palestine: challenges and prospects (pdf

TRANSCRIPT

1

Islamic Microfinance in Palestine: Challenges and Prospects

Md. Sohel Rana1, Mohd Nazari Ismail1, Izlin Ismail2

1. Department of Business Strategy and Policy, Faculty of Business and Accountancy,

University of Malaya, Kuala Lumpur, 50603, Malaysia

2. Department OF Finance and Banking, Faculty of Business and Accountancy,

University of Malaya, Kuala Lumpur, 50603, Malaysia

Email Address: [email protected] (Md. Sohel Rana), [email protected]

(Professor Mohd Nazari Ismail), [email protected] (Dr. Izlin Ismail)

Corresponding Author: [email protected]

Abstract: The objective of the paper is to identify challenges and opportunities in Islamic micro

finance industry by reviewing the present status of Islamic microfinance in Palestine and later

suggestinga multiple-stages financing model which will alleviate poverty significantly. To

accomplish this purpose, we obtain secondary data from various sources. We suggest a financial

framework incorporating several Islamic financial models and the sources of fund applying into

different levels of poverty in Palestine.The paper concludes with some policy recommendations,

which may potentially create small entrepreneurs and alleviate poverty to a certain extent.

Abstrak: Tujuan dari makalah ini adalah untuk mengidentifikasi tantangan dan peluang dalam

industri keuangan mikro syariah dengan meninjau status sekarang dari keuangan mikro Islam di

Palestina dan kemudian menyarankan model pembiayaan multi-tahap yang akan mengurangi

kemiskinan secara signifikan. Untuk mencapai tujuan ini, kami mendapatkan data sekunder dari

berbagai sumber. Kami menyarankan kerangka keuangan menggabungkan beberapa model

keuangan Islam dan sumber dana menerapkan ke dalam berbagai tingkat kemiskinan di

Palestina. Makalah ini diakhiri dengan beberapa rekomendasi kebijakan, yang dapat berpotensi

menciptakan pengusaha kecil dan mengentaskan kemiskinan sampai batas tertentu.

Key Words: Islamic Microfinance, Palestine, Challenges, Prospects.

JEL: F63

2

Introduction

The conventional and Islamic microfinances are becoming professional industries and offering a

wide range of products to the poor population all over the world. Both the concepts got the wide

range of global acceptance to pull a certain segment of the population by making them enabled in

generating income and changing their lives with small capital they get as a micro finance from

Microfinance Institutions. The conventional microfinance was initiated in order to eradicate

poverty by giving a small amount of credit to the poor by charging interest. On the contrary,

Islamic microfinance was introduced to give a substitution to interest. The Muslim population is

increasing rapidly in the world. According to (Haub et al. 2011), It is estimated that the Muslim

population on this earth may reach to 2 .2 billion by 2030.The World (Bank 2012) shows the

almost 896 million people live on earning less than USD 1.90 per day.The Muslim countries are

facing high unemployment, poverty and low level of financial access which predominantly

created a huge demand of micro-credit and reached successfully in the poor Muslim countries

like Bangladesh and Indonesia. The excessive number of poverty in the Muslim countries is

believed to be the improper way of financing with high interest rate to the poor people of those

countries. The interest is strictly forbidden in Islamic law. The high interest rate is depriving the

poor people from improving their living standard and other benefits. Thus the ultimate goal of

microfinance of eradicating poverty and keeping it in the museum is becoming unsuccessful.

The Islamic financing system to the poor Muslim people living all over the world that support

religious perception against the interest rate in conventional micro financing is becoming a

formidable way to make the millions of poor Muslim’s economically solvent which will bring

them out of the fence of high interest payment. Islamic microfinance will involve the poor

Muslims in sharia compliant suitable credit system and bring the unbanked poor under the

umbrella of Islamic microfinance.

According to(Nimrah Karim 2011), almost 20 percent of the people in Algeria and Jordan

denied conventional microfinance and giving the excuse of the religious region. In case of

Yemen and Syria the percentage rises to 40 percent. According to (Karim et al. 2008)revealed

that the local practitioners and key informants suggested similar demand trends in Indonesia,

Afghanistan, Pakistan, and the Palestinian territories and also Muslim majority areas of India, Sri

Lanka, Brunei, Cambodia and the Philippines. Islamic microfinance shows an alternative model

3

for those poor people who are not currently entertained by conventional microfinance. Thus it is

rather important for this thriving industry to come up with some innovative and comprehensive

microfinance business model in order to provide sustainable services which will meet the

financial demand of the Muslim poor. The present status of Islamic microfinance in the world is

the USD 1 billion which is still less than 1 percent of Islamic finance market (USD 1.6 trillion).

Moreover, around 300 microfinance institutions are operating worldwide. The major markets of

Islamic microfinance includes Sudan, Yemen, Pakistan, Indonesia, Egypt, Qatar, Bahrain,

Jordan, Mali, Lebanon, Syria, KSA, Iraq, Palestine, Afghanistan and others (Ahmed et al. 2015).

