investments val & capital

TRANSCRIPT

8/12/2019 Investments Val & Capital

http://slidepdf.com/reader/full/investments-val-capital 1/11

INVESTMENT VALUATION AND IT’S IMPOTANCE & RETURN ON

INVESTMENT

Traditional Technique!

A" PA# $AC% PERIOD

The pay back period is also one of the derivative of the flows. It is a simple

technique and does not employ the discount cash flow techniques. It simple measures the

time within which the initial investment of the project would or can be recovered basedon the cash accruals generated by the project.

IIIutration on a' (ac) eriod

A project has an initial outlay of Rs. 1 lakhs and it is e!pected that the project wouldgenerate cash accruals as per the following.

It is required to estimate the pay back period of the project.It may be seen from the above figures that the company will generate cash accruals of Rs.

1 lakhs by the end of the fourth year. Thus the project would pay back the initial

investment within a period of four years.There can be cases where the pay back period may not be in e!act number of years. In

these kinds of situation the e!trapolation can be done to find out the fraction of years

within which the project will generate cash accruals to repay the project"s initial outlay.

A*era+e Rate o, Return Method"

The Average Rate of Return #ARR$ method is also known as %Accounting Rate of

Return ðod' or %(inancial )tatement ðod' or %Return on Investment ðod' or*nadjusted Rate of Return ðod.' It attempts to measures the rate of return on

investment on the basis of the accounting information contained in the financial

statements. +ormally, a minimum #cut-off$ rate of return is determined and fi!ed by the

firms which constitutes the accept reject criterion. /roject e!pected to give a return below this rate are rejected, otherwise accepted. In case of several alternative investment

proposals, projects with higher ARR would be preferred to those having lower ARR.

There are two possible interpretations of investment

i. The original cost of investment, and

ii. Average investment.

#ear A-ount R" In La)h

1st

0nd

rd

2th

3th

4th

5th

6th

7th

1

03

3

03

03

030

8/12/2019 Investments Val & Capital

http://slidepdf.com/reader/full/investments-val-capital 2/11

Average investment takes into consideration that the original investment in an asset

diminishes from year to year over its life because of recovering capital cost by way of

depreciation charges assuming that the straight line method is used for chargingdepreciation. In this case the average investment over the lifetime of the asset is half the

depreciable part plus the whole of the non-depreciable part #i.e. scrap value$ of the cost of

asset.

a$ Net Preent *alue .NPV Method"/! The +et /resent 8alue is the difference

between the total present value of future cash inflows and the total present valueof cash outflow. This is the best and scientific method used for evaluating the

capital investment proposals. *nder this method, cash inflows and cash outflows

associated with each project are worked out. The present values of these cash

inflows and outflows are calculated at the rate of return acceptable to themanagement. This rate of return is considering as the cut-off rate and it is

generally determined on the basis of cost of capital suitable adjusted to allow for

the risk element involved in the project. In case of mutually e!clusive project,

the projects, whose +/8 is higher will be selected.

The +et /resent 8alue method considers the time value of money concept. Itconsiders the cash inflows over the entire life of a project. It also considers the total

benefits arising out of proposal over its life. It is useful for selection of mutually

e!clusive projects. 9owever, the accuracy of this method depends on the authenticity ofthe discounting rate for calculating the present values. There is a lot of difference of

opinion regarding the method of calculation. This method may not give satisfactory result

when two projects having different effective life are being compared.

b$ Pro,ita(ilit' Inde0! The +/8 can be used to decide the criteria whether to

:Accept" or Reject the proposal. In case the +/8 is positive the project is

accepted, otherwise not. 9ence, the present value of cash inflows should bemore than the present value of cash outflow for the project. The project is

accepted if +/8 is positive and it is rejected if the +/8 is negative. 9owever, if

the two projects have different investment and different periods, then it isdifficult to use +/8 method. *nder such circumstances the profitability Inde! is

used. The profitability Inde! is calculated as under.

/resent 8alue of cash Inflows /rofitability Inde! ; /resent 8alue of cash <utflows

The project having higher profitability Inde! #/I$ can be selected using this

technique.

c$ Internal Rate o, Return! Internal Rate of return is that rate of return at which

the sum of discounted cash inflows is equal to the sum of discounted cashoutflows. In other words, IRR is the discount rate at which the aggregate present

value of cash inflows is equal to the aggregate present value of cash outflow.

