interim results 2020 - harworth group plc

TRANSCRIPT

INTERIM RESULTS 20206TH OCTOBER 2020

www.harworthgroup.com

Harworth invests to transform land and property into sustainable places where people want to live and work

3

1. WELL POSITIONED TO DELIVER LONG-TERM VALUE 4 OWEN MICHAELSON, CHIEF EXECUTIVE

2. SOLID PERFORMANCE IN H1 5-14 OWEN MICHAELSON, CHIEF EXECUTIVE

3. AN UNDERLYING ROBUST BUSINESS 15-20 KITTY PATMORE, CHIEF FINANCIAL OFFICER

4. WELL POSITIONED FOR THE FUTURE 21-26 KITTY PATMORE, CHIEF FINANCIAL OFFICER

APPENDIX 1 27-33 ESG AND THE HARWORTH WAY

APPENDIX 2 34-37 DETAILED PORTFOLIO INFORMATION

DISCLAIMER 38

INTERIM RESULTS 2020

4

HUGE LATENT VALUE IN UNDERLYING LAND PORTFOLIO

c.30,000potential homes in

land portfolio

CREATING SUSTAINABLE NEW PLACES WHERE PEOPLE WANT TO LIVE AND WORK IS MORE RELEVANT THAN EVER FOLLOWING THE COVID-19 PANDEMIC

WELL POSITIONED TO DELIVER LONG-TERM VALUE

LONG-TERM UNDERSUPPLY CONTINUES TO DRIVE RESIDENTIAL PROPERTY MARKET

E-TAILING AND LACK OF SUPPLY IS DRIVING INDUSTRIAL PROPERTY MARKET

6.8%VACANCY ACROSS UK

ONLY

300,000

!

0 10 20 30 40 50 60 70 80 90 100

UNLOCKING CORE LOGISTICS SITES

of industrial space

Industrial Investment portfolio drives growth and provides defensive income stream to cover overheads

Occupancy rates

£236.2M

Annual delivery well below

UK homes target

STRONG INVESTMENT PORTFOLIO

25,4 0 0 , 0 0 0 sq ft

PURP

OSE

PORT

FOLI

OM

ARK

ETS

Net Loan to Value

13.0%

STRONG TECHNICAL TRACK RECORD

SIGNIFICANT FINANCIAL HEADROOM

LOW LEVEL OF GEARING£63.3m

as at 30 September 2020 as at 30 September 2020

TEC

HN

ICA

LS

5

ACQUISITIONS & LAND ASSEMBLY

Land acquisitions and PPAs with potential for 1,438 residential plots

Income acquisitions generating £1.2m annual rent at 10% NIY

Biggest ever land pipeline

MASTERPLANNING

Live applications for 2,391 residential plots and 2.4m sq. ft of commercial space

PLANNING APPROVAL

Consent granted for schemes delivering 300 residential plots and 1.1m sq. ft of commercial space

SOLID PERFORMANCE IN H1 2020: KEY HIGHLIGHTSSOLID PERFORMANCE IN H1

LAND PREPARATION & INFRASTRUCTURE DEVELOPMENT

Infrastructure works progressing on 7 major development sites

All housebuilders back on site

TWO KEY SALES ABOVE BOOK VALUE:

First sale at Coalville to Redrow – first of 2,016 homes to be delivered on our largest Midlands site

Major commercial sale at Skelton Grange to Wheelabrator

Sell down of 899 acres from non-core portfolio

New nuclear fusion testing facility for UKAEA at AMP now practically complete with new 20-year lease

PLOT SALE & BUILD OUT PLACEMAKING

FOR

SALE

ASSET MANAGEMENT

c.95% of rent from investment portfolio collected for March & June

Business Space vacancy of 3.7% - its lowest ever level, with WAULT now at 13.2 years

£2.4MPROFIT

excluding value gains

FINANCIAL HIGHLIGHTS

Revolving credit facility increased to £130m

Effect of CV19 on property market results in value losses of £(23)m

Total Return (4.5)%

Profit Excluding Value Gains grew to £2.4m - up 16.3% year-on-year

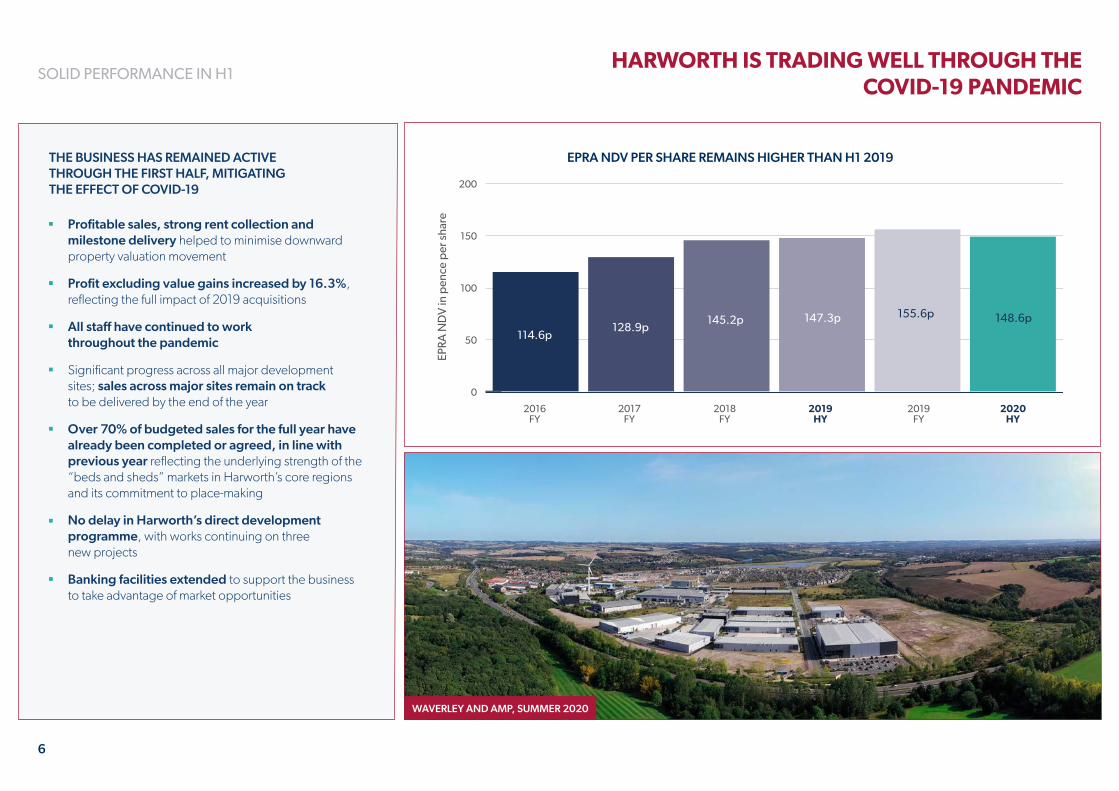

EPRA NDV per share 148.6p

Dividends reinstated with interim dividend increased by 10%

6

THE BUSINESS HAS REMAINED ACTIVE THROUGH THE FIRST HALF, MITIGATING THE EFFECT OF COVID-19

Profitable sales, strong rent collection and milestone delivery helped to minimise downward property valuation movement