Religious perception towards the conventional way of lending created necessity to establish a

suitable lending system which would meet the demand of Muslim people. According to (CGAP

News 2008) survey demonstrated that global Islamic microfinance is contributing very little and

operating merely in few countries (80% of the 380,000 clients of Islamic microfinance

worldwide are in Bangladesh, Indonesia and Afghanistan); Furthermore, the practice of Islamic

microfinance is very little, and it does not surpass more than .05 percent of total microfinance

outreach. In case of Arab world, Microfinance Institutions (MFIs) that have been operating for 7-

10 years typically only reached between 2000-7000 active borrowers through Islamic

microfinance.Therefore, Islamic microfinance needs to be promoted to the poor Muslims as

potential a weapon to fight against poverty. It can develop a valuable human capital base in the

Muslim community and positively contribute towards the economic growth in these countries.

The Islamic Microfinance concept is comparatively new, and it is still facing challenges and

difficulties. Palestine is relatively a conservative Muslim country with extreme poverty and

surrounded by different political and economic problems. According to World Food Programme

WFP (2014) Palestine economy went through a recession specially the Gaza faced a negative

growth and had a sever effect on unemployment which went up to 43 percent. The youth

unemployment in Gaza soared to 60 percent and overall unemployment in West Bank and Gaza

increased to 27 percent in 2014. The Palestinian economy is basically aid driven, but aid cannot

be a sustainable long-term solution for a nation to be developed. Therefore, it is important to

come up with some formidable Islamic micro financing models which will make the economy

dynamic by creating entrepreneurial opportunities in the SMEs and agriculture which will

ultimately open a number of job opportunities.

4

Therefore, the objective of the paper is to identify challenges and opportunities in Islamic micro

finance industry by reviewing the present status of Islamic microfinance in Palestine and

subsequently, provide a sustainable multiple-stages financing model which will alleviate poverty

significantly complying with the Islamic regulations.

Literature Review

Islam does not allow interest and any other activity, which is not permissible by the sharia or

Islamic law. On the other hand, interest is supposed to be a drawback of poverty eradication.

According to(Mollah & Uddin), mentioned that 98 percent of the borrowers under microfinance

program are not aware of the terms and condition of loan and interest rate, and they are

completely disadvantaged, on the contrary, Islam ensures social justice and equity, which guide

to balance and peace in the society.

Muslims have always been struggling for years to retain their values and cultures in almost every

sphere of their lives. (Frasca 2008)focused on the competitiveness of Islamic microfinance and

argued that Islamic microfinance could be a potential sector for the investors who faced badly in

the global credit crisis of the conventional and speculative credit system.(Akhter et al.

2009)conducted a survey on 125 institutions in 19 Muslim countries. It revealed that Islamic

microfinance merely reached to 300,000 clients, Bangladesh contained one third of them

alone.They further mentioned that itwas very important to concentrate in crafting affordable

micro financing models, training and retaining skilled loan officers and administrators,

improving operational efficiency and managing overall business risks to reach more

people.(Obaidullah 2008), concluded that the commercial banks and other Islamic financial

Institutions are not interested in financing micro loans to the lower-income people and Small and

Medium Enterprises in the society and demotivated due to the absence of collateral or credit

guarantee. He further mentioned that it is important to make a linkage among various

organizations, including government agencies, None Government Organizations (NGOs), None

Profit Organizations (NPOs), cooperative companies, Takaful so that they can reach to the

poorest of the poor of a society significantly. The linkage between the organizations will

fruitfully contribute in the micro-enterprises development which will ultimately eradicate

poverty significantly from the grass root levels of a society.According to (Mohammed) describe

the IDLO Report (2009), Islamic microfinance got less attention and remained less developed in

5

the Arab world than the other countries in Asia, Africa and Latin America. In the Social and

Development Summit in Kuwait city at Arab Economy in 2009, the League of Arab States

declared the formation of the USD 2 billion fund run by the Arab Development bank to establish

and implement microfinance programme which targeted at boosting small businesses and

alleviates poverty across the Arab World.

According to (Barden 2010)A number of aid and assistant programmes are being provided in

West Bank and Gaza region to support for a strong and healthy financial sector on a large scale

which will contribute to financing for infrastructure projects. In case of promoting small

businesses and individual a wide range of micro financing programmes has been undertaken. The

financing programmes are specially shahriah based and becoming increasingly widespread in

these days in Palestine.

Data Collection and Methodology

The data collected is mainly from the secondary sources from various journal papers, books,

different official reports, scholar’s studies, newspapers, website, government reports and other

sources. This paper puts an effort to theoretically review the microfinance industry in Palestine

along with the Islamic microfinance models, challenges and opportunities. Furthermore, this

paper suggests multiple- stages integrated model, which will probably be able to fit socio-

economic and political condition of Palestine and alleviate poverty.

