investment in ipo an analysis (initial public offer) by :- gaurav bhut

TRANSCRIPT

1

A

Project Report

On

“INVESTMENT IN IPO : AN ANALYSIS”

Submitted By

Bhut Gaurav B.

Enrollment No. : 137730592002

Academic Year : 2010-11

MBA Semester III

Submitted To

Gujarat Technological University

PREPARE BY :- GAURAV BHUT 2

DECLARATION

To,

The Director,

Sunshine group of institutions,

Behind Rangoli park,

Mota mahuva,

Kalawad Road,

Rajkot-

Respected Sir,

I the undersigned hereby declare that the project report entitled ―INVESTMENT

IN IPO : AN ANALYSIS‖ is an original work developed and submitted by me

under the guidance of Prof. Krishna joshi

The empirical findings in this project report are not copied from any report and

are true and best of my knowledge.

DATE:

PLACE: Rajkot

Enroll. No: 137730592002

Thanking You,

Gaurav bhut

Gaurav Bhut

PREPARE BY :- GAURAV BHUT 3

ACKNOWLEDGEMENT

It is great pleasure for me to acknowledge those who have contributed to this project directly

or indirectly. It would be unfair and unjust if I fail to show my appreciation and gratitude.

I would like to show my profound gratitude to the project guide of prof.krishana joshi whose

guidance encouraged me to carry out the project systematically. I also thank my faculty

members for their constant support and guidance because without the theoretical knowledge

imparted by them, it was not possible to have it applied in practical life.

Last but not the least; I would like to thank my parents for their undying faith in me and my

friends for their constant encouragement.

Thanking You,

Gaurav bhut

Gaurav Bhut

PREPARE BY :- GAURAV BHUT 4

PREFACE

When I am standing on the threshold of 21st century, professionalism is getting on every

body‘s nerves quickly. Trying to cope up with this pace, educational institutions rendering

professional degree courses are growing out like mushrooms.

Practical training is a tool to develop conceptual and analytical ability in the student.

According to M.B.A. schedule, students are required to make a research project on an

industry as a part of practical study.

In accordance with this, I have also made my research project on ‖INVESTMENT IN IPO:

AN ANALYSIS‖. In this, many leading companies are including for research. Indian IPO

market is the booming market in the corporate world of India.

PREPARE BY :- GAURAV BHUT 5

INDEX

SR NO PARTICULARS PAGE

NO

1 EXECUTIVE SUMMARY 1

CHAPTER 1

INTRODUCTION

2.1 SEBI GUIDELINES 5

2.2 PROCEDURE OF IPO 6

2.3 BUY BACK OF SHARES 14

2.4 ROLE OF VARIOUS INTERMEDIARIES IN IPO 16

2.5 IPO GRADING 18

CHAPTER 2

LITERATURE REVIEW

3.1 BACKGROUND OF THE TOPIC 21

3.2 RATIONAL OF THE STUDY 22

3.3 REVIEW OF EXISTING LITERATURE 25

3.4 OBJECTIVES OF THE STUDY 27

CHAPTER 3

RESEARCH METHODOLOGY

PREPARE BY :- GAURAV BHUT 6

4.1 DATA COLLECTION METHOD 30

4.2 HYPOTHESIS TESTING 31

4.3 LIMITATIONS OF THE STUDY 32

4.4 FUTURE SCOPE OF THE STUDY 33

CHAPTER 4

ANALYSIS AND INTREPRETATION

5.1 FUTURE CAPITAL HOLDINGS LTD 35

5.2 KIRI DYES CHEMICAL LTD 40

5.3 RELIANCE POWER 45

5.4 TITAGARH WAGON 48

CHAPTER 5

6 FINDINGS AND SUGGESTIONS 54

7 CONCLUSION 58

8 BIBLIOGRAPHY 60

PREPARE BY :- GAURAV BHUT 7

EXECUTIVE SUMMARY

This project gave me a great insight about the IPO and its Process. The purpose of this

Project was to understand the IPOs; buyback of shares; IPO Grading and Reforms in IPO

Process.

This project was a learning experience for me of IPO and its valuation. I began my study by

going through the SEBI guidelines regarding eligibility norms, pricing structure,

requirements of the promoters and their obligations, post issue obligations, book building

guidelines etc. Proper study of few IPOs has been done by going through their past

financials, business structure, investments, expansion strategies, growth potential, valuations

etc.

The Project report starts with defining the various public issues with the need for the

company to take out an IPO. It goes on further to explain the advantages of an IPO. It

analyses in detail the Indian IPO Scenario. It explains the evolution of the IPO in India and

explains how the scene has changed dramatically after liberalization esp. after the

introduction of book building process.

PREPARE BY :- GAURAV BHUT 8

PREPARE BY :- GAURAV BHUT 9

INTRODUCTION

A company can raise capital through issue of shares or debentures. The various types of

issues are: Public Issue, Rights Issue, Bonus Issue, Private Placement and Bought out Deal.

There can be two kinds of public issues, namely:

Initial Public Offer (IPO)

Further Public Offer (FPO)

Classification of Issues:

IPO

An Initial Public Offer (IPO) is the selling of securities to the public in the primary market. It

is when an unlisted company makes either a fresh issue of securities or an offer for sale of its

existing securities or both for the first time to the public. This paves way for listing and

trading of issuer‘s securities. The sale of securities can be through book building or normal

public issue.

FPO

Further Public Offers are issued by companies or corporate bodies whose shares are already

being traded in the capital market and they are issuing fresh shares either to fund the

expansion of their existing business or to invest into other business activities.

PREPARE BY :- GAURAV BHUT 10

ADVANTAGES OF IPO:

Facilitates future funding by means of subsequent public offerings

Enables valuation of company

Provides liquidity to existing shares

Increases the visibility and reputation of the company

Commands better pricing than placement with few investors

Enables the company to offer its shares as purchase consideration or as an exchange

for the shares of another company

DISADVANTAGES OF IPO:

Dilution of Stake makes co vulnerable to future takeovers

Involves substantial Expenses

Need to make continuous disclosures

Increased regulatory monitoring

Listing fees and Documentations

Cost of maintaining Investor relations

Takes substantial amount of management time and efforts

PREPARE BY :- GAURAV BHUT 11

2.1 SEBI GUIDELINES ON IPO GRADING:

No unlisted company shall make an IPO of equity shares or any other security which may

be converted into or exchanged with equity shares at a later date, unless the following

conditions are satisfied as on the date of filing of Prospectus (in case of fixed price issue)

or Red Herring Prospectus (in case of book built issue) with ROC:

The unlisted company has obtained grading for the IPO from at least one credit

rating agency;

Disclosures of all the grades obtained, along with the rationale/description

furnished by the credit rating agencies for each of the grades obtained, have been

made in the Prospectus (in case of fixed price issue) or Red Herring Prospectus

(in case of book built issue); and

The expenses incurred for grading IPO have been borne by the unlisted company

obtaining grading for IPO.

Most of the market analysts have welcomed this move of SEBI as it will help the investors in

a volatile market to know whether the merchant banker has carried the exercise in

determining the price of an issue in a proper manner or not. It will also help the investors in

knowing whether the price of the issue is justified or not. They even said that management of

a good company will never get afraid of getting graded of their IPOs if they are good. The

only demerit of this step by the SEBI as said by many experts is that there will be a

slowdown in the number of IPOs coming out as grading will be a bit lengthy process and

there will be a cost-factor attached to it also.

PREPARE BY :- GAURAV BHUT 12

2.2 PROCEDURE FOR IPO:

Fixed Pricing versus True Pricing (Book- Building)

The traditional method of doing IPOs is the fixed price offering. Here, the issuer and the

merchant banker agree on an ―issue price‖. Then the investor has a choice of filling in an

application form at this price and subscribing to the issue. Extensive research has revealed

that the fixed price offering is a poor way of doing IPOs. Fixed price offerings, all over the

world, suffer from `IPO under pricing'. In India, on average, the fixed-price seems to be

around 50% below the price at first listing; i.e. the issuer obtains 50% lower issue proceeds

as compared to what might have been the case. This average masks a steady stream of

dubious IPOs who get an issue price which is much higher than the price at first listing.

Hence fixed price offerings are weak in two directions:

dubious issues get overpriced and

Good issues get under priced.

2.2.1 Book building.

A mechanism period for which the IPO is open, bids is collected from investors at various

prices which are above or equal to the floor price (the minimum price). The final price of the

share is determined after the bid closing date, based on certain evaluation criteria.

The SEBI (Disclosure and Investor Protection) Guidelines, 2000, define the term `book-

building' in a rather complex language as "a process undertaken by which a demand for the

securities proposed to be issued by a body corporate is elicited and built-up and the price for

such securities is assessed for determination of the quantum of such securities to be issued by

means of a notice, circular, advertisement, document or information memoranda or offer

document.''

PREPARE BY :- GAURAV BHUT 13

Book building process is a common practice used in most developed countries for marketing

a public offer of equity shares of a company. However, Book building acts as scientific as

well as flexible price discovery method through which a consensus price of IPO‘s may be

determined by the issuer company along with the Book Running Lead Manager (i.e.

merchant banker) on the basis of feedback received from individual investors as well as most

informed investors (who are institutional and corporate investors like, UTI, LICI, GICI, FIIs,

and SFCI etc). The method helps to make a correct evaluation of a company‘s potential and

the price of its shares.

In simple terms, book-building is a mechanism by which the issue price is discovered on the

basis of bids received from syndicate members/brokers and not by the issuers/merchant

bankers.

An Issuer Company can issue capital through book building in following two ways:

75% Book Building process

–

Under this type of public offer, the issue of securities has to be categorized into:

Placement portion category

Net offer to the public

The option of 75% Book Building is available to all body corporate that are otherwise

eligible to make an issue of capital to the public. The securities issued through the book

building process are indicated as 'placement portion category' and securities available to

public are identified as 'net offer to public'. In this option, underwriting is mandatory to the

extent of the net offer to the public. The issue price for the placement portion and offers to

public are required to be same

PREPARE BY :- GAURAV BHUT 14

100% of the net offer to the public through Book Building process –

In the 100% of the net offer to the public, entire issue is made through Book Building

process. However, there can be a reservation or firm allotment to a maximum of 5% of the

issue size for the permanent employees, shareholders of the company or group companies,

persons who, on the date of filing of the draft offer document with the Board, have business

association, as depositors, bondholders and subscribers to services, with the issuer making an

initial public offering.

The number of bidding centers, in case of 75% book building process should not be less than

the number of mandatory collection centers specified by SEBI. In case of 100% book

building process, the bidding centers should be at all the places where the recognized stock

exchanges are situated.

Book Building Process in India

The steps which are usually followed in the book building process can be summarized below:

(1) The issuer company proposing an IPO appoints a lead merchant banker as a BRLM.

(2) Initially, the issuer company consults with the BRLM in drawing up a draft prospectus

(i.e. offer document) which does not mention the price of the issues, but includes other

details about the size of the issue, past history of the company, and a price band. The

securities available to the public are separately identified as ―net offer to the public‖.

(3) The draft prospectus is filed with SEBI which gives it a legal standing.