Thus the net present value becomes =ero at the Internal Rate of Return. The

discount rate depends on the initial outlay and cash inflows of the project under

8/12/2019 Investments Val & Capital

http://slidepdf.com/reader/full/investments-val-capital 3/11

consideration. Therefore, it is called as Internal Rate of Return. The IRR is then

compared with the required rate of return i.e. cut-off rate and decision for

investment is taken on that basis. If the IRR is higher than required rate of returnthen the project is accepted and if IRR is lower than the required rate of return,

the project is rejected because it is not profitability.

The IRR considers the time value of money. It also considers the cashflows over the entire life of project or investment. It does not use the cost of

capital to determine the present value, it itself provides a rate of return indicative

of the profitability of the investment proposal. It also leads to increase in share prices and to ma!imi=e shareholder"s wealth as in case of +/8, method.

9owever, calculation of IRR is a time consuming method, project selected on

the basis of IRR may not be profitable.

1"2

Investment Rs.1

>stimated life 1 yrs.

Ta! rate 3?@ear /rofit before depreciation#Rs.$

epreciation#Rs$

/rofit after depreciation#Rs.$

Ta! B 3?

10

2

24

3

3

11

1

1

3

2

2

1303

0

0

1"3

If the net cash outlay of an investment project is Rs. and annual cash inflows for 3

yrs. are Rs.7C Rs.10C Rs.2C and Rs.3 respectively. Dalculate the payback period for victor ltd.

1"4

>!cel trading co. ltd. is considering the purchase of a new machine for the immediate

e!pansion programme. There are three types of machine in the market for this purpose.Their details are as followsE

Particular Machine A

R"

Machine $

R"

Machine C

R"

Dost of machine>stimated savings in scrap per year

>stimated saving in direct wages per year Additional cost of indirect materials per year >!pected saving in indirect materials per annum

Additional cost of maintenance per year

Additional cost of supervision

>stimated life of machine #yrs$

1532

053-1

53

-

1

10353

42-

33

6

4

703

003-03

3

-

3

Ta!ation at 2? of profit

8/12/2019 Investments Val & Capital

http://slidepdf.com/reader/full/investments-val-capital 4/11

@ou are required to advise the management which type of machine should be purchased

on the basis of a'(ac) eriod

1"5

Alpha Ftd. Is producing articles mostly on hand labour and is considering to replace it by

a new machine. There are two alternative models / and G of the new machine. /repare astatement of profitability showing the pay-back period from the following information.

&achine / &achine G

>stimated life of machine

Dost of &achine

>stimated savings in scrap

>stimated savings in direct wagesAdditional cost of &aintenance

Additional cost of )upervision

2 years

Rs.7,

3

4,6

1,0

3 years

Rs.16,

6

6,1,

1,6

Ignore Ta!ation and depreciation.1"6

The director"s elta India Ftd. is considering the purchase of machine to replace amachine which has been in operation for last 3 years. The details relating to available

alternative machines are as followsE

/articulars <ld machineRs.

+ew machineRs.

/urchase price/ower per year

Donsumable stores per year

<ther charges per year

Hages per running hour )elling price per unit

&aterial cost per unit>stimated life of machine

&achine running hrs. /er year

*nits of output per hour

01

2

134.03

0.31yrs

0hrs

02 units

003

53

23

04.034.03

0.31yrs

0hrs

4 units

Ta! rate 2? of net profit

Assuming that the above sales and cost of sales hold goods for the entire economic life of

the machine, suggest which of the two alternatives should be preferredC using averagerate of return .ARR/. epreciation has to be charged according to straight-line method.

1"7 etermine the #1$ /ay back period and #0$ A.R.R. from the following information of a

proposed project.

R"

Dost 3,0,

8/12/2019 Investments Val & Capital

http://slidepdf.com/reader/full/investments-val-capital 5/11

Annual Pro,it a,ter Ta0 and Dereciation

@ear 1 0

2

3

Total

,3,

5,

7,

. 1,1,

,3,

>stimated life ; 3 years. >stimated scrap value ; Rs. 0,.