An Overview of Islamic Micro-finance and Islamic microfinance Practice in Palestine

Micro-credit was first introduced in 1980s in the occupied Palestinian territory for the rapid

growing demand for financing from small and microenterprises, which were the backbone of

production and employment in Palestinian economy(Dodeen 2013). Before the establishment of

Palestinian National Authority, microfinance associations were the only source of financing.

Afterwards with the monitoring of Palestinian National Authority microfinance organizations

have expanded and attracted attentionof donors given the role of microfinance as one of the key

elements for development and the fight against poverty.As a result the number of financing

institutions, registered NGOs and international organizations have increased remarkably. In

1996, West Bank and Gaza Strip were given a limited political and economic autonomy to be

administered by Palestine National Authority(Arnon & Weinblatt 2001). Since then the territory

6

is experiencing a high degree of political instabilities, military interventions and conflicts, which

have been deeply discussed all over the world but a very little attention has been given to

evaluate economic and business environment. The development of the credit sector was even

more neglected especially the result of negligence of the contribution and dynamism of banks

and not-for- profit organization in practicing microfinance was serious, which hindered smooth

economic performance. This cannot be kept as a passive element which respond to the stimuli

coming from the real economy(King & Levine 1993). The Palestinian economy is largely relied

on Aid. Therefore, the dependence on external donations has major implications in terms of

domination and performance, since donors are mainly motivated by political and ideological

aims.The main reasons for the poor performance and the fluctuation of Palestinian economy have

been attributed to the Israeli policy of limiting the free movement of goods and people from and

to Palestine. Basically, there is less literature on the topic of the development and functioning of

microcredit industry in Palestine and thus the paper will fill that gap. Since the regions in

Palestine are poorer and the banks cannot generate loan utilizing its deposit, therefore the

emergence of Islamic microfinance industry can be the obvious alternative in this perspective.

Although West Bank has gained a measure of economic growth assisted by donor’s aid programs

and nine million members of Palestine diaspora who have sent their hard-earned money as

remittance to help relatives or funds fledgling business activities. Despite this growth, wealth has

not been evenly distributed to the people of West Bank. (Barden 2010) addressed that 50 percent

of the West Bank Population live under the poverty line. In the village many people still live a

Bedouin lifestyle, preferring tents or impoverish housing shelters.

Since transaction of interest is prohibited in Islam and for the devoted Muslims in Palestine, the

financial system is guided by the principles of Shariah where riba meaning that charging

exorbitant rates of interest are totally forbidden. Therefore, microfinance Department of United

Nations relief and Work’s agencies, Palestine Development Fund and even the Gaza Women

Loan Fund provides particularly shariah based loans at comparatively low interest rates of 5 to

10 percent and compel borrowers to attend classes in financial and business management(Barden

2010). But still this financing system does not follow Islamic norms of financing because it

includes interest. Therefore, a sustainable model is highly demanded for the people of Palestine,

which will support Islamic rules and regulations in micro-financing.