(4) A definite period is fixed as the bid period and BRLM conducts awareness campaigns

like advertisement, road shows etc.

(5) The BRLM appoints a syndicate member, a SEBI registered intermediary to underwrite

the issues to the extent of ―net offer to the public‖.

(6) The BRLM is entitled to remuneration for conducting the Book Building process.

PREPARE BY :- GAURAV BHUT 15

(7) The copy of the draft prospectus may be circulated by the BRLM to the institutional

investors as well as to the syndicate members.

(8) The syndicate members create demand and ask each investor for the number of shares

and the offer price.

(9) The BRLM receives the feedback about the investor‘s bids through syndicate members.

(10) The prospective investors may revise their bids at any time during the bid period.

(11) The BRLM on receipts of the feedback from the syndicate members about the bid price

and the quantity of shares applied has to build up an order book showing the demand for the

shares of the company at various prices. The syndicate members must also maintain a record

book for orders received from institutional investors for subscribing to the issue out of the

placement portion.

(12) On receipts of the above information, the BRLM and the issuer company determine the

issue price. This is known as the market-clearing price.

(13) The BRLM then closes the book in consultation with the issuer company and determine

the issue size of (a) placement portion and (b) public offer portion.

(14) Once the final price is determined, the allocation of securities should be made by the

BRLM based on prior commitment, investor‘s quality, price aggression, earliness of bids etc.

The bid of an institutional bidder, even if he has paid full amount may be rejected without

being assigned any reason as the Book Building portion of institutional investors is left

entirely at the discretion of the issuer company and the BRLM.

(15) The Final prospectus is filed with the registrar of companies within 2 days of

determination of issue price and receipts of acknowledgement card from SEBI.

(16) Two different accounts for collection of application money, one for the private

placement portion and the other for the public subscription should be opened by the issuer

company.

PREPARE BY :- GAURAV BHUT 16

(17) The placement portion is closed a day before the opening of the public issue through

fixed price method. The BRLM is required to have the application forms along with the

application money from the institutional buyers and the underwriters to the private placement

portion.

(18) The allotment for the private placement portion shall be made on the 2nd

day from the

closure of the issue and the private placement portion is ready to be listed.

(19) The allotment and listing of issues under the public portion (i.e. fixed price portion)

must be as per the existing statutory requirements.

(20) Finally, the SEBI has the right to inspect such records and books which are maintained

by the BRLM and other intermediaries involved in the Book Building process

Pricing

Before establishment of SEBI in 1992, the quality of disclosures in the offer documents was

very poor.

The main drawback of free pricing was the process of pricing of issues. The issue price was

determined around 60-70 days before the opening of the issue and the issuer had no clear

idea about the market perception of the price determined.

In Book Building the price is determined on the basis of demand received or at price above

or equal to the floor price.

The Allotment Process through Book-building:

Step1-The Company will 'discover' its price

Earlier, the company determined a fixed price for the stock issue. The issue was marketed to

the general public through advertisements and a media campaign.

Today, companies prefer a book building process. Book building is the process of price

discovery. That means there is no fixed price for the share. Instead, the company issuing the

PREPARE BY :- GAURAV BHUT 17

shares comes up with a price band. The lowest price is referred to as the floor and the

highest, the cap. Bids are then invited for the shares. Each investor states how many shares

s/he wants and what s/he is willing to pay for those shares (depending on the price band). The

actual price is then discovered based on these bids.

Step2-Players of the game

Three classes of investors can bid for the shares:

Qualified Institutional Buyers: QIBs include mutual funds and Foreign Institutional

Investors. At least 50% of the shares are reserved for this category.

Retail investors: Anyone who bids for shares under Rs 50,000 is a retail investor. At

least 25% is reserved for this category.

The balance bids are offered to high net worth individuals and employees of the

company.

Individuals who apply for the IPO put in their bids.

The process is transparent. One can check on the issue subscription at the BSE and NSE Web

sites.

After evaluating the bid prices, the company will accept the lowest price that will allow it to

dispose the entire block of shares. That is called the cut-off price.

The process can be illustrated with an example:

Number of shares issued by the company = 100.

Price band = Rs 30 - Rs 40.

If individuals have bid for prices as follows:

PREPARE BY :- GAURAV BHUT 18

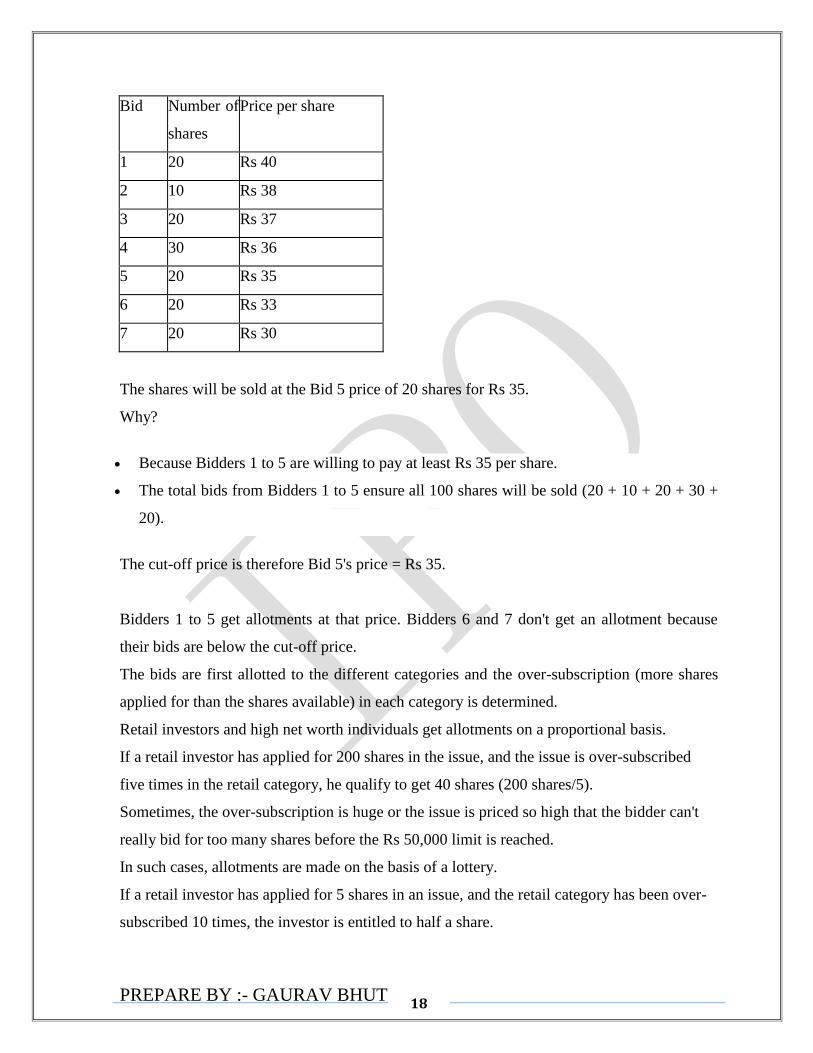

Bid Number of

shares

Price per share

1 20 Rs 40

2 10 Rs 38

3 20 Rs 37

4 30 Rs 36

5 20 Rs 35

6 20 Rs 33

7 20 Rs 30

The shares will be sold at the Bid 5 price of 20 shares for Rs 35.

Why?

Because Bidders 1 to 5 are willing to pay at least Rs 35 per share.

The total bids from Bidders 1 to 5 ensure all 100 shares will be sold (20 + 10 + 20 + 30 +

20).

The cut-off price is therefore Bid 5's price = Rs 35.

Bidders 1 to 5 get allotments at that price. Bidders 6 and 7 don't get an allotment because

their bids are below the cut-off price.

The bids are first allotted to the different categories and the over-subscription (more shares

applied for than the shares available) in each category is determined.

Retail investors and high net worth individuals get allotments on a proportional basis.

If a retail investor has applied for 200 shares in the issue, and the issue is over-subscribed

five times in the retail category, he qualify to get 40 shares (200 shares/5).

Sometimes, the over-subscription is huge or the issue is priced so high that the bidder can't

really bid for too many shares before the Rs 50,000 limit is reached.

In such cases, allotments are made on the basis of a lottery.

If a retail investor has applied for 5 shares in an issue, and the retail category has been over-

subscribed 10 times, the investor is entitled to half a share.

PREPARE BY :- GAURAV BHUT 19

Since that isn't possible, it may then be decided that every 1 in 2 retail investors will get

allotment. The investors are then selected by lottery and the issue allotted on a proportional

basis among.

Reverse Book Building

Reverse book-building is a mechanism by which companies listed on a stock exchange can

delist their shares. The reasons for delisting may be several and sometimes intentional.

The reverse book building is an efficient price discovery mechanism of de-listing of

securities, which is provided for capturing the sell orders on online basis from the

shareholders through respective BRLM. In the reverse book-building scenario, the acquirer

or promoter of a company offers to get back shares from the shareholders. It is a mechanism

where, during the period for which the reverse book building is open, offers are collected at

various prices, which are above or equal to the floor price from the share holders through

trading members appointed by the acquirer or promoter of a company. The reverse book

building price (i.e. final price/ exist price) is determined by BRLM in consultation with the

acquirer or promoter of the company after the offer closing date in accordance with the SEBI

(De-listing of Securities) Guidelines, 2003. which desires to get de-listed, in accordance to

book building process. The offer price has a floor price, which is fixed for de-listing of

securities below which no offer can be accepted. The floor price is the average of 26 weeks

traded price quoted on the stock exchange where the shares of the company are most

frequently traded preceding 26 weeks from the date of public announcement is made. There

is no ceiling on the maximum price.

PREPARE BY :- GAURAV BHUT 20

2.3 BUY BACK OF SHARES:

It is a process whereby a company purchases its own shares or other specified securities from

the holders thereof for improving the earnings per share (EPS), or to improve return on

capital or return on net worth and to enhance the long-term shareholder value, among other

things.

Objectives of buy back:

To increase promoters holding

Increase earning per share

Rationalize the capital structure by writing off capital not represented by available

assets.

Support share value

To thwart takeover bid

To pay surplus cash not required by business

Comment – It is an interesting fact to note that MNCs are using buyback process as the best

strategy to maintain their share price in a bear run by buying back the shares from the open

market at a premium over the prevailing market price.

Procedure for Buy Back:

Where a company proposes to buy back its shares, it shall, after passing of the

special/Board resolution make a public announcement at least one English National

Daily, one Hindi National daily and Regional Language Daily at the place where the

registered office of the company is situated.

The public announcement shall specify a date, which shall be ―specified date‖ for the

purpose of determining the names of shareholders to whom the letter of offer has to

be sent.

A public notice shall be given containing disclosures as specified in Schedule I of the

SEBI regulations.

PREPARE BY :- GAURAV BHUT 21

A draft letter of offer shall be filed with SEBI through a merchant Banker. The letter

of offer shall then be dispatched to the members of the company.

A copy of the Board resolution authorizing the buy back shall be filed with the SEBI

and stock exchanges.

The date of opening of the offer shall not be earlier than seven days or later than 30

days after the specified date

The buy back offer shall remain open for a period of not less than 15 days and not

more than 30 days.