1"8

The cah ,lo9 trea- ,or t9o alternati*e in*et-ent Tata and $ata are!

Dalculate the #1$ /ayback period, #0$ +et present value using 11? discount rate.

1":

)peedage Dompany ltd. is considering a project, which costs Rs.3.The

estimated salvage value is . Ta! rate is 33?. The company uses straight-linedepreciation and the proposed project has cash flows before depreciation and ta!

#D(T$ as followsE

@ear end Dash inflows #Rs$

#ear Tata

.R"/

$ata

.R"/

10

2

3

#0,,$

3,6,

1,,

6,

4,

#0.1,$

6,4,

6,

4,

6,

8/12/2019 Investments Val & Capital

http://slidepdf.com/reader/full/investments-val-capital 6/11

1

0

2

3

13

0303

0

13

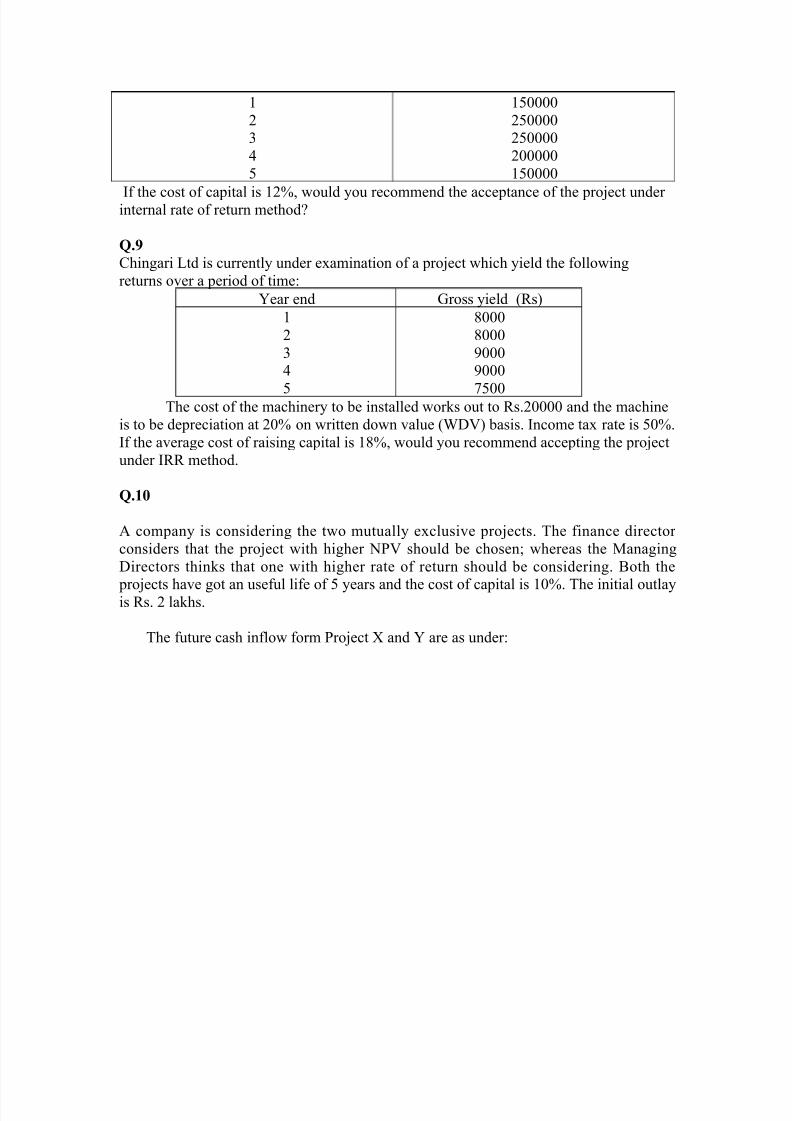

If the cost of capital is 10?, would you recommend the acceptance of the project underinternal rate of return methodJ

1";

Dhingari Ftd is currently under e!amination of a project which yield the following

returns over a period of timeE

@ear end Kross yield #Rs$

1

0

2

3

6

6

77

53 The cost of the machinery to be installed works out to Rs.0 and the machine

is to be depreciation at 0? on written down value #H8$ basis. Income ta! rate is 3?.