7

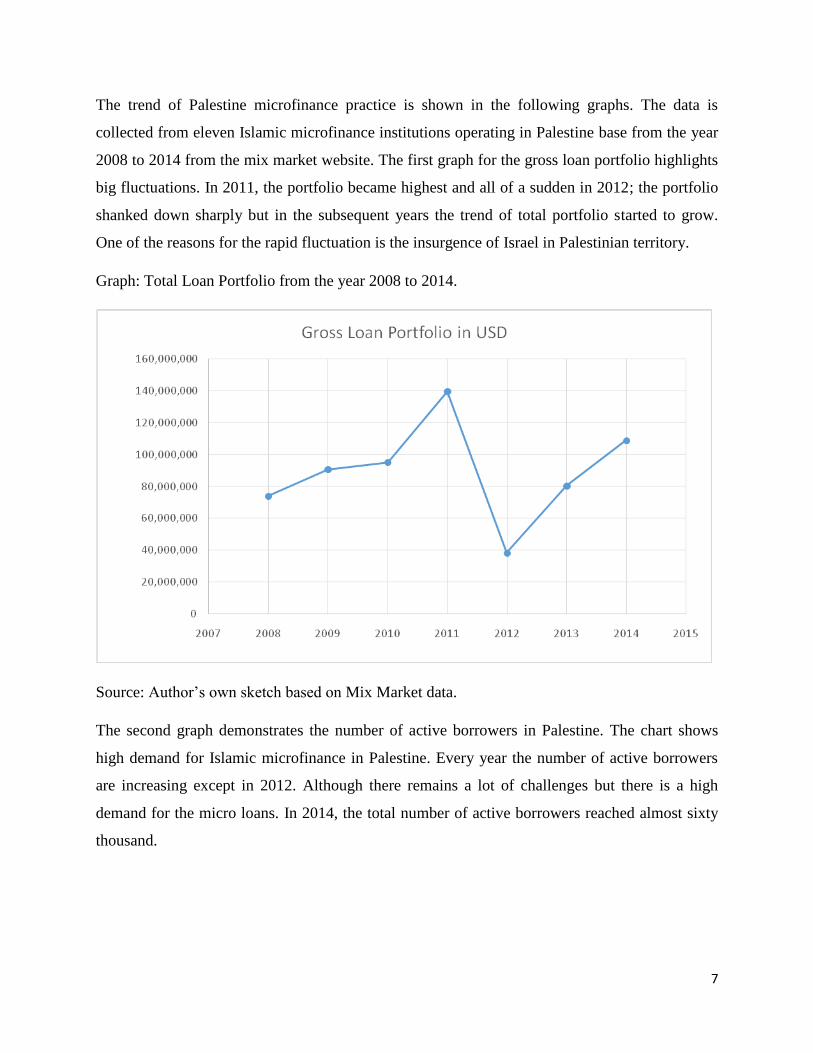

The trend of Palestine microfinance practice is shown in the following graphs. The data is

collected from eleven Islamic microfinance institutions operating in Palestine base from the year

2008 to 2014 from the mix market website. The first graph for the gross loan portfolio highlights

big fluctuations. In 2011, the portfolio became highest and all of a sudden in 2012; the portfolio

shanked down sharply but in the subsequent years the trend of total portfolio started to grow.

One of the reasons for the rapid fluctuation is the insurgence of Israel in Palestinian territory.

Graph: Total Loan Portfolio from the year 2008 to 2014.

Source: Author’s own sketch based on Mix Market data.

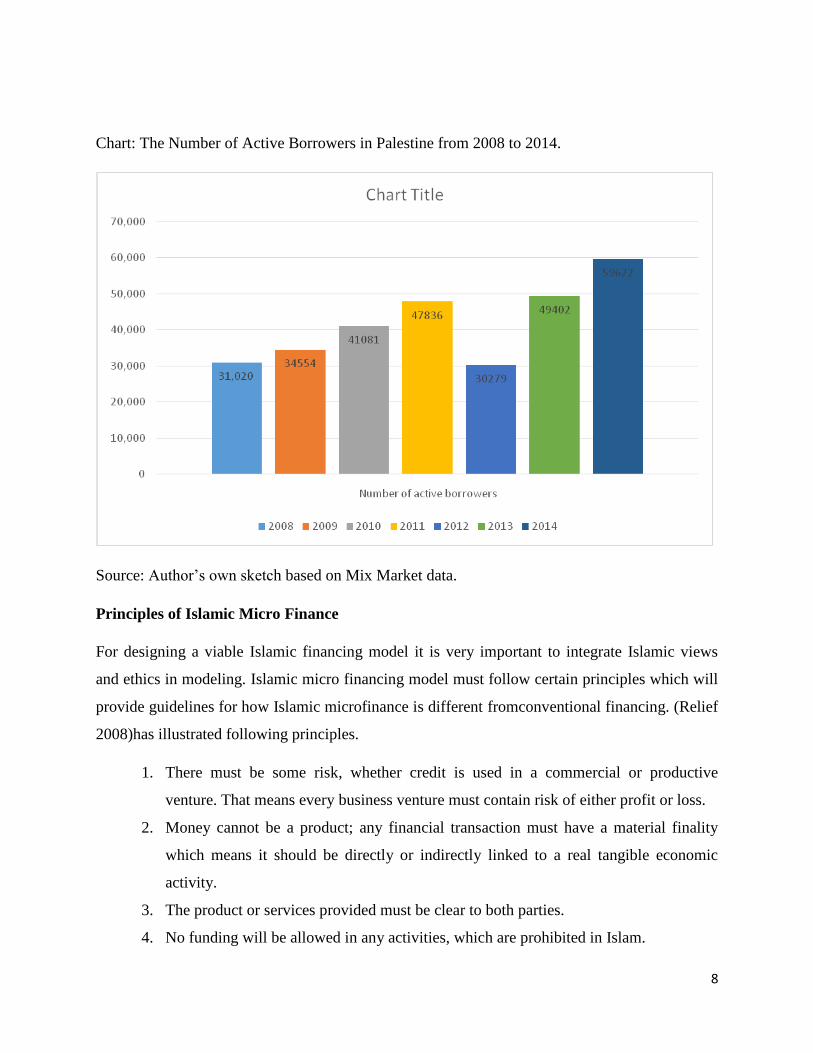

The second graph demonstrates the number of active borrowers in Palestine. The chart shows

high demand for Islamic microfinance in Palestine. Every year the number of active borrowers

are increasing except in 2012. Although there remains a lot of challenges but there is a high

demand for the micro loans. In 2014, the total number of active borrowers reached almost sixty

thousand.

8

Chart: The Number of Active Borrowers in Palestine from 2008 to 2014.

Source: Author’s own sketch based on Mix Market data.