A company opting for buy back through the public offer or tender offer shall open an

escrow Account.

Comment – MNCs are taking advantage of the depressed market conditions to mop

up the shares. There is nothing legally wrong in buying back shares, but it should be

by paying a fair price to minority shareholders.

Difference between Delisting and Buyback:

De-listing is different from ―buy back‖ of securities in which the securities of a company are

extinguished with consequent reduction of capital of the company. In the case of de-listing

there is no reduction of capital. It is needless to mention that in the case of buy back

securities, the company itself is the acquirer and hence provides the funds for buy back. In

the case of de-listing, the securities are acquired by a person other than the company and who

could be the promoter, majority shareholder or a person in control of the management and the

funds have to be provided by that acquirer.

PREPARE BY :- GAURAV BHUT 22

2.4 ROLE OF VARIOUS INTERMEDIARIES IN IPO:

Intermediary‘s help corporations design securities that will be attractive to investors, buy

these securities from the corporations, and then resell them to savers in the primary markets.

Merchant Bankers/ Lead Manager:

Merchant bankers play an important role in issue management process. Lead managers have

to ensure correctness of the information furnished in the offer document. They have to ensure

compliance with SEBI rules and regulations as also Guidelines for Disclosures and Investor

Protection. To this effect, they are required to submit to SEBI a due diligence certificate

confirming that the disclosures made in the draft prospectus or letter of offer are true, fair and

adequate to enable the prospective investors to make a well informed investment decision.

The role of merchant bankers in performing their due diligence functions has become even

more important with the strengthening of disclosure requirements and with SEBI giving up

the vetting of prospectuses. Their functions are:

To act as intermediaries between the company seeking to raise money and the

investors. They must possess a valid registration from SEBI enabling them to do this

job.

They are responsible for complying with the formalities of an issue, like drawing up

the prospectus and marketing the issue.

If it is a book building process, the lead manager is also in charge of it. In such a case,

they are also called Book Running Lead Managers.

Post issue activities, like intimation of allotments and refunds, are their responsibility

as well.

PREPARE BY :- GAURAV BHUT 23

Underwriters:

Underwriters are required to register with SEBI in terms of the SEBI (Underwriters) Rules

and Regulations, 1993. In addition to underwriters registered with SEBI in terms of these

regulations, all registered merchant bankers in categories I, II and III and stockbrokers and

mutual funds registered with SEBI can function as underwriters. Part III gives further details

of registration of underwriters. In 1996-97, the SEBI (Underwriters) Regulations, 1993 were

amended mainly pertaining to some procedural matters.

Bankers to an Issue:

Scheduled banks acting as bankers to an issue are required to be registered with SEBI in

terms of the SEBI (Bankers to the Issue) Rules and Regulations, 1994. These regulations lay

down eligibility criteria for bankers to an issue and require registrants to meet periodic

reporting requirements. Part III gives further details of registration of bankers to an issue.

Portfolio managers:

Portfolio managers are required to register with SEBI in terms of the SEBI (Portfolio

Managers) Rules and Regulations, 1993. The registered portfolio managers exclusively carry

on portfolio management activities. In addition all merchant bankers in categories I and II

can act as portfolio managers with prior permission from SEBI. Part III gives further details

of the registration of portfolio managers.

Registrars to an Issue and Share Transfer Agents:

Registrars to an issue (RTI) and share transfer agents (STA) are registered with SEBI in

terms of the SEBI (Registrar to the Issue and Share Transfer Agent) Rules and Regulations,

1993. Under these regulations, registration commenced in 1993-94 and is granted under two

categories: category I - to act as both registrar to the issue and share transfer agent and

category II - to act as either registrar to an issue or share transfer agent. With the setting up of

the depository and the expansion of the network of depositories, the traditional work of

registrars is likely to undergo a change.

PREPARE BY :- GAURAV BHUT 24

2.5 IPO GRADING:

IPO grading (initial public offering grading) is a service aimed at facilitating the assessment

of equity issues offered to public. The grade assigned to any individual issue represents a

relative assessment of the ‗fundamentals‘ of that issue in relation to the other listed equity

securities in India. IPO grading is positioned as a service that provides ‗an independent

assessment of fundamentals‘ to aid comparative assessment that would prove useful as an

information and investment tool for investors. Moreover, such a service would be particularly

useful for assessing the offerings of companies accessing the equity markets for the first time

where there is no track record of their market performance.

IPO grade assigned to any issue represents a relative assessment of the ‗fundamentals‘ of that

issue in relation to the universe of other listed equity securities in India. This grading can be

used by the investor as tool to make investment decision. The IPO grading will help the

investor better appreciate the meaning of the disclosures in the issue documents to the extent

that they affect the issue‘s fundamentals. Thus, IPO grading is an additional investor

information and investment guidance tool.

Credit Rating agencies (CRAs) like ICRA, CRISIL, CARE and Fitch Ratings who are

registered with SEBI will carry out IPO grading. SEBI does not play any role in the

assessment made by the grading agency. The grading is intended to be an independent and

unbiased opinion of that agency. IPO grading is not mandatory but is optional and the

assigned grade would be a one time assessment done at the time of the IPO and meant to aid

investors who are interested in investing in the IPO. The grade will not have any ongoing

validity.

PREPARE BY :- GAURAV BHUT 25

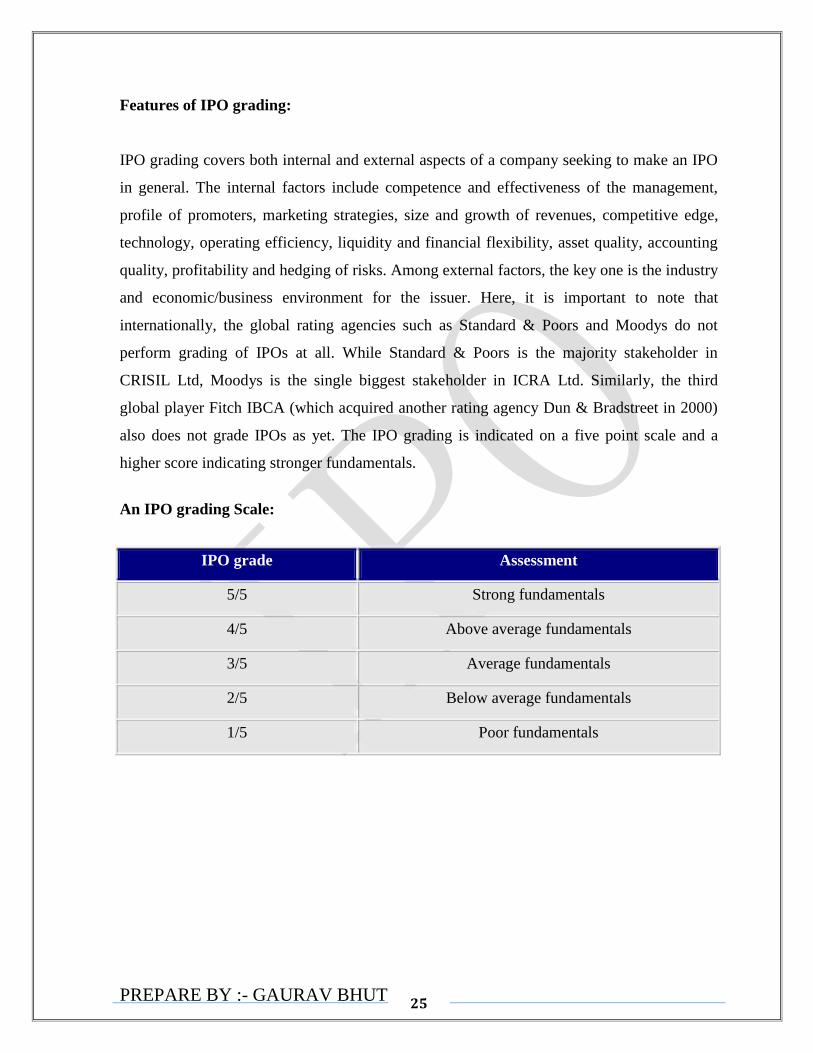

Features of IPO grading:

IPO grading covers both internal and external aspects of a company seeking to make an IPO

in general. The internal factors include competence and effectiveness of the management,

profile of promoters, marketing strategies, size and growth of revenues, competitive edge,

technology, operating efficiency, liquidity and financial flexibility, asset quality, accounting

quality, profitability and hedging of risks. Among external factors, the key one is the industry

and economic/business environment for the issuer. Here, it is important to note that

internationally, the global rating agencies such as Standard & Poors and Moodys do not

perform grading of IPOs at all. While Standard & Poors is the majority stakeholder in

CRISIL Ltd, Moodys is the single biggest stakeholder in ICRA Ltd. Similarly, the third

global player Fitch IBCA (which acquired another rating agency Dun & Bradstreet in 2000)

also does not grade IPOs as yet. The IPO grading is indicated on a five point scale and a

higher score indicating stronger fundamentals.

An IPO grading Scale:

IPO grade Assessment

5/5 Strong fundamentals

4/5 Above average fundamentals

3/5 Average fundamentals

2/5 Below average fundamentals

1/5 Poor fundamentals

PREPARE BY :- GAURAV BHUT 26

Cost Involved In IPO Grading:

Though nothing has been declared officially but most of the credit rating has said that IPO-

grading would not cost much to the issuers. They would be charging 10 basis points of the

amount to be raised with a ceiling of about Rs 10-15 lakhs. Thus, even in the case of a mega

IPO, there would be a cap on fees, he noted. Around 100 IPOs hit the market on an average

every year. However, despite this seemingly big number, the total receipts for the entire

rating industry on account of grading fees would be only about Rs 10-15 crore.

PREPARE BY :- GAURAV BHUT 27

3.1 BACKGROUND OF THE TOPIC

Early Phase: 1992-1995 (Fixed Pricing)

The initiation of the process of reform in India also would not have been possible without

changes in the regulatory framework. The New Economic policy (1991) led to a major

change in the regulatory framework of the capital market in India. The Capital Issues

(Control) Act 1947 was repealed and the Office of the Controller of Capital Issues (CCI) was

abolished. The Securities and Exchange Board of India (SEBI), established in 1988 and

armed with statutory powers in 1992, came to be established as the regulatory body with the

necessary authority and powers to regulate and reform the capital market. SEBI came to be

recognized as a regulatory body for the capital market after the abolition of the CCI. The

control on pricing of capital issue has been abolished and easy access is provided to the

capital market. Initial Public Issue caught the attention of general public only after the

success of Reliance, when millions of small investors made huge returns which were unheard

of till then. Dhirubhai Ambani was the first promoter who raised huge amounts through the

public issue route to finance large facilities.

The issue process was smoothened, procedures were simplified and free pricing was allowed,

although with certain restrictions, The Indian market had the concept of par value of equity

shares, and anything above par was considered premium. The only companies that were

allowed to come with premium issues were those, which had a three year profit-track record

for the preceding five years. New companies without this record could float premium issues

if their promoting companies had the same track record and they had to hold 50% of the post

issue capital. Any new company floated by first generation entrepreneurs could only issue

equity at par. There was no restriction about prices in a premium issue.