Profit excluding value gains increased by 16.3%, reflecting the full impact of 2019 acquisitions

All staff have continued to work throughout the pandemic

Significant progress across all major development sites; sales across major sites remain on track to be delivered by the end of the year

Over 70% of budgeted sales for the full year have already been completed or agreed, in line with previous year reflecting the underlying strength of the “beds and sheds” markets in Harworth’s core regions and its commitment to place-making

No delay in Harworth’s direct development programme, with works continuing on three new projects

Banking facilities extended to support the business to take advantage of market opportunities

SOLID PERFORMANCE IN H1HARWORTH IS TRADING WELL THROUGH THE

COVID-19 PANDEMIC

EPRA NDV PER SHARE REMAINS HIGHER THAN H1 2019

0

50

100

150

200

2016FY

2017FY

2018FY

2019HY

2019FY

2020HY

114.6p128.9p

145.2p 147.3p 155.6p 148.6p

EPRA

ND

V in

pen

ce p

er s

hare

WAVERLEY AND AMP, SUMMER 2020

7

GOVERNMENT AMBITION TO ‘BUILD BUILD BUILD’ FURTHER SUPPORTS GROWTH

DEVOLUTION Further funding to regional authorities has been announced in 2020 as part of the

Government’s levelling-up agenda. This includes funding allocations for infrastructure, low-carbon energy and other themes that could support the ongoing build-out of our sites

ADDITIONAL INFRASTRUCTURE SPENDING Unprecedented infrastructure spending was announced by the Government in the first half

of 2020 which directly supports our business

In March, the Chancellor announced £640bn of gross capital investment into the UK’s roads, railways, schools, hospitals and power networks by the end of the Parliamentary term, a cash injection that will be “triple the average over the last 40 years in real terms”

This was followed in May by £2bn of additional national funding announced to boost more sustainable greener travel, alongside a £1.7bn Transport Infrastructure Investment Fund to upgrade the existing roads and bridges network

PLANNING WHITE PAPER The Government’s planning reform proposals for England are aimed at delivering a

“significantly simpler, faster and more predictable system” through reforms to the ‘local plan’ system and introducing digital technology to the planning process

A number of suggested reforms are welcomed, including local authorities only having 30 months to produce a new-style stripped back local plan, down from a current average of seven years

The White Paper is currently the subject of consultation and we believe it is likely to be at least eighteen months away from becoming enshrined in law

SOLID PERFORMANCE IN H1

GASCOIGNE INTERCHANGE SITE

PLANNING CONSULTATION EVENT AT IRONBRIDGE

8

ACQUISITIONS TOTALLING £13.8M (INCLUDING COSTS) IN H1 2020

One strategic land acquisition made in Bolton that could deliver 140 new residential plots; application to be submitted to Bolton Council in the second half of the year

One Planning Promotion Agreement (PPA) entered into in the West Midlands with the potential to deliver a further 1,298 residential plots in the medium-term

Two income-producing acquisitions during the period, directly supporting strategy to grow the breadth and depth of income portfolio

The acquisition of Thorns Road Industrial Estate for £10.1m (page 14); and

The purchase of a Short-Term Operating Reserve (STOR) facility in Gloucester for £1.2 million, let to UK Capacity Reserve Ltd (Sembcorp Energy UK Ltd) on a lease expiring in 2040, reflecting a net initial yield of 8.25%

ACQUISITIONS: GROWING THE STRATEGIC LAND PIPELINE AND INVESTMENT PORTFOLIO

SOLID PERFORMANCE IN H1

STOPES ROAD, BOLTON

THORNS RD, DUDLEY

9

Planning success achieved at Woodville, Derbyshire in the first half of 2020, adding 300 plots to our consented residential landbank

This was followed up by the receipt of planning consent for Phases 2 and 3 of our Gateway 36 development in Barnsley in July, adding 1.1m sq. ft of consented space to our commercial development landbank

Live applications for 2,391 residential plots and 2.4m sq. ft of commercial space in the planning system as at 30 June 2020, including the outline application for the former Ironbridge power station

This is tempered however by some headwinds remaining on a small number of applications, including:

Wingates (Bolton): 1.1m sq. ft application locally approved by Bolton Council ‘called-in’ for Examination in Public by the Secretary of State later this year, alongside four unconnected major applications in the North West.

Gascoigne Interchange (Selby): Initial application for expansion of existing brownfield area turned down. Application now being re-planned around its extensive on-site rail sidings to connect occupiers to the Strategic Rail Freight network

PLANNING PROGRESS MADE BUT HEADWINDS REMAIN

GATEWAY 36 PHASE 2 AND 3

FORMER IRONBRIDGE POWER STATION

SOLID PERFORMANCE IN H1

10

PLANNING CASE STUDY: GATEWAY 36 PHASES 2 AND 3

BARNSLEY COUNCIL GRANTED CONSENT FOR UP TO 1.1M SQ. FT OF NEW EMPLOYMENT SPACE ACROSS 95 ACRES OF LAND IN JULY 2020, WHICH COULD DELIVER UP TO 2,410 JOBS FOR YORKSHIRE ADJACENT TO JUNCTION 36 OF THE M1

Consented masterplan proposes units of between 25,000 sq. ft and 250,000 sq. ft for light and general industrial use, alongside storage and distribution

The newly consented development will build on the success of Phase 1 of Gateway 36. Harworth directly developed 145,248 sq. ft of employment space between 2015 and 2018, comprising four industrial/warehouse units and one drive-thru retail unit. Five units were leased on a long-term basis to Barnsley Council, Motor Depot and Fieldrose prior to their profitable sale to clients of Mayfair Capital in August 2018

All three phases of Gateway 36, alongside nearby employment and residential land, have been unlocked as part of a £17.1m funding package from the Sheffield City Region Investment Fund, funding key road improvements to increase traffic capacity

Our focus is now on using our in-house remediation and infrastructure skills to engineer land prior to its sale to commercial occupiers or to retaining it for direct development to support our Investment Portfolio

SOLID PERFORMANCE IN H1

INDICATIVE CGI OF GATEWAY 36 PHASES 2 AND 3

11

SALES TOTALLING £30.8M ACHIEVED DURING THE PERIOD, ALL AT OR ABOVE BOOK VALUE

Disposal in March of 19.5 acres of industrial land at Skelton Grange in Leeds to Wheelabrator Technologies for a total consideration of £13.0m, in excess of its 31 December 2019 book value. Wheelabrator and their partners at SSE are now constructing a 42MW energy from waste facility