Principles of Islamic Micro Finance

For designing a viable Islamic financing model it is very important to integrate Islamic views

and ethics in modeling. Islamic micro financing model must follow certain principles which will

provide guidelines for how Islamic microfinance is different fromconventional financing. (Relief

2008)has illustrated following principles.

1. There must be some risk, whether credit is used in a commercial or productive

venture. That means every business venture must contain risk of either profit or loss.

2. Money cannot be a product; any financial transaction must have a material finality

which means it should be directly or indirectly linked to a real tangible economic

activity.

3. The product or services provided must be clear to both parties.

4. No funding will be allowed in any activities, which are prohibited in Islam.

9

5. Financial risk will lie on the investors only and not to any managers or agents related

to the project management.

6. Interest is strictly forbidden but still some mark-up can be included to cover charges

incurred decided by the both parties.

7. It is not allowed to sell what one does not belong. Thus short selling is impermissible.

Islamic microfinance stands on these basic principles supported by the Quran and Sunnah. All

the financial institutions must follow these principles in designing financing models for their

clients. In conventional microfinance any idea can be tested and apply on the clients regardless

of their harmful and negative impacts on the people but in Islamic finance the people are much

prioritized.

Existing Islamic Microfinance Practices around the Globe

Islamic microfinance predominantly follows the instruments of Islamic finance. The widely

accepted models namely Mudaraba (Profit sharing), Musharka (Partnership), Murabaha (Markup

or cost plus), Ijara thuma bai (Hire purchase), Qard hasan (Interest free loan), Bay salam

(forward sale), Wadiah (safe keeping) etc. are adopted by Islamic microfinance and have been

successfully practicing in some Muslim countries like Bangladesh, Indonesia, Malaysia,

Afghanistan and in some middle east and African countries. All the models are not always

accepted by all the countries. The socio-economic, political and countries cultural trends vary

from one country to another. Thus different Islamic models are adopted by different country. In

some cases, the models are designed incorporating social aspects and economic condition of any

particular country. But overall the main aims of all the models remain same of eradicating

poverty, creating employment opportunities, spreading out of education and healthcare facilities

and improvement of standard of life.

According to (Mollah & Uddin)Islamic microfinance was initiated in Sudan in 80s and the

Microfinance Institutes only have Mudarabah and Quard e Hasan products. However, In Syria

Microfinance was launched in 1998 and they only follow Murabaha model. (Mollah &

Uddin)further address that Indonesia has large diversity of both conventional and Islamic Micro-

financing. The country has 97 percent Muslim people but only 11 percent of them understand the

Islamic microfinance products. Quar-e-Hasan model is very popular in Iran. These loans are free

but an administrative cost is charged on the size of the loans and the ability of the borrowers to

10

repay. IDB has provided a model for the Deprived Families Economic Empowerment Program

(DEEP) in Palestine. The family bank is established in Bahrain signing agreement between

Family Bank and Grameen Trust(Mollah & Uddin).Islamic microfinance demands innovative

models to serve various financial needs of the poor around the world. The conventional

microfinance system contains high risk and therefore they charges high interest rate and give

loans in groups. The other group members are taking loans from other MFIs which ultimately

creating debt burden for the borrowers and the loans are becoming unproductive. The existing

Micro financing model are not effective enough in integrating basic need of the poor and lagging

behind the reasonable solution to the real problem in an effective manner. Therefore a societal

integrated model is badly needed.

Challenges of Islamic Micro Finance in Palestine

The promotion and operation of Islamic microfinance in Palestine encounter a lot of challenges

and difficulties. Palestinian monetary system is not fully free and the country is greatly affected

by insurgence and Israeli occupation from time to time. The people of Palestine are religiously

fundamental and consider loan in a negative way. Apart from these issues, there are some

specific challenges which are causing Islamic microfinance slow to contribute in socio-economic

development. These are shown under.

Islamic microfinance is governed and administered by Shariah law, but there is

unavailability of separate Shariah compliant board which could have played a vital role

in promoting Islamic microfinance by providing consultative services to the IMFIs.

Islamic microfinance incur high operating cost for maintaining offices and branches,

meeting costs of salaries for the staffs and utility bills. The IMFIs are not subsidized or

supported by the government.

There are a limited number of microfinance Institutions operating in Palestine. Therefore

they cannot outreach to the maximum number of the poor people.

In Palestine, political conflict and turbulence is very common. There always tensions

between Palestine and Israel government. This conflict carry a big threat to the

economic development of the country. Islamic microfinance encounters huge

challenges in such conflicting regions.

11

Islamic microfinance requires trained and qualified staffs who can come up with

innovative, creative and effective ideas of new Islamic products and services in the

market. But unfortunately IMFIs operating in Palestine find shortage of such trained

and qualified officers for their institutions to carry forward.

There remain a lack of initiatives to promote and spread awareness about the significance

of Islamic microfinance industry especially to poor people and the economic

development of a country.