The offer was always at a fixed price, whether premium or par. The companies had to

appoint intermediaries like merchant bankers, registrars, bankers etc. Merchant bankers had

the responsibility of fixing the prices, in consultation with the company, carrying out with

due diligence, preparing the prospectus (offer documents) etc. The prospectus had to be

submitted to SEBI for getting scrutiny.

PREPARE BY :- GAURAV BHUT 28

The trend continued in the early nineties as many large projects were launched after the

economy was liberalized. Many of these companies came out with public issues and the retail

participation increased dramatically. But many of the companies which raised money during

this period just disappeared without a trace.

Late Liberalization Period: 1996-2005 (Book Building)

The late nineties and the first few years of the current decade did not see much activity in the

primary market even though we saw a huge bull run led by technology stocks at the turn of

the decade. The bad experiences of retail investors kept them away from the market and

made it difficult for companies to launch successful issues. The corporate sector was

recovering from the damage caused by large capacity expansions and new projects set up in

the nineties.

The dormant primary issues market came alive after 2003 mostly because of the divestment

programme of the government. The issue of Maruti Udyog, through which the government

sold part of its stake in the company, rekindled retail investor interest in the primary market.

The issue was made at a very reasonable price and investors made very good returns

immediately.

The year 2004 saw the primary market activity at its historic peak as some large private

companies also came out with issues. Further divestment by the government; including the

largest ever issue by an Indian company from ONGC, attracted more retail investors into the

market. The IPO market continues to buzz in the current year as well. Taking advantage of

the strength in the secondary market, many high profle companies are lining up to raise

money from the market. The year started with the issue from Jet Airways which attracted a

lot of interest from investors. As a result of tougher regulations, the quality of the issues has

gone up substantially.

PREPARE BY :- GAURAV BHUT 29

2006 onwards scenario:

India's IPO market emerged as the eighth largest with $7.23 billion (Rs 30,000 crore) in net

proceeds through 78 public issues, global research and consultancy firm Ernst & Young said

in its Global IPO report. Across the world, the companies raised $246 billion, up from $167

billion in 2005, through a total of 1,729 IPOs, led by Chinese companies at the top with net

proceeds of $56.6 billion. However, the biggest number of IPOs came from the United States

with 187 offerings, followed by Japan with 185 and China with 175 IPOs. According to the

study, India's increasing number of larger deals has been driven by the growth of Indian

corporations and their need for additional capital for potential acquisitions. In 2007 Indian

IPOs continue to surge in numbers. Continued strength is expected in the real estate and

energy sector. "The rapid growth in emerging market economies has resulted in a migration

of capital from the developed economies into the emerging markets," E&Y said.

The localization trend in India is evidenced by several billion-dollar IPOs hosted by Indian

exchanges. In 2006, India's largest IPO, Reliance Petroleum raised $1.8 billion, followed by

the oil production and exploration company, Cairn Energy, which raised $1.3 billion with

both companies listing on domestic exchanges.

However, some Indian companies are also listing abroad, especially London, Singapore and

Luxembourg, primarily for higher valuations and visibility, the report noted.

The private equity rush into India is creating the potential for many IPO exits. In 2006,

private equity firms invested more than $7 billion in India. Top global private equity funds as

well as local funds, have been key drivers of Indian IPO markets.

PREPARE BY :- GAURAV BHUT 30

RATIONAL OF THE STUDY:

To navigate new investors for primary market and for proper investment in IPO.

To learn the procedure of filling the IPO‘s, its basic norms and regulation.

To know the guidelines of SEBI for IPO‘s.

To understand the various Pricing techniques.

To understand practically the fundamental and Technical analysis of IPO‘s.

PREPARE BY :- GAURAV BHUT 31

REVIEW OF EXISTING LITERATURE:

The literature review on IPOs can be divided in the following main heads-

a) Reason and timing of going public.

Going public marks a watershed in the life cycle of the firm. While increased equity can

support the firm‘s future plans of growth, the trade off for the firm is that of increased public

scrutiny.

Brealy and Myers (2005) state that in the context of USA the firms may seek private

equity in their initial years and only later go for public issues.

Pagano, Panetta and Zingales (1998) in their study of Italian firms, find that firms

going public are not seeking money for growth but are rebalancing their accounts

after high investment and growth.

Lerner (1994) found that there are times (windows of opportunity) when the markets

could be extremely optimistic about a particular industry and it may be a good time

for the firms in that industry to go public.

The post IPO period sees a reduction in leverage as well as investment. They state that going

public is a conscious choice that some firms make while some others prefer to remain

private. Thus going public is not a natural element in the life cycle of a firm.

PREPARE BY :- GAURAV BHUT 32

b) Valuation of IPOs.

Benveniste and Spindt (1989) find that under writers try to resolve the information

asymmetry problem between the firm and the investors by providing an incentive to

the investors to reveal their private information about the firm.

Kim and Ritter (1999) in their study of 190 firms find that under writers forecast the

next years earnings numbers and multiply them with PE ratios of comparable firms in

the industry to get the approximate price of the IPO. However they also found that PE

ratios using historical earnings numbers do not give accurate results whereas when

forecasted earnings numbers are used then the valuation is much more accurate.

Purnanandam and Swaminathan (2002) say that IPOs are priced 50% higher than

industry peers. Also they find that more the IPO is overpriced with respect to its

peers, worse is its long term performance.

c) Allocation mechanism.

The allocation mechanisms are specified by the regulators in different countries. Loughran,

Ritter and Rydqvist (1994) find 3 main categories across countries-Auctions, Fixed price

offers and Book Building. Sherman (2005) finds that Book building is a superior mechanism

for selling IPOs rather than auctions.

PREPARE BY :- GAURAV BHUT 33

3.4OBJECTIVES OF THE STUDY:

Main Objectives:

An attempt has been made to analyze the various IPOs and recommend others to

invest in good initial public offerings after thorough research of financial statements

of the companies.

Sub objectives:

To understand various dimensions and problems in IPO process

To understand post IPO performance.

To analyze financial position of Companies as depicted in its Annual report as it serve

an important basis for investors to judge company performance and future prospects.

PREPARE BY :- GAURAV BHUT 34

PREPARE BY :- GAURAV BHUT 35

RESEARCH METHODOLOGY:

Descriptive Research.

Descriptive research is used to obtain information concerning the current status of the

phenomena to describe ―what exists‖ with respect to variables or conditions in a situation.

Descriptive research, also known as statistical research, describes data and characteristics

about the population or phenomenon being studied. Descriptive research answers the

questions who, what, where, when and how. Although the data description is factual,

accurate and systematic, the research cannot describe what caused a situation.

Analytical Research

Analytical research takes descriptive research one stage further by seeking to explain the

reasons behind a particular occurrence by discovering causal relationships. Once causal

relationships have been discovered, the search then shifts to factors that can be changed

(variables) in order to influence the chain of causality.

PREPARE BY :- GAURAV BHUT 36

4.1 DATA COLLECTION METHOD:

The task of data collection begins after a research problem has been defined and research

design/plan chalked out. While designing about the method of data collection to be used for

the study, the researcher should keep in mind two types of data.

1) Primary Data:

The data, which are collected for the first time, directly from the respondents to the base of

knowledge & belief of the research, are called primary data. The normal procedure is to

interview some people individually or in a group to get a sense of how people feel about the

topic. So far as this research is concerned, primary data is the main source of information.

The data collected is through questionnaire & information provided by the respondent.

2) Secondary Data:

When data are collected and compelled from the published nature or any other‘s primary data

is called secondary data. So far my project is concerned secondary data is an important part

of my project that‘s why I had collected the data from websites and newspapers.

PREPARE BY :- GAURAV BHUT 37

4.2 HYPOTHESIS:

Hypothesis is usually considered as the principal instrument in the research. Ordinarily when

one talks about hypothesis, one simply means a mere assumption or some supposition to be

proved or disproved. But for a researcher, hypothesis is a formal question that he intends to

resolve. Thus ―a hypothesis may be defined as a proposition or a set of propositions set forth

as an explanation for the occurrence of some specified group of phenomena either asserted

merely as a provisional conjuncture to guide some investigation or accepted as highly

probable in the light of established facts.‖

Types of Hypothesis:

Null Hypothesis and Alternate Hypothesis:

Alternate hypothesis is usually the one which one wishes to prove and the null hypothesis is

the one which one wishes to disprove. Thus a null hypothesis represents the hypothesis we

are trying to reject and alternate hypothesis is all other possibilities.

Hypothesis of the Study:

H0: ― Investor‘s behaviour is favorable in investing in IPO.‖

H1: ―Investor‘s behaviour is unfavorable in investing in IPO.‖

PREPARE BY :- GAURAV BHUT 38

4.3 LIMITATIONS OF THE STUDY:

My Study and analysis has following limitations.

Due to time Constraint, I could not analyze more on it.

My own inexperience might have affected the study & analysis

My analysis is based on past performances, and past performance is not

Guarantee of future results.

The work is based on secondary data. The secondary data can be inaccurate as it is

published format

PREPARE BY :- GAURAV BHUT 39

4.4 FUTURE SCOPE OF THE STUDY:

The Comparative analysis of primary (IPO) and secondary market.

The comparison between IPO‘s & future and options.

The analysis of pros & cons of long term investment in securities market.

The effect of FII‘s on Indian secondary market.

The Comprehensive study on the measures of corporate governance for razing funds

from primary market.

PREPARE BY :- GAURAV BHUT 40

PREPARE BY :- GAURAV BHUT 41

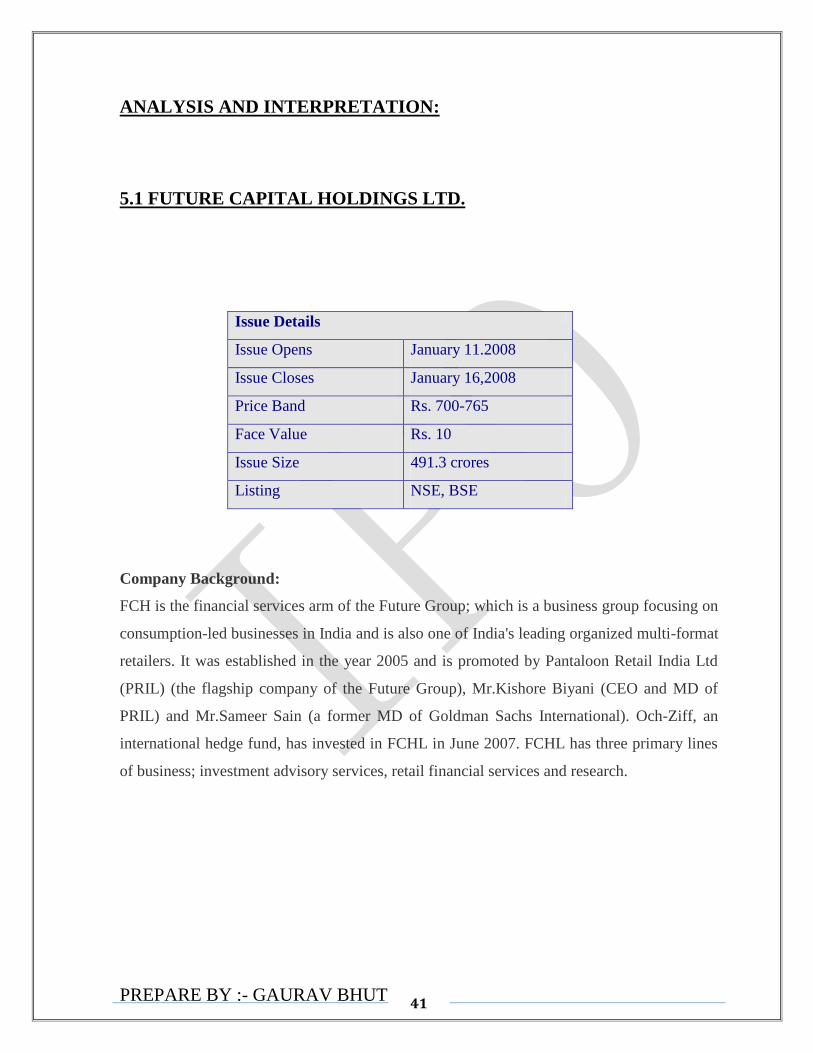

ANALYSIS AND INTERPRETATION:

5.1 FUTURE CAPITAL HOLDINGS LTD.

Issue Details

Issue Opens January 11.2008

Issue Closes January 16,2008

Price Band Rs. 700-765

Face Value Rs. 10

Issue Size 491.3 crores

Listing NSE, BSE

Company Background:

FCH is the financial services arm of the Future Group; which is a business group focusing on

consumption-led businesses in India and is also one of India's leading organized multi-format

retailers. It was established in the year 2005 and is promoted by Pantaloon Retail India Ltd

(PRIL) (the flagship company of the Future Group), Mr.Kishore Biyani (CEO and MD of

PRIL) and Mr.Sameer Sain (a former MD of Goldman Sachs International). Och-Ziff, an

international hedge fund, has invested in FCHL in June 2007. FCHL has three primary lines

of business; investment advisory services, retail financial services and research.

PREPARE BY :- GAURAV BHUT 42

Investment Advisory Services:

It provides private equity and real estate investment advisory services to onshore and

offshore clients. These investment advisory services include investment analysis, research

and recommendations

Retail Financial Services:

Its retail financial services ‗Future Money‘, as a retailer offers financial products and services

in India. It holds rights to provide financial products and services through the retail outlets

which are owned, controlled or managed by PRIL and its subsidiaries. Its primary credit

products currently include consumption loans, which are loans to finance the purchase of

durables, furniture and other consumer goods, and personal loans.

Research:

Future Capital Research conducts and publishes economic research on India with the

objective of enhancing value creation across other businesses.

Purpose of the Issue:

To expand its retail financial services business, in particular, the growth of loan

portfolio.

To meet the long term working capital requirements of the company.

To meet issue related expenses and general corporate purpose.

PREPARE BY :- GAURAV BHUT 43

Fundamental Analysis:

Strong background of Indian retail sector:

One of the pioneering groups to participate in the early stage of India‘s retail story, Future

group has over a decade experience and has developed understanding of the retail and

consumption-led sectors. FCHL launched Future Money in June 2007, which offers financial

products and services to individuals. Currently, it has a presence in 26 cities through 95

outlets across India. Its two main retail financial services products are consumption loans and

personal loans. It also intends to distribute life and non-life insurance products in near future.

Strong research division covering macro factors:

Company‘s research business, Future Capital Research (FCR), conducts and publishes

research on macro-economic trends in India. It has also developed proprietary indices to

highlight trends in consumer behavior. Its reports are also utilized by its advisory division. In

their recent publication ‗XX Factor: The Impact of Working Women on India‘s Growth,

Incomes and Consumption‘, it analyzed the recent rise in women‘s participation in the work

force and the impact of this phenomenon on growth and consumption trends. Other

publication included ‗Is Urban Growth Good for Rural India?‖ studying the urban demand

could be an important engine, which would help to drive a shift from farm to non-farm

employment in rural India. Its in-house research business would help FCHL to invest in the

right segment and right locations.

Dual role of advisory and managing real estate fund:

Currently, FCHL is the investment manager of the Rs3.5bn Kshitij Fund and also advisor to

the investment managers of Rs13.7bn Horizon Fund and Rs7.8bn Indus Fund. It has also

recently entered into a joint venture to create expertise in warehousing logistics. Their real

estate investment activities are in two separate areas of retail/ mixed use and hotels.

PREPARE BY :- GAURAV BHUT 44

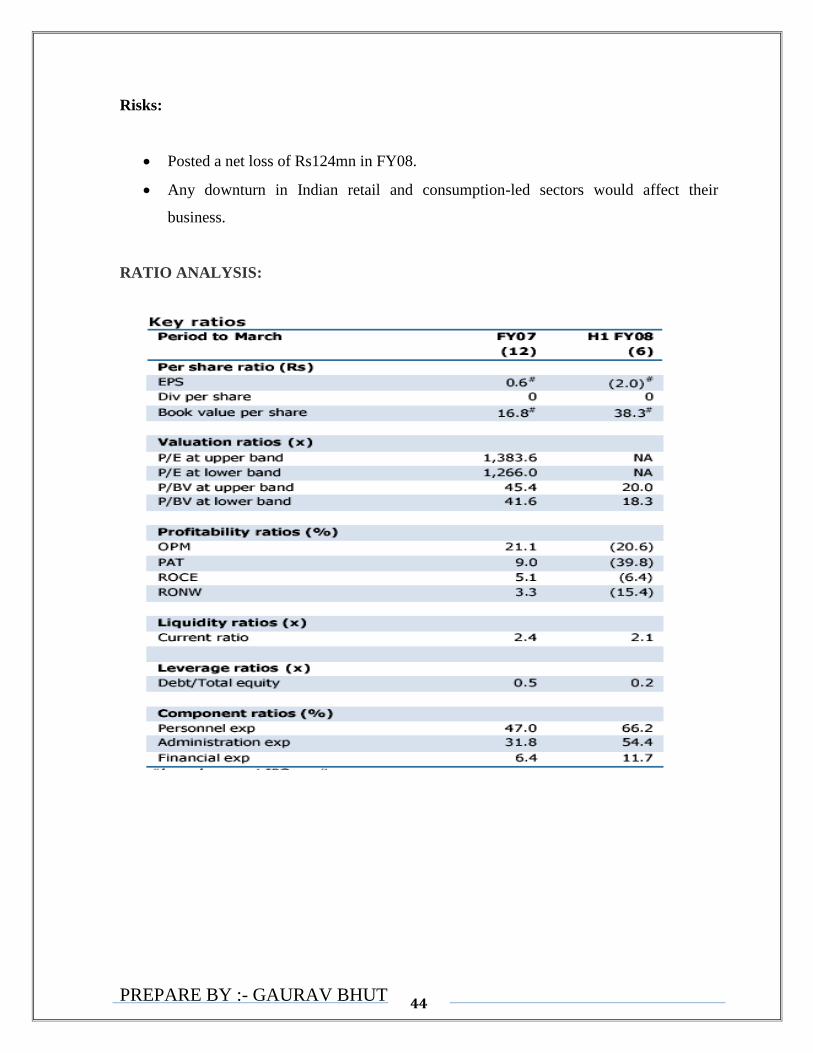

Risks:

Posted a net loss of Rs124mn in FY08.

Any downturn in Indian retail and consumption-led sectors would affect their

business.

RATIO ANALYSIS:

PREPARE BY :- GAURAV BHUT 45

The ideal current ratio is 2:1 and the current ratio of both the years is almost near to

the ideal ratio which indicates that the funds are utilized efficiently.

An ideal debt equity ratio is 2:1.but the debt equity ratio of both the years is low

which implies the use of more equity than debt, which means a larger safety margin

for creditors since owners equity is considered as a margin of safety by creditors and

vice-versa.

Return on Capital Employed shows a negative in the current year which is not a

satisfactory one.

Operating Profit Margin also decreases in the current year.

Valuation of IPO:

FCH is demanding for huge premium on its shares, when compared with companies

such as Reliance Capital, India bulls Financial Services, and IL&FS Investment

Managers, based on price to earnings (P/E) multiple.

The company offers shares at P/E multiple of 137.79 at the floor price and 150.59 at

the cap price (based on annualized earnings per share for first half of FY08, on pre

issue capital of the company).

On the other hand, shares of its peers, Reliance Capital, India bulls Financial

Services, and IL&FS Investment Managers were trading at P/E multiple of 64.72,

27.02 and 41.41(based on annualized earnings per share for first half of FY08 and

share price as on Jan. 10, 2007) while the industry average is 42.8.

In addition, the limited financial history, together with losses of Rs 124 million in its

books for first half of FY08 is cause of concern.

The business undoubtedly offers huge room for scalability; earnings visibility is

extremely low at this juncture.

At Rs 765, the higher end of the price band, the offer values the entire business at a

price-book value (P/BV) of about 6.6 times and Entrenched peers in banking/financial

services with similar opportunities for growth — India bulls Financial, ICICI Bank

and IDFC — are available at comparable valuations.

PREPARE BY :- GAURAV BHUT 46

5.2KIRI DYES AND CHEMICALS LTD

Issue Details

Issue Opens March 25.2008

Issue Closes April 02,2008

Price Band Rs. 125-150

Face Value Rs. 10

Issue Size 3,750,000 shares

Listing NSE, BSE

QIBs 1,875,000 shares

Non Institutional 5,62,500 shares

Retail 1,312,500 shares

Company Background:

Incorporated in 1998, Kiri Dyes and Chemicals Limited is engaged in the business of

manufacturing of reactive dyes which are called synthetic organic dyes used for cotton

fabrics like garments, dress materials, bed-sheets, carpets etc. The dyes are of basically

colours like black, blue, and red, orange, yellow and numerous variants of these basic colours

identified by color index number internationally. The product range of company caters to

textiles, leather, and paint and printing-ink industries with total production capacity of 10800

MTPA.

With plans for further backward integration, the IPO is to fund capital expenditure to set up a

plant to manufacture sulphuric acid, oleum and chloro sulphonic acid, with a combined

capacity of 1, 80,000 tonnes, and a dyes and intermediates unit. A 2.9-MW power plant that

can run from the steam generated by the sulphuric acid plant is also on the anvil. The

electricity generated will be sufficient not only to run the sulphuric acid plant but also the

intermediate plants of VS and H-Acid.

PREPARE BY :- GAURAV BHUT 47

The capacity to produce dyestuff will be increased 3,000 tonnes to 15,000 tonnes by the

fiscal ending March 2010 (FY 2010). The capacity to manufacture dyes intermediates VS

will become 4,200 tonnes in FY 2009 and then further increase to 4,800 tonnes in FY 2010.

The capacity to produce H-acid will increase to 4,200 tonnes in FY 2010.

The Industry produces a wide spectrum of products, which include Pharmaceuticals, Dyes,

Man-made Fibers, Plastics, Pesticides, Fertilizers, Cosmetics and Toiletries, Paint, Auxiliary

Chemicals and wide range of organic and Inorganic compounds for applications ranging

from automobiles, textile industry, engineering industry, construction chemicals and food

additives to veterinary and health care products.