Sale in June of 16.0 acres of residential land at Hugglescote Grange, Coalville to Redrow, in line with its 31 December 2019 book value – our first sale to the housebuilder

9 sites totalling c900 non-core acres sold in H1, allowing further management time to focus on key value-adding projects and reducing drag on the wider portfolio

As at the beginning of October over 70% of budgeted sales for the full year have already been completed or agreed reflecting the underlying strength of the “beds and sheds” markets in Harworth’s core regions and its commitment to place-making

STRONG COMMERCIAL AND RESIDENTIAL SALES PROGRESSSOLID PERFORMANCE IN H1

PROPOSED EFW FACILITY AT SKELTON GRANGE

FIRST PHASE OF RESIDENTIAL DEVELOPMENT AT HUGGLESCOTE GRANGE

12

SALES CASE STUDY: HUGGLESCOTE GRANGE

FIRST MAJOR RESIDENTIAL LAND SALE SINCE ESTABLISHMENT OF MIDLANDS OFFICE

Hugglescote Grange is a 328-acre site, less than two miles from Junction 22 of the M1, with an outline consent in place for 2,016 new homes, alongside supporting uses including a primary school, local community centre and new public realm

16.0 acres of engineered land sold in line with its 31 December 2019 book value. Redrow intends to deliver 204 new family homes on this first phase

The deal followed Harworth completing initial infrastructure works in its role as master developer in order to facilitate the sale, including delivering a new access roundabout from the existing road network alongside internal roads and utilities

Next phase land sale planned for 2021 following a competitive bidding process

SOLID PERFORMANCE IN H1

FIRST TWO PHASES OF HUGGLESCOTE GRANGE DEVELOPMENT

13

INVESTMENT PORTFOLIO REMAINS RESILIENT & CONTINUES TO GROW

INCREASING THE BREADTH AND DEPTH OF OUR INVESTMENT PORTFOLIO REMAINS A LONG-TERM PRIORITY, WITH OVERHEADS AND INTEREST COSTS CONTINUING TO BE COVERED BY OUR RECURRING INCOME BASE FROM PREDOMINANTLY INDUSTRIAL TENANTS

Our portfolio has weathered the pandemic well, with c.95% of rent due at the March and June quarter dates collected and vacancy now at a record low of 3.7%

This has been supplemented by three principal management actions to further grow the portfolio:

The completion of 22 new or renewed lettings during the first half of the year;

The ongoing build out of three commercial units which all have long-term pre-lets in place, with all due to complete by the end of the year; and

Two acquisitions made for a total of £11.3m plus acquisition costs, at a blended Net Initial Yield of 10.0%

Strong industrial and logistics market in our regions resulted in revaluation gains of £6.2m across the Investment Portfolio in H1 2020

SOLID PERFORMANCE IN H1

NUFARM FACILITY, BRADFORD

UK ATOMIC ENERGY AUTHORITY’S NEW FACILITY AT AMP

14

INVESTMENT CASE STUDY: THORNS ROAD

THORNS ROAD INDUSTRIAL ESTATE ACQUIRED IN JUNE FROM XANDOR AUTOMOTIVE FOR £10.1M PLUS ACQUISITION COSTS

Close to both Dudley and Stourbridge town centres and less than ten miles from Birmingham City Centre, the 20.5-acre site comprises three fully let industrial units totalling c. 360,000 sq. ft and generates a passing rent of £1.1m per annum, reflecting a Net Initial Yield of 10.2% and a Reversionary Yield of 12.8%

On completion of the deal, Xandor Automotive entered into a new 15-year lease for c. 240,000 sq. ft of factory space it currently occupies, whilst also agreeing a short-term lease for an additional c. 15,000 sq. ft unit. Xandor Automotive is a key manufacturer in the West Midlands, supplying plastic injection moulded components and fluid conveyance products for customers in the automotive and commercial vehicle industry including JLR, Ford, Denso and Cummins Engineering

The remaining c. 110,000 sq. ft unit is let to Sunrise Medical Ltd, a leading designer, manufacturer and distributor of mobility products, on a lease expiring in July 2022

The site also includes 4.2 acres of open storage land, providing further asset management and residential development potential

SOLID PERFORMANCE IN H1

THORNS RD INDUSTRIAL ESTATE, DUDLEY

15

NET ASSET VALUE MOVEMENT

FOR THE SIX MONTHS ENDING 30 JUNE 2020, EPRA NDV PER SHARE FELL BY 4.5% TO 148.6p, AND NAV PER SHARE BY 1.3% TO 142.2p

As at:31/12/19

Value gains/(losses) Profit excludingvalue gains

Interest &finance costs

Tax Other (pension, swap, dilution etc)

As at:30/06/20

155.0p

150.0p

145.0p

140.0p

135.0p

130.0p

142.2p

(0.5p) (0.5p) (0.2p)

0.8p

4.6p

144.1p

(5.9p)

(1.4p)

0.7p

160.0p

NAV per share EPRA NDV per share

6.4p

11.5p

155.6p

148.6p

AN UNDERLYING ROBUST BUSINESS

16

VALUE GAINS ACROSS THE PORTFOLIO

SIX MONTHS TO 30 JUNE (£’m)HY 2020 2019

Profit on disposal

Revaluation gains/(losses)

Total Value Gains/(Losses)

Portfolio Value Total Value Gains

MAJOR DEVELOPMENTS Management actions continued to move sites forwards; however, national residential market sentiment on short-term certainty on timing and prudent profit assumptions reduced valuations as at 30 June. Despite this, Gross Development Value for our major developments remained almost entirely unaffected with no general increase in costs and continued evidence of plot sales

(0.7) (29.6) (30.3) 220.5 9.9

STRATEGIC LAND Profit on sale and valuation uplift at Skelton Grange combined with values tempered by planning delays

4.9 (4.5) 0.4 103.7 0.1

BUSINESS SPACE Good letting progress achieved across our portfolio including lease regear at Moxon Way (Brighouse) and increase at Nufarm reflecting the value of a high quality covenant on a long term lease

- 4.7 4.7 188.4 -

NATURAL RESOURCES Valuation uplifts as a result of asset management initiatives

0.3 2.2 2.5 36.9 0.2

AGRICULTURAL LAND Small reductions across a handful of sites

0.2 (0.7) (0.5) 10.9 0.9

TOTAL 4.7 (27.9) (23.2) 560.4 11.1

Notes: The table above is presented on an EPRA NDV basis

ROBUST PERFORMANCE FROM DIVERSIFIED PORTFOLIO DESPITE PANDEMIC UNCERTAINTY

AN UNDERLYING ROBUST BUSINESS

Regional industrial and logistics market increased in strength over 2020, owing to growth in e-tailing