The fund for spreading and developing Islamic microfinance in Palestine territory is not

enough. Sometimes the funds are coming as Aid or food or Medicare items to the

people who are victims of the insurgence. These Aid funds serve immediate purpose

only for time being but they become crippled economically. Thus Aid funds cannot

bring long term sustainable economic solution, but only injection of money into any

profit making projects can have long term effect on their lives. Therefore funds for

innovative, entrepreneurial and income generating project is badly needed for Palestine.

Poor infrastructure in the country like communication and transportation, electricity,

foreign currency stability, social security etc. create another challenge for IMFIs to

continue and grow.

Keeping jewelries and property as mortgage is not liked by the general people in

Palestine. Therefore, collateral free loan is another challenge for the IMFIs.

Absence of well-structured and well equipped monitoring body with modern rules and

regulations to absorb the socio-economic and political condition in Palestine is another

big challenge to develop Islamic microfinance institutions in the country.

Prospects for Micro Finance Industry in Palestine

Islamic microfinance waves plenty of opportunities to turn the table to socio-economic

prosperity. The disparity of wealth, poverty, hunger and begging is not accepted in Islam. It

speaks about the equity and extension of helping hands socially and economically. Aid is not

enough to bring sustainable growth for a nation. A nation requires effectiveand well-designed

financial policy to throw the poverty in the museum. Despite having so many challenges,

12

promising demand for Islamic microfinance is lurking to emerge along with a vision to alleviate

poverty to a remarkable extent in Palestine.

Palestine gets enough sympathy from the international donors and developed countries in

the face of Aid programs and Zakat. These aid funds can be effectively utilized in the

Islamic micro financing schemes. According to (Yunus 2007) philanthropy got one life

but never comes back, but business got much means to live. Therefore, society friendly

business model can eradicate poverty by generating income utilizing the aid funds.

The corporate business world has a very important role to play in making the world a

better place to live by making the poor people enable in generating income starting with

SMEs by giving away funds as corporate social responsibility. This will ultimately

integrate poor people in the production cycle by increasing their ability to purchase by

making them economically solvent through Islamic micro financing.

Palestine economy is mainly agriculture dependent. Islamic microfinance can play a very

vital role in investing agrarian production and fishing industries.

Issuance of rules and regulations and establishment of separate promoting and monitoring

department from the government side will support Islamic microfinance develop very

rapidly in Palestine.

Huge number of unemployment of young people in Palestine opens a gateway of Islamic

microfinance. The frustrated young people can be a source of motivation in Islamic

microfinance. By providing small loans and proper training to these unemployed may

bring remarkable success in Islamic microfinance.