The company is engaged in the business of manufacturing and marketing of:

1. Reactive Dyes – Synthetic Organic Dyes (S. O. Dyes)

2. Dyes Intermediate: Vinyl Sulphone

3. Dyes Intermediate: H-Acid

Purpose of the Issue:

1.To fund the capital expenditure for setting up of a plant to manufacture Sulphuric Acid,

Oleum and Chloro Sulphonic Acid with a combined capacity of 500 M.T. per day adjacent to

its existing unit at Village Dudhwada, Taluka Padra, District Vadodara;

2. To fund the capital expenditure for Dyes and Intermediates Unit located at GIDC, Vatva,

Ahmedabad;

3. To fund the additional working capital margin;

4. To meet Issue expenses;

5. To meet expenses of the Issue in order to achieve the benefits of listing on the Stock

Exchanges.

PREPARE BY :- GAURAV BHUT 48

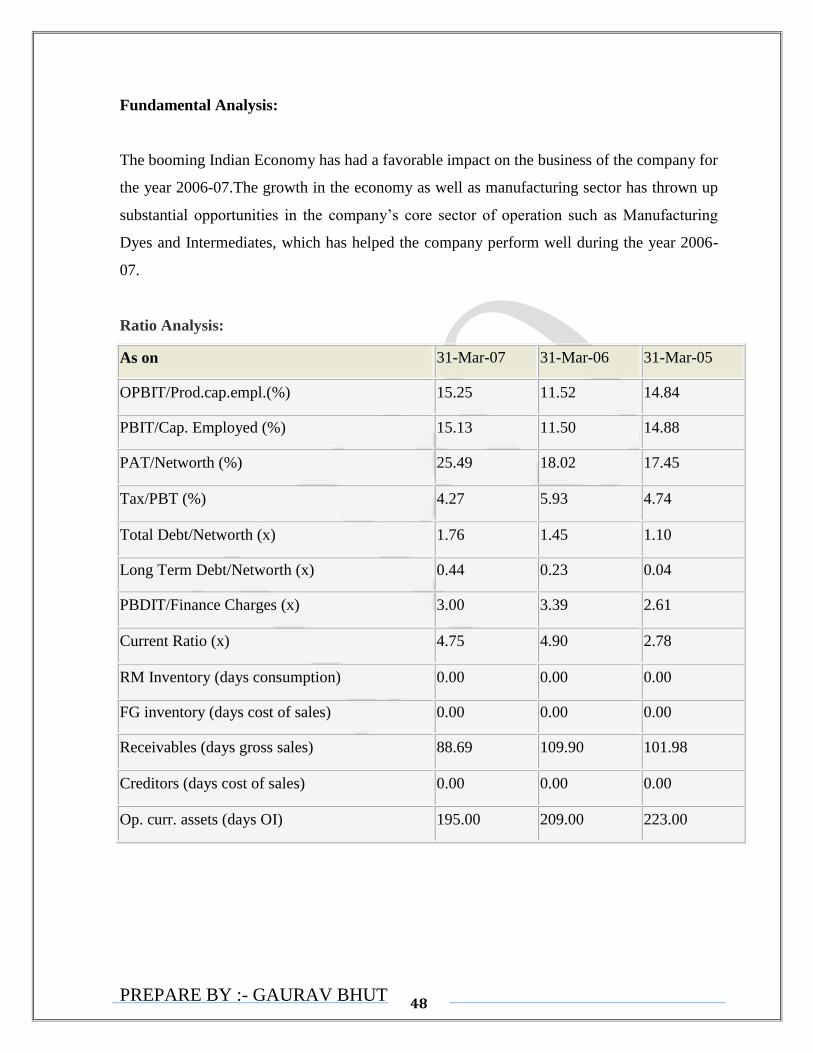

Fundamental Analysis:

The booming Indian Economy has had a favorable impact on the business of the company for

the year 2006-07.The growth in the economy as well as manufacturing sector has thrown up

substantial opportunities in the company‘s core sector of operation such as Manufacturing

Dyes and Intermediates, which has helped the company perform well during the year 2006-

07.

Ratio Analysis:

As on 31-Mar-07 31-Mar-06 31-Mar-05

OPBIT/Prod.cap.empl.(%) 15.25 11.52 14.84

PBIT/Cap. Employed (%) 15.13 11.50 14.88

PAT/Networth (%) 25.49 18.02 17.45

Tax/PBT (%) 4.27 5.93 4.74

Total Debt/Networth (x) 1.76 1.45 1.10

Long Term Debt/Networth (x) 0.44 0.23 0.04

PBDIT/Finance Charges (x) 3.00 3.39 2.61

Current Ratio (x) 4.75 4.90 2.78

RM Inventory (days consumption) 0.00 0.00 0.00

FG inventory (days cost of sales) 0.00 0.00 0.00

Receivables (days gross sales) 88.69 109.90 101.98

Creditors (days cost of sales) 0.00 0.00 0.00

Op. curr. assets (days OI) 195.00 209.00 223.00

PREPARE BY :- GAURAV BHUT 49

The ideal current ratio is 2:1.but the current ration of both the years exceeds the ideal

ratio which indicates that funds are not used efficiently and lying idle.

An ideal debt equity ratio is 2:1.but the debt equity ratio of both the years is low

which implies the use of more equity than debt, which means a larger safety margin

for creditors since owners equity is considered as a margin of safety by creditors and

vice-versa.

Inventory is one area where management has achieved constant success. It has tried

to reduce operating cycle of the division for which it was imperative to reduce the

inventory storage periods consisting of the three components --- raw material, work in

progress, and finished goods. The inventory turnover ratio has increased from

previous year from 9.517 times to 13.766 times. A very high inventory turnover

indicates that overtrading and it may leads to shortage of the working capital.

The ideal quick ratio is 1:1. But the quick ratio of both the years i.e. 3.296 times and

2.878 times exceeds the ideal ratio. Higher quick ratio means excessive amount of

liquid assets have been invested.

Fixed Assets Turnover ratio has decreased from 4.9399 times to 3.1603 times so it is

not a good sign, it indicates that fixed assets remained idle and therefore, the

management should investigate and determine the reasons for the decline.

Return on investment of kiri dyes first decreases in year 2006-07 but then slightly

increase in year 2007-08.The reason for such a low return is that more than half of the

total capital employed used in calculating return on capital hardly yield any return.

PREPARE BY :- GAURAV BHUT 50

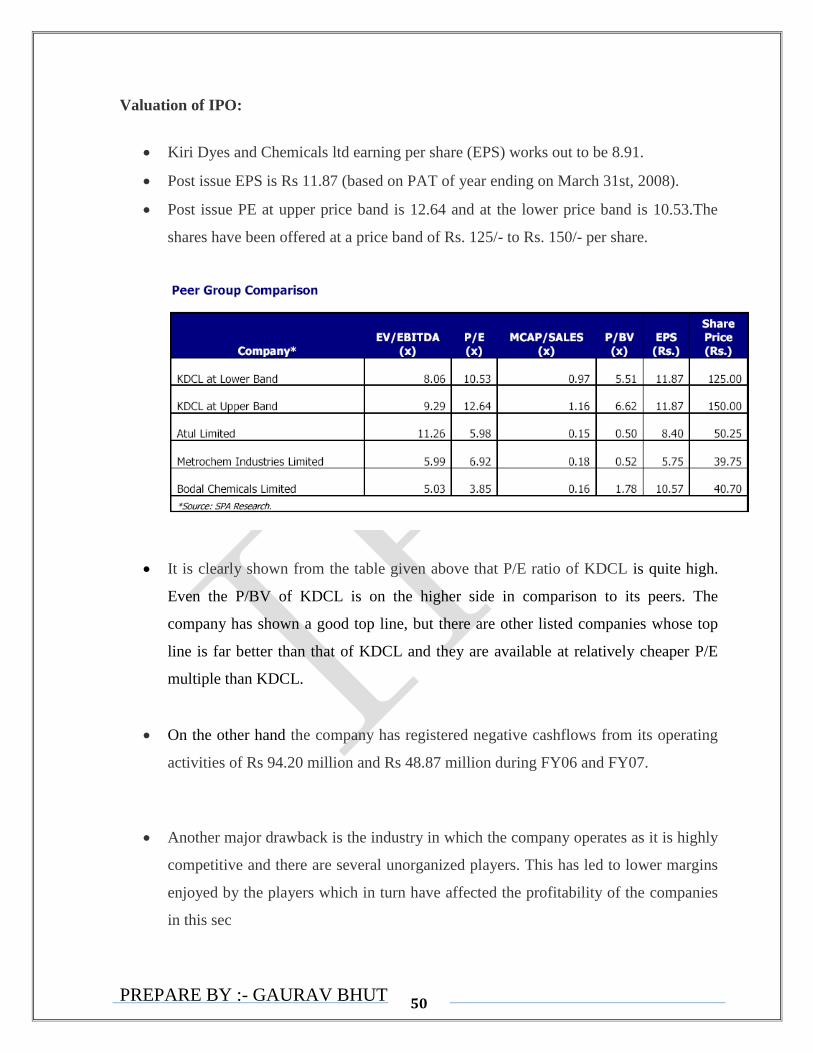

Valuation of IPO:

Kiri Dyes and Chemicals ltd earning per share (EPS) works out to be 8.91.

Post issue EPS is Rs 11.87 (based on PAT of year ending on March 31st, 2008).

Post issue PE at upper price band is 12.64 and at the lower price band is 10.53.The

shares have been offered at a price band of Rs. 125/- to Rs. 150/- per share.

It is clearly shown from the table given above that P/E ratio of KDCL is quite high.

Even the P/BV of KDCL is on the higher side in comparison to its peers. The

company has shown a good top line, but there are other listed companies whose top

line is far better than that of KDCL and they are available at relatively cheaper P/E

multiple than KDCL.

On the other hand the company has registered negative cashflows from its operating

activities of Rs 94.20 million and Rs 48.87 million during FY06 and FY07.

Another major drawback is the industry in which the company operates as it is highly

competitive and there are several unorganized players. This has led to lower margins

enjoyed by the players which in turn have affected the profitability of the companies

in this sec

PREPARE BY :- GAURAV BHUT 51

5.3 RELIANCE POWER:

Issue Details

Issue Opens January 15.2008

Issue Closes January 18,2008

Price Band Rs. 405-450

Face Value Rs. 10

Listing NSE, BSE

Company profile:

Reliance Power Limited (Reliance Power), part of RADAG has been set up to develop,

construct and operate power projects domestically and internationally. It aims to develop 13

power projects with an aggregated generation capacity of 28,200 MW.

Reliance Power will have a diversified project portfolio in terms of geography, fuel mix and

technology.

Nine of the proposed thirteen projects are coal-fired or gas-based and two of those have fuel

security; the rest are yet to be finalized. In our view, for such huge capacity, fuel linkage is of

paramount importance.

Long term PPAs for 8,560MW have been signed, constituting just 32% of the aggregated

generating capacity. Of these, Sasan project (based on domestically procured coal) and

Krishnapatnam project (based on imported coal) have been signed at a tariff of Rs1.19kw/h

and 2.33kw/h per unit respectively, the differential attributable to the high cost of imported

coal. A large number of PPAs are yet to be signed, reflecting some ambiguity on

profitability.