All markets remained active over Q3 2020 including continued demand from end users for logistics land and property and housebuilders for serviced residential land across all Harworth’s regions

17

PORTFOLIO REMAINS DIVERSIFIED

Strategic land Major developments Business space Natural resources Agriculture & other

Notes: 1) Total value of all property – Investment (£297.2m), Development (£188.2m), Joint ventures (£34.4m), Available for sale (£14.4m), Owner Occupied Assets (£0.8m), plus mark to market value of development properties, overages and assets held for sale (£25.4m)

AGRICULTURE & OTHER £10.9m

STRATEGIC LAND

RESIDENTIAL £39.2m

MAJOR DEVELOPMENTS

COMMERCIAL £46.6m

NATURAL RESOURCES £36.9m

BUSINESS SPACE £188.4m

PORTFOLIO CONCENTRATION PORTFOLIO SECTOR SPLIT

STRATEGIC LAND COMMERCIAL £64.4m

MAJOR DEVELOPMENTS

RESIDENTIAL £174.0m

£560.4m

45%

20%

MELTON COMMERCIAL PARK

HUGGLESCOTE GRANGE (COALVILLE)

WAVERLEY (NEW COMMUNITY)

NUFARM

SIMPSON PARK

THORESBY VALE

WAVERLEY AMPGATEWAY 45

PHEASANT HILL PARK

35%

FOUR OAKS BUSINESS PARK

58% CAPITAL GROWTH

INCOME GENERATION 42%

AN UNDERLYING ROBUST BUSINESS

£560.4m

NEXT 10 SITES

REMAINING SITES

18

UNDERLYING PROFITABLE BUSINESS

Notes: (1) Profits/(losses) from disposals of property categorised as investment, overages, development and assets held for sale (2) Revaluation from investment and development properties, joint ventures, overages and assets held for sale (3) The above table is stated on an EPRA NDV basis

Six months to 30 June (£’000) Capital Growth Income Generation Central Overheads 2020 Total 2019 Total

Profit excluding value gains (850) 7,592 (4,369) 2,373 2,041

Profit from disposals1 4,168 544 4,712 4,735

Revaluation2 (34,119) 6,195 (27,924) 6,364

Pension charge (38) (38) (29)

Operating (loss)/profit plus JVs (30,801) 14,331 (4,407) (20,877) 13,111

Interest and finance costs 207 (1,806) (1,599) (1,241)

(Loss)/profit before tax (30,594) 14,331 (6,213) (22,476) 11,870

Tax 1,197 (2,346)

(Loss)/profit after tax (21,279) 9,524

Earnings per share - Statutory (1.6)p 4.7p

Dividend per share 0.3p 0.3p

Profit excluding value gainsPEVG increased reflecting additional income from 2019 acquisitions

Profit from disposalsProfits reflect sales above book value particularly across strategic land sites

Dividend per shareInterim dividend increased by 10% to 0.334p per share. The Board remains committed to considering increasing the final 2020 dividend to reflect the cancellation of the 2019 full-year dividend

Revaluation gainsHalf year third party valuation shows the robust nature of the diversified portfolio and management actions taken to minimise market movements but not at a level to offset the short-term reduction in confidence in the national residential market at that point in time

AN UNDERLYING ROBUST BUSINESS

19

OUR INCOME PORTFOLIO IN DETAIL

SEGMENTMARKET

VALUEANNUALISED

RENTGROSS YIELD

BUSINESS SPACE £190.9m £13.3m 7.0%

NATURAL RESOURCES £38.0m £3.9m 10.2%

TOTAL £228.9m £17.2m 7.5%

BUSINESS SPACE SECTOR ANALYSIS

Chemicals

Transport/Logistics

Manufacturing/Engineering

Automotive/Automotive Repairs

Building supplies/Construction

Plastic Packaging

Housebuilding

NHS Supplies

Other

Notes: The valuation represents the fair value, which is the external market value adjusted for rent free periods and capital contributions

INCOME STRATEGY Investment properties are actively managed by our in-house Income

Generation team to drive recurring income and value gains

Aim remains to grow our recurring income base over time to cover overheads and our banking interest as the business continues to increase in size

Team works collaboratively and flexibly with tenants to ensure their successful operation whilst maximising income generated and collected

Income is supplemented with high-yielding acquisitions with further asset management potential, alongside the sale of lower yielding properties once business plans have been completed

Direct commercial development also undertaken provided internal management tests are met

INCOME PORTFOLIO DETAIL

AN UNDERLYING ROBUST BUSINESS

17%

15%

13%

9%9%

8%

7%

7%

16%

NATURAL RESOURCES SECTOR ANALYSIS

Income generating activities on site

Energy

Surface Water Management

Other49%

37%

12%

2%

PREDOMINANTLY INDUSTRIAL TENANT PORTFOLIO

BPS Vacancy (based on sq. ft): 3.7% BPS WAULT: 13.2 years

20

CONTINUING TO MANAGE CASH FLOWS TO FUND GROWTH

Openingnet debt

31/12/19

Developmentspend

Salesproceeds

Profit excludingvalue gains

Interest,finance costs,

pension charges

Cash and working capital

used in operations

Investment inJoint Ventures

Closingnet debt

30/06/20

£140,000k

£0

£120,000k

£80,000k

£60,000k

£40,000k

£20,000k

Acquisitionsand PPA spend

69,249k

14,126k

2,035

300k1,599k

2,373k

42,085k

13,403k

70,911k

£100,000k

13,968k

Cash 11,833kCash 7,523k

RCF Headroom60,000k

RCF Headroom24,000k

DISCIPLINED APPROACH WITH INVESTMENT IN INFRASTRUCTURE AND ACQUISITIONS LARGELY FUNDED THROUGH DISPOSALS• Net LTV of 12.4% at lower end of target range as at 30 June 2020• Prudent gearing provides headroom and flexibility

POSITION AS AT 30 JUNE 2020 £’000

DRAWN BANK BORROWINGS – RCF 70,000

INFRASTRUCTURE LOANS 7,177

GROSS INTEREST-BEARING DEBT 77,177

CASH 7,523

CAPITALISED FEES 405

NET DEBT 69,249

AN UNDERLYING ROBUST BUSINESS

21

DELIVERY TARGETS FOR REMAINDER OF 2020WELL POSITIONED FOR THE FUTURE

STRATEGY REMAINS CONSISTENT: DRIVING THE CAPITAL GROWTH OF OUR PORTFOLIO AND INCREASING OUR RECURRING INCOME BASE, MAINTAINING FOCUS ON OUR CORE ASSET CLASSES AND REGIONS

ACQUISITIONS Active in all three core regions

for strategic land sites, including in an exclusivity agreement for a major former industrial site, alongside income-producing assets in a variety of industrial classes