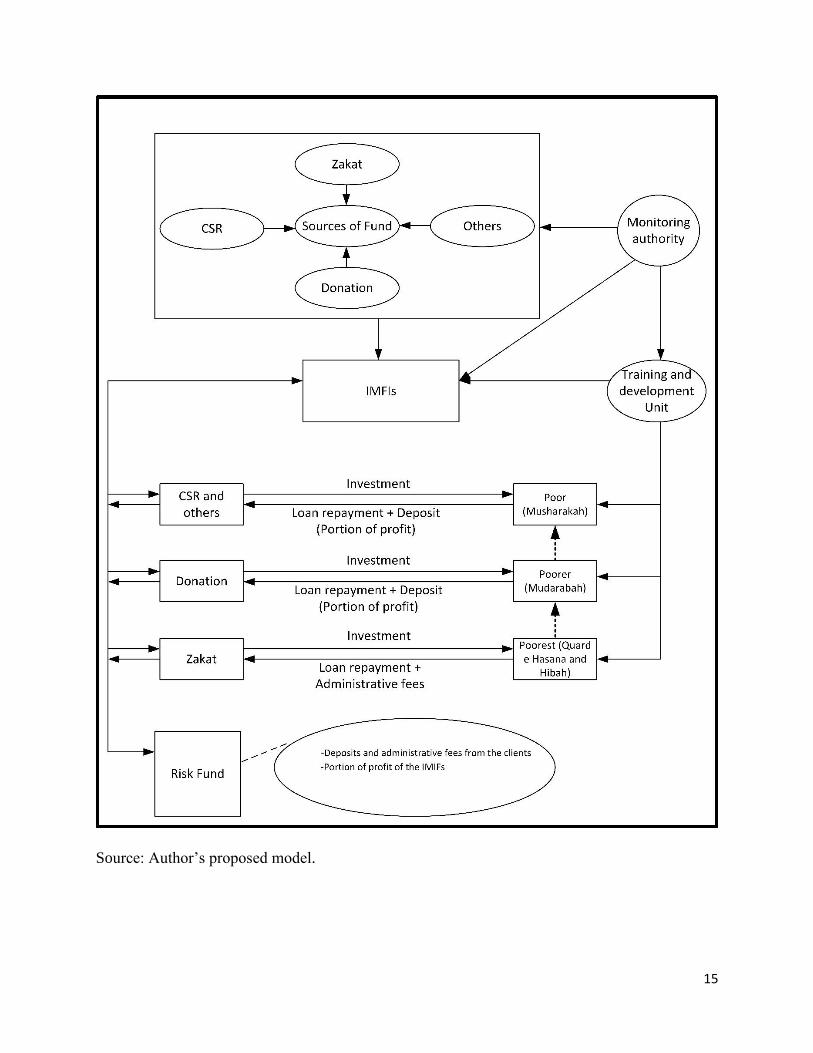

Multiple- Stages Model for Islamic Micro Finance in Palestine

Islamic microfinance can play a vital role in advancing socio-economic development of the poor

and small entrepreneurs without charging interest. The micro entrepreneurs can greatly be

motivated by the ethical attributes of Islamic microfinance. Therefore, it is very important to

develop a suitable model of Islamic microfinance, which will respect the political, social and

religious sentiment of a particular country like Palestine and work effectively to move out of

poverty. For the proposed multiple-stages financing framework, we have divided the borrowers

13

into three segments namely, the poor people, the poorer people and the poorest people1. The

three segments are incorporated with different Islamic financing models in accordance with the

principles and features of those models. The most important thing in the framework is the fund.

There will be a central fund monitored and administered by the board. The board members will

be selected by both the IMFIs and the government. The fund will be accumulated by three

sources of fund or three windows called Zakat window, Corporate Social Responsibility Window

(CSR) and International Aid or donation window. Afterward the fund will be endorsed from the

three windows to the IMFIs fulfilling certain conditions. The IMFIs responsibility would be to

identify and evaluate the three segments of the poor people to whom they will hand over micro

investments. The segments of the poor can be assessed according to the income, retaining of land

or farm land or the amount of property they own and the number of children or family member

they have. The monitoring board will establish a training and development unit which will train

both the investors and the borrowers. They will be given training about the proper utilization of

the fund and how they will be able to design new SMEs businesses. How they are going to

manage their fund and how they will be able to run their business in profit. The training unit will

also help them in consultation from time to time. The IMFIs will prepare package products from

the window funds integrating pertaining Islamic investment models to different segments of

poor. The IMFIs will form a recovery plan by creating a Risk Fund which will be accumulated

by the repayment and deposit share of the clients. The poorest segment will only give an

administrative fee, which will directly go to the risk fund. The recovery plan will be backed by

the risk fund. The percentage of repayment and deposit will be different for the poor and poorer.

The poor will repay installments; determined both by the IMFIs and the borrowers, of the loan

and give a certain percentage as provisional deposit and the rest of the profit after paying

installment and deposit will be solely taken by him. The provisional deposit will work as

collateral but subsequently this deposit will help him manage his own business without taking

any more loan. In case of poorer segment, certain percentage will be estimated as repayment

both by the borrowers and IMFIs.There will also be a provisional deposit and rest of the profit

will be taken by the clients. The poorest segment will be given concession or relaxation in

1Palestinian Central Bureau of Statisticsrevels that according to consumption patterns, the relative poverty line and the deep poverty line (for example household consists of 2 adults and 3 children) in Palestine in 2011 were 2,293 NIS, and 1,832 NIS respectively. The poverty rate among Palestinian individuals was 25.8 (17.8% in the West Bank, and 38.8% in Gaza Strip). 12.9% of the individuals in Palestine were suffering from deep poverty in 2011 according to consumption patterns (7.8% in the WestBank, and 21.1% in Gaza Strip). While 27.4% of youth (15-29) years are under the poverty rate (19.2% in the West Bank and 40.9% in Gaza Strip.

14

repayment of the loan. They will only be obliged to pay nominal administrative fees. Basically,

the Zakat fund will be provided to them as Quard-e-Hasan and Hiba. The following multiple-

stagesmodel will give a clear idea about the whole system of financing.

Multiple-stages Model

15

Source: Author’s proposed model.

16

Since Islamic microfinance is collateral free, therefore, the loans will be given in groups. The

active and matured family members, friends and relatives together will consist small groups of 5

to 8 members. They jointly plan a business project and propose it to the IMFIs. If the officers of

IMFIs understand the business project viable and enough to make them financially sound in the

future, they will take initiatives to process the loan.