PREPARE BY :- GAURAV BHUT 52

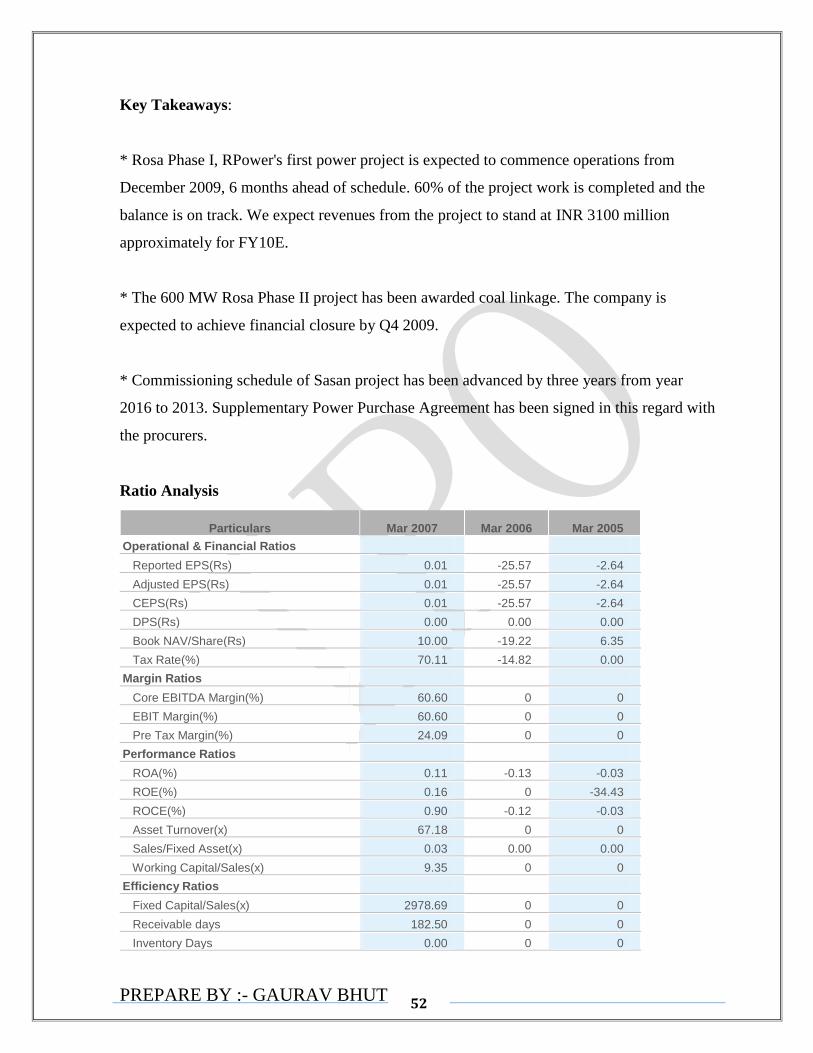

Key Takeaways:

* Rosa Phase I, RPower's first power project is expected to commence operations from

December 2009, 6 months ahead of schedule. 60% of the project work is completed and the

balance is on track. We expect revenues from the project to stand at INR 3100 million

approximately for FY10E.

* The 600 MW Rosa Phase II project has been awarded coal linkage. The company is

expected to achieve financial closure by Q4 2009.

* Commissioning schedule of Sasan project has been advanced by three years from year

2016 to 2013. Supplementary Power Purchase Agreement has been signed in this regard with

the procurers.

Ratio Analysis

Particulars Mar 2007 Mar 2006 Mar 2005

Operational & Financial Ratios

Reported EPS(Rs) 0.01 -25.57 -2.64

Adjusted EPS(Rs) 0.01 -25.57 -2.64

CEPS(Rs) 0.01 -25.57 -2.64

DPS(Rs) 0.00 0.00 0.00

Book NAV/Share(Rs) 10.00 -19.22 6.35

Tax Rate(%) 70.11 -14.82 0.00

Margin Ratios

Core EBITDA Margin(%) 60.60 0 0

EBIT Margin(%) 60.60 0 0

Pre Tax Margin(%) 24.09 0 0

Performance Ratios

ROA(%) 0.11 -0.13 -0.03

ROE(%) 0.16 0 -34.43

ROCE(%) 0.90 -0.12 -0.03

Asset Turnover(x) 67.18 0 0

Sales/Fixed Asset(x) 0.03 0.00 0.00

Working Capital/Sales(x) 9.35 0 0

Efficiency Ratios

Fixed Capital/Sales(x) 2978.69 0 0

Receivable days 182.50 0 0

Inventory Days 0.00 0 0

PREPARE BY :- GAURAV BHUT 53

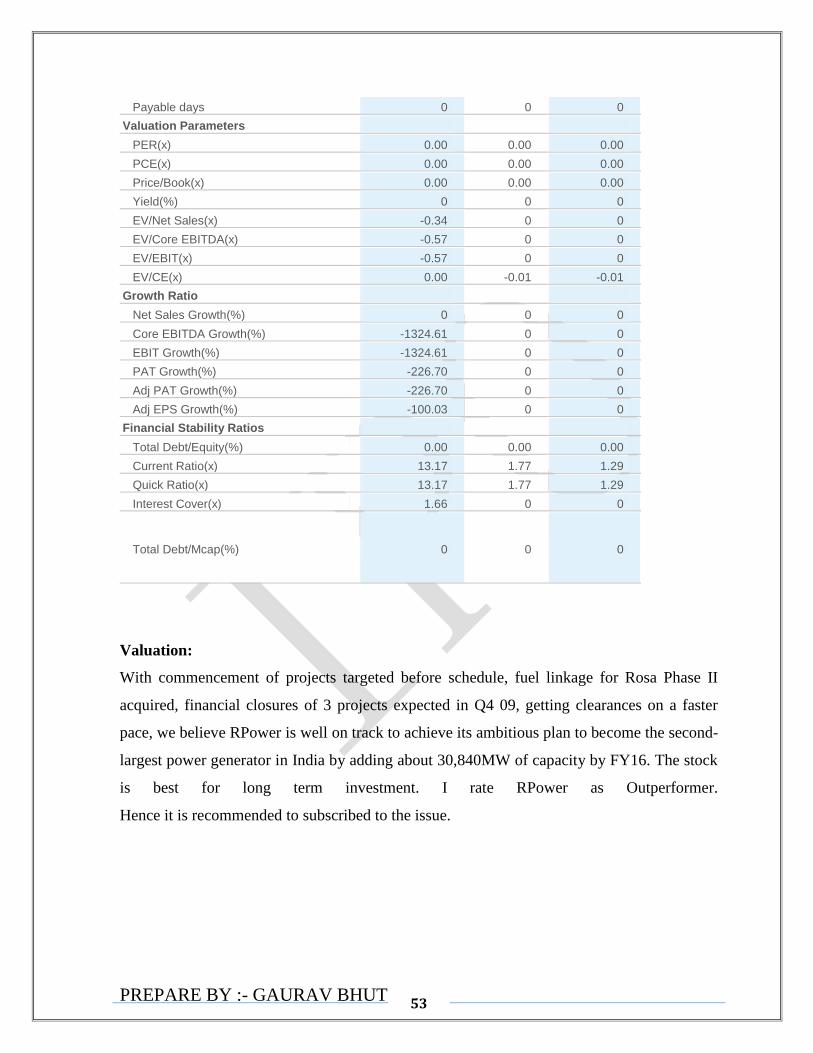

Payable days 0 0 0

Valuation Parameters

PER(x) 0.00 0.00 0.00

PCE(x) 0.00 0.00 0.00

Price/Book(x) 0.00 0.00 0.00

Yield(%) 0 0 0

EV/Net Sales(x) -0.34 0 0

EV/Core EBITDA(x) -0.57 0 0

EV/EBIT(x) -0.57 0 0

EV/CE(x) 0.00 -0.01 -0.01

Growth Ratio

Net Sales Growth(%) 0 0 0

Core EBITDA Growth(%) -1324.61 0 0

EBIT Growth(%) -1324.61 0 0

PAT Growth(%) -226.70 0 0

Adj PAT Growth(%) -226.70 0 0

Adj EPS Growth(%) -100.03 0 0

Financial Stability Ratios

Total Debt/Equity(%) 0.00 0.00 0.00

Current Ratio(x) 13.17 1.77 1.29

Quick Ratio(x) 13.17 1.77 1.29

Interest Cover(x) 1.66 0 0

Total Debt/Mcap(%) 0 0 0

Valuation:

With commencement of projects targeted before schedule, fuel linkage for Rosa Phase II

acquired, financial closures of 3 projects expected in Q4 09, getting clearances on a faster

pace, we believe RPower is well on track to achieve its ambitious plan to become the second-

largest power generator in India by adding about 30,840MW of capacity by FY16. The stock

is best for long term investment. I rate RPower as Outperformer.

Hence it is recommended to subscribed to the issue.

PREPARE BY :- GAURAV BHUT 54

5.4TITAGARH WAGONS LTD

Company Background:

Incorporated in 1997, Titagarh Wagons Limited is one of the leading private sector wagon

manufacturers in India. It is in the business of manufacturing railway wagons, Bailey bridges,

Heavy Earth Moving and Mining equipment, steel and SG iron castings of moderate to

complex configuration etc.

They also manufacture other products for the Indian defence establishment, such as special

purpose wagons, shelters and other engineering equipments. They had approximately 16.9%

market share in the wagon manufacturing segment in Fiscal 2006, which has further

increased to approximately 22.1% in Fiscal 2007.

Titagarh Wagons Limited is the only private sector company registered with the Ministry of

Defence, Government of India to manufacture Bailey bridges and other related accessories in

India. Titagarh Wagons Limited aspires to be a leader as a manufacturer of heavy

engineering equipment and a world-class service provider for the infrastructure sector. They

operate two manufacturing facilities located at Titagarh and Uttarpara, in West Bengal.

Titagarh Wagons Limited operates two manufacturing facilities located at Titagarh and

Uttarpara, in West Bengal. The Uttarpara unit functions as its second manufacturing plant for

wagons, in addition to manufacturing heavy earth moving and mining equipment. As an

―Industry Partner‖ to the Defence Research and Development Organisation, Ministry of

Defence (―DRDO‖), the Company also manufactures other products for the Indian Defence

establishment, such as special purpose wagons, shelters and other engineering equipments.

The Company is structured along three broad business lines: a) wagon manufacturing

division, b) special projects division (includes defence, bailey bridges and other fabricated

equipment) and c) heavy earth moving and mining equipment division

PREPARE BY :- GAURAV BHUT 55

Purpose of the Issue:

The objects of the Issue are to achieve the benefits of listing on the Stock Exchanges & to

raise capital to:

1. Set up an EMU manufacturing facility at our Uttarpara unit;

2. Modernize and expand our existing facilities at our Titagarh and Uttarpara units;

3. set up an axle machining and wheel set assembly facility at our Uttarpara unit;

4. Construct a corporate office and a design cum research and development office;

5. Strategic acquisition or investments;

6. Brand building exercise;

7. General corporate purposes.

Fundamental Analysis:

India railway budget 2008-09 planned to manufacture 20,000 wagons, which

would be the highest level of wagon productions so far.