£67.5m of available headroom to utilise on either strategic land or income-producing property

Deals will continue to comprise a mixture of freehold acquisitions, PPAs and options

SALES Well advanced with 2020

sales, with over 70% of budgeted sales for the full year already completed or agreed, in line with previous year. All budgeted sales continue to progress despite COVID-19

Surplus land sales to continue. 3,380 acres are either in legals for disposal or remain available for sale as part of further portfolio refinement

PLANNING Outline planning applications

for 2,391 plots and 2.4m sq. ft across 8 sites currently awaiting determination

Planning success achieved in July for Phases 2 and 3 of our Gateway 36 development in Barnsley for 1.1m sq. ft of commercial development space

Examination in Public for Wingates development in Bolton, covering 1.1m sq. ft of industrial development, to be heard in November following Secretary of State call-in

INCOME Tenants being sought for final

remaining directly developed unit at AMP (26,000 sq. ft) and final Joint Venture unit at Multiply Logistics North (149,000 sq. ft)

Direct development of c. 50,800 sq. ft industrial unit on Logistics North’s final vacant plot to begin in November

Asset management initiatives continue across our other income producing sites, including continuing to support tenants to trade successfully through the pandemic

22

LONG-TERM LAND PIPELINE

Notes: (1) Planning pipeline numbers include sites where we have signed PPAs, options, our share of joint venture agreements and taken overages (2) The above charts show indicative planning submission dates correct as at 30 June 2020

COMMERCIAL PIPELINE: SQUARE FEET

30.0m

20.0m

15.0m

5.0m

0.0m

10.0m

25.0m

CURRENTLY CONSENTED

8.23m sq. ft

AWAITING DETERMINATION

2.39m sq. ft

H2 2022 ONWARDS

14.75m sq. ft

FREEHOLD/JV

19.61m sq. ft

PPAS/OPTIONS/OVERAGES

5.76m sq. ft

TOTAL 25.36m sq. ft30,000

25,000

15,000

5,000

0

10,000

20,000

35,000

RESIDENTIAL PIPELINE: PLOT NUMBERS

CURRENTLY CONSENTED

10,074

AWAITING DETERMINATION

2,391

H2 2022 ONWARDS

17,667

FREEHOLD/JV

16,976

PPAS/OPTIONS/OVERAGES

13,156

TOTAL 30,132 plots

LAND PIPELINE NOW AT HIGHEST POINT SINCE RE-LISTING, UNDERPINNING THE GROUP’S FUTURE SALES AND DEVELOPMENT PROGRAMMES

Land portfolio continues to meet our purpose of providing sustainable places to live and work

All future deals will need to continue to meet three key management tests before proceeding:

customer requirements

funding and covenants; and

risks and projected returns

WELL POSITIONED FOR THE FUTURE

23

LATENT VALUE IN UNDERLYING PORTFOLIO FOR SALES & INCOME

Acquisitions &land assembly

Masterplanning

Planningapproval

Landpreparation

Infrastructuredevelopment

Plot sale/Build out

Time

Ind

icat

ive

Val

ue A

dd

Acquisitions Strategic land Major developments Income generation

Placemaking

Assetmanagement 17 major development sites at various stages of land

preparations and infrastructure development

Harworth’s remaining consented portfolio currently stands at 10,000 residential plots and 8.2m sq. ft of commercial space

Identified surplus land to be sold

Tenants sought for final vacant direct and co-developed units

Direct development to be undertaken at Logistics North and pre-lets to be sought on a selective basis

Sale of mature assets where business plans have been completed

Clear lines of communication in place with all tenants to support them to trade through the pandemic successfully

Long-term non-consented pipeline of 20,000 plots and 17.1m sq. ft of commercial space

A mixture of freehold acquisitions and the signing of PPAs and option agreements will continue to be made

Selective income producing purchases to be made to drive further value gains and to increase long-term recurring income to continue to cover overheads

Live applications for 2,391 residential plots and over 2.4m sq. ft of commercial space are in the planning system awaiting determination

MOSS NOOK0/900 plots sold

WARMSWORTH GATE0/375 plots sold

SIMPSON PARK316/996 plots sold

RIVERDALE PARK333/600 plots sold

FLASS LANE407/560 plots sold

THORESBY VALE143/800 plots sold

CADLEY PARK507/570 plots soldIRONBRIDGE

Planning submitted; demolition underway

CHATTERLEY VALLEY0/1.36m sq. ft commercial space built or sold

WAVERLEY1,570/3,890 plots sold

1.5m/2.1m sq. ft commercial space built or sold

LOGISTICS NORTH3.9m/4.0 m sq.ft commercial space built or sold

PRINCE OF WALES488/917 plots sold

PHEASANT HILL PARK522/1,200 plots sold

SAXON VALE194/400 plots sold

KELLINGLEY 0/1.45m sq. ft commercial space built or sold

BARDON HILL 0/0.4m sq. ft sold

FURTHER SITES Planning underway

FOCUS REMAINS ON UNLOCKING LATENT PORTFOLIO VALUE AND SELECTIVE ACQUISITIONS

WELL POSITIONED FOR THE FUTURE

HUGGLESCOTE GRANGE204/2,016 plots sold

24

DELIVERING A SUFFICIENT QUANTITY OF GOOD QUALITY NEW HOUSING REMAINS THE UK GOVERNMENT’S KEY LONG-TERM DOMESTIC PRIORITY

Jun

07

Jun

08

Jun

09

Jun

10

Jun

11

Jun

12

Jun

13

Jun

14

Jun

15

Jun

16

Jun

17

Jun

18

Jun

19

Jun

20

400,000

350,000

300,000

250,000

200,000

150,000

100,000

Dec

07

Dec

08

Dec

09

Dec

10

Dec

11

Dec

12

Dec

13

Dec

14

Dec

15

Dec

16

Dec

17

Dec

18

Dec

19

New

hom

es (a

nnau

l rol

ling

) New Planning Consents

Full Planning Consents (20+units)

Energy Performance Certifcates

Net Additional Dwellings

Government Target

0%

10%

20%

30%

40%

50%

Accessibilityto wifi

Amount of garden/outside

space

Separate spaceto work

from home

Environmentalcredentials

Size of rooms

Number ofrooms

Character/architectural style

Significantly more important Somewhat more important Net Balance

DEMAND FOR LAND IS CONSISTENT Continuing nationwide housing undersupply of >50,000 homes

per annum is driving consistent demand for prepared land from housebuilders of all types

Sixteen separate housebuilders have now purchased land from Harworth reflecting the ongoing popularity of a de-risked product that allows them to ‘plug and play’ construction

THE REGIONS REMAIN AFFORDABLE Each of our regions has an affordability ratio for first time buyers

of less than 8, compared to over 11 in London and the South East

COVID-19 has driven an increase in demand for homes with gardens, space to work from home and environmental credentials as well a sense of local community