Recommendation and Conclusion

The famous speech of (Yunus 2007) is that the poverty is not created by the poor rather it is

created by the system which is influenced by institutions and policies. The main purpose of our

study is to eradicate poverty and to link with the famous Nobel Prize winner’s view it can be said

that if a suitable financial framework is designed and established in a war affected country like

Palestine, the economy and the fate of those poor will turn towards the development in the near

future. The success of an effective financial strategy for the development of Islamic microfinance

basically demands concerted efforts by the stakeholders involved like the poor, the investors,

NGOs, (None Profit Organizations) NPOs, government agencies such as Ministry of Finance, the

monetary authority and he capital market authority. Therefore, my recommendation will be both

at micro and macro level. The fund controlling, monitoring and management members will be

selected from the both government and private sector and they will be accountable for the actions

in handling the fund. The government of Palestine will take initiatives to create awareness to

promote Islamic microcredit. Both the IMFIs and government will take steps to issue suitable,

modern and situation demanded rules and regulation to support and promote Islamic

microfinance. The successful and profitable businesses require to be motivated to contribute in

poverty alleviation by supplying fund as CSR. This way the big businesses will patronize small

entrepreneurs. The international donors will make understood that the fund they are supplying as

aid has been utilizing in proper manner in socio-economic development and poverty reduction.

The government will take proper steps to raise Zakat fund. Trained and qualified staffs should be

employed in this industry to develop IMFIs rapidly. The borrowers need to be involved in

training and development programs from time to time to carry out their business projects

successfully. The IMFIs will find markets for the produced items by the borrowers. In this regard

IMFIs can play an intermediary role to reach the products to the consumers in the domestic

market as well as in the international market. More research and development work need to be

17

continued to measure efficiency and productivity of the loans and recommend policies to both

Governments and IMFIs which will be financed by the both parties. Develop infrastructure and

support systems for the borrowers.

If the above recommendations are taken into consideration and prompt measures are taken into

action, the challenges of Islamic Micro finance can be mitigated. Proper management of the

overall system can ensure healthy Islamic microfinance in Palestine.Again referring the famous

quotation of(Yunus 2007), “Run the engine and the engine will run the system automatically.”

For decades, the concentration of the world in Palestine was only war, conflicts, devastation and

casualty but hardly any attention was paid to the poor people waiting to change their destiny by

empowering themselves financially. Now it is time to come up with some innovative, effective

and worthy ideas to hand over them opportunities of developing their socio-economic condition

by Islamic finance.

18

References

Ahmed, H, Mohieldin, M, Verbeek, J & Aboulmagd, FW 2015. On the sustainable development goals

and the role of Islamic finance. The World Bank.

Akhter, W, Akhtar, N & Jaffri, SKA 2009. Islamic Micro-finance and Poverty Alleviation: a case of

Pakistan. Proceeding of the 2 nd CBRC, Lahore.

Arnon, A & Weinblatt, J 2001. Sovereignty and economic development: the case of Israel and Palestine.

The Economic Journal, 111, 291-308.

Bank, W. 2012. Poverty Overview [Online]. Available:

(http://www.worldbank.org/en/topic/poverty/overview 2015].

Barden, KE 2010. Both a Borrower and Lender Be: Can Islamic Microfinance Bring Peace to Palestine?

World Policy Journal, 27, 97-102.

CGAP News. 2008. The Consultative Group to Assist the Poor [Online]. Available: www.cgap.org/

2015].

Dodeen, M. 2013. Microfinance in Palestine: The Legal Framework and the Enforcement of Contracts

[Online]. The Palestine Economic Policy Research Institute (MAS). Available: www.mas.ps.

Frasca, A 2008. AFurther NICHE MARKET: Islamic Microfinance in the Middle East and North Africa.

Center for Middle Eastern Studies and McCombs School of Business University of Texas at

Austin.

Haub, C, Gribble, J & Jacobsen, L 2011. World Population Data Sheet 2011. Population Reference

Bureau, Washington.

Karim, N, Tarazi, M & Reille, X 2008. Islam micro finance: an emerging market niche.

King, RG & Levine, R 1993. Finance, entrepreneurship and growth. Journal of Monetary economics, 32,

513-542.

Mohammed, A OVERVIEW ON ISLAMIC MICROCREDIT AS A SOLUTION TO POVERTY

ALLEVIATION. Al-Madinah Managment and Finance Science|

-ممممممممممممممممممممممممممممممممممممممممممممم

.1 ,ممممممم

Mollah, S & Uddin, MH How could an Islamic Microfinance model play the key roles in poverty

alleviation? European Perspective.

Nimrah Karim, MK. 2011. Taking Islamic Microfinance to Scale [Online]. Available:

www.cgap.org/taking-islamic-microfinance-scale 2015].

Obaidullah, M 2008. Role of Microfinance in Poverty Alleviation: Lessons from Experiences in Selected

IDB Member Countries. Mohammed Obaidullah, ROLE OF MICROFINANCE IN POVERTY

ALLEVIATION: LESSONS FROM EXPERIENCES IN SELECTED IDB MEMBER COUNTRIES,

Islamic Development Bank.

Relief, I 2008. Annual report and financial statements. Accessed March, 12, 2010.

WFP. 2014. Economy of Palestine [Online]. Available: http://www.wfp.org/countries/palestine [Accessed

02/11/2015.

Yunus, M 2007. Banker to the Poor, Penguin Books India.