If the average cost of raising capital is 16?, would you recommend accepting the project

under IRR method.

1"2<

A company is considering the two mutually e!clusive projects. The finance director

considers that the project with higher +/8 should be chosenC whereas the &anaging

irectors thinks that one with higher rate of return should be considering. oth the

projects have got an useful life of 3 years and the cost of capital is 1?. The initial outlayis Rs. 0 lakhs.

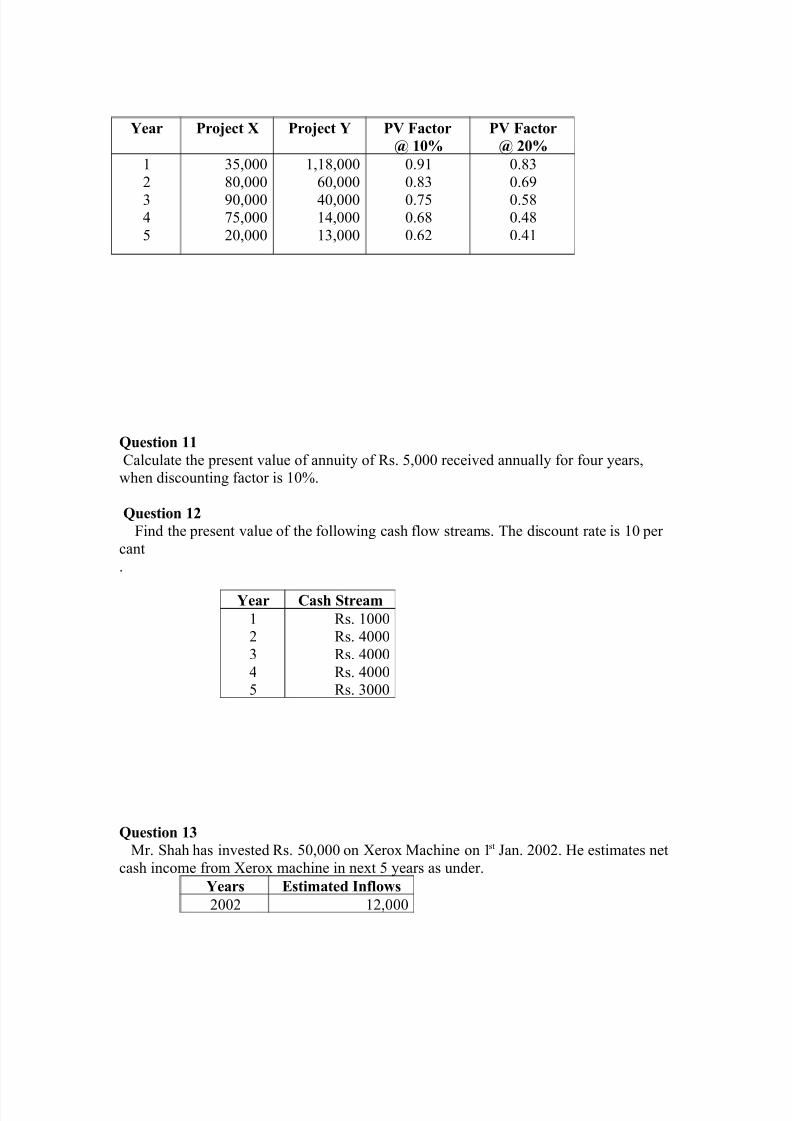

The future cash inflow form /roject L and @ are as underE

8/12/2019 Investments Val & Capital

http://slidepdf.com/reader/full/investments-val-capital 7/11

1uetion 22

Dalculate the present value of annuity of Rs. 3, received annually for four years,when discounting factor is 1?.

1uetion 23

(ind the present value of the following cash flow streams. The discount rate is 1 per

cant

.

1uetion 24

&r. )hah has invested Rs. 3, on Lero! &achine on 1st Man. 00. 9e estimates net

cash income from Lero! machine in ne!t 3 years as under.