GOVERNMENT SUPPORT REMAINS IN PLACE Increasing the quality and supply of new homes remains one of

the UK’s key domestic priorities

Help to Buy remains in place until 2023, whilst the temporary reduction of Stamp Duty rates until March 2021 provides a further short-term incentive for buyers

Proposed reforms to the planning system within the Government’s white paper may also make it easier to secure consents for our developments of scale in the future Source:

Savills Client Survey April 2020

Source: MHCLG, HBF, Glenigan

OUR RESIDENTIAL MARKETS HAVE SOLID FUNDAMENTALS

WELL POSITIONED FOR THE FUTURE

THE UK STILL DELIVERS LESS THAN ITS 300,000 HOMES TARGET

OUR SITES SUIT WHAT PEOPLE WANT FROM A NEW HOME

25

DEMAND AND LOW VACANCY RATES PERSIST IN INDUSTRIAL PROPERTY SECTOR , UNDERPINNING ITS PROJECTED GROWTH

0

5

10

15

20

25

30

35

40

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020YTD

sq �

(mill

ions

)

Q1 Q2

Q3 Q4

H1 average

LEADING PROPERTY SUB-SECTOR Industrial sector has strengthened as a result of COVID-19, driven by further

growth in e-tailing as more consumers become accustomed to buying online

CONSISTENT DEMAND FOR NEW SPACE H1 2020 take-up is the highest ever recorded (66% above the long-term

average), emphasising that demand for well-located industrial space of all sizes remaining very strong in all of our core regions

Yorkshire and East Midlands accounted for 49% of these deals

UK vacancy rate now stands at 6.8% (just 1.2 years’ supply), with all regional markets having a vacancy rate of less than 10%

Vacancy projected to move no more than c5% even in downside scenarios

Speculative development has slowed in 2020 and Grade A supply expected to fall by the year end

Sweet spot remains small to mid-box market of sub-150,000 sq. ft, supporting our direct commercial development projects

SUPPORTED BY STAKEHOLDERS On the whole, local and national support remains for sustainable new

commercial development, driven by the desire for economic regeneration, new jobs and the need for business rate receipts in an era of insecure local government finances

INDUSTRIAL MARKET IS VERY STRONG, DRIVEN BY E-TAILINGWELL POSITIONED FOR THE FUTURE

16%

14%

12%

10%

8%

6%

4%

2%

0%East Midlands West Midlands North West Yorkshire &

The HumberEast of England

Current Baseline Downside Upside

PROJECTED VACANCY RATE TO REMAIN LOW BY 2022

INDUSTRIAL AND LOGISTICS TAKE UP

Source: Savills

26

WE ARE WELL POSITIONED FOR GROWTH

WELL POSITIONED FOR LONG-TERM GROWTH CAPITALISING ON THE OPPORTUNITIES CREATED BY THE RENEWED POLITICAL FOCUS ON THE MIDLANDS AND THE NORTH OF ENGLAND AND THE ACCELERATED STRUCTURAL SECTOR CHANGES AS A RESULT OF COVID-19 PANDEMIC

Biggest ever pipeline of land for both residential and commercial development, with work on our major developments unaffected by COVID

Valuation remains resolute, underpinned by sales continuing to be made at or above book value

Income portfolio continues to grow via robust asset management, new acquisitions and direct development, covering Group overheads and strongly contributing to value gains

Placemaking capabilities embedded within each of our regional teams to add value at all stages of development process

Residential and industrial property markets in our regions remain fundamentally sound, with additional Government financial support and incentives welcomed

The strength of our balance sheet and diversity of portfolio provides a robust underpin for further growth whilst also affording significant flexibility to take advantage of strategic land or income-generating opportunities in the regions

Owen Michaelson to retire at the end of 2020 and new CEO, Lynda Shillaw, joining an experienced executive and management team on 1st November 2020

WELL POSITIONED FOR THE FUTURE

WAVERLEY, ROTHERHAM

LOGISTICS NORTH, BOLTON

APPENDIX 1:

ESG AND THE HARWORTH WAY BASIS OF THE HARWORTH WAY 28

COMMUNITIES 29

PLANET 30

PEOPLE 31

PARTNERS 32

GOVERNANCE 33

28

PLANETWE AIM TO CREATE PLACES IN A SUSTAINABLE WAY, FUTURE PROOFING OUR SITES, AS WELL AS MINIMISING OUR OWN ENVIRONMENTAL IMPACT

PEOPLEWE AIM TO BUILD A BUSINESS WHERE PEOPLE CAN FLOURISH AND PLACEMAKE TO PROVIDE SPACES THAT PROMOTE HEALTH & WELLBEING

COMMUNITIESWE BUILD AND STRENGTHEN OUR COMMUNITIES NOW AND FOR FUTURE GENERATIONS

GOVERNANCEHIGH STANDARDS OF CORPORATE GOVERNANCE ARE ESSENTIAL TO THE EFFECTIVE OPERATION OF THE GROUP

PARTNERSWE DEVELOP STRONG PARTNERSHIPS BASED ON A SHARED SOCIALLY RESPONSIBLE APPROACH WORKING TOWARDS CREATING GREAT NEW PLACES

We launched ‘The Harworth Way’ in March 2020 to reflect how we’re tackling some of society’s key challenges through our work. This forms part of our commitment to delivering shareholder returns in the right way through the effective regeneration of our land and property in the North of England and the Midlands.

Since that time, we have made progress against each of its five themes, with specific detail given in the Appendix. Our long-term ESG Strategy will also be launched in the new year, setting out activities delivered to date and targeted actions, both near and longer-term, that will reflect how we will continue to make strong returns in the right way.

The delivery ‘The Harworth Way’ supports the delivery of the following ten UN sustainable development goals:

APPENDIX 1: THE HARWORTH WAY ESG: THE BASIS OF THE ‘HARWORTH WAY’