Movement of cargo via rail account for approximately 30% of the total cargo

transported in volume terms and 11% in value terms.

The freight loading expected for FY 2008 has been pegged at 785 million

tonnes, and by the terminal year of the 11th Five Year Plan, the Railways

are targeting a freight loading of 1,100 million tonnes

PREPARE BY :- GAURAV BHUT 56

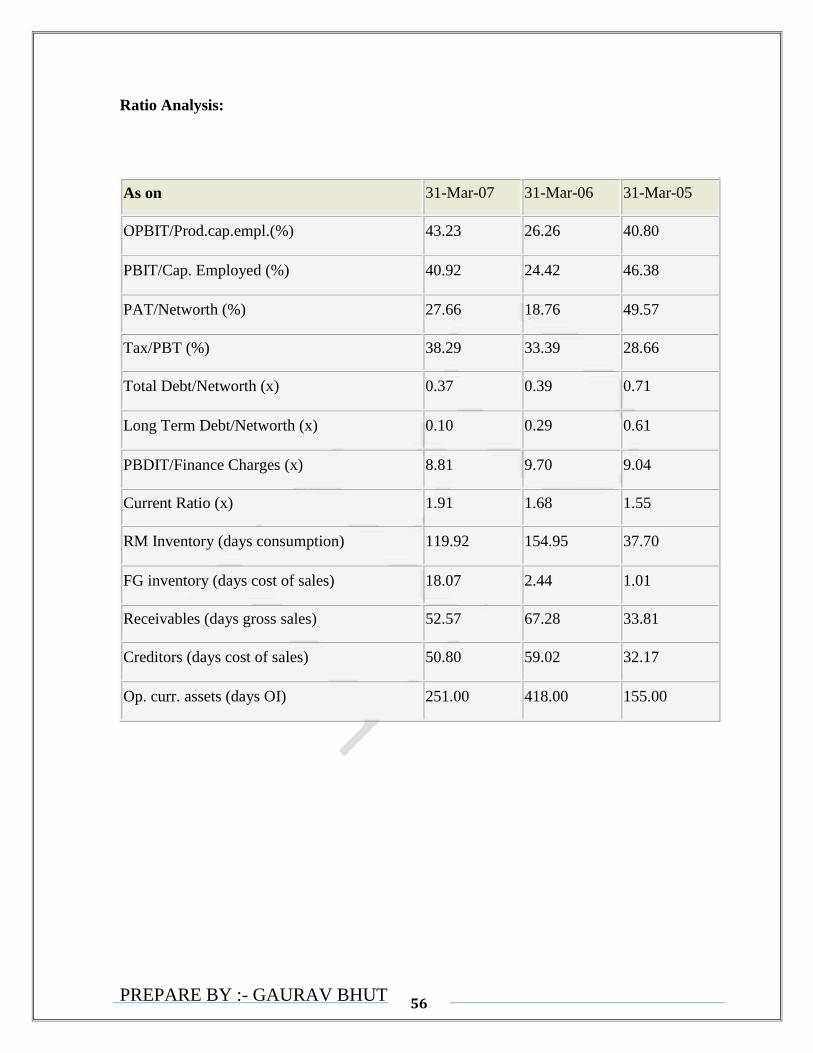

Ratio Analysis:

As on 31-Mar-07 31-Mar-06 31-Mar-05

OPBIT/Prod.cap.empl.(%) 43.23 26.26 40.80

PBIT/Cap. Employed (%) 40.92 24.42 46.38

PAT/Networth (%) 27.66 18.76 49.57

Tax/PBT (%) 38.29 33.39 28.66

Total Debt/Networth (x) 0.37 0.39 0.71

Long Term Debt/Networth (x) 0.10 0.29 0.61

PBDIT/Finance Charges (x) 8.81 9.70 9.04

Current Ratio (x) 1.91 1.68 1.55

RM Inventory (days consumption) 119.92 154.95 37.70

FG inventory (days cost of sales) 18.07 2.44 1.01

Receivables (days gross sales) 52.57 67.28 33.81

Creditors (days cost of sales) 50.80 59.02 32.17

Op. curr. assets (days OI) 251.00 418.00 155.00

PREPARE BY :- GAURAV BHUT 57

The ideal current ratio is 2:1 and the current ratio of the year 06-07 has improved as

compared to previous year which indicates that the funds are utilized efficiently.

An ideal debt equity ratio is 2:1.but the debt equity ratio of both the years is low

which implies the use of more equity than debt, which means a larger safety margin

for creditors since owners equity is considered as a margin of safety by creditors and

vice-versa.

The ideal quick ratio is 1:1. But the quick ratio of both the years slightly increases

than the ideal ratio. Higher quick ratio means excessive amount of liquid assets have

been invested.

Fixed Assets Turnover ratio has increased from 4.34 times to 9.35 times so it is a

good sign for the company.

Gross profit has increased which is plus point for the company. This ratio should be

adequate to cover the administrative and marketing expenses and to provide for fixed

charges, dividends and building up reserves.

Valuation of IPO:

Titagarh Wagon limited earning per share on post-IPO fully diluted equity works

out to be Rs 28.23.

At the offer price band of Rs 540 – Rs 610, the IPO is available at 19.13 at the

lower price band and 21.61 at the upper price band to its FY08 annualized post-

issue EPS.

The comparable listed peer for the company is Texmaco Ltd., which is now ruling

at Rs.1, 300. Texmaco is likely to have a topline of Rs.700 crore, with PAT of

Rs.55 crores, translating into an expected EPS of Rs.55 for FY 08, on an equity of

Rs.10.44 crores. Book value per share of Texmaco is likely to be Rs.200 as at 31-

03-08. This means share is presently ruling at a PE of 24 for Texmaco.

While comparing Titagarh with Texmaco, its book value post issue, would be

close to Rs.200, if shares are issued at Rs.610 per share. The same would be at

Rs.192, if shares are issued at Rs.540. Considering an expected EPS of Rs.31 for

PREPARE BY :- GAURAV BHUT 58

FY 08, share at the upper band is issued at a PE multiple of close to 20. Even post

issue stake of promoters at 49% is close to 53% of Texmaco. FII stake of 38% in

pre-issue instills confidence.

Share at lower band of Rs.540 is quite attractive and at the upper band of Rs.610

also, leaves room for gain, as FY 09 performance of the company would be quite

good.

PREPARE BY :- GAURAV BHUT 59

PREPARE BY :- GAURAV BHUT 60

6. FINDINGS AND SUGGESTIONS:

FINDINGS:

The pro-rata system of allotment favors investors who bid for relatively large

numbers of shares. Perhaps, the process should be changed such that those applying

up to 1,000 shares are allotted in full and beyond this number on pro-rata basis.

Book-building is preferred because the allotment of shares is generally done at a price

determined by the lead merchant banker and issuer within the price band. Since QIBs

are the dominant players and bid at somewhat higher prices within the band, the

issuer and merchant banker fix the price at the higher end such that retail investors

have to accept it. Thus, investors chipping in 35 per cent of the capital have little role

in price discovery. As a matter of fact, the IPO demand curve is skewed by differing

demands at different prices by various bidders. This indicates the need to use multiple

pricing for allotment.

There is considerable amount of difficulties for an investor today in the IPO market

starting from sourcing the application to filling it and submitting it along with

cheques. When we have one of the world's best trading and settlement infrastructure

available why can't we use that infrastructure rather than insisting on a parallel market

for IPOs? This will be a good time to provide a direction to the IPO market as well to

attract new investors into the market.

The grading process will not take into account price valuation, a key parameter in any

stock investment decision. Said Prime Database MD Prithvi Haldea, The market does

PREPARE BY :- GAURAV BHUT 61

not work on fundamentals. A good company is a bad investment at a high price. The

small investors, for whom the grading exercise is basically meant, would despite

disclaimers expect a high graded IPO to quote above the offer price. The whole

purpose of grading an IPO would be defeated if it cannot help an investor decide what

stock to choose and at what price.

SUGGESTIONS:

Keys to a Successful IPO: At the end to make its IPO effective, some important

considerations that should be kept are:

Obviously, having a successful company to offer to the public marketplace is essential.

Beyond that, it is important to recognize this in not a place for do-it-yourselfers. While the

road show represents the formal coming out of the firm, its success will partially depend on

the groups selected for the audience, and this, in turn, depends upon the lead investment

banker/underwriter in the IPO. Choosing the right underwriter is probably second in

importance to choosing the right time to go public. The essential elements to look for in the

ideal lead underwriter are as follows:

1. The underwriter is focused on your industry: The IPO marketplace is a crowded

marketplace and the significant sums you are spending for professional advice to go public

need to be targeted to a firm with real expertise in your industry. Partial evidence of

appropriate expertise would be having an analyst devoted to your industry.

2. The market relies heavily on analyst projections and recommendations: Specifically, the

underwriting firm's analyst in your industry must:

Have the capacity to cover your company with sufficient attention.

Understand your company, customers, and competition.

Indicate sincere commitment to covering your company.

PREPARE BY :- GAURAV BHUT 62

3. Due to the importance of a successful road show, the underwriter must have the ability and

contacts to identify the right investor groups for your presentation and get them committed to

attend. References from previous IPO successes are essential.

4. There must be sufficient evidence of being able to build a quality "book" of potential

orders for your stock.

5. There should be a history regarding the ability to identify the right offer price and size.

6. Finally, but rarely understood by many companies, there must be significant aftermarket

support in terms of maintaining and supporting trading in the stock, providing subsequent

research reports on the company, and continuing institutional exposure to the company.

PREPARE BY :- GAURAV BHUT 63

PREPARE BY :- GAURAV BHUT 64

7. CONCLUSION

Through this research, I came to know that the IPO market is booming market in Indian

history. People now become aware about the IPO than other options of the investment like

fixed deposits, mutual funds, shares, gold and silver and other options of investment.

Hypothesis of the Study: Hence Proved

H0: ― Investor‘s behaviour is favorable in investing in IPO.‖

In this research report, I came to know that how the mechanism of IPO works in the industry.

IPO is a broader concept than any other investment options of the investment.

The Project report starts with defining the various public issues with the need for the

company to take out an IPO. It goes on further to explain the advantages of an IPO. It

analyses in detail the Indian IPO Scenario. It explains the evolution of the IPO in India and

explains how the scene has changed dramatically after liberalization esp. after the

introduction of book building process.

PREPARE BY :- GAURAV BHUT 65

PREPARE BY :- GAURAV BHUT 66

8. BIBLIOGRAPHY

BOOKS:

1. Khan M. Y .and Jain. P.K (2005). Financial management. Pearson publications

WEBSITES:

www.moneycontrol.com

www.capitalline.com

www.nseindia.com

www.sebi.gov.in

www.capitalmarket.com

www.wikipedia.com

www.intimesepctrum.com

www.thehindubusinessline.com

www.financialexpress.com

www.myiris.com

www.icraratings.com

NEWSPAPERS:

1. Economic Times