#ear Eti-ated In,lo9

00 10,

#ear Pro=ect > Pro=ect # PV ?actor

@ 2<

PV ?actor

@ 3<

1

0

2

3

3,

6,

7,53,

0,

1,16,

4,

2,12,

1,

.71

.6

.53.46

.40

.6

.47

.36.26

.21

#ear Cah Strea-

10

23

Rs. 1Rs. 2

Rs. 2

Rs. 2Rs.

8/12/2019 Investments Val & Capital

http://slidepdf.com/reader/full/investments-val-capital 8/11

0

0203

04

13,

16,03,

,

At the end of 3th

year &achine will be sold at )crap value of Rs. 3,. Advice himwhether his project is viable, considering interest rate of 1? p.a.

1uetion 25

(inance company has introduction a scheme of investment of Rs. 2,. The returnwould be Rs. 6, 7, 1, 11 and 10, in the ne!t five years. The indicated

rate of interest is 1?. Dompute the /resent 8alue of the investment and advise

regarding the investment.

1uetion 26

(ind the present value of the following cash flow if the discount rate is 1?.

)tate whether the investment is worthwhile if the amount of cash outflow presently is

Rs. 13,.

1uetion 27

&iss )onali is considering an investment opportunity which will give her cash inflow of

Rs. 1, Rs. 1,3, Rs. 1,0. Rs. 1,1 N Rs. 2 respectively at the end of each of the

ne!t 3 years. The initial investment is Rs. 2,. if the time, preference rate is 1?. )tatewhether the investment is profitable or not. #/resent value factor at 1? are .771,

.6042, .531, .46 and .407$.

1uetion 28

The share of Ridhi Ftd. #Rs. 1$ was quoting at Rs. 10 on 1.2.00 and the price roseto Rs. 10 on 1.2.03. ividends were received at 1? on th Mune each year. Dost

#ear Cah ?lo9

1

0

2

3

3,

2,

3,5,3

0,3

8/12/2019 Investments Val & Capital

http://slidepdf.com/reader/full/investments-val-capital 9/11

of funds was 1?. Is it a worth-while investment, considering the time value of moneyJ

#/resent value factor at 1? were .77, .604 and .531$.