29

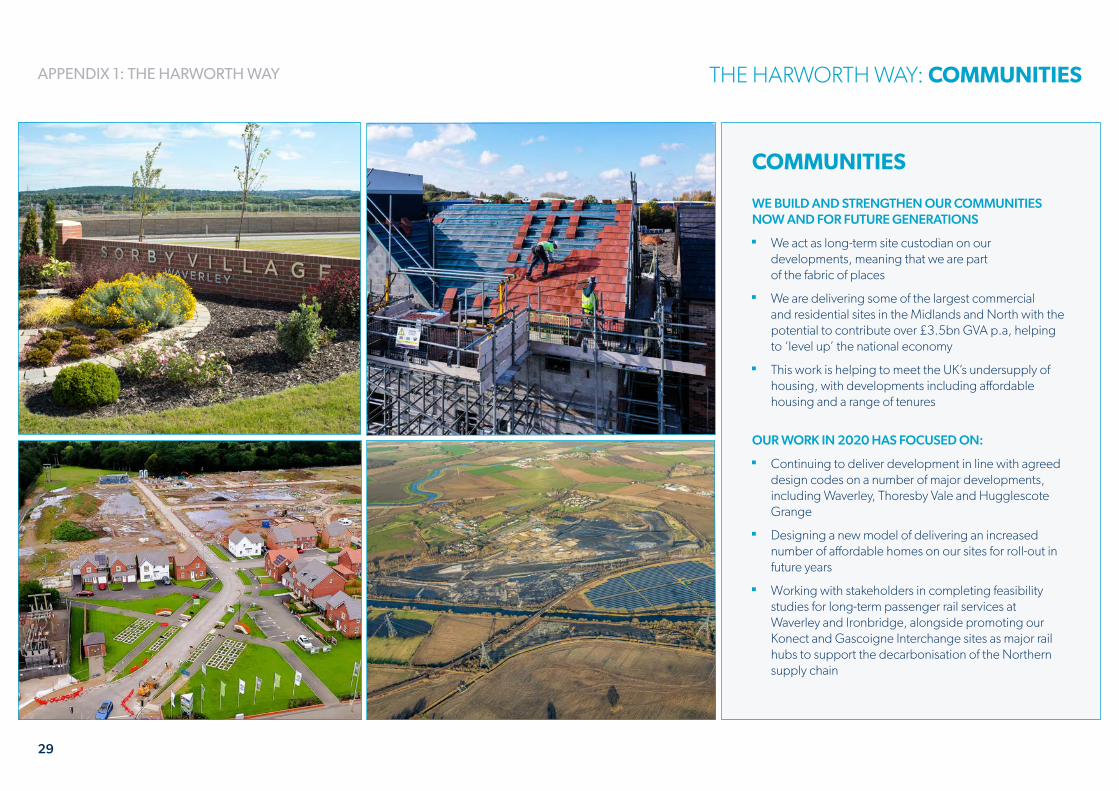

COMMUNITIES

WE BUILD AND STRENGTHEN OUR COMMUNITIES NOW AND FOR FUTURE GENERATIONS

We act as long-term site custodian on our developments, meaning that we are part of the fabric of places

We are delivering some of the largest commercial and residential sites in the Midlands and North with the potential to contribute over £3.5bn GVA p.a, helping to ‘level up’ the national economy

This work is helping to meet the UK’s undersupply of housing, with developments including affordable housing and a range of tenures

OUR WORK IN 2020 HAS FOCUSED ON:

Continuing to deliver development in line with agreed design codes on a number of major developments, including Waverley, Thoresby Vale and Hugglescote Grange

Designing a new model of delivering an increased number of affordable homes on our sites for roll-out in future years

Working with stakeholders in completing feasibility studies for long-term passenger rail services at Waverley and Ironbridge, alongside promoting our Konect and Gascoigne Interchange sites as major rail hubs to support the decarbonisation of the Northern supply chain

THE HARWORTH WAY: COMMUNITIESAPPENDIX 1: THE HARWORTH WAY

30

THE HARWORTH WAY: PLANET

PLANET

WE AIM TO CREATE PLACES IN A SUSTAINABLE WAY, FUTURE PROOFING OUR SITES AS WELL AS MINIMISING OUR OWN ENVIRONMENTAL IMPACT

In our role as master developer, we often regenerate sites with former industrial uses, safely managing any environmental liabilities while we do so

We are landlord for a number of low carbon energy schemes and several leading low-carbon firms are occupiers on our sites such as ITM, Xeros and UKAEA

Surface water attenuation schemes are installed across all of our major developments

OUR WORK IN 2020 HAS FOCUSED ON:

Continuing to deliver engineered land sensitively by reusing materials and assets where possible, including historic roads and power supplies and minimising new waste arisings

Delivering all direct-developed units to BREEAM Very Good standard, including the UK Atomic Energy Authority’s new nuclear fusion research facility at the AMP

Installing Electric Vehicle charging points on major developments including Waverley, Flass Lane and Ironbridge, alongside Harworth’s Advantage House headquarters

APPENDIX 1: THE HARWORTH WAY

31

PEOPLE

WE AIM TO BUILD A BUSINESS WHERE PEOPLE CAN FLOURISH AND PLACEMAKE TO PROVIDE SPACES THAT PROMOTE HEALTH & WELLBEING

We develop the skills of our people and live the “Harworth Values”

Strong Health & Safety culture in place, promoting responsible working across its sites from our staff and contractors in delivering new places

Hundreds of acres of new public open space are delivered each year to support more active lifestyles and mental wellbeing

OUR WORK IN 2020 HAS FOCUSED ON:

Delivering hundreds of acres of new usable public open space across the portfolio, including the completion of Logistics North’s Cutacre Country Park

Safely delivering our major developments, with no Harworth-reported accidents in 2020

Properly supporting our staff through the COVID-19 pandemic, with no staff being furloughed and all 73 staff supported to work remotely effectively

THE HARWORTH WAY: PEOPLEAPPENDIX 1: THE HARWORTH WAY

32

THE HARWORTH WAY: PARTNERS

PARTNERS

WE DEVELOP STRONG PARTNERSHIPS BASED ON A SHARED SOCIALLY RESPONSIBLE APPROACH WORKING TOWARDS CREATING GREAT NEW PLACES

We focus on creating sustainable value through continuing partnerships with customers, local authorities, the Government and our suppliers

Harworth sites are often centres of excellence for industry and stimulate growth. This includes partnerships with 3 leading Universities to promote new skills and innovation relating to advanced manufacturing, wellness and rail

OUR WORK IN 2020 HAS FOCUSED ON:

Continuing to deliver out our Joint Ventures, including Multiply Logistics North in Bolton where only one co-developed unit remains vacant for long-term letting

Establishing a closer working relationship with Homes England to support the delivery of our long-term residential land portfolio, including tenure diversification where possible

Responding to and working with national, regional and local Government on proposed legislative and funding changes, including the Planning White Paper, the proposed Freeports programme and devolved funding opportunities to support development

APPENDIX 1: THE HARWORTH WAY

33

GOVERNANCE

HIGH STANDARDS OF CORPORATE GOVERNANCE ARE ESSENTIAL TO THE EFFECTIVE OPERATION OF THE GROUP

Good governance has been built into the foundations of the Harworth approach from the start. We are now profiling better how governance supports the delivery of our long-term purpose and furtherance of our strategic priorities

We aim to improve continually in these areas and align with industry best practice

OUR WORK IN 2020 HAS FOCUSED ON:

Continuing to evolve the framework of internal controls, processes and reporting, including ESG considerations forming part of all decisions made at Board and Investment Committee level

Delivering its succession plan, including recruitment of next Chief Executive and replacement Non-Executive Directors