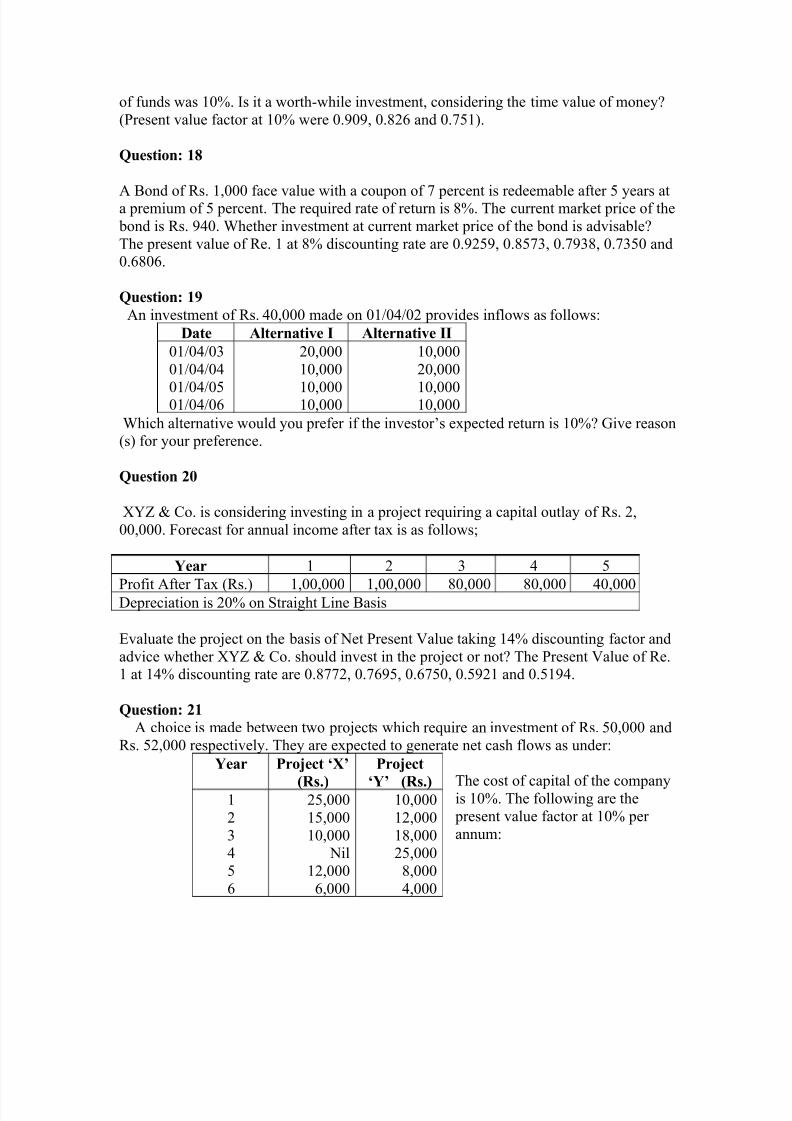

1uetion! 2:

A ond of Rs. 1, face value with a coupon of 5 percent is redeemable after 3 years ata premium of 3 percent. The required rate of return is 6?. The current market price of the

bond is Rs. 72. Hhether investment at current market price of the bond is advisableJ

The present value of Re. 1 at 6? discounting rate are .7037, .635, .576, .53 and.464.

1uetion! 2;

An investment of Rs. 2, made on 120 provides inflows as followsE

Date Alternati*e I Alternati*e II

12

122

123124

0,

1,

1,1,

1,

0,

1,1,

Hhich alternative would you prefer if the investor"s e!pected return is 1?J Kive reason#s$ for your preference.

1uetion 3<

L@O N Do. is considering investing in a project requiring a capital outlay of Rs. 0,

,. (orecast for annual income after ta! is as followsC

#ear 1 0 2 3

/rofit After Ta! #Rs.$ 1,, 1,, 6, 6, 2,epreciation is 0? on )traight Fine asis

>valuate the project on the basis of +et /resent 8alue taking 12? discounting factor and

advice whether L@O N Do. should invest in the project or notJ The /resent 8alue of Re.1 at 12? discounting rate are .6550, .5473, .453, .3701 and .3172.

1uetion! 32

A choice is made between two projects which require an investment of Rs. 3, and

Rs. 30, respectively. They are e!pected to generate net cash flows as underE

The cost of capital of the companyis 1?. The following are the

present value factor at 1? per

annumE

#ear Pro=ect B>’

.R"/

Pro=ect

B#’ .R"/1

0

2

3

4

03,

13,

1, +il

10,

4,

1,

10,

16,03,

6,

2,

8/12/2019 Investments Val & Capital

http://slidepdf.com/reader/full/investments-val-capital 10/11

1uetion 33

A te!tile company is considering two mutually e!clusive investment proposalsC their

e!pected cash flows are given below.

Hhich proposal should be acceptedJ Required rate of return is 1?.

1uetion! 34

A company is considering two mutually e!clusive projects. oth require initial

investment of Rs. 3, each and have a life of five years. The cost of capital of the

company is 13?. The +et Dash inflows after ta! are given belowE

Hhich project should be accepted as per +/8 and IRR methodsJ

#ear Prooal 2 Prooal 3

Initial

Investment1

0

2

3

4

3,,

1,23,

1,23,

1,23,1,23,

1,23,

-

3,3,

1,,

1,1,

1,,1,3,

1,4,

1,3,

#ear Prooal

A .R"/

Prooal $

.R"/

10

23

13,14,

17,

15,30,

0,16,3

14,

15,313,

8/12/2019 Investments Val & Capital

http://slidepdf.com/reader/full/investments-val-capital 11/11

1uetion 35

A choice is to be made between two investment proposal which require an equal

investment of Rs. 3, , and e!pected to generate net cash flows as underE

The cost of Dapital of the company is 1?. The following are the present value factor B1? per annum.

#ear Prooal I.R"/

Prooal II.R"/

1

0

23

4

0,3,

1,3,

1,,

+il1,0,

4,

1,,

1,0,

1,6,

0,3,6,

2,