Implementing Restricted Share Plan and Share Incentive Plan to encourage stewardship from employees throughout the business

THE HARWORTH WAY: GOVERNANCEAPPENDIX 1: THE HARWORTH WAY

APPENDIX 2:

DETAILED PORTFOLIO INFORMATION PROPERTY VALUATION MOVEMENT 35

VALUATION METHODOLOGY 36

CURRENT FINANCING FACILITIES 37

DISCLAIMER 38

35

PROPERTY VALUATION MOVEMENT

£620.0m

£600.0m

£580.0m

£560.0m

£540.0m

£520.0m

£500.0mValue of Properties

at 31/12/2019Development

spendAcquisitions Disposals Revaluation

gainsValue of Properties

at 30/06/2020

£585.3m

£13.4m

£13.8m£23.9m

£27.9m

£560.4m

Net Investmentin JVs

£0.3m

APPENDIX 2: DETAILED PORTFOLIO INFORMATION

36

VALUATION METHODOLOGY

THE PORTFOLIO IS VALUED TWICE YEARLY. FORMAL YEAR-END VALUATIONS ARE UNDERTAKEN BY BNP AND SAVILLS, WHILST THEY HAVE ALSO UNDERTOOK A DESKTOP VALUATION FOR HALF YEAR TO SUPPORT THE PRODUCTION OF THESE RESULTS

VALUATION IS PROPERTY BY PROPERTY ON THE BASIS OF MARKET VALUE (RICS RED BOOK DEFINITION) GIVEN THE HIGHEST AND BEST USE OF THE PORTFOLIO

BUSINESS SPACEMarket comparison with direct reference to observable market evidence: rental values; yields; and capital values, adjusted for: the quality of the properties; the covenant profile of the tenants; and the volatility of cash flows.

STRATEGIC LAND & DEVELOPMENT SITESDiscounted cash flows, measured by current land values adjusted to reflect the: quality of the development opportunity; potential development costs; and likelihood of planning consent

Residual development appraisals, a form of discounted cash flow which estimates the current site value from future cash flows measured by observable current land and/or completed built development values and estimated developments costs and returns.

VALUATION TECHNIQUES FOR THE BROAD CATEGORIES OF THE PORTFOLIO ARE:

APPENDIX 2: DETAILED PORTFOLIO INFORMATION

37

CURRENT FINANCING FACILITIES

WEIGHTED AVERAGE COST OF DEBT IS 3.27% (USING 30 JUNE 2020 BALANCES AND RATES) WITH A 0.9% NON-UTILISATION FEE ON UNDRAWN RCF AMOUNTS

£45m fixed at 1.235% plus 225 basis point margin until July 2022

LENDER SITE AMOUNT DRAWN (£’K) INTEREST RATE END DATE

HOMES ENGLAND Simpson Park 4,271 2.2% plus EU Reference Rate20 business days from the sale of last

part of site, or December 2022

SHEFFIELD CITY REGION JESSICA

AMP 2,906 2.2% plus EU Reference RateDecember 2020 but with an ability to

extend if development not let

RBS/SANTANDERAll sites.

Floating debenture70,000 ICE Libor rate plus 2.25% February 2023

GROSS INTEREST-BEARING DEBT 77,177

CAPITALISED FEES (405)

TOTAL GROSS BORROWINGS 76,772

APPENDIX 2: DETAILED PORTFOLIO INFORMATION

38

DISCLAIMER

For the purpose of the following disclaimer, reference to this ‘presentation’ shall be deemed to include reference to the presentation slides, the presenters’ speeches, the question and answer session and any other related verbal or written communication.

This presentation, which has been issued by Harworth Group plc ("Harworth"), comprises slides for a presentation in relation to Harworth’s results for the half-year ended 30 June 2020 and is solely for use at such presentation. This presentation is confidential and may not be reproduced, redistributed or passed directly or indirectly to any person or published in whole or in part for any purpose.

This presentation includes forward-looking statements with respect to the business, performance and financial condition of Harworth. These forward-looking statements can be identified by the use of forward-looking terminology, including without limitation the terms "estimates", "plans", "anticipates", "targets", "aims", "continues", "expects", "intends", "may", "will", "would", "could" or "should“ or, in each case, their negative or other various or comparable terminology. These statements are made by Harworth’s directors in good faith based on the information available to them at the date of Harworth’s interim results announcement for the half-year ended 30 June 2020. By their nature, these statements may involve risks, uncertainties or assumptions given future events and circumstances which are beyond Harworth's control, including amongst other things, fluctuations in the property market for the price of land, the timing effect and other uncertainties of future acquisitions, the effect of tax and other legislation or regulations in the United Kingdom, all or any of which can cause results and developments to differ materially from those anticipated. Further details of certain risks and uncertainties were set out in Harworth’s Annual Report and Financial Statements for the year ended 31 December 2019, available to view at www.harworthgroup.com. Nothing in this presentation should be construed as a profit forecast. Except as required by applicable law or regulation, Harworth disclaims any obligation or undertaking to update these statements to reflect events occurring after the date these statements were published.

Actual results may differ materially from those expressed in forward-looking statements. As such, you are cautioned not to put undue reliance on any forward-looking statements. No investment advice is being given in this presentation. No representation, warranty or undertaking is given by, or on behalf of, Harworth or any of its directors, officers, employees and advisers that Harworth will achieve any results set out in such statement or as to the accuracy, completeness or reasonableness of any projections, targets, estimates, forecasts, beliefs, opinions or information contained in or given during this presentation and no liability is accepted or incurred by any of them for or in respect of the same, provided that nothing in this paragraph shall exclude liability for any representations or warranty made fraudulently.

In making this presentation available, Harworth makes no recommendation to buy, sell or otherwise deal in shares in Harworth or in any other securities or investments whatsoever, and you should neither rely nor act upon, directly or indirectly, any of the information contained in this presentation in respect of any such investment activity. Past performance is no guide to future performance. If you are considering engaging in investment activity, you should seek appropriate independent financial advice and make your own assessment.

By accepting these presentation slides, you agree to be bound by the above conditions and limitations.

This presentation does not constitute or form part of any offer or invitation to sell, or any solicitation of any offer to purchase, any shares in Harworth or any other securities, nor shall it or any part of it, nor the fact of its distribution form the basis of, or be relied upon in connection with, any contract or investment decision related thereof.

The financial results contained within this presentation are extracted from Harworth’s interim results announcement for the financial half-year ended 30 June 2020.

SECTION

T: 0114 349 3131 E: [email protected]

HEAD OFFICEAdvantage House Poplar Way Rotherham S60 5TR

BIRMINGHAMWaterloo House 20 Waterloo Street Birmingham B2 5TB

MANCHESTERPhoenix House Cross Street Manchester M2 4JF

LEEDSPinnacle 67 Albion Street Leeds LS1 5AA